Mad Hedge Technology Letter

August 21, 2024

Fiat Lux

Featured Trade:

(SPEND UNTIL REVENUE COMES)

(NVDA), (SMCI), (AVGO)

Mad Hedge Technology Letter

August 21, 2024

Fiat Lux

Featured Trade:

(SPEND UNTIL REVENUE COMES)

(NVDA), (SMCI), (AVGO)

Spend, spend, and spend some more.

That is the current zeitgeist in the tech community about the direction of generative artificial intelligence.

Companies are trying to outdo each other to see how much cash they can splurge to build out the AI infrastructure.

This is no joke.

Remember that there have been no meaningful explanations about how much revenue will directly come from AI, but my belief is that we are still in the “honeymoon phase” of the AI movement.

Eventually, and gradually, real questions will be asked and results will need to be provided instead of “building” nonstop with no accountability.

We are still in the phase of giving AI a pass which is why many have suggested stocks like Nvidia are turning into a bubble similar to 2001.

How do I know that AI is back?

Look at the chips stocks who were leading the tech rally for most of the year.

They sold off violently because of the unwinding of the Japanese yen carry trade, but the dip was bought because the discounts were too good to pass up for investors and because the AI trade isn’t over yet.

The snapback in chip stocks was v-shaped and set the stage for the rest of the year to power into the close.

I do believe the tech sector will receive better-than-expected news from the wider economy that shows the consumer is in better shape than initially thought.

The bar is extremely low for tech stocks to jump over and I do believe the ones with great balance sheets will use shareholder returns to convince shareholders to stick with their stocks.

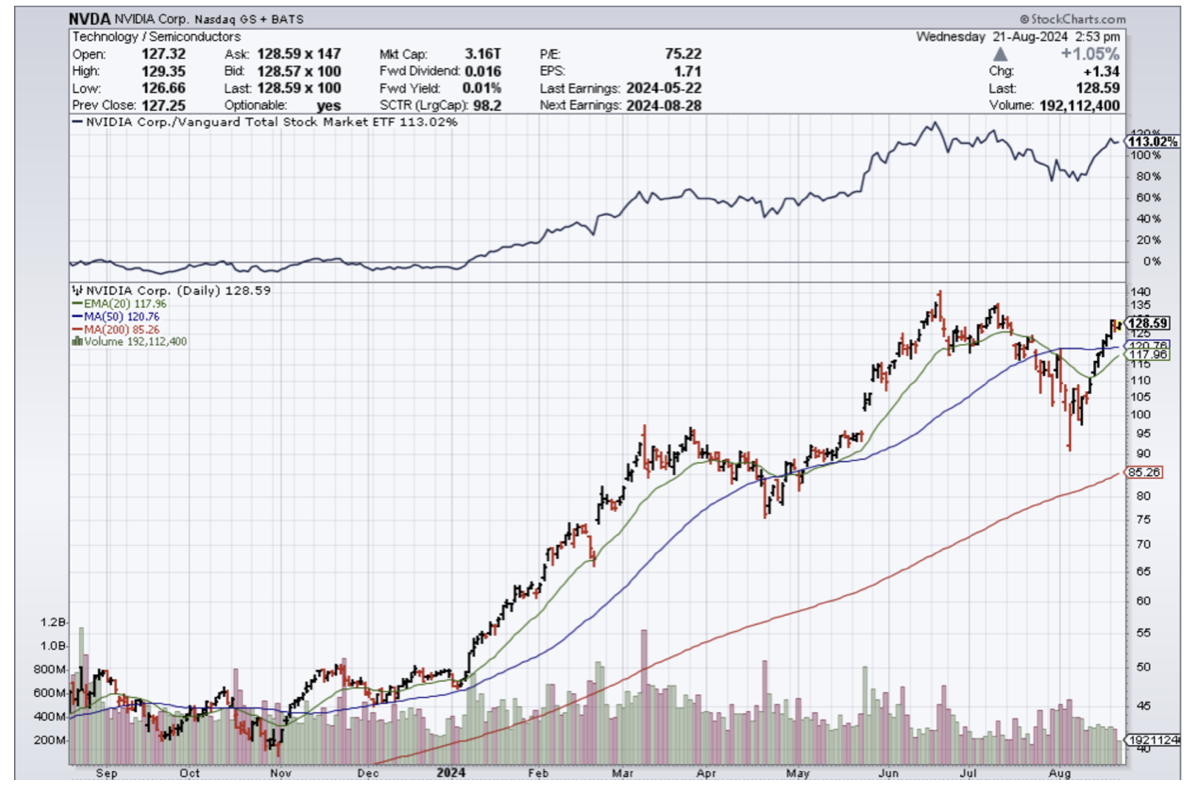

AI hardware and chip companies have led the bounce in the Nasdaq from its August low, with Nvidia the index’s top performer, up almost 30% and just 6.1% short of the all-time high, as of its last close. Similar stocks like Micron, Marvell Technology, Super Micro Computer, and Broadcom have all participated in the snapback.

