Mad Hedge Biotech and Healthcare Letter

November 5, 2024

Fiat Lux

Featured Trade:

(DANCING WITH SHADOWS)

(RHHBY), (SGMO), (LLY), (BIIB), (ABBV)

Mad Hedge Biotech and Healthcare Letter

November 5, 2024

Fiat Lux

Featured Trade:

(DANCING WITH SHADOWS)

(RHHBY), (SGMO), (LLY), (BIIB), (ABBV)

In 1906, Dr. Alois Alzheimer first encountered what he called a “mysterious” mental illness, examining the brain of a 55-year-old woman who had died under strange neurological circumstances.

Over a century later, that mystery hasn’t let up. We’re still scratching our heads—and burning through money.

By 2050, Alzheimer’s is projected to cost the U.S. healthcare system $1.3 trillion, more than the entire GDP of Australia.

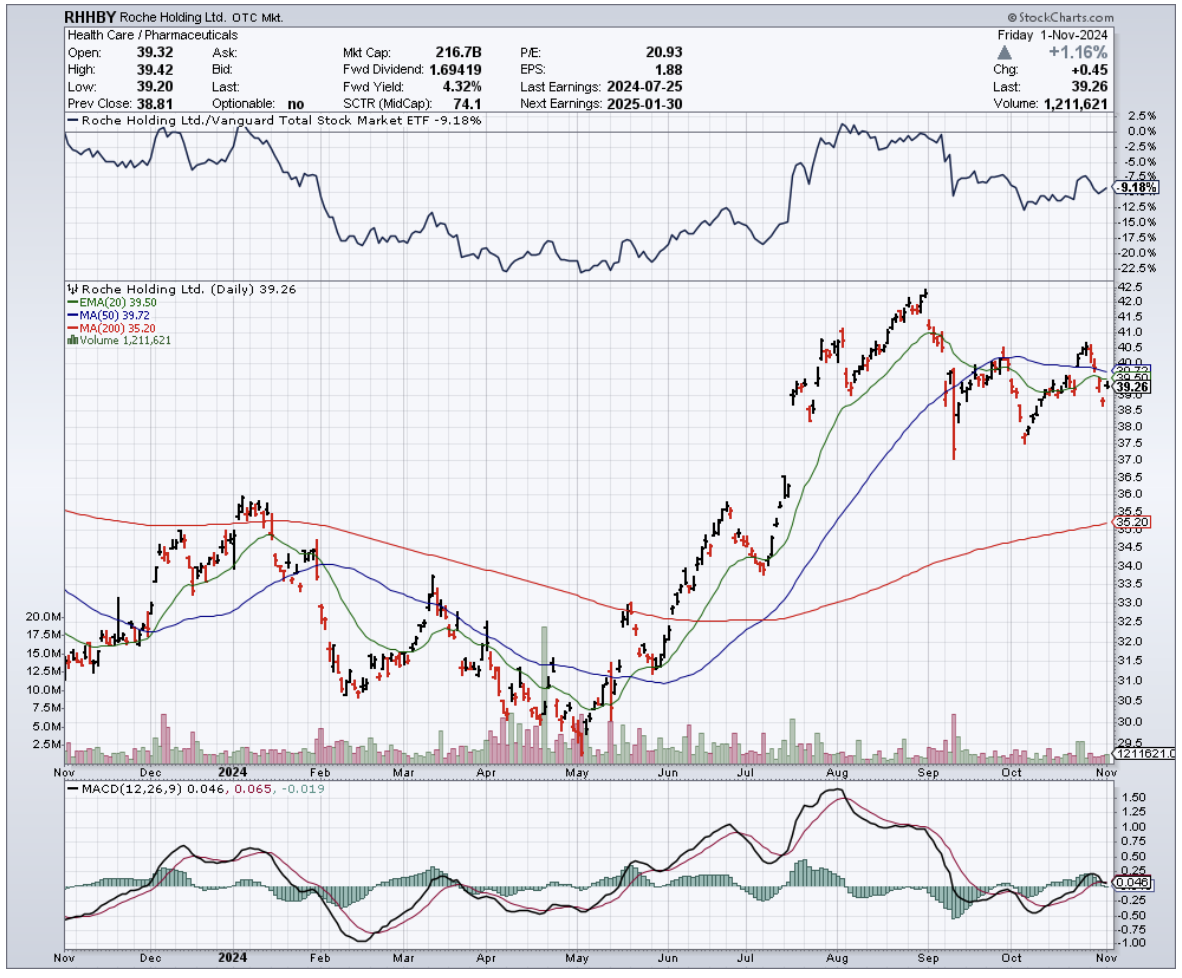

But something’s happening at Roche (RHHBY) that’s got my scientific spidey senses tingling.

