(MARKET OUTLOOK FOR THE WEEK AHEAD or S&P 500 6,000 TARGET ACHIEVED, plus REPORT FROM THE FROZEN WASTELANDS OF THE WEST),

(CCI), (DHI), GLD), (SLV) (JPM), (MS), (BLK),

(CCJ), (NVDA), (AMZN), (TSLA), (DGE)

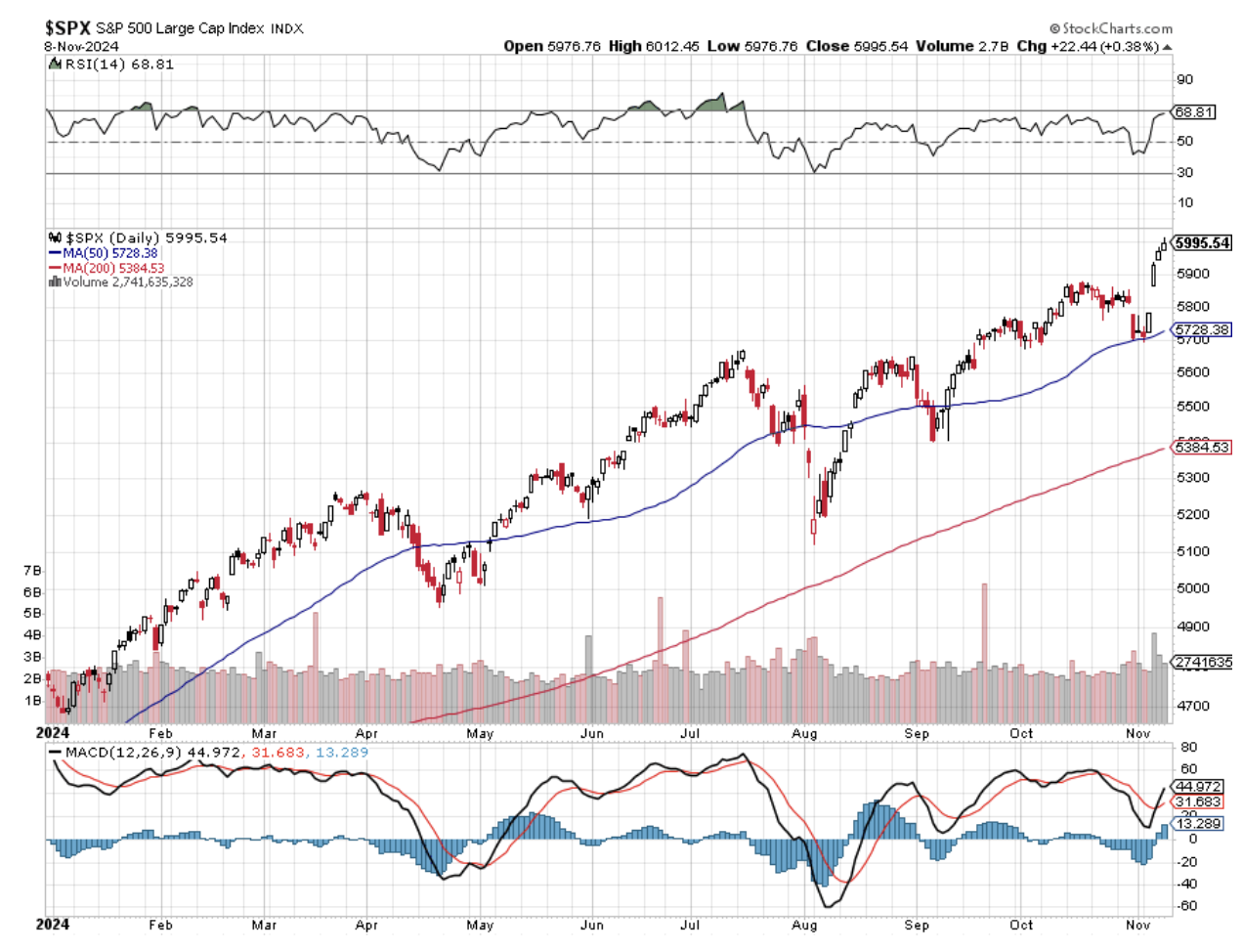

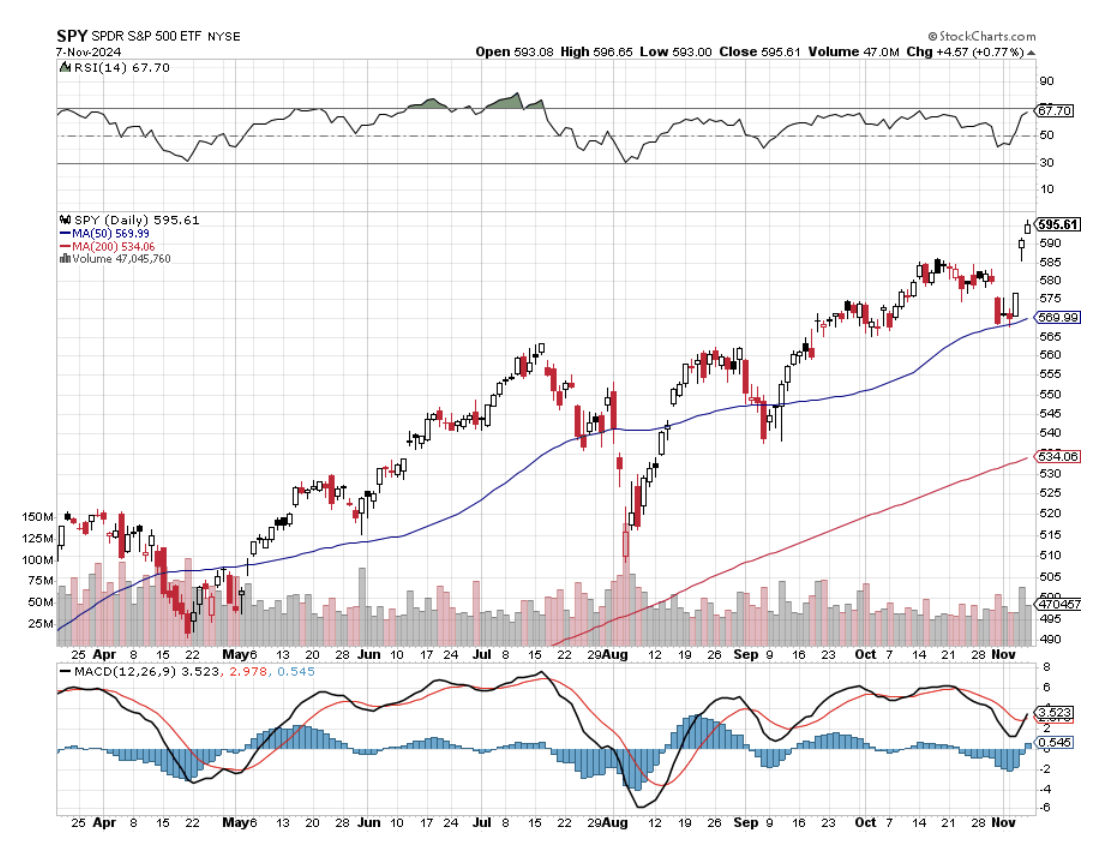

I was reviled, abused, and outright laughed at by the investment community when, last January 5, I predicted that the S&P 500 would hit 6,000 by yearend, click here for the link. I was accused of sending out clickbait.

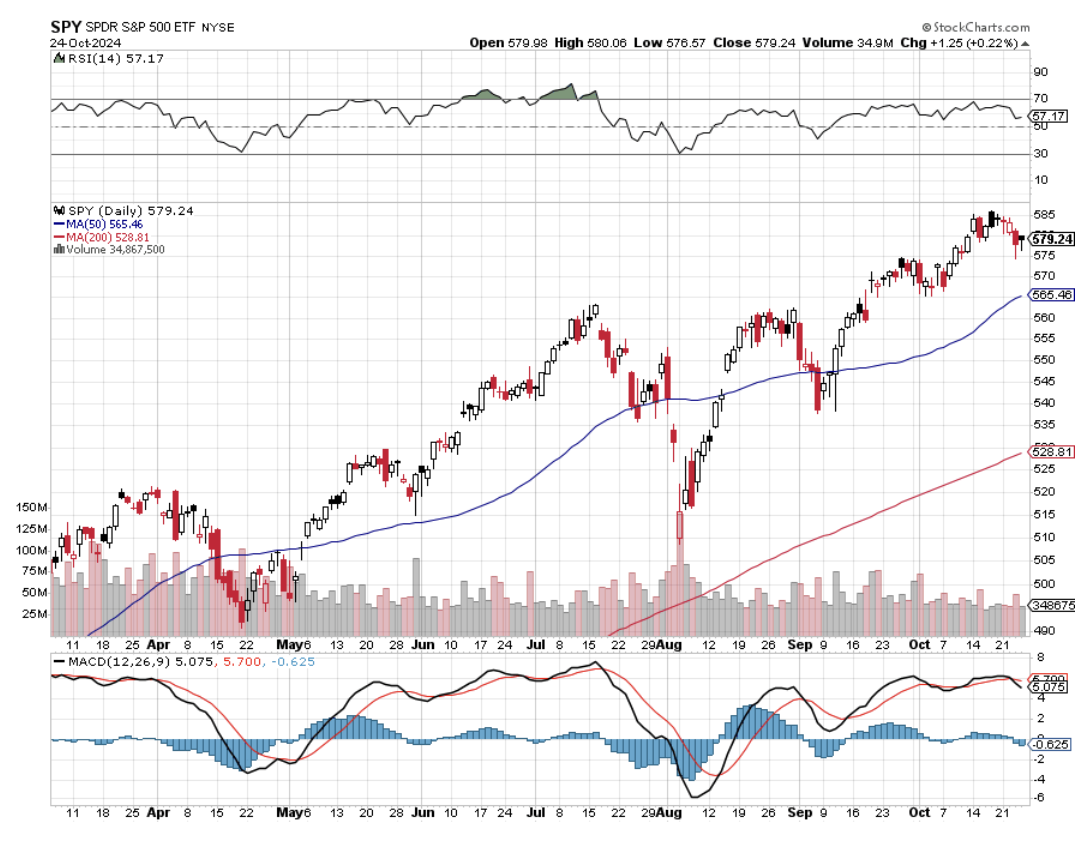

Yet here, ten months and change into the year here, we are with an intraday high today of 6,013.

Of course, in this business, you’re only as good as your last trade. So, the big question now is, what happens next?

The next two months are a gimme. The $8 trillion that has been sitting on the sideline is now pouring into the market. An S&P 500 target of 6,600 is within range. Speaking to fund managers around the country, the big concern was not over who won but whether we had a winner at all.

Three months of litigation with no outcome would have raised uncertainty to extremes and crashed the market. The risk of that scenario is now gone, which was worth a $1,500 rally in a day.

However, while the bull market continues, the targets have changed. As you will hear many times over the next four years, elections have consequences.

