Mad Hedge Technology Letter

December 16, 2024

Fiat Lux

Featured Trade:

(OVERCOMING UNCERTAINTY IN 2025)

($COMPQ), (SOFTBANK)

Mad Hedge Technology Letter

December 16, 2024

Fiat Lux

Featured Trade:

(OVERCOMING UNCERTAINTY IN 2025)

($COMPQ), (SOFTBANK)

There have been many prognosticators concerned that next year is trouble for tech stocks, but I am here to dispel that notion.

The uncertainty has permeated into global investment fund management with some even calling for a mild pullback in tech valuations ($COMPQ).

Concerns are concerns and that doesn’t mean we will get a wild selloff or a crash.

There are still too many drivers that tech can pull to bail itself out of any hole they or others might dig for them.

I do agree with the notion that the era of super growth for the current tech business model is over and we are really trying hard to eke over the bar every quarter now.

One trend that could go into overdrive next year is the acceleration of AI investment from funds waiting on the sidelines.

I’ve mentioned to people off the record the staggering amount of capital that has poured into the US after the election.

The surprising part of this is that a meaningful amount of these funds are foreign.

Remember that in places like China and Europe, economics are going in the wrong direction and investment funds have nowhere to place their capital.

Europe has overregulated itself to death more interested in protecting the old money and destroying anything closely relating a start-up.

I argue to clients that Europe is the last place on earth I would ever start a tech company.

China has reached the end of its current growth phase and now has a system that won’t change just to protect the incumbents.

Inherently, Chinese tech could turn into the next Japan.

The end results are a terrible foreign tech scene in most places not named the United States.

Japan, for a matter of fact, has produced people like Softbank CEO Masayoshi Son who try to scrape as many billions together to throw into US tech.

Part of the foreign capital I talk about comes from him, but also other massive funds such as Norway’s sovereign fund valued at over $2 trillion now.

More than 40% of that portfolio is in US tech stocks giving them ammunition for an even bigger step up next year.

President-elect Donald Trump, with SoftBank Group CEO Masayoshi Son at his side, announced that SoftBank would invest $100 billion in the U.S. over the next four years in what would be a boost to the U.S. economy.

Trump said in his joint appearance with Son that the investment would create 100,000 jobs focused on artificial intelligence (AI) and related infrastructure, with the money to be deployed before the end of Trump's term.

Son has been a strong proponent of the potential for AI and has been pushing to expand SoftBank's exposure to the sector, taking a stake in OpenAI and acquiring chip startup Graphcore.

The uncertainty is warranted, because we will replace a U.S. administration with a vastly different view of the economy and tech scene.

I do believe we missed a bullet. If Harris won, she would of choked off the vitality of Silicon Valley and placed power and control in the hands of a few.

I say that even though tech stocks performed greatly the past 4 years.

I don’t believe that tech stocks are about to lose steam and the case for the new administration turbo charging the economy is definitely realistic.

Trump wants to cut U.S. corporate tax to 15% and that 6% drop for U.S. tech firm would represent a gargantuan windfall to the bottom line.

If Silicon Valley is the beneficiary pro-corporate legislation, the sky is the limit for tech stocks next year even if they don’t create anything game changing.

Playing with house money is fun and we could be in a situation next year where U.S. tech firms can shoot for the stars.

Mad Hedge Technology Letter

November 22, 2023

Fiat Lux

Featured Trade:

(YEN COULD DRAG DOWN TECH STOCKS)

(FXY), ($COMPQ), (WEWKQ), (SOFTBANK)

The Japanese yen has helped boost tech stocks ($COMPQ).

Institutional money is borrowing Japanese yen (FXY) by the bucketful because Japanese interest rates have been anchored at 0% and betting big on tech stocks.

The strategy has worked like clockwork and Japanese stocks have also felt the wind at its sails.

What now?

Lurking in the shadows is a potentially catastrophic problem called Japanese tech company Softbank.

Softbank reported a "shocking" Q2-2 loss, revealing, in particular, how dangerously exposed they are to a Japanese yen devaluation.

Selling in Softbank stock would trigger panic selling in Japanese Banks. The contagion risk here is crystal clear.

JGB yields will spike following the US Treasury yields overnight trend. This will put even further pressure on banks' liquidity with a risk of exacerbating the sell-off.

What's important to understand here is the risk of Softbank triggering a $226 billion (the total amount of Softbank balance sheet liabilities) credit event right now.

To begin with, with a BB rating from S&P, Softbank has a pitiful credit rating tying its hands.

Now Softbank has liabilities mostly in US dollars while on the hook to repay $48 billion in the next 12 months.

Days before WeWork (WEWKQ) filed for bankruptcy, Softbank paid $1.5 billion to WeWork bank lenders.

