After a half-century in the markets, I have noticed that it is the investors with the correct long-term views who make the biggest money. My favorite example is my friend, Warren Buffet, who doesn’t care if an investment turns good in five minutes or five years.

Buffet’s Berkshire Hathaway (BRKB) is the largest outside investor in Apple (AAPL). And guess what his cost has been? By the time you add up the compounded dividends he has collected since he started buying the stock in 2011, it's zero. The value today? $15.5 billion.

Buffet didn’t buy Apple for its hardware, iPhone, or iTunes. He bought it for the brand, which has improved astronomically. Look at Berkshire’s portfolio and it is packed with brands, like American Express (AXP), Coca-Cola (KO), and Exxon (XOM).

When did Buffet last buy Apple? In May when it hit $130.

That’s why Warren Buffet is Warren Buffet and you are you.

While the inflation news last week has been great and it is likely to get better, I believe that investors are missing the bigger, more important long-term picture.

The fact is that markets are now discounting an earlier than expected end to the Ukraine War, much earlier.

I get constant updates on the war from the Joint Chiefs of Staff, Britain’s Defense Committee, and NATO headquarters and I can tell you that the war has taken a dramatic turn in Ukraine’s favor just in the last two weeks.

Russian casualties have topped 80,000, nearly half the standing army. They have lost 2,200 of their 2,800 operational tanks. Some 120 front line aircraft have been destroyed. This week, Ukraine attacked the principal Russian air base in Crimea, leaving the smoking ruins of seven more aircraft there.

Russia is in effect fighting a modern digitized war with 50-year-old Cold War weapons and it isn’t working. Its generals have no experience fighting wars against determined opposition. Putin would do better listening to the retired generals on CNN for military advice.

America’s High HIMARS (the M142 High Mobility Artillery Rocket System) has become the Stinger missile of this war. The Lockheed Martin (LMT) factory in Camden, Arkansas that makes these missiles is running 24/7 on doubled orders.

The sanctions against Russia have been wildly successful. The Russian economy is utterly collapsing. What oil they are selling now is at half price. Aircraft are being cannibalized for parts to keep others flying. Much of the educated middle class has fled the country. Draft dodging is rampant.

What does all this mean for you and me?

The commodity price spike the war prompted has ended and most are now in steep downtrends. Gold (GLD), where the Russians were major buyers, has been flat as a pancake. This has put our inflation numbers into freefall. Interest rate fears peaked in June and are now in the rear-view mirror.

As is always the case, markets have seen these developments and correctly ascertained their consequences far before we humans did (except for maybe me). It has been no surprise that they have been tracking the Russian defeat day by day and have been on an absolute tear since June 15.

Even small techs suffering 18-month bear markets have now begun major recoveries, with companies like Snowflake (SNOW), up 50%, Netflix (NFLX), up 39%, and Cathie Wood’s Innovation Fund (ARKK) up 57%. Even crypto has returned from the grave, with Ethereum (ETHE) up an eye-popping 105%.

But don’t go gaga over stocks just yet.

The Fed ramps up quantitative tightening in September to $95 billion a month and will deliver another interest rate hike. That's why I am running a double short in the bond market (TLT), (TBT) once again.

We also have the midterms to worry about which, with recent developments, promise to be more contentious than ever. Look for another round of tiring new election fraud claims.

That’s great because these events will give us good entry points lower down for trade alerts, not the short-term top we are looking at right now.

It helps that with ten-year US Treasury yields at 2.80%, it has an effective price earning multiple of 37, while stocks growing earnings at 10% a year boast a price earnings multiple of only 16. That sets up a massive, long stock/short bond trade which Mad Hedge will be pushing well on into 2023.

And you know what?

The smart guys I know in the hedge fund community are starting to model for the next Fed interest rate CUT. Markets will love it and discount this far in advance.

If you want to get on the train with me before it leaves the station, just keep reading this newsletter.

Yes, markets are now being driven by rate cuts and peace prospects, not rate rises and war!

Your retirement fund will love it.

I just thought you’d like to know.

CPI Dives to 8.5%, down 0.6% in July. The peak is in, and stocks rallied 500. Look for another drop in August, with gasoline prices falling daily. The 800-pound gorilla in the room has exited.

