Global Market Comments

March 26, 2024

Fiat Lux

Featured Trade:

(THE DEATH OF THE MALL….NOT),

(SPG), (MAC), (TCO),

(QUANTITATIVE EASING EXPLAINED TO A 12-YEAR-OLD)

Global Market Comments

March 26, 2024

Fiat Lux

Featured Trade:

(THE DEATH OF THE MALL….NOT),

(SPG), (MAC), (TCO),

(QUANTITATIVE EASING EXPLAINED TO A 12-YEAR-OLD)

We’ve all heard this story before.

Malls are dying. Commerce is moving online at a breakneck pace. Investing in retail is a death wish.

No less a figure than Bill Gates, Sr. told me before he died that in a decade, malls would only be inhabited by climbing walls and paintball courses, and that was a decade ago.

Except it didn’t quite work out that way. Lesser quality malls are playing out Mr. Gates’ dire forecast. But others are booming. It turns out that there are malls, and then there are malls.

Let me expand a bit on my thesis.

We are just entering a decade-long decline in interest rates, probably starting in June. Malls are highly leveraged entities that often are financed by Real Estate Investment Trusts) REITS. That makes some mall-based REITS some of the most attractive investments in the market.

Technology is moving forward at an exponential rate. As a result, product performances are improving dramatically, while costs are falling. Commodity and energy prices are also rising, they are but a tiny fraction of the cost of production.

In other words, DEFLATION IS HERE TO STAY!

The nearest hint of real inflation won’t arrive until the late 2020s, when Millennials become big spenders, driving up the cost of everything.

So, let's go back to the REIT thing. Real Estate Investment Trusts are a creation of the Internal Revenue Code, which gives preferential tax treatment for investment in malls and other income-generating properties.

There are 1,100 malls in the United States. Some 464 of these are rated as B+ or better and are concentrated in the biggest spending parts of the country (San Francisco, North New Jersey, Greenwich, CT, etc).

Trading and investing for a half-century, I have noticed that most managers are backward-looking, betting that existing trends will continue forever. As a result, their returns are mediocre at best and terrible at worst.

Truly brilliant managers make big bets on what is going to happen next. They are constantly on the lookout for trend reversals, new technologies, and epochal structural changes to our rapidly evolving modern economy.

I am one of those kinds of managers.

These are not your father’s malls. It turns out the best quality malls are booming, while second and third-tier ones are dying the slow painful death that Mr. Gates outlined.

It is all a reflection of the ongoing American concentration of wealth at the top. If you are selling to the top 1% of wealth owners in the country, business is great. If fact, if you cater even to the top 20%, things are pretty damn fine.

You can see this in the top income-producing tenants in the “class A” malls. In 2000, they comprised J.C. Penney. Sears, and Victoria’s Secret. Now Apple, L Brands, and Foot Locker are sought-after renters. Put an Apple store in a mall, and it is golden.

And what about that online thing?

After 25 years of online commerce, the business has become so cutthroat and competitive that profit margins have been beaten to death. You can bleed yourself white watching Google AdWords empty out your bank account. I know, because I’ve tried it.

Many online-only businesses are now losing money, desperately searching for that perfect algorithm that will bail them out, going head-to-head against the geniuses at Amazon.

I open my email account every morning and find hundreds of solicitations for everything from discount deals on 7 For All Mankind jeans, to the new hot day trading newsletter, to the latest male enhancement vitamins (although why they think I need the latter is beyond me).

Needless to say, it is tough to get noticed in such an environment.

It turns out that the most successful consumer products these days have a very attractive tactile and physical element to them. Look no further than Apple products, which are sleek, smooth, and have an almost sexual attraction to them.

I know Steve Jobs drove his team relentlessly to achieve exactly this effect. No surprise then that Apple is the most successful company in history and can pay astronomical rents for the most prime of prime retail spaces.

It turns out that “Clicks to Bricks” is becoming a dominant business strategy. A combination of the two is presently generating the highest returns on investment in retail today.

People start out by finding a product online and then going to the local mall to try it on, touch it, and feel it. Apple does this.

Research shows that two-thirds of Millennials prefer buying their clothes and shoes at malls. Once there, the probability of a serendipitous purchase is far greater than online, anywhere from 20% to 60% of the time.

This explains why pure online businesses by the hundreds are rushing to get a foothold in the highest-end malls.

Immediate contact with a physical customer gives retailers a big advantage, gaining them the market intelligence they need to stay ahead of the pack. In “fast fashion” retailers like H&M and Uniqlo, which turn over their inventories every two weeks, this is a really big deal.

There’s more to the story. Malls are not just shopping centers they have become entertainment destinations as well. With an ever-increasing share of the population chained to their computers all day, the demand for a full out-of-the-house shopping, dining, and entertainment family experience is rising.

