Below please find subscribers’ Q&A for the October 6 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: When will Freeport McMoRan (FCX) go up?

A: When the China real estate crisis ends, and they start buying copper again to build new apartment buildings.

Q: Do rising interest rates imply trouble for tech?

A: Yes, they do, but only for the short term. Long term, these things all double on a three-year view; and the next rise up in tech stocks will start when interest rates peak out, probably with 10-year yields at 1.76% or 2.00%. The great irony here is that all the big techs profit from higher rates because they have such enormous cash flows and balances. But that is just how markets work.

Q: I know you’ve been promoting Tesla (TSLA) for a very long time. What do you think about it here?

A: We’ve just gone from $550 to over $800. It actually has been one of the best performing stocks in the market for the past four months. Short term, you want to take profits; long term you want to hold it because it could go up 10 times from the current level. They just broke all their sales records and are the fastest growing car company in the US or Europe.

Q: If Blackrock (BLK) is reliant on interest rates, will the rise in interest rates hurt them?

A: No, it’s the opposite. Rising interest rates are positive for Blackrock because it improves the return on their investments, which they get a piece of; so rising interest rates mean more money and more fees. That's why I own it— it is a rising interest rate play, not a falling interest rate play.

Q: What do you think about Baidu (BIDU)?

A: Stay away from all China trades right now, it’s uninvestable. Not only do I not know what the Chinese are going to do next—they seem to be attacking a new industry every week—but the Chinese don’t even seem to know. This is all new to them; they had been embracing the capitalist model for the last 40 years and they now seem to be backtracking. There are better fish to fry, like Morgan Stanley (MS) and JP Morgan (JPM).

Q: Don’t you have a bear put spread on Baidu (BIDU)?

A: We did have a bear put spread on Baidu, but that's only a very short term, front month trade. It does look like it’s going to make money; but keep in mind those are high-risk trades.

Q: Could Natural Gas (UNG) trigger an economic crisis?

A: Not really. In the US, natgas is only a portion of our total energy needs, about 34%, and that’s mostly in the Midwest and California. The US has something like a 200-year supply with fracking. Plus, we’re on a price spike here—we’ve gone from $2 to $20/btu in Europe, entirely manipulated by Russia trying to get more money on their exports and more political control over Europe. So, it’s a short-term deal, and you can bet a lot of pros are out there shorting natgas like crazy right here. The real issue here is that no one wants to invest in carbon-based energy anymore and that is creating bottlenecks in the energy supply chain.

Q: How long will it take to provide EV infrastructure to mass gas station availability?

A: The EV infrastructure has in fact been in progress for 20 years, if you count the first generation of EV in the late 90s, which bombed. Tesla has been building power stations in the US for 10 years. They have 10,000 chargers now in 1,800 stations and their goal is 20,000 charging stations. In fact, most people already have the infrastructure for EV charging—you just charge them at home overnight, like I do. The only time I ever need a charge is when I go to Lake Tahoe. For gasoline engines, on the other hand, it took 20 years to build infrastructure from 1900 to 1920 to replace horses. Believe it or not, gasoline cars were the great environmental advance of the day, because it meant you could get rid of all the horses. New York City used to have 150,000 horses, and the city was constantly struggling through streets of two-foot-deep manure piles. So that was the big improvement. It only took 100 years to take the next step.

Q: The latest commodity with supply constraints I hear about is cotton. Is this all just a temporary thing and can we expect supply capacity to be back to normal next year? Is this just the failing of a just-in-time model that simply doesn’t work in the age of deglobalization?

A: We are losing possibly one third of our current economic growth due to part shortages, labor shortages, supply chain problems—those all go away next year, and that one third of economic growth just gets postponed into 2022 which means that the economic recovery is extended over a longer period of time, and so is the bull market in stocks, how about that! That’s why I’m loading the boat right here. It’s the first time I've been 100% invested since May.

Q: What do you think about the airlines here?

A: High risk, but high return play for the next year. Delta (DAL) is a play on business travel recovery. Alaska Airlines (ALK) and Southwest(LUV) are a play on a vacation travel return flying return, which has already started—we’re back to pre-pandemic TSA clearances at airports.

Q: Is Facebook (FB) a buy now?

A: No, I want to wait for the dust to settle before I go back in. I think it does recover and go to new highs eventually but will go to lower lows first. Regulation is certainly coming but we don’t know what.

Q: When will the chip shortage end?

A: Two years. My prediction is much longer than anybody else's because people are designing chips into new products like crazy. All predictions for the chip shortage to end in only a year don’t take that into account.

Q: When do we go into the (ROM) ProShares Ultra Technology long play?

A: When interest rates peak out sometime early next year. It’s probably a great entry point for tech; until then they go nowhere.

Q: Does the appetite for financials extend to Canada and their banks with higher dividends?

A: Yes, US and Canadian interest rates tend to move fairly closely so that rising rates here should be just as good for banks in Canada, and you might even be able to get them cheaper.

Q: Do you suggest we buy Altcoin?

A: No, not unless you're a Bitcoin professional like a miner, who can differentiate between all the different Altcoins. You can buy up to 100 different Altcoins on the main exchanges like Coinbase (COIN). In the crypto business, there is safety and size; that means Bitcoin ($BTCUSD) and Ethereum (ETHE), which between them account for about three quarters of all the crypto ever issued. A Lot of the smaller ones have a risk of going to zero overnight, and that has already happened many times. So go with the size—they’re less volatile but they’ll still go up in a rising market. And you should subscribe to our bitcoin letter just to get the details on how that market works.

Q: Target for Bitcoin by Christmas?

