Global Market Comments

September 28, 2018

Fiat Lux

Featured Trade:

(WHAT WILL TRIGGER THE NEXT BEAR MARKET?)

(JPM), (SNE), (TLT), (ELD), (AMZN),

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON

GLOBAL STRATEGY LUNCHEON)

Global Market Comments

September 28, 2018

Fiat Lux

Featured Trade:

(WHAT WILL TRIGGER THE NEXT BEAR MARKET?)

(JPM), (SNE), (TLT), (ELD), (AMZN),

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON

GLOBAL STRATEGY LUNCHEON)

To paraphrase Leo Tolstoy in Anna Karenina, all bull markets are alike; each bear market takes place for its own particular reasons.

Now that the wreckage of the past financial crises is firmly in our rearview mirror, it is time for us to start pondering the causes of the next one. I’ll give you a hint: It will all boil down to excessive debt…again.

Global quantitative easing has been going on for a decade now, keeping interest rates far too low for too long. The unintended consequences will be legion, and the day of atonement may be a lot closer than you think.

The 1991 bear market was prompted by the Savings & Loan Crisis, where too many unsophisticated financial institutions in a newly unregulated world dreadfully mismatched asset and liabilities.

Every time I drive by a former Home Savings and Loan branch, with its unmistakable quilt decorations and accents, I remember those frightful days. Back then, when I looked at buying a home in San Francisco, the seller burst into tears when the price I offered would have generated a negative equity bill due for him.

The 2000 Dotcom crash can easily be explained by the monstrous amounts of debt provided to stock speculators. The 2008 crash was produced by massive, unregulated, and largely unknown lending to the housing sector through complex derivatives that virtually no one understood, especially the buyers.

So, here we are in 2018 nearly a decade out of the last crisis. Potential disasters are lurking everywhere under the surface while blinder constrained investors blithely power ahead. Once they metastasize, they rapidly feed into each other, creating a domino effect. They always do.

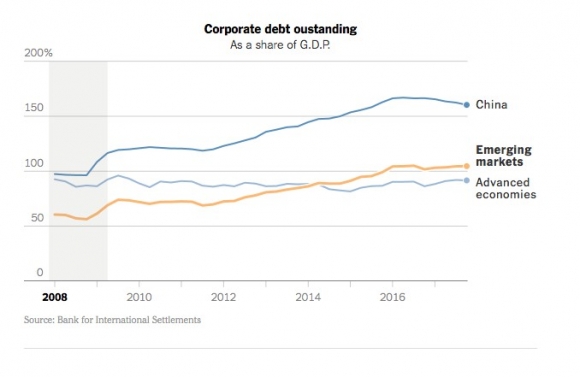

Emerging Market Debt

Lacking domestic capital markets with any real depth, companies in emerging economies prefer to borrow in U.S. dollars. When the dollar is weak that’s great because it means liabilities on the balance sheet shrink when brought back into the home currency. When the greenback is strong, the opposite happens. Dollar debt can grow so large that it can wipe out a company’s total equity.

This is already happening in a major way in Turkey, where the lira has plunged 50% in the past year, effectively doubling their debt. And once it starts, a global contagion kicks in as all emerging companies become suspect. This is not a small problem. Emerging market debt has rocketed from 55% to 105% of GDP since 2008.

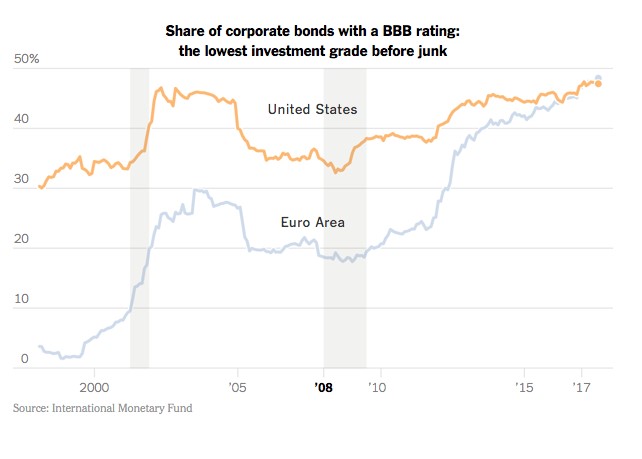

The Rise of Junk Borrowers

In recent years there has been a massive expansion in borrowing by marginal credits. This is taking place because fixed income investors are willing to accept a large increase in the amount of risk for only a small marginal rise in interest rates.