Strong monthly sales from Taiwan Semiconductor Manufacturing similarly pointed to robust AI demand.

The build-out of AI infrastructure is expected to be both enormous and long-lasting and investment in data center infrastructure needed to support GenAI could reach $6 trillion.

Capex from big tech could potentially increase by as much as 25% in 2025, well above the consensus expectation for 10-15% growth. This is especially positive for AI enablers in the semiconductors field.

Nvidia’s expensive valuation is completely justified when you understand that they carry the entire tech sector which is carrying the entire market on their back.

Shorting NVDA has probably been one of the worst trades you could have made in the past few years.

Mad Hedge Technology Letter

July 3, 2024

Fiat Lux

Featured Trade:

(SHOULD I INVEST IN AI CHIPS OR AI SERVERS?)

(SMCI), (NVDA), (DELL)

The AI server market is booming and so are the AI chip markets.

I’ll talk about 2 prestigious companies right in the mix of things.

For long-term portfolios, it’s essential to not miss out on these supercharge growth companies.

I just don’t think that average investors will be able to make up the performance if they miss the boat of these 2 companies. The law of large numbers will just put you too far behind.

All the hot new money is going into AI which adds to the momentum of the share price trajectories.

Even the old money, after not being convinced by Bitcoin, is starting to come around to AI partly because most of the companies involved in AI are publicly listed companies on the New York Stock Exchange.

It makes it a lot easier when the source of exponential growth isn’t on some alternative exchange in some alternate currency in some backwater jurisdiction.

With a few clicks and moving a few dollars here and there, investors can be part of the AI future whether it be in AI chips or AI servers like the companies I am about to talk about.

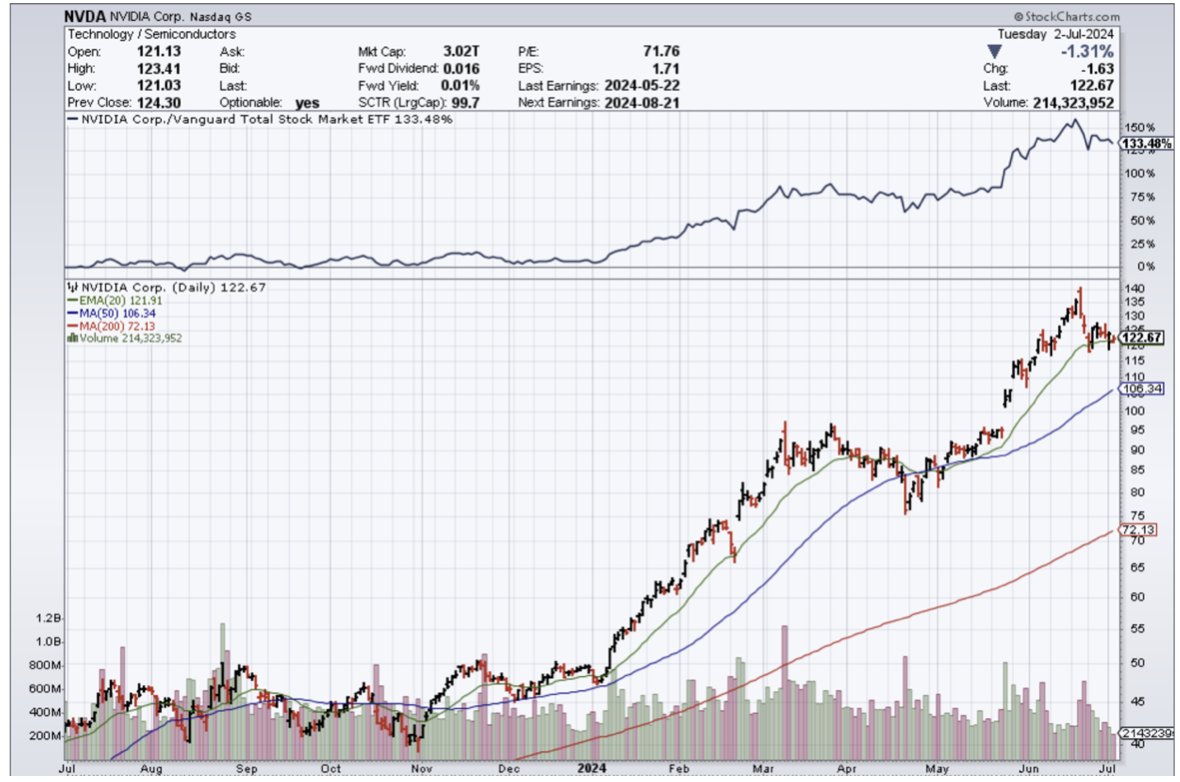

What up with Nvidia?

