Mad Hedge Technology Letter

September 26, 2018

Fiat Lux

Featured Trade:

(DID SIRIUS OPEN UP PANDORA'S BOX?),

(SPOT), (P), (SIRI), (AAPL), (AMZN)

Mad Hedge Technology Letter

September 26, 2018

Fiat Lux

Featured Trade:

(DID SIRIUS OPEN UP PANDORA'S BOX?),

(SPOT), (P), (SIRI), (AAPL), (AMZN)

In a flurry of deals, the music streaming industries consolidation is powering on as some of the industry’s biggest players have completed new acquisitions.

Is there a new King of the Castle?

Not yet.

In any case, the shakeout still allows Spotify to claim itself as the No. 1 company in the music streaming industry, but Apple (AAPL) and Sirius XM (SIRI) have gained.

There is still work to be done for the trailing duo but it is a step in the right direction.

Apple’s deal with Shazam, which just gained approval, was consummated last December, but was held up by European regulators over antitrust problems.

The Europeans have clamped down on American tech companies of late forcing them to play nicer after decades of running riot inside the region.

The Shazam app analyzes then pinpoints titles from music, movies, and television shows based on a brief sample through the device’s microphone.

If your neighbors are blasting the tunes upstairs at a Friday night shindig and you want to find out what song is causing you to lose sleep at night, just turn on your microphone and upload it into Shazam.

Shazam will tell you exactly the song’s title and the artist’s name.

Even dating back to 2013, this app was among the top 10 most popular apps in the world.

In 2018, Shazam has carved out a user base of more than 150 million monthly average users (MAU) and growing.

Shazam is used more than 20 million times per day.

An opportunity lies in urging Shazam users to then adopt Apple music.

Interestingly enough, to upgrade the quality of the app’s functionality, Apple is stripping away digital ads in Shazam.

Apple has made an unrelenting attempt to avoid introducing lower grade tech that could potentially taint its clean-cut brand.

Recently enough, film producers have complained that Apple is completely averse to any content with gratuitous violence, excessive drug use, and candid sex scenes.

Apple wants to cultivate and sell its pristine image.

Digital ads also fail to make the cut.

This spotless image boosts Apple’s pricing power along with the high quality of products that has seen Apple retain its place as the producer of the best smartphone in the world.

Other smart phone brands are still in catchup mode with a brand image significantly inferior to Apple’s.

And Apple CEO Tim Cook isn’t even interested in monetizing Apple music, and is more focused on “doing the right thing” for it.

Yes, the job of every company is to be in the black, but the No. 1 responsibility for a modern tech company is to grow and grow profusely.

Tech investors pay for growth, period.

As investors have seen with Netflix, companies can always raise prices after seizing market share because of the stranglehold on eyeballs inside a walled garden.

That potent formula has been the bread and butter of powerful tech companies of late.

Spotify is a captive of the music industry, of which it is entirely dependent for its source of goods, in this case songs.

At the same time, the music industry has fought tooth and nail to destroy the likes of Spotify, which benefits immensely from distributing the content it creates.

History is littered with failed music streaming services outgunned in the courtroom. Pandora (P) is the biggest public name out there whose share price has tanked over the long haul.

Pandora has created a proprietary algorithm offering song recommendations to listeners, but it is more or less an online music streaming app heavily reliant on a freemium pricing model with ads.

Sirius XM Holdings, a satellite radio company, signaled its intent in the music streaming business by taking a 19% in Pandora’s business last year.

It has followed that up now by completing a full takeover of the Oakland, California company for $3.5 billion.

This move adds 75 million users to its 36 million usership on Sirius and, in my view, the main objective is an eyeball grab to buy more listeners dragging them into its walled garden.

To triple a user base instantly to 75 million listeners is a boon for Sirius, which now has the firepower to legitimately compete with Spotify.

Pandora has been shopping itself around for the past two years, and companies such as Facebook were whispered to be eyeing this company.

Facebook chose to focus on developing dating and romance functions on its platform, and has mainly ignored the music streaming possibilities.

More critically, it allows Sirius to diversify out of the car space where satellite radio is predominantly used.

As much as Americans love to drive, the home is where they rest, and sleep, and Pandora will unlock a path into the home of listeners.

Synergies between home audio through Pandora, and car audio through Sirius should be evident over time.

The music streaming industry, such as the television streaming industry, has become fiercely competitive as of late. And this is a prudent move for Sirius to buy a new customer base at the same time as moving into the home.

The trend of tech companies penetrating the home and making it as smart as possible is revived constantly.

This piece of news isn’t as earth-shattering as Amazon’s (AMZN) smart home product launch event, but nonetheless indicates another leg up in competition for fresh user growth and its data.

This M&A surge is occurring amid a backdrop of the music industry’s obsession to exterminate Spotify and the other music streaming companies.

