Mad Hedge Technology Letter

December 17, 2018

Fiat Lux

Featured Trade:

(WHY TENCENT WILL REMAIN TRAPPED IN CHINA)

(TME), (SPOT), (IQ), (GOOGL), (FB)

Mad Hedge Technology Letter

December 17, 2018

Fiat Lux

Featured Trade:

(WHY TENCENT WILL REMAIN TRAPPED IN CHINA)

(TME), (SPOT), (IQ), (GOOGL), (FB)

So you thought that Tencent Music Entertainment (TME), the Spotify (SPOT) of China, going public at $13 a share on the New York Stock exchange would mean the music streaming giant would potentially tyrannize the Western music streaming market.

Relax, it will never happen, China’s personal data laws are analogous to Facebook’s (FB) lax data guidelines multiplied by a factor of 10.

There is no possible scenario in which a Chinese content service constructed at the magnitude of Tencent Music Entertainment Group would ever get the thumbs up from American regulators.

The ongoing trade war has effectively barred any Chinese capital’s ability to snap up key American technological firms, as well as stymieing any Chinese tech unicorns dishing out streaming content in participating in a monetary relationship with the American consumer.

In August, the Department of the Treasury which chairs the Committee on Foreign Investment in the United States (CFIUS) rolled out an expansionary pilot program widening CFIUS’ jurisdiction to review foreign non-controlling, non-passive investments in companies that produce, design, test, manufacture, fabricate, or develop “critical technologies” within certain industries deemed paramount to national security.

Even though the amendment does not specify China, it means China.

If you had a hunch that Tencent would take over the music streaming world, then the better question is to ask yourself if Tencent Entertainment is equipped to take over the Chinese streaming world and monetize the product efficiently.

What really is (TME)?

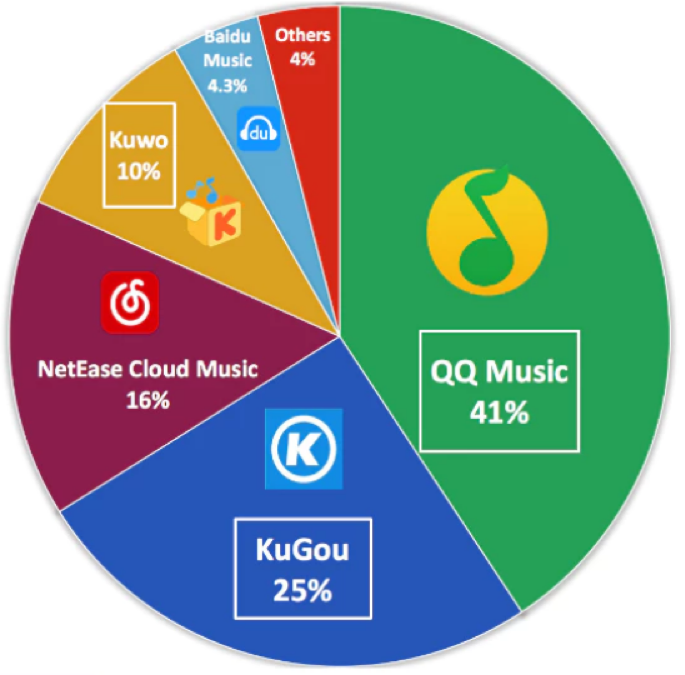

(TME) is the Tsar of Chinese music streaming with apps that allow users to stream music, sing karaoke, and watch musicians perform live. (TME) dominates this sphere of Chinese tech with a combined 800 million monthly active users.

(TME) is a concoction of services including QQ Music, Kugou, Kuwo, and karaoke app WeSing making up over 70% of the music streaming industry in China.

Its daily active users (DAUs) spend over 70 minutes per day on the platform and have inked exclusive deals with elite Western artists.

Tencent Music's revenue nearly doubled YOY to $2 billion during the first nine months of 2018, and its net income more than tripled to $394 million.