Nvidia (NVDA) dominates an impressive 94% of the AI chip market. It’s basically a monopoly or close to it.

Revenue is rising a stunning 262% year over year.

Even more interesting, emerging growth avenues in the nascent AI market indicate that Nvidia could end up doing even better than that.

For instance, governments are also betting the ranch on AI and this stable source of revenue will highly likely grow substantially for the foreseeable future.

Nvidia's customer base is diversifying beyond the major cloud infrastructure providers that have been deploying its chips in large numbers to train and deploy AI models.

Spending on AI chips is expected to grow more than 10-fold over the next decade, generating $341 billion in revenue in 2033 compared to $23 billion last year.

Nvidia should remain the Tom Brady of AI stocks as the race to develop AI applications by companies and governments alike has created a secular growth opportunity.

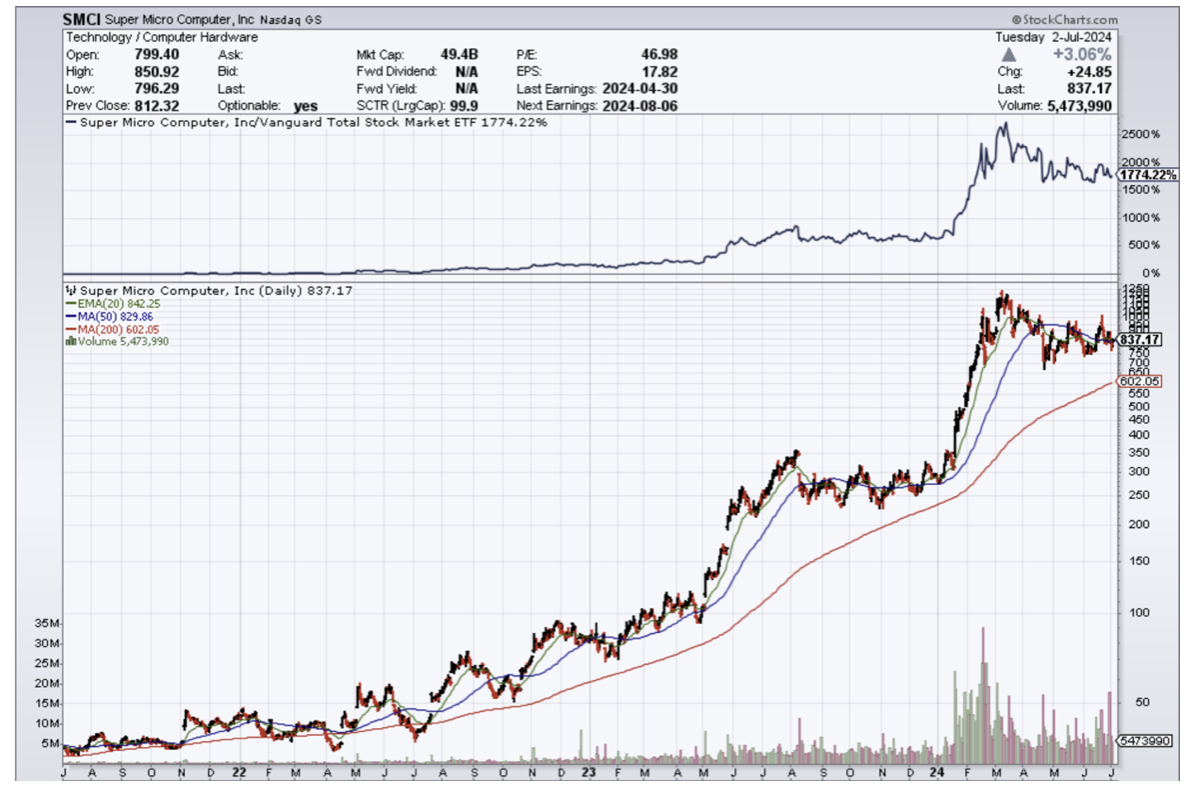

What about Super Micro Computer?

Supermicro's future prospects are attached to some extent with that of Nvidia’s.

Data center operators require server rack solutions of the type that Supermicro sells to mount the processors sold by Nvidia and other chipmakers.

Revenue jumped 200% year over year and Supermicro isn't all that far behind Nvidia when it comes to how AI has supercharged its fortunes.

I expect its top line to nearly double over the next couple of years.

Demand for AI servers is expected to expand at a compound annual rate of 25% through 2029.

Supermicro is growing at a faster pace than the AI server market right now. As it turns out, its growth is faster than that of more established companies such as Dell.

How to invest?

Supermicro is cheaper than Nvidia and Nvidia’s run-up to a more than $3 trillion market valuation has got to scare some people with sticker shock.

People with a time advantage of more than a few years should invest in Super Micro, whereas investors looking for that quick sugar high should buy the dips in Nvidia.