They are on a mission to force up the royalties these Internet giants must pay to pad their pockets and protect their interests.

Royalties are the music streaming companies’ main cost, and for Spotify, these royalty payments eat up 78% of total revenue.

But that does not mean Spotify is a bad company or even a bad stock.

Every company has its share of pitfalls. Throw in the mix that Amazon (AMZN) and Apple have music streaming services that do not even need to make a profit, and you will understand why some might be wary about putting new money to work in music streaming business stocks.

The primary reason that Spotify shares will outperform for the foreseeable future is because it is the preeminent music streaming platform.

Also, there is favorable latitude to make way toward the goal of monetization, and ample space to improve gross margins.

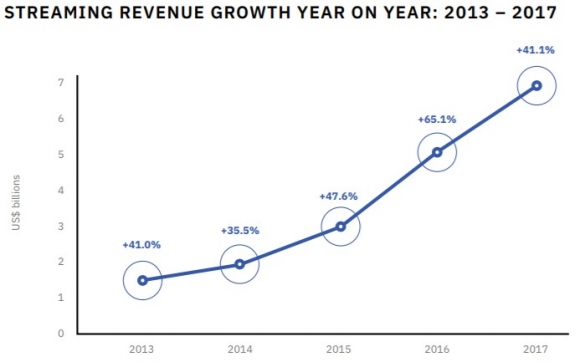

Global streaming revenue growth has gone ballistic as the migration to mobile devices and cord cutting has exacerbated the monetization prospects of the music industry.

Streaming revenue was a shade under $2 billion in 2013, and continued to post a growth trajectory of more than 40% each year since.

As it stands now, total global streaming revenue registered just a tick under $7 billion per year in 2017, and that was an improvement of 41.1% from 2016.

The choice among choices is Spotify in 2018.

The company was dogged by many years of famous artists removing their proprietary content from the platform citing unfavorable terms.

Eventually, almost all artists have relented and reinstalled their music on Spotify. They depend on alternative moneymaking avenues to compensate for lack of royalties, mainly live music.

Spotify has seized even more industry power with its new function of completely bypassing the music industry altogether, by offering a way for aspiring artists to directly upload music content onto its online platform.

Crushing the middleman has been a widespread theme in the tech industry for the past few decades, and the music industry is no different.

As technology has hyper-accelerated, the cost of producing music has plummeted giving access to just about anyone who has any talent.

No need to rent a sound studio for thousands of dollars per hour anymore in West Hollywood, and the music industry knows it.

It could be possible that the next cohort of viral artists will never cough over a dime to the music industry, and the bulk of the profits will be collected by a music streaming titan that distributes their content online.

How does Spotify make money?

It earns its crust of bread through paid subscriptions but lures in eyeballs using an ad-supported free version of its platform.

Naturally, the paid version is ad-less, and this subscription is around $5 to $15 per month.

In the second quarter, Spotify’s paid subscription volume surpassed 83 million, a sharp uptick of 40% YOY.

Ad-supported users came in at more than 101 million, even under the damage that General Data Protection Regulation (GDPR) did to western tech companies.

The ad-supported subscribers rose 23% YOY, and the paid version expects between 85 million to 88 million paid subscribers in the third quarter.

Many of the new paid subscribers are converts from its free model.

Spotify is poised to increase revenue between 20% to 30% for the rest of 2018.

The rise of Spotify's developing data division could extract an additional $580 million of revenue in 2023, making up 2% of total revenue.

When Spotify did go public, the robust price action was with conviction, making major investors - such as China’s Tencent, which possess a 9.1% stake and Tiger Global Management, which owns 7.2% - happy stakeholders.

In the last quarter’s earnings report, Spotify CFO Barry McCarthy reiterated the company’s goal to push gross margins from the mid-20% range to “gross margins in the 30% to 35% range.”

A jump in gross margins would go a long way in making Spotify appear more profitable, and that is the imminent goal right now.

Bask in the glow of the growth sweet spot Spotify finds itself in right now.

For the time being, the music division of Amazon and Apple are just a side note, even with Apple’s purchase of Shazam.

But Apple is vigorously improving its service products as its software and services segment moves from strength to strength, but that doesn’t particularly mean Apple Music.

Investors must sit on their hands to see how Sirius’s acquisition of Pandora plays out. These are by no means two extraordinary companies, and a major overhaul is required to make these two mediocre companies into one overperformer.

If you had to choose among Sirius, Pandora, or Spotify, then cautiously leg into a few shares of Spotify to test the waters.

Mad Hedge Technology Letter

August 29, 2018

Fiat Lux

Featured Trade:

(THE BEST TECH STOCK YOU’VE NEVER HEARD OF),

(TTD), (AMZN), (GOOGL), (NFLX), (BIDU), (BABA), (SPOT), (P), (FB)

If you asked me which is the best company that most people do not know about then there is one clear answer.