There is now $1.4 trillion in low grade BBB bonds outstanding, with one-third of this one downgrade away from junk. There has also been a dramatic rise in “covenant lite” issuance, which minimizes the rights of bond holders in the event of default. When the next round of trouble arrives, you can expect this market to shut down completely, as it did in 2008.

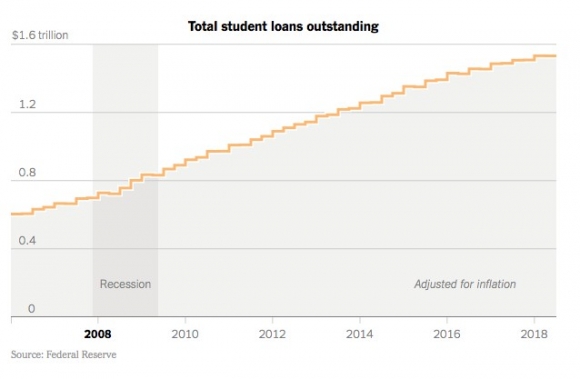

Student Loans

These have been the sharpest rising form of borrowing over the past decade, doubling to $1.5 trillion. Some 10% are now in default. This acts as a major drag on the economy as heavily indebted students don’t borrow, buy homes or cars, or really participate in the economy in any way, banned by lowly FICO scores. This is why millennials in general have been slow to enter the housing market for the first time.

Shadow Banking

Would you like to know today’s equivalent of subprime the lending that took the financial system down in 2008? That would be shadow banking, or off the books, unreported lending by hedge funds, private equity funds, and mortgage companies. Again, this is all in pursuit of high interest rates in a low interest rate world.

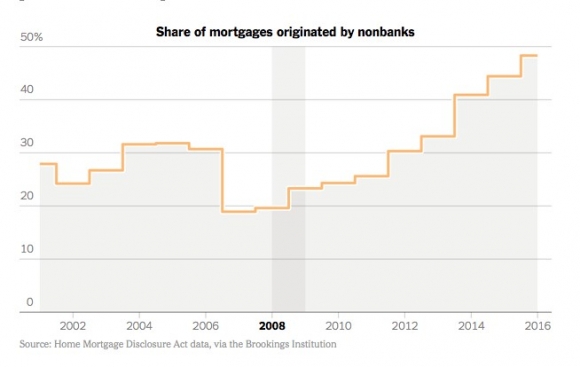

Yes, liars’ loans are back, just not to the extent we saw 10 years ago…yet. I’m waiting for my cleaning lady to get offered a great refi package again, just as she was in the run-up to the last crisis. How many of these loans are out there? No one has any idea, especially the Fed. As a result, nearly 50% of all mortgage lending is now from unregulated nonbank sources.

The Outlier

Remember when Sony (SNE) was almost put out of business by a hack attack from North Korea? What if they had done this to JP Morgan (JPM)? That would have created a chain reaction of defaults throughout the financial system that would have been impossible to stop. When this happened in 2008, it took the Fed three months to reopen markets such as commercial paper. If big bankers need a reason to lie awake at night, this is it.

I’m not saying that markets can’t go higher before they go lower. In fact, I dove back into Amazon (AMZN) only this morning.

However, as an Australian farmer told me on my last trip down under, “Be careful when you cross the field, mate. Deadly snakes abound.” Add up all the above and it will turn into a giant headache for investors everywhere.