A: My conservative target is $66,000, but if we really go nuts, we could go as high as $100,000. That’s the “laser eyes” target for a lot of the early investors.

Q: Suggestions for a Crypto ETF?

A: It’s not out yet but will be shortly. I think that Crypto will run like crazy in anticipation of the Bitcoin ETF that we don’t have yet.

Q: Should I buy Moderna (MRNA) on this dip at 320 down from 400, or is this a COVID revenue flash in the pan that won’t come back?

A: It’ll come back because they’re taking their COVID technology and applying it to all other human diseases including cancer, which is why we got in this thing two years ago. But we may have to find a lower low first. So I would wait on all the drug/biotech plays which right now are getting hammered with the demise of the delta virus.

Q: What’s your favorite ETF right now?

A: Probably the (TBT) Double Short Treasury ETF. I’m looking for it to go up another 30% from here to 24 or 25 by sometime next year.

Q: EVs have been hot this year; Lordstown Motors is down to only $5 from $27 and just got downgraded by an analyst to $2. Should I buy, or is this a dangerous strategy?

A: I would say highly dangerous. This company has been signaling that it’s on its way to bankruptcy essentially all year, so don’t confuse “gone down a lot” with being “cheap” because that’s how you buy stuff on the way to zero.

Q: What about Anthony Scaramucci’s ETF?

A: We will have Anthony Scaramucci as a guest in our December summit. And the ETF is a basket of stocks as diverse as MicroStrategy (MSTR), Blok (BLOK), Visa (V), and Nvidia (NVDA), so you will only get a fraction of the Bitcoin volatility. That means if Bitcoin goes up 100% you might get a 40% or 50% move in the actual ETF.

Q: Do you have a Bitcoin book coming out soon?

A: I do, it should be out by the end of this month. That’s The Mad Hedge Guide to Trading Bitcoin, and it will have all the research I’ve accumulated on trading Bitcoin in the past year.

Q: Why have you only issued one trade alert in Bitcoin?

A: You don’t get a lot of entry points for Bitcoin. You buy the periodic bottoms and then you run them. Dollar cost averaging is very useful here because there are no traditional valuation measures to use, like price earnings multiples or price to book. When it comes time to sell, we'll let you know, but there aren’t a lot of Bitcoin plays outside the Bitcoin exchanges.

Q: Thoughts on silver (SLV)?

A: It’s horribly out of favor now and will continue to be so as long as Bitcoin gets the spotlight. Also, there’s a China problem with the precious metals.

Q: There are 8 or 10 good public Bitcoin and Ethereum ETFs in Canada.

A: That’s true, if you’re allowed to trade in Canada.

Q: Can the US ban Bitcoin like China did?

A: No, if they did, it would just move offshore to the Cayman Islands or some other place outside the world of regulation.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log on to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Sightseeing in Laos in 1975

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/john-thomas-1975-laos.png620450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-08 10:02:572021-10-08 12:27:24October 6 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the September 22 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: When’s the United States US Treasury bond fund (TLT) going to go down?

A: When J. Powell tapers, which will be either today or in 6 weeks. That's the time frame we’re looking at now, and people are positioning now for the taper—that's why financials are taking off like a rocket. Buy those financials and don't expect too much from your tech stocks for the next few months.

Q: What do you think of adding corporate or municipal bonds to my portfolio?

A: Don’t do that on pain of death please; you will lose money. Corporate bonds will get slaughtered the second interest rates turn because they have the most exposure from a credit point of view to any downgrades resulting from rising interest rates. Better to keep your money in cash than buy bonds here. It was a great idea 10 years ago, but a terrible idea today. Just buy cash or buy extremely deep-in-the-money LEAPS which will get you a 10-20% per year return.

Q: What are the chances that the government defaults?

A: Zero, because corporate profits this year will increase from $2 trillion to $10 trillion, spinning off massive tax revenues for the government. The deficit will come down substantially in the future as a result. Keep expecting upwards surprises in profits and taxable revenues. That may be why the (TLT) is staying so high.

Q: I need a customized LEAPS on a stock.

A: We do those for our concierge customers. If you’re interested, then email Filomena at customer support at support@madhedgefundtrader.com.

Q: What brand of shot did you get?

A: Pfizer (PFE).

Q: The Government is showing no sign of balancing a budget and the hole will only get deeper; what are your thoughts?

A: I agree, and that’s why I'm short the (TLT). All we need is a taper to really get some juice under that trade; we really don’t need that much. Ten-year US Treasury yields are now around 1.30% and we only need the yield to get up to about 1.70% for us to make a maximum profit on our positions. One taper hint and it could get us up to those levels.

Q: Why is Visa (V) dropping so much?

A: Fear of being replaced by Bitcoin. This is the big thing dragging all three credit card companies down, including American Express (AXP) and master Card (MA). That's why I have not added a Visa position among my financials in this go around.

Q: How can the Fed unwind their balance sheet and normalize interest rates to a historical average of 4-5%?

A: Quite easily: quit buying bonds. They’re still buying $120 billion/month worth. Technology has accelerated with the pandemic and we all know this is highly deflationary. I expect the next peak in interest rates to be only 3% or 3.5%, not the 6% we saw in the last peak in interest rates in the 2000s. So yeah, bonds are going to go down but not back to 2000’s level.

Q: Thoughts on the Johnson & Johnson (JNJ) shot?

A: No thank you. If you get to choose, Moderna (MRNA) is now producing the best immunity data on a year-to-date basis if you’re starting out from scratch. Some people are mixing, they start out with Pfizer and then get Moderna. They get a worse reaction because the Moderna initial reaction shot sees the Pfizer vaccine as a new virus, so you may get a small flu as a result of that.