The Trade Desk (TTD).

This company was founded by one of the pioneers of the ad tech industry Jeff Green, and he has spent the past 20 years improving data-based digital advertising.

Green established AdECN in 2004 and its claim to fame was the world’s first online ad exchange.

After three years, Microsoft gobbled up this firm and Green stayed on until 2009 when he launched The Trade Desk. This is where he planned to infuse everything he learned about the digital ad agency into his own brainchild.

Green concluded that creating a self-service platform, avoiding privacy issues, and harnessing big data for digital ad campaigns was the best route at the time.

Green hoped to avoid the pitfalls that damaged the digital ad industry mainly bundling random ads together that diluted the quality and potency of the ad campaigns.

It did not make sense that a digital ad for baby diapers could be commingled with an ad for retirement homes.

Green created real-time bidding (RTB), which is a process in which an ad buyer bids on a digital ad and, if won, the buyer’s ad is instantly displayed on the selected site.

This revolutionary method allowed ad buyers to optimize ad inventory, prioritize ad channels, and boost the effectiveness of campaigns.

(RTB) is a far better way to optimize digital ad campaigns than static auctions, which group ads by the thousand.

In real time, advertisers are able to determine a bespoke ad for the user to display on a website. Green used this model to develop his company by building a platform tailor-made to execute (RTB).

Naturally, he won over many naysayers and his company took off like a rocket.

Results, in a results-based business, were seen right away by ad buyers.

A poignant example was aiding a performance-based ad agency in trimming ad waste by more than 50% for a national fast food chain with thousands of locations across America.

It took just one year for The Trade Desk to carve out a profitable business as ad agencies flocked to its platform desiring to take advantage of (RTB) or also commonly known as programmatic advertising.

Customer satisfaction is evident in its client retention rate of 95% for the past few years highlighting the dominating position The Trade Desk possesses in the digital ad industry.

The Trade Desk has not raised fees for ad buyers lately, but the value added from The Trade Desk to customers is accelerating at a brisk pace.

A great value proposition for potential clients.

The vigor of the business was highlighted when Green cited that each second his company is “considering over 9 million ad opportunities” for their ad inventory shows how The Trade Desk is up to date on almost every single ad permutation out there.

This speaks volume of the ad tech, which is the main engine powering the bottom lines at Google search and rogue ad seller Facebook (FB).

Google only gets 63,000 searches per second and shows that The Trade Desk has pushed the envelope in providing the best platform for ad buyers to seek its perfect audience.

Green’s mission of supporting big ad buyers optimize their ad budget has really caught fire and in a way that is completely transparent and objective.

The foundations that Green has assembled became even more valuable when Alphabet (GOOGL) chose to remove DoubleClick IDs, which would now prevent ad buyers from cross-platform reporting and measurement.

Previously, DoubleClick ID could cull data from assorted ads and online products based on a unique user ID named DoubleClick ID.

Ad purchasers then would data transfer to pull DoubleClick log files and measure them against impressions served from other ad servers across the web.

Effectively, ad buyers could track the user through the whole ad process and determine how useful an ad would be to that specific user.

In an utter conservative move to satisfy Europe’s General Data Protection Regulation (GDPR), DoubleClick IDs are no longer available for use, and tracking the ad inventory performance from start to finish became much harder.

Cutting off the visibility of the DoubleClick ID in the DoubleClick ecosystem was a huge victory for The Trade Desk because DoubleClick ID measured 75% of the global ad inventory.

Ad buyers would be forced to find other measurement systems to help calculate ad performance.

Branding and executing as the transparent and fair ad platform helping ad agencies was a great idea in hindsight with the world becoming a great deal more sensitive to data privacy.

The Trade Desk is perfectly placed to reap all the benefits and boast excellent technology to capitalize on this changing big data landscape. It is already seeing this happen with new business wins including large global brands such as a major food company, a global airline, and another large beverage company.

The global digital ad market is a $700 billion market today and trending toward $1 trillion in the next five to seven years

The generational shift to mobile and online platforms will invigorate The Trade Desk’s bottom line as more big ad buyers will make use of its proprietary platform to place programmatic ads.

Content distribution systems are fragmenting into skinny bundles hyper-targeting niche content users such as Sling TV, FuboTV, and Hulu.

There are probably 30 different ways to watch ESPN now, and these 30 platforms all require ad placement and optimization.

Some of the names The Trade Desk is working with are the who’s who of digital content ownership or distribution including Baidu (BIDU), Google, Alibaba (BABA), Pandora (P), and Spotify (SPOT) -- and the names are almost endless.

It’s the Wild West of ads and content these days because TV distribution has never been more fragmented.