Global Market Comments

March 26, 2018

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT WASHINGTON FINALLY MATTERED),

(THE IRS LETTER YOU SHOULD DREAD),

(PANW), (CSCO), (FEYE),

(CYBR), (CHKP), (HACK), (SNE)

(TESTIMONIAL)

Nearly two years ago, the Japanese government introduced the Individual Retirement Account for individual investors in Japan for the first time.

The move was part of Prime Minister Shinzo Abe?s multifaceted efforts to revive Japan?s economy, and could unleash as much as $690 billion in net buying into Japanese equities by 2018.

The move was inspired by American IRA?s, which were first introduced in 1981. After that, the Dow average soared by 25 times. It is amazing to what lengths people will go to avoid the taxman.

Starting October 1, 2013 individuals have been permitted to contribute up to ?1 million a year into Nippon Individual Savings Accounts (NISA) or some $8,000, while married couples can chip in ?2 million.

These funds are exempt from capital gains and dividend taxes for five years. At the same time, capital gains taxes will rise from 10% to 20%.

Thanks to a 22-year long bear market, only 7.9% of personal assets in Japan are currently invested in stocks, compared to 34% in the US. Individuals account for only 28% of the daily trading volume in Tokyo, while foreigners take up 63%. Still, that?s up from only 21% a year earlier.

Over the past 10 years, individuals sold a net $214 billion in equities, keeping their eyes firmly on the rear view mirror. Almost all of the funds were deposited into bank accounts yielding near zero.

Even 10 year Japanese Government Bonds are yielding only 0.41% as of today. That doesn?t buy you much sushi in your retirement.

Over the past three years, Japan has enjoyed having the world?s fastest growing industrialized economy. The latest data show that it is expanding at a white hot 3.5%, versus a far more modest 2% rate in the US, and only 0.5% in Europe.

Early indications are that the NISA?s are hugely popular. Japanese brokers have launched a massive advertising effort to promote the program, which promises to substantially boost their own earnings. Firms have had to lay on extra customer support staff to assist with online applications, where clueless investors have spent two decades in hiding. That certainly makes Japanese brokers, like Nomura (NMR), a buy. Another of my favorites is Sony (SNE).

To get some idea of the potential, take a look at how Merrill Lynch?s stock performed after 1981, which rose by many multiples. The bear market has lasted for so long that many applicants confess to investing in equities for the first time in their lives.

Since Shinzo Abe announced his candidacy for prime minister and his revolutionary economic and monetary program nearly four years ago, the Japanese stock market (DXJ) has soared by an amazing 176% in US dollar terms. The short Japanese yen 2X ETF (YCS) has similarly rocketed by a huge 232%.

Regular readers of the Mad Hedge Fund Trader have been mercilessly pounded to buy Japanese stocks and sell short the Japanese yen for the best of three years. I can almost hear ?Oh no, here comes another yen bashing piece!?

The need to bolster Japan?s retirement finances is overwhelming. It has the world?s oldest population, with some 26% of their 127.6 million over the age of 65.

The average life span in Japan is 82.6 years. That is a lot of people to support for a $6 trillion GDP. Thanks to plummeting fertility rates, the population is expected to decline to 106 million by 2055.

By yanking $690 billion out of the banks and moving out the risk spectrum, Abe?s new IRA?s provide additional means through which the economy can permanently return to health.

Higher stock prices will provide cheap equity financing for public companies, which can then reinvest in the domestic economy and create jobs.

I have written endlessly on the fundamental case for a strong Japanese stock market this year (to read my previous articles on yen, please click the following links: ??Rumblings in Tokyo?, ?New BOJ Governor Craters Yen??and ?New BOJ Governor Crushes the Yen?).

If you live long enough, you see everything.

After a 25-year hiatus, here I am finally back making money in the Japanese stock market once again.

Any sentient being couldn?t help but notice the specular results the Japanese stock market has produced so far in 2015.