The social entertainment services aspect has been a massive revenue driver for them including income from virtual gifts on WeSing, a platform where fans gift virtual items to favorite singers, and sign up for premium memberships giving users access to exclusive concerts.

This collection of clever services mixed with social media has been successful, and the reason why it comprises 70% of total revenue.

Paid membership has grown 24% YOY to 9.9 million while paid users only make up 4.4% in China. This is a huge change in the tech climate from the past when Chinese netizens would never pay for internet content. This has allowed the average revenue per user (ARPU) to creep up to $17.22 per paid user.

The other 30% of revenue can be attributed to its ad-less music service which is not ad-less for free users.

So, in fact, the 30% of the business that mirrors Spotify is its Achilles heels echoing the painstaking task of monetizing pure music content.

No company has ever shown that a pure music streaming internet model can be profitable, the music streaming graveyard is littered with the failed attempts of companies from the past.

The unit registered a mere $1.24 in average revenue per paid user during the third quarter, paltry compared to (TME)’s social media products.

(TME)’s combination of social media and music entertainment weighted towards virtual gifts’ income is a weak business model in the west and would not extrapolate in the western world.

It is a supremely China model only unique to China and other Asian countries.

Therefore, I would point out that even if this arm of Tencent could migrate to America, management knows better than to put square pegs in round holes.

That being said, its potential in China is its long runway and most Chinese content companies haven’t been able to crack the western market.

The only types of Chinese companies that have had any remnant of success in the west are hardware companies and look what happened to telecommunication equipment companies Huawei and ZTE recently – taken out by the western regulatory sledgehammer.

It’s crystal clear that the Chinese understanding of personal data and IP regulation simply don’t marry up with western standards, and that is why I suggested that these two massive tech worlds are in for a hard splintering dividing these two competing models.

There has been some intense jawboning going on behind the scenes as Huawei, who is in the lead to develop 5G technology, still needs Qualcomm’s radio access technology to make 5G a reality.

The scenario of a hard fork between western and Chinese 5G becomes more real each passing day.

Part of Tencent Music’s ability to perform revolves around its swanky position installed in the center of the most popular chat app in China called WeChat.

Using this position as a fulcrum, Tencent Music plans to invest 40% of the capital raised from its IPO on expanding its music library, 30% on product development, 15% on marketing, and the last 15% on M&A.

For right now, there is an elevated emphasis on growing the number of paid users and converting its free users to premium subscriptions.

Ironically enough, Spotify has a 9% stake in Tencent Music and Tencent has a 7.5% holding in Spotify. Just by having stakes in each other is enough reason to avoid migrating into the same competitive markets with each other.

If you read between the lines, the stakes seem more a pledge of trading expertise in developing each other’s business as you see traces of each other in both unicorns.

Would I invest in Tencent Music?

One word – No.

There are almost 1,000 pending lawsuits alleging copyright infringement, not a huge surprise here.

Tencent concedes around 20% of the music content is not licensed.

Pouring fuel on the fire, a Tencent Music executive is also being sued by a seed investor claiming he was bullied into selling his stake ahead of its IPO.

There are question marks surrounding this company and that might have been part of the justification of tapping up the American public markets to prepare for this next stage of uncertainty.

As it is, Spotify cannot make money because of the elevated royalty costs eroding its business model, (TME) probably can if it steals most of its music, but that is a suicide mission waiting to happen.

Fortunately, Tencent is a hybrid mix of not only pure music streaming but of social media fused with music apps through gift giving gimmicks and karaoke-themed services.

These higher margin drivers are the reason why Tencent is profitable and Spotify is not, plus the giant scale of servicing 800 million Chinese users that give credence to the freemium model.

However, it’s entirely feasible that Tencent Music could use a good portion of the $1.1 billion from the IPO to battle the slew of pending lawsuits waiting around the corner.

Would you want to invest in a company that went public just to fund their legal defense?

Definitely not.

Look at its streaming cousin iQIYI (IQ), shares peaked over $40 in June after its IPO and have swan-dived ever since going down in a straight line and is trading around $17 today.