Content creation avenues are desperate to boost ad income and are increasingly attempting to go direct to consumers.

Ad-funded Internet TV barely existed a few years ago. And ad inventory is all up for grabs benefitting The Trade Desk.

All of this explains why the stock is up more than 180% in 2018, and this is just the beginning.

The growth numbers put Amazon (AMZN) and Netflix (NFLX) to shame.

The Trade Desk scale on inventory has spiked by more than 700% YOY.

The option to hyper-target increases as more ad inventory is stocked.

Management mentioned in its second-quarter performance that “nearly everything went right. We executed well and one of the most dynamic environments we've seen.”

It is one of the most bullish statements I have heard from a public company.

Quarterly revenue ballooned 54% YOY to a record $112 million, and the 54% YOY growth equaled the 54% YOY growth in Q2 2017.

Ad Age's top 50 worldwide advertisers doubled ad spend in the past year positioning The Trade Desk for continued hyper-growth, not only for 2018 but in 2019 and beyond.

Mobile spend jumped nearly 100% YOY, accounting for 45% of ad spend on the platform, which is 400% higher than the industry average for mobile ad spend according to eMarketer.

Data spend was also a huge winner rising by nearly 100% smashing another record.

In the meantime, the overseas business continued its robust growth in Europe and Asia, up 85% YOY.

The Trade Desk confidence in its performance chose to increase guidance to $456 million for the year, a 48% YOY improvement.

When upper management says “when we see surprises, they typically are to the upside” you take notice, because this tech company is perfectly placed in a growth sweet spot.

Massive developing markets are just starting to dabble with programmatic advertising. Markets such as China will see it become the new normal soon, opening up even more business for The Trade Desk.

The Trade Desk is also rolling out new products that will automate more of the process and reduce the number of clicks.

Wait for the pullback to get into this ad tech stock because even though it is up big this year, we are still in the early innings, and shares will march even higher.

________________________________________________________________________________________________

Quote of the Day

“I have a deep respect for the fundamentals of television, the traditions of it, even, but I don't have any reverence for it,” – said Netflix chief content officer Ted Sarandos.

Mad Hedge Technology Letter

August 28, 2018

Fiat Lux

Featured Trade:

(SPOTIFY STILL HAS SOME UPSIDE),

(SPOT), (AMZN), (AAPL), (P)

Investors sulking about Spotify’s (SPOT) inability to make money do not get the point.

Yes, the job of every company to be in the black, but the No. 1 responsibility for a modern tech company is to grow, and grow fast.

Tech investors pay for growth, period.

As investors have seen from Netflix, companies can always raise prices after seizing market share because of the stranglehold on eyeballs inside a walled garden.

That potent formula has been the bread and butter of powerful tech companies of late.

Spotify is a captive of the music industry, of which it is entirely dependent for its source of goods, in this case songs.

At the same time, the music industry has fought tooth and nail to destroy the likes of Spotify, which benefits immensely from distributing the content it creates.

History is littered with failed music streaming services outgunned in the courtroom. Pandora (P) is the biggest public name out there whose share price has tanked over the long haul.

The music industry will battle relentlessly to exterminate Spotify and force up the royalties these Internet giants must pay as their main input.

But that does not mean Spotify is a bad company or even a bad stock.

Every company has its share of pitfalls. Throw in the mix that Amazon (AMZN) and Apple (AAPL) have music streaming services that do not even need to make a profit, and you will understand why some might be wary about putting new money to work in music streaming business stocks.

The primary reason that Spotify shares will outperform for the foreseeable future is because it is the preeminent music streaming platform.

Also, there is favorable latitude to make way toward the goal of monetization, and ample space to improve gross margins.

Global streaming revenue growth has gone ballistic as the migration to mobile and cord cutting has exacerbated the monetization prospects of the music industry.

Streaming revenue was a shade under $2 billion in 2013, and continued to post a growth trajectory of more than 40% each year since.

As it stands now, total global streaming revenue registered just a tick under $7 billion per year in 2017, and that was an improvement of 41.1% from 2016.

There are no signs of yielding as more avid music fans push into the music streaming space.

Social media platforms have helped publicize popular artists’ content.

Music is effectively a strong part of youth culture, which will eventually see the youth integrate a music streaming app into their daily lives for the rest of their adult lives.

The choice among choices is Spotify in 2018.

The company was dogged by many years of famous artists removing their proprietary content from the platform citing unfavorable terms.

A prime example was in 2009 when Lady Gaga’s hit song “Poker Face” only received $167 in royalty payments from Spotify for the first million streams. This highlighted the rock-solid position Spotify has curated inside the music industry.

Individual artists’ fight against Spotify has been dead on arrival from the outset, but the benefits and exposure from cooperating with the company far outweigh the drawbacks.

