Mad Hedge Technology Letter

July 12, 2018

Fiat Lux

Featured Trade:

(NEWSPAPERS REALLY KNOW WHO YOU ARE),

(TRNC), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)

Mad Hedge Technology Letter

July 12, 2018

Fiat Lux

Featured Trade:

(NEWSPAPERS REALLY KNOW WHO YOU ARE),

(TRNC), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)

Mad Hedge Technology Letter

July 11, 2018

Fiat Lux

Featured Trade:

(MASAYOSHI SON'S VISION TO TAKE OVER THE WORLD),

(SFTBY), (BABA), (NVDA)

Mad Hedge Technology Letter

April 24, 2018

Fiat Lux

Featured Trade:

(WHAT THE MEDIA REALLY WANTS FROM YOU),

(TRNC), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)

Publishing magnate and self-described populist William Randolph Hearst was a deep admirer of Adolph Hitler and did not shy away from using his newspapers as a de-facto mouthpiece spouting off Der Fuhrer's propaganda.

Hearst created content sympathizing with the Nazi ethos and even mobilized an embedded secret agent from the German government to act as a correspondent that followed hot, daily scoops inside Germany.

Hearst also used his publishing clout to pull the strings in the 1932 presidential election backing candidate John Nance Garner or "Cactus Jack" who later agreed to be Franklin D. Roosevelt's running mate.

The fusion of politics and media has been chiseled into human DNA since antiquity. However, the purpose of newspapers has evolved significantly since it became impossible to break even about 10 years ago.

Print newspapers are a lot like the US Postal Service - they specialize in losing money.

However, the (USPS) was never politicized as was the publishing industry until President Trump managed to commingle the loss-making mail outfit and Amazon as a joint problem roiling society.

The politicization comes at a cost to society.

All the well-intentioned journalists involved in earnest and quality journalism lose out because the new normal for newspapers has evolved into a William Hearst-like blatant tool promoting targeted interests.

Do you ever wonder why the Washington Post hardly ever publishes content harmful to the image of Amazon?

Because it is owned by the same man, Jeff Bezos, who founded Amazon (AMZN) in 1994, as he cruised in his car cross-country from New York to Seattle where he would start his tech empire.

Effectively, Jeff Bezos has the ear of each corner of the political power grid in Washington.

And while the president has been attacking Bezos as a job destroyer on a daily basis, Amazon has in fact been the largest private job CREATOR in the US. It added a staggering 130,000 new jobs in 2017, and an eye-popping 560,000 jobs over the past 10 years.

Last year saw Laurene Powell Jobs, widow to Steve Jobs, acquire the Boston-based American magazine The Atlantic.

The Atlantic earns more than $10 million per year in revenue and lures in over 33 million readers per month.

Billionaire biotech investor Patrick Soon-Shiong reached a deal with Tronc Inc. (TRNC), which possesses a vast array of various legacy media assets, to take over the LA Times and San Diego Union-Tribune for $500 million.

Tronc Inc. is on the verge of catching another bid with SoftBanks' (SFTBY) Masayoshi Son, looking to scoop up parts of the extensive portfolio.

Private equity group Apollo and media firm Gannett Company are also in the mix to acquire Tronc Inc.

Some of Tronc Inc.'s crown assets are the Chicago Tribune, the New York Daily News, and the Baltimore Sun among other regional newspapers with a large audience base.

Tronc's shares spiked almost 10% on whispers of the rumored news.