In general, most Chinese tech stocks have been collateral damage of a wider trade war pitting the maestros of crude geopolitical strategies against each other.

This year has not been kind to Chinese tech shares, and considering most of Tencent’s music library has been stolen, investors would be crazy to invest in this company.

I am surprised this company held up as well as it did on IPO day because the timing of the IPO couldn’t have been worse in a segment of tech that is awfully difficult to become profitable in a country whose economy is softening by the day in an insanely volatile stock market.

And to be honest, I would have stopped listening about this company after knowing they face pending lawsuits of up to 1000.

As for Spotify, yes, they are the industry leader in music streaming but investors need concrete proof they can become profitable. I like the direction of increasing operating margins, but that all goes to naught if it’s in a perpetual loss-making enterprise. I would sit out on both these stocks with a much negative bias towards its ticking time bomb Chinese music version.

Regulation and the trade war have taken a huge swath of tech off the gravy trade such as semiconductors, Google, social media, hardware, American tech who possess supply chains in China and I would smush in Chinese tech ADR’s on that list too.

Stay away like the plague.

Global Market Comments

December 14, 2018

Fiat Lux

Featured Trade:

(DECEMBER 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (MU), (PYPL), (SPOT), (FXE), (FXY), (XLF), (MSFT), (AMZN), (TSLA), (XOM),

(SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader December 12 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader

Q: Is the bottom in on the S&P 500 (SPX) or are we going to go on another retest?

A: It’s stuck right in the 2600-2800 range, and I think that’s probably where we bounce off of 2600 again. The question is whether or not we can clear the top of the range at 2800. If we can’t, I would fully expect a retest of this bottom in which case I could see it going down to 2500.

Q: You say you’ll go 100% cash by Dec 21st but also stated that the S&P 500 will go up 5% by the year's end. Should we stay in until we get the up 5% move?

A: Yes, all of our options positions expire by the 21st but if you’re just long in stocks, I would stay long, probably through the end of the year.

Q: Will the Chinese-U.S. dispute ruin the Tech industry?

A: No, I think the Trump Administration will have to do some kind of deal and call it a victory, otherwise the trade war will pull the U.S. into recession. If we go into the next presidential election with another recession—well, no one has ever survived that. Even with the China-U.S. dispute, the U.S. is still dominant in the Tech industry and will continue to do so for decades to come.

Q: China has managed to duplicate Micron Technology’s (MU) biggest selling chip, undercutting prices—thoughts?

A: True, Micron is the lowest value added of the major chip producers, therefore their stock has gotten hit the worst of any of the chip stocks down by about 46%, but I know Micron very well and they have a whole range of chips they’re currently upgrading, moving themselves up the value change to compete with this. So, that makes it a great company to own for the long term.

Q: I’m up 90% on my PayPal (PYPL) position—should I take a profit?

A: Yes! Absolutely! How many 90% profits have you had lately? You are hereby excused from this webinar to go execute this trade. And well-done Dr. Denis! And thank you for the offer of a free colonoscopy.

Q: What can you say about Spotify (SPOT)?

A: No, thank you—there’s lots of competition in the music streaming business. We are avoiding the entire space. The added value is not great, and many of these companies will have a short life. And with China’s Tencent growing like crazy, life for Spotify is about to become dull, mean, and brutish.

Q: What’s your view on currencies?

A: So you’re looking to make another fortune? Yes, I think the Euro (FXE) and the Yen (FXY) really are looking hard to rally, and the trigger could be dovish language in the next Fed meeting. Once the Fed slows its rate of interest rates rises, the currencies should take off like a scalded chimp.

Q: Will the banks (XLF) rally in the next 6 months for a better sell?

A: Many people are waiting for a rally in the banks so they can unload them and haven’t gotten it—they’re back to pre-election price levels. The issue here is structural, and you don’t get recoveries from major structural changes in an industry. It’s significant that this is the first bull market that had no net new employment in the banks whatsoever; the business is fading away. They are the new buggy whip makers. These gigantic national branch networks will all be gone in ten years because the banks can’t afford them.

