Global Market Comments

November 16, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or RAIDING THE PIGGY BANK),

(SPY), ($INDU), (JPM), (CAT), (UNP), (UPS), (SLV), (TLT), (TSLA)

Global Market Comments

November 16, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or RAIDING THE PIGGY BANK),

(SPY), ($INDU), (JPM), (CAT), (UNP), (UPS), (SLV), (TLT), (TSLA)

I remember the last time that the market went up 10% in ten days.

In the fall of 1982, I was in the office of Carl Van Horn, the chief investment officer of JP Morgan Bank. I was interviewing him about the long-term prospects for the stock market with the Dow Average at 600 and gurus like Joe Granville predicting Dow 300 by yearend.

The odd thing about the interview was that he kept ducking out of the room for a minute at a time and then coming back in. I finally asked him what he was doing. He answered, “Oh, I had to go out and buy $100 million worth of stock.”

And that was back when $100 million actually bought you something!

Over the last two weeks, the Dow Average has tacked on a historic $4,000 points. For a few fleeting second, it actually touched 30,000. Cassandras everywhere are tearing their hair out.

The monster rally began a few days before the election and has continued unabated. In my view, this is the second leg of a 20-fold move that started in 2009 when the Dow was at 6,000 and will continue all the way up to 120,000 by 2029.

No wonder investors are so bullish! It seems that recently, quite a few have come over to my way of thinking.

And how could they not be so bovine-inclined?

The most contentious election in history over. The pandemic is about to end. In a year we’ll, all have our Covid-19 vaccinations, at least those who want them. I’m planning on getting all six.

The greatest burst of economic growth in history is about to be unleased. Consumption wasn’t destroyed, just deferred into 2021 and 2022, unless you’re in the cruise, airline, or restaurant business. The exponential profit growth unleashed by the pandemic isn’t even close to being discounted.

This hasn’t been just any old rally. Stocks left for dead years ago, the old-line industrials and cyclicals have sprung back to life. Union Pacific (UNP) has exploded. JP Morgan Chase (JNP) has gone off to the races. Caterpillar (CAT) is in orbit.

The great thing about these moves is that it is very early days. They could run for years. But where will the money come from to pay for these? How about raising the big tech piggy bank, which has been leading markets for years and is now wildly overvalued.

However, $4,000 points is a lot. So, we may get some back and fill and a sideways “time” correction before we attempt higher highs by yearend. The only thing that could upset this scenario is if Covid-19 cases explode, which they are now doing.

Where will the market care? Who knows, but like stock prices, US Corona cases have doubled in ten days to 160,000.

Covid-19 is cured! News that Pfizer (PFE) has discovered a Covid-19 vaccine that is 90% effective has sent stocks soaring to new all-time highs! The Dow futures were up $1,800 at the highs pre-market. The Great Depression is over. Recovery stocks like banks, cruise ships, restaurants, energy, and railroads are exploding to the upside, with stay-at-home stocks such as couriers, precious metals, and streaming companies in free fall. Some 500,000 health care workers have priority in getting the two-shot regime. The US Army will begin national distribution almost immediately, but you may not get it until the summer.

Market volatility crashed, with the Volatility Index (VIX) down from $41 last week to $18. Happy times are here again, at least says the market, this minute. I told you to go short last week!

Walt Disney is the best recovery play in the market. With theme parks, hotels, and cruise ships, it had the most exposure of any blue-chip company to the pandemic. It is also best positioned for any recovery. The stock was up 26% at the highs this morning. Only its rock-solid balance sheet gets this company alive. My 2021 target is $200 a share. Back to waiting in lines for hours, packing shoulder to shoulder on rides, and paying $20 for hamburgers.

The end of the depression may be in sight, but the US still faces a massive loan default wave that could erode confidence in the economy. A full economic recovery in a year will be too late for millions of businesses, especially small ones. The Fed says the risks are “severe,” and Disneyland is still laying off workers. Just when you think we are risk-free; we are not.

A big recovery in dividend stocks is coming after sitting in the doghouse for years while big tech hogged the limelight. Phillip Morris (PM) at a 6.7% yield? AbbVie (ABBV) at 5.5%? Williams Co (WMB) at 8.3%? They certainly will draw some buyers in this near-zero interest rate world. High yields REITs are also in for some joy now that a vaccine is on the horizon.

Home Prices are soaring at the fastest rate in seven years. Ultra-low interest rates and a structural shortage create the perfect storm for higher prices. Houses are now seen as “safe” since they didn’t crash 40% like the stock market did in the spring. Mortgage brokers are so overloaded it takes three months to get a refi done. This could continue for another decade.

