Mad Hedge Technology Letter

April 15, 2019

Fiat Lux

Featured Trade:

(XXXXX)

(SNAP), (FB), (PINS), (TWTR), (GOOGL)

Mad Hedge Technology Letter

April 15, 2019

Fiat Lux

Featured Trade:

(XXXXX)

(SNAP), (FB), (PINS), (TWTR), (GOOGL)

America is full – that is what domestic social media growth is telling us.

The once mesmerizing service that captured the imagination of the American public has soured in the country that created it.

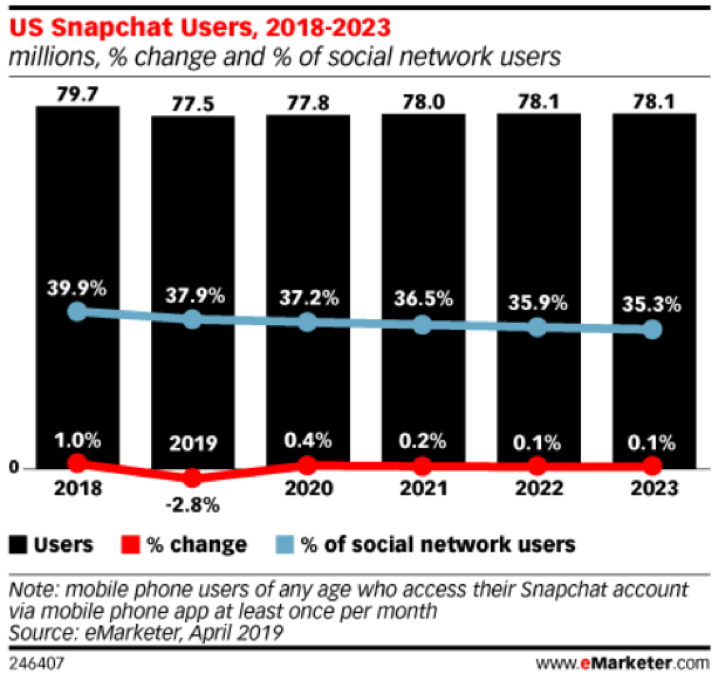

Online advertising consultant emarketer.com issued a report showing that Snapchat (SNAP), the worst of the top social media outlets, will lose users in 2019.

The 77.5 million users forecasted by the end of 2019 represents a 2.8% YOY decrease.

This report differs greatly from the report eMarketer issued just past August showing that Snapchat was preparing for a rise of 6.6% YOY in 2019.

The delta, rate of change, represents a massive downshift in expectations and the sentiment stems from the widespread saturation of social media assets.

Market penetration has run its course and the players have run out of bullets mainly targeting Generation Z.

These platforms have given up on baby boomers and Snap feels that pursuing the millennial demographic would be an exercise in futility.

Even more disheartening is that between 2020-2023, there will be only a minor uptick of user growth by 600,000 users clamping down on the impetus of a comeback of sorts shackling the business model.

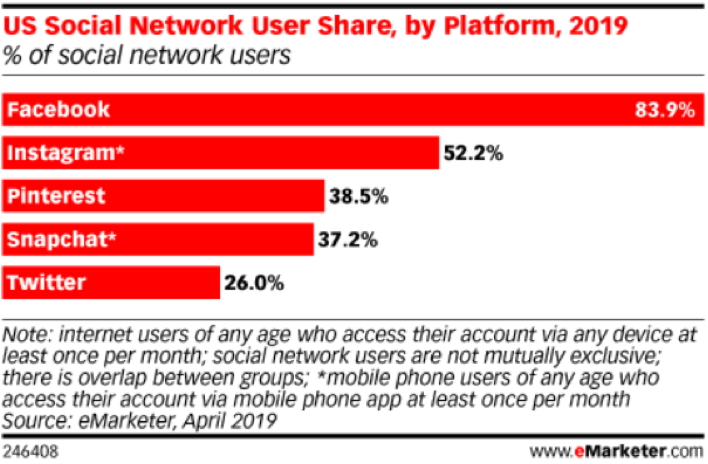

The trend is not mutually exclusive to Snap, Twitter or Facebook, social media as a group will only expand the overall user base by 2.4% in 2020 hardly satisfying the appetite for growth that these companies publicly advertise.

Remember that much of Instagram’s growth originates from borrowing Snapchat users by way of copying their best features.

Even with this dirty tactic, growth seems to be petering out.

