Going against the market consensus has been working pretty well lately.

When the world prayed for a Santa Claus rally, I piled on the shorts. When traders expected a New Year January crash, I filled my boots with longs.

That’s how you earn an eye-popping 19.83% profit in a mere nine trading says, or 2.20% a day.

The other day, someone asked me how it is possible to get mind-blowing results like these. It’s very simple. Get insanely aggressive when everyone else is terrified, which I did on January 3. I also knew that with the Volatility Index (VIX) falling to $18, pickings would quickly get extremely thin. It was make money now, or never.

To quote my favorite market strategist, Yankees manager Yogi Berra, “No one goes to that restaurant anymore because it’s too crowded.”

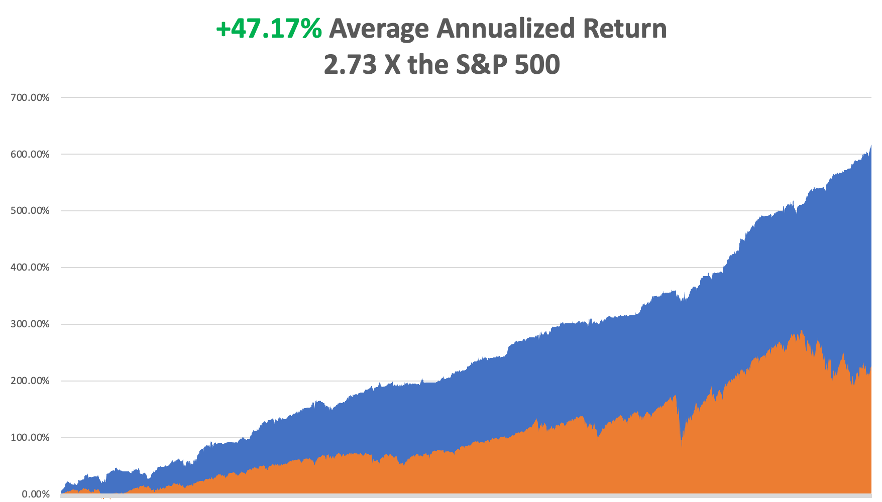

My performance in January has so far tacked on a welcome +19.83%. Therefore, my 2023 year-to-date performance is also +19.83%, a spectacular new high. The S&P 500 (SPY) is up +3.78% so far in 2023.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 15 years ago. My trailing one-year return maintains a sky-high +103.30%.

That brings my 15-year total return to +617.03%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +47.17%, easily the highest in the industry.

I took profits in my February bonds last week (TLT), taking advantage of a $5 pop in the market. All my remaining positions are profitable, including longs in (GOLD), (WPM), (TSLA), (BRK/B), and (TLT), with 30% in cash for a 10% net long position.

Since my New Year forecasts have worked out so well, I will repeat the high points just in case you were out playing golf or bailing out from a flood when they were published.

Buy Falling Interest Rate Plays, as I expect the yield on the ten-year US Treasury yield to fall from 3.50% to 2.50% by yearend. That means Hoovering up any kind of bond, like (TLT), (MUB), (JNK), and (HYG). Falling interest rates also shine a great spotlight on precious metals like (GLD), (SLV), (GOLD), and (WPM).

The US Dollar Will Continue to Fall. Commodities love this scenario, including (FCX), (BHP), and emerging markets (EEM).

Inflation Will Decline All Year and should go below 4% by the end of 2023. In fact, we have had real deflation for the past six months. Financials do well here, like (MS), (GS), (JPM), (BAC), (C), and (BRK/B).

Which creates another headache for you, if not an opportunity. We may have a situation where the main indexes, (SPY), (QQQ), and (IWM) go nowhere, while individual stocks and sectors skyrocket. That creates a chance to outperform benchmarks…and everyone else. There has been a lot of discussion among traders lately about the collapse of the Volatility Index ($VIX) to $18, a two-year low and what it means.

They are distressed because a ($VIX) this low greatly shrinks the availability of low risk/high return trading opportunities. A ($VIX) this low is basically shouting at you to “STAY AWAY!”

Does it mean that an explosion of volatility is following? Or are markets going to be exceptionally boring for the next six months?

Beats me. I’ll wait for the market to tell me, as I always do.

Consumer Price Index Falls 0.1% in December, continuing a trend that started in June. Stocks popped and bonds rallied. YOY inflation has fallen to 6.5%. “RISK ON” continues. Now we have to wait another month to get a new inflation number. The economy has now seen de facto deflation for six months. Gas prices led the decline, now 9.4%. We might get away with only a 0.25% interest rate hike at the February 1 Fed meeting.

Bond Default Risk Rises, as well as a government shutdown, as radicals gain control of the House. This is the group that lost the most seats in the November election. Bonds are the only asset class not performing today, and paper with summer maturities is trading at deep discounts. It certainly casts a shadow over my 50% long bond position. However, I don’t expect it to last more than a month and my longest bond maturity is in February.

The US Consumer is in Good Shape, according to JP Morgan’s Jamie Diamond. Spending is now 10% greater than pre covid, and balance sheets are healthy. No sign of an impending deep recession here.

Boeing Deliveries Soar from 340 to 480 in 2022, and 479 new orders. A sudden aircraft shortage couldn’t have happened to a nicer bunch of people. The 737 MAX has shaken off all its design problems after two crashes four years ago. Cost-cutting here can be fatal. Europe’s Airbus is still tops, with 663 deliveries last year. Don’t chase the stock up here, up 79% from the October lows, but buy (BA) on dips.

Small Business Optimism Hits Six-Month Low to from 91.9 to 89.8, adding to the onslaught of negative sentiment indicators, so says the National Federation of Independent Business (NFIB).

Copper Prices Set to Soar Further with the post-Covid reopening of China, according to research firm Alliance Bernstein. After a three-year shutdown, there is massive pent-up demand. Copper prices are at seven-month highs. Keep buying (FCX) on dips.

Australian Metals Exports Soar, as the new supercycle in commodities gains steam. Shipments topped $9 billion in November, 20% higher than the most optimistic forecasts. Keep buying copper (FCX), aluminium (AA), iron ore (BHP), gold (GLD) and silver (SLV) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, January 16, markets are closed for Martin Luther King Day.