Notice how Merry Go Rounds have started popping up at the best properties? Imax Theaters are spreading like wildfire. And yes, they have climbing walls too. I haven’t seen any paintball courses yet, but the guns and accessories are for sale.

And notice that theaters are now installing first-class adjustable heated seats and will serve you dinner while the movie is playing. (Warning: if you eat in the dark, you will end up wearing half of it home).

This is why all of the highest-rated malls in the country are effectively full. If you want space, there you have to wait in line. REIT managers pray for tenant bankruptcies so that can jack up rents on the next incoming client or pivot their strategy towards the newest retail niche.

Malls are also in the sweet spot in the alternative energy game. Lots of floor space means plenty of roof space. That means they can cash in on the 30% federal investment tax credit for solar roof installations. Some malls in sunny southwestern states are net power generators, effectively turning them into min local power utilities. By the way, the cost of solar has recently crashed.

Fortunately for us investors, we are spoiled for choice in the number of securities we can consider, most which can now be bought for bargain basement prices. Many have a return on investment of 9-11%, a portion of which is passed on to the end investor.

There are now 25 REITs in the S&P 500. The sector has become so important that the ratings firm is about to create a separate REIT subsector within the index.

According to NAREIT.com (click here for the link), these are some of the largest mall-related investment vehicles in the country.

Simon Growth Property (SPG) is the largest REIT in the country, with 241 million square feet in the US and Asia. It is a fully integrated real estate company that operates from five retail real estate platforms: regional malls, Premium Outlet Centers, The Mills, community/lifestyle centers, and international properties. It pays a 4.88% dividend.

Macerich Co. (MAC) is a California-based company that is the third largest REIT operator in the country. It has been growing through acquisitions for the past decade. It pays a 5.31% dividend.

Mind you, REITs are not exactly risk-free investments. To get the high returns you take on more risk. We remember how disastrously the sector did when the credit crunch hit during the 2009 financial crisis. Many went under, while others escaped by the skin of their teeth.

There are a few things that can go wrong with malls. Local economies can die, as it did in Detroit. Populations age, shifting them out of a big spending age group. And tax breaks can be here today and gone tomorrow.

These are all highly leveraged companies, so any prolonged rise in interest rates could be damaging. But as I pointed out below, there is little chance of that in the near future.

The bottom line here is that we are seeing anything but the death of the mall. It just depends on the mall.

All in all, if you are looking for income and yield, which everyone on the planet is currently pursuing, then picking up some REITs could be one of your best calls of the year.

Global Market Comments

July 30, 2021

Fiat Lux

Featured Trade:

(JULY 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CRSP), (TLT), (TBT), (BABA), (BIDU), (FXI), (RAD), (TSLA), (NASD), (NKLA), (NIO), (INTC), (MU), (NVDA), (AMD), (TSM), (VXX), (XVZ), (SVXY), (FCX), (ROM), (SPG)

July 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the July 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV.

Q: What is your plan with the (SPY) $443-$448 and the $445/450 vertical bear put spreads?

A: I’m going to keep those until we hit the lower strike price on either one and then I’ll just stop out. If the market doesn’t go down in August, then we are going straight up for the rest of the year as the earnings power of big tech is now so overwhelming. Sorry, that’s my discipline and I’m sticking to it. Usually, what happens 90% of the time when we go through the strike, and then go back down again by expiration for a max profit. But the only way to guarantee that you'll keep your losses small is by stopping out of these things quickly. That’s easy to do when you know that 95% of the time the next trade alert you’ll get is a winner.

Q: Are you still expecting a 5% correction?

A: I am. I think once we get all these great earnings reports out of the way this week, we’re going to be in for a beating. I just don't see stocks going straight up all the way through August, so that’s another reason why I'm hanging on to my short positions in the S&P 500 (SPY).

Q: What’s the best way to play CRISPR Therapeutics (CRSP) right now?

A: That is with the $125-$130 vertical bull call spread LEAPS with any maturity in 2022. We had a run in (CRSP) from $100 up to $170 and I didn’t take the damn profit! And now we’ve gone all the way back down to $118 again. Welcome to the biotech space. You always take the ballistic moves. Someday I should read my own research and find out why I should be doing this. For those who missed (CRSP) the last time, we are one proprietary drug announcement, one joint venture announcement, or one more miracle cure away from another run to $170. So that will probably happen in the next year, you get the $125-$130 call spread, and you will double your money easily on that.

Q: I’m down 40% on the United States Treasury Bond Fund (TLT) January $130-$135 vertical bear put spread LEAPS. What would you do?