Roche has been chasing Alzheimer’s solutions for over two decades, pouring resources into this elusive brain burglar that defies every rule in the book.

And yet, here they are—undaunted, driven by a noble (and, yes, profitable) goal to relieve the massive toll AD takes on patients, families, and entire healthcare systems.

It hasn’t been smooth sailing; setbacks and “whoops, not this time” moments have kept things bumpy. Recently, though, I’ve been seeing hints of a breakthrough that just might bring this long, shadowy dance with Alzheimer’s closer to the light.

For those who've been reading my letter since 2008, you know I rarely get excited about big pharma unless there's real meat on the bone. Well, this time there is, and it's called Brainshuttle technology.

If you’ve never heard of it, think of it as a kind of souped-up delivery service for the brain—no, not that kind. This tech helps Roche’s meds cross the blood-brain barrier, that stubborn security guard that only lets a select few molecules into the brain.

It’s great at keeping out random junk but also frustratingly good at blocking drugs we actually want to get in there.

Brainshuttle could change that, allowing antibodies to cross over more easily and making lower doses (and hopefully fewer nasty side effects) possible.

Enter trontinemab, a drug that’s caught a lot of eyes recently. Armed with Brainshuttle, this amyloid-beta antibody is like the brain’s personal pest control.

Early trials are promising: Roche reported that trontinemab is sweeping out amyloid plaque faster than a Roomba on espresso, and all at lower doses.

Less dose, more punch, and fewer side effects? Sounds like the AD holy grail. They’re even eyeing an accelerated approval path with the FDA.

Now, the FDA isn’t exactly known for sprinting to approval—especially with Alzheimer’s drugs—but trontinemab’s early results make it a strong contender.

But Roche isn’t putting all its eggs in one beta basket. AD research has been dominated by amyloid-beta, but there’s another protein that scientists are pretty excited about: tau.

If amyloid-beta is the ringleader, tau is the muscle, the heavy that clogs up brain cells and wreaks havoc.

To tackle tau, Roche has teamed up with Sangamo Therapeutics (SGMO), a company with tech that sounds like it’s straight out of a sci-fi novel—zinc finger molecules.

These little DNA-grabbers are designed to silence the tau gene, essentially telling it to cool it and stop producing the stuff that clogs up the brain.

The partnership also gives Roche access to something else in Sangamo’s arsenal: an adeno-associated virus capsid. (Translation: a delivery mechanism that gets things across the blood-brain barrier.)

If these tools work as planned, Roche may have a real chance to give AD a one-two punch with both amyloid-beta and tau treatments.

But let's be real here. This is still the Wild West of biotech, and Roche has had its share of setbacks.

They recently walked away from a partnership with UCB, returning the rights to an anti-tau antibody called bepranemab.

Even though UCB called the Phase 2a data "encouraging," it apparently didn't meet Roche's internal bar. That's the thing about Alzheimer's drug development - it's about as predictable as my teenager's mood swings.

The competition isn't sleeping either. Eli Lilly (LLY), Biogen (BIIB), and AbbVie (ABBV) are all throwing everything but the kitchen sink at this disease. But Roche's Brainshuttle technology might just be their secret weapon in this fight.

Here's what keeps me optimistic: Roche’s multi-pronged strategy, combining amyloid-beta and tau, might just give them an edge. It’s not guaranteed—far from it—but having multiple avenues does give them a better shot at success.

This is what I call a "chess not checkers" opportunity. The potential payoff is massive - we're talking about a market that could make crypto's best days look like pocket change. But timing is everything.

So, I'll be watching trontinemab's development like a hawk. The Sangamo collaboration is also on my radar - any breakthrough in tau-targeted therapies could be a game-changer.

As always, don’t bet the farm, folks—not even on a biotech darling like this. But if you’re itching to add a little intellectual flair to your portfolio, Roche’s Alzheimer’s gambit is worth a look. Buy the dip, but set those stop losses. After all, even the best-laid plans of mice and biochemists often go awry.