In short, anyone under the age of 40 and many years in front of them should invest long-term in Super Micro at a market cap of $50 billion. With Nvidia, I could easily see its market cap climbing to $4 trillion soon, but a wicked pullback would mean its market cap going from $4 to $3 trillion.

Either way, these are two tech firms with great prospects in the current and future.

Mad Hedge Technology Letter

June 7, 2024

Fiat Lux

Featured Trade:

(HEWLETT PACKARD – REMEMBER THEM?)

(HPE), (SMCI), (NVDA), (ORCL), (DELL)

Artificial intelligence is not always the golden ticket, but some legacy companies, they are using this trend to springboard themselves back to relevancy.

Look at companies like Dell (DELL) or Oracle (ORCL) – they epitomize what I am talking about.

For years, these certain legacy tech firms were crowbarred into this narrow definition of some aging enterprise software company that was from yesteryear.

It was true back then but some have changed.

Hewlett Packard (HPE) is another Silicon Valley brand name that has reinvented itself for artificial intelligence and its stock price has reaped the dividends.

The stock has exploded to the $20 per share range after languishing in the teens for years.

HPE latest report was topped up with its better-than-expected revenue fueled by sales of servers built for artificial intelligence work.

The strong performance was due to the company’s server business, which generated revenue of $3.87 billion.

Sales of AI-oriented systems doubled from the first quarter to more than $900 million.

Increased demand and better availability of high-powered semiconductors from Nvidia (NVDA) led to an increase in AI systems sales.

HPE would be a good way to play the catch-up trade in AI servers compared with its peers in the server space, including Dell Technologies (DELL) and Super Micro Computer (SMCI).

HPE’s current backlog for AI systems is now $3.1 billion.

This is the first quarter HPE has broken out AI server revenue and investors likely welcome the increased disclosure.

The AI-server ramp-up is finally materializing.

The full-year forecast is underwhelming given the increased AI business, suggesting other business lines, such as networking, are dragging down the results.

I am not saying that HPE is the finished article right now and is a pure AI play. I am not. They have a lot to work on and that might be a generous statement to even say that.

There is still plenty to dislike about HPE who are saddled with legacy businesses that barely move the needle.

However, if HPE smartly harnesses resources right, I do believe they could eventually turn into an above-average AI play.

At this point, many tech companies view the participation of AI or not as an existential matter.

Many companies will get left behind and swept into the dustbin of history.

When the biggest tech companies in the world talk about AI constantly on their earnings call, it is not a head fake. This is the real deal so get with the program.

There are many different types of semiconductors with different levels of sophistication, from simple chips in kitchen appliances to cutting-edge graphics processing units (GPUs) used in artificial intelligence (AI) applications, as well as cryptocurrency mining.

In many of these use cases, semiconductor chips will need an AI server to act as storage for the data or some other similar function.

The data produced is substantially greater than analog chips and of higher quality.

We are still in the early innings of the AI revolution, so it is important to know which stocks possess an upward trajectory in terms of business models and sub-sectors.

In 2024, semiconductor chips and AI server stocks have made their stamp in the tech world and aren’t going away.

Remember that the trend is your friend and I wouldn’t fight this one. It’s a massive trend to fight and be on the wrong end.

Moving forward, I believe HPE will make meaningful optimization decisions to amplify its AI server business while minimizing its legacy divisions to the benefit of the future share price.

If they can somewhat achieve these results, the stock should easily rise by 3X.

Global Market Comments

June 3, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE MALLARD MARKET and ME AND 23 AND ME),

(AAPL), (GOOGL), (AMZN), (TSLA), (MSFT), (META), (AVGO), (LRCX), (SMCI), (NVR), (BKNG), (LLY), (NFLX), (VIX), (COPX), (T), (NVDA), (LEN), (KBH)