Q: What is the put spread you’re recommending on the TLT?

A: The May 2022 $150-$155 vertical put spread. That is the sweet spot now on the short side on (TLT) LEAPS. You should earn a 115% profit in eight months on this trade if interest rates remain unchanged or fall.

Q: Do you expect the ProShares Ultra Short 20 year+ Treasury ETF (TBT) to make it to $20 this year?

A: Yes, I do; $16 to $20 isn’t that much of a move. Remember, the (TBT) is a two times short ETF.

Q: Are you recommending bank stocks?

A: Yes, Morgan Stanley (MS) and JP Morgan (JPM) are two of the best. They will lead the yearend rally starting from here.

Q: When do you expect the semiconductor shortage to end?

A: End of next year, or maybe even 2023, because what all the analysts keep underestimating is that the end of shortages is based on companies getting the chips they want today. The actual issue is that companies are designing billions of chips into their products at an exponential rate, and what they’ll need in a year from now is far higher than most people realize. The semiconductor shortage is much more structural than people realize—that's my theory. They don’t throw up a $2 billion fab overnight. So, this will keep going on for a while and be a drag on economic growth.

Q: Are you sure we won’t see $100 oil (USO)?

A: With oil, you're never sure about anything, although I highly doubt it. We’d have to have monster economic growth in China to get oil up to $100 a barrel. Right now, China is going the other way.

Q: What’s your view on the debt ceiling? Will it give us a good buying opportunity?

A: Probably not, our good buying opportunity was yesterday or Monday. These debt crises are always one minute before midnight solutions. They always get solved. Never underestimate the ability of Congressmen to spend money in their own district. So, I don’t think that would create a stock market crash like it might have done 20 years ago.

Q: What about Freeport McMoRan (FCX)?

A: It’s taking a dip here because of a possible real estate crash in China, and of course China is the world’s largest buyer of copper for apartment construction. I’m kind of taking a break here on Freeport McMoRan and US Steel (X) until we learn a little more about the China situation. They did move to start a bailout today. Let’s see if that continues.

Q: When will the airlines come back?

A: They’ll come back when business travel returns, which I think could be next year. If you eliminate the virus completely, these things double easily. That's the bet you’re making. Let’s see if the covid boosters work, the childhood shots work, and then you can take another look at Delta (DAL) and Alaska (ALK).

Q: If Bitcoin gains mass adoption, does that put banks out of business just like electric vehicles are making oil obsolete?

A: No, not if the banks go into the Bitcoin business. And the banks actually have the cash, resources, and infrastructure to take over the Bitcoin area once the technology matures. And the corollary to that is that the oil industry is that the majors have the infrastructure, the manpower, and the capital to take over the alternative energy business if they choose to do so and oil goes to zero, which it eventually will. The proof of that is the largest investor in all the Silicon Valley energy startups are Saudi Arabian venture capital funds. They’re huge investors in solar here. If Saudi Arabia has a lot of oil, they have even more solar. Believe me, I’ve been there.

Q: Will a lack of inventory and rising interest rates end the bidding wars on houses soon?

A: Only if you consider 10 years soon. That is how long it will take for the sizes of different generations to come into balance, the Millennials (85 million) versus the Gen Xers (45 million). That’s when the housing bubble will end, but that won’t be for another decade. We still have a structural shortage of new home construction (about 5 million units a year) because all the home builders who went bust in the financial crisis in 2008/2009 and never came back—all of that new construction is still missing. And the surviving ones haven’t increased production to meet that shortfall because they want to manage their risk. Eventually, they will and that probably will be the next top, but that’s really 2030 type business.

Q: What about Federal Express (FDX)?

A: Labor shortages. It's hitting (UPS), (FDX), the Post Office, and DHL too—all the couriers.

Q: When do you think gold (GLD) and silver (SLV) rise back to 2,000?

A: I am avoiding gold and silver as long as Bitcoin has buyers. The action in Bitcoin is 10x the movement you get in gold and that’s attracted all the speculative capital in the market, draining all interest from gold, which hit a new six-month low just last week.

Q: What’s your buy target for Apple (AAPL)?

A: I would say if you can get it at $135, that would be a gift. We did get close to $140 at the lows this week; that’s when you start nibbling, and then you double up again at $135. I doubt Apple is going down more than 10% in this cycle. There are too many people still trying to get into it. And they’re still the largest buyer of stock in the world. They only buy one stock, their own.

Q: I never got any IPath Series B S&P 500 VIX Short Term Futures ETN (VXX) alerts.

A: That's because we never sent any out. (VIX) has become an incredibly difficult game to play, accumulating positions for months and then trying to get out on a one-day spike that lasts a few minutes. The insiders have too much of a house advantage here, who only play from the short side. There are too many better fish to fry.

Q: What about the Apple electric vehicle?

A: I’ll believe it when I see it; I've been hearing about this for something like seven years. My guess is that Apple is more likely to supply consoles and parts to other EV makers and help them get into the game with software and so on. I think that will be Apple's role in all of this.

Q: How much has China Evergrande Group stock fallen?

A: It’s a really illiquid stock in China so we never got involved in it. I think it’s down more than half. Even the professional short-sellers like Jim Chanos and Kyle Bass, have been targeting that stock for 10 years are now screaming they’re vindicated. Of course, they lost fortunes in the meantime. So, I'll pass on that one.

Q: What about stop losses on LEAPS trades?

A: I don’t really run LEAPS portfolios or issue stop losses. The idea is to run these into expiration, and we’ve never had one expire out of the money, although I may break that record if TLT doesn’t turn around in the next three months.