Eventually, almost all artists have relented and reinstalled their music on Spotify. They depend on alternative moneymaking avenues to compensate for lack of royalties, which is mainly live music.

That is why it costs an arm and a leg to go see Taylor Swift in living flesh now, and why those summer festivals dotted around America such as Coachella command premium ticket prices.

How does Spotify make money?

It earns its crust of bread through paid subscriptions but lures in eyeballs using an ad-supported free version of its platform.

Naturally, the paid version is ad-less, and this subscription is around $5 to $15 per month.

In the second quarter, Spotify’s paid subscription volume surpassed 83 million, a sharp uptick of 40% YOY.

Ad-supported users came in at more than 101 million, even under the damage that General Data Protection Regulation (GDPR) did to western tech companies.

The ad-supported subscribers rose 23% YOY, and the paid version expects between 85 million to 88 million paid subscribers in the third quarter.

Many of the new paid subscribers are converts from its free model.

Spotify is poised to increase revenue between 20%-30% for the rest of the year.

The rise of Spotify's developing data division could extract an additional $580 million of revenue in 2023, making up 2% of total revenue.

Remember that Spotify’s reference price set by the New York Stock Exchange (NYSE) was $132 in April 2018. The parabolic move in the stock on the verge of eclipsing $200 undergirds the demand for high-quality tech companies.

When Spotify did go public, the robust price action was with conviction, making major investors - such as China’s Tencent, which possess a 9.1% stake and Tiger Global Management, which owns 7.2% - happy stakeholders.

In the last quarter’s earnings report, Spotify CFO Barry McCarthy reiterated the company’s goal to push gross margins from the mid-20% range to “gross margins in the 30% to 35% range.”

A jump in gross margins would go a long way in making Spotify appear more profitable, and that is the imminent goal right now.

The path to real profitability is still a long way down the road and small victories will offer short-term strength to the share price.

If Spotify can retrace to around the $185, that would serve as a perfect entry point into a stock that has given investors few chances in which to participate.

July and August have only offered meager entry points into this stock, one around the $180 level in August, and another around $170 in July.

Spotify enjoyed a great first day of being public after its unorthodox IPO ending the day at $149. The momentum has continued unabated while Spotify has posted all the growth targets investors come to expect from companies of this ilk.

Bask in the glow of the growth sweet spot Spotify finds itself in right now.

The long-term narrative of this stock is intact for a joyous ride upward, and only whispers of Amazon and Apple meaningfully attempting to monetize this segment could derail it.

For the time being, the music part of Amazon and Apple are just a side business. They have other priorities, such as Apple’s battle to avoid being exterminated from communist China, and Amazon’s integration of Whole Foods and new-fangled digital ad business.

________________________________________________________________________________________________

Quote of the Day

“Ever since Napster, I’ve dreamt of building a product similar to Spotify,” – said cofounder and CEO of Spotify Daniel Ek.

Mad Hedge Technology Letter

August 15, 2018

Fiat Lux

Featured Trade:

(HOW TO PLAY THE NEW FORTNITE GAMING FAD),

(ATVI), (EA), (AMD), (NVDA), (MSFT), (AAPL), (GOOGL), (TWTR), (SNAP), (FB), (SPOT), (GAMR)

Each generation grows up in its own unique environment.

Childhood experiences differ more and more as the world rapidly changes because of hyper-accelerating technology.

Millennials are usually defined as children born between 1981 to 1996.

They were the last generation to grow up outside breathing crisp, fresh air and meandering around the neighborhood with their friends looking for excitement.

Generation Z is the first generation in America generally raised indoors because of their overwhelming preference and broad-based addiction to technology.

Social media stocks have been a huge winner from this new paradigm shift in the behavior of young adults.

Instead of running around the block in packs, children are laser focused on these platforms communicating with the entire world and propping up their social lives.

Children meet a lot less than they used to and convening on a social media platform of choice has become the new normal.

Platforms such as Twitter (TWTR), Instagram and Snapchat (SNAP) have convincingly won over these new eyeballs even so much so that the new "going out" is congregating on Snapchat with a group of friends.

Facebook (FB) is now considered a legacy social media platform full of millennials and the older crowd.

Generation Z do not fancy drugs or drinking like the youth before them, rather, their panacea is video games and a lot of them.

These new societal trends will hugely affect your portfolio going forward.

A battle royal game is a video game category mixing the survival, exploration and scavenging elements together with last-man-standing gameplay.

These types of games predominantly contain 100 players sharing the same experience on a broadband connection.

This genre has been all the rage with PlayerUnknown's Battlegrounds (PUBG) piling up 400 million gamers across the globe selling 50 million copies of the game.

Of the 400 million gamers, 88% access the game via mobile devices highlighting the vigorous shift to mobile for younger generations.

PUBG made more than $700 million in sales in 2017.