Snap’s shares have made a nice double after peaking shortly over $25 after the IPO.

But the double was a case of investors believing that management and execution had hit rock bottom – the proverbial dead cat bounce in full effect.

Now investors will pause to reassess whether there is another reasonable catalyst to drive the stock higher.

First, investors will need to ask themselves, is Snap in for another double?

Absolutely not.

So where does Snap go from here?

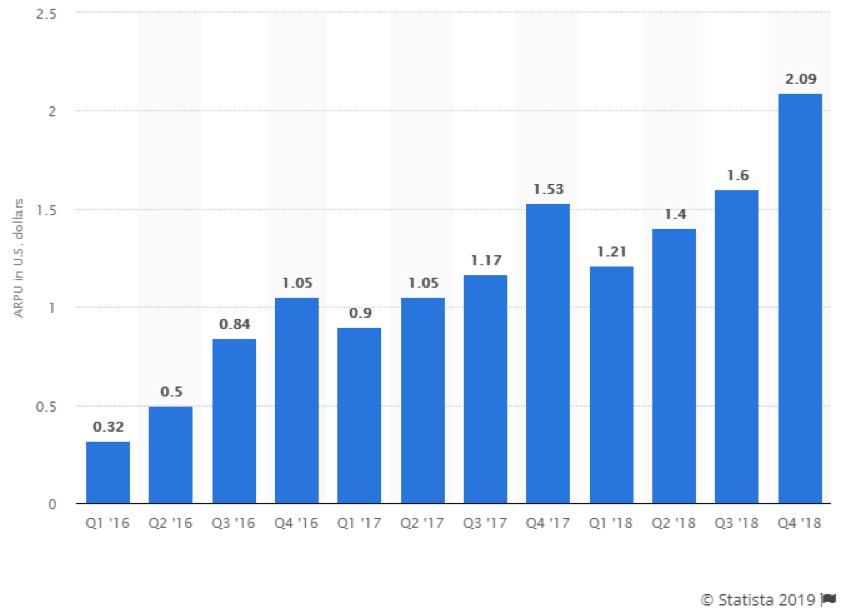

I believe they will borrow from the playbook of Mark Zuckerberg and attempt to emphasize supercharging average revenue per user (ARPU).

Whether the company arrives at this conclusion by chance or strategy, they must confront the reality that there are almost no other levers to pull if they want to perpetuate this growth story.

M&A is also off the table because the company is burning through cash.

Facebook’s (ARPU) came in at $7.37 last quarter indicating how Snap needs to make substantial headway in this metric with last quarter’s paltry (ARPU) at $2.09.

Essentially, management will conclude that each user isn’t absorbing enough ads because of declining user engagement.

Snap CEO Evan Spiegel will need to improve the pricing power charging advertisers at higher rates.

Obviously, the lack of an attractive platform resulting from poor execution and engineering problems needs a quick turnaround.

It’s not all smooth sailing for Facebook either, they keep chopping and reshaping strategy by the day attempting to minimize costs as the regulation burdens rot at the bottom line.

On the bright side, regulation hasn’t been as bad as initially thought – usership hasn’t dropped by orders of magnitudes.

In fact, Facebook’s users have shown a resurgent indifference to Facebook chopping up their data and repackaging it to 3rd parties, meaning Facebook has come through rather unscathed in the face of a PR storm.

There have even been recent reports of Zuckerberg being persuaded to start paying journalists for original content, a vast pivot for his hyped-up propaganda machine of being in the distribution business.

Juicing up (ARPU) is the lowest hanging fruit on offer for Snapchat and Facebook right now, overperforming in this sphere will improve financials and keep the mosquitoes away while affording them time to ponder how to reaccelerate user growth.

One outsized negative trend is that 90% of user growth appears to originate from undeveloped nations with a lack of discretionary spending power showing that this strategy has its limits.

Searching for another tool in its toolkit will redefine Snapchat, Twitter, and Facebook as we know it.

I would even classify it as an existential crisis.

Instagram have bought Facebook the most time to readjust its future direction highlighting that stealing Snapchat’s audience is still effective, expecting user growth to climb to 106.7 million US users, up 6.2% from 2018.

Instagram will continue its expansion by adding nearly 19 million new US users by 2023, but as much as it adds to its new social media asset, Facebook will be struggling for new net adds.

Snapchat is in dire straits and the stock market bubble could support the share price for up to another 8-12 months, but when the guillotine drops on Snapchat, the blood will smatter everywhere.