The Nikkei Average is up a robust 11.7%, while the Wisdom Tree Japan Hedged Equity Fund (DXJ), which eliminates all of the underlying yen currency risk, has tacked on an impressive 13.2%. This compares to a US Dow average return for the same period of essentially zero.

So, is it too late to get in? Are we joining the tag ends of a party that is winding down? Or is the bull market just getting started?

To answer that question, you have to go to a 30 year chart for the Nikkei average which chronicles all of the violence, heartbreak and drama of the great Japanese stock market crash, and the budding recovery that has since ensued.

The bulls see a crucial triple bottom at ?7,500 that has spread out over ten years, from 2003 to 2013. The initial resistance for the bull market was at ?18,000. That level was decisively broken last week.

And as any long in the tooth technical analyst will tell you, the longer the base building, the longer the recovery.

It is no accident that this sea changing technical action is happening now. Last year rumors abounded that the Japanese government would mandate higher equity weighting by Japanese pension fund managers.

That is exactly what happened at the end of February. The government required pension fund managers to increase equity weightings from 8% to 25%, at the expense of their Japanese government bond holdings. I guess the 0.33% yield on the ten-year wasn?t exactly tickling their fancy.

To meet the new guidelines, managers have to buy $120 billion worth of stocks over the next two years.

That is a lot of stock.

Japanese pension fund managers are the world?s most conservative. Since they can no longer buy all the domestic bonds they want, they are investing in stocks that are essentially bond equivalents.

These include relatively high dividend yielding domestic defensive sectors, like pharmaceuticals, railroads, services, chemicals and foods. With the program only just starting, the Nikkei will be underpinned by local Japanese institutional buying, possibly for years. That eliminates your downside.

Enter the foreign investor. Gaijin mutual fund and hedge fund managers alike were net sellers of Japanese stock for all of 2014. They turned to net buyers only three weeks ago.

Guess what kind of stocks foreigners like to buy? The same kind they buy at home: technology stocks. Take a look at the charts below for Sony (SNE) and Canon (CAJ) and the breakouts there exactly match up with the timeline I described above.

Sony, in particular deserves special mention. Sony was the Apple of Japan during the 1980?s, and should have been the Apple of today. But the company lost its way after 1990, when the founder, my friend Akio Morita, passed away.

Succeeding management was dull, sluggish, and unimaginative. The world quit buying its top of the line stereo systems. As a result, its market capitalization plunged from $150 billion to only $10 billion.

The final indignity came when North Korean hackers almost wiped out the company last year when it released The Interview, a spoof on dictator Kim Jong-un.

These days, Sony is leading the resurgence of the Japanese stock market. Management modernized and westernized. It launched a range of new high tech products. It is selling at a dirt cheap 12X multiple. I also think it is safe to say that their hacking defenses are now state of the art.

It doesn?t hurt that when foreign investors think of buying Japan, picking up Sony is the first thing that comes to mind.

So the technicals and the supply/demand picture lines up, how about the fundamentals?

Go into Japan now, and you are betting that Prime Minister Shinzo Abe (I knew his dad), will succeed in his ?three arrows? plan for economic and financial reform. Insiders believe he can pull this off.

The December election gave him a continued mandate from the Japanese people. The Bank of Japan is also in his corner, implementing a monetary policy that is so aggressive that it was once thought unimaginable. Doubling the money supply in two years?

This is why the Japanese yen will continue to depreciate, which is also highly reflationary for the economy, and is the subject of my Trade Alert below to sell yen.

If all of this lines up, then the next target for the Nikkei is for it to add another ?10,000, up nearly 50% from here. Beyond that, the Japanese stock average is likely to take a run at its old 1989 high of ?39,000.

I remember the day it hit that level all too well.

The rock group Chicago was leading the charts with Look Away. The office at Morgan Stanley was packed with women wearing these big shoulder pads that made them look like football players. Huge sunglasses, neon colors and big hair were everywhere.

Like I said, if you live long enough, you see everything, even another Japanese bull market.