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

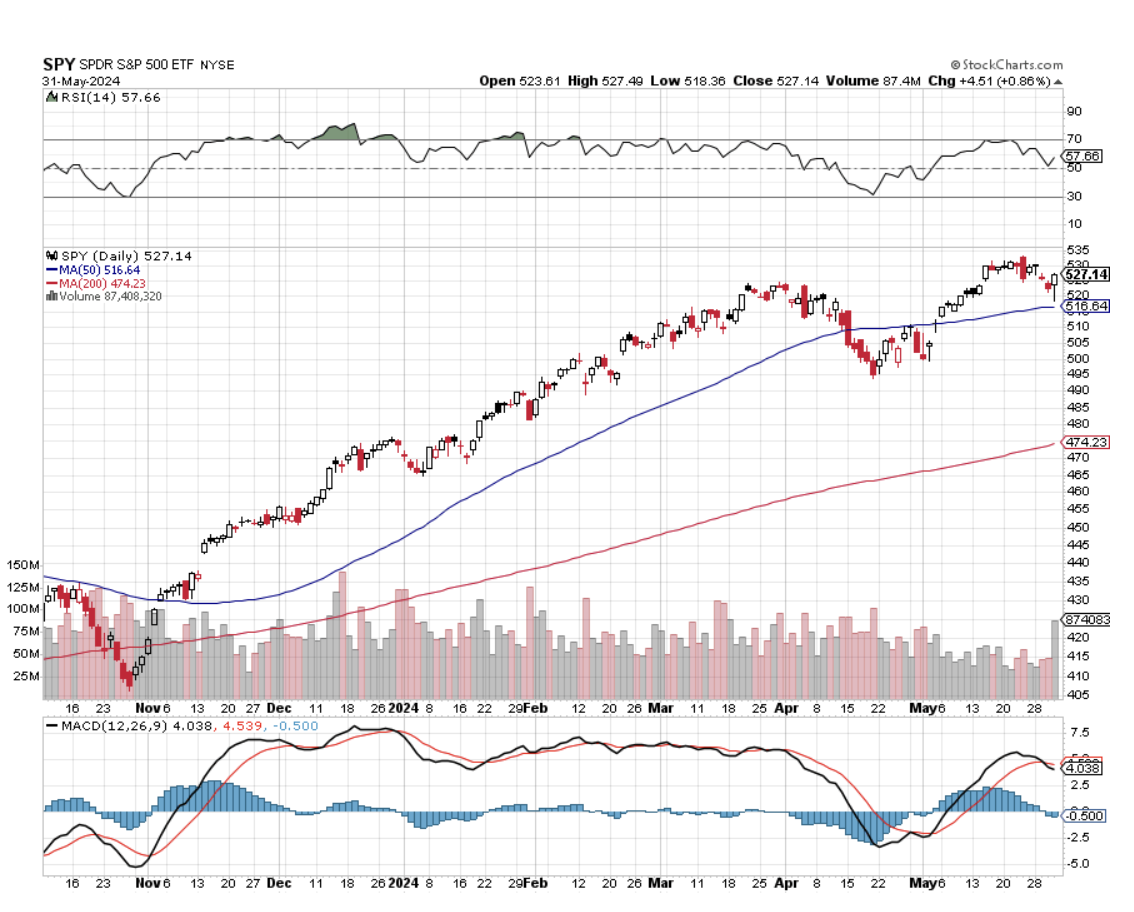

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

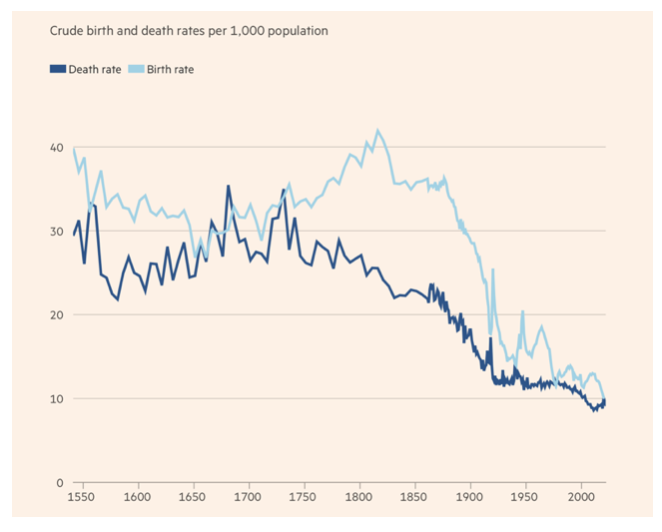

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

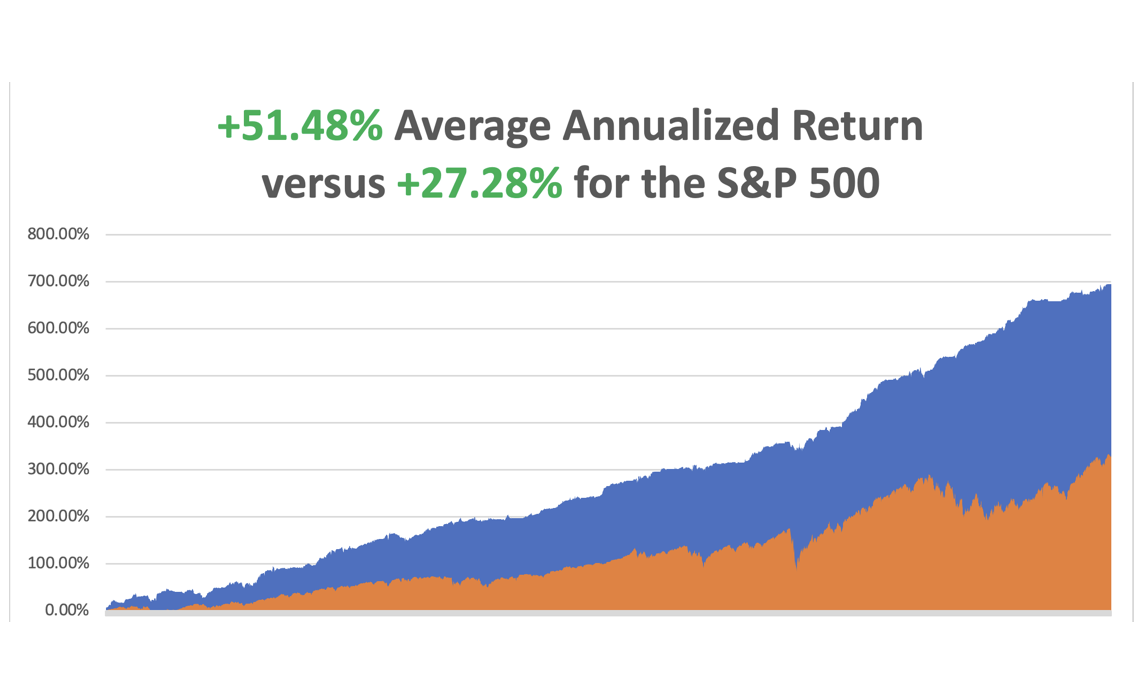

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%. The S&P 500 (SPY) is up +10.48% so