Q: Would you enter the Microsoft (MSFT) trade today?

A: I actually think I would; Microsoft only pulled back 10% when everything else was dropping 30%, 40%, or 50%. That shows you how many people are trying to get into this name so if you could take a little short-term pain (like 5%), the stock outright is probably a screaming buy here. I think it’ll go to $200 one day, so here at $110-$111 it looks like a pretty good deal. The story here is that Microsoft is rapidly taking market share from Amazon (AMZN) in the cloud business and that’s going to continue.

Q: When will you be updating your long-term model portfolio?

A: I usually do it at the end of the year, and rarely make any big changes. I’ll still be selling short bonds and still like Tesla (TSLA) and Exxon (XOM).

Q: I just joined your service. What is the best way to get started?

A: I’ll give you the same advice that I gave every starting trader at Morgan Stanley (MS). Start trading on paper only. When you are making money reliably on paper, move up to using real money, but only with one contract per position. When that is successful, slowly increase your size to 2, 3, 5, 10, and 20 contracts. Pretty soon, you will be swinging around 1,000 contracts a lot like I do. The further you move down the learning curve the greater you can increase your size and your risk. If you never get past the paper stage at least it’s not costing you any money.

I hope this helps.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 18, 2018

Fiat Lux

Featured Trade:

(UNDERSTANDING THE REAL COMPETITION),

(SPOT), (AAPL), (GOOGL), (MSFT), (HUAWEI)

Microsoft sells computers?

That was the bizarre look I got after telling my friend that Microsoft (MSFT) is in the business of selling laptops, desktop computers, and tablets that convert into laptops from a product line called Microsoft Surface.

This is not your father’s Microsoft.

Things are different now.

Everything changed once they got rid of Steve Ballmer whose inertia prevented Microsoft from taking advantage of the huge influence they culled in the tech sector from being the universal operating system for PCs.

Ballmer’s lack of technical expertise was his own downfall stemming from his terrible decision to buy Nokia’s handset business for $7.6 billion.

The board of directors forced him out and was a blessing in disguise.

Thousands were laid off in the Nokia handset division and a massive write-down was taken.

As big tech spread out their wings and branch off into various businesses they never imagined before, they have reinvented the former images of themselves.

This goes for Microsoft who’s taking their legacy business of Microsoft Office and Windows and leveraging it with the cloud to create a stellar product.

And with the cash hoard, not only are they creating new products by fusing together old products with new technologies, they are overlapping into other big tech companies’ turf.

The overlapping products can be seen in hardware products made by this software behemoth and their neighbors.

The Microsoft Surface division is up 25% YOY speaking volumes to the quality hardware Microsoft produce now even if you didn’t know about it.

Apple (AAPL) has attracted most of the conversation in the "smart" headphones space because of the AirPods.

The sleek white earbuds are becoming ubiquitous with the headphone space trending to a smaller and "true" wireless.

A schism has formed as the AirPods don’t satisfy the entire spectrum of smart headphone fans.

The retro ear-muff shaped headphone with more immersive sound is what I am talking about, and I do recognize that Beats has been in the market for a decade.

Microsoft chose to go this route with their smart headphones and this is their answer to the iconic AirPods and the Google (GOOGL) Pixel Buds.

This smart headphone comes with an embedded digital assistant and integrates noise cancellation.

I tried out the Microsoft's Surface Headphones before they came on the market, and I only had positive things to say about the quality and experience.

They sound impressive, the controls are easy to use, and the modern design is definitely a plus.

The color could use a little reimagination but all in all, I was pleased.

Microsoft Cortana, Microsoft’s digital assistant, for all who don’t know, is also slipped into the experience and a tap on the right earcup will summon Cortana.

It seems that Microsoft still needs a few kinks to work out with Cortana, but voice activation and smart assistants like Siri and Google Assistant can be found in almost every hardware and software product now.

