Global Market Comments

March 13, 2020

Fiat Lux

Featured Trade:

(MARCH 11 BIWEEKLY STRATEGY WEBINAR Q&A),

(INDU), (SPX), (LVMH), (CCL), (WYNN), (AXP), (JPM), (MSFT), (AAPL), (NVDA)

Global Market Comments

March 13, 2020

Fiat Lux

Featured Trade:

(MARCH 11 BIWEEKLY STRATEGY WEBINAR Q&A),

(INDU), (SPX), (LVMH), (CCL), (WYNN), (AXP), (JPM), (MSFT), (AAPL), (NVDA)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader March 11 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What is the worst-case scenario for this bear market?

A: The average earnings loss for a recession is 13%. Last year, we earned $165 a share for the S&P 500. So, a recession would take us down to $143 a share. Multiply that by the 15.5X hundred-year average earnings multiple, where we are now, and that would take the (SPX) down to 2,200. However, if we get 100 million cases and 5 million deaths, as some scientists are predicting, we could get a 2008 repeat and a 50% crash in the (SPX) to 1,700. With the administration asleep at the switch, that is clearly a possibility. Nice knowing you all.

Q: Do you think we’re still setting up for another roaring 20s?

A: Yes, absolutely. We could not have a roaring 20s unless we got a major selloff and clearing out of old positions like we're getting now. That flushes out all the old capital and positions and paves the way for people to set up brand new positions at really bargain prices. If you missed the 2009 bottom, here's another chance.

Q: Will the fiscal stimulus help defeat the coronavirus?

A: No, viruses are immune to money. They don’t take PayPal or American Express (AXP). The president has been able to buy his way out of all his other problems until now; there’s no way to buy his way out of this one.

Q: Is JP Morgan’s (JPM) Jamie Dimon getting a heart attack related to the financial crisis?

A: Probably, yes. In a normal time, the pressure of a CEO in these big banks is enormous. All of a sudden half of your small customers are looking at bankruptcy—the pressure has to be immense. You've got customers screaming for short term loan facilities, you’ve got risk managers asking for margin extensions. And you certainly don't want to buy the banks here. I think this may be the final selloff with legacy banks, from which they never recover. The banks will disappear and come back online.

Q: What would you do with a $45,000-dollar portfolio right now? I don’t do options.

A: Look at my story on Ten Leaps to Buy at Market Bottom. Use those names—Microsoft (MSFT), Apple (AAPL), NVIDIA (NVDA), etc.—and just buy the stocks. Buy half now and a half in a month. This is a time to dollar cost average. And you’re looking at doubles at a minimum 3 years down the road—at the end of this year if you’re lucky. Once the virus burns out, it will only take a couple months to do that. Then it will be off to the races once again.

Q: Since the 2018 low was never tested, what do you think of 2400/2450?

A: I think that’s great. And you can get a half dozen different analyses that all come up with numbers around 2400, 2500, 2600. That’s where the final low will be—where you get a convergence of multiple support lines and opinions.

Q: Will buybacks come back or are they over for now?

A: They will come back once markets bottom. Companies aren’t stupid; they don’t like buying their own stocks at all-time highs, but they certainly will come in with major amounts of buying when they see their stocks down 20% or 30%. That's certainly what Apple is going to do.