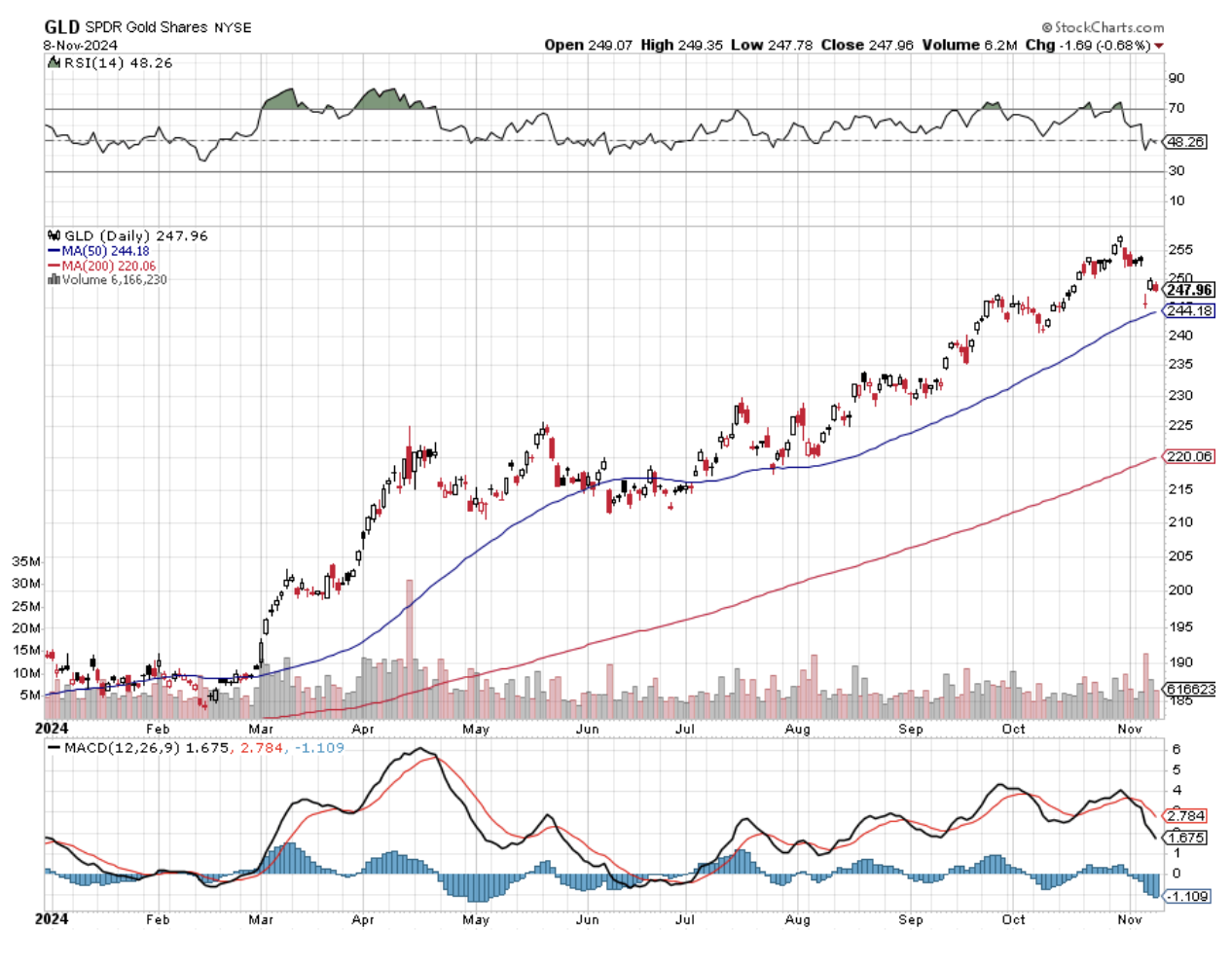

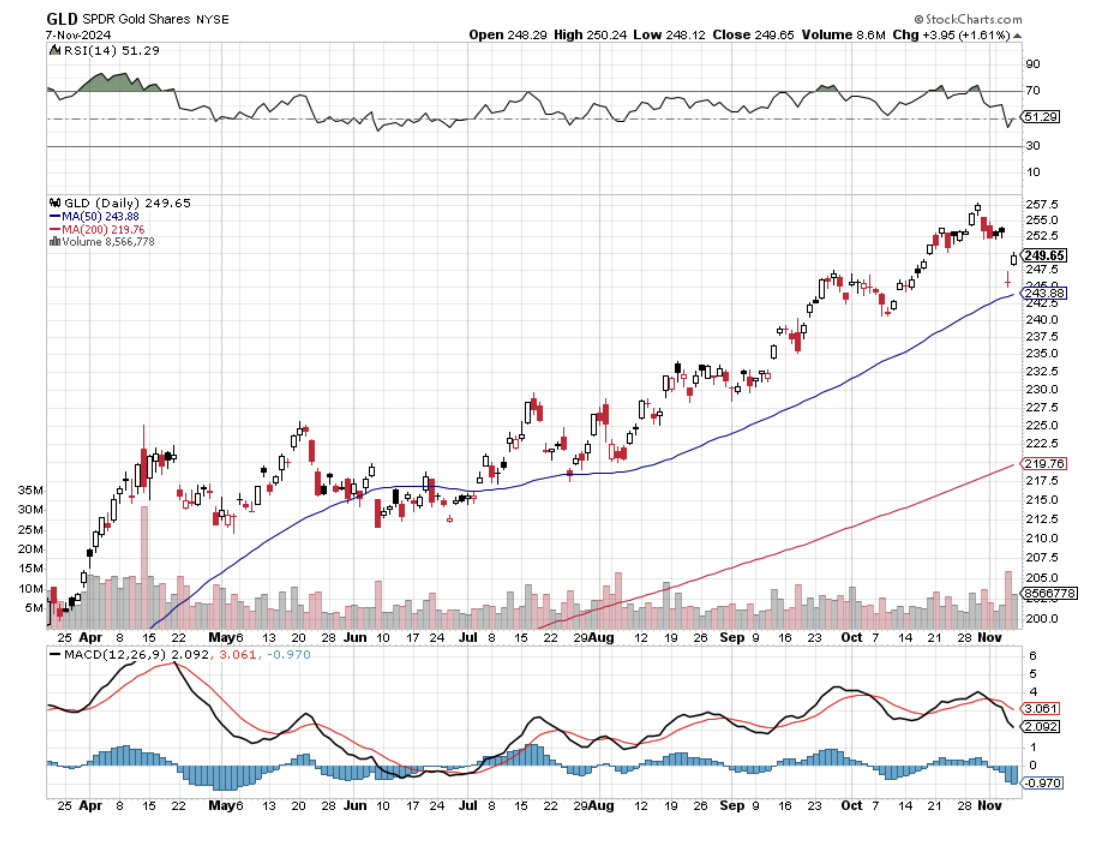

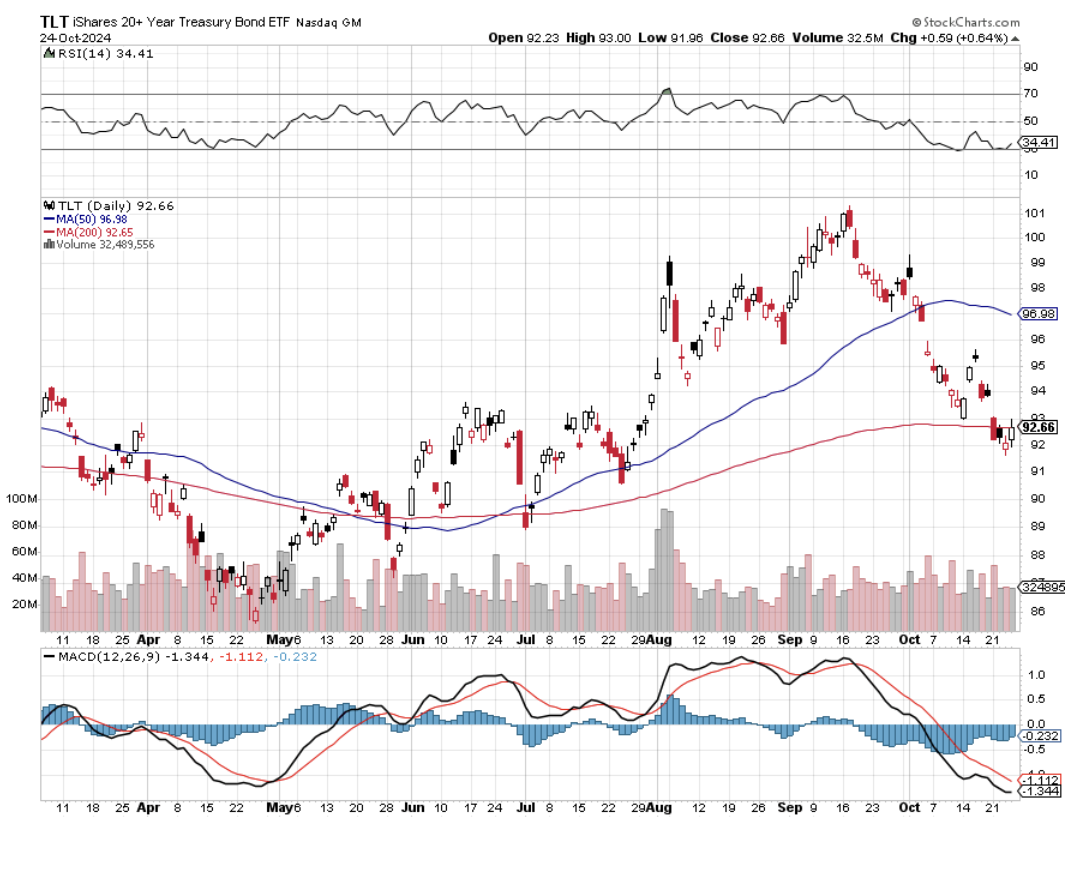

Falling interest rate plays are out. Don’t expect much performance from real estate, REITS (CCI), new homebuilders (DHI), gold GLD), and silver (SLV).

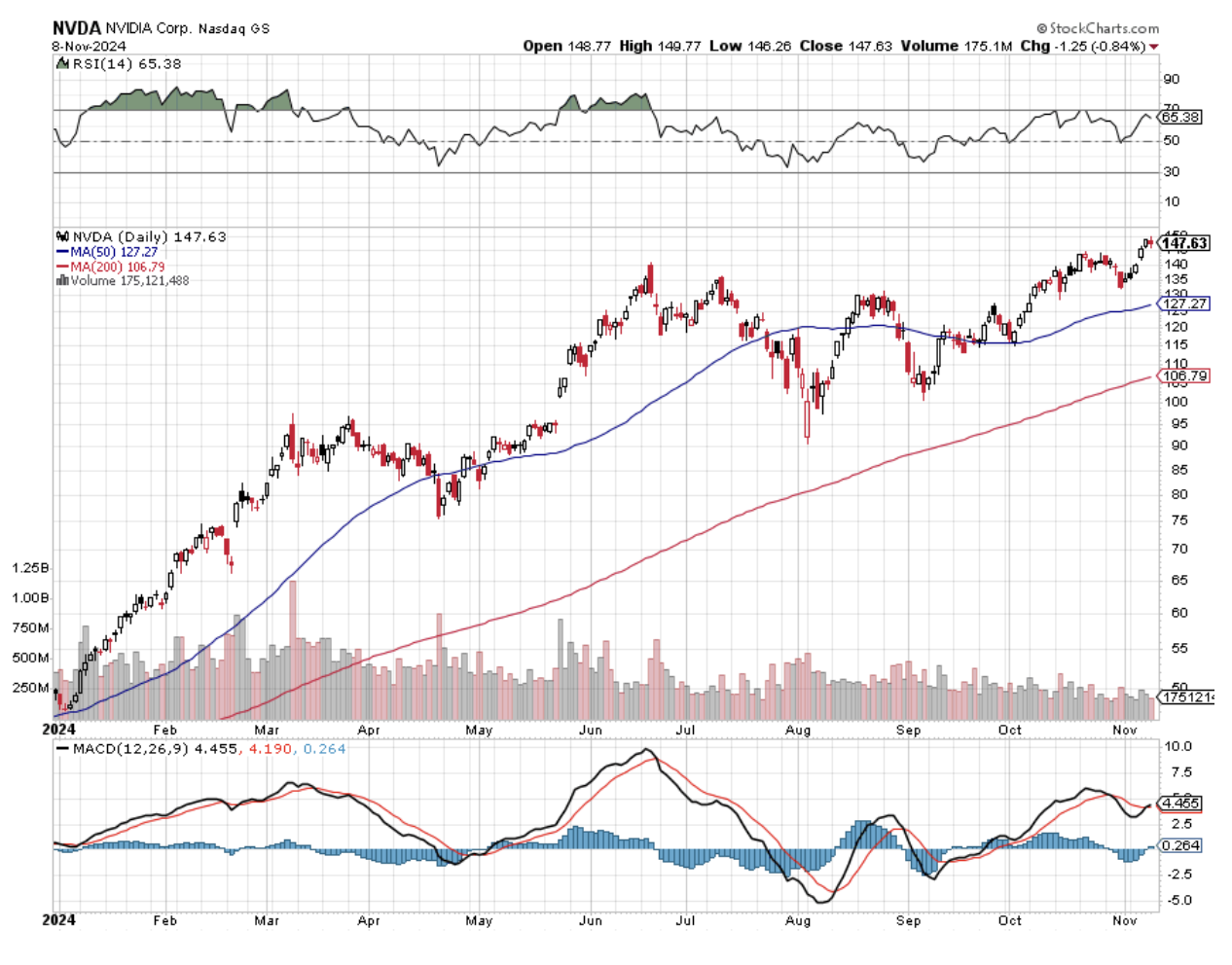

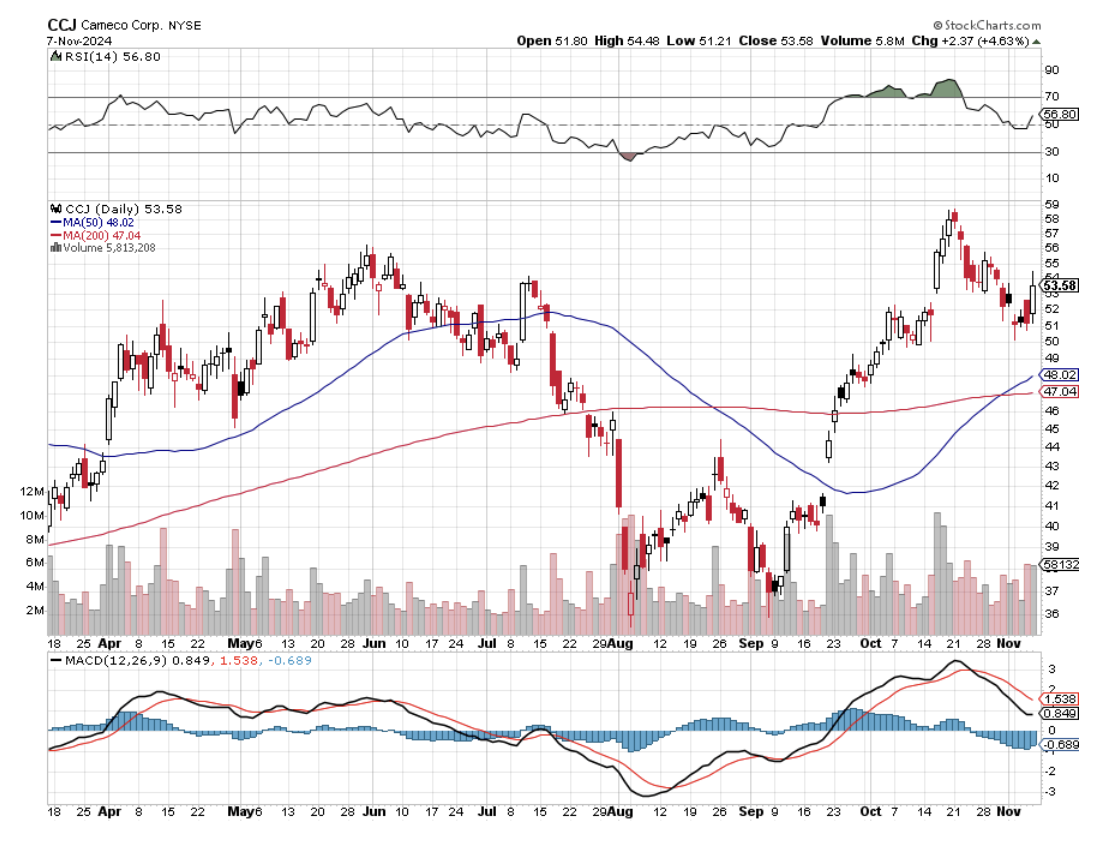

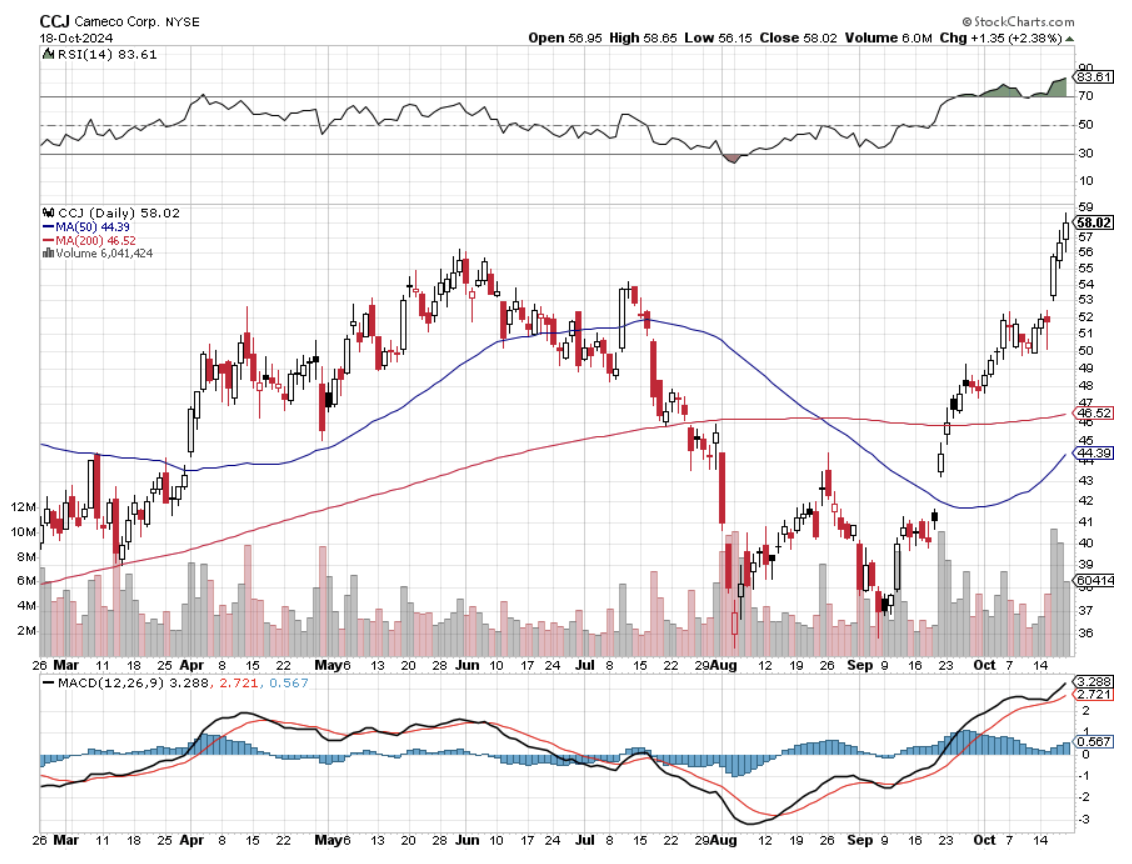

Deregulation plays are in. The good news is that this is a fairly wide sector. It includes banks (JPM), brokers (MS), money managers (BLK), new nuclear (CCJ), big tech that had been targeted by antitrust (NVDA) and (AMZN), and Tesla (TSLA).