The rise of the billion-dollar video games is alive and well.

In fact, Activision Blizzard (ATVI) stakes claim to eight gaming franchises commanding more than $1 billion in annual revenue with titles such as Overwatch, Candy Crush, and Call of Duty.

The popularity of video games will drive GPU manufacturers Nvidia (NVDA) and AMD (AMD) to new heights because gamers require high-quality GPUs to effectively game.

Nvidia CEO Jensen Huang even spouted that "the success of Fortnite and PUBG are just beyond comprehension" boosting GPU sales and capturing the imagination of global youth.

Fortnite, a "Hunger Games" style battle royal video game mirroring PUBG, has taken the world by storm in 2018.

This cultural juggernaut surpassed the 125 million gamer mark in just one year.

In February 2018, Epic Games, the maker of Fortnite, earned $126 million in one month, and it was the first time it passed PUBG in monthly sales.

In April 2018, it followed up monster February numbers by pulling in $296 million.

The growth trajectory is parabolic. Hold onto your hats.

Fortnite sparkles in the sunlight because its free-to-play model does not exclude anyone and is available on all devices.

At first, Fortnite was available for iOS customers and Samsung Android holders because it inked an exclusive deal with Samsung.

This week is the first week Epic Games is rolling out Fortnite to non-Samsung Android users with an interesting caveat.

The Android version of Fortnite bypasses Google Play (Google's app store on Android) preferring to sell the game direct for download from its official website.

This highlights that content is truly king.

Epic Games is betting the surge in popularity for its juggernaut game will sell itself.

This decision will cost Alphabet (GOOGL) $70 million per year in commission.

Apple makes it mandatory that any app downloaded to its devices must be downloaded from Apple's app store.

However, Android doesn't have the same requirements as its system is more functional, open, and a developer's dream.

Simply put, there are ways to download the game on Android without ever touching Google Play.

Going forward this could have a similar effect Spotify (SPOT) had on Wall Street on its IPO.

The middlemen or broker app could get bypassed in favor of direct sales.

Apple pockets commission on 30% of all in-app spending raking in around $60 million from Fortnite.

In-game add-on revenue is how Fortnite makes money from this free-to-play game.

The bulk of spending comes in the form of costumes better known as skins, where players pay to dress up their character in various garments selected for purchase.

The other revenue stream is a season subscription on sale for $10.

The tech sector has been migrating to subscription-based offerings and video games are no different.

This could play havoc with Alphabet's Google Play and Apple's app store down the line if prominent content producers choose to bypass their stores to sell directly.

The lack of video game exposure to the FANG group is mind-boggling. It seems they have their finger on the pulse of every other major trend in technology but have missed out on this one.

Microsoft (MSFT) is the closest FANG-like stock deep inside the video game ecosphere by way of its famous console Xbox.

In fact, Microsoft earns more than $10 billion per year from its gaming segment surpassing Nintendo at $9.7 billion per year.

This doesn't eclipse Sony's gaming revenue, which is $17 billion per year, but the 36% YOY growth in Xbox-related revenue signals its intent in the gaming industry that plays second fiddle to its cloud and software businesses.

Gaming is just a side business for Microsoft right now.

Ironically, Tencent has a 40% stake in Epic Games and is patiently waiting for government approval to sell Fortnite in China, which could be painstakingly arduous.

If Tencent gets the green light, Fortnite could develop into a monster business in 2018, and this is just the beginning.

Regrettably, Tencent has been mired in regulatory issues with the communist government reluctant to approve selling in-game products, which usually make up the bulk of revenue.

Recent blockbuster hit "Monster Hunter: World" was blocked by censors after debuting to great fanfare on August 8, 2018.

This title was expected to be one of the most popular video games of 2018.

Chinese state censors are on a short-term crusade to block the video game industry from receiving critical licenses and is the main reason for Tencent shares' headwinds.

Tencent shares peaked in January and are down almost 15% in 2018 because of uncertain gaming revenues.

Investors need to wake up and understand the gaming industry is about to mushroom because of demographics and the migration away from outdoor activity.

Following generations will have an even stronger bias toward technology-based indoor entertainment.

We are entering into the unknown of $4 billion per year video game businesses based on just one title and not one company.

Fortnite made PUBG's $700 million in revenue last year look paltry.

Gamers will soon see the rise of a $5 billion game franchise in 2019 and the sky is the limit.

This industry has growth, growth, and more growth and these single titles could surpass revenue of large semiconductor or hardware companies.

Don't underestimate the power of your child gaming away in your basement, he or she is part and parcel of a wicked tech growth driver about which not many people know.

Unfortunately, Epic Games is not a public company and shares cannot be purchased, but the success of Fortnite means that investors must pay heed to these new developments.