Q: How would autonomous trucking impact rail transportation?

A: They’re two totally different things. Trucking companies like Yellow Corporation (YELL) carry smaller cargo for local deliveries or small long-distance deliveries. 7Some 70% of all railroad traffic is coal going to China, and the rest is bulk commodities like wood chips, iron ore, etc. Trucks don’t carry any of that, so they’re totally separate businesses. But, if we went totally autonomous on trucking, it would make all the main trucker companies massively profitable, as they get rid of their drivers. Right now, every trucking company in the US has a driver shortage.

Q: United Airlines (UAL) pilots are now ordered to get vaccinated.

A: I think within months to hold a job anywhere in the US, you will have to get vaccinated. They do not want you in the office without a vaccination. Jobs are not worth risking lives, and we hit 2,000 deaths again yesterday. The corporations are taking the lead, not the government. The exception will be the politically motivated companies, like the My Pillow Guy; I doubt they'll ever require vaccinations at My Pillow. And there are a few other companies such as Hobby Lobby that are also anti-vaxers. But all public transport companies, hospitals, etc., are going to say get vaccinated or get out—it’s very simple.

Q: Should I buy Berkshire (BRKB) here?

A: Yes, it’s a great entry point, even if you can't get my price. Go higher in the strikes or go farther out in maturity.

Q: Is copper metal (CPER) a buy here?

A: Probably long term, but short term will be subject to the whims of the Chinese real estate crisis if there is one.

Q: Won’t Natural Gas (UNG) outperform in the power grid since all EVs must be charged?

A: Not if the grid is 100% electric. Natural gas still has carbon in it, although only half as much as oil or gasoline. I think even natural gas eventually gets phased out because you can expect solar panels to improve by 80% over the next ten years. At that point, any other energy source won’t be able to compete—oil, natural gas, you name it. And that is why you don’t see any long-term money going into carbon energy sources.

Q: Iron ore has just gone from $200 to $100, why are you bullish?

A: Yes, Because it has just gone from $200 to $100. Eventually, China recovers, despite a short-term financial and housing crisis. Buy low, sell high—that’s my revolutionary new strategy.

Q: What are your thoughts on Bitcoin vs Ethereum?

A: I think Ethereum will outperform Bitcoin because it has a more modern technology. It’s only six years old, vs 12 years for Bitcoin. It’s also more efficient, using less energy in its production. In fact, we did get a double in Ethereum in August as opposed to only a 50% move in Bitcoin.

Q: Do you have any concerns on holding the financials through earnings in October?

A: No, I think the results will be fantastic, and I want to be long going into those.

Q: What does the current situation with China mean for Alibaba (BABA)?

A: Keep your stocks, you’ve already taken the hit—down 53%. The next surprise is that China quits beating up on capitalism and these things will all recover bigtime. However, any options you may have could expire before that happens. So, keep the stocks, get rid of the options, salvage whatever time value you can, and then wait for China to start doing the right thing.

Q: What are the best solar stocks?

A: First Solar (FSLR) and SunPower (SPWR), which have both done great.

Q: If bonds are a no-no, and governments are getting more indebted than ever, who will buy them?

A: Governments. The only buyers of bonds now are non-economic buyers. Those would be governments, central banks, and banks who are required by law to own certain amounts of bonds to meet regulatory capital requirements. No individual in their right mind is buying any bonds here at all, nor is any financial advisor recommending them.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/tootsie.png331522Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-24 09:02:442021-09-24 11:19:08September 22 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the August 25 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from The Atlantis Casino Hotel in Reno, NV.

Q: How does a 2X ProShares Ultra Technology ETF (ROM) February 2022 vertical bull call spread on the ROM look? Would you do $110-$115 or $115-$120?

A: I would do nothing here at $112.50 because we’ve just gone up 10 points in a week. I’d wait for some kind of pullback, even just $5 or $10 points, and then I would do the $110-$115. I’m leaning towards more conservative LEAPS these days—bets that the market goes sideways to up small rather than going ballistic, which it has done for the last 18 months. Think at-the-money strikes, not deep out-of-the-money on your LEAPS from here on for the rest of this economic cycle. The potential profits are still enormous. The only problem with (ROM) is that the longest maturities on the options are only six months.

Q: How do you recommend entering your long-term portfolio?

A: I would use the one-third rule: you put on ⅓ now, ⅓ higher or lower later on, and ⅓ higher or lower again. That way you get a good average price. Long term, everything goes up until we hit the next recession, which is probably several years off.

Q: I keep reading that the Delta variant is a market risk, but I don’t think that investors will look through this. Is Delta already priced into the shares?

A: Yes, what is not priced into the shares is the end of Delta, the end of the pandemic—and that will lead to my “everything” rally that I’ve been talking about for a month now. And we have already seen the beginning of that, especially with the price action this week. So yes, Delta in: dead market; Delta out: roaring market.

Q: Do you think there will eventually be a rotation into emerging markets (EEM), or has the virus battered these markets too much to even consider it?

A: Sometime in our future—not yet—the emerging markets will be our core holding. And the trigger for that will be the collapse of the dollar, which is hitting an interim high right now. When the greenback rolls over and dies, you can expect emerging markets, especially China, to take off like a rocket. That’s going to be our next big trade. I don't know if it will be this year or next year but it’s coming, so start doing your emerging market research now, and keep reading my newsletter.

Q: Is the coming tax hike a problem for the stock market?