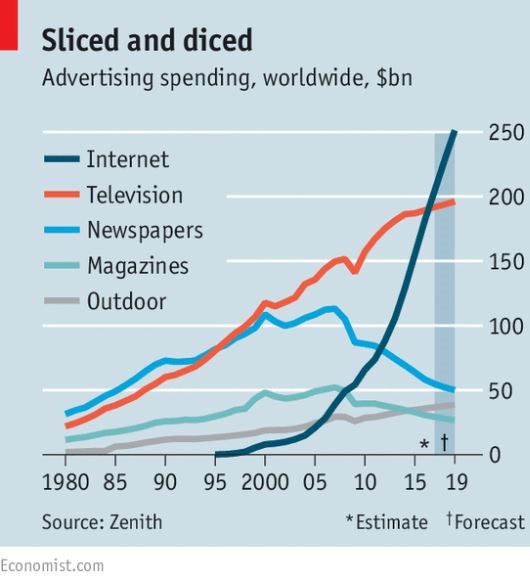

The courting of these news media assets comes at a time when Google (GOOGL) is funding a project to automate more than 30,000 stories per month for the local media as a cost-effective way to advance the business model.

Quality journalism written by a human is the last thing in which these mega-tech companies are interested.

The first thought that came into my head when I heard about SoftBank's vision fund swooping in for another company was data grab.

We have seen this story time and time again.

Newspapers and how an online subscriber behaves on a digital newspaper platform offer valuable data points that cannot be extracted elsewhere.

The data will reveal the political ideas, topics of interest, and other sensitive information deduced into a comprehensive data profile.

Effectively, a company such as SoftBank will be able to create a functional shadow profile for almost anyone.

The concept of shadow profiling emerged from the acrimony of Mark Zuckerberg's testimony in Washington and could be the next point of heated contention.

What are shadow profiles?

Shadow profiles are digital profiles crafted by data that were not directly handed over to Facebook (FB) by the user.

This data is extracted through fringe third parties, other friends on Facebook if they post content unique to you, and specifically through the "find your friends" function that recommends the uploading of an entire digital address book giving Facebook access to everyone you know.

Scarily, there is no opt-out for shadow profiling, and there probably won't be another congressional testimony about this topic anytime soon.

If Facebook wanted to turn into the FBI, it would be easy.

The treasure trove of data would give insight on the subtle nuances of authentic human behavior.

This artificial profile would seem real.

If you are an Android user like most of the world, Google could fill out the most comprehensive profile with a high degree of accuracy on most people.

The scandalous bit about shadow profiling is that these profiles are whipped up even if a user has never signed up for Facebook.

Shadow profiling, along with other data, becomes more precise as the volume of data piles up. To understand the behavior, trends, and tastes of most of the world's population is incredibly valuable.

Facebook could use this shadow profiling data to understand the wide range of non-Facebook user behavior.

This way of monetizing data would be highly illegal if leaked to an actionable third party and would be significantly worse than the Cambridge Analytica scandal.

This data should be deleted immediately, but Facebook has a backdoor way to keep the data in the system.

If Facebook got slammed for data leakage then others are in danger, too. That's because Facebook is not the only player mining data for money.

It wouldn't be surprising if other large cap tech companies started to create these shadow profiles to get dirt on their competitors as well as other use cases.

Tech is evolving at such a fast pace. It subconsciously encourages the never-give-up mentality that coerces firms to stay one step ahead, which Amazon has been able to do since its inception.

Newspaper companies are next in line to be absorbed by large cap techs continuously expanding web assets that hyper-focus on exponential data generation.

These newspapers will defend tech's interests in the economy similar to how newspapers were used as William Hearst's rallying cry for politics.

Jeff Bezos has chosen silence to react to President Trump's tweet offensive, but he could easily mobilize his newspaper to protect Amazon's interests.

Bezos just shrugs his shoulders and goes about his day because he knows Washington cannot do anything to change Amazon's dominance at the top of the tech food chain.

Better take the high road.

Not only do these big tech companies know who you talk to, what you buy, and where you are, but now they are given deeper access into the identity of users.

Be on the lookout for these assets to get cherry-picked and look forward to reading your future newspaper owned by Google, Facebook and the usual cast of characters.

The recently elevated existential risk that big cap tech is coping with will see meaningful reforms that will implement better defensive tactics, pre-emptive posturing to promote a positive big-picture narrative, and a bulletproof attempt to protect the moats around lucrative business models.