On Tuesday, January 17 at 8:30 AM EST, the New York Empire State Manufacturing Index is out

On Wednesday, January 18 at 11:00 AM, the Producer Price Index is announced, giving us another inflation read.

On Thursday, January 19 at 8:30 AM, the Weekly Jobless Claims are announced. US Housing Starts and Building Permits are printed.

On Friday, January 20 at 7:00 AM, the Existing Home Sales are disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, the University of Southern California has a student jobs board that is positively legendary. It is where the actor John Wayne picked up a gig working as a stagehand for John Ford which eventually made him a movie star.

As a beneficiary of a federal work/study program in 1970, I was entitled to pick any job I wanted for the princely sum of $1.00 an hour, then the minimum wage. I noticed that the Biology Department was looking for a lab assistant to identify and sort Arctic plankton.

I thought, “What the heck is Arctic plankton?” I decided to apply to find out.

I was hired by a Japanese woman professor whose name I long ago forgot. She had figured out that Russians were far ahead of the US in Arctic plankton research, thus creating a “plankton gap.” “Gaps” were a big deal during the Cold War, so that made her a layup to obtain a generous grant from the Defense Department to close the “plankton gap.”

It turns out that I was the only one who applied for the job, as postwar anti-Japanese sentiment then was still high on the West Coast. I was given my own lab bench and a microscope and told to get to work.

It turns out that there is a vast ecosystem of plankton under 20 feet of ice in the Arctic consisting of thousands of animal and plant varieties. The whole system is powered by sunlight that filters through the ice. The thinner the ice, such as at the edge of the Arctic ice sheet, the more plankton. In no time, I became adept at identifying copepods, euphasia, and calanus hyperboreaus, which all feed on diatoms.

We discovered that there was enough plankton in the Arctic to feed the entire human race if a food shortage ever arose, then a major concern. There was plenty of plant material and protein there. Just add a little flavoring and you had an endless food supply.

The high point of the job came when my professor traveled to the North Pole, the first woman ever to do so. She was a guest of the US Navy, which was overseeing the collection hole in the ice. We were thinking the hole might be a foot wide. When she got there, she discovered it was in fact 50 feet wide. I thought this might be to keep it from freezing over but thought nothing of it.

My freshman year passed. The following year, the USC jobs board delivered up a far more interesting job, picking up dead bodies for the Los Angeles Counter Coroner, Thomas Noguchi, the “Coroner to the Stars.” This was not long after Charles Manson was locked up, and his bodies were everywhere. The pay was better too, and I got to know the LA freeway system like the back of my hand.

It wasn’t until years later when I had obtained a high-security clearance from the Defense Department that I learned of the true military interest in plankton by both the US and the Soviet Union.

It turns out that the hole was not really for collecting plankton. Plankton was just the cover. It was there so a US submarine could surface, fire nuclear missiles at the Soviet Union, then submarine again under the protection of the ice.

So, not only have you been reading the work of a stock market wizard these many years, you have also been in touch with one of the world’s leading experts on Artic plankton.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/john-thomas-peleliu-island-1975.png434628Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-17 09:02:252023-01-17 14:36:18The Market Outlook for the Week Ahead, or Going Against the Consensus

Below please find the subscribers’ Q&A for the January 11 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: In your trade alert you expected that the (TLT) might go up as much as 30% this year. But in your latest newsletter, you mentioned that the chaos in the US House of Representatives would greatly raise the risk of a default on US government debt by the summer and certainly cast a shadow over your 50% long bond position. Is it still a good idea to hold on to the (TLT) ETF over the next 2-6 months?

A: It is. The extremists who now control the House are not interested in governing or passing laws but gaining clicks, raising money, and increasing speaker’s fees. It may have converted (TLT) from a straight-up trade to a flat-line trade. We will still make the maximum profit on call spreads and LEAPS but with greater risk. But even chaos in the House can’t head off a recession, which the bond market seems intent on pricing in by going up. However, if you depend on government payments for any reason, be it Social Security, a government salary, a tax refund, or a payment for a contract, expect delays. The housing market also ceases because closings can’t take place during government shutdowns. Also, 30% of my bond longs expire in four trading days, and the remainder on February 17.

Q: Is it wise to sell the 2X ProShares Ultra Technology ETF (ROM) now or keep holding?

A: I think the (ROM), NASDAQ, and technology stocks in general may make several runs at the lows over the next six months but won’t fall much from here. A recession is priced in. Once we get through this, you’re looking at doubles and triples for the best names. So, the risk/reward overwhelmingly favors holding on to a one-year view.

Q: would you buy Tesla (TSLA) here?

A: I would start scaling in. The bad news is about to dry up, like Twitter, the recession, the pandemic in China, and Elon Musk selling shares. Then we face an onslaught of good news, like the new Mexico factory announcement, the Cybertruck launch, solid state batteries, and annual production hitting 2 million. At this level, the shares are priced in multiple worst-case scenarios. It is selling at 10X 2025 earnings, half the market multiple. At the end of the day, Tesla has an unassailable 14-year start over the rest of the industry and is the only company in the world that makes money on EVs. There’s an easy 10X here on two-year LEAPS.

Q: I’m in the Freeport McMoRan (FCX) January 25 2-year LEAP approaching the upper end of the 42/45 range. If it crosses 45, do we close the position?

A: Sell half, take your profit. If you’re in the LEAP, my guess is you probably have a 500% profit here in only 3 months, which is not bad. And then you keep the remaining half because you’re then playing with the house's money, and Freeport has a shot of going all the way to $100 a share by the 2025 expiration, and that will get you your full 1,000% return on the position. It’s always nice to be in a position where it’s impossible to lose money on a trade, and that certainly is where you are now with your (FCX) LEAP and everybody else in the FCX LEAP in October also.

Q: As a member of the Florida Retirement System, I’m curious how Blackrock (BLK) and other firms are dealing with the Santos’ plan for their portfolios.

A: Having a state governor manage your portfolio and make your sector and stock picks is an absolutely terrible idea. I can’t imagine a worse possible outcome for your retirement funds. Florida is not the only state doing this—Louisiana and Texas are doing it too. The goal is to drive money out of alternative energy and back into the oil industry, and obviously, this is being financed by the oil industry, which is pissed off over their low multiples. Suffice it to say it’s not a good idea to move out of one of the fastest-growing industries in the market and move into an industry that’s going to zero in 10 years. If that’s their investment strategy, I wish they’d stick to politics and leave investing for true professionals to do.