A: Number one, if you have any more cash I would double up. Number two, I would wait, because I would think that starting from the Fall, the Fed will start to taper; even if they do it just a little bit, that means we have a new trend, the end of the free lunch is upon us, and the (TLT) will drop from $150 down to $132 where it was in March so fast it will make your head spin. I'm hanging onto my own short position in (TLT). If you are new to the (TLT) space and you want some free money, put on the January 2020 $150-$155 vertical bear put spread now will generate about a 75% return by the January 21, 2022 options expiration. I just didn't figure on a 6.5% GDP growth rate generating a 1.1% bond yield, but that’s what we have. I'm sorry, it’s just not in the playbook. Historically, bonds yield exactly what the nominal GDP growth rate is; that means bonds should be yielding 6.50% now, instead of 1.1%. They will yield 6.5% in the future, but not right now. And that's the great thing about LEAPS—you have a whole year or 6 months for your thesis to play out and become right, so hang on to those bond shorts.

Q: Do you have any ideas about the target for Facebook (FB) by the end of the year?

A: I would say up about 20% from current levels. Not only from Facebook but all the other big tech FANGS too. Analysts are wildly underestimating the growth of these companies in the new post-pandemic world.

Q: Do you think the worst of the pandemic will be over by September?

A: Yes, we will be back on a downtrend by September at the latest and that will trigger the next leg up in the bull market. Delta with its great infectious and fatality rates is panicking people into getting shots. The US government is about to require vaccinations for all federal employees and that will get another 5 million vaccinated. Americans have the freedom to do whatever they want but they don’t have the freedom to kill their neighbors with fatal infections.

Q: What should I do with my China (BABA), (BIDU), (FXI) position? Should I be doubling down?

A: Not yet, and there’s no point in selling your positions now because you’ve already taken a big hit, and all the big names are down 50% from the February high. I wouldn't double down yet because you don’t know what's happening in China, nobody does, not even the Chinese. This is their way of addressing the concentration of the wealth in the top 1% as has happened here in the US as well. They’re targeting all the billionaire stocks and crushing them by restricting overseas flotations and so on, so it ends when it ends, and when that happens all the China stocks will double; but I have absolutely no idea when that's going to happen. That being said, I have been getting phone calls from hedge funds who aren’t in China asking if it's time to get in, so that's always an interesting precursor.

Q: What happened to the flu?

A: It got wiped out by all the Covid measures we took; all the mask-wearing, social distancing, all that stuff also eliminates transmission of flu viruses. Viruses are viruses, they’re all transmitted the same way, and we saw this in the Rite Aid (RAD) earnings and the 55% drop in its stock, which were down enormously because their sales of flu medicines went to zero, and that was a big part of their business. I didn’t get the flu last year either because I didn’t get Covid; I was extremely vigilant on defensive measures in the pandemic, all of which worked.

Q: Why would the Fed taper or do much of anything when Powell wants to be reappointed in February 2022?

A: I don’t think he is going to get reappointed when his four-year term is up in early 2022. His policies have been excellent, but never underestimate the desire of a president to have his own man in the office. I think Powell will go his way after doing an outstanding job, and they will appoint another hyper dove to the position when his job is up.

Q: What are your thoughts on the Chinese electric auto company Nio competing here in the U.S.?

A: They will never compete here in the U.S. China has actually been making electric cars longer than Tesla (TSLA) has but has never been able to get the quality up to U.S. standards. Look what happened to Nikola (NKLA) who’s founder was just indicted. Avoid (NIO) and all the other alternative startup electric car companies—they will never catch up with Tesla, and you will lose all your money. Can I be any clearer than that?

Q: You recently raised the ten-year price target up for the Dow Average from 120,000 to 240,000. What is Nasdaq's target 10 years out?

A: I would say they’re even higher. I think Nasdaq (NASD) could go up 10X in 10 years, from 14,000 to 140,000 because they are accounting for 50% of all earnings in the U.S. now, and that will increase going forward, so the stocks have to go ballistic.

Q: What do you think of Intel (INTC)?

A: I don’t like it. They had a huge rally when they fired their old CEO and brought in a new one. There was a lot of talk on reforming and restructuring the company and the stock rallied. Since then, the market has started insisting on performance which hasn’t happened yet so the stock gave up its gains. When it does happen, you’ll get a rally in the stock, not until then, and that could be years off. So I'd much rather own the companies that have wiped out Intel: (MU), (NVDA), (AMD), and (TSM).

Q: When you do recommend buying the Volatility Index (VIX), do you recommend buying the (VIX) or the (VXX)?

A: You can only buy the VIX in the futures market or through ETFs and ETNs, like the (VXX), the (XVZ), and the (SVXY), or options on these. I would be very careful in buying that because time decay is an absolute killer in that security, and that's why all the professionals only play it from the short side. That's also why these spikes in prices literally last only hours because you have professionals hammering (VIX). Somebody told me once that 50% of all the professional traders in the CME make their living shorting the (VIX) and the (VXX). So, if you think you’re better than the professionals, go for it. My guess is that you’re not and there are much better ways to make money like buying 6-to-12-month LEAPS on big tech stocks.