Stay away from these legacy newspaper stocks and only weigh up the media stocks that have already pivoted to the online streaming business model of scaling original premium content.

__________________________________________________________________________________________________

Quote of the Day

"The real danger is not that computers will begin to think like men, but that men will begin to think like computers." - said journalist Sydney Harris.

The biggest initial public offering in history is about to be issued by Chinese Internet commerce giant, Alibaba. The floatation, which could raise as much as $18 billion in cash, could value the total company as high as $220 billion, making it the fifth largest company in the US.

The big question now facing equity strategists around the world is whether the Alibaba issue is so big that it will destroy the market?

It certainly is a fair question. Some 44% of the IPO?s that have taken place this year are now underwater. The bloom has clearly gone off the new issue rose, especially for tech issues. If portfolio managers sell $18 billion of other stocks to buy the offering, it could literally suck the life out of an already fragile market.

Alibaba should have done their deal in January, when these deals were still hot. Did they miss the window?? It seems so.

The Chinese Internet juggernaut has another problem, what I call the ?Apple disease.? At $220 billion the company is so big that there is not enough money in the world to get the share price up substantially from the opening print.

Like Apple, it may become one of those behemoths that is permanently cheap, endlessly trolling the bottom of traditional valuation ranges. That frustrates the hell out of value investors. Multiple expansions never happen.

More than eye opening was the 2,300 page registration statement the company filed this week with the SEC. It included financial data for the last nine months of 2013. We learned that revenues were $5.66 billion, net profits were $2.85 billion, and the company is husbanding $7.88 billion in cash. Fair value should come to $40-$50 a share. Not bad for a communist country!

Most amazing are the 48% operating margins that the company is claiming. If true, they make competitors Amazon (AMZN) and eBay (EBAY) appear wildly overvalued.

The firm?s customer base grew by 44% YOY to 231 million last year. Chinese Internet usage generally is expected to soar from 618 million to 790 million by the end of 2016, up another 28%.

Yahoo (YHOO) paid a mere $1 billion for 40% of Alibaba in 2005, probably the only good decision they made in 15 years. After successive dilutions, the stake has fallen to 22.6%.

Yahoo really blew it when they passed on Microsoft?s (MSFT) offer to purchase the company for $31 a share just before the Great Crash, when it then plummeted to $8 a share. It was one of the worst calls I?ve ever seen, and a classic example of great technology innovators becoming lousy managers, and fall victim to hubris.

The sad thing is if you strip out the value of Yahoo?s Alibaba and Japan holdings, it is worth zero. That is probably a fair valuation given the depth to which the quality of the product has fallen. Mobile? What?s that?

The deal will make instant billionaires out of several individuals, most notably founder, Jack Ma, who is facing a $20 billion payday. Don?t you just love China!

Alibaba Ownership

34% Softbank

23% Yahoo

31% Others

8.8% Jack Ma-founder

3.6% Joseph Tsai-CEO

As for me, I?ll be passing on the IPO. It seems like the only time I get allocated shares in a new deal are when they fail. British Petroleum (BP) in 1987, ouch!

You can be sure Alibaba will be one of the most overhyped events in history, complete with dancing characters on the floor of the New York Stock Exchange (dancing pandas? Dancing soy sauce bottles?). After all, that is all it is good for, now that all the trading has gone online and is controlled by high frequency traders.

I am sure that there will be a later opportunity to buy much lower, such as we saw with the Tesla (TSLA) public offering in 2010, which dropped by half to $16 before the ink was barely dry. Then it was the ?BUY? of the century.

Make Jack Ma an Offer

Make Jack Ma an Offer

The day I bought my second lot of shares in the internet giant on December 12 was the exact point where a year of upward momentum in this stock came to a juddering halt.

The shares have since been like an errant teenaged child who you keep giving the benefit of a doubt until he goes out and steals a car. That is show business.

The immediate cause for the selloff was a downgrade of Alibaba by an unnamed Chinese internet analyst, in which Softbank is a major shareholder. The imminent IPO of Alibaba was the whole reason for owning Softbank.