far in 2024. My trailing one-year return reached +35.74%.

That brings my 16-year total return to +694.78%. My average annualized return has recovered to +51.48%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day.

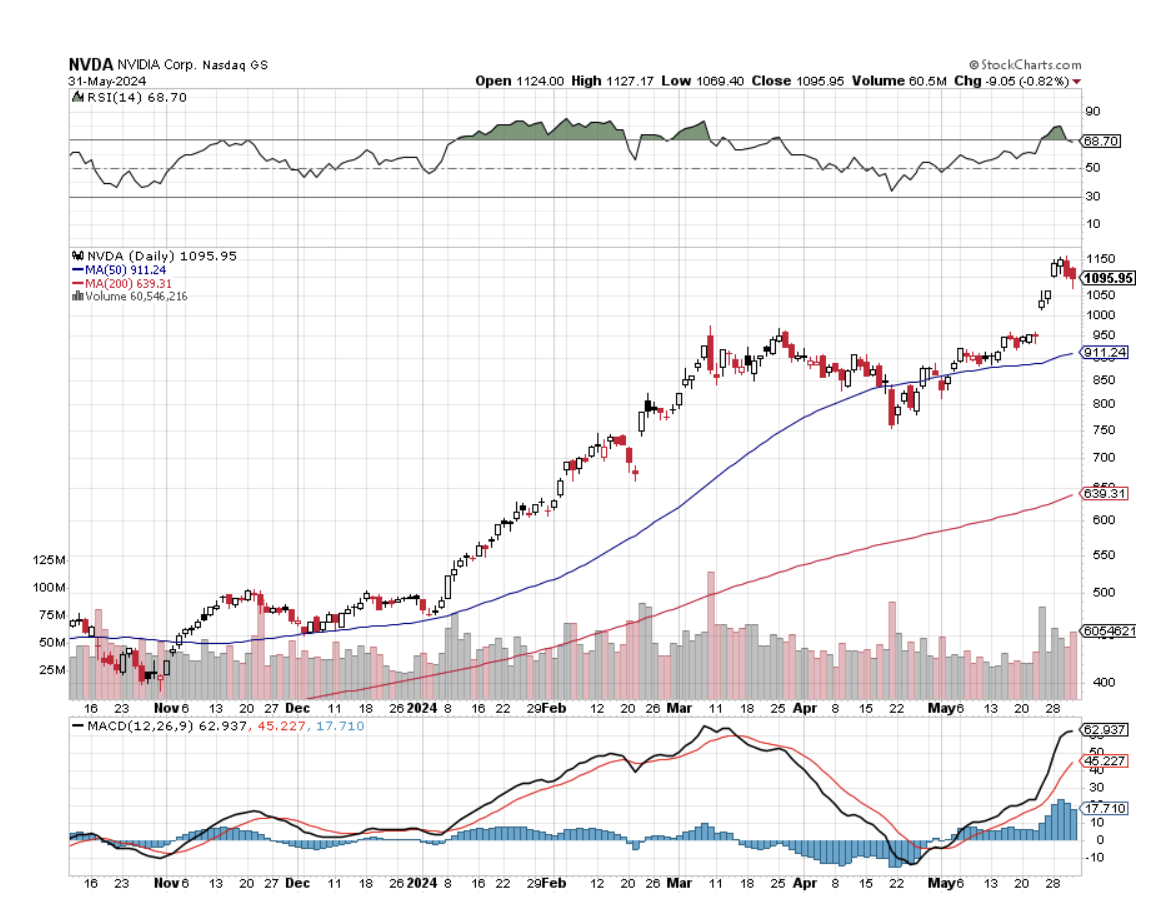

NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity. By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