The company also plans to introduce a gaming service to take advantage of the popularity with its core users, Generation Z.

This should be the trick that breathes life into operating margins and (ARPU) which is why I believe the stock will hold up for the next period of time.

But with the gaming initiatives also comes rampant competition with the likes of Alphabet (GOOGL) and don’t forget Fortnite is still the 800-pound gorilla.

These trends also bode negatively for Pinterest (PINS) who might be going public as the last shot of tequila is downed at the after party.

Global Market Comments

February 1, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF KING COAL),

(KOL), (PEA),

(THE BRAVE NEW WORLD OF ONLINE RETAILING),

(SNAP), (GPRO), (APRN), (SFIX)

Mad Hedge Technology Letter

January 8, 2019

Fiat Lux

Featured Trade:

(WHY I SOLD SHORT APPLE),

(AAPL), (FB), (SNAP), (SQ), (AMZN), (BB), (NOK)

Apple (AAPL) needs Jack Dorsey to save them.

That is what the steep sell-off is telling us.

Lately, Apple’s tumultuous short-term weakness is indicative of the broader mare’s nest that large-cap tech is confronting, and the unintended consequences this monstrous profit-making industry causes.

These powerful tech companies have sucked out the marrow of the innovative bones that the American economy represents, applying this know-how to pile up ceaseless profits to the detriment of the incubational start-ups that used to be part and parcel of the DNA of Silicon Valley.

In the last few years, the number of unicorns has been drying up rapidly on a relative basis to decades of the ’90s and the early 2000s – this is not a startling coincidence.

The mighty FANGs were once fledging start-ups themselves but have become entrenched enough to the point they transcend every swath of culture, society, and digital wallet now.

Becoming too big to boss around has its competitive advantages, namely harnessing the hoards of data to destroy any competition that has any iota of chance of uprooting their current business model.

And if these large tech companies can “borrow” the innovation that these smaller firms cultivate, they wield the necessary resources to undercut or just decapitate the burgeoning competition.

The net effect is that innovation has been crushed and the big tech companies are milking their profits for what its worth.

Fair?

Not at all.

But tech has never been a fair game and going to a gun fight with a knife is why militaries incessantly focus on technology to accrue a level of firepower head and shoulders above their peers.

The career of Co-Founder of Jet.com, an e-commerce platform bought by Walmart for $3.3 billion in 2016, perfectly illustrates my point.

Marc Lore was born from the mold of leaders such as Amazon (AMZN) founder Jeff Bezos, leveraging the wonders and functionality of the e-commerce platform to construct a thriving business empire.

Quidsi, an e-commerce company, was founded by Marc Lore on the back of Lore maxing out personal credit cards to rent trucks to head to wholesale stores up and down the East coast to buy diapers, wipes, and formula in large quantities.

Under the umbrella of Quidsi, diapers.com and soap.com were successful e-commerce businesses and a segment that Amazon hadn’t cracked yet.

CEO of Amazon Jeff Bezos identified Lore as a mild threat to his low-end pricing, high-volume business empire.

Yes, this was a market grab, but to avoid a looming and an escalating price war, Amazon bought Quidsi for $500 million and $45 million of debt leaving Lore with millions after repaying earlier investors but effectively neutering Lore and putting him out to pasture.

The best way to ensure there is not another Jeff Bezos is for Jeff Bezos to buy out the upcoming Jeff Bezos before he can get close enough to go for the kill.

While both Bezos and Lore extolled the acquisition with pleasantries, Lore later described it as a glass half empty scenario akin to a mourning.

Getting a golden parachute-like payment for innovation is the best-case scenario for these up and coming stars of tech.

Others aren’t as lucky.

The castle that Bezos built and this type of reaction to stunting competition cannot be quantified and has a net negative effect on the overall level of innovation in the tech sector.

Then there is the worst-case scenario for tech companies such as Snapchat (SNAP). They have been courted numerous times by Facebook (FB) and offered sweetened deals that most people would salivate over.

Each rebuff followed a further Facebook retrenchment onto Snapchat’s territory hoping that they would gradually tap out from this vicious headlock.

In return, Snapchat has had the Turkish carpet pulled out from underneath them and most of their in-house innovation has been borrowed by Facebook’s subsidiary social media platform Instagram.

During this time span, Snapchat’s share price has nosedived and the defiant Snapchat management has lost the momentum and bravado that was emblematic to their business model.