Headphones are city workers’ second most important smart device because of its functionality.

Have you ever been on the New York metro and seen how many people are wearing smart headphones?

Quality headphones shut off the outside world and warm up the insides with the user’s favorites on Spotify (SPOT) or Apple Music.

Stressing out on the commute into work in an Uber is common and calming the frayed nerves before workers enter into the office of dungeons and dragons has a type of value that can never be replicated.

Urban dwellers need high-quality smart headphones and these big tech companies are acutely aware of this.

Google has made an audacious attempt to integrate real-time foreign translation into the Pixel Buds. It only works with Google’s Pixel phones, is hard to operate, and needs the Google Translate app on the phone.

It’s a good first step but the applications using smart headphones are endless.

Smart assistants are the key.

As they become more adept at processing the real world, they streamline and better a human’s life.

Microsoft’s smart headphones have embedded Skype, one of Ballmer’s positive acquisitions during his tenure. And with Cortana integration, it could morph into a natural extension of the Windows 10 experience.

Microsoft’s smart headphones morph into a point of conversion for more of Microsoft’s hardware products as they start to construct an expanding moat.

Headphones used to be more or less the same.

Plug it into the jack and you’re on your merry way.

The headphones of today are looking more different from each other with every iteration.

This was glaringly evident when Apple chose to no longer sell any phones with a 3.5mm headphone jack.

Ironically enough, Google dumped the headphone jack with its Pixel 2 phones a year later even though they bashed Apple for it a few months earlier.

The reason was mainly functional as Google said, “We want the display to go closer and closer to the edge.”

Gradually, smartphones will get rid of everything except a razor-thin screen. All the other clunky business in and around it needs to go. This is the first step and home buttons have been chopped off smartphones as well.

It is fine to get consumed in the battle of smart products between Silicon Valley companies, but there is a larger threat.

Chinese smart products are rapidly catching up to what American companies can produce.

The Middle Kingdom hasn’t surpassed American tech expertise yet but they are debuting devices relative to the competition that could only be dreamed about a few years ago.

Huawei's flagship smartphone Mate 20 and Mate 20 Pro pack a lot of punch and this must be frightening to the FANGs.

The timing of the phone debut is a big victory for American smartphone companies because this phone is good enough to grab market share from existing American companies but aren’t allowed to sell inside America.

Congress putting the kibosh on any sliver of a chance to partner with an American carrier means that there will be no chance of Chinese phones gutting the American smartphone market.

What it does mean is that they will invade and dominate other markets such as South East Asia, Eastern Europe, and Russia.

The same will go for any Chinese smart device.

Huawei has given up trying to circumvent the government blockade.

The Huawei Mate 20 is priced around $800 and the Mate 20 Pro at $1140. They are probably two of the best smartphones ever made and are a direct threat to any American company’s revenue that manufactures smartphones and smart devices.

Mad Hedge Technology Letter

October 17, 2018

Fiat Lux

Featured Trade:

(THE SPOTIFY REGIME),

(SPOT), (AAPL), (NFLX), (MSFT), (AMZN), (GS)

It’s not earth-shattering to concede that our attention spans have shrunk and as a result, there are unintended consequences.

The various smart devices and other technology vying for a slice of your precious attention have been accepted as the new normal.

Whether it’s binging on Netflix (NFLX) or gaming on a Microsoft Xbox (MSFT), consumers are absorbed obsessively staring into a screen most of the day.

As tech penetrates the core of our existence, the music industry has been the recipient of changes that were hard to fathom just a few years ago.

And as all businesses morph into pseudo-tech enterprises supported by data analytic teams, management is able to unearth some compelling data and utilize it to commercialize the audience.

Spotify (SPOT), the world’s leading music streaming platform, doesn’t monetarily reward music artists unless a stream surpasses a minimum of 30 seconds.

This is just one way that Spotify’s founder and CEO Daniel Ek has changed the music industry.

Think about the implications.