A: No, I don’t think so. First off, I don’t think they’re going to do a tax bill this year; they don’t want anything to interfere with the 2022 election, so it may be next year’s business. Also, any new taxes are going to be overwhelmingly focused on billionaires, carried interest, offshoring, and large corporations. The middle class, people who make less than $400,000 a year, will not see any tax hike at all, possibly even getting some tax cuts via restored SALT deductions. So, I don't really see it affecting the stock market at all.

Q: What do you think about Chinese stocks (FXI)?

A: Long-term they’re okay, short term possibly more downside. Interestingly, the bigger risk may not be China itself and how the government is beating up its own tech companies, but the SEC. It has indicated they don’t really like these offshore vehicles that have been listed on the New York Stock Exchange, and they may move to ban them. I’m not rushing into China right now, only because there are just so many better opportunities in the US stock market for the time being. I may go back in the future—it’s a case where I’d rather buy them on the way up than trying to catch a falling knife on China right now.

Q: Do you expect any market impact from the Jackson Hole meeting?

A: Yes, whatever J Powell says, even if he says nothing, will have a market impact. And it will have a bigger impact on the bond market than it will on the stock market, which is down a full point this morning. So yes, but not yet. I imagine we’ll hear something very soon.

Q: September and October tend to be volatile; do you see us having a 5% or 10% pullback in those months?

A: I don’t see any more than 5%, with the hyper liquidity that we have in the system now. There just aren’t any events out there that could trigger a pullback of 10%—no geopolitical events, and the economy will be getting stronger, not worse. So yes, an “everything rally” doesn’t give you many long side entry points, so I just don’t see 10% happening.

Q: What about a Walt Disney (DIS) January 2022 $180-$220 LEAPS?

A: I would do the $180-$200. I think you can afford to be tighter on your spread there, take some more risk because I think it’s just going to go nuts to the upside once we get a drop in COVID cases. By the way, Disney parks are only operating at 70% capacity, so if you go back up to 100% that's a near 50% increase in profits for the company. And it’s not just Disney, but Netflix (NFLX), Amazon (AMZN), and everybody else that’s about to have the greatest number of blockbuster movies released of all time. They’re holding back their big-ticket movies for the end of the pandemic when people can go back into theaters. We’ll start seeing those movies come out in the last quarter of this year, and I’m particularly looking forward to the next James Bond movie, a man after my own heart.

Q: Are EV car charging companies like ChargePoint Holdings (CHPT) going to do as well as the car companies?

A: No. They’re low margin business, so it’s not a business model for me. I like high-profit margins, huge barriers to entry, and very wide moats, which pretty much characterizes everything I own. The big profits in EVs are going to be in the cars themselves. Charging the cars is a very capital-intensive, highly regulated, and low-margin business.

Q: Would a Fed taper cause a 10% pullback?

A: Absolutely not; in fact, I think a taper would make the market go up because Jay Powell has been talking it into the market all year. And that’s his goal, is to minimize the impact of a taper so when they finally do it, they say ho-hum and “okay you can take that risk out of the market.” That’s the way these things work.

Q: What is your yearend target for United States Treasury Bond Fund (TLT)?

A: $132. Call it bold, but I'm all about bold. I think the first stop will be at $144, then $138, then bombs away!

Q: What will it take for (TLT) to dip below $130?

A: Another year of hot economic growth, which Congress seems hell-bent on delivering us.

Q: What are your ProShares Ultra Short 20+ Year Treasury ETF (TBT) targets?

A: When we were at 1.76% on the 10-year bond, the (TBT) made it all the way back to 22 ½. Next year we go higher, probably to $25, maybe even $30.

Q: What’s your 10-year view on the (TBT)?

A: $200. That’s when you get interest rates back to 10% in 10 years on the 10-year bond. So yes, that’s a great long-term play.

Q: How long can we hold (TBT)?

A: As long as you want. Ten years would be a good time frame if you want to catch that $17 to $200 move. The (TBT) is an ETF, not an option, therefore it doesn’t expire.

Q: Are you working on an electrification stock list?

A: I am not, because it’s such a fragmented sector. It’s tough to really nail down specific stocks. I think it’s safe to say that the electric power grid is going to change beyond all recognition, but they won’t necessarily be in high margin companies, and I tend to prefer high-profit-margin, large-moat companies which nobody else can get into, like Apple (AAPL) or Google (GOOG).

Q: What about gas pipelines with high yields?

A: They have a high yield for a reason; because they’re very high risk. If you're going to a carbon-free economy, you don’t necessarily want to own pipelines whose main job is moving carbon; it’s another buggy whip-type industry I would avoid. I’ve seen people get wiped out by these things more times than I could count. If you remember Master Limited Partnerships, quite a few of them went bankrupt last year with the oil crash, so I would avoid that area. These tend to be very highly leveraged and poorly managed instruments.

Q: Best play on silver (SLV)?

A: Wheaton Precious Metals (WPM) is the highest leveraged silver play out there, and a great LEAPS candidate. Go out 2 years and triple your money.

Q: Geopolitical oil (USO) risks?

A: No, nobody cares about oil anymore—that’s why we’re giving up on Afghanistan. China is buying 80% of the Persian Gulf oil right now. We don’t really need it at all, so why have our military over there to protect China’s oil supply?

Q: What about Freeport McMoRan (FCX)?

A: I absolutely love it. Any big economic recovery can’t happen without copper, and you have a huge tailwind there from electric cars which need 200 pounds of copper each, as opposed to 20 pounds in conventional cars.

Q: I see AMC Entertainment Holdings (AMC) is up 20% today; should everyone be chasing this stock?

A: No, absolutely not. (AMC) and all the meme stocks aren’t investments, they’re gambling, and there are better ways to gamble.