In total, Softbank had to write off more than $14 billion in US dollars on that terrible WeWork investment while the Japanese yen crashed.

Now here the big problem is that Softbank doesn't disclose the amount of "off-balance-sheet" guarantees they issued either directly or through the Vision Fund.

Lastly, things might turn quite bad for Masayoshi Son personally, because 35% of his personal shares in Softbank are already pledged to financial institutions.

It doesn't take much to figure out what financial institutions will do if Softbank stock starts crashing, right?

The Japanese government will need to bail out not only Softbank but also the Japanese banks.

This tinderbox could explode anytime and the Yen would then become the focus.

If the Japanese government finally does embark on an interest hiking cycle then under this scenario, the Bank of Japan would be forced to raise the cost of capital on investors and households.

The global and Japanese financial system isn’t ready to take away the low-interest carry trade and it’s hard to quantify the unintended consequences.

Large parts of the Japanese system could go under water and the Japanese yen would greatly strengthen.

I specifically am worried about all the adjustable loans taken out by the Japanese consumer.

Loan defaults would surge.

If the Japanese government is forced to save Softbank and the Japanese financial system then expect another tidal wave of inflation as the purchasing power of the Japanese yen is even more devalued.

The string of abysmal tech investments by Softbank is threatening to accelerate the financial death spiral in Japan.

In my view, this would ice the tech rally momentarily, but not derail it long-term.

In all honesty, Softbank did deliver ample liquidity to many poorly run Silicon Valley tech companies and this fortified tech stocks during the bull run.

Now Softbank cannot throw around the cash they used to and tech stocks have concentrated into a group of 7 outperformers.

In the short term, the tech bull run continues in just a few narrow names but 2024 could trigger a broader run in secondary tech names as well.

Mad Hedge Technology Letter

July 28, 2023

Fiat Lux

Featured Trade:

(ANOTHER IMPLOSION BEGGING TO HAPPEN)

(RAPPI), (SOFTBANK)

There’s a reason why Softbank lost $32 billion in technology investments last quarter, and it stems mostly from terrible investment decisions.

Most of Masayoshi Son’s Softbank targets are at the small time level where a few hundred million of revenue per year is something they are interested in.

The thinking behind this is to hit those 10 baggers, and to his credit, he did pocket some of those like Alibaba and Uber in the days of yore.

A broken clock is right twice a day.

Do Son’s actions signal a turning of the corner from his hefty losses?

I would strongly suggest he is doubling down on his losing strategy based on what he’s green-lighted in South America.

Take for instance the recent news of his investment in Rappi, a food delivery app that has grown into one of Latin America’s most-valuable startups.

They just announced they will offer loans to restaurants in Mexico and Colombia.

The plan is to offer loans to restaurants that have been selling via the app for at least three months.

The foray into commercial lending shows how Rappi has adapted its business model to add more revenue streams in the eight years since it started as a grocery delivery business.

Facing stiff competition from the likes of Naspers Ltd’s iFood and UberEats, Rappi has increasingly embraced financial technology as it expands in the region.

In its latest push, Rappi is targeting $60 million in loans across the two countries.

Rappi didn’t disclose the terms of the loans it will offer. The credits will be repaid through the restaurants’ sales via the app.

The company could expand the loan business to some of the other nine countries where it has operations as soon as this year.

This strategy screams desperation and low-quality decision-making.

Restaurant revenue isn’t stable enough to base a loan on a highly changeable industry.

There are no fixed contracts as to how many tacos per month are sold and the hilarious concept of offering loans based on 3-months of operating the app is irresponsible.

The company wouldn’t comment on what type of terms they would offer because they most likely will be highly predatory because this maneuver is highly risky.

Don’t expect Japanese bond levels of 0% and think of something more like 18% similar to Russian mortgage rates.

My understanding here is that management is trying to pump up revenue in the short term just to shine up the business metrics for the IPO.

After the IPO, the management will be able to cash out, and then management can throw the business to the wolves for all they care.

The great news here is that Softbank funding this type of weak tech business model is good for the entire tech ecosystem because tech needs that sucker that juices up the purses.

If other parts of tech didn’t get any investment, then there wouldn’t be the top 7 big tech stocks that boss the S&P.

Much of the reason tech shares have reached Himalayan highs is because a stream of short-sellers must cover their shorts with every explosion to the upside.

Son subsidizing the bottom feeders of global tech apps is in fact positive for Silicon Valley as a whole.

Tech needs guys like him to get stuck with the bill so people like us cash out at the top.

It’s a dog-eat-dog world.

Unfortunately for Rappi, the restaurant loan business is ripe to implode betting on a financially unproven population to power this app to the public market.

Rappi’s management better hope they can unload vested shares before the whole game is up.