Gone are the elaborate instrumentals to warm listeners up before a catchy chorus hooks you forever.

Songs are entirely front loaded now with the end goal of persuading listeners to not swipe until the 30-second barrier is passed.

Whatever happens after that doesn’t matter – the song might as well go silent because Spotify will pay the artist.

According to Spotify data, Ed Sheeran’s “The Shape of You” is Spotify’s most-streamed song with 1.94 billion listens.

This is just one scant nugget of data in Spotify’s treasure trove of global music data that finely chronicles the state of the music industry and how consumers devour music.

Spotify CFO Barry McCarthy promptly explained the Spotify’s relationship with data and music at the Goldman Sachs’ (GS) Communacopia conference by saying, “The company with the most data wins. The company with the most data insights wins. The company with the engineering culture, software-driven business wins. And that’s the play we’re making.”

In the current tech climate, I will take software over hardware any day of the week.

Hardware sales are a one-off event until the next cycles bring an upgraded iteration which could take years to execute.

Software sales are an annual recurring revenue stream that is as sticky as the software's quality giving hope to company CFO’s of a perpetual income stream.

It doesn’t matter that Spotify isn’t profitable. The end goal isn’t to make money in an industry that is notoriously difficult to combat the royalty expenses eroding 70% of every $1 of revenue.

What has happened is that Spotify is too big to fail and it loves every second of it.

The music industry needs Spotify just as much as Spotify needs the music industry and this awkward partnership is far from a match made in heaven, but it works for the foreseeable future.

It helps that artists, for the most part, have bought into the data-based streaming model.

Music artists have turned into tech-like firms themselves.

Their new goal is to compile an audience then monetize like Spotify itself.

It speaks volumes of how the tech model has penetrated every corner of the world.

Apple (AAPL) is acutely aware of the potency a music streaming service offers and has been investing in Apple Music, its music streaming arm.

Rumors have been swirling that Apple absorbed the entire staff of a music analytics firm called Asaii including the owners, for a tad under $100 million.

This talent grab on the heels of the Shazam purchase indicates that Apple seeks a better understanding of how to curate music playlists and better serve music fans who own Apple devices.

Even though Apple has the second leading music streaming service, they have ceded the battle to Spotify.

CEO of Apple Time Cook is on record saying, “We’re not in it for the money.”

Indirectly, Cook means Apple Music is a loss-making division and he doesn’t care because it is just a small fragment of what makes Apple one of the best companies in the world.

Apple has also commissioned 24 television shows and 2 films costing them $1 billion.

A single billion is peanuts considering the eye-popping amount of Apple’s cash hoard. They can afford to take the long-term view and slowly enhance the ecosystem instead of Spotify whose eggs are all in one basket.

Apple is more concerned about offering iOS users the best experience possible and in return Cook hopes to count on them to use iOS devices for a lifetime.

Apple Music’s biggest weakness is its biggest strength.

In short, Apple music is tailored to the iOS operating system.

If you sign up, the app directs users to sign up for an Apple ID if you do not already have one.

Android lovers have little interest in signing up for Apple Music considering they do not have an Apple device and then must pay $9.99 per month after the introductory 3-month offer expires when Spotify is free. It’s not worth the extra hassle.

It is almost certain that Spotify will enact an Android operating system pivot to build a moat around its business and that is something Apple cannot do.

Spotify will start partnering with Samsung, Microsoft, and the Android-based Asian manufacturers to focus on monetizing the Android audience and make it even more inconvenient for listeners to access Apple Music.

Signing up for Spotify and listening to its ad-free subscription without creating an Apple ID is more appealing.

And after three months, users have the option to continue a free version of Spotify, albeit with digital ads popping up.

This leads me to the belief that there is definitely space for more than one player in the music streaming industry.

Amazon is another tech firm who has a music streaming service but are more concerned if they convert users into prime memberships.

If compiling the most music data wins out, then Spotify is in the lead with its 83 million paid users and 101 million free users.