Q: What do you think about cannabis stocks?

A: I’m a better user of the product than the stock. How about that? How hard is it to grow weed? At the end of the day, these are just pure marketing companies, and that value added is low. Plus, they have huge competition from the black market still selling ½ to ⅓ below market prices because they’re tax-free; the local taxes on these cannabis sales are enormous.

Q: Would you recommend selling a bear market rally when the S&P goes to 405?

A: The (QQQ) would be the better short, something like the $310-320 vertical bear put spread for February to bring in some free money. That’s what I'm planning to do if we get up that high, which we may not.

Q: How do you take advantage of a low CBOE Volatility Index (VIX)?

A: You don’t; there’s nothing to do here with the (VIX) at $22. My trades this year were not volatility trades—because we did them with low volatility, they were pure directional trades betting that the longs would go up and the shorts would go down and they all worked.

Q: Will Rivian (RIVN) survive?

A: Yes, they have two years of cash flow in the bank, and they’re boosting production. However, a high-growth, non-earning stock like Rivian is just out of favor right now. Will they come back into favor? Yes, probably in a year or so, but in the meantime, people are much happier buying Microsoft (MSFT) at a discount than Rivian.

Q: Do you ever buy butterfly spreads?

A: No, four-legged trades run up a lot of commissions, are hard to execute because you have 4 spreads, and have lower returns. They are also lower risk and for people who have no idea what the market is going to do. I don’t need the lower risk trades because I know what markets are going to do.

Q: Do you suggest any Microsoft (MSFT) LEAPS?

A: Yes, go out two years with LEAPS and go out about 50% on your strike prices. A 50% move here in Microsoft in two years is a complete no-brainer.

Q: With weakness in retail, rising inventories, and high consumer debt, will consumers dip into savings?

A: Yes they will, but that will predominantly happen at the bottom half of the economy—the part of the economy that has minimal to no savings. The upper half seems to be doing well—the middle class and of course, the wealthy— and are not cutting back their spending at all, which is why this seems to be a recession that may not actually show up. So, what can I say? The rich are doing great and everyone else is doing less than great, and stocks are reflecting that. Nothing new here.

Q: Would you hold off on tech LEAPS for a bigger selloff, or closer to April?

A: If we do get another big selloff and challenge the October lows, I’ll be pumping out those LEAPS as fast as I can write them; except then, a two-year LEAPS will have an April of 2025 expiration.

Q: I just signed up. What are the advantages of LEAPS?

A: A possible 10x return in 2 years with very low risk. I would suggest going to my website, logging in, and doing a search for LEAPS. There will be a piece there on how to execute a LEAPS, and the Concierge members can also find that piece by logging into their website.

Q: Best and worst sectors?

A: First half, already mentioned them. We like commodities, healthcare, financials, and Berkshire Hathaway (BRK/B) in the first half and tech in the second half.

Q: Have we reached a low in cryptocurrencies?

A: Probably not, and I’ll tell you why I’ve given up on cryptos: I may not live long enough to see the bottom in crypto. It has Tokyo written all over it, and it took Tokyo 30 years to resume a bull market after it crashed in 1990. We’re still at the scandal stage where it turns out that the majority of these trading platforms were stealing money from customers. This is not a great inspiration for investing in that sector. When you have the best quality growth stocks down 80-90%; why bother with something that may not exist or may never recover in your lifetime? I’m out of the crypto business, but there are a wealth of crypto research sources still online and I’m sure they’d be more than happy to give you an opinion.

Q: Why have defense stocks like Raytheon (RTX) and Lockheed Martin (LMT) been weak recently?

A: A couple of reasons. #1 Just outright profit taking into the end of the year in one of the best-performing sectors. #2 The end of the war in Ukraine may not be that far off, and if that happens that could trigger a major round of selling in defense. We did get the three-day ceasefire over the Russian Orthodox New Year, that’s a possible hint, so that may be another reason.

Q: Political outlook on 2024?

A: It’s too early to make any calls, anything could happen; but if we get a repeat of the November election outcome, you could have Democrats retake control of both houses of congress—that’s where the betting money is going right now.

Q: Would you bottom fish in the United States Natural Gas Fund (UNG)?

A: No, I would not—I am avoiding energy like the plague. Remember the all-time low for natural gas is $0.95 per MM BTU, so we still could have a long way to go.

Q: Would you buy iShares China Large-Cap ETF (FXI) on a post-COVID breakout?

A: It looks like it’s already moved, so maybe kind of late on that. The problem is that in China, you don’t know what you are buying and the locals have a huge advantage in reading Beijing.

Q: What do you think about the Biden administration wanting to ban gas stoves?

A: That’s actually not a federal issue, it’s a state issue. California has already banned gas pipes for all new construction. It looks like New York will follow and that’s one-third of the US population. The goal is to replace them with electrical appliances which emit no carbon. I have a non-carbon house myself, I went down that path about 10 years ago, and it seems to be the only way to reduce carbon emissions—is to either price gasoline or oil out of the market, or to make it illegal, and they’re already making gasoline cars illegal, so gas and oil won’t be far behind. From 1900, we went from a hay powered economy to a gasoline-powered one in only 20 years so it should be doable.

Q: How can the push for all electric work well when we have so many shutdowns, much higher electricity cost, and cannot keep up with the demand already here?

A: Buy lots of copper for new local electric powerlines at the house level and buy lots of aluminum for the long-distance transmission lines. Global demand for both aluminum and copper has to triple to accommodate the grid buildout that is already planned. As far as hurricanes in Florida, there’s nothing you can do to stop those on a hundred-year view; I would move to higher ground, which is hard to do in Florida as the highest point in the state is only 345 feet and that’s a garbage dump.

Q: Can I get a copy of all these slides?

A: Yes, we post the PowerPoint on the website at www.madhedgefundtrader.com usually two hours after the production.

Q: Are you recommending buying precious metals right now (GLD), (GDX), (SLV), (and WPM) even after the upside breakout?