Q: Should I buy the lumber dip?

A: Yes. I think the slowdown on housing is temporary because it will take 10 years for supply and demand in the housing market to come back into balance because of all the millennials entering the housing market for the first time. So, that would be a yes on lumber and all the other commodities out there that go into housing like copper, steel, and aluminum.

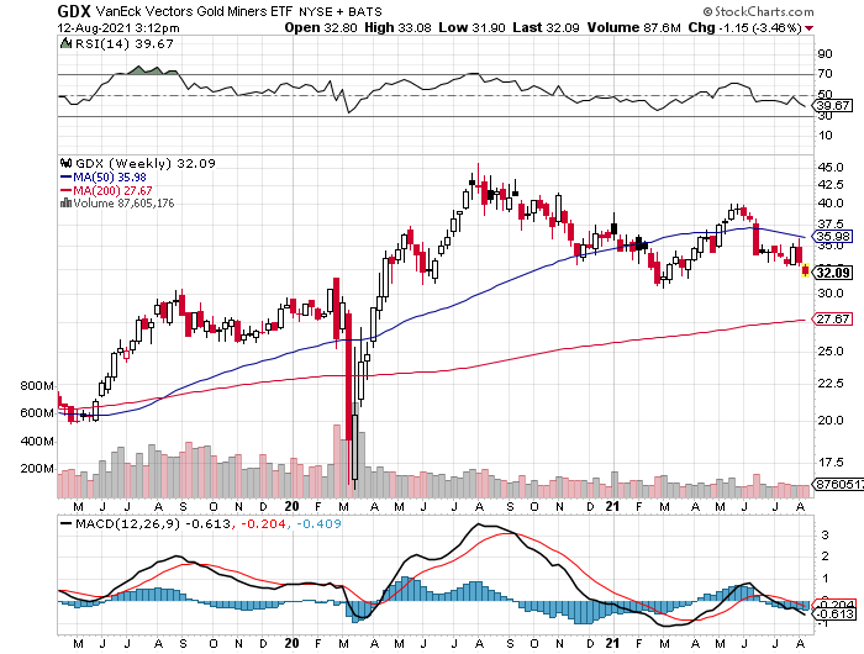

Q: Should I put money into Canadian Junior Gold Miners (GDX)?

A: No, I would rather go out and take a long nap first. These are just so high risk, and they often go bankrupt. The liquidity is terrible, and the dealing spreads are wide. I would stick with the bigger precious metal plays like Newmont Mining (NEM), Barrick Gold (GOLD), and Wheaton Precious Metals (WPM).

Q: Is Boeing (BA) a buy here?

A: Yes, we’re back at the bottom end of the trading range for the stock. It’s just a matter of time before they get things right, and the 737 Max orders are rolling in like crazy now that there’s an airplane shortage.

Q: What do you think about Robinhood (HOOD)?

A: I like it quite a lot; I got flushed out of my long position on Friday with a 10% down move. Of course, 90% of my stop losses end up expiring at their maximum profit points, but I have to do it to keep the volatility of the portfolio down. So yes, I’ll try to buy it again on the next dip. The trouble is it’s kind of a quasi-meme stock in its own right, hence the volatility; so I would say on the next 10% down day, you go into Robinhood, and I probably will too.

Q: How are the wildfires around Tahoe?

A: They’re terrible and there are three of them. I did a hike two days ago there, and out of a parking lot with 100 spaces, I was the only one there. It’s the only time I’d ever seen Tahoe deserted in August. With visibility of 500 yards, it's just terrible. Fortunately, I was able to hike without coughing my guts out—it’s not so thick that you can’t breathe.

Q: What do you think of US Steel (X)?

A: I like it, I think the whole industrial commodity complex rallies like crazy going into the end of the year.

Q: As a new member, where is the best place to start? It’s just kind of like drinking from a fire hose.

A: Wait for the trade alerts; they only happen at sweet spots and you may have to wait a few days or weeks to get one since we only like to enter them at good points. That’s the best place to enter new positions for the first time. In the meantime, keep reading all the research, because when these trade alerts do come out, they’re not surprises because I’m pumping out research on them every day, across multiple fronts. Be patient— we are running a 93% success rate, but only because we take our time on entering good trades. The services that guarantee a trade alert every day lose money hand over fist.

Q: If they do delist Chinese stocks, will US investors be left holding the bag?

A: Yes, and that will be the only reason they don’t delist them, that they don’t want to wipe out all current US investors.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (whichever applies to you), then select WEBINARS and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-wine-1.png812562Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-27 10:02:412021-08-27 11:03:48August 25 Biweekly Strategy Webinar Q&A

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on February 2, 2021. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing and you don’t want to remain glued to a screen all day, these are the investments you can make. Then don’t touch them until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red on the spreadsheet.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, the click on the “Long Term Portfolio” button, then “Download.”

Changes

Biotech

Pfizer (PFE) has nearly doubled in six months, while Crisper Therapeutics (CRSP) has almost halved. Since the pandemic, which Pfizer made fortunes on, is peaking and we are still at the dawn of the CRISPR gene editing revolution, the natural switch here is to take profits in (PFE) and double up on (CRSP).

Technology

I am maintaining my 20% in technology which are all close to all-time highs. I believe that Apple (AAPL), (Amazon (AMZN), Google (GOOGL), and Square (SQ) have a double or more over the next three years, so I am keeping all of them.

Banks

I am also keeping my weighting in banks at 20%. Interest rates are imminently going to rise, with a Fed taper just over the horizon, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, keep Morgan Stanley (MS), Goldman Sachs (GS), JP Morgan (JPM), and Bank of America, which will profit enormously from a continuing bull market in stocks. They are also a key part of my” barbell” portfolio.