Apple trails in second place with 50 million users which is still an extraordinary number of listeners and easily monetizable.

The way music streaming platforms works is that users are more likely to listen to the most popular artists and songs and not look for an adventure.

The app is merely there to locate the songs they already like or click on a recommendation produced by an algorithm.

It’s not like going out on a Friday night to experience some unknown singer in a grunge basement and becoming a new fan. Users know what they want, and they desire to access it. Such is the nature of internet search.

Spotify’s data shows that out of 3 million artists on the platform, 200,000 artists receive 70% of the music streams, clearly segmenting the haves and have-nots.

The rest of the 2.8 million are struggling to be discovered and cannot cut a wage off of Spotify’s platform.

Online music streaming products also align perfectly well with artificial intelligence-based voice activation technology.

These services will deeply integrate this technology into its services as they desire to ramp up the quality of services.

As for the music streaming business hopefuls, it's game over as the three major players have the leverage to put out any fires that crop up.

When you break it down, Spotify has a 180 million user audience growing at 30% YOY and is hellbent on becoming profitable.

As they enhance the platform’s tools and services, gradually expect more subscription-based products to entertain users.

And even if Spotify doesn’t become profitable as soon as they would like, the aggregate hoard of data will multiply in value.

Spotify is already the most prized music asset in the world with a market cap of $26 billion, about $10 billion higher than all global music revenues.

Yes, Spotify destroyed album artwork and its audio quality of 320 kilobits per second is no match for CD-quality audio. But this is the world we live in today and Daniel Ek’s Spotify is the 800-pound gorilla in the room.

Spotify is a great long-term buy-and-hold asset. Take the latest weakness to add to your position.

Mad Hedge Technology Letter

October 3, 2018

Fiat Lux

Featured Trade:

(OUR HOME RUN ON SQUARE),

(SQ), (V), (AMZN), (GRUB), (SPOT), (MSFT), (CRM), (AAPL)

Pat yourself on the back if you pulled the trigger on Square (SQ) when I told you so because the stock has just lurched over an intra-day level of $100.

It was me aggressively pushing readers into buying this gem of a fin-tech company at $49. To read that story, please click here (you must be logged in to www.madhedgefundtrader.com).

Since then, the price action has defied gravity levitating higher each passing day immune to any ill-effects.

The Teflon-like momentum boils down to the company being at the cross-section of an American fin-tech renaissance and spewing out supremely innovative products.

At first, Square nurtured the business by targeting the low hanging fruit– small and medium size enterprises in dire need of a strong injection of fin-tech infrastructure.

It largely stayed away from the big corporations that adorn billboards across the Manhattan skyline.

That was then, and this is now.

Square is going after the Goliath’s fueling a violent rise in gross payment volume (GPV).

Modifying themselves for larger institutions is the next leg up for Square.

They recently inaugurated Square for Restaurants for larger full-service restaurants.

Business owners do not need technical backgrounds to operate the software and integrating Caviar into this program emphasizes the feed through all of Square’s software.

Dorsey has built an ecosystem that has morphed into a one-stop shop for comprehensively running a business.

Migrating into business with the premium corporations offers an opportunity to augment higher margin business.

This is the lucrative path ahead for Square and why investors are festively lining up at the door to get a piece of the action.

The downside with an uber-growth company like Square are lean profits, but they have managed to eke out three straight quarters of marginal spoils.

However, the absence of profits can be stomached considering the total addressable market is up to $350 billion.

Grabbing a chunk of that would mean profits galore for this too hot to handle company.

Expenses are always a head spinner for Silicon Valley firms and attracting a dazzling array of engineers to spin out breathtaking profits can’t be done on the cheap.

The Cash app download figures are sizzling and is one of the most popular apps in the app store.

Square’s marketing strategy is also turning a corner getting out their name leading to sale conversions.

These are just several irons in the fire.

The last two years has seen this stock double each year, could we be in for another double next year?

If measured by growth, then I see why not.