Q: Can the Delta variant get a bigger pullback?

A: Yes. I expect one in August, about 5%. But if Delta gets worse, the selloff gets worse. You saw what it did last year, down 40% in the (SPY) in only two months, so yes, it all depends on the Delta virus. I'm not really worrying about Delta, it's the next one, Epsilon or Lambda, which could be the real killer. That's when the fatality rate goes from 2% to 50%, and if you think I'm crazy, that's exactly what happened in 1919. Go read The Great Influenza book by John Barry that came out 20 years ago, which instantly became a best seller last year for some reason.

Q: Does the Matterhorn have enough flat space on the top to stand on it?

A: Actually, there is a 6’x6’ sort of level rock to stand on top of the Matterhorn. If you slip, it’s a 5000’ fall straight down on any side, and on a good weather day in the summer, there are 200 people climbing the Matterhorn. There's sometimes a one-hour line just to take your turn to get to the top to take your pictures, and then get down again to make space for the next person. So that's what it's like climbing the Matterhorn, it's kind of like climbing Mount Everest, but I still like to do it every year just to make sure I can do it, and one year I hope to win the prize for the oldest climber of the year to climb the Matterhorn. Every year this German guy beats me; he’s two years older than me.

Q: When will Freeport McMoRan (FCX) start going up? I have the 2023 LEAPS

A: Good thing you have the two-year LEAPS because that gives you two years for inflation to show its ugly face once again. You just have to be patient with these. I think we’ll get a rally in the Fall along with all the other interest rate plays like banks, industrials, money management companies, and so on. (FCX) will certainly participate in that. In the meantime, if we get all the way down to $30 in Freeport McMoRan, I would double up your position.

Q: Why is oil (USO) not a buy? Oil is the ultimate inflation hedge.

A: Yes, unless all of the cars in the United States become electric in the next 15 years, which they will, wiping out half of all demand from the largest oil consumer. The United States consumes about 20 million barrels of oil a day, half of that is for cars, and if you take that out of the demand picture you dump 10 million barrels a day on the market and oil goes back to negative numbers like we saw last year. Never do counter-trend trades unless you’re a professional in from of a screen 24 hours a day.

Q: Should I take profits on my ProShares Ultra Technology ETF (ROM) November $90-$95 vertical bull spread and then enter a new spread when tech sells off?

A: Absolutely! When you have that much leverage and you get these price spikes, you sell! The leverage on this position is 2X on the ETF and 10X on the options for a total of 20X! Well done, nice trade and nice profit, go out and buy yourself a new Tesla and wait for the next dip in tech, which may have already started, and which could power on for the rest of August.

Q: What’s the next move for REITs?

A: REITs came off of historic lows last year; a lot of people thought they were going to go bankrupt, and for companies like (SPG) it was a close-run thing. I would be inclined to take profits on REITs here. The next thing to happen is for interest rates to go up and REITs don’t do that great in a rising rate environment.

Q: When is the off-season in Incline Village?

A: It’s the Spring and the Fall, in between ski season and the summer season. That means there are four months a year here, May/June and September/October, where I’m the only one here and the parking lots are empty. There is no one on the trails, the weather is perfect, the leaves are changing colors, and the roads aren’t crowded, so that is the time to be here. It’s a mob scene in the winter and a worse mob scene in the summer!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

August 14, 2020

Fiat Lux

Featured Trade:

(BIG TECH AND THE FUTURE OF COLLEGE CAMPUSES)

(SPG), (AMZN), (APPL), (MSFT), (FB), (GOOGL)

The genie is out of the bottle and things will never go back to how they once were. Sorry to burst your bubble if you thought the economy, society, and travel rules would just revert to the pre-coronavirus status quo.

They certainly will not.

One trend that shows no signs of abating is the “winner take all” mentality of the tech industry.

Tech giants will apply their huge relative gains to gut different industries.

Once a shark smells blood, they go in for the kill; and nothing else will suffice until these revenue machines get their way in every other adjacent industry.

Recently, we got clarity on big box malls becoming the new tech fulfillment centers with the largest mall operator in the United States, Simon Property Group (SPG), signaling they are willing to convert space leftover in malls from Sears and J.C. Penny.

Then I realized that another bombshell would hit sooner rather than later.

College campuses will become the newest of the new Amazon, Walmart, or Target eCommerce fulfillment centers starting this fall, and let me explain to you why.

When the California state college system shut down its campuses and moved classes online due to the coronavirus in March, rising sophomore Jose Garcia returned home to Vallejo, California where he expected to finish his classes and hang out with friends and family.