International

China has been a disaster this year, with Alibaba (BABA) dropping by half, while emerging markets (EEM) have gone nowhere. I am keeping my positions because it makes no sense to sell down here. There is a limit to how much the Middle Kingdom will destroy its technology crown jewels. Emerging markets are a call option on a global synchronized recovery which will take place next year.

Bonds

Along the same vein, I am keeping 10% of my portfolio in a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis so go read Global Trading Dispatch. Eventually, massive over-issuance of bonds by the US government will destroy this entire sector.

Foreign Exchange

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). Eventually, the US dollar will become toast and could be your next decade-long trade. The Aussie will be the best performing currency against the US dollar.

Australia will be a leveraged beneficiary of the synchronized global economic recovery through strong commodity prices which have already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

Precious Metals

As for precious metals, I’m keeping my 0% holding in gold (GLD). From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

I am keeping a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles. The arithmetic is simple. EV production will rocket from 700,000 in 2020 to 25 million in 2030 and each one needs two ounces of silver.

Energy

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

The Economy

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade after this year’s superheated 7% performance.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 700% or more from 35,000 to 240,000 in the coming decade. The American coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again. If I forget, please remind me.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-19 10:02:182021-08-19 12:09:09My Newly Updated Long-Term Portfolio

Below please find subscribers’ Q&A for the August 11Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA.

Q: If we see a correction in stocks, what would you do?

A: Buy more stocks (SPY). All of our positions expire next week, and we go 100% into cash. I’m looking for just a 5% correction and then I’m just going to go piling in 100% invested with a barbell portfolio since everything is working now and some of the best tech stocks like Amazon have already had 10% corrections.

Q: Time for LEAPS again on Amazon (AMZN)?

A: Yes, but let Amazon have more time to bottom out. It may just be a “time” correction where it goes sideways for a month or two. The company is still growing at an incredible rate.

Q: What about FedEx (FDX) and Walt Disney (DIS) LEAPS?

A: Those LEAPS I would do, right here, right now. We’ve had our corrections already in those sectors and they’re ready to take off. It’s just a matter of time before these sectors come back into favor. These are both delta peaking plays.

Q: It seems that the US government is taking the stance that they can tax their way out of the fiscal hole; is this true?

A: No, they don’t need to tax their way out of the fiscal hole; deflation will wipe out all US government debt on a 30-year view, and this is what’s happened to not only all the government debt in US history but all government debts all over the world starting with France in the 1600s. By the time the government has to pay back its 30-year bonds, the purchasing power of that dollar will have fallen by 80% or 90%, meaning that essentially the bonds get deflated away to nothing. And this is why we have governments, so they can borrow that money now, spend it now to rescue the economy, and then they never have to pay it back in real dollars. This is why governments borrow. The investors who really have to pick up the bill for this are bond owners, who see the purchasing power of the bonds decline by 2%-3% a year.

Q: When do you see a correction, and what would you do?

A: It’s either going to be in the next couple of weeks or never. If we get one, I would load the boat again with more long positions. Of the five positions out of 100 I’ve lost money this year, four have been short positions, so you can see why we’re really trying to limit the short positions here.

Q: Visa (V) is going ex-dividend tomorrow—is there a risk of early assignment?

A: There is, but if you get an early assignment, just say thank you very much, Mr. Market, call your broker to tell them to exercise your long call position to cover your call short position, and you will get the maximum profit several days earlier than expiration. This happens sometimes as hedge funds try to get the quarterly dividend on the cheap, but you have to act fast, otherwise, you’ll end up with a short position in Visa on your hands, and most likely a margin call. Brokers are not allowed to automatically exercise longs to meet calls anymore. You have to call them and order them to exercise that long. So, pay attention going into quarterly option expirations.

Q: I don’t trust your COVID information any more than I trust the government line.

A: All of my Covid data comes from Johns Hopkins University and is interdependently collated from every country in the United States. If you have any complaints you can go to them. All I can say is there are 620,000 bodies in the country that died of something. Oh, and we had the lowest population growth last month in 50 years. I’ve had family members die from it so I believe that.

Q: If the Republicans win in 2022 and 2024, will the bull market continue?

A: Absolutely not. We get a new recession and another bear market. Everything that’s going well now reverses, the entire environmental infrastructure strategy goes down the toilet, and Covid makes a huge recovery. I would go with what’s working, and 6.5% economic growth now and a market going up 30% a year totally works for me. Of course, I would make another fortune on the short side.