The Producer Price Index Dives 0.5%, confirming last week’s weak CPI number. And many core prices are indicating that we will get another drop when the August numbers are reported in September. It was worth another 300-point rally in the Dow Average, which is getting seriously overbought.

Consumer Inflation Expectations dive to 6.2% for the coming year and only 3.2% for three years. according to a New York Fed Survey. Expectations for food costs saw the largest decline. The CPI is out on Wednesday. No doubt a media onslaught over a coming recession has a lot to do with it.

Elon Musk Sells $6.9 billion worth of Tesla (TSLA) Stock, explaining the $100 drop in the shares last week. Ostensibly, this is to pay for Twitter if he loses his court case. Musk clearing took advantage of a 60% rise in (TSLA) to head off distress sales in the future. Musk also opened the door to share buy backs in the future. Buy (TSLA) on dips.

85,000 IRS Agents are Headed Your Way, but only if the government can hire them and only if you are a billionaire or a profitable large oil company. The rest of us will be ignored by this unpublicized portion of the Biden inflation bill.

US Dollar (UUP) Takes a Hit on CPI Report, which effectively showed that the US saw deflation in July. The greenback is pulling back the 20-year highs which gave you the cheapest European vacation in your lives. The prospect of interest rates rising at a slower pace is dollar negative. Buy (FXA) and (FXC) on dips.

Boeing (BA) Delivered its First 787 Dreamliner in a year, after long-awaited regulatory approval. The monster 30% rise in the shares off the June low predicted as much. A global aircraft shortage helps. Airbus is going to have to start earnings its money again. Keep buying (BA) on dips.

Weekly Jobless Claims Pop 12,000 to 262,000, a new high for the year. It’s not at concerning levels yet but is definitely headed in the wrong direction. Maybe it’s just a summer slowdown? Maybe not.

Shipping Container Charges are Plunging Everywhere, except in the US, which currently has the world’s strongest economy. It’s a sign that global supply chain problems are easing. But the US leads the world in demurrage, or delays, with New York the worst, followed by Long Beach. Import Prices are Plunging, thanks to a super strong dollar, taking more pressure off of inflation. They fell 1.4% in July according to the Department of Labor. Easing supply chain problems are helping. Biden has had the run of the table for months now

My Ten-Year View

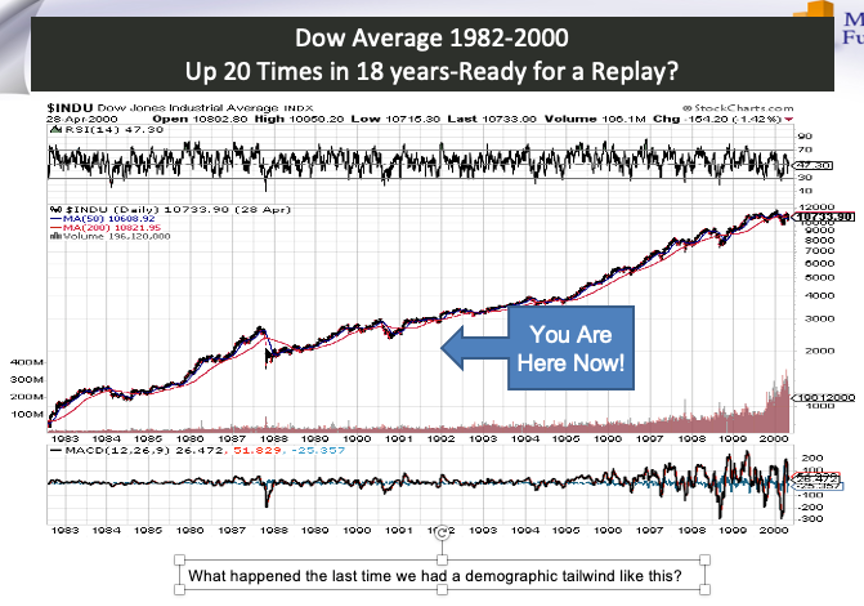

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil prices now rapidly declining, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