Then Amazon announced plans to fill 100,000 positions across the U.S at fulfillment and distribution centers to handle the surge of online orders. A month later, the company said it needed another 75,000 positions just to keep up with demand. More than 1,000 of those jobs were added at the five local fulfillment centers. Amazon also announced it would raise the minimum wage from $15 to $17 per hour through the end of April.

Garcia, a marketing and communications major, applied and was hired right away to work in the fulfillment center near Vallejo that mostly services the greater Bay Area. He was thrilled to earn extra spending money while he was home and doing his schoolwork online.

This is just the first wave of hiring for these fulfillment center jobs, and there will be a second, third, and fourth wave as eCommerce volumes have exploded. Even college students desperate for the cash might quit academics to focus on starting from the bottom in Amazon.

Even though many of these jobs at Amazon fulfillment centers aren’t those corner office job that Ivy League graduates covet, in an economy that has had the bottom fall out from underneath, any job will do.

Chronic unemployment will be around for a while and jobs will be in short supply.

When you marry that up with the boom in ecommerce, then there is an obvious need for more ecommerce fulfillment centers and college campuses would serve as the perfect launching spot for this endeavor.

The rise of ecommerce has happened at a time when the cost of a college education has risen by 250% and, more often than not, doesn’t live up to the hype it sells.

Many fresh graduates are mired in $100,000 plus debt burdens that prevent them from getting a foothold on the property ladder and delays household formation.

Then consider that many of the 1000s of colleges that dot America have borrowed capital to the hills building glitzy business schools and rewarding the entrenched bureaucrats at the school management level outrageous compensation packages.

The cost of tuition has risen by 250% in a generation, but has the quality of education risen 250% during the same time as well?

The answer is a resounding no, and there is a huge reckoning about to happen in the world of college finances.

America will be saddled with scores of colleges and universities shutting down because they can’t meet their debt obligations.

Not to mention the financial profiles of the prospective students have dipped by 50% or more in the short-term with their parents unable to find the money to send their kids to college.

Then there is the international element here with the lucrative Chinese student that added up to 500,000 total students attending American universities in the past.

They won’t come back after observing how America basically shunned the pandemic and the U.S. public health system couldn’t get out of the way of themselves after the virus was heavily politicized on a national level.

The college campuses will be carcasses with mammoth buildings ideal to be transformed into eCommerce inventory centers.

The perfect storm is hitting on every side for Mr. Jeff Bezos to go in and pick up a bunch of empty college campuses for pennies on the dollar as the new Amazon fulfillment centers.

This will happen as the school year starts and schools realize they have no pathway forward and look to liquidate their assets.

Defaults will happen by the handful in the fall, while some won’t even open at all because too many students have quit.

Then the next question we should ask is: will a student want to pay $50,000 in tuition to attend online Zoom classes for a year?

My guess is another resounding no.

By next spring, there will be a meaningful level of these college campuses that are repurposed, as eCommerce delivery centers with the best candidates being near big metropolitan cities that have protected white collar jobs the best.

The coronavirus has exposed the American college system, b as university administrators assumed that tuition would never go down.

Not every college has a $40 billion endowment fund like Harvard to withstand today’s financial apocalypse.

It’s common for colleges to have too many administrators and many on multimillion-dollar packages.

These school administrators made a bet that American families would forever burden themselves with the rise in tuition prices just as the importance of a college degree has never been at a lower ebb.

Like many precarious industries such as college football, commercial real estate, hospitality, and suburban malls, college campuses are now next on the chopping block.

Big tech not only will make these campuses optimized for delivery centers but also gradually dive deep into the realm of educational revenue, hellbent on hijacking it from the schools themselves as curriculum has essentially been digitized.

Colleges will now have to compete with the likes of Google (GOOGL), Facebook (FB), Amazon (AMZN), Apple (AAPL) and Microsoft (MSFT) directly in terms of quality of digital content since they have lost their physical presence advantage now that students are away from campus.

Tech companies already have an army of programmers that in an instance could be rapidly deployed against the snail-like college system.

The only two industries now big enough to quench big tech’s insatiable appetite for devouring revenue is health care and education.

We are seeing this play out quickly, and once tech gets a foothold literally on campus, the rest of the colleges will be thrust into an existential crisis of epic proportions with the only survivors being the ones with large endowment funds.

It’s scary, isn’t it?

This is how tech has evolved in 2020, and the tech iteration of 2021 could be scarier and even more powerful than this year’s iteration. Imagine that!

AMAZON PACKAGES COULD BE DELIVERED FROM HERE SOON!

Global Market Comments

January 9, 2020

Fiat Lux

Featured Trade:

(WEDNESDAY, FEBRUARY 5 MELBOURNE, AUSTRALIA STRATEGY LUNCHEON)

(CAPTURING SOME YIELD WITH CELL PHONE REITS),

(CCI), (AMT), (SBAC),

(JNK), (SPG), (AMLP), (AAPL), (VZ), (T), (TMUS), (S)

I am constantly bombarded with requests for high-yield, low-risk investments in this ultra-low interest rates world.