Mad Hedge Biotech and Healthcare Letter

April 4, 2024

Fiat Lux

Featured Trade:

(A HIGH RISK, HIGH REWARD BIOTECH)

(VYGR), (SNY), (ABBV), (NBIX), (NVS), (AZN), (SGMO), (BIIB), (RHHBY), (IONS)

Global Market Comments

February 13, 2023

Fiat Lux

Featured Trade:

(HOW CRISPR TECHNOLOGY MAY SAVE YOUR LIFE)

(TMO), (OVAS), (CLLS), (SGMO)

CLICK HERE to download today's position sheet.

When I was a DNA scientist at UCLA 50 years ago, the team used to slack off whenever our professor was attending an out-of-town conference.

We used to take pure 200 proof ethanol the university kept on hand “for research purposes,” used it to bring our beer up to 100 proof, and then speculate about the future of our obscure, neglected field.

With the technology at hand, we predicted it would take 3,000 years to fully decode the 3 billion base pairs of a length of human DNA. It then might take another 1,000 years to manipulate our genes to accomplish something useful, like curing cancer.

Maybe it was our “enhanced” beer talking, but we were off on our bold forecast by only 2,970 years.

Dr. Craig Venter published a map of his own DNA in 2001 using sophisticated algorithms to vastly accelerate our own snail-like progress.

The second step, that of functional genetic engineering, took only another decade instead of a millennium.

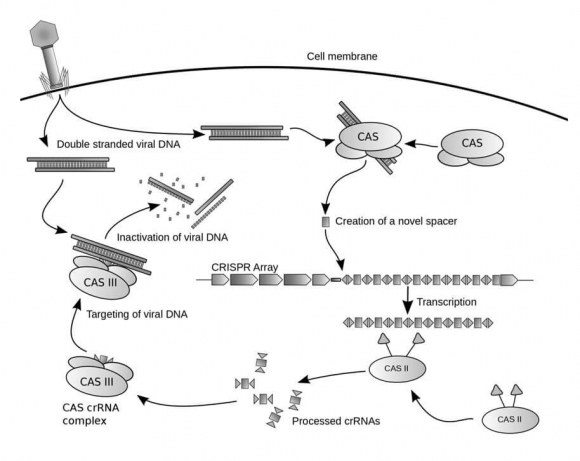

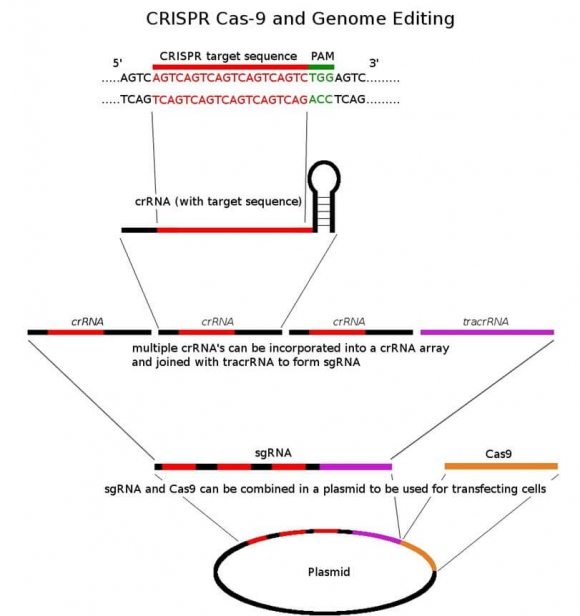

Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR).

Memorize this term, write it in your diary, and put it on a post-it note on your computer.

It may save your life someday, if not add decades to your life. And it could also make you a multimillionaire if you play your cards right. More on that below.

And I count myself on becoming one of its fortunate users, once the technology goes retail, which should be soon.

If you are another DNA scientist, all I need to tell you is that CRISPR is used to manipulate segments of prokaryotic DNA containing short repetitions of base sequences.

Each repetition is followed by short segments of spacer DNA from previous exposures to a bacteriophage virus or plasmids. The protein fragments that identify and snip these crucial gene segments are called CRISPRs.

If you are the average Joe stock trader, which most of you are, suffice it to say that CRISPR technology is being developed that will enable you to edit your own DNA on a customized basis and then pass the changes on to your future generations.

This will eventually allow you to become immune to all diseases, increase your intelligence, and possibly live forever. Just cut out a bad gene and put in a new one and you and all your future decedents are fixed for good.

You only have to make it five or ten more years at the most with your current vintage DNA, and you can easily live another century.

Oh, and by the way, the company that successfully brings CRISPR products to market in an economical, cost affordable way should see its stock price rise tenfold, if not one hundredfold.

Interested?

Reading up on the research for this piece, one thought kept recurring in my mind: “I can’t believe they are already doing this NOW!”