Innovation has also been strangled in Venice, California as declining usership has been partly due to a lack of fresh features and an emphasis on profit creation instead of innovation that led to a botched redesign and sacking of 100 engineers.

Then there is that one's company, two's a crowd and three's a party and Snapchat’s growth model trailed Facebook and Twitter who took advantage of the era of zero regulation to build usership and brand awareness.

Snapchat was late to the feast and has suffered because of it.

The climate and mood for social media have significantly soured in the past six months and have tainted this whole niche sector with one toxic stroke with a brushstroke that has encapsulated any company within two degrees of this sector.

So where do the innovative problems start with Apple?

Right at the top with CEO Tim Cook.

Apple is known for brilliantly rewriting history and not fine-tuning it.

This is why I have preached the emphatic value of erratic but visionary leaders such as Steve Jobs and Elon Musk.

They take big risks and do not apologize for their smoking weed on podcasts and laugh about it.

Investors put up with these shenanigans because these leaders understand the scarcity value of themselves.

They don’t play it safe even if profits are the easiest option.

To save Apple, Apple would need to hire Square and Twitter CEO Jack Dorsey to innovate out of this mess.

The stock would double from here because Dorsey would bring back the innovative juices that once permeated through the corridors in Cupertino through Job’s genius ideas.

Under Cook’s tutelage, Apple has made boatloads of cash, but they were going to do that anyway because of Steve Job’s creations.

However, Cook has presided over China rapidly encroaching on its revenue source and is over-reliant on iPhone revenue.

They had years to develop something new but now China is beating Apple at its own game.

Not only has the smartphone market sullied, but so has the relative innovation that once saw every iPhone iteration vastly different from the prior generation.

The petering out of innovative smartphone features has gifted time to the Chinese to figure out how to snatch iPhone loyalists in China with vastly improved devices but at a way lower price point.

The erosion of Samsung’s market share in China should have been a canary in the coal mine and China is in the midst of replicating this same phenomenon in India too.

And I would argue that this would have never happened if Steve Jobs was still alive.

Jobs would have reinvented the world two times over by now with a product that doesn’t exist yet because that is what Jobs does.

As it is, Cook, a great operation officer, is a liability and probably should still be an operations manager.

Cook blared the sirens in early January with a public interview saying that revenue would drop by $9 billion.

This was the first profit warning in 16 years and won’t be the last if Cook retains his position.

Cook has steered the mystical Apple brand careening into the complex dungeon of communist China and was late to react.

Jobs would act first and others would have to react to his decisions, a staple of innovation.

Sailing Apple’s ship into the eye of the China storm stuck out like a sore thumb once Trump took over.

Adding insult to injury, consumers are opting for cheaper Android-based phones that function the same as iPhones.

The 10% of quality that Apple adds to smartphones isn’t enough to persuade the millions of potential customers to pay $1000 for an iPhone when they can get the same job done with a $300 Android version.

Cook badly miscalculated that Apple would be able to leverage its luxury brand to convince prospective buyers that iPhones would be a daily fixture and can’t-miss product.

Even though it was in 2010, it isn’t now.

The type of price points Apple is offering for new iPhone iterations means that this version of the iPhone should be at least 35% or 40% better than the previous version giving the impetus to customers to trade-up.

Sadly, it’s not and Cook was badly caught out.

Therefore, it is confusing that Apple didn’t apply more of its mountain of capital and luxurious brand status to cobble together a game-changing product.

Cook could have put his stamp on the Apple brand and might not have the chance now.

Cook being an “operations guy” has gone to the well too many times and the narrative and direction of Apple is a big question mark going forward.

This is the exact time needed for some long-term vision.

What does this all mean?

The shares’ horrific sell-off means that it is in line for some breathing room from the relentless downward price action.

However, unless the geopolitical tornados can subside, Apple debuts a Steve Jobs-esque bombshell of a product, or Square (SQ) CEO Jack Dorsey takes over the reins in Cupertino, the share price has limited upside in the short-term.

Apple will not have the momentous and breathtaking gap ups until something is fundamentally changed in the house that Steve Jobs built and that is what the tea leaves are telling us.

This has led me to execute a deep-in-the money put spread to take advantage of this limited upside.

Apple is a great long-term hold, but even Cook is threatening this premise.

As Cook is stewing in his office pondering his uncertain future, he forgets what it was that got Apple to the top of the tech ladder – innovation and lots of it.

The Mad Hedge Technology Letter ranks innovation as the most important input and x-factor a tech company can possess.