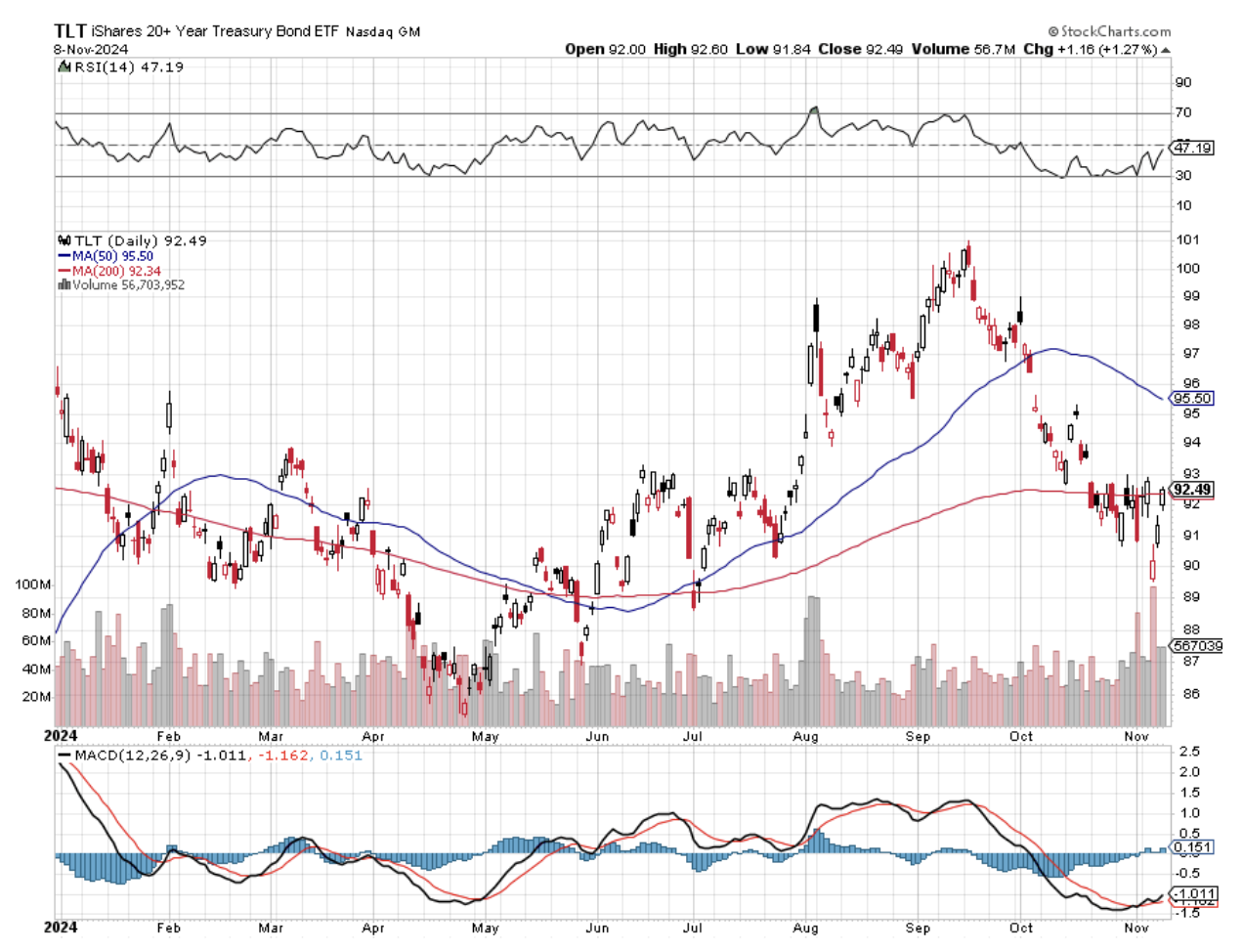

Bonds are toast.

Promised Trump policies of tax cuts and spending increases will balloon the National Debt by $10-$15 trillion. The bond market is unlikely to be able to handle this amount of new issuance, especially with annual interest payments owed by the government already at $1 trillion. It is the second largest budget item after Social Security.

Selling into a national debt of $50 trillion is going to be completely different than selling into a national debt of $27 trillion when Trump last left office. This is the reason why major hedge funds are running Treasury bond shorts as their biggest positions, who were all Trump supporters and donors.

It all depends on inflation. This is not some far-distant theoretical thing. It is happening already. I got hit with several price increases today, and I am hearing about rises in other industries, like steel. The expectation is that a stronger economy can handle the price hikes.

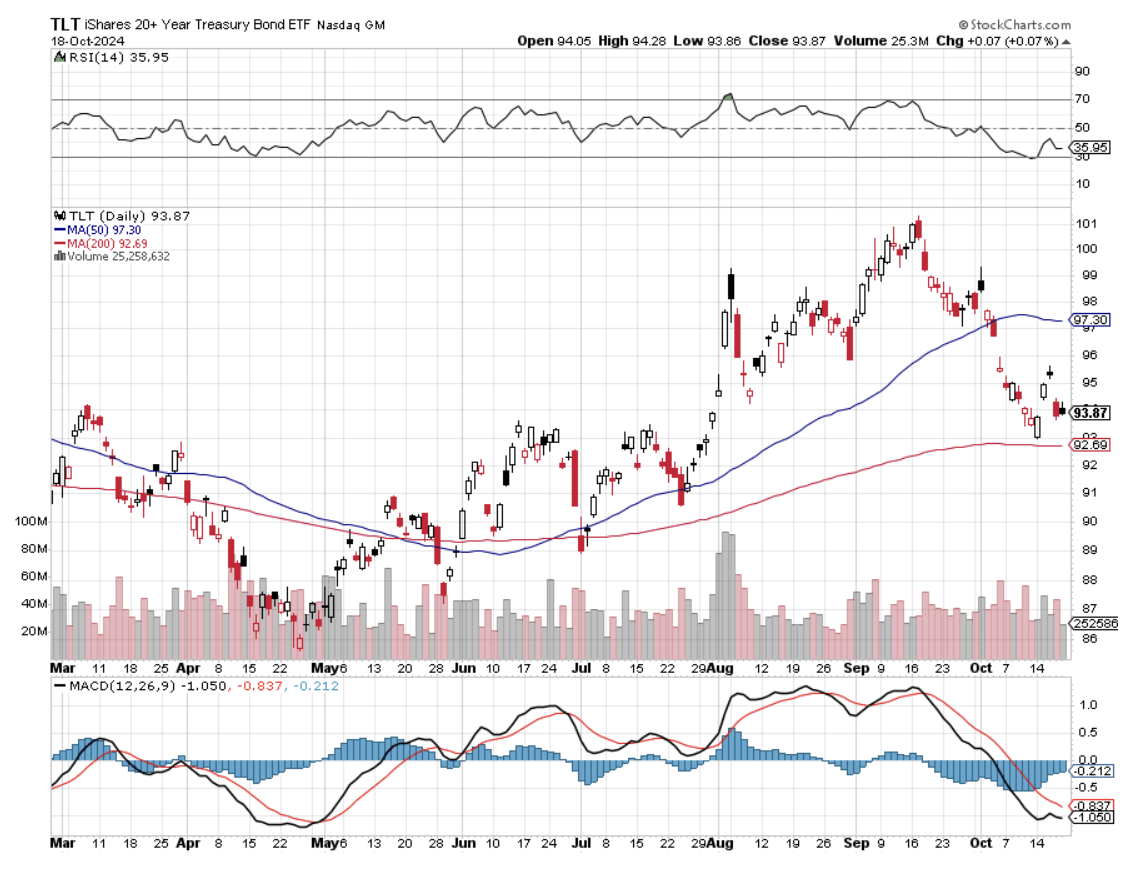

So, the best case for bonds is that the (TLT) chops around here. The worst case is that we retest new lows at $82. It won’t help that the Federal Reserve is cutting interest rates by another 25 basis points on December 18. The Fed controls only overnight interest rates, not the 10–20-year bond market. Even if Trump appoints an ultra-dove as chairman of the Federal Reserve in 2026, bond vigilantes may have other ideas.

Then there is the matter of trade tariffs. I have been through many of these. Remember when Nixon banned the import of Japanese textiles in 1972? They don’t make textiles in Japan anymore because their rising labor costs drove that industry to China.

Trade wars are a negative sum game. There are only losers. The game is to punish your neighbors faster than they are punishing you. They shrink the pie.

If we raise tariffs on our allies, they will retaliate in kind. This will be a problem for big tech, which gets 50%-60% of their sales from abroad. Europe will target uniquely American products, like Captain Morgan rum. Notice that the brand owner, major exporter Diageo (DGE), saw its shares slaughtered last week. As a result, the price of everything here will soon start going up.

The (TLT) will be a great position to have going into the next recession. But the market won’t start discounting that for two or three years. That makes the (TLT) a trade for another day. In any case, there are better fish to fry.

Sell all (TLT) LEAPS now before they go down even more.

About that recession. Every bear market in my lifetime started with a Republican president. The pattern is always the same. Tax cuts, an excess stimulus, and deregulation lead to a higher high in the stock market as euphoria prevails. This leads to inflation, high interest rates, and recession.

This is not exactly an original thought. High rates caused the bear markets of 2008, which took the Dow Average down -52%, 2000 (-30%), 1990 (-30%), 1987 (30%). Previous bear markets in 1979 and 1973 were caused by oil shocks. 2027?

We shall see.

So make hay while the sun shines. The current euphoria binge will last three to six months. After that, we will need to reassess and start shopping for short plays among the most extreme moves, which I have already done with Tesla.

The bottom line for all of this is that equity returns for the next four years will be lower than the last four. If a recession hits, they could well be zero. This won’t be a problem if you get out at the top, as I did in 2008, 2000, 1990, and 1987. Conclusion: You need me now more than ever.

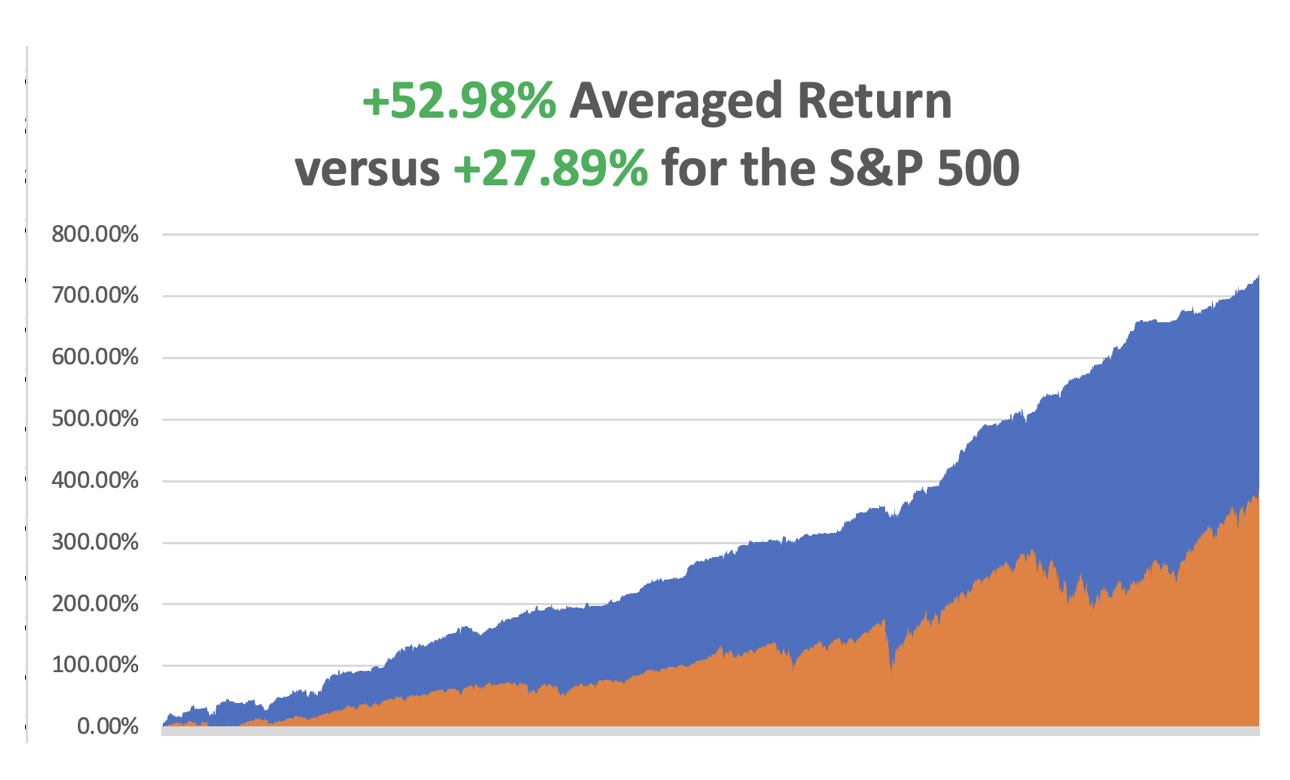

In November, we have gained a breathtaking +7.63%, thankfully because we went into the election with 70% cash and then poured money into deregulation plays. My 2024 year-to-date performance is at an amazing +60.77%.The S&P 500 (SPY) is up +25.73%so far in 2024. My trailing one-year return reached a nosebleed +69.73%. That brings my 16-year total return to +737.30%.My average annualized return has recovered to +52.98%.