China’s “Single’s Day” breaks all records, bringing in an eye-popping $116 billion in sales for Alibaba (BABA). US customers were the biggest buyers, eclipsing our “Black Friday” by a huge margin. I told you (BABA) was a “BUY”.

Biden could lock down the economy for 4-6 weeks if new cases keep growing at their current rate. That would knock the pandemic on the nose for good, but is it worth the price? That is an idea making the rounds in the incoming Biden administration. Cases could be peaking at 250,000 a day right around the inauguration. I may not go this year.

Stocks may Go up for years. That’s is what the Volatility Index (VIX) is telling us down here at $22. If we break below $20 and stay there, then the long-term Bull market becomes a sure thing. Stocks are now discounting the end of the pandemic.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

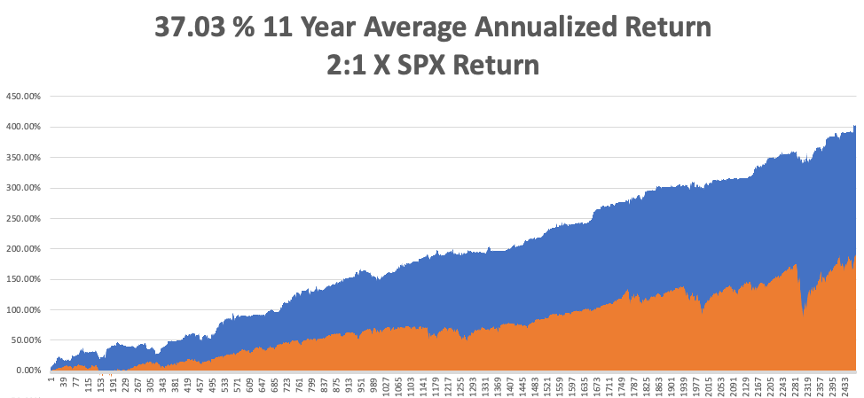

My Global Trading Dispatch exploded to another new all-time high last week. November is up 12.31%, taking my 2020 year-to-date up to a new high of 48.34%. That brings my eleven-year total return to 404.25% or double the S&P 500 over the same period. My 11-year average annualized return now stands at a new high of 37.03%.

It was a week of profit-taking on the fully invested portfolio I piled on just before the election. My one new long was in the silver ETF (SLV) and my one new short was in (TLT), both of which turned immediately profitable. I used the one dip of the week to cover a short in the (SPY) close to cost.

It worked in spades.

The coming week will be a sleeper compared to the previous one. We also need to keep an eye on the number of US Coronavirus cases and deaths, now over 10 million and 240,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, November 16 at 9:30 AM EST, the Empire State Manufacturing Index is out.

On Tuesday, November 17 at 9:30 AM, US Retail Sales are published.

On Wednesday, November 18 at 9:30 AM, US Housing Starts for October are released.

On Thursday, November 19 at 8:30 AM, the Weekly Jobless Claims are announced. At 11:00 AM, the big Existing Home Sales for October are announced.

On Friday, November 13, at 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I’ll be cleaning off the grime from the last Boy Scout trip of the year up to the giant redwoods of north Mendocino County. I haven’t been up there in 13 years and boy has it changed. The vineyards have ground enormous and entire new exurbs have been constructed. There are only a few apple farms left, where I picked up some nice cider, pie, and bags of fresh apples.

There are still a few bits of the old California left.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 16, 2020

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL)

Global Market Comments

August 14, 2020

Fiat Lux

Featured Trade:

(AUGUST 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (TLT), (TSLA), (AAPL), (FB), (AMZN), (VXX), (VIX), (JPM), (BAC), (GDX), (NUGT), (MRNA), (BRK/B), (SLV), (FCX)

Below please find subscribers’ Q&A for the August 12 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: I just joined your service. Can you explain the logic to your current model trading portfolio?

I always try to balance long positions with short position. That greatly mitigates the risk of an out-of-the-blue crash, like we saw in February. Also, every individual position has a long and short, further reducing volatility. And you never can lose more money than you put up, so your risk is defined. That’s another classic risk control measure.

There is a further four hedge in that the portfolio is spread across all asset classes. So, I am long banks (JPM), (BAC), short US Treasury bonds (TLT), short a basket of big tech stocks (AAPL), (AMZN), (FB) and long gold (GLD). Something is always working where you can take profits. Our proprietary Mad Hedge Market Timing Index is always a big help in judging the best time to enter and exit these asset classes.