A: On upside breakouts, you buy the dips. A perfect dip would be a retest of the 200-day moving average. But we may not get that, since it seems to be everyone’s number-one choice right now. By the way, I haven’t been telling people to buy gold and LEAPS on all the gold plays since October—that’s where the big move has already been made.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip.

The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 14 Pro Max.

Here is the bottom line which I have been warning you about for months. In 2023, we will probably top the 84.63% we made last year, but you are going to have to navigate the reefs, shoals, and hurricanes. Do it and you can laugh all the way to the bank. I will be there to assist you to navigate every step.

The first half of 2023 will be all about trading. After that, I expect markets to go straight up.

And here is my fundamental thesis for 2023. After the Fed kept rates too low for too long, then raised them too much, it will then panic and lower them again too fast to avoid a recession. In other words, a mistake-prone Jay Powell will keep making mistakes. That sounds like a good bet to me.

Let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2023

1) When will the Fed pivot?

2) How much of a toll will the quantitative tightening take?

3) How soon will the Russians give up on Ukraine?

4) When will buyers return to technology stocks from value plays?

5) Will gold replace crypto as the new flight to safety investment?

6) When will the structural commodities boom get a second wind?

7) How fast will the US dollar fall?

8) How quickly will real estate recover?

9) How fast can the Chinese economy bounce back from Covid-19?

10) How far will oil prices keep falling?

Whether we get a recession or not, you can count on markets fully discounting one, which it is currently doing with reckless abandon.

Anywhere you look, the data is dire, save for employment, which may be the last shoe to fall. Technology companies seem to be leading us in the right direction with never-ending mass layoffs. Even after relentless cost-cutting though, there are still 1.5 tech job offers per applicant, which is down from last year’s three.

The Fed is currently predicting a weak 0.5% GDP growth rate for 2023, the same feeble rate we saw for 2022. What we might get is two-quarters of negative growth in the first half followed by a sharp snapback in the second half.

Whatever we get, it will be one of the mildest recessions or growth recessions in American economic history. There is no hint of a 2008-style crash. The banking system was shored up too well back then to prevent that. Thank Dodd/Frank.

Since my job is to make your life incredibly easy, I am going to narrow my equity strategy for 2023.

It's all about falling interest rates.

When interest rates are high, as they are now, you only look at trades and investments that can benefit from falling interest rates.

In the first half, that will be value plays like banks, (JPM), (BAC), (C), financials (MS), (GS), homebuilders (KBH), (LEN), (PHM), industrials (X), capital goods (CAT), (DE).

As we come out of any recession in the second half, growth plays will rush to the fore. Big tech will regain leadership and take the group to new all-time highs. That means the volatility and chop we will certainly see in the first half will present a generational opportunity to get into the fastest-growing sectors of the US economy at bargain prices. I’m talking Cadillacs at KIA prices.

A category of its own, Biotech & Healthcare should do well on their own. Not only are they classic defensive plays to hold during a recession, technology and breakthrough new discoveries are hyper-accelerating. My top three picks there are Eli Lily (ELI), Abbvie (ABBV), and Merck (MRK).

Block out time on your calendars because whenever the Volatility Index (VIX) tops $30, I am going pedal to the metal, and full firewall forward (a pilot term), and your inboxes will be flooded with new trade alerts.

There is another equity subclass that we haven’t visited in about a decade, and that would be emerging markets (EEM). After ten years of punishment by a strong dollar, (EEM) has also been forgotten as an investment allocation. We are now in a position where the (EEM) is likely to outperform US markets in 2023, and perhaps for the rest of the decade.

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a new business. This time, bonds face the gale force headwinds of three promised interest rate hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

With a major yield advantage over the rest of the world, the US dollar has been on an absolute tear for the past decade. After all, we have the world’s strongest economy.

That is about to end.

If your primary assumption is that US interest rates will see a sharp decline sometime in 2023, then the outlook for the greenback is terrible.

Currencies are driven by interest rate differentials and the buck is soon going to see the fastest shrinking yield premium in the forex markets.

That shines a great bright light on the foreign currency ETFs. You could do well buying the Australian Dollar (FXA), Euro (FXE), Japanese yen (FXE), and British Pound (FXB). I’d pass on the Chinese yuan (CYB) right now until their Covid shutdowns end.

5) Commodities (FCX), (VALE), (DBA)

Commodities are the high beta play in the financial markets. That’s because the cost of being wrong is so much higher. Get on the losing side of commodities and you will be bled dry by storage costs, interest expenses, contangos, and zero demand.

Commodities have one great attribute. They predict recessions earlier than any other asset class. When they peaked in March of 2022, they were screaming loud and clear that a recession would hit in early 2023. By reversing on a dime on October 14, they also told us that the recovery would begin in July of 2023.

You saw this in every important play in the sector, including Broken Hill (BHP), Peabody Energy (BTU), Freeport McMoRan (TCX), and Alcoa Aluminum (AA). Excuse me for using all the old names.

The heady days of the 2011 commodity bubble top are about to replay. Now that this sector is convinced of a substantially weaker US dollar and lower inflation, it is once more a favorite target of traders.

China will still demand prodigious amounts of imported commodities once its pandemic shutdown ends, but not as much as in the past. Much of the country has seen its infrastructure built out, and it is turning from a heavy industrial to a service-based economy, much like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase three-fold in a decade to accommodate this increase, no easy task, or prices will have to rise.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate all commodities on dips.

Snow Angel on the Continental Divide

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (XLE), (AMLP)

Energy was the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero sooner than you think. However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are bailing on their own industry. Instead of reinvesting profits back into their future exploration and development, as they have for the last century, they are paying out more in dividends and share buybacks.

Take the money and run.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and share prices for the energy industry.

Energy now counts for only 5% of the S&P 500. Twenty years ago, it boasted a 15% weighting.

The gradual shutdown of the industry makes the supply/demand situation infinitely more volatile.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

And guess who the world’s best oil trader was in 2022? That would be the US government, which drew 400 million barrels from the Strategic Petroleum Reserve in Texas and Louisiana at an average price of $90 and now has the option to buy it back at $70, booking a $4 billion paper profit.