I am highly bullish on the video game sector and a big proponent of Activision (ATVI). A secondary name would be EA Sports (EA), which curates the Madden and FIFA franchises.

ATVI has felt the Fortnite effect in its share price selling off 11% because of investors' nervousness of Fortnite siphoning off ATVI gamers.

This short-term drop is a nice entry point into a solid video gaming company with various successful franchises that have withstood the test of time.

The 200-day moving average has provided ironclad support on the way up, and the Fortnite phenomenon won't last forever.

I would avoid the video game ETF ticker symbol GAMR because it includes one of my bona fide shorts - GameStop (GME).

It's mainly comprised of American, Japanese, and a Korean name but it would be sensible to focus on the companies with the highest quality comprehensive content.

The ETFs recent drop is also due to the strength of Fortnite.

________________________________________________________________________________________________

Quote of the Day

"Companies in every industry need to assume that a software revolution is coming." - said Silicon Valley venture capitalist Marc Andreessen.

Mad Hedge Technology Letter

April 17, 2018

Fiat Lux

Featured Trade:

(WHY THE CLOUD IS WHERE TRADING DREAMS COME TRUE),

(ZS), (ZUO), (SPOT), (DBX), (AMZN), (CSCO), (CRM)

Dreams don't often come true - but they do frequently these days.

Highly disruptive transformative companies on the verge of redefining the status quo give investors a golden chance to get in before the stock goes parabolic.

Traditional business models are all ripe for reinvention.

The first phase of reformulation in big data was inventing the cloud as a business.

Amazon (AMZN) and its Amazon Web Services (AWS) division pioneered this foundational model, and its share price is the obvious ballistic winner.

The second phase of cloud ingenuity is trickling in as we speak in the form of companies that focus on functionality, performance, and maintenance on the cloud platform.

This is a big break away from the pure accumulation side of stashing raw data in servers.

However, derivations of this type of application are limitless.

Swiftly identifying these applied cloud companies is crucial for investors to stay ahead of the game and participate in the next gap up of tech growth.

The markets' reaction to Spotify's (SPOT) and Dropbox's (DBX) hugely successful IPOs was head-turning.

Both companies finished the first day of trading firmly well above their respective, original opening prices -- or for Spotify, the opening reference price.

The pent-up momentum for anything "Cloud" has its merits, and these two shining stars will give other ambitious cloud firms the impetus to go public.

If Spotify and Dropbox laid an egg, momentum would have screeched to a juddering halt, and companies such as Pivotal Software would reanalyze the idea of soon going public.

Now it's a no-brainer proposition.

There are more than 40 more public cloud companies that are valued at more than a $1 billion, and more are in the pipeline.

To understand the full magnitude of the situation, evaluating recent IPO performance is a useful barometer of health in the tech industry.

The first company Zscaler (ZS) is an enterprise company focused on cloud security that closed 106% above its opening price when it went public this past March 16.

It opened up at $16 a share and finished the day at $33.

Zscaler CEO, Jay Chaudhry, audaciously rebuffed two offers leading up to the March 16 IPO. Both offers were more than $2 billion, and both were looking to acquire Zscaler at a discount.

The decision to forego these offers was a prudent move considering (ZS)s current market cap is around $3.3 billion and rising.

One of the companies vying for (ZS) was Cisco Systems (CSCO), which is also in the cloud security business. Cisco is looking to add another appendage to its offerings with the cash hoard it just repatriated from abroad.

Cisco has been willing to dip into its cash hoard by buying San Francisco-based AppDynamics for $3.7 billion in 2017, which specializes in managing the performance of apps across the cloud platform and inside the data center.