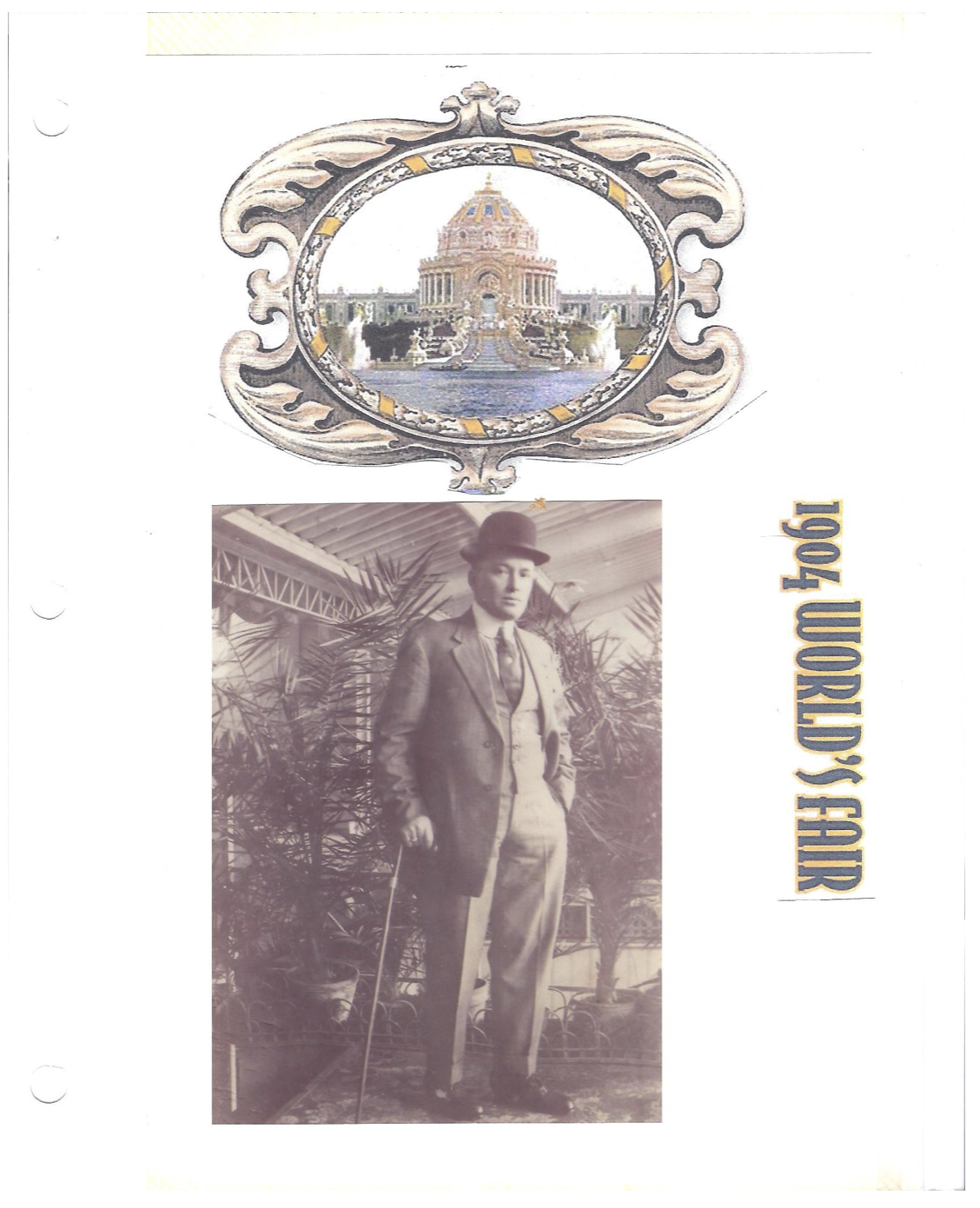

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

May 31, 2024

Fiat Lux

Featured Trade:

(ANOTHER AI SERVER STOCK)

(DELL), (SMCI), (NVDA), (ORCL)

Nvidia CEO Jensen Huang complimented Dell by saying it’s a “great partnership” at its GTC conference and said that “nobody is better at building end-to-end systems of very large scale for the enterprise than Dell.”

Words like this go a long way in this industry let alone partnering with the best tech firm in the industry.

To have the best CEO in tech flatter your products means staying power but in the short-term, the stock has come too far too fast.

That’s what this deep selloff is about as Dell shares.

The stock is down 19% today but that doesn’t diminish the 207% gain in the past 365 days.

Dell has reinvented itself as an AI stock and specifically a company specializing in servers that serve AI chips.

The company has done so well lately that they are gearing themselves up for inclusion into the S&P index.

That would honestly be a game-changer for the stock.