That is the short course on hedge fund risk management 101.

Q: Is it a good time to add in gold (GLD) here?

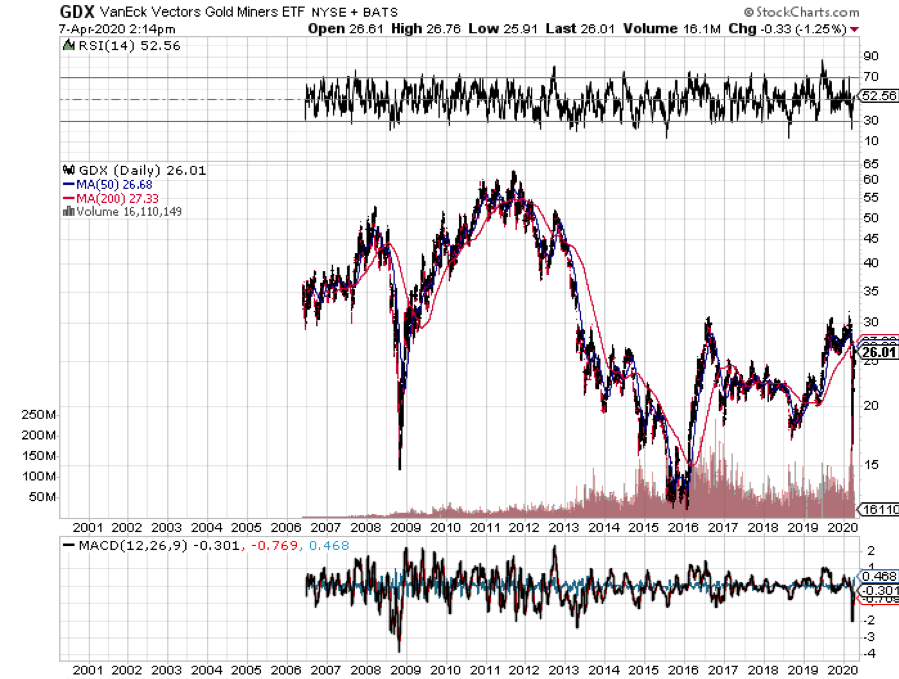

A: Yes, my long-term target for gold is $3,000/oz, possibly higher—it’s very common once you get a breakout from a 7-year bottoming process to get a big move like that. You always go back and retest that breakout level, that’s what’s happening now. I would use this dip to buy gold. You can look at (GLD) itself, the (GDX) gold miners which will give you 4:1 leverage over gold, or any of the 2x or 3x gold leveraged ETFs like (NUGT). There are lots of ways to play gold this time left from over the last bull market in gold ten years ago. So yes, bullish on gold with a temporary pullback in store. This recovery trade, which is buying banks, casinos, hotels, restaurants, weak dollar, weak buy market, weak gold—this is all temporary, this is just a trade. Those will all reverse themselves, probably by September if not sooner. So, if you missed the first round in the gold bull market, there’s certainly another chance to get back in.

Q: Do you think Biden and Harris will crash the stock market if elected?

A: No, since Biden started to run away in the polls, the stock market basically went straight up every day, and I prefer the stock market’s judgment on these things to opinion polls or talking heads. As far as Harris is concerned, she was the most middle of the road conservative pick of the 12 or so people they were looking at for vice president. Certainly, she’s a favorite with Wall Street, and isn’t it interesting they’re looking for the talents of a prosecutor in the White House? Who do you think they have in mind? So yes, that’s a net positive for the market. If anything, a new administration will bring a whole new round of Quantitative Easing and deficit spending, except it will be focused on bailing out Main Street, not Wall Street.

Q: Is the vaccine drug maker Moderna (MRNA) overbought here at 70?

A: Yes, I think to get any more appreciation you need to get an actual result on the many vaccines that are out there.

Q: Will Tesla (TSLA) pass 2,000 by year end?

A: I tend not to think so; Tesla had a once-in-a-lifetime 10-fold increase over a year. That is a very big move to digest, and while I’m saying people should keep their Tesla longs for the long term, short term you want to be selling calls against your long positions to hedge any downside and to take in some extra income.

Q: What caused ten-year US Treasury yields (TLT) to jump 14% yesterday? What will yields do from here?