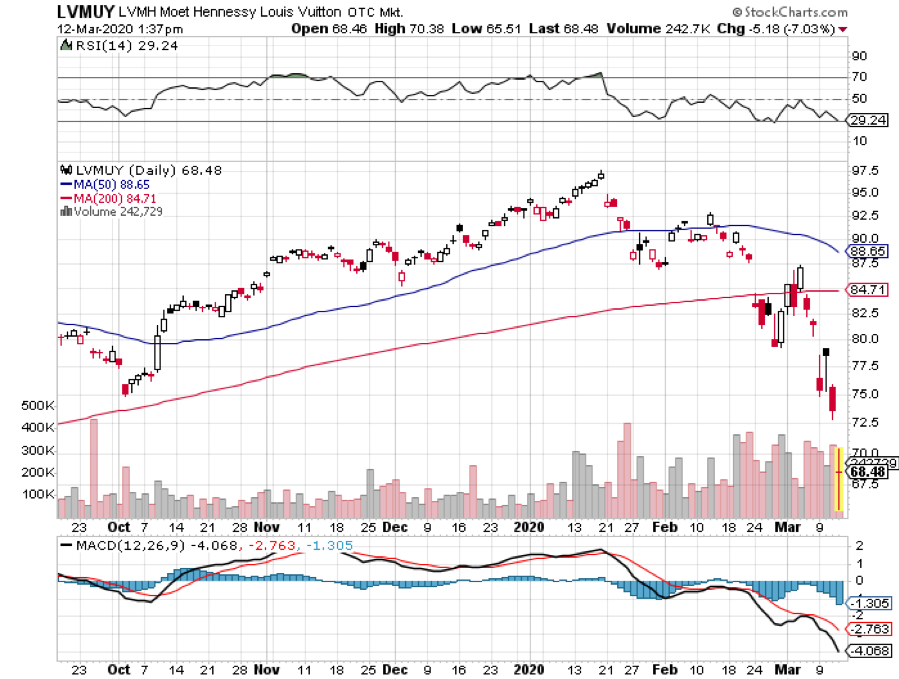

Q: Will luxury retail shares get killed in the current market?

A: Yes, especially stocks like (LVMH), the old Louis Vuitton Moet Hennessey. They’re already down 37% this year. When it becomes clear that we are in an actual recession, these luxury names across the board will get completely abandoned. By the way, I worked with the son of the founder of this company when I was at Morgan Stanley. We called him “Bubbles.”

Q: Are there any similarities to 2008?

A: Yes; it’s worse because the market is dropping much faster than it ever has before. The 52% selloff in 2008 was spread out over the course of 18 months. Here, it’s taken only 14 trading days to see half of the damage done back then. It’s truly unbelievable.

Q: What do you think about gold (GLD)?

A: Even though gold is going up, gold miners (GDX) are doing terribly because they are stocks. They get tarred with the same brush blackening all other stocks. This is exactly what happened during the 2008-2009 crash. Fundamentals go out the window in these kinds of trading conditions, but they always come back.

Q: Is Europe in recession?

A: Absolutely, yes. I saw an interview with the Adidas CEO (ADDYY) this morning on TV and they said sales are off 90% on a month-on-month basis. Their stock is down 49% this year. You can bet that every other consumer company in Europe is suffering similar declines.

Q: What will real estate do in the next 3 months?

A: It's impossible to price real estate so finely because it's so illiquid. However, I expect it to hold up here because of super low interest rates, and then keep rising over the long term. We’re not going to get anything like the crashes we saw in 2008-2009 because all the excess leverage is not in the real estate market now, it’s in the stock market, where we are getting a much-deserved crash. If anything, I’d be buying rental properties here in low cost cities.

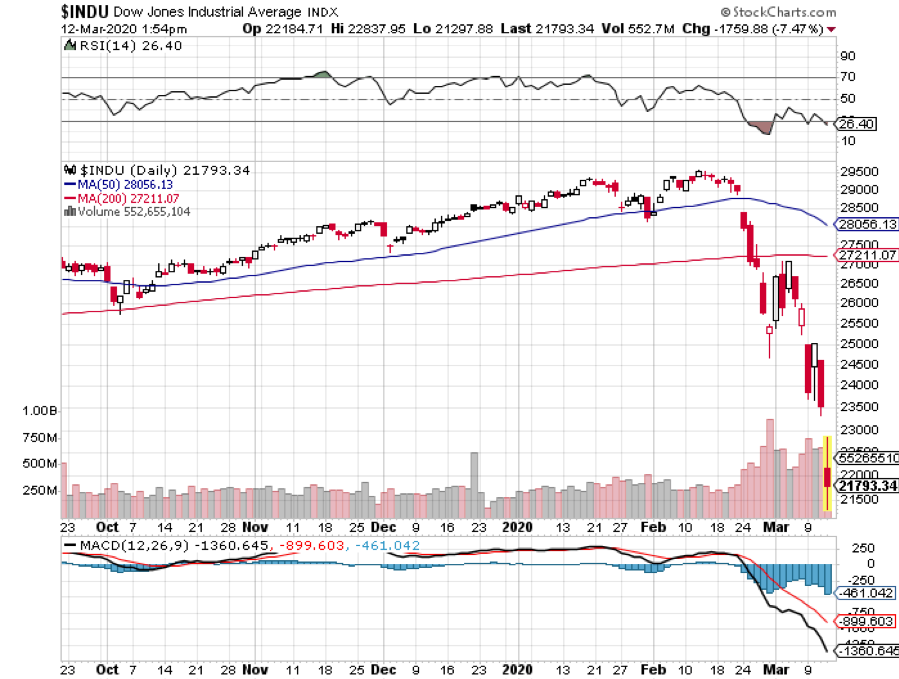

Q: What if the Dow Average (INDU) reaches the 300-day moving average?

A: It’s a nice theory, but technicals are meaningless in the face of panic selling. You don't want to get too fancy looking at these charts. When you have a billion shares to go at market, the 200 or 300 day moving average means nothing.