CRISPR technology was first mooted by a Japanese researcher in 1987. It turns out that the Japanese have a huge head start in developing DNA technologies thanks to a 300-year track record in brewing potent rice wines, like sake.

By 2007, CRISPR went mainstream, attracting funding from a broad range of industries. There was initial heavy interest from the food producers, which sought to make plants and their seeds immune to common crop-destroying diseases.

Their work is partly responsible for the record crop yields that are presently crushing agricultural prices across the board.

As of today, there have been over 3,000 peer-reviewed papers published about CRISPR, each one taking us an infinitesimal step forward.

Currently, there are clinical trials underway employing CRISPR technology to fight multiple forms of cancer, herpes viruses, and advance immunosuppression in human organ transplants.

A legal battle broke out over who owns the rights to CRISPR technology, with Thermo Fisher Scientific (TMO) holdings several key patents.

OvaScience Inc. (OVAS) has started applying CRISPR to human embryos. It didn’t take long to ignite a firestorm of controversy over the prospect of permanently altering the human germline.

Will the wealthy buy their way into genetic superiority and immortality? Or will we accidentally create an organism that could wipe out the human race? Cries of “Social Darwinism” are everywhere.

Or worse, what if the Chinese make their own population immune to bioweapons which they then unleash on the rest of the world?

What if a gene treatment that cures cancer also makes individuals, aggressive, paranoid, or violent?

Talk about letting a genie out of a bottle while also opening Pandora’s Box!

Some leading scientific journals, like Nature and Science, have refused to publish some CRISPR paper over ethical concerns. Unsurprisingly, Chinese scientists have the lead in the most controversial applications.

It’s all way beyond my pay grade.

During my lifetime, I have seen science drop some real clangers.

While in Europe this summer, I saw a Thalidomide baby grown up, now in his fifties. The anti-morning sickness drug developed by a German company produced children with horrifying flippers instead of arms.

Even today, Thalidomide is held out as an example of the need for enhanced drug regulation in the US.

In the early 1950s, one doctor developed the bright idea of giving newborn babies pure oxygen. Everyone who received this treatment went completely blind for life.

And then the CIA developed LSD as a potential weapon, testing it on its own unwitting employees, who developed an unfortunate tendency to jump out of windows from high floors. We all know how that one worked out.

We already know what genes people will choose when given the opportunity to do so, instead of using the ones they inherited, the old-fashioned way.

The unregulated human artificial insemination industry makes available genotypes of every race and nationality in abundance. More than 90% choose tall, blonde, intelligent donors, inadvertently creating a financial windfall from the UC Berkeley Men’s Water Polo Team.

It is an outcome Adolph Hitler would have been proud of, as more than 1 million of these children have been born in the US alone.

Some prolific water polo players have sired more than 100 children, which are now using websites like 23andMe and Ancestry.com to find each other and socialize.

It was not in the game plan.

As is always the case with new, cutting edge, groundbreaking technologies, it is hard to find a rifle shot investment that gives you a pure play.

Many such efforts are subsumed inside huge companies where a specific technology never moves the needle. Starts ups often go bust because they can’t keep up with rapidly evolving technology.

That’s what happened to the 3D printing industry, and I can’t remember how many hard drive companies and PC makers that have gone under.

Editas (EDIT), Caribou Biosciences (CRBU), Intellia (NTLA), CRISPR Therapeutics (CRSP), and Precision Biosciences (DTIL) have all gone public over the last five years. Here is your bite of the apple.

Cellectis (CLLS) is a $1.1 billion French company that is involved in both gene editing and cancer immunotherapy. The Company has improved the quality of crops for the food and agriculture industries.

And here is the really good news.

Many of these shares have dropped 70%-80% in the last year, thanks to the generalized biotech meltdown and the wholesale flight from profitless companies. Crisper alone fell 77% top to bottom, much to my own personal financial destruction.

Many will find the prospect of living another century enticing. I might be interested if I could get back the body I has when I was 25 but still know what I know now.

The possibility of finding a stock that could rise 10 or 100 times is MUCH more interesting.

Putting Another 100 Years on the Clock?

Mad Hedge Biotech and Healthcare Letter

January 17, 2023

Fiat Lux

Featured Trade:

(COMPROMISE IS THE BEST STRATEGY)

(JNJ), (AMGN), (TAK), (VRTX), (CRSP), (EDIT), (PFE), (CRBU), (SGMO), (LLY), (AXSM)

An optimist looks at bubbles and visualizes champagne, while a pessimist’s mind goes to Alka-Seltzer. The same thing happens with investors.