A: Yields will go up and retest the 95-basis point level we saw a couple of months ago. That means we’re going to have a clear shot at adding shorts, probably for the next several weeks or months.

Q: I got the first TLT trade, but when I added the second one, I had to automatically close out my 175 short position to add the long 175 put position.

A: That is the correct way to do this. And what you end up with is a wider spread with a much larger size. So, you take all three positions we currently have, and you now have a (TLT) August $170-177.5 bear put spread in triple the original size and triple the profit, which expires in 5 trading days. It’s a trade with a very high return over a very short time frame. It’s the kind of trade that’s only available with very high volatilities in the market—at $25 in the (VIX), and you get very high accelerated time decay going into the close. So, it really was a two-week expiration play on the (TLT).

Q: Apple (AAPL) has been able to avoid any major damage in its share price in this trade war. How long can it last?

A: It can last 3 more months, until the election. It’s really quite amazing that the Chinese have not retaliated against Apple in all of these trade wars, and the reason for this is that Apple employs a million people in China, and they make a ton of money out of it. Apple has also managed their relationship with the communist government perfectly. So, that’s why they haven’t been hit. General Motors, other US companies—they could get expropriated. If the US can expropriate TikTok, what’s to stop China from expropriating General Motors, Starbucks, or even Apple for that matter?

Q: How do we know who has a real vaccine and who has a fake one? There’s so much information out there, I have a hard time filtering through what is real.

A: Wait for 100,000 people to try it out first—that’s what my plan is. That will be the safe way to do it. And if that means quarantining another couple of months to make sure you get the real deal, it’s worth the investment. Most industry safety standards, like animal trials, have been ditched by the FDA in order to get Trump a vaccine before the election. Putin is doing the same in Russia.

Q: Why is Warren Buffet buying back shares of Berkshire Hathaway (BRK/B) in record amounts? Is it because he sees no good investments?

A: He’d rather buy his own shares at parity or at a small premium than pay record PE multiples for essentially anything else in the market. Because the government rushed in so quickly to support the stock market, there never were any real deals in stocks, they never really got cheap. Yes, it sounds like down 40% in 2 months is cheap, but stocks weren’t, not even close to cheap, on a PE multiple basis. We never got close to the 9 ½X we saw in 2009. Also, if you believe in a recovery play, the ultimate recovery play is Berkshire Hathaway because they own predominantly old-line industrial cash flow stocks, which will lead any real recovery in the economy. So, at this point, Berkshire Hathaway will probably get you a higher return on a 12-month view than say Apple, Facebook or Amazon.

Q: Gold (GLD) vs Silver (SLV)? Which is better? And what about Copper (FCX)?

A: Silver always outperforms gold by at least 2 to 1 in any real economic recovery. Copper prices have risen 30% in 4 months; that is discounting a real economic recovery someday, so I would be buying copper on dips also.

Q: How do we learn more about options?

A: I suggest you go to the “How to Trade” section on our website, and that has links. Every trade alert we send out also has a link to a video that tells you exactly how to do the options part of that trade. And if you don’t want to do options, we also propose ETF and single stocks.

Q: What year end effect on the market do you see from a Biden tax plan on long term capital gains and qualified dividends at the ordinary income rate?

A: Well, if he actually proposes that, there will be a rush to sell assets by the end of the current year so people can take advantage of the very favorable capital gains tax that exist now. However, it’s not known whether that is actually the tax increase he’s proposing; it’s more likely he’ll simply return to the pre-Trump tax rates. However, I do expect him to come up with highly punitive tax rates on any real estate-related investment as a way of getting back at Trump. And that’s like loss carry forwards, steps up in the cost basis, 1031 exchanges—things specific to the real estate industry.

Q: If you think markets are going to come off, why aren’t you more aggressive buying the iPath Series B S&P 500 VIX Short Term Futures ETN (VXX)?

A: (VXX) has become such a professional market it really has become a day trading vehicle. It’s hard to get customers in and out of this thing fast enough to make them money, as most of my followers are not set up to be day traders. It’s a market where 90% of the professionals are playing from the short side, so when you get moves up, they essentially happen over 1 or 2 days, and then they spend weeks or months bleeding off. It really is a tough trade for a retail trader to do; and it is an area where the insiders in Chicago trade this thing and really do have an in-house advantage that I would rather not try to bet against.

Q: I sold the top on all precious metals positions and started buying back today. Was that the right thing to do?

A: Yes, I have a feeling it is. Start scaling in—if you’re nervous about buying gold here, buy a third of a position now, a third if it’s higher or lower, and a third if it’s higher or lower again. That’s what any pro would do.