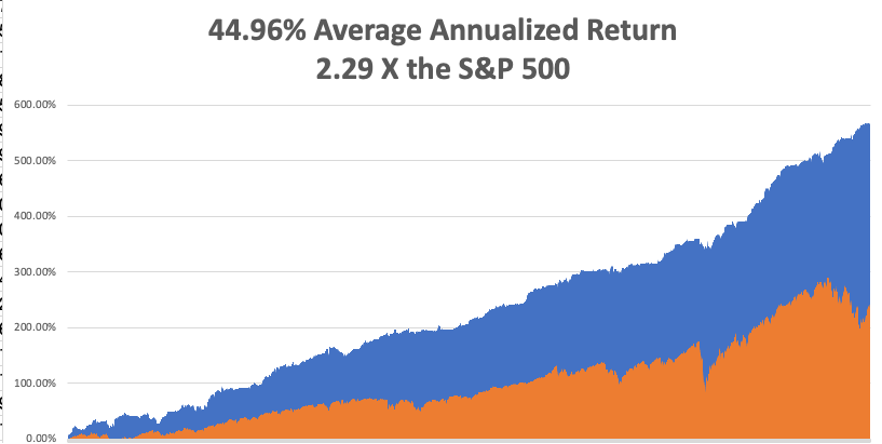

My August performance climbed to +2.14%. My 2022 year-to-date performance ballooned to +56.97%, a new high. The Dow Average is down -7.0% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 74.76%.

That brings my 14-year total return to 569.53%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.96%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 93 million, up 300,000 in a week and deaths topping 1,037,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, August 15 at 8:30 AM EDT, the New York Empire State Manufacturing Index for August is released.

On Tuesday, August 16 at 8:30 AM, the Housing Starts for July are out.

On Wednesday, August 17 at 8:30 AM, Retail Sales for July are published. At 11:00 AM the Fed Minutes from the last meeting are printed.

On Thursday, August 18 at 8:30 AM, Weekly Jobless Claims are announced. Existing Home Sales for July are announced. On Friday, August 19 at 2:00 the Baker Hughes Oil Rig Count is out.

As for me, while we’re all waiting for the dog days of August to end, it is time to reminisce about my old friend George Schultz who passed away last year at the age of 101.

My friend was having a hard time finding someone to attend a reception who was knowledgeable about financial markets, White House intrigue, international politics, and nuclear weapons.

I asked who was coming. She said Reagan’s Treasury Secretary George Shultz. I said I’d be there wearing my darkest suit, cleanest shirt, and would be on my best behavior, to boot.

It was a rare opportunity to grill a high-level official on a range of top-secret issues that I would have killed for during my days as a journalist for The Economist magazine. I guess arms control is not exactly a hot button issue these days.

I moved in for the kill.

I have known George Shultz for decades, back when he was the CEO of the San Francisco-based heavy engineering company, Bechtel Corp in the 1970s.

I saluted him as “Captain Schultz”, his WWII Marine Corp rank, which has been our inside joke for years. Now that I am a major, I guess I outrank him.

Since the Marine Corps didn’t know what to do with a PhD in economics from MIT, they put him in charge of an anti-aircraft unit in the South Pacific, as he was already familiar with ballistics, trajectories, and apogees.

I asked him why Reagan was so obsessed with Nicaragua, and if he really believed that if we didn’t fight them there, would we be fighting them in the streets of Los Angeles as the then-president claimed.

He replied that the socialist regime had granted the Soviets bases for listening posts that would be used to monitor US West Coast military movements in exchange for free arms supplies. Closing those bases was the true motivation for the entire Nicaragua policy.

To his credit, George was the only senior official to threaten resignation when he learned of the Iran-contra scandal.

I asked his reaction when he met Soviet premier Mikhail Gorbachev in Reykjavik in 1986 when he proposed total nuclear disarmament.

Shultz said he knew the breakthrough was coming because the KGB analyzed a Reagan speech in which he had made just such a proposal.

Reagan had in fact pursued this as a lifetime goal, wanting to return the world to the pre nuclear age he knew in the 1930s, although he never mentioned this in any election campaign. Reagan didn’t mention a lot of things.

As a result of the Reykjavik Treaty, the number of nuclear warheads in the world has dropped from 70,000 to under 10,000. The Soviets then sold their excess plutonium to the US, which has generated 20% of the total US electric power generation for two decades.

Shultz argued that nuclear weapons were not all they were cracked up to be. Despite the US being armed to the teeth, they did nothing to stop the invasions of Korea, Hungary, Vietnam, Afghanistan, and Kuwait.

Schultz told me that the world has been far closer to an accidental Armageddon than people realize.