Some believe that the steep losses suffered by stocks and bonds in 2022 are a much-needed “cleansing,” which would set the stage for renewed partnerships and collaborations along with high returns. Others simply view it as the first chapter in a protracted bear market.

Meanwhile, a handful believes that it’s a combination of both perspectives—especially for the biotechnology industry.

Roughly two years following the decline of biotechnology stocks, several executives from small and midsize organizations finally concede that their share prices might no longer be able to bounce back anytime soon. In fact, some have been fielding panicked calls from execs of fledgling biotech firms, offering to sell their companies at a discount.

The alteration in the medical device and biotechnology landscape only started a few months before the previous year ended.

This is because, before the change in perspective, when the SPDR S&P Biotech exchange-traded fund (XBI) had slid by about 40% from its 2021 peak, many leaders in the biotech sector still believed that their companies could regain momentum.

The primary concern for smaller biotech and medical devices companies, which allocate years to developing and testing products without any commercially approved treatment, is that the continuous decline in their valuations has made it practically impossible to generate new money to fund any of their projects.

Given this scenario, many small and midsize biotechs would go under soon, particularly those with no data strong enough to provide near-term growth catalysts.

This is where Big Pharma names are expected to come in. After all, these large-cap companies offer an alternative option with their non-dilutive sources of funding and ever-growing war chests.

Big companies, though, have been more cautious in cutting big checks for acquisitions. Despite the high expectations last year, we only saw a few massive deals, including Abiomed’s sale to Johnson & Johnson’s (JNJ) for $19 billion and Amgen’s (AMGN) $30 billion agreement with Horizon Therapeutics.

Instead, these Big Pharma companies appear to prefer partnerships and collaborations. In these deals, they give out smaller payments to biotechnology firms to work with them on specific early-stage programs.

This type of investment seems to be a safer bet for big companies because it allows them to make several deals without spending too much. They can even collaborate with competing biotechs to determine which could develop the most effective and cost-efficient solution.

Smaller biotechs benefit from this type of deal as well.

In the pre-pandemic era, the valuations of these companies quickly soared based on the potential of their pipeline candidates. Some share prices would skyrocket with just a hint of positive data. This is no longer the case these days, not only because investors have become more discerning but also more anxious over experimental programs.

So instead of getting acquired, smaller biotechs can choose to strike partnerships with large-cap companies. This is an excellent way to inject some funding into their programs and, hopefully, provide them with revenue streams, especially since Big Pharma companies know how to market new products.

It sounds challenging, but a genuinely promising program could fetch a large sum.

Perhaps the most significant indicator that not all hope is lost comes from Takeda (TAK) when it purchased an experimental treatment undergoing tests as a potential psoriasis medication.

This candidate, developed by a privately held biotechnology firm called Nimbus Therapeutics, was sold for a whopping $4 billion upfront, plus roughly $2 billion more for future milestone payments. And here’s the clincher: Takeda got the experimental drug by a razor-thin margin.

In terms of acquisitions, some larger companies have been open to that route. For instance, AstraZeneca (AZN) shelled out $1.3 billion for CiniCor Pharma, while Ipsen (IPSEY) purchased Albireo Pharma (ALBO) for $1 billion.

While the future for smaller biotechs remains uncertain, several names continue to be in conversations whenever acquisitions are discussed.

There’s Vertex Pharmaceuticals (VRTX), which has long been reported to take interest in acquiring CRISPR Therapeutics (CRSP) and Editas Medicine (EDIT), with the latter looking more attractive thanks to its cheaper price tag.

Meanwhile, Pfizer (PFE) has been shopping around for a biotech to bolster its gene-editing programs, and so far, Caribou Biosciences (CRBU) and Sangamo Therapeutics (SGMO) are under serious consideration.

With its continuing interest in central nervous system diseases, such as Alzheimer’s and Parkinson’s, Eli Lilly (LLY) has been aggressive in its search for a company to acquire. Among the strongest candidates is Axsome Therapeutics (AXSM).

With this daunting reality setting in, one thing has become absolutely sure: the biotechnology sector has become a buyer’s market for big companies with cash to spare for acquisitions and collaborations.

Mad Hedge Biotech and Healthcare Letter

May 6, 2022

Fiat Lux

Featured Trade:

(A PANDEMIC CONQUEROR READY FOR MORE)

(PFE), (BNTX), (AMGN), (JNJ), (BIIB), (RHHBY), (SGMO), (BMRN)

The past 50 years have been excellent for investors as stocks have climbed by over 100% within a five-year span ending last December 2021.