Growth is the ultimate acid test deciding whether this stock will be dragged down into the quick sand or let loose to run riot.

Other second-tier tech firms in the middle of a sweet growth spot pack a potent punch like Spotify (SPOT) and Grubhub (GRUB) which are growing annual sales around 50-60%.

Material profits are also irrelevant for the aforementioned tech juggernauts.

Square is expanding at the same fervent pace too, and the hyper-growth only makes payment processors like Visa (V) quasi-jealous of such staggering numbers.

And when Square trots out numbers to the public like that with (GPV) shooting out the roof, the stock does nothing but go gangbusters.

Either way, Square has popularized making credit card payments through smartphones and that in itself was a tough nut to crack amongst tough nuts.

Square also has a line-up of impressive point-of-sales products such as Caviar.

In fact, merchant sellers are adopting an average of 3.4 Square software apps with invoices, loans, marketing, and payroll software being the most beloved.

Square also offers other software that can handle back office tasks and manage inventory.

The software and services business is on pace to register over $1 billion in sales in 2019.

The breadth of functions that can boost a company’s execution highlights the quality of software Dorsey has produced.

I always revert back to one key ingredient that all tech companies must wildly indulge in to fire up the stock price – innovation.

Innovation in bucket loads is something all the brilliant tech firms crave such as Microsoft (MSFT), Amazon, and Salesforce (CRM).

Overperformance starts from the top and trickles down to the people they hand pick to manage and run the businesses.

Jack Dorsey is right up there with the best of them and his influence cannot be denied or ignored.

His stewardship over his other company Twitter (TWTR) is sometimes worrisome because of a pure scheduling conflict, but it’s obvious which company is having a better year.

Square steers clear of the privacy and regulatory minefields handcuffing Twitter.

And it could be safely assumed that Dorsey enjoys his afternoons more at Square than his mornings across the street at Twitter where he is bombarded by heinous problems up the wazoo.

When you conjure up an up-and-coming company that could rattle the establishment, Square is one of the first companies that comes to mind.

Some analysts even argue this company deserves to be lifted into the vaunted Fang group.

I would say they are on their merry way but they just aren’t big enough to command a spot on the Fang roster.

I have immense conviction this stock will be a deep influencer of our time, and its diversified software offerings add limitless dimensions underpinning massive revenue streams.

In Q2, the subscription revenue grew 127% YOY underscoring the success the software team is having, crafting productive apps applicable to business owners.

Business owners can even take out a loan through Square Capital which issues micro-loans to small business owners.

In need of financing? Ring up Dorsey’s company for a few quid.

Starkly contrasting Square in the payment processors space is Visa (V).

Visa is not a hyper-growth company going ballistic, but a stoic behemoth unperturbed.

The 3.283 billion visa cards that adorn its insignia represents scintillating brand awareness and efficiency.

When Tim Cook was asked if Apple (AAPL) plans to disrupt Visa, he smirked and said, “People love their credit cards.”

This is a prototypical steady as she goes-type of company.

They do not offer micro-loans to small businesses or dabble with any of the murky sort of products that can be found on the edge of the risk curve.

They are a safe and steady pure payment processor.

Its network can digest 65,000 transactions per second and is universally cherished as a brand around the world.

All of this led to an operating margin of 66% in 2017.

Square has identified other parts of the payment process to snatch and do not directly compete with Visa.

They partner with Visa and pay them a processing fee.

Subsequently, Square is paid a merchant fee after the payment is approved.

Visa has a monopoly and a moat around their business as wide as can be.

Square is a different type of beast – growing uncontrollably and hell-bent on spawning a revolutionary fin-tech paradigm shift.

The question is can Square eventually turn payment heavyweights like Visa on its head?

The path is fraught with booby traps and as Square generates the projected sales and bolsters its revenue, it could start to encroach on these legacy processors too.

Yet, it’s too early to delve into that threat yet.

Enjoy the ride with Square and better to lay off this potent stock until a better entry point presents itself.

This stock will go higher. Giddy-up!