Twice during his term as Secretary of State, he was awoken in the middle of the night by officers at the NORAD early warning system in Colorado to be told that there were 200 nuclear missiles inbound from the Soviet Union.

He was given five minutes to recommend to the president to launch a counterstrike. Four minutes later, they called back to tell him that there were no missiles, that it was just a computer glitch projecting ghost images on a screen.

When the US bombed Belgrade in 1989, Russian president Boris Yeltsin, in a drunken rage, ordered a full-scale nuclear alert, which would have triggered an immediate American counter-response. Fortunately, his generals ignored him.

I told Schultz that I doubted Iran had the depth of engineering talent needed to run a full-scale nuclear program of any substance.

He said that aid from North Korea and past contributions from the AQ Khan network in Pakistan had helped them address this shortfall.

Ever in search of the profitable trade, I asked Schultz if there was an opportunity in nuclear plays, like the Market Vectors Uranium and Nuclear Energy ETF (NLR) and Cameco Corp. (CCR), that have been severely beaten down by the Fukushima nuclear disaster.

He said there definitely was. In fact, he was personally going to lead efforts to restart the moribund US nuclear industry. The key here is to promote 5th generation technology that uses small, modular designs, and alternative low-risk fuels like thorium.

Schultz believed that the most likely nuclear war will occur between India and Pakistan. Islamic terrorists are planning another attack on Mumbai. This time, India will retaliate by invading Pakistan. The Pakistanis plan on wiping out this army by dropping an atomic bomb on their own territory, not expecting retaliation in kind.

But India will escalate and go nuclear too. Over 100 million would die from the initial exchange. But when you add in unforeseen factors, like the broader environmental effects and crop failures (CORN), (WEAT), (SOYB), (DBA), that number could rise to 1-2 billion. This could happen as early as 2023.

Schultz argued that further arms control talks with the Russians could be tough. They value these weapons more than we do because that’s all they have left.

Schultz delivered a stunner in telling me that Warren Buffet had contributed $50 million of his own money to enhance security at nuclear power plants in emerging markets.

I hadn’t heard that.

As the event ended, I returned to Secretary Shultz to grill him some more about the details of the Reykjavik conference held some 36 years ago.

He responded with incredible detail about names, numbers, and negotiating postures. I then asked him how old he was. He said he was 100.

I responded, “I want to be like you when I grow up”.

He answered that I was “a promising young man.” I took that as encouragement in the extreme.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We’re Getting Pretty High

https://www.madhedgefundtrader.com/wp-content/uploads/2022/08/wristwatch.jpg331441Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-15 09:02:082022-08-15 13:26:22The Market Outlook for the Week Ahead, or What the Market is Really Discounting Now

Below please find subscribers’ Q&A for the February 3 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Incline Village, NV.

Q: Is there a big difference between COVID-19 vaccines?

A: The best vaccine is the one you can get. It’s better than being dead. But there are important differences. The Pfizer (PFE) and Moderna (MRNA) vaccines are RNA vaccines, they’re very safe, and getting similar results. But the evidence shows that about 15% of Moderna recipients are coming down with flu-like symptoms on their second shot. Nobody knows why, as the two are almost biochemically identical. AstraZeneca is a killed virus type vaccine, which means if they have a manufacturing error, you end up giving the disease to people by accident, as with the original polio vaccine. So that's the less safe vaccine. So far, that one has only been used in Europe and Australia, as it is made in England. There isn’t enough data about the John & Johnson (JNJ) single-shot vaccine.

Q: Is Moderna (MRNA) a long term buy?

A: The trouble with all the vaccine plays is that we’re heading for a global vaccine glut in about 4 months when we’ll have something like 12 companies around the world making them. The rush for everyone to get a vaccination as soon as possible is leading to inevitable overproduction and falling stock prices. Moderna is already a 12 bagger for us. I’m not really looking to overstay my welcome, so to speak. Time to cash in and say, “Thank you very much, Mr. Market.” There will be another cycle down the road for (MRNA) as its technology is used to cure cancer, but not yet.

Q: Would you recommend a silver (SLV) LEAP?