While high-yield energy Master Limited Partnerships LIKE (AMLP) can offer double-digit returns, they carry immense risks. After all, if the prices of oil drop to $5-$10 a barrel, replaced by alternatives as I eventually expect, all of these instruments will get wiped out.

You can earn 5%-8% from equity-linked junk bonds. However, their fates are tied to the future of the stock market at a 20-year valuation high against flat earnings.

You might then migrate to Real Estate Investment Trusts (REITs) like Simon Property Group (SPG), which acts as a pass-through vehicle for investments in a variety of property investments. However, many of these are tied to shopping malls and the retail industry, the black hole of investment today.

So where is the yield-hungry investor to go?

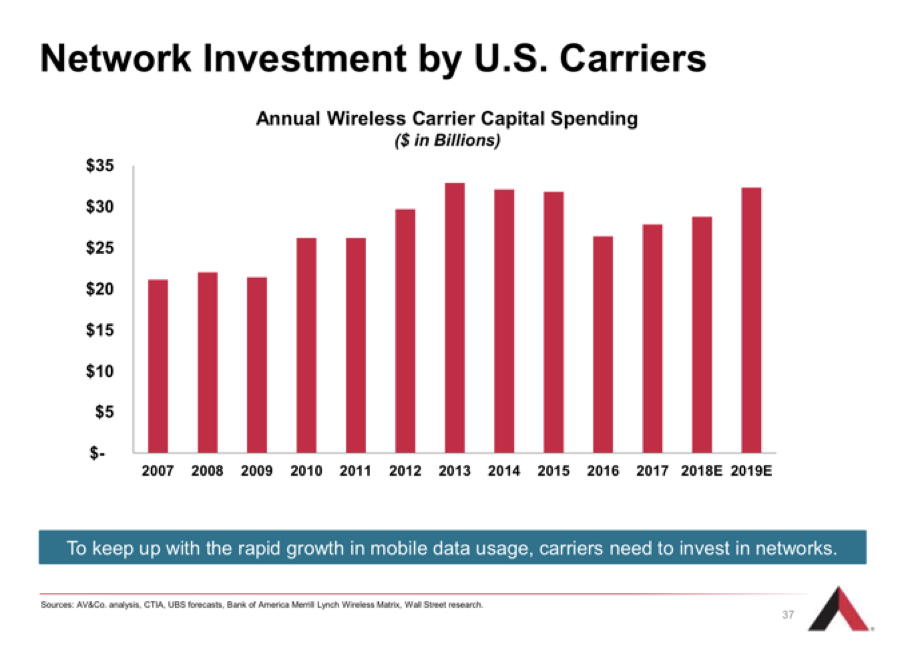

You may have heard about something called 5G. This refers to the rollout of fifth-generation wireless technology that will increase smartphone capabilities tenfold. Whole new technologies, like autonomous driving and artificial intelligence, will get a huge boost from the advent of 5G. Apple (AAPL) will launch its own 5G phone in September.

