Mad Hedge Technology Letter

December 11, 2023

Fiat Lux

Featured Trade:

(DIGITAL MARKETING REBOUND)

(PINS), (SNAP)

Mad Hedge Technology Letter

December 11, 2023

Fiat Lux

Featured Trade:

(DIGITAL MARKETING REBOUND)

(PINS), (SNAP)

In prior years, big social media companies were the class of the tech industry.

It’s not so much like that today but they still have highly profitable models and a lot of juice left in the tank.

I do believe big social media companies will still do well in 2024 because they have proved themselves through the test of time.

However, now that media has fragmented, smaller social media stocks that are tailored to a certain niche are due to overperform in 2024.

This is happening at a time when cord-cutting is accelerating and the lowering of interest rates next year could serve as a catalyst to higher share prices for the likes of Snap and Pinterest.

Then there is the wider trend of potential beneficiaries from a recovery in the digital advertising market.

As marketing clients look to redeploy their dollars following post-pandemic cutbacks, stocks such as Snap and Pinterest could be next in line for a payday.

For Pinterest, I have been highly bullish on them ever since Elliot Management scooped them up and revamped management.

Snap is in the sweet spot catering to a growing demographic who are seeing their earning power rise as they come of age.

Still, the industry faces risks given an uncertain economic backdrop.

I anticipate higher ad sales of online retail platforms that will jump 20% versus last year. Moreover, online ad growth should accelerate meaningfully in 2024.

I believe the media will obtain about $17 billion in political ads next year when many U.S. campaigns will be in full swing.

It’s hard not to see social media stocks winning out in a presidential election year in one of the most polarizing contests in recent memory.

More and more consumers spend most of their days online and most of those funds likely will be spent on digital platforms where these consumers station eyeballs.

And worldwide, ad spending is expected to jump 8.2% next year, a sharp acceleration from the 4.4% gain anticipated this year.

Marketers spend money on platforms in direct proportion to the number of users that they attract.

Digital platforms, which include search, social, commerce, retail media, and digital video platforms, will account for about 64% of all advertising in 2023.

Digital platform-focused companies are expected to collectively grow 11%, led in large part by retail media, which will account for about $42 billion in advertising revenue in 2023, up 20% over 2022.

Traditional television, both national and local, will experience declines over the year.

The setup is boding nicely for these smaller social media stocks and that is not to say stocks like Meta and Google will perform poorly.

Realistically, the Nasdaq can’t move higher without the Magnificent 7, but based on pure percentage gains, I do believe Snap and Pinterest have a good chance to beat out the heavyweights next year.

There is a high likelihood that tech will lead this next bull market because they are the largest winner from the lowering of interest rates.

Not only will tech IPOs be back in vogue, but the prototypical tech zombie firms that burn cash will pop up again showing that investors reserve large amounts of capital for potential tech growth companies.

Part of the capital allocation will be to Snap and Pins which are solid companies with a great brand image.

I believe 2024 will be a year where investors pile into these 2 stocks much like how investors piled into Uber in 2023.

Mad Hedge Technology Letter

November 30, 2022

Fiat Lux

Featured Trade:

(WEAK SALES FOR 2023)

(CRWD), (APPL), (SNAP), (DASH)

Tech growth needs a timeout.

The recent earnings report from cyber security software firm CrowdStrike (CRWD) illustrates the difficulty for firms to project strength in forward guidance.

2023 isn’t looking so rosy for selling security software.

CRWD management offered us weak guidance citing a weakening macroeconomic picture and specifically telling us that small businesses are reluctant to sign new contracts for 2023.

The macroeconomic picture at best isn’t getting better, therefore, some of the forward guidance is coming in tepid.

The natural reaction is for tech stocks to sell off.

In 2022, it’s never been more difficult being a tech CEO and some of the best tech growth companies are getting haircuts that we used to never see before.

Even more worrisome is that tech companies like Apple and Twitter are starting to cannibalize each other because tech is now perceived as a zero sum game more than at any other time I can remember it.