Steve Jobs understood that, yet, failed to pass on this hard-learned but important lesson to his protégé.

If Apple stays on the same track, they risk being the next Nokia (NOK) or Blackberry (BB).

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

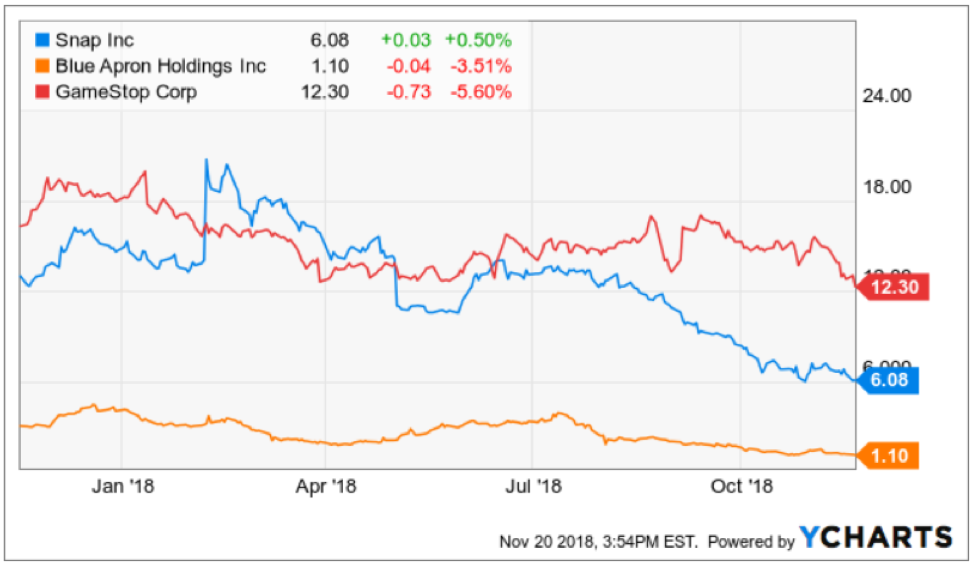

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

Mad Hedge Technology Letter

November 1, 2018

Fiat Lux

Featured Trade:

(LOOK AT ZENDESK FOR YOUR NEXT TEN BAGGER)

(ZEN), (RHT), (AMZN), (MSFT), (CRM), (IBM), (SNAP)

At the recent Mad Hedge Lake Tahoe Conference, I pinpointed software companies as a robust group of tech stocks that are the perfect late cycle investment in the economic environment we find ourselves in now.

To add some granularity about my thesis, I would like to start elaborating on an up-and-coming software stock that I find compelling and in the middle of a growth sweet spot.

And with the rapacious pullback, the tech sector has experienced as of late, this high-octane growth stock is poised to rev back up, albeit with more than your average volatility attached to its stock symbol.

If you can stomach the volatility, then Zendesk (ZEN) is the company for you to dip your toe in.

Zendesk is a customer service software offering solutions to clients through a flexible platform revolving around customer service tickets.

This $6 billion market cap tech firm thriving in the dodgy San Francisco Tenderloin district only need to be reminded of how fast a tech firm can be disrupted by stepping out of the office and experiencing ground zero of the San Francisco homeless movement in the scruffy Tenderloin.

I usually get lambasted for the lack of time I spend following budding tech firms, but you cannot blame me when the bulk of this year’s stock market gains have been extracted by the biggest and mightiest tech titans.

That does not mean all small tech is dead, but they certainly do have heightened existential risk because of the Amazons (AMZN) and Microsofts (MSFT) of the world, spreading their network effects far and wide.

International Business Machines Corporation’s (IBM) purchase of cloud company Red Hat (RHT) underscores the value of applying M&A to grow the top and bottom line, and the chronic bidders of these smaller minnows are usually the Amazons and Microsofts themselves who have the cash to dole out.

Salesforce (CRM) is always adding to its arsenal of integrated software companies that can scale up in the cloud, and Marc Benioff’s M&A strategy has thrived to devastating effect boosting the bottom and top line.

I must admit, tech does get the rub of the green over other industries because of the scaling effect afforded to profit poor tech companies.

The ample time to prove to investors they can snatch a growing user base, enhance product offerings, and develop an eco-system intertwined with recurring subscription products is not fair to other industries who are judged on different metrics mainly profits and profits now.

Well, life isn’t fair.

The addressable market is usually massive causing investors to stick with these burgeoning tech firms through thick and thin.