The possibility of a huge government bid at $70 will support oil prices for at least early 2023. Whether the Feds execute or not is another question. I’m advising them to hold off until we hit zero again to earn another $18 billion. Why we even have an SPR is beyond me, since America has been a large net energy producer for many years now. Do you think it has something to do with politics?

To understand better how oil might behave in 2023, I’ll be studying US hay consumption from 1900-1920. That was when the horse population fell from 100 million to 6 million, all replaced by gasoline-powered cars and trucks. The internal combustion engine is about to suffer the same fate.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2022 was a terrible year for precious metals until we got the all-asset class reversal in October. With inflation soaring, stocks volatile, and interest rates soaring, gold had every reason to fall. Instead, it ended up unchanged on the year, thanks to a 15% rally in the last two months.

Bitcoin stole gold’s thunder until a year ago, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand were just not enough to keep gold afloat. That is over now for good and that is why gold is regaining its luster.

Chart formations are starting to look very encouraging with a massive head-and-shoulders bottom in place. So, buy gold on dips if you have a stick of courage on you, which I hope you do.

Higher beta silver (SLV) will be the better bet as it already has been because it plays a major role in the decarbonization of America. There isn’t a solar panel or electric vehicle out there without some silver in them and the growth numbers are positively exponential. Keep buying (SLV), (SLH), and (WPM) on dips.

Crossing the Great Nevada Desert Near Area 51

8) Real Estate (ITB), (LEN), (KBH), (PHM)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Those in the grip of a real estate recession take solace. We are in the process of unwinding 2022’s excesses, but no more. There is no doubt a long-term bull market in real estate will continue for another decade, once a two year break is completed.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s. You don’t have a real estate crash when we are short 10 million homes.

The reasons, of course, are demographic. There are only three numbers you need to know in the housing market for the next ten years: there are 80 million baby boomers, 65 million Generation Xers who follow them, and 86 million in the generation after that, the Millennials.

The boomers (between ages 58 and 76) have been unloading dwellings to the Gen Xers (between ages 46 and 57) since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis. That has created a massive shortage of housing, both for ownership and rentals.

There is a happy ending to this story.

Millennials now aged 26-41 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes. They are also just entering the peak spending years of middle age, which is great for everyone.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to the pandemic and Zoom, many are never returning to the cities. That has prompted massive numbers to move from the coasts to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should continue to rise during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are considered. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 16 years. The 50% of small home builders that went under during the Financial Crisis never came back.

We are still operating at only a half of the 2007 peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

There is a new factor at work. We are all now prisoners of the 2.75% 30-year fixed rate mortgages we all obtained over the past five years. If we sell and try to move, a new mortgage will cost double today. If you borrow at a 2.75% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free. That’s why nobody is selling, and prices have barely fallen.

This winds down towards the end of 2023 as the Fed realizes its many errors and sharply lowers interest rates. Home prices will explode…. again.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now after you throw in all the tax breaks. It’s also a great inflation play.

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

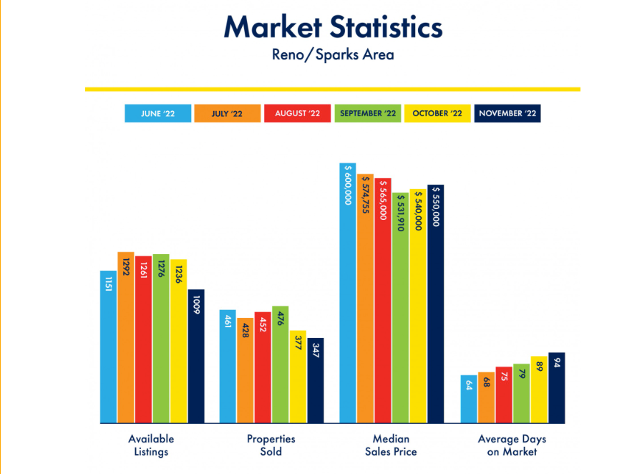

Recent Reno Real Estate Statistics

Crossing the Bridge to Home Sweet Home

9) Postscript

We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff has made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2023!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2023!

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/market-statistics.png474632Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-04 15:00:552024-01-03 10:44:502023 Annual Asset Class Review

Below please find subscribers’ Q&A for the November 30 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: You keep mentioning December 13th as a date of some significance. Is this just because the number 13 is unlucky?

A: December 13th at 8:30 AM EST is when we get the next inflation report, and we could well get another 1% drop. Prices are slowing down absolutely across the board except for rent, which is still going up. Gasoline has come down substantially since the election (big surprise), which is a big help, and that could ignite the next leg up in the bull market for this year. So, that is why December 13 is important. And we could well flatline, do nothing, and take profits on all our positions before that happens, because whatever it is you will get a big move one way or another (and maybe both) on December 13.

Q: I’m a new subscriber, and I am intrigued by your structuring of options spreads. Why do you do debit spreads instead of credit spreads?

A: It’s really six of one and a half dozen of the other—the net profit is pretty much the same for either one. However, debit spreads are easier to understand than credit spreads. We have a lot of beginners coming into this service as well as a lot of seasoned old pros. And it’s easier to understand the concept of buying something and watching it go up than shorting something and watching it go down. Now, doing the credit spreads—shorting the put spread—gives you a slight advantage in that it creates cash which you can then use to meet margin requirements. However, it’s only a small amount of cash—only the potential profit in that position. And guess what? All the big hedge funds actually kind of like easy-to-understand trade alerts also, so that’s why we do them.

Q: I have a lot of exposure in NVIDIA (NVDA), so is it worth trading out of it and coming back in at a lower rate?

A: NVIDIA is one of the single most volatile stocks in the market—it’s just come up 50%. But it could well test the lower limits again because it is so volatile, and the chip industry itself is the most volatile business in the S&P 500. If your view is short-term, I would take profits now, and look to go back in next time we hit a low. If you’re long-term, don’t touch it, because NVIDIA will triple from here over the next 3 years. I should caution you that if you do try the short-term strategy, most people miss the bottom and end up paying more to get back into the stock; and that's the problem with all these highly volatility stocks like Tesla (TSLA), NVIDIA (NVDA) and Advanced Micro Devices (AMD) unless you’re a professional and you sit in front of a screen all day long.

Q: Would you buy now and step in to make it long-term?