Q: Do you see another big economic crisis in 2021?

A: I don’t think so; I think any continued weakness will be hit with massive liquidity from the Fed and more government spending. Now that they found the model to keep the economy going, they’re going to just keep at it, no matter who is in power. Roosevelt kept at it for 5 years to end the Great Depression, until he was bailed out by WWII, so hopefully we don’t have to bail our economy out the same way with WWIII.

Q: What about Bitcoin here?

A: We don’t trade Bitcoin as we think the whole thing is a giant scam. There’s also no value added by anyone. Insiders have a huge advantage, the people who are creating the bitcoin to sell. So, it’s a security with no fundamentals—thus unanalyzable.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 8, 2020

Fiat Lux

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (GOLD), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

SPECIAL GOLD ISSUE

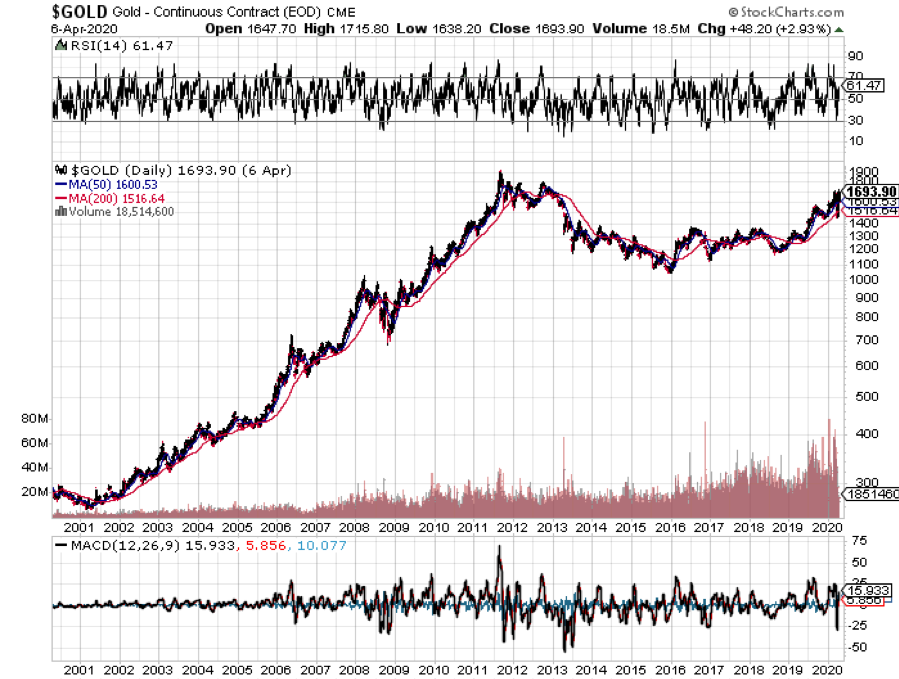

I have been bullish on gold (GLD) for the last three years and the payoff is finally here (click here).

How high could it really go?

The recent massive stimulus measures to fight the Coronavirus-induced depression is certainly bringing forward the rebirth of inflation. The Fed has just increased all of the $17 trillion quantitative easing created globally over the past decade by a staggering 50% in weeks!

This is hugely gold-friendly.

I was an unmitigated bear on the price of gold after it peaked in 2011. In recent years, the world has been obsessed with yields, chasing them down to historically low levels across all asset classes.

But now that much of the world already has, or is about to have negative interest rates, a bizarre new kind of mathematics applies to gold ownership.

Gold’s problem used to be that it yielded absolutely nothing, cost you money to store, and carried hefty transactions costs. That asset class didn’t fit anywhere in a yield-obsessed universe.

Now, we have a horse of a different color.

Europeans wishing to put money in a bank have to pay for the privilege to do so. Place €1 million on deposit on an overnight account, and you will have only 996,000 Euros in a year. You just lost 40 basis points on your -0.40% negative interest rate.

With gold, you still earn zero, an extravagant return in this upside-down world. All of a sudden, zero is a win.

For the first time in human history, that gives you a 40-basis point yield advantage over Euros. Similar numbers now apply to Japanese yen deposits as well.

As a result, the numbers are so compelling that it has sparked a new gold fever among hedge funds and European and Japanese individuals alike.

Websites purveying investment grade coins and bars crashed multiple times last week due to overwhelming demand (I occasionally have the same problem). Some retailers have run out of stock.