Zendesk is another company burning money, but let me tell you, they are no Snapchat (SNAP).

Operating margins are marching towards positive territory, meaning this outfit is well-run.

It was only at the beginning of 2015 when Zendesk’s operating margin registered -53%, and since then, they have dramatically reduced it to -36% at the end of 2016 and now -24% in 2018.

Gross margins next quarter will be hit a bit with its acquisition of Base CRM, headquartered in Mountain View, California and R&D offices in Krakow, Poland, offering a web-based all-in-one sales platform featuring tools for email, phone dialing, pipeline management, and forecasting.

Improving service offerings in the tech world usually means nabbing niche cloud companies that can easily be integrated into the larger eco-system and Base CRM, even though it has lower margins than Zendesk, is a nice pickup for the company boosting the top line while expanding cross-selling activities.

Then there is the sales revenue growth demonstrating all the hallmarks powerful software companies live up to with its 39% quarterly revenue growth.

Zendesk’s management has remarked that they fully expect to hit $1 billion in total sales by 2020 which is more than double the 2017 annual revenue of $430 million.

This year, Zendesk is forecasted to post just shy of $600 million in sales.

Large clients keep piling in hoping to modernize their customer service operations and wean themselves off the siloed legacy systems.

Disruption by some fresh newcomer in a disruptive industry that they operate in is usually the trigger forcing companies to spruce up their customer service software.

This path of migration will healthily continue for Zendesk reaffirming management’s thesis of $1 billion in sales by 2020.

Zendesk, flaunting off their innovation skills, identified the universal popularity of messenger app WhatsApp as an effective platform for its services and rolled out a product that integrates Zendesk services with WhatsApp.

This will allow businesses to manage customer service interactions and engage with customers directly on WhatsApp.

The customized integration links conversations between businesses and their customers on WhatsApp within Zendesk.

This move will allow Zendesk to stretch their tentacles further and wider while being able to provide faster support for customer service tickets which are incredibly time-sensitive.

Since management highlighted that WhatsApp is the go-to messenger in Asia Pacific and Latin America, there was no reason not to extend their offerings in a way that captures this vital userbase.

The WhatsApp pivot has been a nice addition with Zendesk’s management remarking that they “handle over 20% of our order status inquiries daily with WhatsApp and Zendesk, which is much faster than traditional methods.”

Omnichannel support within Zendesk’s platform will be key to securing the growth it needs to reach its $1 billion of sales milestone.

Innovation is the crucial ingredient in constructing the perfect products that can maximize customer service performance.

Its overseas exploits are not just a flash in the pan with its services supported in 30 languages and offices in 15 different countries. It all makes sense considering half their revenue is outside of America.

With IBM’s recent acquisition of Red Hat, buyers are still hunting for the right pieces to add to their portfolio.

The Red Hat purchase proved that demand still eclipses supply by a far margin.

Zendesk is one of those in the queue for a big buyer to swoop in with a mega offer.

It’s no guarantee that a company will pay a 63% premium like IBM did, but some sort of premium will be definitely warranted.

Zendesk offers the type of robust growth and premium cloud services that could easily fit into a bigger cloud player looking to improve their assortment of cloud tools.

This type of tailwind itself will naturally boost the stock by 5-10% alone if the macro picture can somehow manage to gain footing for the rest of the year.

As with the rest of tech, Zendesk dipped about 20% in the last 30 days but by no means does that mean this is a bad company with a weak future.

I would very much argue the opposite.

The weakness in sales offers a prime entry point in a fast-growing company that is part of the software and cloud movement that I have incessantly harped about.

If this company can show continued operating margins growth, maintain sales growth of above 30% YOY, and demonstrate product innovation, this stock will break out to higher levels.

As of now, that is exactly the road they are headed down.

Business abroad is doing so well that Zendesk recently splurged on a Europe, Middle East and Africa (EMEA) headquarters in Dublin, Ireland coined as the “the tech capital of Europe.”

Zendesk started with two employees in Dublin in 2012 and now boast over 300 employees occupying 58,000 square feet in a new office costing $10 million.

By 2020, Zendesk expects to build their Dublin branch to over 500 employees implying that the overseas pipeline is ripe for the taking.

I am highly bullish Zendesk and recommend that readers check out this attractive growth story.

![]()

Mad Hedge Technology Letter

October 11, 2018

Fiat Lux

Featured Trade:

(WHY SNAPCHAT SNAPPED),

(SNAP), (FB), (AMZN), (NFLX)