Mad Hedge Technology Letter

April 14, 2023

Fiat Lux

Featured Trade:

(GLOBAL TECH GRINDS TO A HALT)

(BABA), (CCP), (SOFTBANK)

Hard to believe that Softbank is throwing in the towel on its stake in Alibaba (BABA), but that is what is happening.

If you can remember, Alibaba was that can’t miss e-commerce company that ran into the wall that is the Chinese Communist Party (CCP).

They were then regulated into oblivion.

Even through arbitrary lockdowns, Softbank didn’t sell its stake so I find it peculiar that they would finally decide to divest out of China because maybe they know something that I don’t.

The golden years of Chinese ecommerce development is far in the rear view mirror.

However, there was a reason Softbank held onto its BABA stake for all this time, and BABA being a monopoly is a great reason.

This relationship epitomized the freewheeling globalization which many of us grew to love in the early 2000s and the decades after that.

That type of globalization has been replaced by something a lot more insidious that looks something more similar to balkanization.

It could be a simple as getting money out of China.

Many investors have recently said withdrawing money abroad has become almost impossible these days as the CCP has really tightened up capital outflow.

This is not only bad news for Chinese tech companies, but bad for all international tech deals in general at a time when venture capital money in tech has dried up.

SoftBank has sold more than $7 billion in Alibaba shares this year through prepaid forward contracts, after selling $29 billion last year.

The contracts give SoftBank the option to buy the shares back from Alibaba, but the group has settled previous deals by handing over the stock.

The sales will reduce the Japanese conglomerate’s ownership of Alibaba to less than 4% which is a far cry from the 14.6% stake the company said it was slated to hold as of end-September.

Softbank once owned about a third of the company spanning from an early $20 million investment in one of venture capital’s most famous bets.

Last month, the online commerce leader said it plans to split its $240 billion empire into six units that will individually raise funds and explore initial public offerings.

SoftBank, once one of Silicon Valley’s largest investors, has been crippled by billions of dollars of losses.

SoftBank’s billionaire founder Masayoshi Son has said he wants to focus on a planned listing of its chip design unit Arm Ltd. later this year and make the debut “the biggest” in the history of the semiconductor industry.

The re-listing of Arm, which had traded on the London exchange prior to SoftBank’s $32 billion acquisition in 2016, is expected to be a big windfall for the world’s biggest technology investor.

However, the Arm deal could be one of the last in the door for tech as many economies have become nationalistic and inward looking.

India is supposed to be the next China, and I believe it will be difficult for Silicon Valley money to get ahead there if defensive barriers are erected in the support of local capital.

The golden years of Silicon Valley are in the record book, and the next chapter appears to be focused on generative artificial intelligence super charging profits.

Tech shares will see a big decoupling of companies that jump on this hot new technology and the ones who are left behind.

Like always in Silicon Valley, iterate or die.

Mad Hedge Technology Letter

March 1, 2023

Fiat Lux

Featured Trade:

(THE VISION FUND LACKING VISION)

(WE), (SOFTBANK), (VISION FUND)

The most painful place to be in tech these days is where the venture capitalists used to make their name.

Private startups used to be glamorized, and now nobody wants to touch them with even a 10-foot pole.

VCs are the capital-rich guys who used to buy companies privately, hold onto them until they grew 10X, and then dish them off to the public once they went ex-growth.

That playbook was the surefire way to capitalize from companies during their highest growth phase.

Softbank’s Vision Fund was the poster boy for this strategy as the founder of Softbank Masayoshi Son deployed gargantuan resources from his Japanese telecom company (mostly in the form of debt) to pour into private tech firms.

Now, The Vision Fund has basically blown up as ideas like throwing $300 million at a dog walking app haven’t resulted in higher valuations from ludicrous types of aggressive investments.

Markets can behave irrationally for a while, but sooner or later, it regresses back to reality.

In the end, the world’s most brazen tech investor, Softbank, wasted billions helping to artificially lift tech valuations, only to see them plunge and lose their own money along with other adjacent investors.

In some cases like the office sub-let company WeWork (WE), they were the only investors to value assets at such lofty valuations. In WeWork’s case, they valued the company at $48 billion at its peak, and at the time of this writing, WE has a valuation of $920 million after finally going public.

So it’s not a surprise to see WE’s experience highlighting a broader failure of epic underperformance from Softbank with a decline in value for 73% of its 472 investments from an expert boutique firm that apparently is on the pulse of every new tech trend.

They would have done better with a monkey throwing darts at a dart board.

To address the headwinds, they are drastically reducing investment for the time being because they are tired of being wrong.