Firms simply don’t think the pie is big enough to share.

This is why ecosystems like Apple and others are executing policies that directly hinder competition.

Unfortunately, cyber security is another add-on that is being sacrificed as tech companies become leaner and meaner.

Many tech companies can still function by skimping on the security defenses.

Shaving the fat to the bone is what we are currently seeing and that doesn’t bode well in the short term for tech stocks that are used to thriving in the excesses.

Another example is Snapchat (SNAP), which ordered back staff to a 4-day in-office work week starting February.

And it’s not just Snapchat or CrowdStrike.

The belt tightening has been broad-based in technology with DoorDash cutting another 1,250 jobs today.

Many of these growth companies over-hired during the government-mandated lockdowns and now are regressing back to the mean.

Since there are no more lockdowns in non-Chinese countries, there is no need for the giant number of DoorDash food deliverers.

Yet the US consumer is still spending even if they get less for each incremental $1 spent.

CrowdStrike reported annual recurring revenue (ARR) of $2.34 billion, up 54% year over year. The company also added 1,460 net new subscription customers for the quarter.

In high times, CrowdStrike and the tech growth with superior business models are unique and stand out.

However, in overwhelming macroeconomic weakness, CRWD gets lumped in with the rest.

I don’t recommend buying CRWD on the dip even if it feels cheap.

The peak CRWD share price almost reached $300 meaning the current stock price is only around 35% of what it once was.

Tech growth will overshoot to the upside when it finds it mojo again, which won’t come back until sometime in 2023.

The lockdowns brought forward a tsunami of demand, revenue, and momentum.

Now we are experiencing the reversing of those tailwinds which is why the stock price has suffered.

Avoid tech growth for now, they will have their time in the sun once again once the headwinds have been digested and CRWD should be on your list for a tech growth stock to purchase on the way up.

Global Market Comments

October 24, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MY SECRET MARKET INDICATOR),

(SPY), (USO), (TSLA), (TBT), (NFLX), (FXY), (SNAP)

I have access to inside information that is worth far more than any other technical or fundamental data out there.

It is almost always right and has made fortunes for me over the year, the dreams of avarice.

If the SEC knew about it, they would lock me up and throw away the key.

Here it is. But first, let me tell you about the performance it has delivered.

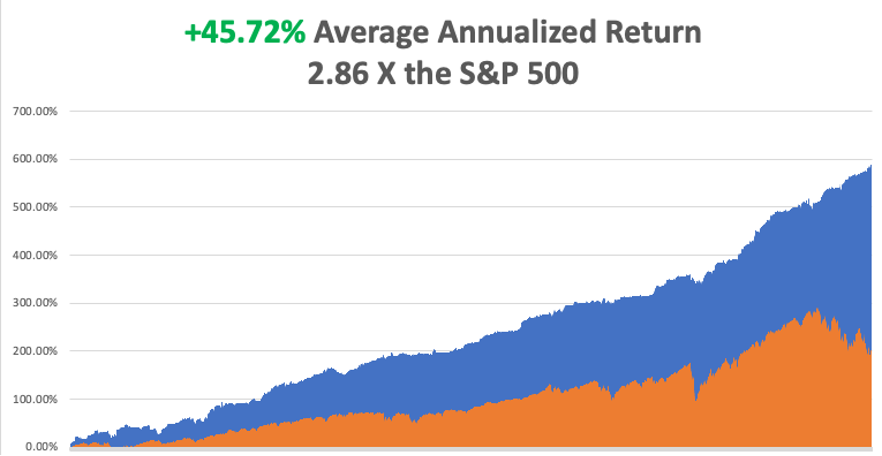

With some of the greatest market volatility in market history, my October month-to-date performance ballooned to +6.55%.

I used last week’s option expiration to take profits on my longs in JP Morgan (JPM), Visa (V), and Tesla (TSLA), and my one short in the S&P 500 (SPY). That leaves me with only one short in the (SPY) and 90% cash.

My 2022 year-to-date performance ballooned to +76.23%, a new high. The Dow Average is down -14.37% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +76.50%.