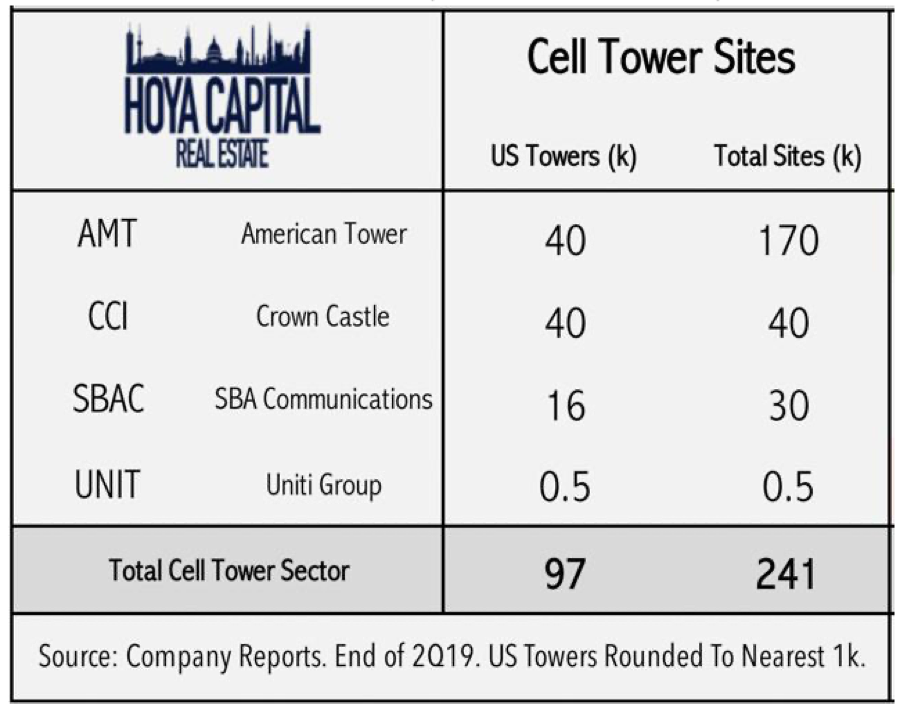

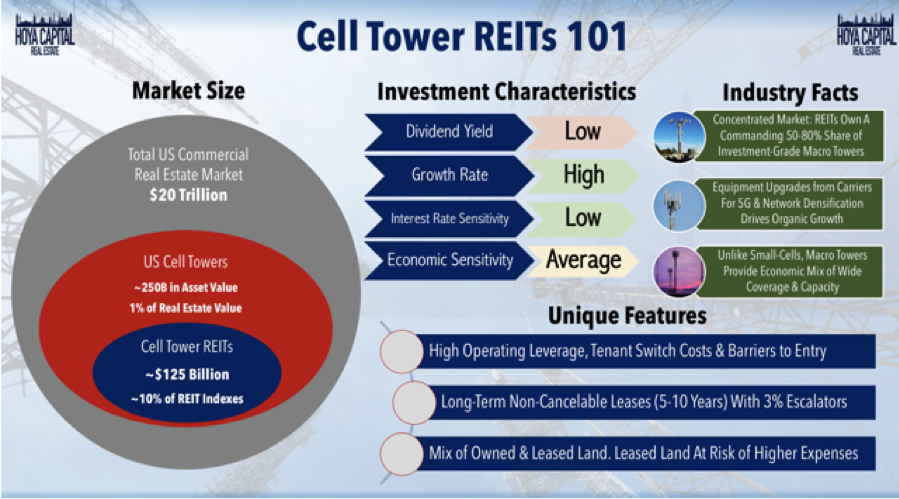

5G, like all cell phone transmissions, rely on 50-200-foot steel towers strategically placed throughout the country, frequently on mountain peaks or the tops of buildings. With demand from the big phone carriers soaring, there is a construction boom underway in cell phone towers. There just so happens to be a class of REITs that specializes in investment in this sector.

Cells Phone REITs constitute a $125 billion market and make up 10% of the REIT indexes. They own 50%-80% of all investment-grade towers. They are all benefiting from a massive upgrade cycle to accommodate the 5G rollout. These REITs own or lease the land under the cell towers and then lease them to the phone companies, like Verizon (VZ), AT&T (T), T-Mobile (TMUS), and Sprint (S) for ten years with 3% annual escalation contracts.

American Tower (AMT) is far and away the largest such REIT, with 170,000 towers, has provided an average annual return over the past ten years, and offers a fairly safe 1.65% yield. They are currently expanding in Africa. Even during the 2008 crash, (AMT) still delivered an 8% earnings growth.

SBA Communications (SBAC) is the runt of the sector with only 30,000 towers. However, it has a big presence in Central and South America and is seeing earnings grow at a prolific 80% annual rate. (SBAC) is offering a 1.48% yield at today’s prices.

Crown Castle International (CCI) is in the middle with 40,000 large towers and 65,000 small ones. 5G signals travel only a 1,000 meters, compared to several miles for 4G, requiring the construction of tens of thousands of small towers where (CCI) is best positioned. (CCI) offers a hefty 3.39% yield.

Small cell towers are roughly the size of an extra-large pizza box and will soon be found on every urban street corner in the US. AT&T (T) has estimated that there is a need for over 300,000 small cell phone towers in the US alone.

So, if you’re looking for a sea anchor for your portfolio, a low-risk, high-return investment that won’t see a lot of volatility, Cell phone REITs may be your thing. Buy (CCI) on dips.

Can you hear me now?

Global Market Comments

November 1, 2019

Fiat Lux

Featured Trade:

(OCTOBER 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(SQ), (CCI), (SPG), (PGE), (BA), (MSFT), (GOOGL), (FB), (AAPL), (IBB), (XLV), (USO), (GM), (VNQ)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 30 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Would you buy Square (SQ) around here?

A: I don’t want to buy anything around here—that’s why I’m 90% cash. Would I buy Square on a market selloff? Absolutely, it's one of our favorite fintech stocks for the long term. The fintech stocks are eating the lunch of the legacy banks at an accelerating rate.

Q: What's the best yield play currently, now that bonds have gone so high?

A: High-quality REITs—especially cell tower REITs. We’re going to get a significant increase in the number of cell towers, thanks to 5G, and there are REITs specifically dedicated to cell phone towers. An example is Crown Castle (CCI), which has a generous 3.45% dividend yield. The worst REITs are the mall-based like Simon Property Group (SPG).