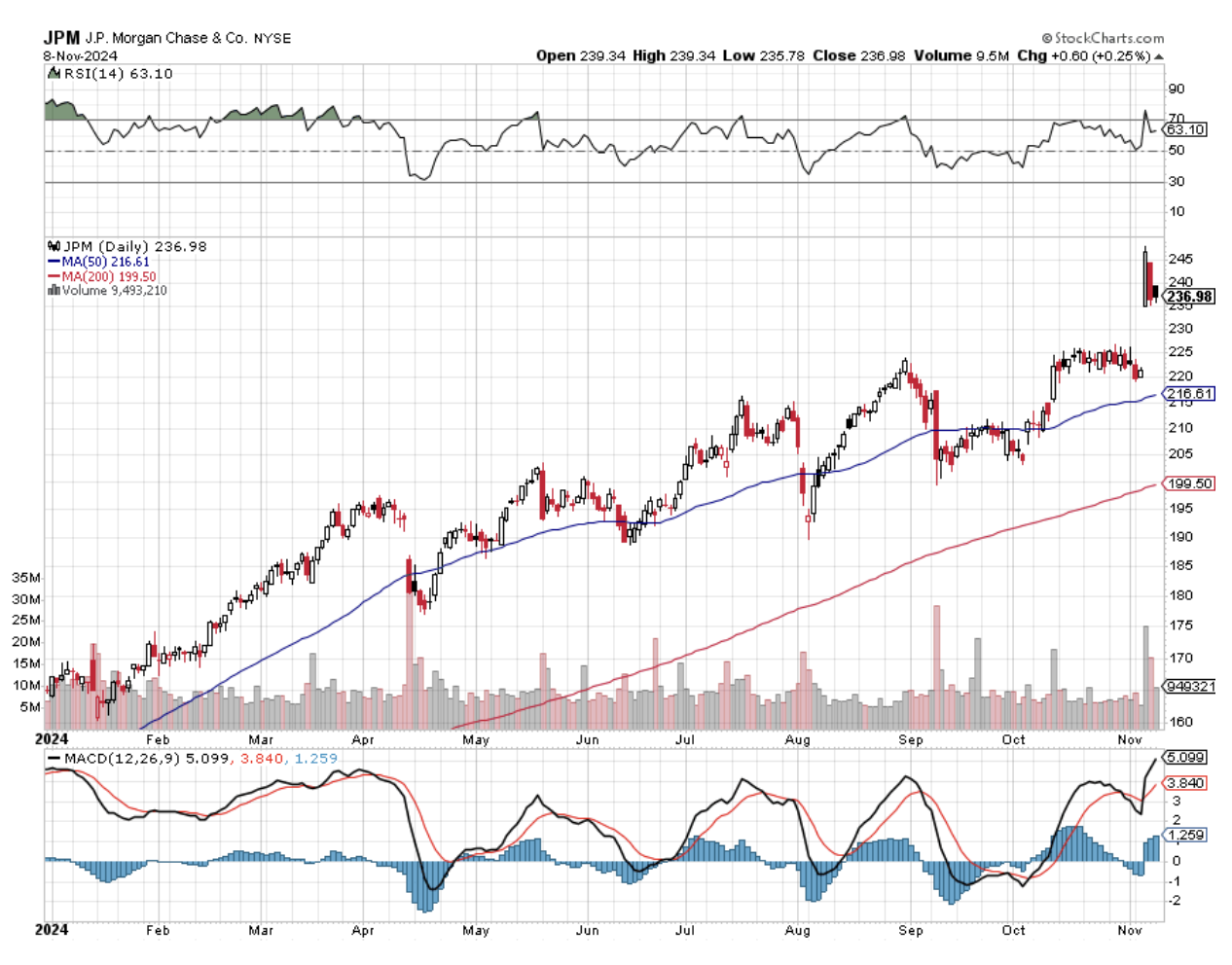

I went into the election with two positions in (JPM) and (NVDA), which turned out to be great deregulations plays. I stopped out of my one interest-sensitive play in (GLD) near cost. I piled on new deregulation plays in (TSLA), (CCJ), and (MS). I also added a new short in (TSLA), taking advantage of a monster 60% implied volatility for the options.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 69 of 89 trades have been profitable so far in 2024, and several of those losses were really break evens. Some 22 out of the last 25 trade alerts were profitable. That is a success rate of +88.80%.

Try beating that anywhere.

My Ten-Year View – A Reassessment

When we have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at a headwind. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

My Dow 240,000 target has been pushed back to 2035.

On Monday, November 11 is Veterans Day, so banks, the bond market, and the post office will be closed. On Tuesday, November 12 at 6:00 AM EST, the NFIB Business Optimism Index takes place.

On Wednesday, November 13 at 8:30 PM, the Consumer Price Index rate is announced.

On Thursday, November 14 at 8:30 AM, the Producer Price Index is out.

On Friday, November 15 at 8:30 AM, the Retail Sales are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I am writing this from a High Sierra peak at 12,000 feet in the at the beginning of winter. It is 15 degrees, and the wind is gusting at 70 miles an hour, turning my backpack into a sail and practically blowing me off the mountain. Over the side, the next stop is 1,000 feet below. I am thirsty, but the water in my canteen is frozen solid.

I had planned to follow my tracks in the snow back down to my car, but the wind had totally obliterated them. So, I am using an old-fashioned army compass to navigate back in total whiteout conditions. Good thing I got the letter out early today!

Actually, I am not writing this, I am thinking it. If I took my hands out of my heavy mittens, my fingers would freeze in seconds. Remember, no fingers, no Trade Alerts!

A couple of times a year, I feel the need to abandon civilization and contemplate the meaning of life while accomplishing a great physical challenge. For me, this is a mandatory religious experience.

This time, I attempted to emulate one of the great physical feats in history. In October 1847, the Donner Party’s wagon train was hopelessly snowed in at a Sierra pass. Starvation loomed. When word reached Sacramento, four rescue parties were sent out, only to be repulsed by driving blizzards.

Finally, a giant of heroic strength, the famous Snowshoe Thompson, who stood at 6’6”, broke through. He emptied his massive wood frame backpack of food and then stuffed it with the two smallest children he could find. He snowshoed back to safety 120 miles over three days, nonstop. The kids grew up to become the founding fathers of modern-day Marin County, California.

I thought, “Gee, I wonder if I could do that?”

So, I sought to replicate the feat, subject to a few modern compromises. Today, Interstate 80 sits astride Thompson’s original route. Instead, I determined to snowshoe 120 miles of the Tahoe Rim Trail around Lake Tahoe, with an average elevation of 9,000 feet. I figured that the 60-pound pack I usually carry was worth the weight of two kids.

My one concession to my advanced age was that instead of going nonstop or camping out at night, I would break the epic trek into ten days at 12 miles each. That allowed me to repair my Tahoe lakefront estate nightly to thaw out my toes, treat injuries, and get some shuteye. Howling winds keep you awake at night.

I fasted while accomplishing this, eating only 600 calories a day of raw fruit and nuts. I’m down about ten pounds since I began.

Hint to readers: almonds have unique, hunger-fighting chemical properties. Eat a handful before you go to sleep, and hunger pangs won’t wake you in the middle of the night. I plan on eating some industrial strength this Christmas, things like Tom and Jerry’s and See's Peanut Brittle, so I need to get ahead of the curve. (note to self: 223 calories in a cup of eggnog).

My friends call this a death march, make excuses why they can’t come, and worry about my sanity. I think of it as a cleansing and a general stocktaking, and I feel great! I always go alone. How many other 72-year-olds do you know who are in a condition to do this sort of thing?

Sure, I might break my ankle someday, die of exposure, and have my bones scattered by wild animals. Who cares? It would be a good death. It’s worth it.

The scenery up here is so spectacular that I almost didn’t feel the pain. Almost. On more than one occasion, while gazing at the endless shades of blue the pristine waters of Lake Tahoe offered, I tripped on my snowshoes.

Once, I landed on some tree roots, which cut right through to the bone in my left forearm. I managed to stop the bleeding by tying off a tourniquet with my teeth. When I got home, I then soaked the wound in Jack Daniels to ward off infection. It works every time! (see pics below). In a pinch, Stolichnaya Vodka works just as well. It’s an old combat first-aid trick.

While hiking along the East Ridge, succeeding mountain ranges in northern Nevada explored every shade of purple. I managed to summit each major peak around the body of water the Washoe Indians called “da-ow-a-ga”, or edge of the lake, which they considered the origin of the universe. Those included Squaw Peak (8,885), Mt Tallac (9,735 feet), Monument Peak (10,067), and Mount Rose (10,776 feet). When the trail got too steep, my trusty ice ax and crampons saw me through.

I was constantly reminded that I was in the “Old West” by the many artifacts I encountered. Prominent granite boulders displayed prehistoric Indian petroglyphs. I found a few abandoned log cabins, complete with potbelly stoves and canned food from the 1850s. Rusted-out cast iron mining equipment was strewn about everywhere, covered with snow. Along the old Pony Express Trail, one finds old horseshoes and the occasional ancient bottle turned purple by the sun.

Lake Tahoe supplied all the water and bracing wood for the Comstock silver mining boom of the 1870s. A hundred years ago, not a single tree was left standing, except for the southwest section of the lake owned by mining baron “Lucky Baldwin” who won it in a card game and made it his private retreat. It was all covered in meticulous and colorful detail for the Virginia City newspaper, The Territorial Enterprise, by a budding young newspaperman who went by the name of Mark Twain.

My ambitious goals often saw me hiking well into darkness. After the batteries died on my three backup headlamps, that flashlight app on the iPhone 5s proved a real lifesaver. It’s good for a full hour and illuminates the eyes of onlooking wildlife a bright yellow up to 200 yards away.

One night, I got back to the car and found that my keys had frozen and were useless. So, I sat on them. In 15 minutes, the car flashed its lights, and the doors magically opened. There was barely enough charge to get the engine started, a trick I accomplished by holding the key right up to the ignition button. Toyota designs them to do this. It’s no fun getting stranded at 10,000 feet at 10 degrees in the middle of nowhere. No Auto Club here!

I often looked behind to make sure a mountain lion was not stalking me. Don’t worry. Only 20 people have been killed by mountain lions in California over the last 100 years. More are killed by their pet dogs every year in the Golden State, mostly by pit bulls. Besides, I am good at staring down mountain lions and black bears. It is just a matter of attitude.

The old souvenir stand for the Ponderosa Ranch, of the TV series Bonanza fame, is now the Tunnel Creek Station Café and mountain bike rental. Good luck to Patty and Max! The nearby Flume Trail offers some of the best cross-country skiing in the world.

Of course, I am not just thinking Great Thoughts during these hikes. An endless series of economic and market data points are constantly churning around in the back of my mind, and I occasionally reach a “Eureka” moment. I keep a pen and notebook in my pack so I don’t forget these earth-shaking revelations.

It was during a similar expedition up the face of the Matterhorn in the Swiss Alps (14,692 feet) last summer when I realized that the S&P was beginning a long run up that would take it to 6,000 by yearend. I’ll never forget the expression on my guide’s face when I stopped midpoint through an abseil and started feverishly writing notes. That little maneuver cost me a bottle of schnapps. The readers and Trade Alert followers prospered mightily.

What is this year’s “Eureka” conclusion? The stock market could keep going up into 2025 but with more volatility. This year was a cakewalk, as my 69.3% trailing return testifies. After that, stocks will be unable to ignore the consequences of a Trump election.

I have been doing this sort of thing since I was 22 and was in somewhat better shape. Then, I was one of the few foreigners attending karate school in Japan, learning the iron discipline and focus of samurai warriors, known as “bushido”. The actor, Steven Segal, studied at a competing school down the street.

Every February, we underwent “kangeiko”, or “winter training. This involved the entire class running the five miles around Tokyo’s Imperial Palace in a pack, suffering freezing temperatures, barefoot, every day for a week. When we returned to the dojo, we were hosed down with ice-cold water, our feet senseless, bloody stumps. Then we would train for three more hours.

The idea was that the extreme pain and exhaustion would deliver insights into us and the world at large. It worked. At least one current reader endured the experience with me and is still alive. Remember that, David? By the way, thanks for knocking out my front teeth.

On the way home, I stopped in Sacramento for a well-deserved double cheeseburger, fries, and chocolate shake at In and Out Burger. You can’t take this diet and health thing too seriously. Snowshoe Thompson would have envied me.

Well, next week, it is back to normal. I’ll be glued in front of my screens, scouring the planet for the next great trading opportunity, although I’m not sure I’ll find many. Buying market tops is against my nature. What are you supposed to do when all of your forecasts and predictions come true? I have a feeling that the answer is not to make more forecasts and predictions.

Perhaps the right answer is to take another hike. Anyone care to join me?

Your Intrepid Reporter

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2013/12/John-Thomas-Hiking.jpg321426april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-11-11 09:02:442024-11-11 11:22:56The Market Outlook for the Week Ahead, or S&P 500 6,000 Target Achieved

Below, please find subscribers’ Q&A for the November 6 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

Q: What do we do in the market now in view of the Trump Victory?

The driving theme of the market has completely changed overnight. Falling interest rate plays are dead. The new theme is deregulation. The good news is that there are a lot of cheap deregulation plays out there, especially in financials. Deregulation is also a factor with (NVDA), where the government was lining up for an antitrust suit. New nuclear stocks like (CCJ) and (VST) also do well with a lighter regulatory touch.

Q: How will the defense industry perform under Trump?

A: Poorly. If we cease supplying Ukraine with weapons and withdraw from our international commitments, there’s no need for weapons at all. We’ll just have to be happy with the 50-year-old weapons that we have right now. And, of course, that's one of the reasons why Putin was such a big supporter of Trump. Avoid (LMT) and (RTX). Other stocks were already selling off as Trump rose in the polls.

Q: Will housing be a loser with the housing shortage?

A: Yes, it will, because you won’t find home buyers if they don’t have any money—if interest rates and mortgage payments are too high, those buyers are absent from the market. They can’t afford to step up to the current price levels and mortgage levels.

Q: Do you really think the Fed may not cut interest rates?

A: All of the announced Trump policies are highly inflationary, and one of the Fed’s primary missions is to control inflation. But, it comes down to: is the Fed going to look forward or look back? Historically, it is very much a “look back” organization, so they will probably wait on their higher interest rates. And that is what uncertainty is all about; all of a sudden, you go from very firm convictions of what’s going to happen next—what stocks to buy, what sectors to play—to “I don’t know!”. With a Harris win, at least you had some certainly. With Trump, we don’t know what he really wants to do, can do, or be allowed by the courts. It will take time to figure all this out.

Q: Why did none of these issues occur during Trump’s first term?

A: Well, virtually all of Trump’s first term, interest rates were at zero because the Fed was still doing quantitative easing, trying to recover from the ‘08 financial crisis, but also recovering from the pandemic. The amazing thing about the Biden administration is that the stock market did so well during the 5% interest rates that prevailed practically for his entire term.