That brings my 14-year total return to +586.79%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.72%, easily the highest in the industry.

So here is my unfair advantage:

I get to see what my own customers do, and I’m the only one who sees it.

For my own subscribers are among the most highly trained and disciplined in the market. 50% a year profits are common and every year, I learn of a couple of 1,000% profits (or 10X returns).

And here is what my customers are telling me today.

The end of the bear market is near. In fact, a “Big Turn” across all asset classes may be upon us.

Bonds are about to bottom out and yields peak. The US dollar may be double-topping. Commodities are crawling off a bottom. Price earnings multiples for stocked have just cratered from 21X to a decade low of 16X. Many stocks, like Tesla are trading at the lowest multiples in their lives.

Thus, the demand for LEAPS recommendations that offer tenfold two-year returns on far more modest equity appreciation has been skyrocketing.

I can’t blame them.

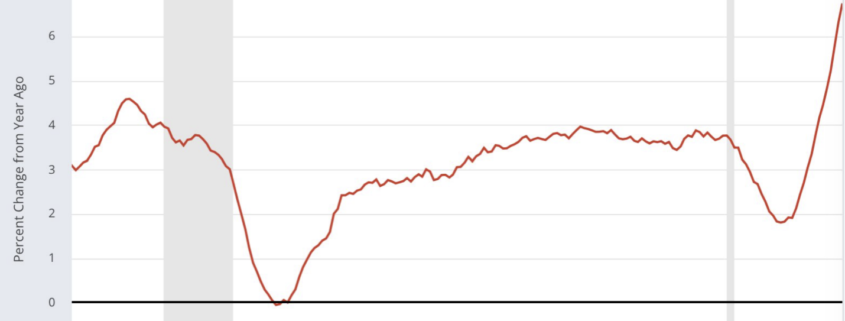

A final capitulation in the bond market is fast approaching. The United States Treasury Bond Fund (TLT) has collapsed by $88, from $180 to $92, or some 48.89%, covering the last six points in two days.

Ten-year yields have rocketed from 2.55% to 4.43% since August. The 2X short bond ETF (TBT) has spiked from $14 to $39 in a year. If you don’t cover the bond market on a daily basis, you may not know this.

It just so happens that I do.

It's an old investment nostrum that if you want to know what stocks are going to do, then take a close look at the bond market.

As Winston Churchill once said, “This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”

If you believe that the last interest rate hike in this cycle is only two months off, and we see interest rate cuts after that, then you need to be buying stocks now. You may be risking 10% of downside if you do, but miss out on 100% of upside if you don’t.

Here's another market old reliable. Markets always move more than you expect.

These may all sound like bold predictions. But then my followers are coming off of the best year for trading and investment in their entire lives. Confidence begets confidence.

If you are searching for global contagion, you don’t have far to look. The Japanese yen has cratered some 24% this year and is down by half from its last peak. That’s because the Bank of Japan, one of my old haunts, remains stubbornly insistent that ten-year JBG yields remain pegged at 0.25% while the US was raising from 0.25% to 4.43%.

You have to wonder what they are smoking in the Land of the Rising Sun. Their goal was to create a massive export boom with an ultra-cheap currency and runaway inflation with all the money printing. So far it hasn’t happened. GDP growth in Japan is stuck at snail-like 1.7%, while inflation remains a lowly 3.00%.

Go to Japan for the sushi, the public baths, and the Kurosawa samurai movies, not for inspiration on economic policy, which has been a disaster for 45 years. It’s tough to prosper against a gail-force demographic headwind.

Foreign exchange markets are easy to trade. You just follow the money and pile into the currency with the best yield advantage. Right now, that happens to be the US dollar (UUP).

Why wasn’t I selling short the Japanese yen (FXY) earlier this year? Because there were far better opportunities selling short US stocks, which I amply took advantage of.

It’s all in my numbers.