Sadly, this story has taken a different course in 2022 as investors became more cautious primarily due to inflationary fears.

However, a handful of businesses are strong and promising enough to survive and even thrive in a high inflation environment.

One company that met this challenge head-on in the healthcare and biotechnology sector is Pfizer (PFE).

In fact, Pfizer didn’t simply meet the estimates of Wall Street in its 2022 first-quarter earnings report. It blew past their expectations.

Pfizer recorded $25.7 billion in revenue for the first quarter, well above the consensus estimate of $23.9 billion. This represented a 77% surge year-over-year.

Meanwhile, its earnings per share of $1.62 was notably higher than the average $1.47.

As anticipated, these gains were mainly driven by the staggering revenues from its COVID-19 vaccine and antiviral medication.

Comirnaty continued its winning ways, with Pfizer generating a jaw-dropping $13.2 billion in sales from the vaccine it co-created with BioNTech (BNTX).

The company's market share in the developed world currently stands at 67%, while it holds 62% of the global market.

As for its Paxlovid antiviral treatment, this drug raked in $1.5 billion in the first quarter and claimed approximately 90% of the US market.

Evidently, Pfizer continues to receive massive boosts from its COVID-19 treatments.

Now, the real question moving forward hinges on whether these financial results can be normalized as part of Pfizer’s future regardless of the pandemic’s effects.

After all, the vaccine sales comprised almost 60% of the company’s total revenue. With this in mind, Pfizer remains firm in its projections that it could rake in $98 billion to $102 billion in annual revenue for 2022.

While this still indicates a strong belief in the pandemic-related treatments, it’s also indicative of a deeper and more diverse pipeline.

Although not as high-flying as the COVID-19 vaccines, a number of other categories notched notable gains year-over-year, like its rare disease segment, which saw a 23% increase.

The growth of its oncology sector, which recorded a 6% climb, was mainly attributed to the 35% rise and expansion of Pfizer’s biosimilar arm.

So far, the top-selling treatments in this segment are Retactrit, a biosimilar of Amgen’s (AMGN) Epogen and Johnson & Johnson’s (JNJ) Procrit, Zirabev, a biosimilar of Roche’s (RHHBY) Avastin, and Rixience, a biosimilar of Biogen’s (BIIB) Rituxan.

Even Pfizer’s pneumonia vaccines showed off a 22% growth this quarter with $1.57 billion in sales.

Apart from these, the FDA has recently lifted the hold on the Hemophilia A gene therapy clinical trials of Pfizer and Sangamo (SGMO).

Without this limitation, the two companies may already have the opportunity to catch up to the leading biotech in this sector, BioMarin (BMRN). If everything works out, Pfizer and Sangamo are slated to release a readout from this program by the second half of 2023.

Another venture that’s expected to pay off soon is Pfizer’s $6.7 billion acquisition of Arena Pharmaceuticals, which was seen as a decisive move to bolster its inflammation and immunology segment.

The company is expected to file for a regulatory for Etrasimod, Arena’s lead program on ulcerative colitis and Crohn’s disease, by the second half of 2022.

This means that the recent acquisition is already expected to add to the near-term growth of Pfizer, which could be as early as 2023.

Moreover, Etrasimod represents an incredible market opportunity, with the treatment projected to reach $28 billion in annual sales by 2025.

Aside from the promising potential of Arena’s pipeline, Pfizer’s move also shows how the company is leveraging the capital influx from its COVID sales and its strategy on a more aggressive growth investment cycle.

On top of that, Pfizer’s partnership with BioNTech highlighted the benefits and competitive advantage in terms of how the biopharmaceutical titan works and collaborates with smaller biotechnology firms.

Hence, Pfizer has made itself the first and obvious choice among budding companies with groundbreaking innovations.

Overall, Pfizer has proven itself more than capable of handling any economic and health crisis. Not only has it come up with a solution that ultimately saved humanity from a deadly virus, but it also emerged victorious and stronger amid a global meltdown.

Given its history and trajectory, it looks like it has nowhere else to go but up. Hence, it would be best if you bought the dip.

Global Market Comments

April 6, 2022

Fiat Lux

SPECIAL CRISPR TECHNOLOGY ISSUE

Featured Trade:

(HOW CRISPR TECHNOLOGY MAY SAVE YOUR LIFE),

(TMO), (OVAS), (CLLS), (SGMO)