A: I think we get a couple more runs at the lows myself. We won’t get to the old lows, but we may get close. Those are your big buying points for your favorite stocks and also for LEAPS. And I’m going to hold back on new LEAPS recommendations—we’ve done 12 in the last two months for the Concierge members, and maybe half of those went out to Global Trading Dispatch before they took off again. So, that would be my approach there.

Q: How much farther can the Fed raise interest rates until they reverse?

A: 1%-2%, unless they get taken over by the data—unless suddenly the economy starts to weaken so much that they panic and reverse like crazy. I think that's actually what’s going to happen, which is why we went hyper-aggressive in October on the long side, especially in bonds (TLT). You drop rates on the ten-year from 4.5% to 2.5% in six months—that’s an enormous move in the bond market. That is well worth running a triple long position in it; I think that’s what's going to happen. That’s where we will make out the first 30% in 2023.

Q: Should I short the cruise lines here, like Royal Caribbean (RCL)?

A: They do have their problems—they have massive debts they ran up to survive the pandemic when all the ships were mothballed, so it is an industry with its major issues. The stock has already doubled since the summer so I wouldn’t chase it up here. I’m not rushing to short anything here right now though unless it’s really liquid or has horrendous fundamentals like the oil industry, which everyone seems to love but I hate—right now the haters are winning for the short term, until December 16, which is all I care about.

Q: Is the diesel shortage going to affect farmers and all other industries like the chip?

A: As the economy slows down, you can expect shortages of everything to disappear, as well as all supply chain issues, which is a positive for the economy for the long term.

Q: What about the 2024 iShares 20 Plus Year Treasury Bond ETF (TLT) 95—is that not a trade?

A: That’s a one-year position with a 100% potential profit. That is worth running to expiration unless we get a huge 20-point move up in the next 3 months, which is possible, and then there won’t be anything left in the trade—you’ll have 95% of the profit in hand at which point you’ll want to sell it. So, with these one-year LEAPS or two-year LEAPS, run them one or two years unless the underlying suddenly goes up a lot, and then grab the money and run; that's what I always tell people to do. Because if you sell your position, they can’t take the money away from you with a market correction.

Q: Is the current US economy the best economy in the world?

A: It is. If you look at any other place in the world, it’s hard to find an economy that's in better shape, and it’s because we have the best management in the world and hyper-accelerating technology which everyone else begs and borrows. Or steals. People who are predicting zero return on stocks for 10 years are out of their minds. You don’t short the best economy in the world. If anything, technology is accelerating, and that will take the stock market with it in the next year or so.

Q: Do you see the Dow ($INDU) outperforming the other indexes until the Fed positive pivots?

A: Absolutely yes, because the S&P 500 (SPY) has a very heavy technology weighting and technology absolutely sucks right now. That would probably be a good 3-month trade—buy the Dow, and short the S&P 500 in equal amounts. Easy to do—you might pick up 10% on a market-neutral trade like that.

Q: Do you see a Christmas rally this year?

A: Actually, I do, but it won’t start until we get the next inflation report on December 13, at which point I'm going 100% cash. I’ve made enough money this year, and this is a problem I had when I ran my hedge fund: when you make too much money, nobody believes it, so there's really no point in making more than 50% or 60% a year because people think it’s fake. This is true in the newsletter business as well. Markets also have a nasty habit of completely reversing in January; this year, we had one up day in January, and then it was bombs away and we just piled on the shorts like crazy, so you have to wait for the market to first give you the fake move for the year, and then the real one after that. The best way to take advantage of that is to be 100% cash, and that’s why I usually do.

Q: What indicators do you see that give you the most confidence that inflation has peaked?

A: There's one big one, and that’s real estate. Real estate is absolutely in a recession right now and has the heaviest weighting of any individual industry in the inflation calculation. If anybody thinks house prices are going up, please send me an email and tell me where, because I’d love to know. The general feeling is they’re down 10-15% over the last six months. New homes are only being sold with massive buydowns in interest rates and free giveaways on upgrades. It is an industry that is essentially shut down, with interest rates having gone from 2.75% to 7.5% in a year, so there’s your deflation, but unfortunately, real estate is also the slowest to price in in the Fed’s inflation calculation, so we have to go through six months of torture until the Fed finally sees proof that inflation is falling. So, welcome to the stock market because it's just one of those factors. Just for fun, I got a quote on financing an investment property. The monthly payment would have been double for half the house that I already have.

Q: Are LEAPS a buy with the CBOE Volatility Index (VIX) this low?

A: No, you want to look at stocks first, and then the VIX; and with all the stocks sitting on top of 30-50% rises, it’s a horrible place to do LEAPS. LEAPS were an October play—we bought the bottom in a dozen LEAPS in October, and those were great trades, except for Tesla (TSLA) and Rivian (RIVN) which still have two years left to run. Up here, you’re basically waiting on a big selloff before you go into these one to two-year options positions.

Q: Why does Biden keep extending student loans? Will this catch up at some point?

A: He’s going to take it to the Supreme Court, and if he loses at the Supreme Court, which is likely, then he’ll probably give up on any loan extensions. At this point, the loan extensions on student loans are something like 2 or 2.5 years. The reason he’s doing this is to get 26 million people back into the economy. As long as you have giant student loan balances, you can’t get credit, you can’t get a credit card, you can’t buy a house, you can’t get a home loan. Bringing that many new people into the economy is a huge positive for not only them but for everyone else because it strengthens the economy. That has always been the logic behind forgiving student loans—and by the way, the United States is virtually the only country in the world that makes students pay back their loans after 30 or 40 years. The rest give college educations away either for free or give some interest-free break on repayments until they can get a salary-paying job.

Q: Does the budget deficit drop impact the stock market?

A: Yes, but it impacts the bond market first and in a much bigger way. That’s one of the reasons that bonds have rallied $13 points in six weeks because less government borrowing means lower interest rates—it’s just a matter of supply and demand. This has been the fastest deficit reduction since WWII, and markets will discount that.

Q: Will the US dollar (UUP) crash?

A: Yes, it will. You get rid of those high interest rates and all of a sudden nobody wants to own the US dollar, so we have great trades setting up here against everything, except maybe the Yuan where the lockdowns are a major drag.

Q: Is silver (SLV) a buy now?