A: Yes, silver was run up 35% for a day by the GameStop (GME) crowd and crashed the next day, which was to be expected because there are no short positions in silver. Everything was just hedged to look like there were short positions because the big banks had huge open short options positions that were public and hedges in the futures and silver bars that were private. The (GME) people only saw the public short positions. Long term, I would go for a $30-$32 vertical call spread expiring in 2023. Go out 2 years, and I think you could get silver at $50. So, a good LEAP might get you a 1000% return in two years. Those are the kinds of trades I like to do.

Q: What do you think of Amazon now that Jeff Bezos is retiring?

A: Buy the daylights out of it. That was the great unknown overhanging the stock for years, Jeff’s potential retirement. Now it's no longer unknown, you want to buy (AMZN). Even before the retirement, I was targeting $5,000 a share in two years. Now we have everybody under the sun raising their targets to $5,000 or more— we even had one upgrade today to $5,200. There are at least half a dozen businesses that Amazon can expand into, like healthcare, which will be multibillion-dollar earners. And then if you break it up because of antitrust, it doubles in value again, so that's a screaming buy here. We have flatlined for six months, so this could be a trigger for a long-term breakout.

Q: Is there anything else left after GameStop? Another short play?

A: Well, this was the worst short squeeze in 25 years, and everyone else covered their other shorts because they don't want to get wiped out like the one Melvin Capital. There were only around a dozen potential single-digit heavily shorted stocks out there, and those are mostly gone. So, the GameStop crowd will have to roll up their sleeves and do some hard work finding stocks the old fashion way—by doing research. I’m guessing that GameStop was a one-hit-wonder; we probably won’t be surprised again. At the same time, you should never underestimate the stupidity of other investors.

Q: What do you think of the cloud plays like Cloudera and Snowflake?

A: I love cloud plays and there will be more coming. The entire US economy is moving on to the cloud. But everyone else loves them too. Snowflake (SNOW) doubled on its first day, and Cloudera (CLDR) doubled over the last three months, so they're incredibly expensive and high risk. But you can't argue with their business models going forward—the cloud is here to stay.

Q: Would you buy LEAPS in financials?

A: Absolutely yes; go out two years for your maturity and 30% on your strike prices, you will get a ten bagger on the trade. If I’m wrong, it only goes to zero.

Q: Is US Steel (X) a buy?

A: Yes. They are being dragged up by the global commodity boom triggered by the global synchronized recovery. (X) took a hit today because they just priced a $700 million secondary share issue which the flippers dumped like a hot potato. If given the choice, I’d rather do a copper play with Freeport McMoRan (FCX) which is seeing much more buying from China. I bought it on Monday.

Q: Any chance you can include one-, three-, and five-year price targets?

A: No chance whatsoever. I’ve never heard of a fund manager that could do that and be right. Stocks are just too imprecise an instrument with all the emotion that’s involved. But for the better stocks, you can with confidence predict at least a double. And by the way, all my predictions for the last 13 years have been way, way on the low side, so I tend to be conservative. Like, remember when Amazon was at $10? I said it would go to $20. Boy was I right!

Q: How can you say the next four years will be good for the stock market?

A: Well, $10 trillion in fiscal stimulus, $10 trillion in QE; stocks tend to like that. Oh, and technology exponentially accelerating on all fronts and far more broadly than what we saw in the 1990s. Also, there is a certain person who is no longer president, so add about 10-20% on top of all stock valuations. Companies can finally do long term planning again, after being unable to do so for four years because policies were anti-trade, anti-business, and flip-flopping every other day. So yes, I think that's enough to make the next 4 four years good; and actually, I think the next 8 years could be good—I'm predicting Dow 120,000 by 2030, if you recall.

Q: When do you expect the next 5% correction if there is one? February is always very volatile.

A: With an unlimited liquidity market like we have, it is really tough to see negatives of any kind. What kind of negatives are out there? The pandemic doesn’t stop—that's the main one. There’s another one people aren't talking about: the reason we got all these vaccines so fast is they took all regulation and threw it out the window. What if one of these vaccines kill off a million people? That would be pretty negative for the market. Interest rates could rocket faster than expected. But I’m always short there so that would be a moneymaker. But these are pretty out there possibilities, and that is why the market is not backing off, and when it does, it only gives us 5%.

Q: Is the Fed stimulating the economy too much?

A: The bond market says no with a ten-year yield of 1.10%, and the bond market is always the ultimate arbiter of when the stimulus ends. That’s because the Fed can’t directly control bond market interest rates, only overnight rates. But when we get bonds up to, say, a 3% yield (which is probably 2 or 3 years off), that’s when we’re getting too much stimulus, and we’ll probably take our foot off the pedal way before then. I know Janet Yellen and she agrees with me on this point. She’ll be throttling back well before we see a 3% yield in the Treasury market.

Q: Do you manage other people’s money?

A: No, because it costs a million dollars in legal fees to set up even a small fund these days. When I set up my hedge fund 30 years ago, there were no regulatory costs because no one knew what a hedge fund was; they all thought they were doing something illegal, so they didn't have to register for anything. That’s why it’s changed now.

Q: What is your target on NVIDIA (NVDA), and will it split?

A: It’s an easy double, with a global chip shortage running rampant. They make the best graphics cards in the world, bar none. These big tech companies tend not to split until they get share prices into the thousands, which is what Apple (AAPL) and what Tesla (TSLA) did three or four times.

Q: If we get 3.25% in bonds, is that going to hurt gold?

A: Yes, and that’s one of the reasons I bailed on my gold positions a couple of weeks ago. It effectively turned into a bond long. A sharp rise in interest rates is bad for gold because we all know that gold yields to zero.

Q: What about Fireye (FEYE)?

A: Yes, we also love Fireye in addition to Palo Alto Networks (PANW) because there is a near-monopoly—there are only about six players in the entire cybersecurity industry and hacking is getting worse by the day. Look at the Solar Winds (SWI) fiasco and the national Russian hack there.

Q: What about copper as a recovery play?

A: Well, I voted with my feet on Monday when I bought a position in Freeport McMoRan, after it just sold off 15%. I think (FCX) could double at some point in the coming economic recovery. So, copper is an absolute winner, and when having to choose between copper and steel, I’ll pick copper all day long.

Q: What do you recommend for gold (GLD)?

A: Gold is a trading range for the time being. Buy the dips, sell the rallies; you won’t get more than about 10% or 15% range on that. And there are just better fish to fry right now, like financials, which benefit from rising interest rates as opposed to being punished. Bitcoin is stealing gold’s thunder and the markets keep creating more Bitcoins.

Q: Should high-frequency trading be banned?

A: I don’t think it should be. It does create liquidity; the effect on the market is wildly overexaggerated. They’re basically trading for pennies or tenths of pennies, so they do provide buying on selloffs and selling at huge price spikes. They do have a positive effect and they’re probably only taking about $10 or $20 billion in profit a year out of the market.

Q: Should I buy Wynn Resorts (WYNN) here?

A: Buy the dips for sure; this is a major recovery play. We here in Nevada are expecting an absolute tidal wave of people to hit the casinos once the pandemic ends, and (WYNN), (MGM), and (LVS) would be a great play in those areas.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/lake-tahoe-sunrise.png460612Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-05 09:34:282021-02-05 08:16:16February 3 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the December 9 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Incline Village, NV with my guest and co-host Bill Davis.

Q: Is gold (GLD) about ready to turn around from here?

A: The gold bottom will be easy to call, and that’s when the Bitcoin top happens. In fact, we have a double top risk going on in Bitcoin right now, and we had a little bit of a rally in gold this week as a result. So, longer term you need actual inflation to show up to get gold any higher, and we may actually get that in a year or two.

Q: The US dollar (UUP) has been weak against most currencies including the Canadian dollar (FXC), but Canada has the same problems as the US, but worse regarding debt and so on. So why is the Canadian dollar going up against the US dollar?

A: Because it’s not the US dollar. Canada also has an additional problem in that they export 3.7 million barrels a day of oil to the US and the dollar value have been in freefall this year. Canada has the most expensive oil in the world. So, taking that out of the picture, the Canadian dollar still would be negative, and for that reason I've been recommending the Australian dollar (FXA) as my first foreign currency pick, looking for 1:1 over the next three years. Of the batch, the Canadian dollar is probably going to be the weakest, Australian dollar the strongest, and the Euro (FXE) somewhere in the middle. I don’t want to touch the British pound (FXB) as long as this Brexit mess is going on.

Q: Would you buy the IPO’s Airbnb (ABNB) and Dash (DASH)?

A: No on Dash. The entries to new competitors are low. Airbnb on the other hand is now the largest hotel in the world, and it just depends on what price it comes out at. If it comes out at a stupid price, like 50% over the IPO, I wouldn’t bother; but if you can get close to the IPO price, I would probably buy it for the long term. I think you would have another double if we got close to the IPO price, so that is worth doing. They have been absolutely brilliant in their management and the way they handled the pandemic; they basically captured all the hotel business because if you rent an apartment all by yourself, the COVID risk is much lower than if you go into a Hilton or another hotel. They also made a big push on local travel which was successful. They gave up long-distance travel, and they’re now trying to get you to explore your own area; and that worked beyond all expectations. Even I have rented some Airbnb’s out in the local area like in Carmel, Monterey, Mendocino, and so on and I came back disease-free.

Q: If the United States Treasury Bond Fund (TLT) goes to a 1.00% yield, what would that translate to in the (TBT) (2x short treasury ETF)?

A: My guess is probably about $18, which has been upside resistance for a long time, but it depends on how long it takes to get there. You have about a 3% a year cost of carry on the TBT that you don’t have in Treasuries.

Q: Should we buy China stocks when the current administration is so negative on China?

A: Yes, that’s when you buy them—when the current administration is negative on China; because when you get an administration that’s less negative on China, the Chinese stocks will all rocket. There’s an easy 20-30% in most of the headline Chinese stocks from here sometime in 2021. And I'm looking to add more Chinese stocks. I currently have Alibaba (BABA), and that’s working well. I want to pick up some more.

Q: What about the New Zealand currency ETF (NZD)?

A: It pretty much moves in sync with the Australian dollar, but it’s usually a few cents cheaper and more volatile.

Q: Legalized sports betting seems to be on the upswing. Where do you see DraftKings (DKNG) going?

A: I think it goes up. I think there’s going to be a recovery in all kinds of entertainment type activities. Draft Kings got a huge market share from the pandemic which they will probably keep.

Q: Do we use spreads when playing (FXA)?

A: Yes, you can probably do something like a $70-$72 here one month out and make some decent money.

Q: How do you feel about Snowflake (SNOW)?

A: I wanted to get into this from day one, but it doubled on the IPO, and then it doubled again. It’s one of the only technology stocks Warren Buffet has bought in the last several years besides Apple (AAPL). So, it’s just too popular right now, it’s hotter than hot. They have a dominant market share in their big data platform, so it’s a great place to be but it’s really expensive now.

Q: Do your options trade alerts have any risk of assignment?

A: Yes, they do, but when you get an assignment it’s a gift, because they’re taking you out of your maximum profit point, weeks before the expiration. All you do is tell your broker to use your long position to cover your short position, and you will get the 100% profit right then and there. I say this because the brokers always tell you to do the wrong thing when you get an assignment, such as going into the market to close out each leg separately. That is a huge mistake, and only makes money for the brokers. For more details, log in and search for “assignments” at www.madhedgefundtrader.com

Q: Congratulations on your great performance; what could derail your bullish prediction?

A: Well, we’ve already had a pandemic so obviously that’s not it, and then you have to run by your usual reasons for an out-of-the-blue crash; let’s say Donald Trump doesn't leave the presidency. That would be worth a few thousand points of downside. So would a major war. We could have both; we could have a major war before a disrupted inauguration. The president has essentially unlimited ability to go to war at any time, so there aren’t too many negatives on the near-term horizon, which is why everyone is super bullish.

Q: What’s your opinion on the solar area, stocks like First Solar (FSLR) and the Invesco Solar ETF (TAN)?

A: I’m bullish. Even though they're over 300% since March, we’re about to enter the golden age of solar. Biden wants to install 500,000 solar panels next year and provide the subsidies to accomplish that. This all looks extremely positive for solar. In California, a lot of people will go solar, because getting an independent power supply protects you from the power shut-offs that happen every time the wind picks up, in which response to wildfire danger. We had ten days of statewide power blackouts this year.

Q: What are your thoughts on lithium?

A: I’m not a big believer in lithium because there is no short supply. The key to producing lithium is finding countries with no environmental controls whatsoever because it’s a very polluting and messy process to mine. Better to let other countries mine your lithium cheap, refine it, and then send it to you in finished form.

Q: Since you love CRISPR (CRSP) at $130, what about shorting naked puts? The premiums are really high.

A: I never advocate shorting naked puts. Occasionally, I will at extreme market bottoms like we had in March, but even then, I do it only on a 1 for 1 basis, meaning don’t use any leverage or margin. Never short any more puts than you’re willing to buy the stock lower down. People regularly see the easy money, sell short too many puts, and then get a market correction and a total wipeout of their capital. And they won't have to do that liquidation themselves; their broker will do it for them. They’ll do a forced liquidation of your account and then close it because they don't want to be left holding the bag on any excess losses. You won’t find out until afterwards. So, I would not recommend shorting naked puts for the normal investor. If you want to be clever, just buy an in-the-money call spread, something like a $110-$120 out a couple of months. That's probably a far better risk reward than shorting a naked put. By the way, I came close to wiping out Solomon Brothers 30 years ago because my hedge fund was short too many Nikkei Puts. In the end, I made a fortune, but only after a few sleepless nights (remember that Mark?).

Q: What do you think about defense stock right now?

A: I’m avoiding defense stock because I don’t see any big increases in defense spending in the future administration, and that would include Raytheon (RTX), Northrop Grumman (NOC), and some of the other big defense stocks.

SEE YOU ALL IN 2021!

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/06/john-bike.jpg14241605Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-11 09:02:102020-12-11 10:23:11December 9 Biweekly Strategy Webinar Q&A

The good news is that investors are thirsting for new cloud IPOs boding well for tech firms like Airbnb who plans to go public later this year.

The long-term health of the U.S. tech sector is on solid footing.

Most recently we had Snowflake (SNOW) who is a cloud provider and has an impressive enterprise business.

The public cloud is the data storage unit which literally everyone stores their operations on that has benefited from a massive wave of digital migration.

Many of the cloud-targeted tech firms of recent years have been 10-baggers and have dominated the overall market's returns.

Typically, these companies trade at high premiums, and rightly so, because of the corresponding growth trajectories and Snowflake is no different.

The stock has doubled after less than half a month as a tradable market-moving instrument.

Even by the standards of the most expensive software companies on the Nasdaq index, Snowflake is not cheap, although it’s a growth monster.

Snowflake was valued at $12.4 billion in February and even has investor Warren Buffett, the Oracle of Omaha, among its investors.

Buffett dove headfirst into tech investments in Apple and even some Indian fintech firms as well.

Snowflake is the largest software IPO on record and the largest since Uber's $8.1 billion IPO in May 2019.

The firm was striving for a valuation of $20 billion. In total, Snowflake has raised $1.4 billion from investors including Sequoia and Iconiq Capital.

Snowflake even makes the high-flying Zoom (ZM) Video Communications look cheap which is hard to do.

Zoom is growing three times faster than Snowflake, but trades at roughly half of Snowflake's price-to-sales ratio.

Zoom is also profitable, whereas Snowflake is a huge loss maker and that is a staple of many tech startups. This is an economic environment that is more conducive to profit drive companies instead of the tech model of promising future growth.

Snowflake is over four times more expensive than cloud company Datadog.

Snowflake's market is thought to be bigger than most other niche software applications, and therefore it may have a longer runway. In the regulatory filing, Snowflake claimed its total addressable market was around $81 billion.

Along with many other growth companies, Snowflake's ultimate margin potential is still hard to fathom and more passengers are starting to arrive in the sector than drivers.

Even worse, Snowflake not only competes with legacy data warehouse companies such as Oracle (ORCL) and Dell but also with products from the cloud infrastructure company it collaborates with.

Since shares have already doubled, I do believe that investors will need to wait for a pullback to put money to work in Snowflake.

The company said it had about 3,100 customers, including 56 clients that contributed about $1 million in a 12-month period.

Even with the pricey valuations, Snowflake is the pre-eminent cloud listing of the second half of 2020 and its enterprise business is sustainable.

If a broader sell-off drags this name down into the $180s, pull the trigger and start wading into this one.

The stock is currently priced as such that it represents flawless execution quarter after quarter for many years, and they would have to live up to lofty expectations to grow into its valuation.

While the management is stellar and is known for its execution, the odds of Snowflake's stock faltering are high because of the high bar.

Keep this one on your hot list because with all the variables waiting to pull down the market, there will be a time when the price is right in Snowflake.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-23 10:02:592020-09-23 19:02:59The Hot Cloud IPOP of Fall 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.