UK Government Collapses, with the resignation of prime minister Liz Truss in the shortest government in history. A new conservative leader will be elected next week. Truss took over a sinking ship. Her promised tax cuts delivered a fall in the British pound to a 40-year low. No matter what any future leader does, the UK standard will drop by half in the coming years, thanks to Brexit. THE HEAD OF LETTUCE WON!

30-Year Fixed Rate Mortgage Hits an Eye-popping 7.4%, in a clear Fed effort to shut down the real estate market. If this doesn’t kill the economy, nothing will. But home prices are nowhere near to 50%-70% declines seen in 20098-2011.

Existing Home Sales Plunge 23.8% YOY, in September, in the eighth straight month of sales declines. There are 1.2 million homes for sale, a six-month supply. The median home prices rose to $384,800.

Housing Starts Hit Two-Year Low, as the luxury end takes a hit. Starting families can no longer buy more houses than they can afford.

US Budget Deficit Drops by Half, after the sharpest decline in government spending in history. The red ink shrank from $2.78 trillion to only $1.38 trillion. It’s why I think the bond market may soon be bottoming out, with the (TLT) at $92 and the (TBT) at $38. A trillion here, a trillion there, and sooner or later, it adds up to a lot of money.

Ten-Year US Treasury Yields Hit 20-Year High, at 4.43%. If you’re waiting for rates to peak before buying stocks, it’s not yet. I’m looking for 4.50% before the crying is all over.

Fed Beige Book Says the Economy is Growing Modestly, an improvement from the last one. Travel & tourism is booming, auto sales are sluggish, and retail spending is flat. Manufacturing is steady, thanks to easing supply chain problems. High mortgage rates are a problem. Labor is still tight. It’s a very mixed report.

Tesla Earnings Beat Estimates for the 13th consecutive quarter profitability, taking the shares down 5%. Revenues came in at 24 billion, while units sold hot 340,000. The strong dollar is weakening Chinese and European sales. Tesla is still a decade ahead of the competition and boasts a global footprint. Production could hit 450,000-500,000 in Q4 once Austin and Berlin go to full production. The only competition will come from China. The Cybertruck comes out in 2023 and already has a million orders.

Netflix Earnings Blow Out, taking the stock up 15%, after a massive crackdown on password sharing. Some 30 million views are still watching the streaming channel for free. Some 2.41 new subscribers joined in Q3. The shift to advertising is next. Buy (NFLX) on dips.

SNAP Dives by 25%, thanks to a horrific earnings shortfall. Advertising Demand went from overwhelming to non-existent practically overnight. Small-cap growth is still being punished severely for any disappointments. The company is cutting 20% of its staff. Avoid (SNAP).

Supply Chain Problems are Disappearing, as two years of port congestion ease. A slowing economy is helping. After a year, I finally got my sofa from Vietnam. Overorders are coming back to haunt big retailers.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 24 at 8:30 AM, the S&P Global Flash PMI for September is released.

On Tuesday, October 25 at 7:00 AM, the S & P Case Shiller National Home Price Index for July is out.

On Wednesday, October 26 at 8:30 AM, New Home Sales for September are published.

On Thursday, October 27 at 8:30 AM, Weekly Jobless Claims are announced. US Q3 GDP is also announced.

On Friday, October 28 at 8:30 AM US Personal Income & Spending is printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, back in 2002, I flew to Iceland to do some research on the country’s national DNA sequencing program called deCode, which analyzed the genetic material of everyone in that tiny nation of 250,000. It was the boldest project yet in the field and had already led to several breakthrough discoveries.

Let me start by telling you the downside of visiting Iceland. In the country that has produced three Miss Universes over the last 50 years, suddenly you are the ugliest guy in the country. Because guess what? The men are beautiful as well, the decedents of Vikings who became stranded here after they cut down all the forests on the island for firewood, leaving nothing with which to build long boats. I said they were beautiful, not smart.

Still, just looking is free and highly rewarding.

While I was there, I thought it would be fun to trek across Iceland from North to South in the spirit of Shackleton, Scott, and Amundsen. I went alone because after all, how many people do you know who want to trek across Iceland? Besides, it was only 150 miles, or ten days to cross. A piece of cake really.