A: No, it’s just had a big 10% move; I would wait for any kind of dip in silver and gold (GOLD) before you go into those trades. And when/if you do, there are better ways to do it.

Q: How is the Ukraine war going?

A: It’ll be over next year after Ukraine retakes Crimea, which they’ve already started to do. Russia is running out of ammunition, and so are we, by the way. However, the United States, as everybody learned in WWII, has an almost infinite ability to ramp up weapons production, whereas Russia does not. Russia is literally using up leftover ammunition from WWII, and when that’s gone, they’ve got nothing left, nor the ability to produce it in any sizable way. All good reasons to sell short oil companies ahead of a tsunami of Russian oil hitting the market. By the way, oil is now down for 2022.

Q: What's the number one short in oil (USO)?

A: The most expensive one, that would be Exxon Mobile (XOM).

Q: What’s going to happen to the markets in January?

A: After this Christmas rally peters out, I’m looking for profit-taking in January.

Q: When is a good time to buy debit spreads on oil?

A: Now. Look at every short play you can find out there; I just don’t see a massive spike up in oil prices ahead of a recession. And by the way, if the war in Ukraine ends and Russian oil comes back on the market, then you’re looking at oil easily below $50.

Q: What is the best way to invest in iShares Silver Trust (SLV) in the long term?

A: A two-year LEAP on the Silver (SLV) $25-$26 call spread—that gets you a 100%-200% return on that.

Q: Is lithium a good commodity trade?

A: Lithium will move in sync with the EV industry, which seems to have its own cycle of being popular and unpopular. We’re definitely in the unpopular phase right now. Long term demand for lithium will be increasing on literally hundreds of different fronts, so I would say yes, lithium is kind of the new copper. Look at Albemarle (ALB), Societe Chemica Y Minera de Chile (SQM), and FMC Corp. (FMC).

Q: If we do a LEAPS on Crown Castle Incorporated (CCI), you won’t get the dividend right?

A: No, you won’t, it’s a dividend-neutral trade because you’re long and short in a LEAPS. You have to buy the stock outright and become a registered shareholder to earn the dividend which, these days, is a hefty 4.50%. That said, if you’re looking for a high dividend stock-only play, buying the (CCI) down here is actually a great idea. For the stock-only players, this would be a really good one right now.

Q: Do you know people who are selling because of large capital gains?

A: The only people I know who are selling have giant tax bills to pay because of all the money they made trading options this year. I happen to know several thousand of those, as it turns out. So yes, I do know and that could affect the market in the next couple of weeks, which is why I went with the flatlined scenario for the next two weeks. Most tax-driven selling will be finished in the next two weeks, and after that, it kind of clears the decks for the markets to close on a high note at the end of the year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING or DISPATCH TECHNOLOGY LETTER as the case may be, then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/12/john-thomas-TA-418.jpg600864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-02 13:02:582022-12-02 14:01:23November 30 Biweekly Strategy Webinar Q&A

I got a call from my daughter the other day, who is a Computer Science major at the University of California at Santa Cruz. The university was on strike and shut down, so she suddenly had a lot of free time on her hands.

The Teaching Assistants were only getting $12 an hour, which is not enough to live on in the San Francisco Bay Area by a mile. Some one-third were living in their cars, which can get chilly on the Northern California coast in winter.

Fast food workers in California will get $22 an hour from January, thanks to a bill passed in the recent election. The TAs, most of whom are working on master’s degrees and PhD’s in all kinds of advanced esoteric subjects, are simply asking to bring their pay in line with Taco Bell.

The entire UC system is on strike, affecting ten campuses, 17,000 TAs and 200,000 students. I have noticed that the most liberal universities often have the most draconian employment policies. It’s legalized slave labor. I speak from experience as a past victim, as I was once an impoverished work-study student at UCLA earning $1.00 an hour experimenting with highly radioactive chemicals.

What was my tuition for four years at the best public university in the world? Just $3,000, and I didn’t even pay that, as I was on a full scholarship, something about rocket engines I built when I was a kid. Werner Von Braun liked them. The 800 Math SAT score probably helped a tiny bit too.

UCSC is the feeder university for Silicon Valley. Graduates in Computer Science earn $150,000 a year out the door and $200,000 with a Master's degree. PhDs get offered founders’ stock in the hottest Silicon Valley startups.

I hope the TAs get their raise.

My daughter was calling me to apologize for her poor trading performance this year. I thought, “My goodness, did she just lose her entire college fund in some crypto scam?”

“How much did you lose,” I asked.

She answered that she didn’t lose anything and in fact was up 59% this year. She knew my performance was topping 78%, and that some subscribers had made up to 1,000%.

But she missed the October low because she had a midterm and was late on my (TLT) LEAPS because she was on a field trip. She promised to pay closer attention so she could earn the money to pay for her PhD.

My kids never ask me for money. If they need it, they just go into the markets and get it themselves. But then this is a family that discussed implied volatilities, chaos theory, and the merits of the Black Scholes equation over dinner every night. That’s what it’s like to have a hedge fund manager for a dad. Any extra money I have I give away to kids not as lucky as mine.

Then we talked about the most important issue of the day, how to cook the turkey this week. Brine, or no brine, with or without a T-shirt, or deep fat fry? She cautioned me to take it out of the freezer three days early to thaw. I bought my turkey a month ago because I knew prices would rise, and they have done so mightily. In case I get in over my head, I can always call the Butterball Thanksgiving Turkey Emergency Hotline at 844-877-3436.

But that’s just me.

Whenever making money gets too easy, I get nervous.

There’s a 90% chance we saw the bottom in this bear market on October 14. But how we proceed from here is the tricky part. Too much now depends on a single monthly data point, namely the Consumer Price Index, and that is a tough game to play. The next one is out on December 13.

The truth is that even with overnight interest rates at 4.75%-5.00% , the economy is holding up far better than anyone imagined possible. Some sectors, like financials, are positively booming. And while housing is weak, we really have not seen any major price falls that could threaten a financial crisis. Consumers are in good shape with savings near record levels.

There isn’t going to be a hard landing. There isn’t even going to be a soft landing. In fact, we may not have a landing at all, with the economy continuing to motor along, albeit at a slower rate just above stall speed.