So I’ll take this opportunity to review a short history of the gold market (GLD) for the young and the uninformed.

Since it peaked in the summer of 2011, the barbarous relic was beaten like the proverbial red-headed stepchild, dragging silver (SLV) down with it. It faced a perfect storm.

Gold was traditionally sought after as an inflation hedge. But with economic growth weak, wages stagnant, and much work still being outsourced abroad, deflation became rampant (click here).

The biggest buyers of gold in the world, Indian investors, have seen their purchasing power drop by half, thanks to the collapse of the rupee against the US dollar. The government increased taxes on gold in order to staunch precious capital outflows.

You could also blame the China slowdown for the declining interest in the yellow metal, which is now in its sixth year of falling economic growth.

Chart gold against the Shanghai index, and the similarity is striking, until negative interest rates became widespread in 2016.

In the meantime, gold supply/demand balance was changing dramatically.

While no one was looking, the average price of gold production soared from $5 in 1920 to $1,300 today. Over the last 100 years, the price of producing gold has risen four times faster than the underlying metal.

It’s almost as if the gold mining industry is the only one in the world which sees real inflation, since costs soared at a 15% annual rate for the past five years.

This is a function of what I call “peak gold.” They’re not making it anymore. Miners are increasingly being driven to higher risk, more expensive parts of the world to find the stuff.

You know those giant six-foot high tires on heavy dump trucks? They now cost $200,000 each, and buyers face a three-year waiting list to buy one.

Barrick Gold (GOLD) didn’t try to mine gold at 15,000 feet in the Andes, where freezing water is a major problem, because they like the fresh air.

What this means is that when the spot price of gold fell below the cost of production, miners simply shut down their most marginal facilities, drying up supply.

Barrick Gold, a client of the Mad Hedge Fund Trader, can still operate as older mines carry costs that go all the way down to $600 an ounce.

I am constantly barraged with emails from gold bugs who passionately argue that their beloved metal is trading at a tiny fraction of its true value and that the barbaric relic is really worth $5,000, $10,000, or even $50,000 an ounce (GLD).

They claim the move in the yellow metal we are seeing now is only the beginning of a 30-fold rise in prices, similar to what we saw from 1972 to 1979, when it leapt from $32 to $950.

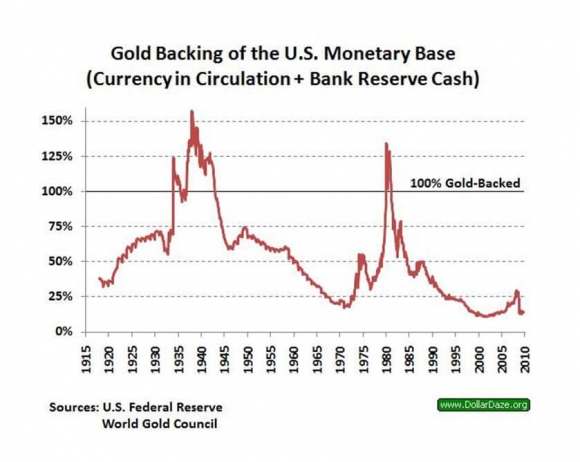

So, when the chart below popped up in my in-box showing the gold backing of the US monetary base, I felt obligated to pass it on to you to illustrate one of the intellectual arguments these people are using.

To match the gain seen since the 1936 monetary value peak of $35 an ounce when the money supply was collapsing during the Great Depression and the double top in 1979 when gold futures first tickled $950, this precious metal has to increase in value by 800% from the recent $1,050 low. That would take our barbarous relic friend up to $8,400 an ounce.

To match the move from the $35/ounce, 1972 low to the $950/ounce, 1979 top in absolute dollar terms, we need to see another 27.14 times move to $28,497/ounce.

Have I gotten you interested yet?

I am long term bullish on gold, other precious metals, and virtually all commodities for that matter. But I am not that bullish. These figures make my own $2,300/ounce long-term prediction positively wimp-like by comparison.

The seven-year spike up in prices we saw in the seventies, which found me in a very long line in Johannesburg, South Africa to unload my own Krugerrands in 1979, was triggered by a number of one-off events that will never be repeated.

Some 40 years of unrequited demand was unleashed when Richard Nixon took the US off the gold standard and decriminalized private ownership in 1972. Inflation then peaked around 20%. Newly enriched sellers of oil had a strong historical affinity with gold.

South Africa, the world’s largest gold producer, was then a boycotted international pariah teetering on the edge of disaster. We are nowhere near the same geopolitical neighborhood today, and hence, my more subdued forecast.