Near the trailhead, the scenery could have been a scene from Lord of the Rings, with undulating green hills, craggy rock formations, and miniature Icelandic ponies galloping in herds. It was nature in its most raw and pristine form. It was all breathtaking.

Most of the central part of Iceland is covered by a gigantic glacier over which a rough trail is marked by stakes planted in the snow every hundred meters. The problem arises when fog or blizzards set in, obscuring the next stake, making it too easy to get lost. Then you risk walking into a fumarole, a vent from the volcano under the ice always covered by boiling water. About ten people a year die this way.

My strategy in avoiding this cruel fate was very simple. Walk 50 meters. If I could see the next stake, I proceeded. If I couldn’t, I pitched my tent and waited until the storm passed.

It worked.

Every 10 kilometers stood a stone rescue hut with a propane stove for adventurers caught out in storms. I thought they were for wimps but always camped nearby for the company.

One of the challenges in trekking near the north Pole is getting to sleep. That because the sun never sets and its daylight all night long. The problem was easily solved with the blind fold that came with my Icelandic Air first class seat.

I was 100 miles into my trek, approached my hut for the night and opened the door to say hello to my new friends.

What I saw horrified me.

Inside was an entire German Girl Scout Troop spread out in their sleeping bags all with a particularly virulent case of the flu. In the middle was a girl lying on the floor soaking wet and shivering, who had fallen into a glacier-fed river. She was clearly dying of hypothermia.

I was pissed and instantly went into Marine Corp Captain mode, barking out orders left and right. Fortunately, my German was still pretty good then, so I instructed every girl to get out of their sleeping bags and pile them on top of the freezing scout. I then told them to strip the girl of her wet clothes and reclothe her with dry replacements. They could have their bags back when she got warm. The great thing about Germans is that they are really good at following orders.

Next, I turned the stove burners up high to generate some heat. Then I rifled through backpacks and cooked up what food I could find, force-fed it into the scouts, and emptied my bottle of aspirin. For the adult leader, a woman in her thirties who was practically unconscious, I parted with my emergency supply of Jack Daniels.

By the next morning, the frozen girl was warm, the rest were recovering, and the leader was conscious. They thanked me profusely. I told them I was an American “Adler Scout” (Eagle Scout) and was just doing my job.

One of the girls cautiously moved forward and presented me with a small doll dressed in a traditional German Dirndl which she said was her good luck charm. Since I was her good luck, I should have it. It was the girl who was freezing to death the day before.

Some 20 years later, I look back fondly on that trip and would love to do it again.

Anyone want to go to Iceland?

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Iceland 2001 with German Girl Scout

Mad Hedge Technology Letter

October 21, 2022

Fiat Lux

Featured Trade:

(A SMART WAY OUT)

(TWTR), (TSLA), (SNAP)

In a crazy turn of events, the US government is considering a national security review of Elon Musk’s Twitter (TWTR) takeover deal.

The review could potentially block the deal, saving Musk $44 billion.

I would say that Musk has been playing up this angle for quite some time.

It’s no coincidence that he started meddling in the Russian-Ukraine dialogue just recently.

Hatching a plan to tick off the US government enough for them to decide a perceived pro-Putin supporter cannot control the reigns of the biggest public discourse forum in the world would signify a massive victory for Musk.

We know Twitter isn’t worth $44 billion.

Snap issued terrible earnings which meant the new valuation of SNAP went from $19 billion to $13 billion company in one day.

Things are so bad at SNAP that they chose to not offer guidance for the 2nd straight quarter.

Musk has also voiced how he plans to reinstate former US President Donald Trump and fire 75% of the Twitter staff on the first day on the job.

He is doing his best to “achieve” a national security review which is executed by the Committee on Foreign Investment in the US (CFIUS).

CFIUS carries out security reviews if a "transaction threatens to impair the national security of the United States," according to federal regulations.

It’s also not a shocker that Musk recently threatened to stop supplying the Starlink satellite service to Ukraine.