It doesn?t help that the global emerging market rout has sent traders into ?RISK OFF? mode, especially in China. The doubling of Turkish interest rates overnight focused a great giant spotlight on the problem.

When in doubt, sell, especially stocks with funny sounding foreign names. ?Brave new world? technology stocks, like Alibaba, have been put on hold. A full handle move up in the yen against the US dollar to a new high for the year was further fat on the fire.

But what really tipped me over to the sell side was to see the Nikkei Average up a robust 2.70% last night, but Softbank shares drop by -1.30%. If it can?t catch a bid with this tailwind, it?s time to get out of dodge, or in this case, Kabutocho.

You knew this eventually had to happen. Since June, my Trade Alerts have enjoyed an almost unbelievable success rate of 90%. My followers have earned a +41.15% return on their capital, a multiple of what the market did. It was just a matter of time before I got slapped across the face with a fresh piece of sushi. But the entire world had to conspire against me to do it.

If you do have to lose money, this is the way to do it. By owning shares instead of options I was able to limit my loss to 2.86% off the back of a 14.3% fall in the shares. The trade was part of the general deleveraging that I have been implementing with my trading book since the end of 2013. It?s far better to have leveraged gains and unleveraged losses than the reverse.

No doubt, everything I predicted about Alibaba and Softbank will come true, and vast fortunes will be made by shareholders. But for the time being, we will have to restrict ourselves to reading about it in the newspapers from the sidelines.

Ouch!!

Ouch!!

Rumors hit the market Friday that Sprint (S) will mount a $20 billion takeover bid for T-Mobile (TMUS) in early January. The news caused a late day kerfluffle on what would otherwise have been a slow December pre holiday Friday.

The Shares of both companies immediately jumped 10%, which left many analysts scratching their heads. Normally, the shares of the acquirer falls (they?re spending money), while those of the target rise (they are selling for a premium to the market).

Why do I care about a minor US phone company? Guess who owns Sprint? Softbank, which took over the company for $21.8 billion last July, and carries a hefty 20% weighting in my model-trading portfolio.

The move would make Softbank one of the three largest US carriers. That will automatically trigger an antitrust review by the Justice Department, which blocked a similar takeover attempt for giant AT&T (T) earlier. Look at how Eric Holder stood in the way of the American Airlines-US Air deal, which both firms clearly needed to survive. And this is in a country with 100 airlines. So any decision here could be a long wait.

I think this is just an opening shot in a long campaign that eventually leads up to the Alibaba IPO, expected to be one of the largest in history (the biggest was also from China, the $128 billion deal for the Industrial Bank of China in 2010). Expect to hear a lot about Softbank?s role in all of this in coming months. This should be good for its stock price.

As part of the build up, my old employer, the Financial Times of London, named Alibaba founder and CEO, Jack Ma, as its Person of the Year. The paper chronicles Ma?s rise for abject poverty in Hangzhou, China, where he was the son of impoverished traditional performers, to becoming one of the world?s richest men.

Ma was fascinated by the English language at an early age, and used to listen to my own broadcasts on BBC Radio to learn new words (another one of my former employers). After graduating in 1988, he earned $12 an hour as a teacher in China. While working for the Foreign Trade and International Cooperation, he escorted foreign visitors to the Great Wall. One of them turned out to be Jerry Yang, co founder of Yahoo.

Thus inspired, Ma went on to found Alibaba in 1999. Its initial strategy was to match up Chinese manufacturers with American customers, an approach that proved wildly successful. He then took on Ebay. In the following years the US e-commerce giant saw its Chinese market share plummet from 80% to 8%, most of that going to Alibaba. Today, Alibaba has 600 million registered users, and one day in November it clocked a staggering $6 billion in sales.

The FT estimates its current market value at $100 billion. To read the rest of the FT profile, please click here. Its IPO will be one of the preeminent investment events of 2014. Better to get in early.