But then again, I could be wrong.

In the end, gold may have to wait for a return of real inflation to resume its push to new highs. The previous bear market in gold lasted 18 years, from 1980, to 1998, so don’t hold your breath.

What should we look for? The surprise that your friends get out of the blue pay increase, the largest component of the inflation calculation.

This is happening now in technology and healthcare, but nowhere else. When I visit open houses in my neighborhood in San Francisco, half the visitors are thirty somethings wearing hoodies offering to pay cash.

It could be a long wait for real inflation, possibly into the mid 2020s when shocking wage hikes spread elsewhere.

You’ll be the first to know when that happens.

As for the many investment advisor readers who have stayed long gold all along to hedge their clients other risk assets, good for you.

You’re finally learning!

Global Market Comments

February 27, 2020

Fiat Lux

Featured Trade:

(GET READY TO TAKE A LEAP BACK INTO LEAPS),

(AAPL), (BA),

(TESTIMONIAL)

Global Market Comments

February 26, 2020

Fiat Lux

SPECIAL GOLD ISSUE

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (ABX), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

With global stock markets in free fall and interest rates everywhere headed to zero, the outlook for gold has gone from strength to strength.

Shunned as the pariah of the financial markets for years, the yellow metal has suddenly become everyone’s favorite hedge.

Now that gold is back in fashion, how high can it really go?

The question begs your rapt attention, as the Coronavirus has suddenly unleashed a plethora of new positive fundamentals for the barbarous relic.

It turns out that gold is THE deflationary asset to own. Who knew?

I was an unmitigated bear on the price of gold after it peaked in 2011. In recent years, the world has been obsessed with yields, chasing them down to historically low levels across all asset classes.

But now that much of the world already has, or is about to have negative interest rates, a bizarre new kind of mathematics applies to gold ownership.

Gold’s problem used to be that it yielded absolutely nothing, cost you money to store, and carried hefty transactions costs. That asset class didn’t fit anywhere in a yield-obsessed universe.

Now we have a horse of a different color.

Europeans wishing to put money in a bank have to pay for the privilege to do so. Place €1 million on deposit on an overnight account, and you will have only 996,000 Euros in a year. You just lost 40 basis points on your -0.40% negative interest rate.

With gold, you still earn zero, an extravagant return in this upside-down world. All of a sudden, zero is a win.

For the first time in human history, that gives you a 40-basis point yield advantage by gold over Euros. Similar numbers now apply to Japanese yen deposits as well.

As a result, the numbers are so compelling that it has sparked a new gold fever among hedge funds and European and Japanese individuals alike.

Websites purveying investment grade coins and bars crashed multiple times last week, due to overwhelming demand (I occasionally have the same problem). Some retailers have run out of stock.

And last week, the virus went pandemic as silver rocketed 8.6% and others like Palladium (PALL) were also frenetically bid.

So I’ll take this opportunity to review a short history of the gold market (GLD) for the young and the uninformed.

Since it last peaked in the summer of 2011 at $1,927 an ounce, the barbarous relic was beaten like the proverbial red-headed stepchild, dragging silver (SLV) down with it. It faced a perfect storm.

Gold was traditionally sought after as an inflation hedge. But with economic growth weak, wages stagnant, and much work still being outsourced abroad, deflation became rampant.

The biggest buyers of gold in the world, the Indians, have seen their purchasing power drop by half, thanks to the collapse of the rupee against the US dollar. The government increased taxes on gold in order to staunch precious capital outflows.

Chart gold against the Shanghai index, and the similarity is striking, until negative interest rates became widespread in 2016.

In the meantime, gold supply/demand balance was changing dramatically.

While no one was looking, the average price of gold production soared from $5 in 1920 to $1,400 today. Over the last 100 years, the price of producing gold has risen four times faster than the underlying metal.

It’s almost as if the gold mining industry is the only one in the world which sees real inflation, since costs soared at a 15% annual rate for the past five years.

This is a function of what I call “peak gold.” They’re not making it anymore. Miners are increasingly being driven to higher risk, more expensive parts of the world to find the stuff.

You know those tires on heavy dump trucks? They now cost $200,000 each, and buyers face a three-year waiting list to buy one.

Barrick Gold (GOLD), the world’s largest gold miner, didn’t try to mine gold at 15,000 feet in the Andes, where freezing water is a major problem, because they like the fresh air.