Good Luck and Good Trading. And stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 9, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SEARCHING FOR A BOTTOM),

(SPX), (VIX), (VXX), (CCL), (UAL), (WYNN)

OK, I’ll give it to you straight.

If the American Coronavirus epidemic stabilizes at current levels of infection, the double bottom in the S&P 500 (SPX) at 2,850 will hold, down 16% from the all-time high two weeks ago.

If it gets worse, it won’t, possibly taking the index down another 8.8% to 2,600, the 2018 low. Not only have we lost the 2019 stock market performance, we may be about to lose 2018 as well.

Of course, the problem is testing kits, which the government has utterly failed to provide in adequate numbers. The president is relying on disease figures provided by Fox News and ignoring those of his own experts at the CDC. And the president told us that the governor of Washington state, the site of the first US Corona hot spot, is a “snake,” and that the outbreak on the Diamond Princess is not his fault.

It’s not the kind of leadership the stock market is looking for at the moment. It amounts to an economic and biological “Pearl Harbor” where the government slept while the disease ran rampant. Until we get the true figures, markets will assume the worst. The real number of untested cases could be in the hundreds of thousands or millions, not the 350 reported. And stock prices will react accordingly.

There is an interesting experiment going on at the Grand Princess 100 miles off the coast of San Francisco right now which will certainly affect your health. Of the 39 showing Corona symptoms, 21 were found to have the disease and 19 of these were crew.

That means ALL of the passengers who took the last ten cruises were exposed, about 30,000 people, 90% of whom are back ashore. The Grand Princess may turn out to be the “Typhoid Mary” of our age.

You can see these fears expressed in the volatility index, which hit a decade high on Friday at $55, although it closed at $42. We live in a world now were all economic data is useless, earnings forecasts are wildly out of date, and technical analysis is ephemeral at best. Airlines, restaurants, and public events are emptying out everywhere and the deleterious effects on the economy will be extreme.

That is kind of hard to trade.

The good news is that this won’t last more than a couple of months. By June, the epidemic will be fading, or we’ll all be dead. All of the buying you see now is of the “look through” kind where investors are picking up once in a decade bargains in the highest quality companies in expectation of ballistic moves upward out the other side of the epidemic.

Enormous fortunes will be made, but at the cost of a few sleepless nights over the next few weeks. The bear market will end when everyone who needs tests get them and we obtain the results.

The Fed cut interest rates by 50 basis points taking the overnight rate down to 1.25%. They may cut again in two weeks. Traders were looking for some kind of global stimulus to head off a global recession. Markets are in “show me” mode and were down 300 prior to the announcement.

Quantitative Easing has become the cure for all problems. So, if it doesn’t work, try, try again? The Fed has now used up all its dry powder levitating the stocks, with the market already at a 1.00% yield for ten-year money. We need a vaccine, not a rate cut. New York schools close on virus fears.

The Beige Book says Corona is a worry, in their minutes from the last Fed meeting six weeks ago, mentioning it 48 times in yesterday’s report. No kidding? Travel and leisure are the hardest hit, and international trade is in free fall. The presidential election is also arising as a risk to the economy. Worst of all, the new James Bond movie has been postponed until November. The report only applies to data collected before February 24.

The next recession just got longer and deeper, as the Fed gives away the last of its dry powder. It’s the first time the central bank was used to fight a virus. It only creates more short selling and volatility opportunities for me down the line. Thanks Jay!

Gold ETF assets hit all-time high, both through capital appreciation and massive customer inflows. Fund values have exceeded the 2012 high, when gold futures reached $1,927. They saw 84 metric tonnes added to inventory in February. The barbarous relic is a great place to hide out for the virus. I expect a new all-time high this year and a possible run to $3,000.

Biotech & healthcare are back! Bernie’s thrashing last week in ten states takes nationalization of health care off the table for good. Biden should sweep most of the remaining states. There’s nothing left for Bernie but Michigan and Florida. Buy Health Care and Biotech on the dip!

The Nonfarm Payroll was up 273,000 in February, much higher than expectations. At least we HAD a good economy. The headline unemployment rate was 3.5%%. As if anyone cares. The only number right now that counts is new Corona infections. This may be the last good report for a while, possibly for years.

Private Payrolls were up 183,000, says the February ADP Report. No Corona virus here. Do you think companies believe this is a short-term ephemeral thing? What if they gave a pandemic and nobody came?

Mortgage Applications were up 26%, week on week, as free money keeps the housing market on fire. Don’t expect too much from the banks though. Mine offered a jumbo loan at 3.6%. Banks are not lining up to sell at the bottom.