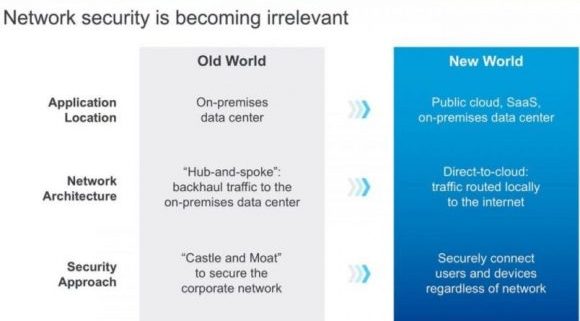

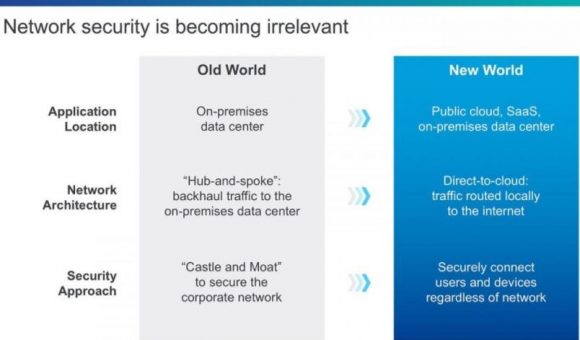

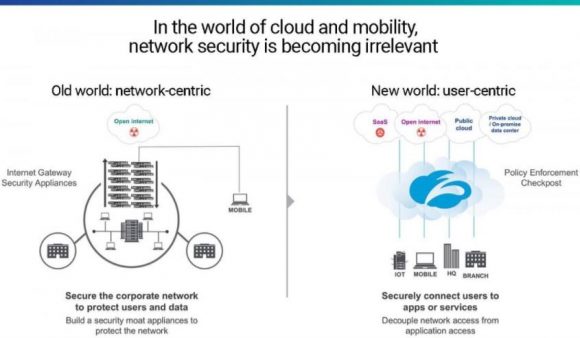

Cloud security is critical for outside companies to feel comfortable implementing universal cloud technology.

Storing sensitive data online in a storage server is also a risk and difficult to migrate back once on the cloud.

Without solid security to protect data, data-heavy companies will hesitate to vault up their data in a public place and could remain old-school with external data locations storing all of a firm's secrets.

However, this traditional approach is not sustainable. There is just too much generated data in 2018.

Cybersecurity has expeditiously evolved because hackers have become greatly sophisticated. Plus, they are getting a lot of free PR.

Data center and in-house applications secured operations by managing access and using an industrial strength firewall.

This was the old security model.

Security became ineffective as companies started using cloud platforms, meaning many users accessed applications outside of corporate networks and on various devices.

The archaic "moat" method to security has died a quick death, as organizations have toiled to ziplock end points that offer hackers premium entry points into the system.

Zscaler combats the danger with a new breed of security. The platform works to control network traffic without crashing or stalling applications.

As cloud migration accelerates, the demand for cloud security will be robust.

Another point of cloud monetization falls within payments.

Tech billing has evolved past the linear models that credit and debit in simplistic fashion.

SaaS (Software as a Service), the hot payment model, has gone ballistic in every segment of the cloud and even has been adopted by legacy companies for legacy products.

Instead of billing once for full ownership, companies offer an annual subscription fee to annually lease the product.

However, reoccurring payments blew up the analog accounting models that couldn't adjust and cannot record this type of revenue stream 10 to 20 years out.

Zuora (ZUO) CEO Tien Tzuo understood the obstacles years ago when he worked for Marc Benioff, CEO of Salesforce (CRM), during the early stages in the 90s.

Cherry-picked after graduating from Stanford's MBA program, he made a great impression at Salesforce and parlayed it into CMO (Chief Marketing Officer) where he built the product management and marketing organization from scratch.

More importantly, Tzuo built Salesforce's original billing system and pioneered the underlying system for SaaS.

It was in his nine years at Salesforce that Tzuo diagnosed what Salesforce and the general industry were lacking in the billing system.

His response was creating a company to seal up these technical deficits.

Other second derivative cloud plays are popping up, focusing on just one smidgeon of the business such as analytics or Red Hat's container management cloud service.

SaaS payment model has become the standard, and legacy accounting programs are too far behind to capture the benefits.

Zuora allows tech companies to seamlessly integrate and automate SaaS billing into their businesses.

Tzuo's last official job at Salesforce was Chief Strategy Officer before handing in his two-week notice. Benioff, his former boss, was impressed by Tzuo's vision, and is one of the seed investors for Zuora.

These smaller niche cloud plays are mouthwateringly attractive to the bigger firms that desire additional optionality and functionality such as MuleSoft, integration software connecting applications, data and devices.

MuleSoft was bought by Salesforce for $6.5 billion to fill a gap in the business. Cloud security is another area in which it is looking to acquire more talent and products.

If you believe SaaS is a payment model here to stay, which it is, then Zuora is a must-buy stock, even after the 42% melt up on the first day of trading.

The stock opened at $14 and finished at $20.

One of the next cloud IPOs of 2018 is DocuSign, a company that provides electronic signature technology on the cloud and is used by 90% of Fortune 500 companies.

The company was worth more than $3 billion in a round of 2015 funding and is worth substantially more today.

These smaller cloud plays valued around $2 billion to $3 billion are a great entry point into the cloud story because of the growth trajectory. They will be worth double or triple their valuation in years to come.

It's a safe bet that Microsoft and Amazon will continue to push the envelope as the No. 1 and No. 2 leaders of the industry. However, these big cloud platforms always are improving by diverting large sums of money for reinvestment.

The easiest way to improve is by buying companies such as Zuora and Zscaler.

In short, cloud companies are in demand although there is a shortage of quality cloud companies.

__________________________________________________________________________________________________

Quote of the Day

"The great thing about fact-based decisions is that they overrule the hierarchy." - said Amazon founder and CEO, Jeff Bezos