What this means is that when the spot price of gold fell below the cost of production, miners simply shut down their most marginal facilities, drying up supply. That has recently been happening on a large scale.

Barrick Gold, a client of the Mad Hedge Fund Trader, can still operate, as older mines carry costs that go all the way down to $600 an ounce.

No one is going to want to supply the sparkly stuff at a loss. So, supply disappeared.

I am constantly barraged with emails from gold bugs who passionately argue that their beloved metal is trading at a tiny fraction of its true value, and that the barbaric relic is really worth $5,000, $10,000, or even $50,000 an ounce (GLD).

They claim the move in the yellow metal we are seeing now is only the beginning of a 30-fold rise in prices, similar to what we saw from 1972 to 1979, when it leapt from $32 to $950.

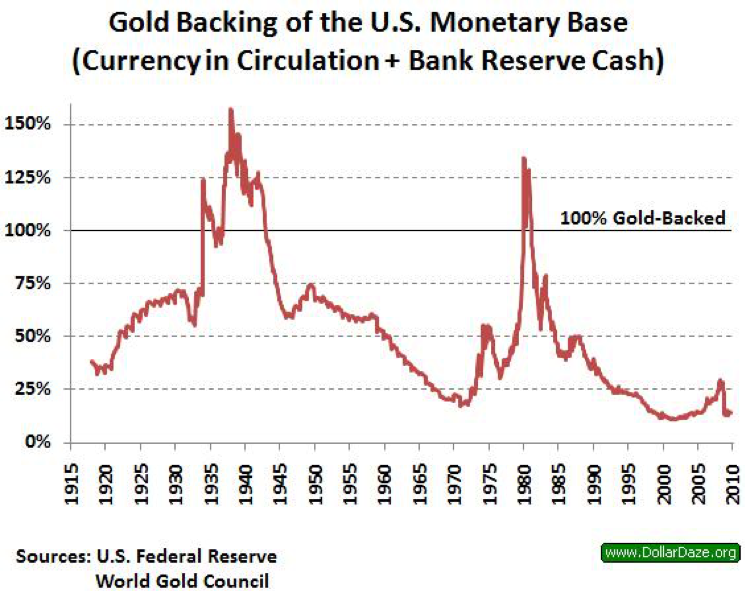

So, when the chart below popped up in my inbox showing the gold backing of the US monetary base, I felt obligated to pass it on to you to illustrate one of the intellectual arguments these people are using.

To match the gain seen since the 1936 monetary value peak of $35 an ounce, when the money supply was collapsing during the Great Depression, and the double top in 1979 when gold futures first tickled $950, this precious metal has to increase in value by 800% from the recent $1,050 low. That would take our barbarous relic friend up to $8,400 an ounce.

To match the move from the $35/ounce, 1972 low to the $950/ounce, 1979 top in absolute dollar terms, we need to see another 27.14 times move to $28,497/ounce.

Have I gotten your attention yet?

I am long term bullish on gold, other precious metals, and virtually all commodities for that matter. But I am not that bullish. These figures make my own $2,300/ounce long-term prediction positively wimp-like by comparison.

The seven-year spike up in prices we saw in the seventies, which found me in a very long line in Johannesburg, South Africa to unload my own Krugerrands in 1979, was triggered by a number of one-off events that will never be repeated.

Some 40 years of unrequited demand was unleashed when Richard Nixon took the US off the gold standard and decriminalized private ownership in 1972. Inflation then peaked around 20%. Newly enriched sellers of oil had a strong historical affinity with gold.

South Africa, the world’s largest gold producer, was then a boycotted international pariah and teetering on the edge of disaster. We are nowhere near the same geopolitical neighborhood today, and hence, my more subdued forecast.

But then again, I could be wrong.

In the end, gold may have to wait for a return of real inflation to resume its push to new highs. The previous bear market in gold lasted 18 years, from 1980 to 1998, so don’t hold your breath.

What should we look for? The surprise that your friends get out of the blue pay increase, the largest component of the inflation calculation.

This is happening now in technology and is slowly tricking down to minimum wage workers. When I visit open houses in my neighborhood in San Francisco, half the visitors are thirty-somethings wearing hoodies offering to pay cash.

It could be a long wait for real inflation, possibly into the mid-2020s, when shocking wage hikes spread elsewhere.

I’ll be back playing gold again, given a good low-risk, high-return entry point.

You’ll be the first to know when that happens.

As for the many investment advisor readers who have stayed long gold all along to hedge their clients' other risk assets, good for you.

You’re finally learning!