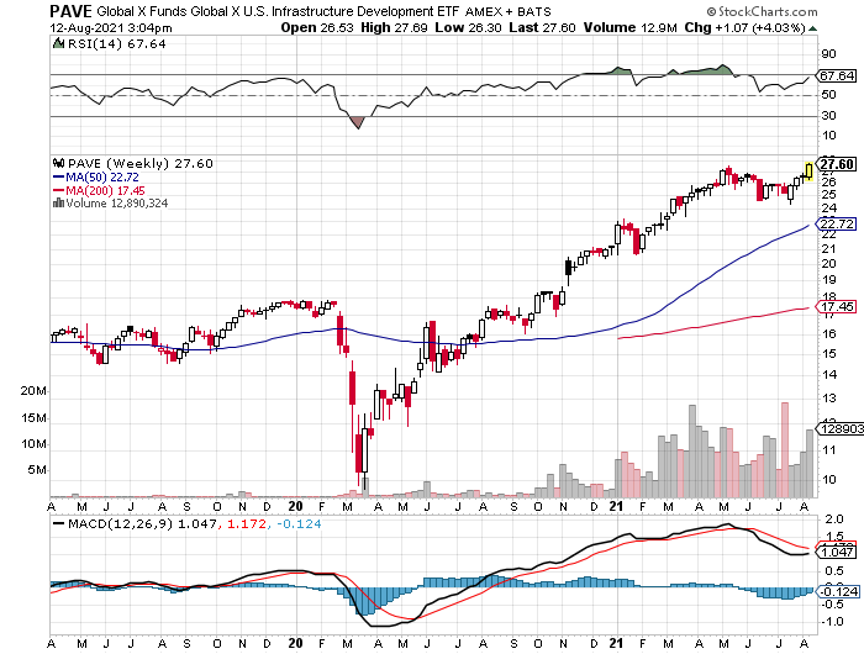

Q: How should you play infrastructure?

A: There is an infrastructure ETF called the Global X Funds Infrastructure ETF (PAVE) that has already had a big move, up 176% in 17 months. Other than that you can just play your basic commodity stocks like US Steel (X), Nucor (NUE), and Freeport McMoRan (FCX).

Q: How long will the hot housing market continue?

A: Ten more years. That's how long it will take to digest the current 85 million strong millennial generation who are now buying first-time homes or upgrading what they’ve got. And remember, we’re still operating with half of the new home construction capacity that we had 15 years ago before the last financial crisis.

Q: What's your prognosis for semiconductors?

A: They just had a super-heated spike; I expect them to take a break. That's why I took profits on Advanced Micro Devices (AMD). We’ll find a new bottom, and then I want to buy back into it. It’s taking a break with the rest of technology right now, which is perfectly normal.

Q: Would you take this dip to add to mRNA and BioNTech?

A: I would say yes. This is an industry that’s on the eve of a biotech revolution—the cure of all human diseases. And these two companies with their mRNA technologies are in the best place to take advantage of that.

Q: Will there be a big spike down in August?

A: It looks like it’s not happening. Like I said, if it doesn’t happen in the next few weeks, it’s not going to happen. Excess liquidity is just driving all investment decisions. If it doesn’t go down now, what’s the reason for it to go down in October? I just see no negatives at all on the horizon except for another out-of-the-blue variant like a Lambda or an Epsilon variant.

Q: Does slow population growth include illegal immigration?

A: It does, immigration both legal and illegal has been constant for decades and decades, it’s about a million people a year. But Americans are not reproducing like they used to, the birth rate hit a 50-year low last year because women did not want to go to the hospitals which were full of COVID patients. A lower population growth over the long term is very bad for economic growth. That is why Japan has essentially been in a nonstop recession for the last 32 years, because of their baby bust.

Q: Do you have political debt ceiling concerns?

A: No, these are always last-minute before midnight deals. I don't see this being any different, never underestimate the ability of Congress to spend more money, no matter who is in power.

Q: What do you think of oil in the short run?

A: Short term it may go sideways, we may even have a rally to new highs, but the long-term trade for oil is that it’s going out of business. EVs, mean you lose 50% of demand for oil in the next 10 years, and they will start discounting that now in the price of oil.

Q: Why is silver down so much?

A: It’s being dragged down by Gold (GLD), and silver (SLV) always moves twice as fast as gold.

Q: How are muni bonds going forward?

A: I don’t see them going much further. They had a massive rally, discounting an increase in taxes which hasn’t happened. So even if they do raise taxes which may be next year’s business, that is fully discounted in the Muni market already.

Q: What am I missing? You’ve been saying for months not to get involved with Bitcoin but then I heard you say you bought LEAPS.

A: No, I didn’t buy the LEAPS. I tried to buy the LEAPS but missed them and it ran away and they ended up tripling in two weeks. It’s just not like buying a normal stock. Once these things turn, they just start going up every day for weeks with no pullbacks whatsoever. This is valuation-free security with no dividend, interest, or earnings. It’s driven by pure supply and demand.

Q: What do you think of the precious metal miners like the Van Eck Vectors Gold Miners ETF (GDX)?

A: Let the current meltdown burn out and then go into long term LEAPS.

Q: What’s the best way to buy silver?

A: The best way is doing 2-year LEAPS on Wheaton Precious Metals (WPM) at current levels.

Q: What do you think about Coinbase (COIN)?

A: It’s definitely a candidate, but you want to get it on a down day. Coinbase is in the “selling shovels to the gold miners” business which is always a fantastic business model and we here in California know all about it. It’s just a question of when and where to get involved. It’s been gyrating this week because of their new burden of doing the tax reporting on all crypto buyers among their customers. That will definitely be a drag on the business.

Q: What's your short-term view on the big commodity plays like Freeport McMoRan (FCX), Alcoa Aluminum (AA), and US Steel (X)?

A: I would say they’re all going up. Maybe half the infrastructure bill has been discounted into the metals prices, but not all of it, therefore they have more to go to the upside.

Q: What are the best real estate buys?

A: There are none anywhere; maybe somewhere in eastern Europe, but still unlikely. It’s the best time ever now to rent. Buying here would be madness. And by the way, I predicted this property boom 10 years ago, if you go back in my research because 2021 was when the millennials would show up as massive buyers in the housing market, right when there was going to be a demographic shortage. That’s why I think the real estate boom goes on for another 10 years. But you won't see the gains that we’ve seen this year. You will maybe see 5% or 10% gains a year, definitely not 50% or 100% gains that we’ve just seen.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in here, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-wine.png538374Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-13 09:02:332021-08-13 10:17:50August 11 Biweekly Strategy Webinar Q&A

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.