Followers of my Trade Alert Service will notice that this is one of the few outright equity trades that I have done this year. This is a way for me to deleverage my exposure after a spectacular stock market run. Equity ownership ducks the time decay that plagues call options, and avoids the leverage inherent in call spreads.

If the stock is unchanged over the holidays, it won?t cost me a dime. One thing is for sure. When the Alibaba IPO is announced, it will be a surprise. The only way to participate is to get in indirectly through a minority owner now.

Don?t expect an allocation from your broker, unless they think it is going o fail.

I can?t believe how fast the year has gone by. It seems like only yesterday that I was riding the transcontinental railroad from Chicago to San Francisco, writing my 2013 All Asset Class Review. Now 2014 is at our doorstep.

As usual, the market has got it all wrong. There is not going to be a taper by the Federal Reserve next week. If there is, it will be only $5-$10 billion, which means that $70-$75 billion a month in Fed bond buying continues. Either way it is a win-win.

However, managers are eternally loath to trade against an unknown, hence the weakness we are seeing this week. I think that we have entered another one of those sideways corrections that has been a hallmark of the market all year, and that there is a reasonable chance that we saw the low of the entire move down this morning at 1,780 in the S&P 500.

That sets up a dead, range trading market into the Fed decision next Wednesday afternoon. Once their Solomon like choice is out, it will be off to the races for the markets once again, probably all the way until 2014.

However, we are heading in the Christmas holidays, when volume and volatility shrivel to a shadow of its former selves, with daily ranges often falling within 50 Dow points. So it is important to have a large short volatility element to your portfolio.

That way, you will make money on every flat day, of which there should be many. That?s why I have 70% of my current model-trading portfolio invested in call spreads.

My current holding in the (SPY) has me profitable at all points above $175.68. If we move below that, any losses should be more than offset by profits thrown off by the rest of the portfolio. The same is true for my call spread in the financial ETF (XLF).

The Japanese yen is clearly in free fall, probing new lows almost every day. That should take the (FXY) to $95, and explains my triple weight 30% holding in the area. Bonds (TLT) just can?t get a break, failing to rally over $105 for the third time. Lower levels beckon, making my bear put spread look pretty good, my second one this month.

With a dramatically weakening yen, you have to add to Japanese equities, which will benefit hugely. That?s why I doubled up on my position in Masayoshi Son?s Softbank (SFTBY) this morning. The day they announce the Ailibaba IPO, probably early next year, these shares should be up 10%-20%.

To summarize, this portfolio is perfectly set up for the following: ?A sideways move for four more trading days, then an upside breakout after the Fed decision, then going to sleep inside a slow grind up over Christmas and New Years.

The grand finale should come on January 2, the first trading day of 2014, when I expect the value of the portfolio to pop a full 5% or more. This will be delivered by a massive new wave of capital into the markets, which for calendar and legal reasons couldn?t be invested until this day.

What will they buy? Everything that worked last year. After all, that?s why these managers were hired. Why not start the New Year with a bang, and then spend the rest of the year trading against that profit.

It certainly worked this year.

Has It Been That Long?

Has It Been That Long?

I have always been a big fan of buying a dollar for 30 cents. That appears to be the opportunity now presented by the Japanese software giant, Softbank (SFTBY).

This gorilla of the Internet space was founded and run by my old friend, Masayoshi Son, who many refer to as a combination of the Jeff Bezos and the Bill Gates of Japan. I have known Mas, as his friends call him, for 30 years, meeting him, of all places, at a University of California Alumni Association meeting. Mas received his BA in economics from Berkeley in 1980.

In three decades, Mas has turned an obscure, hard copy Japanese computer hobbyist magazine into today?s massive online empire. You may know him as the organizer of the huge Comdex conferences in Las Vegas every January, the Woodstock of technology gatherings. Today, Mas has an estimated personal net worth $9 billion, not bad for a kid who wore the same pair of ragged Levis to his economics classes every day.