Which begs me to repeat that the next new trend in interest rates will be down, and that this will be the principal driver of all your investment decisions going forward. Bonds may make the initial move up, as last week’s trade alerts suggested. But I have no doubt that equities will have a big move in 2023 as well.

Producer Price Index Fades, up only 0.2%, half of what was expected. That’s a big decline from 8.4% to 8.0% YOY. It’s another bell ringing that inflation has topped. Stocks rallied 500 on the news.

Bonds Continue on a Tear, with the (TLT) up a breathtaking eight points from the October low. It could reach $120 in 2023. Keep buying (TLT) calls, call spreads, and LEAPS on dips.

FTX Keeps Getting Worse, as it is looking like it’s a Bernie Madoff X 10, or an Enron X 20. A new CEO has been appointed by the bankruptcy court, John Ray, the former liquidator of Enron and a distant relative of mine. This will spoil investment in most digital coins and tokens for good, which are now worthless, and coins unless they are guaranteed by JP Morgan (JPM) or Goldman Sachs (GS). FTX never had a CFO, and Sam Bankman-Fried is blaming it all on his girlfriend, not exactly what creditors want to hear. In any case, Bitcoin has been replaced by Taylor Swift tickets.

A Massive Silver Shortage is Developing, with demand up 16% in 2023 to 1.21 million ounces. With EV production increasing from 1.5 million to 20 million units a year within the decade, its share of the market will rise from 5% to 75%. Solar panel demand is also rising. Buy (SLV) and (WPM) on dips. My next LEAPS will be for silver on the next dip.

NVIDIA Sales Rise, but profits dip, taking the stock up 3%. Games sales dropped a heartbreaking 50% and crypto took a big hit. The company expects $6 billion in sales in Q4 and is still operating at an incredible 53.6% gross margin. The company is creating a new line of dumbed-down products to comply with China export bans. Keep buying (NVDA) on dips. We caught a 50% move in the past month.

Retail Sales Rise 1.3% in October, causing analysts to raise Q4 GDP forecasts. Rising prices are a major factor. Where is that darn recession?

Who Has the World’s Worst Inflation? Not the US, where price gains have been relatively muted. Venezuela leads with 21,912%, followed by Zimbabwe at 2019%, Lebanon at 1071%, Argentina at 194%, Turkey at 124%. Even Russia is at 25%. Who has the lowest? Japan at 1.0%, but their currency has just collapsed by 40%.

The 60/40 Portfolio is Back, after a 15-year hiatus. JP Morgan Chase says that keeping 60% of your money in stocks and 40% in bonds should deliver a 7.2% annual return. I believe the balanced portfolio return will be much higher, as everything will go up in 2023 and fixed income is now yielding 5% or better. 2022 saw the worst 60/40 return in 100 years.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 21 at 8:00 AM, the Chicago Fed National Activity Index for October is out.

On Tuesday, November 22 at 8:30 AM, the Richard Fed Manufacturing Index is released.

On Wednesday, November 23 at 8:30 AM, Durable Goods for October is published. At 11:00 AM, the FOMC minutes from the previous meeting are out. Weekly Jobless Claims are announced. New Homes Sales for October are out.

On Thursday, November 24, Markets are closed for Thanksgiving.

On Friday, November 25, stock markets close early at 1:00 PM. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I have dated a lot of interesting women in my lifetime, but one who really stands out is Melody Knerr, the daughter of Richard Knerr, the founder of the famed novelty toy company Wham-O (click here). I dated her during my senior year in high school.

At six feet, she was the tallest girl in the school, and at 6’4” I was an obvious choice. After the senior prom and wearing my cheap rented tux, I took her to the Los Angeles opening night of the new musical Hair.

In the second act, the entire cast dropped their clothes onto the stage and stood there stark naked. The audience was stunned, shocked, embarrassed, and even gob-smacked. Fortunately, Melody never revealed the content of the play to her parents, or I would have been lynched.

In a recurring theme of my life, while Melody liked me, her mother liked me even more. That enabled me to learn the inside story of Wham-O, one of the great untold business stories of all time.

Richard Knerr started Wham-O in a South Pasadena garage in 1948. His first product was a slingshot, hence the company name, the sound you make when firing at a target. Business grew slowly, with Knerr trying and discarding several different toys.

Then in 1957, he borrowed an idea from an Australian bamboo exercise hoop, converted it to plastic, and called it the “Hula Hoop.” It instantly became the biggest toy fad of the 20th century, with Wham-O selling an eye-popping 25 million in just four months. By 1959, they had sold a staggering 100 million.

The Hula Hoop was an extremely simple toy to manufacture. You took a yard of cheap plastic tubing and stapled it together with an oak plug, and you were done. The markup was 1,000%. Knerr made tens of millions and bought a mansion in a Los Angeles suburb with a stuffed lion guarding his front door which he had shot in Africa.

The company made the decision to build another 50 million Hula Hoops. Then the bottom absolutely fell out of the Hula Hoop market. Midwestern ministers perceived a sexual connotation in the suggestive undulating motion to use it and decried it the work of the devil. Orders were cancelled en masse.

Whamo-O tried to stop their order for 50 million oak plugs, which were made in England, but to no avail. They had already shipped. So, to cut their losses Whamo-O ordered the entire shipment dumped overboard in the North Atlantic, where they still bob today. The company almost went bankrupt.

Knerr saved the company with another breakout toy, the Frisbee, a runaway success which is still sold today. Even Incline Village, Nevada has a Frisbee golf course. The US Army tested it as a potential flying hand grenade. That was followed by other monster hits like the Super Ball, the Slip N Slide, and the Slinky.

Richard Knerr sold his company to toy giant Mattel (MAT) for $80 million in 1994. He passed away in 2008 at the age of 82.

As for Melody, we lost touch over the years. The last I heard she was working at a dive bar in rural California. Apparently, I was the high point of her life. The last time I saw her I learned the harshest of all lessons, never go back and visit your old high school girlfriend. They never look that good again.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Hula Hoop Inventor Chuck Knerr

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/chuck-knerr.png155228Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-21 10:02:432022-11-21 13:45:43The Market Outlook for the Week Ahead, or Slowing to Stall Speed

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-04 09:04:522022-11-04 11:25:47November 4, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.