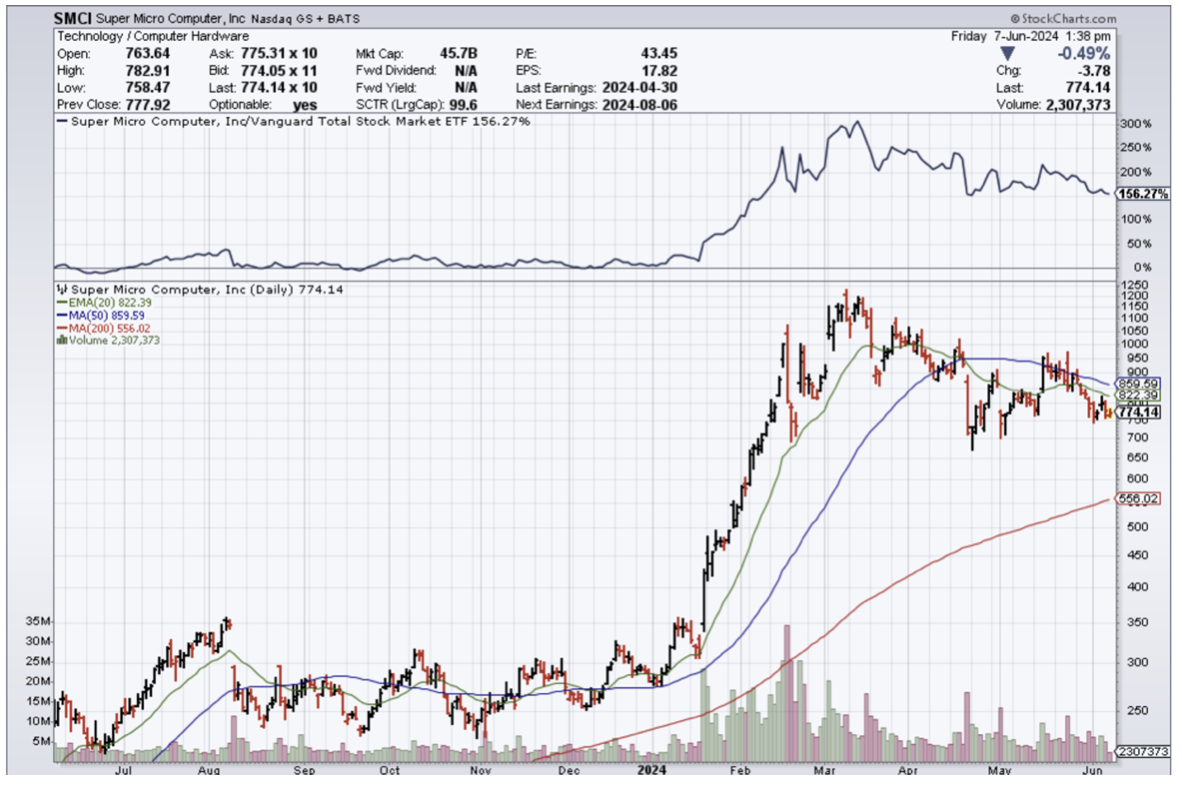

Super Micro Computer (SMCI), another play on AI servers, was added in March, despite having a market cap below $50 billion.

Confirmation of improving growth prospects could continue to support a stock that’s at a record high while trading at a discount to other tech favorites.

Dell recently generated excitement by unveiling a line of PCs optimized for AI, adding to hopes that such features could prompt a long-awaited upgrade cycle from customers and businesses. HP even reported the first increase in PC sales in two years.

The firm has become a critical cog in the AI ecosystem.

Both the PC and the server businesses will drive growth in coming years, and that’s supportive of both the stock price and the multiple.

I believe we can now say the company has turned itself into both a growth and a value play since the growth story is still under-appreciated and the multiple is very low relative to other AI plays.

The S&P 500 is rebalanced quarterly, with the next scheduled to occur in June. Becoming a component would open Dell up to a fresh avalanche of investors who use the S&P 500 as their benchmark, as well as flows into passive funds that track the index.

All things considered, I believe this is one of the best tech stocks to play server momentum, sky-rocketing storage demand, and an improving PC market.

Dell is becoming an increasingly strategic vendor in AI, but there’s a lot more appreciation for this than there was a few months ago.

Demand for AI systems remains healthy, but other parts of the business remain cyclical, and if we see a macro downturn, even a growth story as powerful as AI could slow down.

I like that investors are looking through the bad PC numbers and only focusing on Dell's AI server story.

This means that readers should be dissuaded from reach for this tech play even though they have a saturated computer business.

The most important and hardest endeavor in the tech industry is to reinvent when business is slowing down.

Only so many firms can pull it off and now that the pivot is into AI, companies are scrambling like Google and Apple in order to stay relevant.

Dell is a stock that should be bought on dips now and I feel funny saying that because that wasn’t the case not too long ago.

Another stock that has reinvented itself with the AI craze has been Oracle (ORCL).