Q: PG&E (PGE) has just had a huge selloff of 50%. Should I buy it now or is it a potential zero?

A: I wouldn’t touch PG&E at all—They’re already in bankruptcy, and they are now accepting responsibility for starting another eight fires this week, including the big Kincaid fires. You could have the state government take over the company and wipe out all the shareholders— the liabilities are just growing by the second, so I would turn my attention elsewhere. Don’t reach for new ways to get in trouble.

Q: Regarding Boeing (BA), it looks like you caught the bottom on the last dip—should I buy it here or wait for another dip?

A: Wait for another dip. The company seems to have an endless supply of bad news. That said, if we visit $325 a share one more time, I would buy it again. We caught about a $10 dollar move in Boeing to the upside. Keep buying the dips. The bad news story on this is almost over.

Q: Do you think the earnings season will be better than expected? If so, which sectors do you think will outperform?

A: It’s always better than expected because they always downgrade right before earnings, so everything is a surprise to the upside. Some 80% of all stocks surprise to the upside every quarter. And what would I be buying on dips? Big Tech. Especially things like Apple (AAPL), Facebook (FB), Alphabet (GOOGL), and Microsoft (MSFT) —that is where the only reliable longer-term growth is in the economy. If you want to buy cheap companies on dips, go for Biotech (IBB) and Health Care (XLV), which have gone up almost every day since we launched the Biotech letter a month ago. To subscribe to the Mad Hedge Biotech and Healthcare Letter, please click here.

Q: What does it mean that the Chile APEC summit is cancelled? What is Trump going to do now for signing on the trade deal?

A: There may not be a trade deal. It's another postponement and could be another trigger for a long-overdue selloff in the market. We've basically been going up nonstop now for 2½ months, and almost everyone's market timing indicators are saying extreme overbought territory here, including ours.

Q: Will there be a replay of this webinar posted?

A: Yes, we always post these on the website a couple of hours after it airs. Some 95% of our viewers watch the recordings, especially those overseas in weird time zones like Australia and India. You need to be logged in to access it. Just go to www.madhedgefundtrader.com, log in, go to My Account, then Global Trading Dispatch, then click on the Webinars button. It’s there in all its glory.

Q: Does Invesco DB US Dollar Index Bullish Fund ETF (UUP) make sense (the dollar basket)?

A: No, I'm staying out of the currency market because there are no clear trends right now and there are much clearer trends in other asset classes, like stock and bonds.

Q: How do you see General Electric (GE)?

A: There are a lot of people shouting accounting fraud like Harry Markopolos, the whistleblower on Bernie Madoff. Sure, they had a good today, up a buck, but their problems are going to take a long time to fix. So, don't think of this as a trading vehicle, but rather a long-term investment vehicle.

Q: Could the Saudi Aramco IPO push the price of oil up?

A: You can bet they're going to do everything humanly possible to get the price of oil (USO) up and to get this IPO off their hands—that's why you shouldn't buy the IPO. The Saudis are desperate to get out of the oil business before prices go to zero and are pouring money into alternative energy and technology through Masayoshi Son’s Vision Fund. When you have the chief supplier of oil rigging the price, you don’t want to be anywhere near the distributor and that’s Saudi Aramco.

Q: What about selling the (SPG) (Simon Property) REIT?

A: It’s kind of too late to sell, but what you might think of doing is selling short just one deep out-of-the-money put, just to bring in a small amount of income. These things don’t crash, they grind down; so, it could be a good naked put shorting situation, but only on a very small scale. If you want to play REITs on the long side, look at the Vanguard Real Estate ETF (VNQ), which pays a handy 3.12% dividend. Guess what its largest holdings are? 5G cell tower REITs.

Q: Is General Motors (GM) a buy on the union detent?

A: Only for a trade, but not much; the auto industry is the last thing you want to buy into going into a recession, even just a growth recession.

Q: Have we topped out on Apple (AAPL) for the year at $250?

A: If we did, it’s probably just short term. Remember their 5G phone is coming out next September and I expect the stock to go to $300 dollars just off of that. Any dips in Apple won’t last more than a month or two.

Q: Could we get another leg up for the end of the year?

A: Yes, not much, maybe another 5% from here, and I wouldn't do that until we get another 5% drop in the market first which should happen sometime in November. If that happens, then you’ll have a shot at making another 10% by the end of the year, which is exactly what I plan on doing for myself. That would take our 2019 performance from 50% to 60%.

Q: Is the Fed’s printing infinite money going to lead to runaway inflation crashing the value of the dollar?

A: Yes, but it may take us a couple of years to get to that point. So far, no sign of inflation, except inflation of things you want to buy, like healthcare, a college education, and so on. For anything you want to sell, like your labor or service, the prices are collapsing. That’s the new inflation, the type that screws you the most.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader