Mad Hedge Technology Letter

November 18, 2024

Fiat Lux

Featured Trade:

(SPOTIFY WORTH A LOOK)

(SPOT), (META), (PINS)

Mad Hedge Technology Letter

November 18, 2024

Fiat Lux

Featured Trade:

(SPOTIFY WORTH A LOOK)

(SPOT), (META), (PINS)

If new research from Pew Research is anything close to accurate, there appears to be a massive shift underway that has major ramifications for the online media landscape.

Pew Research discovered that 40% of young adults rely on social media influencers without formal journalism training.

Gone are the days when journalists needed to cut their teeth doing coverage on the ground.

This phenomenon has reversed with social media influencers and podcasters dishing out the real media from the comfort of their home.

Yes, this has been happening for a while, but the data suggests we are on the cusp of the legacy media becoming the minority.

The evolving landscape was most notably taken advantage of the richest man in the world, Elon Musk, who used X.com to propel him into politics.

Most social media users relying on news influencers say the information they offer is unique and sometimes more helpful than what they’d find elsewhere and less likely to be fake.

Social media news is also reliant on ad revenue to stay afloat, so in that sense, it could be beholden to advertiser demands on viewpoint and ideology. The legacy media has the same ongoing problem with advertisers, and I believe there is no perfect model.

Yet, the direct connection of social media profiles to audience has grown and will remain attractive moving forward.

According to the survey, traditional journalism is dead, and 40% of young adults under 30 rely on these news influencers to stay updated on current events and politics.

While X, formerly Twitter, is the most popular platform for news influencers, video app TikTok and Google’s YouTube are home to the largest share of news influencers who monetize their content and have no formal background in journalism. Of the news influencers on TikTok, 84% haven’t worked in journalism, and roughly three-quarters of those influencers try to make money off their news analysis, whether by asking for tips, peddling merchandise, or touting separate subscriptions to additional exclusive material, Pew found.

The Pew report analyzed hundreds of news influencer accounts with more than 100,000 followers; surveyed more than 10,600 US adults about their news consumption habits; and reviewed content from more than 100,000 posts across Facebook, Instagram, TikTok, X, and YouTube from July and August.

One of the reasons traders cannot short META stock is because of this cash cow business tied to social media.

Instagram and Facebook are still great businesses, even if they aren’t growing like they used to.

TikTok is a private company, and so is X.com, and there are no stock opportunities there.

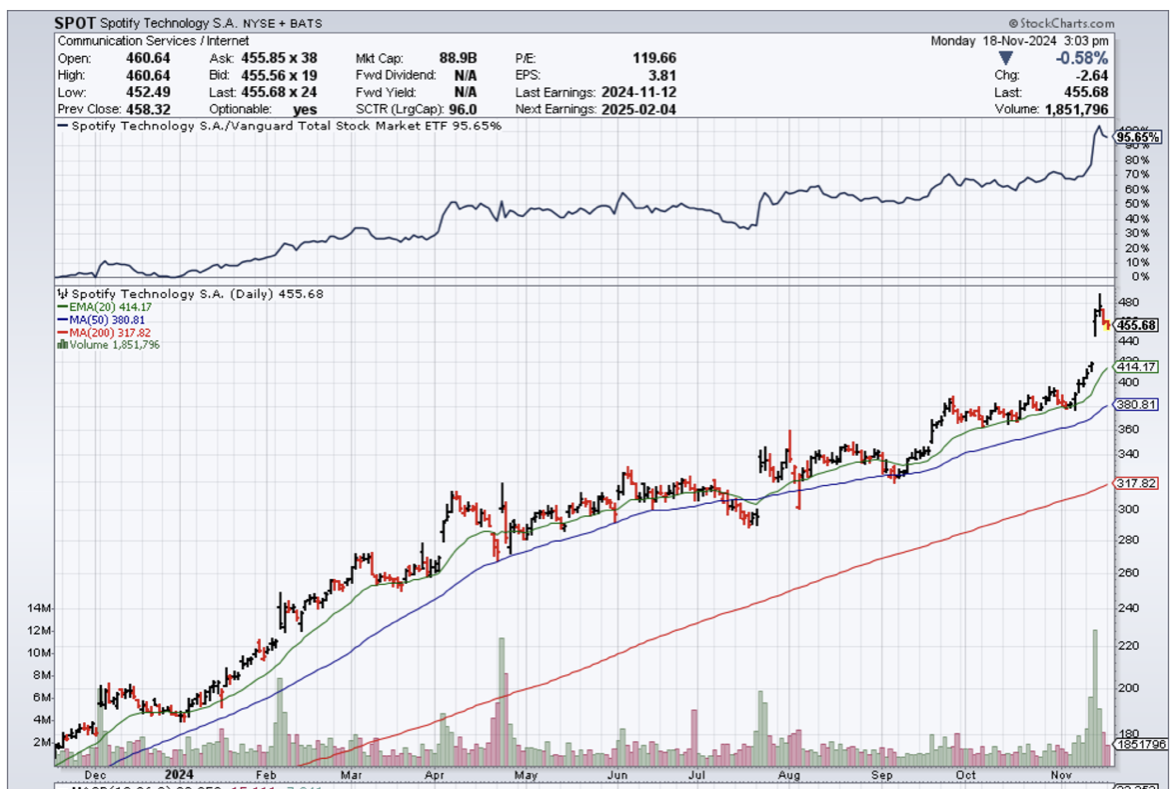

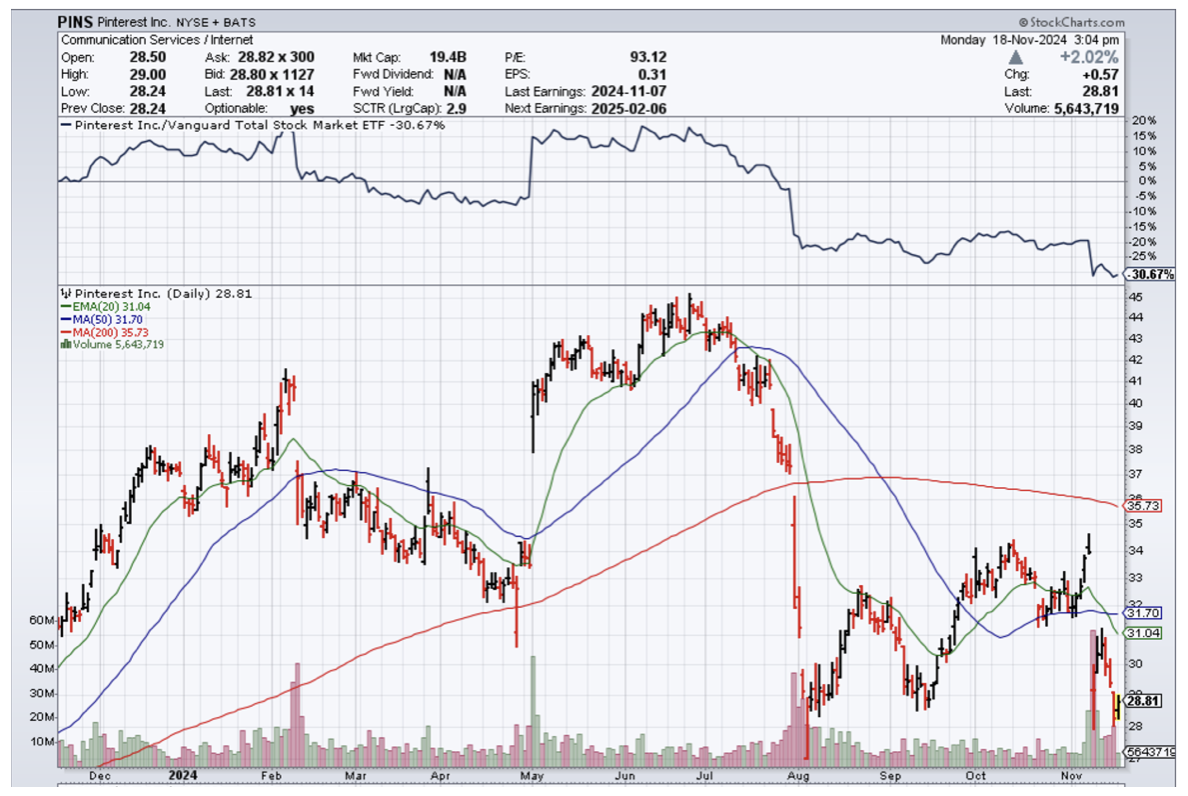

However, I would suggest readers take a look at Pinterest (PINS) and Spotify (SPOT).

PINS is still growing almost 20% per year, and I do believe the stock has an upside with the recent involvement of venture capitalists.

SPOT is in the podcast industry and has a locked-in quasi-monopoly in this sub-sector.

Podcasts and their popularity have exploded in the past few years, highlighted by SPOT signing podcaster Joe Rogan to a monster $100 million contract.

Legacy media has also followed up the election with terrible audience numbers, suggesting that the existing viewer base has decided to move on or temporarily pause participation.

META, PINS, and SPOT should be serious buy-the-dips candidates moving forward as the pivot to alternative media goes from a drip to a waterfall. As I am rereading this newsletter, the AP just fired 8% of its staff, citing “fast- changing conditions in the media industry.”

Mad Hedge Technology Letter

June 3, 2024

Fiat Lux

Featured Trade:

(RAISING SUBCRIPTION PRICES MEANS PROFITS FOR SPOTIFY)

(SPOT), (NFLX)

Mad Hedge Technology Letter

April 10, 2024

Fiat Lux

Featured Trade:

(PODCASTS A NEW EXPERIMENT FOR SPOTIFY)

(SPOT)

The dominant music streaming platform Spotify is trying harder these days.

When I say trying harder, I mean trying harder to become profitable because after almost a generation of when burning cash was ok, investors suddenly demand a business that doesn’t run a minus every year.

Zero rates have had an oversized effect on the balance of business in 2023 and 2024.

Failure isn’t rewarded with gaudy executive compensation and more vested shares.

Belt tightening by cutting staff and streamlining operations is the paradigm we are finding ourselves in.

Spotify was the prototypical loss maker in tech that was given a pass because it grew users fast.

Now that interest rates are high, tech companies are penalized by going to the debt markets too much and the effect is magnified if a company needs a high amount of debt.

Logically, SPOT has made diversifying revenue a top bullet point in their strategic future and that is exactly what they are doing.

SPOT has also discovered it can generate additional money from the most diehard music fans. Currently, all listeners pay the same rate for access to a musician’s catalog. But there are fans willing to pay far more to support an artist they love, as evidenced by the rising price of concert tickets, merchandise, and even vinyl for Korean artists.

SPOT plans to raise the price of its popular audio service in several key markets for the second time in a year, a crucial step toward reaching long-term profitability.

The streaming giant will increase prices by about $1 to $2 a month in five markets by the end of April, including the UK, Australia, and Pakistan, according to people familiar with the matter.

It will raise prices in the US, its largest territory, later this year, said the people, who asked not to be identified discussing confidential plans.

The higher prices will help cover the cost of audiobooks, a popular service introduced late last year.

Spotify offers customers up to 15 hours of audiobook listening a month as part of their paid plan. While the company pays publishers for books, it has so far only collected additional revenue from listeners who exceed the limit.

Spotify paid record labels, artists, and others more than $9 billion last year – from $13.2 billion in revenue.

Last year, SPOT posted its best year of user growth ever, with 113 million new sign-ups to its free and paid services.

Spotify had 602 million users at the end of 2023, including 236 million paying customers.

The success of the price increase has given management confidence to seek even more. Under the new pricing, individual plans will go up by about $1 a month, while family plans and so-called duo plans for couples will rise by $2.

In the last 365 days, the stock has catapulted from $134 to over $300 per share.

The stock is absolutely resonating with investors and moves by management have been aggressive to branch out from the music royalty business.

Buy SPOT on the dip.

Mad Hedge Technology Letter

December 4, 2023

Fiat Lux

Featured Trade:

(SPOTIFY SHOWS US THE WAY)

(SPOT)

The music streaming service Spotify (SPOT) is living in the future and by that I mean they are cutting 17% of staff.

Silicon Valley will be a lot leaner in the future and this is just one of many firms that will shed to become more efficient.

The announcement was made today and is making shockwaves through the industry.

Many ponder what might be the catalyst to the next move up in the tech sector.

Well, look no further than Spotify which is delivering the playbook to squeeze out higher earnings at a time when tech earnings are exposed to potential downgrades.

It’s no joke that tech salaries are exorbitant and gutting the froth is the next stage of Silicon Valley.

Elon Musk delivered us a preview when he dumped 80% of Twitter’s staff realizing that most of his staff didn’t meaningfully contribute or justify what they earned.

Spotify is next to take a magnifying glass to its balance sheet as it hopes to appease shareholders as we head into a 2024 interest rate-cutting year.

It’s my guess that CEO Daniel Ek wants to get his show to benefit from that slingshot effect next year for Spotify shares.

In an email sent out to staff, Ek said that Spotify was taking “substantial action to rightsize our costs,” adding that the company took on too many employees over the years 2020 and 2021 when the capital was cheap and tech companies could invest significant sums into team expansion.

The latest round of cuts equates to roughly 1,500 jobs.

It comes after Spotify reported a 65 million euros ($70.7 million) profit in the third quarter, citing lower spending on marketing and personnel.

Spotify raised the prices of its subscription plans earlier this year and has been expanding into podcasts and audiobooks.

Spotify cut 6% of its workforce, or about 600 employees, at the start of the year. Spotify then laid off 2% of staff, equivalent to roughly 200 roles, in June.

This isn’t the first time they have shed staff and won’t be the last.

Europe has barreled straight into an economic recession and the macroeconomic backdrop has given a great reason for Ek to downsize.

With the way generative AI is going, I don’t believe any further staff cuts will be followed by a hiring bump, because AI will get the job done instead of humans.

Around 2021, we blasted through peak tech hiring and we will never see not only that type of volume hiring, but gone are the days of sweet salaries.

It’s a lot cheaper to plug in software and tech firms will continue to downsize even though economic growth waves come and go.

No economic growth wave in the future will prompt a massive uptick in fresh faces.

AI and its advancement of will effectively mean that Spotify will be run by a few people running servers, infrastructure, and algorithms.

Eventually, the entire tech sector will be run by a handful of people and software underpinning their investments and Ek of Spotify will be included in one of the handful in this exclusive group.

Buy SPOT on the dip.

Mad Hedge Technology Letter

August 2, 2023

Fiat Lux

Featured Trade:

(SPOT ON WITH SPOTIFY)

(SPOT), (AMZN), (APPL)

Many industries have experienced consolidation in the last few years and music streaming has been no exception.

The strong emergence of a few companies running the show has resulted in these same companies wielding extraordinary pricing power.

Spotify (SPOT) has been one of the leading music streaming platforms for years, and when companies harness pricing power, they can raise prices to compensate for higher expenses.

That is exactly what Spotify did recently as their stock sold off on a wider-than-expected loss for the second quarter, even though subscribers surged.

The streaming service posted a net loss of 302 million euros.

Monthly active users (MUAs) beat estimates of 530 million to hit 551 million — a 27% improvement compared to the year-ago period. Net additions of 36 million represented Spotify's largest quarterly net addition performance in its history.

Premium subscribers also surpassed expectations of 217 million, jumping another 17% year over year to hit 220 million.

In its first-quarter report, the company said it expected to add 15 million new monthly active users in Q2, bringing its total to 530 million. It also expected revenue of 3.2 billion euros and to report 217 million paid subscribers in the quarter.

Spotify is continuing to invest in advertising, and its ad-supported revenue grew 12% year over year. The company said podcast advertising revenue growth reaccelerated to more than 30% year over year.

Spotify will increase the price of its Premium subscription offerings by as much as $2, which translates to a 20% rise for some plans.

In the U.S., Spotify’s Premium Individual offering now costs $10.99, up from $9.99, and the price of its Premium Duo plan changed to $14.99, up from $12.99. The company’s Premium Family plan is now priced at $16.99, up from $15.99, and the Student offering costs $5.99, up from $4.99.

Spotify doesn’t expect a drawdown in product demand from the price increase, and let’s face it, most people can handle paying an extra 2 bucks for something they use every day.

Music streaming is definitely close to becoming an industry participated in by just a few for as long as it’s a viable business.

That means Spotify will also have the opportunity to raise subscription prices again in the future.

The licensing issues alone are too much of a hurdle for most companies to get to launch so to really compete takes a high amount of upfront funds and in the world of high interest rates, tech firms can’t fund this type of retread business again.

Spotify isn’t a pure monopoly.

The others involved are Apple Music, Amazon, Tidal, Deezer, and Pandora.

SPOT’s stock has increased by over 85% after the earnings pullback, and at one point they were up over 100%.

Growing subscriptions at 27% is still considered something that a growth company does at a time when growth companies are hard to find.

It doesn’t matter that they aren’t profitable yet, as long as they add more subscribers, which they have strongly indicated they will.

The stock has pulled back from $175 and once the negative shakeout fades away, traders should get into SPOT while they still can.

Mad Hedge Technology Letter

March 22, 2021

Fiat Lux

Featured Trade:

(WHAT’S THE DEAL WITH SPOTIFY?)

(SPOT)