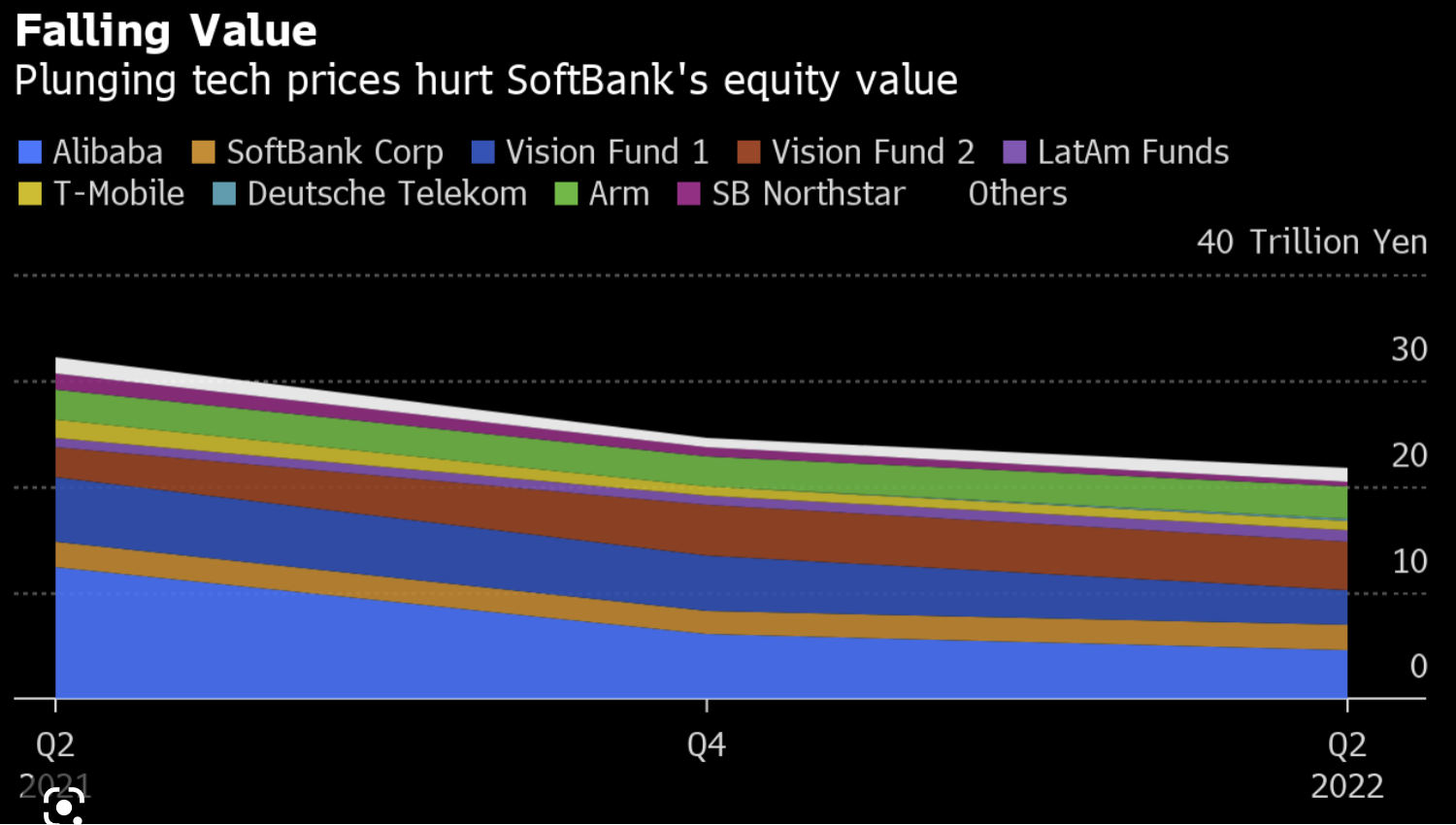

For the October to December quarter, SoftBank reported an investment loss of ¥731.94bn ($5.5bn), compared with a ¥1.38tn loss in the previous quarter for its two Vision Funds and a fund investing in start-ups in Latin America.

As of the end of December, SoftBank said the fair value of the $100bn Vision Fund I was down 4.4% from a year earlier due to markdowns in privately held companies despite gains in some listed holdings, such as ride-hailing groups Didi and Grab. The valuation for investments in Vision Fund II was down 6.2%

Son announced last year that he would step back from day-to-day operations to basically get out of the way of himself.

I applaud him for doing that because many arrogant leaders don’t understand when their time is up.

The private markets aren’t what they used to be and the deal breaker is higher rates.

This part of tech won’t come back until cheap money floods visionary ideas because these ideas are usually risky and most attempts become a zero.

Tech stocks will continue to be choppy in the meantime and continue to represent ideal trader markets for investors to jump in and out of tech stocks.

It’s natural for a reversion to the mean after a blistering January and big moves up and down will be the likely story in this stock pickers market for 2023.

However, the time for those 10Xers from VCs is dead until further notice.