Q: Do you have a “BUY” target for iShares 20+ Year Treasury Bond ETF (TLT) on the downside after the Trump win?

A: The answer is we are going to retest the low of the year, which is $82 in the TLT, and last time I checked, we were at $89.78—so down seven points. But again, we now have a lame-duck government, so no dramatic action with a split Congress. We basically have until January 20th, when the new government comes in, to find out what they will actually try to do. I think you'll find that the “campaign Trump” and the “in-office Trump” are two totally different people.

Q: Okay, what about the iShares 20+ Year Treasury Bond ETF (TLT) LEAPS position you put out two weeks ago? Should we sell or hold?

A: Well, if you want to be cautious, go cash—sell. But this is a LEAPS that has another 15 months to expiration, and there's a pretty decent chance we'll be going into recession sometime next year, especially if interest rates and inflation take off. That could make your LEAPS trade very attractive—it could drive interest rates down to 3.5%, which is virtually where they were in September. Since September, bonds have basically given up their entire rally for the year on the possibility of a Trump win. So, you know, would I put on that trade today? No. Will I put it on at $82, I probably will. We'll just have to see what the new world looks like.

Q: What's the direction for gold (GLD) and silver (SLV)?

A: Down. Those two plays were dependent on falling interest rates, which are now gone. Now that they're going back up again, it kind of trashes the entire gold-silver trade. So, at some point, gold will drop to a point where the flight to safety bid offsets the fear of rising interest rates. You still have a lot of Chinese savings in gold going on and central bank buying. That's where you get back in. Where that is is anybody's guess.

Q: Any thoughts on Crown Castle International (CCI)?

A: It is an interest-rate play. We did really well with CCI from April to September, when the 10-year treasury went from 4.5% to 3.5%. Run that movie in reverse, and it doesn't do very well. We've had a big sell-off on (CCI) this morning. So it's getting killed on the prospect of rising rates and inflation.

Q: Do smaller stocks do better under Trump?

A: No. Smaller stocks are much more dependent on interest rates than large stocks because they're very heavy borrowers at high rates. So, any rally there should be sold into.

Q: Should I bet the ranch on crypto here?

A: Absolutely not. $6,000 is where you should have bet the ranch on crypto, not at $75,000. Crypto is barely moving today, despite promises by Trump to completely deregulate the sector. So, no, I am definitely not a buyer of crypto here.

Q: What about the gold trade alert that I sent out yesterday?

A: That was on the assumption that Harris would win, and she didn't. If you want to be conservative, get out of the position now. We have five weeks to expiration on that position, so it really depends on where gold finds its bottom—it could hold up here or a little bit lower, and we'll still be at the max profit. If we go into free fall, I'm going to just stop out of the position and write that one off as me being too aggressive before the election when I had the perfect positions going into it, being long JP Morgan (JPM) and Nvidia (NVDA).

Q: Is the Occidental Petroleum (OXY) spread okay?

A: For energy, I would say yes, probably. But we'll have to see how sustainable this current rally is.

Q: So, wait on the currency plays, like (FXA), (FXE), (FXB), and (FXC)?

A: Absolutely, yes. It's another wait for the dust to settle trade.

Q: What will the price of crude oil do from here?

A: Probably go down more with large new supplies coming out of the U.S.

Q: Why are financial stocks up huge?

A: Deregulation. Financials are among the most regulated industries in the world. If you don't believe me, try running a hedge fund someday, where they're breathing down your neck every five seconds for audits, reports, and so on. They also win on the revenue side with restrictions coming off mergers and acquisitions with the end of antitrust enforcement.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE IS YOUR POST-ELECTION PORTFOLIO

plus THE LAST SILVER BUBBLE)

(NVDA), (META), (CRM), (TLT), (JNK), (CCI), (DHI), (LEN), (PHM),

(GLD), (SLV), (NEM), (FXE), (FXB), (FXA), (TSLA), (JPM),(BAC), (GS)

The world was supposed to end at midnight on December 31, 1999 because computers would be unable to cope with the turnover of the new millennium. I remember making presentations to big hedge funds, predicting that Y2K was a big nothing burger and, worst case, somebody’s toaster wouldn’t work.

I spent that New Year’s Eve with my kids at Disneyland in Orlando, watching one heck of a fireworks display. What happened the next morning? Even the toasters worked.

I think we are setting up for another Y2K outcome, except that this time, it’s the presidential election that has everyone in a tizzy.

The polls are tied at 48%-48% with a margin of error of 4%. In fact, for the last 50 years, the opinion polls have been wrong by an average of 3.4%. One side already has that 3.4% and probably more, plus all seven battleground states, but we won’t know for sure until November 6.

As an investment manager, it is not my job to pick a side or impose my view upon you but to deliver the best possible investment returns for my clients.

And let me tell you how.

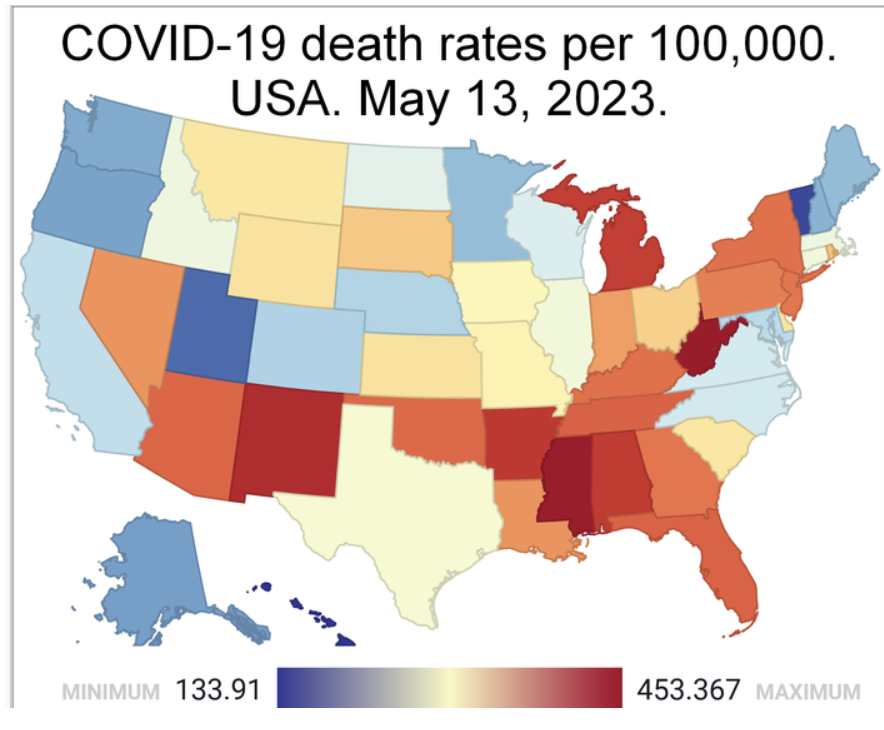

Remember the Pandemic? Four years after the event, we now have the luxury of copious hard data. Out of 103,436,829 cases, some 1,203,648 Americans died, or 1.3%. But, the death rate in red states was much higher than in blue states.

For example, California suffered only 101,159 deaths out of a population of 39,128,162 for a death rate of 0.26%. Florida saw 86,850 deaths out of a population of 22,634,867 for a death rate of 0.38%. Deaths in Florida were 68% higher in the Sunshine State than in the Golden State.

Florida, in effect, traded lives for business profits. Florida also had a Typhoid Mary effect in that by staying open for spring breaks and vacations; it increased the death rates in surrounding red states.

Assume that half of those who died were voters and apply this math to the entire country, and Republicans lost 393,059 votes to the pandemic compared to only 268,935 for Democrats. Some 124,125 more Republican voters died than Democrats. Is 124,125 votes enough to decide this election?

Absolutely!

In the 2020 presidential election, Biden won the three battleground states of Georgia by the famous 11,779 votes, Arizona by 10,457 votes, and Nevada by 33,596 votes. That’s 33 electoral college votes right there out of 270 needed.

The opinion polls have missed these numbers by a mile because their algorithms don’t take the pandemic into consideration. They are counting dead voters, while the actual election polls only count live ones. I predict that the opinion polls will be spectacularly wrong….again.

Of course, these are back-of-the-matchbook ballpark calculations. I’ll leave it to some future aspiring PhD candidate to research his thesis with more precise figures. I have better things to do.

So, how do we make money off of all this? I have never seen investors so underweight and cautious going into a major risk event like this election. They have been scared out of the market by the media. Therefore, I expect the stock market to rise by 10% after the election, taking the S&P 500 as high as 6,400.

Let the great chase begin!

Here is your model portfolio for the rest of 2024.

(NVDA), (META), (CRM) – Underweight fund managers will chase this year’s best performers so they can look good at yearend. Similarly, they will dump their worst performers in the energy sector. So will individual investors for tax loss harvesting.

(TLT), (JNK), (CCI) – All interest rate plays make back recent losses as the threat of $10-$15 trillion in new borrowing by a future president, Trump, disappears.

(DHI), (LEN), (PHM) – There is no better interest rate play than new homebuilding. It’s tough to beat a structure shortage of 10 million homes.

(GLD), (SLV), (NEM) – Precious metals also do very well as they have less yield competition from other interest rate plays. These have become the principal savings vehicle for Chinese individuals.

(FXE), (FXB), (FXA) – A falling interest rate advantage for the US dollar means you want to buy all the currencies.

(JPM), (BAC), (GS) – Banks also do exceedingly well in a falling interest rate environment, and brokers and money managers will cash in on exploding stock market volume.

Also, on November 6, your toaster will probably still work. And I will never understand why the Center for Disease Control never accepted my application out of college. So, I went to Vietnam instead.

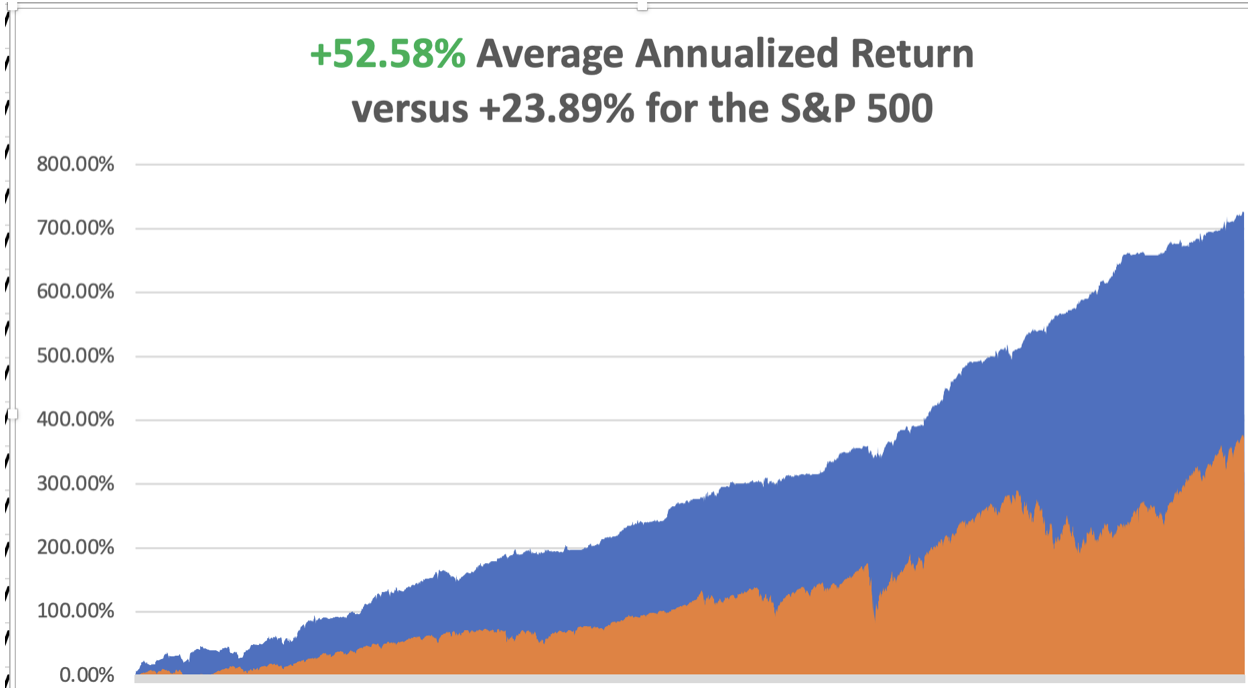

So far in October, we have gained a breathtaking +5.46%.My 2024 year-to-date performance is at an amazing+50.70%.The S&P 500 (SPY) is up +21.38%so far in 2024. My trailing one-year return reached a nosebleed +66.31. That brings my 16-year total return to +727.33%.My average annualized return has recovered to +52.58%.

I am remaining cautious with a 70% cash, a 20% long, and a 10% short. I maintained two longs in (GLD) and (JPM) that are well in the money. I sold short (TSLA) to take advantage of a massive 29% gain in two days off the back of blockbuster earnings.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 61 of 81 trades have been profitable so far in 2024, and several of those losses were really break evens. Some 16 out of the last 19 trade alerts were profitable. That is a success rate of +75.30%.

Try beating that anywhere.

New Home Sales Jumped 4.1% in September at 738,000 seasonally adjusted units on a signed contract basis. The median home price rose to 426,300. This despite a roller coaster month on interest rates, falling to 6.0% for the 30-year, then jumping back up to 7.0%.

Fusion is going Commercial in San Francisco, with a German company, Focused Energy, making a $65 million investment. The firm will draw heavily from staff from nearby Lawrence Livermore National Labs, which achieved a net energy gain for the first time in 2022. Focused Energy is one of eight companies given grants to accommodate a doubling of power demand by 2050. Commercial fusion will be the next big thing, where three soda cans of heavy hydrogen can power San Francisco for a day.

Money Market Funds See Massive Pre-Election Inflows, as investors see to avoid promised post-election violence. According to LSEG data, investors acquired a net $29.98 billion worth of money market funds during the week, posting their fourth weekly net purchase in five weeks. Personally, I think it is another Y2K moment.

Tesla Earnings Shock to the Upside, with both third-quarter profits and margins topping estimates. Elon Musk said that he expects 20% to 30% vehicle growth next year, sending the company's shares up 11% in post-market trading. The company still sees 2025 production of a cheaper model, maybe the Model 2. The Cybertruck has reached profitability for the first time and is reaching mass production. Tesla will see “slight growth” in deliveries this year. I am using the spike in the share price to take profits on my long to avoid election risk.

Apple iPhone Sales are Lagging, according to a leading analyst, with a drop in 10 million orders expected, down to 84 million units. The stock dropped 4% from an all-time high.

Boeing Reports $6 Billion Loss, a disastrous report from a dying company with awful management. This is going to be a very long-term workout. A strike resolution may market the bottom. Avoid (BAC) like a stalling airplane.

Newmont Mining Dives 7% after missing Wall Street expectations for third-quarter profit on Wednesday. Higher costs and lower production in Nevada took the shine away from a rise in total output. Newmont said that its costs rose due to planned maintenance at the Lihir project in Papua New Guinea — which it acquired following a $17 billion buyout of Newcrest — and higher expenditure for contract services across its portfolio. Buy (NEM) on dips.

McDonald's Kills Two in E.Coli Outbreak, linked to quarter pounders sold in Colorado and Nebraska. The stock dropped 10%. It’s clearly a supply chain problem. Given their vast size, with 45,000 stands in 100 countries, it’s amazing that this doesn’t happen more often. Avoid (MCD).

Bonds Plunge Anticipating a Trump Win, with the (TLT) down $10 from the recent high. If he does win, expect another $10 decline to $82. If Harris wins, expect a $10 rally. This is the best election trade out there.

Nvidia Tops $3.5 Trillion, as the shares hit a new all-time high at $144.45. It looks like it’s on a run to $150, then $160. Earnings are about to double when reported on November 20. Before then, investors will get some insight into demand for Nvidia’s newest Blackwell chips with earnings reports from big technology companies, including Microsoft (MSFT) coming at the end of this month. Buy (NVDA) on dips.

Hedge Funds Pour into Technology Stocks, such as semiconductors and hardware, at the fastest in five months amid the start of the third-quarter earnings season, according to Goldman Sachs on Friday. Outside the U.S., diverging reports from chipmaker Taiwan Semiconductor Manufacturing (TSM) and chipmaking equipment supplier ASML Holding (ASML) in opposite directions while investors await semiconductor companies such as Advanced Micro Devices (AMD) and Nvidia (NVDA) to unveil their earnings as they seek a trend. They are betting on a big post-election move-up.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy is decarbonizing, and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000, here we come!

On Monday, October 28 at 8:30 AM EST, the Dallas Fed Manufacturing Index is published. On Tuesday, October 29 at 6:00 AM, the S&P Case Shiller National Home Price Index is out. We also get the US JOLTS Job Openings Report. Alphabet (GOOGL) and (AMD) report.

On Wednesday, October 30 at 11:00 AM, the ADP Employment Change Report is printed. (META) and (MSFT) report.

On Thursday, October 31 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the US Core PCE Price Index. (AMZN) reports.

On Friday, November 1 at 8:30 AM, the October Nonfarm Payroll Report is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, with silver on fire once again and at 12-year highs, I thought I’d recall the last time a bubble popped for the white metal. I picked up this story from my late friend Mike Robertson, who ran the Dallas-based Robertson Wealth Management, one of the largest and most successful registered investment advisors in the country.

Mike is the last surviving silver broker to the Hunt Brothers, who in 1979-80 were major players in the run-up in the “poor man’s gold” from $11 to a staggering $50 an ounce in a very short time. At the peak, their aggregate position was thought to exceed 100 million ounces.

Nelson Bunker Hunt and William Herbert Hunt were the sons of the legendary HL Hunt, one of the original East Texas wildcatters and heirs to one of the largest Texas fortunes of the day. Shortly after President Richard Nixon took the US off the gold standard in 1971, the two brothers became deeply concerned about financial viability of the United States government. To protect their assets, they began accumulating silver through coins, bars, the silver refiner, Asarco, and even tea sets, and when it opened, silver contracts on the futures markets.

The brother’s interest in silver was well-known for years, and prices gradually rose. But when inflation soared into double digits, a giant spotlight was thrown upon them, and the race was on. Mike was then a junior broker at the Houston office of Bache & Co., in which the Hunts held a minority stake and handled a large part of their business.The turnover in silver contracts exploded. Mike confesses to waking up some mornings, turning on the radio to hear silver limit up, and then not bothering to go to work because they knew there would be no trades.

The price of silver ran up so high that it became a political problem. Several officials at the CFTC were rumored to be getting killed in their personal silver shorts. Eastman Kodak (EK), whose black and white film made them one of the largest silver consumers in the country, was thought to be borrowing silver from the Treasury to stay in business.

The Carter administration took a dim view of the Hunt Brothers’ activities, especially considering their funding of the ultra-conservative John Birch Society. The Feds viewed it as an attempt to undermine the US government. The proverbial sushi hit the fan.

The CFTC raised margin rates to 100%. The Hunts were accused of market manipulation and ordered to unwind their position. They were subpoenaed by Congress to testify about their motives. After a decade of litigation, Bunker received a lifetime ban from the commodities markets, a $10 million fine, and was forced into a Chapter 11 bankruptcy.

Mike saw commissions worth $14 million in today’s money go unpaid. In the end, he was only left with a Rolex watch, his broker’s license, and a silver Mercedes. He still ardently believes today that the Hunts got a raw deal and that their only crime was to be right about the long-term attractiveness of silver as an inflation hedge. Nelson made one of the greatest asset allocation calls of all time and was punished severely for it. There never was any intention to manipulate markets. As far as he knew, the Hunts never paid more than the $20 handle for silver and that all of the buying that took it up to $50 was nothing more than retail froth.

Through the lens of 20/20 hindsight, Mike views the entire experience as a morality tale, a warning of what happens when you step on the toes of the wrong people.

The white metal’s inflation-fighting qualities are still as true as ever, and it is only a matter of time before prices once again take another run to the upside.

Unfortunately, Mike won’t be participating in the next silver bubble. Suffering from morbid obesity, he died from a heart attack a decade ago.

Silver is Still a Great Inflation Hedge

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/10/man-with-glasses.png606468april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-28 09:02:442024-10-28 11:23:59The Market Outlook for the Week Ahead, or Here is your Post Election Portfolio

Below, please find subscribers’ Q&A for the October 23 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

Q: What the heck is happening with the iShares 20+ Year Treasury Bond ETF (TLT)? It keeps dropping even though interest rates are dropping. It seems to be an anomaly.

A: It is. What’s happening is that bonds are discounting a Trump win, and Trump has promised economic policies that will increase the national debt by anywhere from $10 to $15 trillion. Bonds don’t like that—you borrow more money through bonds, and the price goes up. Interest rates could go as high as 10% if we run deficits that high (at least the bond market may go that low.) On the other hand, stocks are discounting a Harris win. Stocks went up 60% over the last four years. I did roughly double that. And a Harris win would mean basically four more years of the same. So stocks have been trading at new all-time highs almost every day until this week when the election got so close that the cautious money is running to the sidelines. So what happens if there's a Harris win?Bonds make back the entire 10 points they lost since the Fed cut interest rates. And what happens if Trump wins? Bonds lose another 10 points on top of the 10 points they've already lost. Someone with a proven history of default doesn't exactly inspire confidence in the bond market. So that is what's going on in the bond market.

Q: Will the US dollar continue its run into year-end?

A: No, I have a feeling it’s going to completely reverse in two weeks and, give up all of its gains, and resume a decade-long trend to new lows. So, I think everything reverses after election day. Stocks, bonds, commodities, precious metals—the only thing that doesn't is energy, and that keeps going down because of global oversupply that even a Middle Eastern war can’t support.

Q: Are you expecting a major correction in 2025?

A: I am, actually. We basically postponed all corrections into 2025 and pulled forward all performance in 2024. So, I think we could get at least a 10% correction sometime next year, and that is normal. Usually, we get a couple of them. This year, we only got the one in July/August. So, back to normal next year, which means smaller returns from the stock market. In fact, smaller returns from everything except maybe gold and silver. This is why they're going up so much now.

Q: Are you discounting a huge increase in the deficit under Biden-Harris?

A: No, the huge increase in the deficit is behind us because we had all the pandemic programs to pay for, and if anything, technology inflation should go down because of accelerating technology. We're already seeing that in many industries now, so I don't think there'll be any policy changes under Harris, except for little tweaks here and there. All the big policies will remain the same.

Q: What is a dip?

A: A dip is different for every stock and every asset class. It depends on the recent volatility of the underlying instrument. You know, a dip in something like McDonald's (MCD) or Berkshire Hathaway (BRK/B) might be 5%, and a dip in Nvidia (NVDA) might be 15 or 20%. So, it really depends on the volatility of the underlying stock, and no two volatilities are alike.

Q: What are your top picks on nuclear?

A: Well, we've been in Cameco (CCJ), the Canadian uranium company, since the beginning of the year, and it has doubled. Vistra Corp (VST) is another one, and there are many more names after that.

Q: What are your thoughts on Toyota (TM)?

A: I love Toyota for the long term. The fact that they were late into EVs is now a positive since the EV business is losing money like crazy. They're the ones who really pioneered the hybrid business, and I’ve toured many of their factories in Japan over the years. Great company, but right now, they're being held back by the slow growth of the Japanese economy.

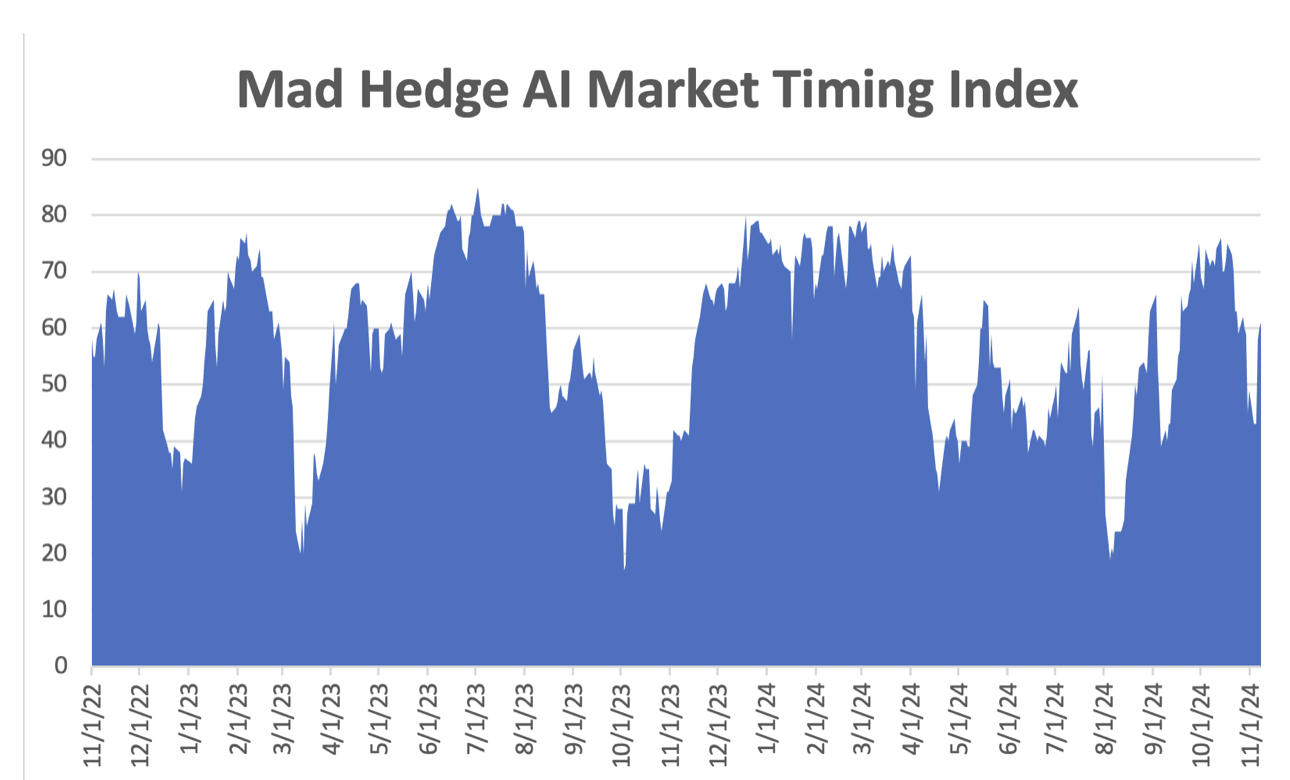

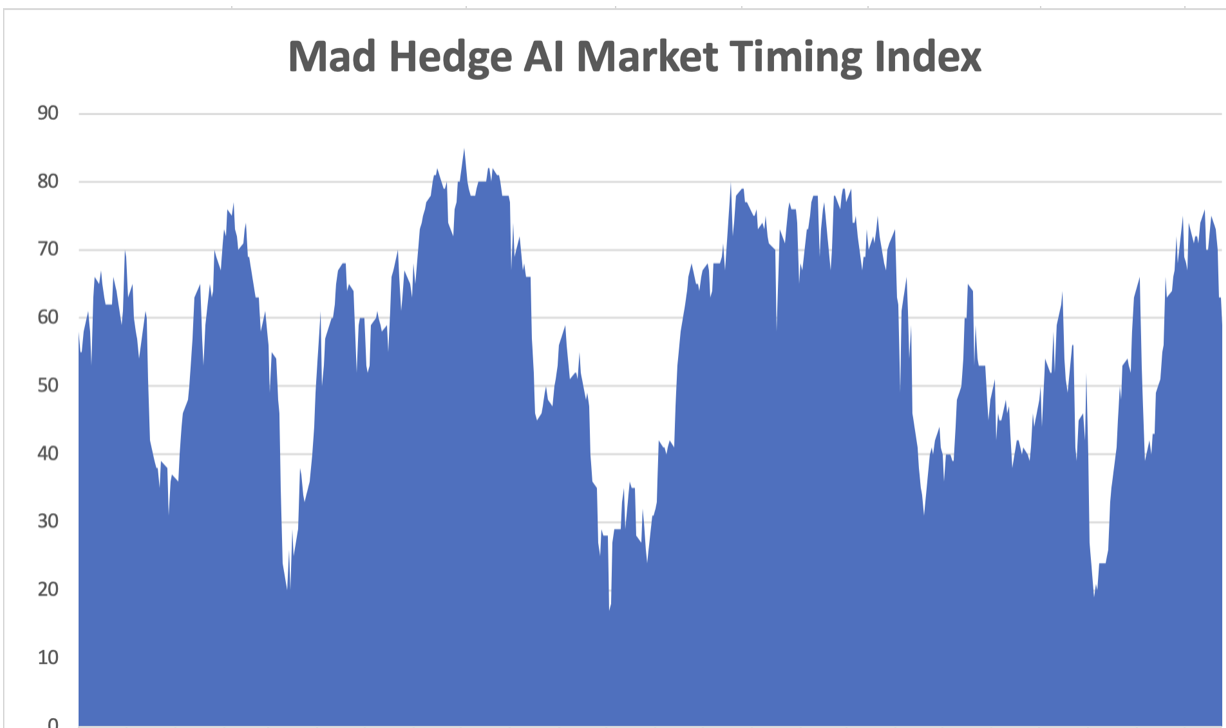

Q: Market timing index says get out. We're heading into the seasonally bullish time of the year. Should we be in or out over the next two months?

A: I would be in as long as you can handle some volatility around the stock market. When the market timing index is at 70, that means any new trades that you initiate have a 30% chance of making money. Now, they can sit at highs sometimes for months, and it actually did that earlier this year. Markets can get overbought and stay overbought for months, and that is a really difficult time to trade. If you're a long-term investor, you just ignore all of this and just stay in all the time.

Q: Silver has broken out; what's next?

A: Silver had had a massive run since the beginning of September—some 30%. We're up to about $31/oz. The obvious target for silver is the last all-time high, which I think we did 40 years ago, and that was at $50/oz. So there's another easy 60% of upside in silver. That's why I put out a LEAPS on the 2x long silver play (AGQ), and people are already making tons of money on that one. I think Silver will be your big performer going forward.

Q: Too late to invest in Chinese stocks?

A: No, it's selling off again. IT Could retest the lows, especially if the government sits on its hands for too long with more stimulus packages.

Q: Is big tech still a good bargain buy?

A: I would take “bargain” out of that. The rule on tech investing is you're always buying expensive stuff because the future always has a spectacular outlook. So, tech investing is all about buying something expensive that gets more expensive. This is exactly what tech stocks have been doing for the last 50 years, so it's not exactly a new concept. I know tons of people who never touched Nvidia (NVDA) or Tesla (TSLA) because it was too expensive. (NVDA) was too expensive when it was $2, and now it's even more expensive at $140 or, in Tesla's case, $260.

Q: Will Tesla (TSLA) go up or down tonight?

A: I have no idea. Anybody else who says they have an idea is lying. You go to timeframes that short, and you are subjecting yourself to random chance; even the weather could affect your position by tomorrow.

Q: How uncomfortable is the stem cell extraction?

A: Extremely uncomfortable. If they say it won't hurt a bit, don't believe them for a second. They take this giant needle hammer it into your backbone to get your spinal fluid (and I count the hammer blows.)Last time, I think I got up to 50 before I couldn't take the pain anymore, and they extracted the spinal fluid to get the stem cells. So, for those who don't tolerate pain very well, this is absolutely not for you.

Q: Why is Intel (INTC) stock doing so badly this year?

A: Low-end products, no new products, poor manager. Whenever a salesman takes over a technology company, you want to run a mile. That's what happened at Intel because they have no idea how the technology works.

Q: Should I sell my Philip Morris (PM) stock? It's just had a huge run-up.

A: No. For dividend holders, this is the dream come true. They pay a 4.1% dividend. This was a pure dividend play ever since the tobacco settlement was done 40 years ago. Then they bought a Swedish company that has these things called tobacco pouches, and that has been a runaway bestseller. So, all of a sudden, the earnings at Philip Morris are exploding. The dividend is safe. I think Philip could go a lot higher, so buy PM on dips. And I will dig into this story and try to get some more information out of it. I love high growth high dividend plays.

Q: What's the best play for silver?

A: I'm doing the ProShares Ultra Silver (AGQ), which is a 2x long silver and has gone from $30 to $50 since the beginning of September. If you want to sleep at night (of course, I don't need to), then you just buy the iShares Silver Trust (SLV), which is a 1x long silver play and that owns physical silver. I think it's held in a bank vault in London.

Q: Time to sell Copper (FCX)?

A: Short term, yes, as China weakens. Long-term, hang on because we are coming into a global copper shortage, and that'll take the price of copper up to $100 or (FCX) up to $100. So yes, love (FCX) for the long term. Short term, it has a China drag.

Q: Will inflation come back in 2025?

A: No, it won't. Technology is accelerating so fast, and AI is accelerating so fast it's going to cut costs at a tremendous rate. And that's why you're seeing these big tech companies laying off people hundreds at a time; it's because the low-end jobs have already been replaced by AI. There is a lot more of that to come. I'm not worried about inflation at all.

Q: Do you disagree with Tudor Jones on inflation?

A: Yes, I disagree with him heartily. Tudor Jones is talking his own book, which means he doesn't want to get a tax increase with a Harris administration. So he's doing everything he can to talk up Trump, and that isn't helping me with my investment strategy whatsoever. By the way, Tudor Jones is often wrong, you know; he made most of his money 30 years ago. And before that, it was when he was working for George Soros. So, yes, I agree with the man from Memphis. He’s in the asset protection business. You’re in the wealth creation business, a completely different kettle of fish.

Q: Do you hold the ProShares Ultra Silver (AGQ) overnight?

A: I've been holding my (AG for four months, and the cost of carry-on that is actually quite low because silver doesn't pay any dividend or interest. There really isn't much of a contango in the precious metals anyway—it's not like oil or natural gas. It’s a 3X plays that you really shouldn’t hold overnight.

Q: Where is biotech headed?

A: Up for the long term, sideways for the short term. That's because, after the election, risk on will go crazy. We could have a melt-up in stocks, and when that happens, people don't want to buy “flight to safety” sectors like Biotechs and healthcare; they want to buy more Nvidia. Basically, that's what happens. More Nvidia (NVDA), more Meta (META), and more Apple (APPL). They want to buy all the Mag7 winners. Well, let's call them the Mag7 survivors, which are still going up after a ballistic year.

Q: Any suggestions on where to park cash for five to six years?

A: 90-day T-Bills are yielding 4.75%. That would be a safe place to put it. And you might even peel off a little bit of that—maybe 10% — and put that into a junk fund, which is yielding 6%. You're still getting a lot of money for cash—but not for much longer. The golden age of the 90-day T-bill is about to end.

Q: BlackRock (BLK) keeps growing, trillions after trillions. Why is the stock so great at building value?

A: Because you get a hockey stick effect on the earnings. As the stock market goes up, which it always does over time, their fees go up. Plus, their own marketing brings in new money. So, you have multiple sources of income rising at a rapid pace. I'm kicking myself for not buying the stock earlier this year.

Q: How does any antitrust action by the government affect stock prices?

A: Short-term, it caps them. Long term, it doubles them because when you break up these big companies, the individual pieces are always worth a lot more than the whole. We saw that with AT&T (T), where you're able to sell the individual seven pieces for really high premiums. So, that's why I'm never worried about antitrust.

Q: Do dividend stocks provide little upward appreciation since they're paying investors already?

A: To some extent, that's true because low-growth companies like formerly Philip Morris (PM) and Altria (MO) had to pay high dividends to get people to buy their stock because the industries were not growing. AT&T is another classic example of that—high dividend, no growth. But that does set you up for when a no-growth company can become a high-growth company, and then the stocks double practically overnight. And that's what's happening with Philip Morris.

Q: Are you buying physical gold (GLD) and silver (SLV)?

A: I bought some in the 1970s when it was $34/oz for gold, and the US went off the gold standard, and I still have them. It's sitting in a safe deposit box in a bank I will not mention. The trouble with physical gold is high transaction costs—it costs you about 10% or more to buy and sell. It can be easily stolen—people who keep them hidden at home or have safes at home regularly get robbed. And what if the house burns down? You really can't insure gold holdings accept with very high premiums. So, I've always been happy buying the gold ETFs. The tracking error is very small unless you get into the two Xs and three Xs. Gold coins are good for giving kids as graduation presents—stuff like that. I still have my gold coins for my graduation a million years ago (and that was a really great investment! $34 up to, you know, $2,700.)

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

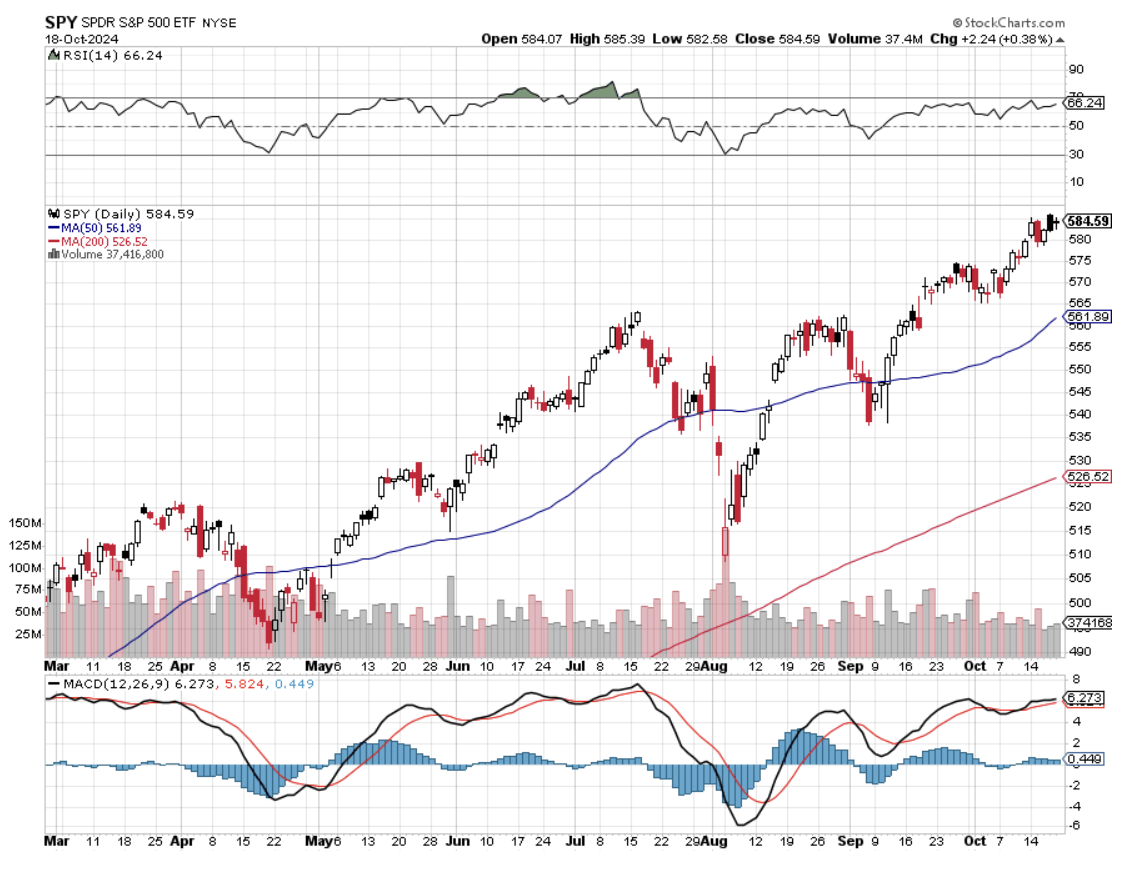

We are now nearly three months into an almost straight-up move in the stock market, and money managers everywhere are scratching their heads. We are now only 136 points or 2.32% from my yearend (SPX) target of 6,000, which is starting to look pretty conservative. The price-earnings multiple for the S&P 500 is now 21X, the Magnificent Seven 28X, and NVIDIA 65X.

I’ve seen all this before.

We are about as close to a perfect Goldilocks scenario as we can get. Interest rates and inflation are falling. A 3% GDP growth rate means the US has the strongest major economy and is the envy of the world. We have entered the euphoria stage of the current market move in almost all asset glasses. Gold (GLD) has gone up almost every day. Some big tech remains on fire. Energy prices are in free fall. Even bonds (TLT) are trying to put in a bottom.

Complacence is running rampant.

So, how the heck do we trade a market like this? You play the laggard trade.

The biggest risk to the gold trade is that it has gone up 40% in a year. So, what do you do? The response by traders has been to move into lagging silver (SLV) (AGQ), which has been on a tear since September.

Had enough with the Mag Seven? Then, rotate in the sub $1 trillion part of the market with Broadcom (AVGO), ASML Holdings NV (ASML), Micron Technology (MU), and Lam Research (LRCX).

Tired of watching your DH Horton (DHI) go up every day? Then, flip into smaller homebuilders like Pulte Homes (PHM) and Lennar (LEN).

And then there is the biggest laggard of all, the nuclear trade, which is just crawling out of a 40-year penalty box. With news that Amazon (AMZN) was planning to order up to eight Small Modular Reactors to power its AI efforts, all uranium plays continue to go ballistic. The proliferation of power-hungry data centers is driving the greatest growth of power needs since WWII and the Manhattan Project.

Fortunately, I got in early. This is a trend that could become the next NVIDIA, as the public stocks involved are coming off such a low base. I have personally interviewed the founders and examined Nuscale’s plans with a fine tooth come and consider them genius. The company is, far and away, the overwhelming leader in the sector. The puzzle for the pros who understand the technology is why it took so long. Buy (CCJ), (VST), (CEG), (BWXT), and (OKLO) on dips.

It's like everything is racing towards a key, even with an unknown outcome. There happens to be a big one coming up: the US presidential elections on November 6.

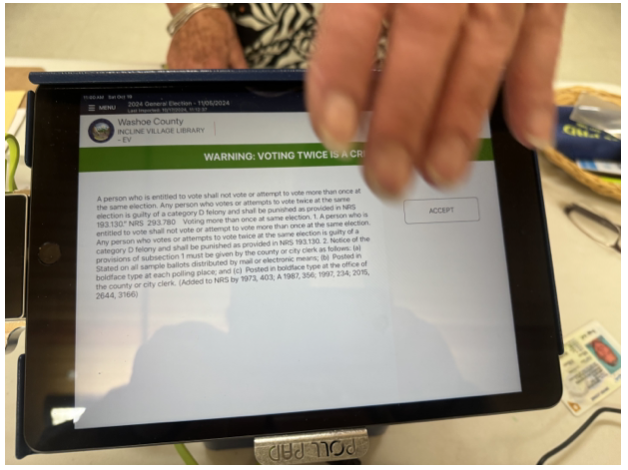

Speaking of elections, I took the time to participate in the first day of voting in Nevada on Saturday, October 19, at the Incline Village Public Library. I waited in line for two hours in a brisk and breezy 40 degrees. I wore my Marine Corps cap and Ukraine Army ID just to confuse people. Some got so tired of waiting in the cold that they went home, retrieved their mail-in ballots, and returned to the polls to drop them off.

I looked back on the line, and women outnumbered the men by three to one. Where did all these women come from? There used to be such a shortage of women at Lake Tahoe that it was impossible to get a date. Hunting, fishing, long-distance backpacking, and skiing weren’t used to attract such large numbers of the female gender. Maybe now they do? But now they’re driving up in Mercedes AMG’s and Range Rovers.

When I finally arrived at the front of the line, I was asked to sign an agreement with my finger, acknowledging that I knew it was illegal to vote twice. The poll worker noticed my ID. When I explained what it was in the Cyrillic alphabet, she burst into tears, apologized, and said she had goosebumps all over.

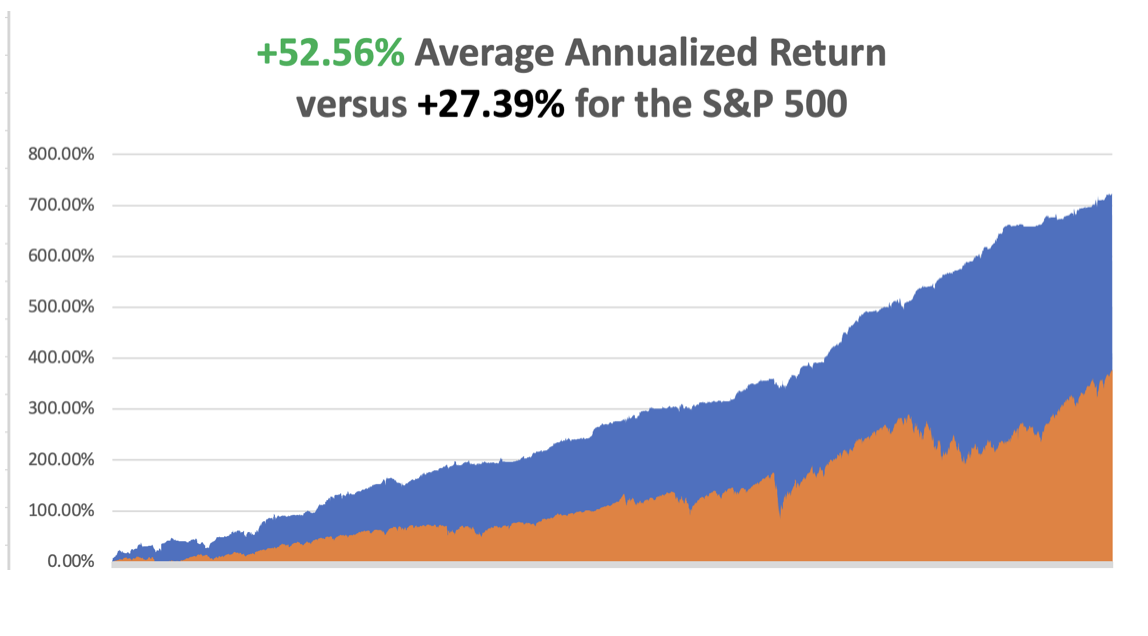

It was another blockbuster week, up over 6%. So far in October, we have gained +4.89%.My 2024 year-to-date performance is at +50.13%.The S&P 500 (SPY) is up +22.43%so far in 2024. My trailing one-year return reached a nosebleed +65.90. That brings my 16-year total return to +726.76%.My average annualized return has recovered to +52.56%.

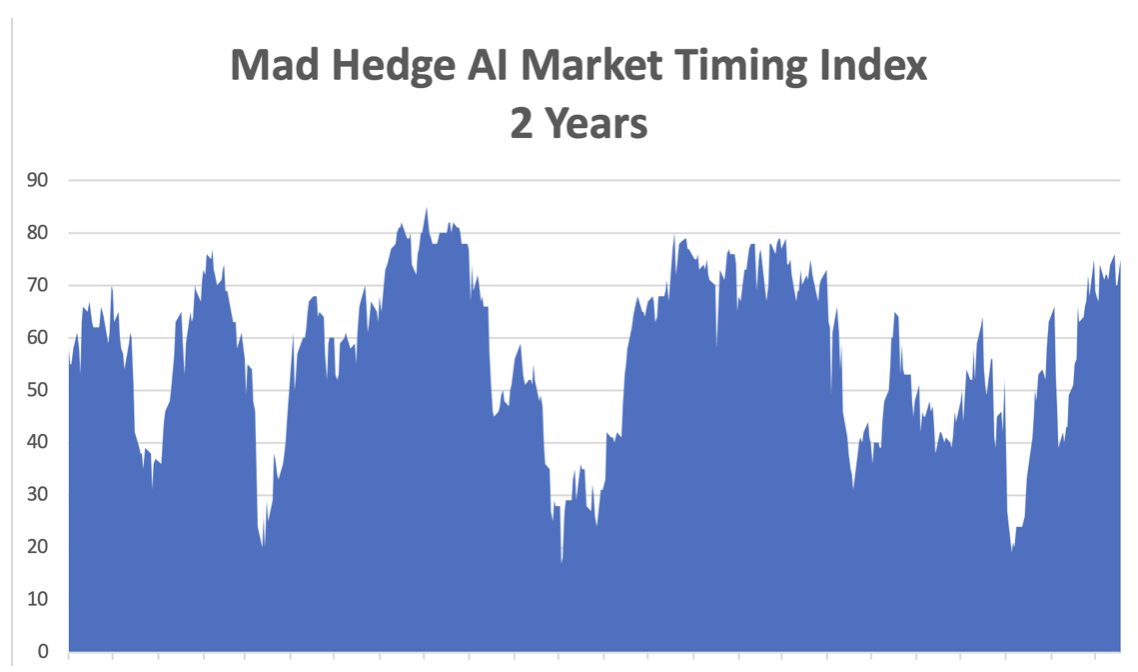

With my Mad Hedge Market Timing Index at the 70 handles for the first time in five months, I am remaining cautious with a 70% cash and 30% long. I look for a small profit in (TSLA) to reduce risk. Two of my positions expired at their maximum profit point for (NEM) and (DHI) on Friday, October 18 options expiration.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 60 of 80 trades have been profitable so far in 2024, and several of those losses were really break-even. Some 16 out of the last 19 trade alerts were profitable. That is a success rate of +75.00%.

Try beating that anywhere.

Risk Adjusted Basis

Current Capital at Risk

Risk On

(TSLA) 11/$165-$175 call spread 10.00%

(JPM) 11/$195-$205 call spread10.00%

(GLD) 11/230-$235 call spread 10.00%

Risk Off

NO POSITIONS 0.00%

Total Net Position 30.00%

Total Aggregate Position 30.00%

Netflix Soars on Blockbuster Earnings, up 11% at the opening on a 5 million gain in subscribers. The company posted earnings per share of $5.40 for the period ended Sept. 30, higher than the $5.12 LSEG consensus estimate.

Crucially, Netflix saw momentum in its ad-supported membership tier, which surged 35% quarter over quarter. The streaming wars are over, and (NFLX) won. Buy (NFLX) on dips.

Silver is Ready to Break Out to the Upside after a year-long-range trade. The white metal is a predictor of a healthy recovery and a solar rebound. It’s a long overdue catch-up with (GLD). Buy (AGQ) on dips.

Apple China Sales Jump 20% on the new iPhone 16 launch. Both Apple and Huawei's (HWT.UL) latest smartphones went on sale in China on Sept. 20, underscoring intensifying competition in the world's biggest smartphone market, where the U.S. firm has been losing market share in recent quarters to domestic rivals. Buy (AAPL) on dips.

Taiwan Semiconductor Soars on Spectacular Earnings, dragging up the rest of the chip sector with it. The world's largest contract chipmaker raised its expectation for annual revenue growth and said sales from AI chips would account for mid-teen percentage of its full-year revenue. U.S.-listed TSMC shares rose nearly 9%, and if gains hold, the company's market capitalization would cross $1 trillion. Buy (NVDA) on dips.

Weekly Jobless Claims Fall. Initial claims for state unemployment benefits dropped 19,000 last week to a seasonally adjusted 241,000 for the week ended Oct. 12, the Labor Department said on Thursday. Economists polled by Reuters had forecast 260,000 claims for the latest week. Claims jumped to more than a one-year high in the prior week, attributed to Helene, which devastated Florida and large swathes of the U.S. Southeast in late September.

Morgan Stanley Announces Blowout Earnings, fueling a 32% profit jump for the third quarter. Revenue from the trading business rose 13%. That followed gains recorded by its biggest rivals as the market business lifted fortunes across the industry, and a steady rebound in investment banking fees increased dealmaking. The wealth unit generated revenue of $7.27 billion, higher than analysts’ expectations, with $64 billion in net new assets. The unit boosted its pretax margin to 28%, driven by growth in fee-based assets. Buy (MS) on dips.

Global EV Sales Up 30% in September, with the largest gains in China. Gains in the U.S. market have been lagging in anticipation of the Nov. 5 election. Chinese carmakers are seeking to grow their sales in the EU despite import duties of up to 45% and amid cooling global demand for electric cars. Chinese and European automakers were going head-to-head at the Paris Car Show on Monday. Buy (TSLA) on dips.

Dollar Hits Two Month High on rising US interest rates. Ten-year US Treasuries have risen from 3.55% to 4.12% since the September Nonfarm Payroll Report. A string of U.S. data has shown the economy to be resilient and slowing only modestly, while inflation in September rose slightly more than expected, leading traders to trim bets on large rate cuts from the Fed. Buy all foreign currencies on dips (FXA), (FXE), (FXB), (FXY).

S&P 500 Value Gain Hits $50 Trillion, since the 1982 bottom, which I remember well and is up 50X. The index hit a record high Wednesday and is trading Thursday at around 5770, up 21% so far in 2024. The index’s value is up sixfold since it stood at $8 trillion at year-end 2008, near the depth of the bear market during the financial crisis.

JP Morgan Delivers Blowout Earnings. Its stock, trading around $223, was on course for its biggest daily percentage gain in 1-1/2 years.

(JPM)'s investment-banking fees surged 31%, doubling guidance of 15% last month. Equities propelled trading revenue up 8%, exceeding an earlier 2% forecast. These earnings are consistent with the soft-landing narrative of modest U.S. economic growth. Buy (JPM) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy is decarbonizing, and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000, here we come!

On Monday, October 21 at 8:30 AM EST, nothing of note takes placeis out. On Tuesday, October 22 at 6:00 AM, the Richmond Fed Manufacturing Index is out.

On Wednesday, October 23 at 11:00 AM, the Existing Home Sales is printed.

On Thursday, October 24 at 8:30 AM, the Weekly Jobless Claims are announced. We also get New Homes Sales.

On Friday, October 25 at 8:30 AM, the US Durable Goods Orders are announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I am headed out for early voting in Nevada this morning. It’s been a year since I came back from Ukraine badly wounded, so I thought I would recall my recollections from that time.

You know you’re headed into a war zone the moment you board the train in Krakow, Poland. There are only women and children headed for Kiev, plus a few old men like me. Men of military age have been barred from leaving the country since the Russians Invaded. That leaves about 8 million to travel to Ukraine from Western Europe to visit spouses and loved ones.

After a 15-hour train ride, I arrived at Kiev’s magnificent Art Deco station. I was met by my translator and guide, Alicia, who escorted me to the city’s finest hotel, the Premier Palace on T. Shevchenka Blvd. The hotel, built in 1909, is an important historic site as it was where the Czarist general surrendered Kiev to the Bolsheviks in 1919. No one in the hotel could tell me what happened to the general afterward.

Staying in the best hotel in a city run by Oligarchs does have its distractions. Thanks to the war, occupancy was about 10%. That didn’t keep away four heavily armed bodyguards from the lobby 24/7. Breakfast was well populated by foreign arms merchants. And for some reason, there are always a lot of beautiful women hanging around with nothing to do.

The population is definitely getting war-weary. Nightly air raids across the country and constant bombings take their emotional toll. Kiev’s Metro system is the world’s deepest and, at two cents a ride, the cheapest. It’s where the government hid out during the early days of the war. They perform a dual function as bomb shelters when the missile attacks become particularly heavy.

My Look Out Ukraine has duly announced every incoming Russian missile and its targeted neighborhood. The buzzing app kept me awake at night, so I turned it off. Let the missiles land where they may. For this reason, I reserved a south-facing suite and kept the curtains drawn to protect against flying glass.

The sound of the attacks was unmistakable. The anti-aircraft drones started with a pop, pop, pop until they hit a big 1,000-pound incoming Russian cruise missile, then you heard a big kaboom! Disarmed missiles that were duds are placed all over the city and are amply decorated with colorful comments about Putin.

The extent of the Russian scourge has been breathtaking, with an epic resource grab. The most important resource is people to make up for a Russian population growth that has been plunging for the last century. The Russians depopulated their occupied territory, sending adults to Siberia and children to orphanages to turn them into Russians. If this all sounds medieval, it is. Some 19,000 Ukrainian children have gone missing since the war started.

Everyone has their own atrocity story, almost too gruesome to repeat here. Suffice it to say that every Ukrainian knows these stories and will fight to the death to avoid the unthinkable happening to them. There will be no surrender.

It will be a long war.

Touring the children’s hospital in Kiev is one of the toughest jobs I ever undertook. Kids are there shredded by shrapnel, crushed by falling walls, and newly orphaned. I did what I could to deliver advanced technology and $10,000 in cash, but their medical system is so backward, maybe 30 years behind our own, that it couldn’t be employed. Still, the few smiles I was able to inspire made the trip worth it. This is the children’s hospital that was bombed a few months ago.

The hospital is also taking the overflow of patients from the military hospitals. One foreign volunteer from Sweden was severely banged up, a mortar shell landing yards behind him. He had enough shrapnel in him, some 250 pieces, to light up an ultrasound and had already been undergoing operations for months. It was amazing he was still alive.

To get to the heavy fighting, I had to take another train ride a further 15 hours east. You really get a sense of how far Hitler overreached in Russia in WWII. After traveling by train for 30 hours to get to Kherson, Stalingrad, where the German tide was turned, is another 700 miles east!

I shared a cabin with Oleg, a man of about 50 who ran a car rental business in Kiev with 200 vehicles. When the invasion started, he abandoned the business and fled the country with his family because they had three military-aged sons. He now works at a minimum-wage job in Norway and never expects to do better.

What the West doesn’t understand is that Ukraine is not only fighting the Russians but a Great Depression as well. Some tens of thousands of businesses have gone under because people save during war and also because 20% of their customer base has fled.

I visited several villages where the inhabitants had been completely wiped out. Only their pet dogs remained alive, which roved in feral starving packs. For this reason, my major issued me my own AK47. Seeing me heavily armed also gave the peasants a greater sense of security.

It’s been a long time since I’ve held an AK, which is a marvelous weapon. It’s it’s like riding a bicycle. Once you learned, you never forget.

I’ve covered a lot of wars in my lifetime, but this is the first fought by Millennials. They post their kills on their Facebook pages. Every army unit has a GoFundMe account where doners can buy them drones, mine sweepers, and other equipment.

Everyone is on their smartphones all day long, killing time, and units receive orders this way. But go too close to the front, and the Russians will track your signal and call in an artillery strike. The army had to ban new Facebook postings from the front for exactly this reason.

Ukraine has been rightly criticized for rampant corruption, which dates back to the Soviet era. Several ministers were rightly fired for skimming off government arms contracts to deal with this. When I tried to give $10,000 to the Children’s Hospital, they refused to take it. They insisted I send a wire transfer to a dedicated account to create a paper trail and avoid sticky fingers.

I will recall more memories from my war in Ukraine in future letters, but only if I have the heart to do so. They will also be permanently posted on the home page at www.madhedfefundtrader.com under the tab “War Diary”.

Donating $10,000 to the Children’s Hospital

On the Front at Crimea with a Dud Russian Missile

A Gift or Piroshkis from Local Peasants

One of 2,000 Destroyed Russian Tanks

The Battle of Kherson with my Unit

This Blown Bridge Blocked the Russians from Entering Kiev

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-21 09:02:412024-10-21 12:00:25The Market Outlook for the Week Ahead, or Complacence is Running Rampant

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.