If Musk is perceived to not be working for Ukraine, in the political world today, this means he can be labeled a pro-Russian, pro-Putin, anti-democratic, anti-American figure worthy of tech deals getting banned.

Ironically enough, he does the dirty work for the Chinese Communist Party because he operates a gigafactory in Shanghai which produces the most Tesla’s per factory.

Musk later backed down from his threat to stop deploying Starlink and agreed to continue to suffer losses operating the service.

Musk has been providing the service for free but has said SpaceX loses $20 million a month servicing Ukraine.

I must say that Musk has a serious pathway to wriggle himself out of this $44 billion deal.

If the deal is blocked, Twitter would be valued at around $15 billion-$20 billion range, possibly $25 billion is a stretch.

It would be a devastating blow for the Twitter management and shareholders.

Management would need to change instantly because of the brand damage and loss of credibility. Musk has attacked the management and staff at Twitter non-stop throughout this process.

A major restructuring is in the cards no matter what.

Job morale at the firm is at an all-time low as Twitter employees experience depression through a threat of possible termination upon Musk’s purchase.

The fiasco is essentially what Musk wanted in the first place and I could argue that the free PR he is receiving is worth at least $100 billion from start to finish.

Musk understands the more digital footprints he plants all around the internet, the richest man in the world will get many articles published about him. Just do a Google search of Musk and he’s everywhere.

Whether it is about spaceships or social media, Musk has launched himself front and center into almost every discourse including sensitive geopolitics to solving world hunger. He even said one time he wants to buy soccer club Manchester United.

About social media tech stocks, this is highly negative news for the valuations of other social media stocks like Meta (META), but this is great news for Tesla stock if Musk doesn’t need to sell Tesla stock to pay for the Twitter deal.

Musk still needs another $10 billion in financing to cover the balance of the deal to finish the deal.

Mad Hedge Technology Letter

September 19, 2022

Fiat Lux

Featured Trade:

(READING THE TECH TEA LEAVES)

(GOOGL), (FDX), (META), (SNAP)

Logistics company FedEx, although not a tech company, offers a fascinating insight into the health of the economy and the current state of the tech world.

Unfortunately for tech readers, the shipping company rang the alarm on the rapidly deteriorating state of the economy in August.

It’s my job to tell you how it will shake out for tech stocks.

FedEx’s earnings report disappointed signaling that tech stocks too, could be on the chopping block. I would agree with that too.

This debunks the myth of the “soft landing” that the US Central Bank likes to refer to with their challenge of high inflation. I believe the soft landing is priced into tech stocks, but not a hard landing yet.

The result is possibly more downside price action to tech stocks.

CEO Raj Subramaniam painted a gloomy picture of what to expect in terms of lower volumes.

FedEx could be the canary in the coal mine signaling ugly earnings for other large tech companies that do business around the world.

The tech companies that come to mind are Apple, Google, Facebook or Meta (META), and Snapchat (SNAP).

Raj is not the only executive who is spooking the tech market.

CEO of Alphabet or Google Sundar Pichai had his own gloomy opinion that adds insult to injury to the already negative sentiment prevailing in trader sentiment.

He said he feels “very uncertain” about the macroeconomic backdrop, and he is one of the few who has deep insight into the different layers of this complicated US economy.

He also warned that layoffs could be in the cards as the company seeks to boost its efficiency by 20% while staving off fierce economic headwinds and antitrust investigations.

A large element of such downbeat forecasts by executives is the roaring price hikes from everything like diapers to salami.

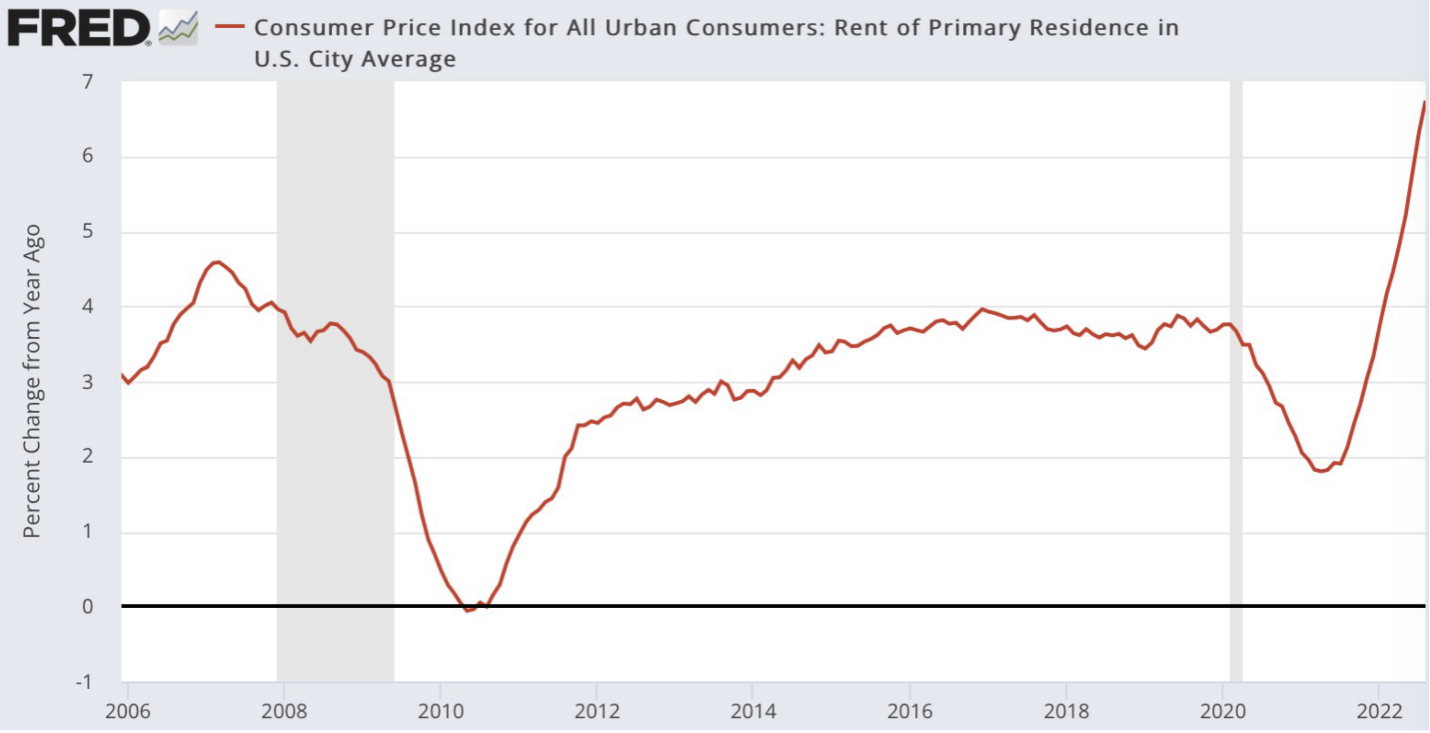

The one ironic tidbit that I took away from the last inflation report was that the recent explosion in inflation has been in rental housing.

If this is the case, then high-income individuals, who mostly own rental real estate, are passing on inflationary costs to their tenants who are strapped with a worse financial profile.

This means that high-income individuals still harness the resources to spend, spend, spend.

Why not go lease a new Maserati or Aston Martin?

If that’s the case, we could see this group pick up the slack and power spending all the way until Christmas which is a net negative for tech stocks because it delays the Fed pivot.

Warnings from Subramaniam and Pichai indeed have weight to them, but keep in mind that these businesses are optimized for scale and reflect the general situation of Americans, not just rich people.

High net worth individuals reloading the consumer bazookas don’t move the needle for the entire US economy, but they do have enough gunpowder to trigger another bout of inflation or rental increases to build on the already high inflation existing in US prices.

Short-term traders should focus on selling rallies in poor tech stocks as upside momentum cannot be sustained in the face of anticipated interest rate rises.