The really interesting thing about Softbank right now is not what Mas is doing, but what he owns. That includes a 37% stake in the Chinese Internet giant, Alibaba, which boasts an overwhelming 80% market share in the Middle Kingdom.

The Hangzhou based Alibaba is actually a group of Internet-based e-commerce businesses including business-to-business online web portals, online retail and payment services, a shopping search engine and data-centric cloud computing services. Think of it as Amazon (AMZN), eBay (EBAY), Google (GOOG), and Oracle (ORCL) all wrapped into one.

In 2012, two of Alibaba?s portals together handled 1.1 trillion Yuan ($170 billion) in sales, more than competitors eBay and Amazon.com combined.

Its sales account for no less than 3% of China?s total GDP. Yikes! To learn more about their website please: http://news.alibaba.com/specials/aboutalibaba/aligroup/index.html.

Online commerce in China is now growing faster than in any other place on the planet, including the US. Some 5% of retail transactions in the People?s Republic take place on the Internet, and that is expected to grow to 25% over the next three years. By comparison, it took online business in America 15 years to reach that market share.

What is happening in China now is truly fascinating. They are leapfrogging traditional brick and mortar stores, going straight from barter to online purchases, completely skipping the Wal-Mart stage of the retail evolution. I saw the same thing happen during the early nineties, when eastern Europeans jumped straight from having no phones to mobile ones, bypassing decades of unreliable and indifferent landline service.

The value of Alibaba is anyone?s guess as the company is still private. However, my former employers at The Economist magazine estimate that it is worth anywhere from $55-$120 billion. What this means is that you can buy Softbank now purely for the value of its Alibaba ownership, and get everything else the company does in the online universe for free.

But wait! It gets better. Softbank also owns major stakes in Yahoo, whose shares are up a gob smacking 157% since last year (Thank you Marissa Meyer!). It owns a major chunk of Sprint (S), which has gained a mind blowing 325% since 2012. Can Mas pick them, or what? Softbank also owns pieces of Japan Cellular and many other companies.

Add it all up together, and you get a Softbank that is worth at least $250 billion, almost triple its current $97 billion market capitalization. In other words, it?s a steal at this price.

Yes, you may say, this all sounds great. But how do I buy shares in Japan in yen? Easy. Softbank trades on the pink sheets in the US (hence the five letter ticker symbol) and is denominated in US dollars. Normally this means nothing, as liquidity in the pink sheets is notoriously poor.

Not so for (SFTBY), which saw 1.6 million shares worth $67 million trade around $42 a share on a slow Friday with a reasonably narrow spread. You may not be able to margin these, but at least you can get them. You also have some yen exposure here, as these shares are tied to the domestic shares in Japan. As for the big hedge funds, they have to go to Tokyo to get the size they want, and then hedge out their yen risk.

OK, OK, you say. Great story. But the road to perdition is paved with fabulous value plays that were never realized in the marketplace. This thing could stay cheap forever, like Apple (AAPL).

Aha! I got you! Alibaba is about to go public in the US, with Goldman Sachs now polling major institutional investors about potential interest. Given the chance to buy an Amazon clone at ten year ago prices, this IPO will be a blockbuster, making the recent Twitter (TWTR) float pale by comparison.

Did I mention that my buddy, Dan Loeb of hedge fund giant Third Point Partners, totally agrees with me, and has bought $1 billion worth of Softbank shares already? In fact, many believe that Alibaba could be the Apple of this decade, about to deliver a tenfold increase in its share price.

That seems to be the right thing to do this year.

Hitch Your Wagon to Mas

Hitch Your Wagon to MasI have always been a big fan of buying a dollar for 30 cents. That appears to be the opportunity now presented by the Japanese software giant, Softbank (SFTBY).

This gorilla of the Internet space was founded and run by my old friend, Masayoshi Son, who many refer to as a combination of the Jeff Bezos and the Bill Gates of Japan. I have known Mas, as his friends call him, for 30 years, meeting him, of all places, at a University of California Alumni Association meeting. Mas received his BA in economics from Berkeley in 1980.

In three decades, Mas has turned an obscure, hard copy Japanese computer hobbyist magazine into today?s massive online empire. You may know him as the organizer of the huge Comdex conferences in Las Vegas every January, the Woodstock of technology gatherings. Today, Mas has an estimated personal net worth $9 billion, not bad for a kid who wore the same pair of ragged Levis to his economics classes every day.

The really interesting thing about Softbank right now is not what Mas doing, but what he owns. That includes a 37% stake in the Chinese Internet giant, Alibaba, which boasts an overwhelming 80% market share in the Middle Kingdom.

The Hangzhou based Alibaba is actually a group of Internet-based e-commerce businesses including business-to-business online web portals, online retail and payment services, a shopping search engine and data-centric cloud computing services. Think of it as Amazon (AMZN), eBay (EBAY), Google (GOOG), and Oracle (ORCL) all wrapped into one.

In 2012, two of Alibaba?s portals together handled 1.1 trillion Yuan ($170 billion) in sales, more than competitors eBay and Amazon.com combined.

Its sales account for no less than 3% of China?s total GDP. Yikes! To learn more about their website please visit http://news.alibaba.com/specials/aboutalibaba/aligroup/index.html.

Online commerce in China is now growing faster than in any other place on the planet, including the US. Some 5% of retail transactions in the People?s Republic take place on the Internet, and that is expected to grow to 25% over the next three years. By comparison, it took online business in America 15 years to reach that market share.

What is happening in China now is truly fascinating. They are leapfrogging traditional brick and mortar stores, going straight from barter to online purchases, completely skipping the Wal-Mart stage of the retail evolution. I saw the same thing happen during the early nineties, when eastern Europeans jumped straight from having no phones to mobile ones, bypassing decades of unreliable and indifferent landline service.

The value of Alibaba is anyone?s guess as the company is still private. However, my former employers at The Economist magazine estimate that it is worth anywhere from $55-$120 billion. What this means is that you can buy Softbank now purely for the value of its Alibaba ownership, and get everything else the company does in the online universe for free.

But wait! It gets better. Softbank also owns major stakes in Yahoo, whose shares are up a gob smacking 157% since last year (Thank you Marissa Meyer!). It owns a major chunk of Sprint (S), which has gained a mind blowing 325% since 2012. Can Mas pick them, or what? Softbank also owns pieces of Japan Cellular and many other companies.

Add it all up together, and you get a Softbank that is worth at least $250 billion, almost triple its current $97 billion market capitalization. In other words, it?s a steal at this price.

Yes, you may say, this all sounds great. But how do I buy shares in Japan in yen? Easy. Softbank trades on the pink sheets in the US (hence the five letter ticker symbol) and is denominated in US dollars. Normally this means nothing, as liquidity in the pink sheets is notoriously poor.

Not so for (SFTBY), which saw 1.6 million shares worth $67 million trade around $42 a share on a slow Friday with a reasonably narrow spread. You may not be able to margin these, but at least you can get them. You also have some yen exposure here, as these shares are tied to the domestic shares in Japan. As for the big hedge funds, they have to go to Tokyo to get the size they want, and then hedge out their yen risk.

OK, OK, you say. Great story. But the road to perdition is paved with fabulous value plays that were never realized in the marketplace. This thing could stay cheap forever, like Apple (AAPL).

Aha! I got you! Alibaba is about to go public in the US, with Goldman Sachs now polling major institutional investors about potential interest. Given the chance to buy an Amazon clone at ten year ago prices, this IPO will be a blockbuster, making the recent Twitter (TWTR) float pale by comparison.

Did I mention that my buddy, Dan Loeb of hedge fund giant Third Point Partners, totally agrees with me, and has bought $1 billion worth of Softbank shares already?

I?ll wait for a dip before I send out the Trade Alert. If I don?t get one, I may just throw in the towel and buy it at market.

That seems to be the right thing to do this year.

Hitch Your Wagon to Mas