The OPEC Meeting was desperate to stabilize prices and they failed utterly. But if they fail to deliver at least 1 million barrels a day in production slowdowns at their Friday Vienna meeting, Texas tea could reach the $30 a barrel handle in days.

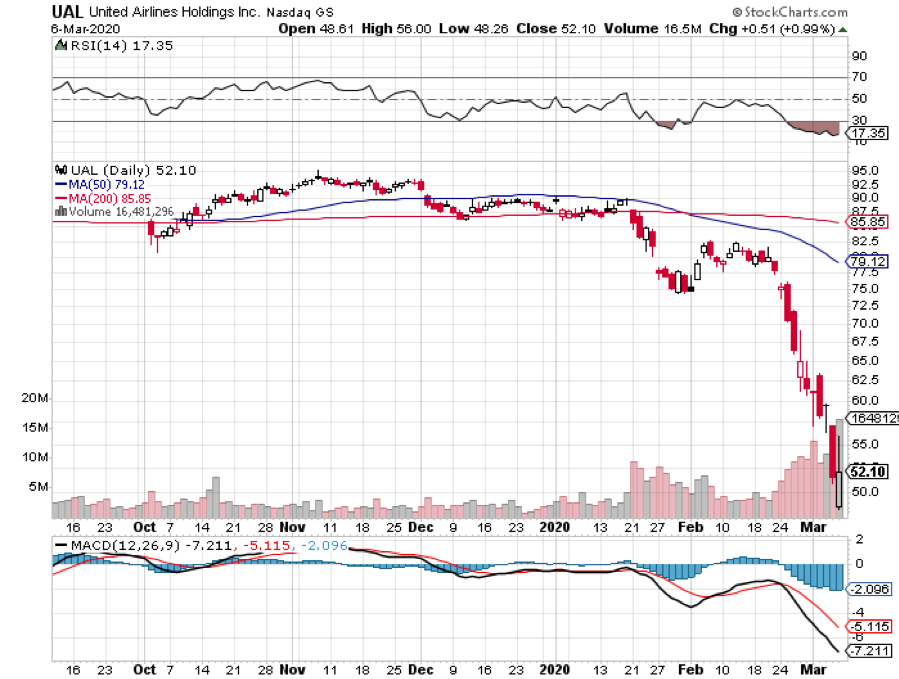

The airline industry will lose $113 billion from the virus, says IATA, the International Air Transport Association. All events everywhere have been cancelled, even my Boy Scout awards dinner for Sunday night and my flight to a wedding in April. Lufthansa just cancelled half of all it flights worldwide. Who knows where the bottom is for this industry? I bet you didn’t know that airline ticket sales account for 8% of all credit card purchases. Keeping my short in United Airlines (UAL).

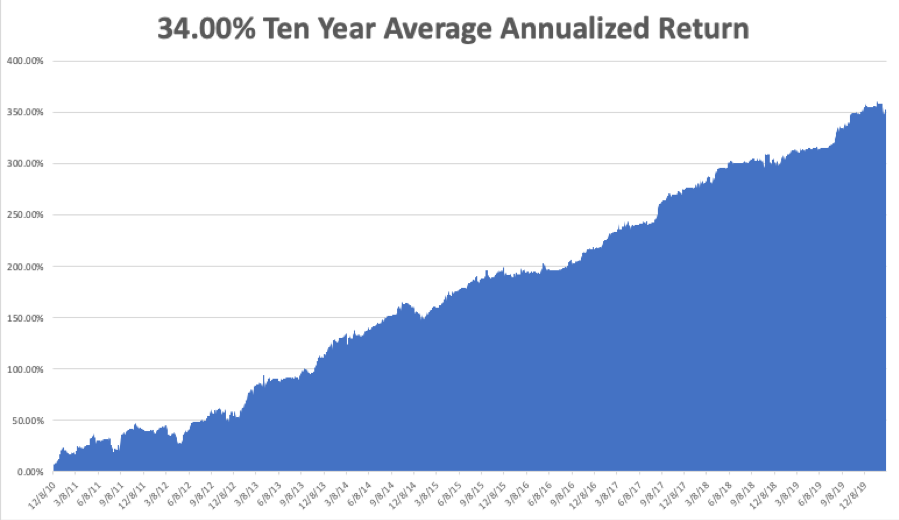

My Global Trading Dispatch performance took a shellacking, pulling back by -4.41% in March, taking my 2020 YTD return down to -7.33%. That compares to a return for the Dow Average of -16% at the Friday low. My trailing one-year return is stable at 48.44%. My ten-year average annualized profit ground back up to +34.00%.

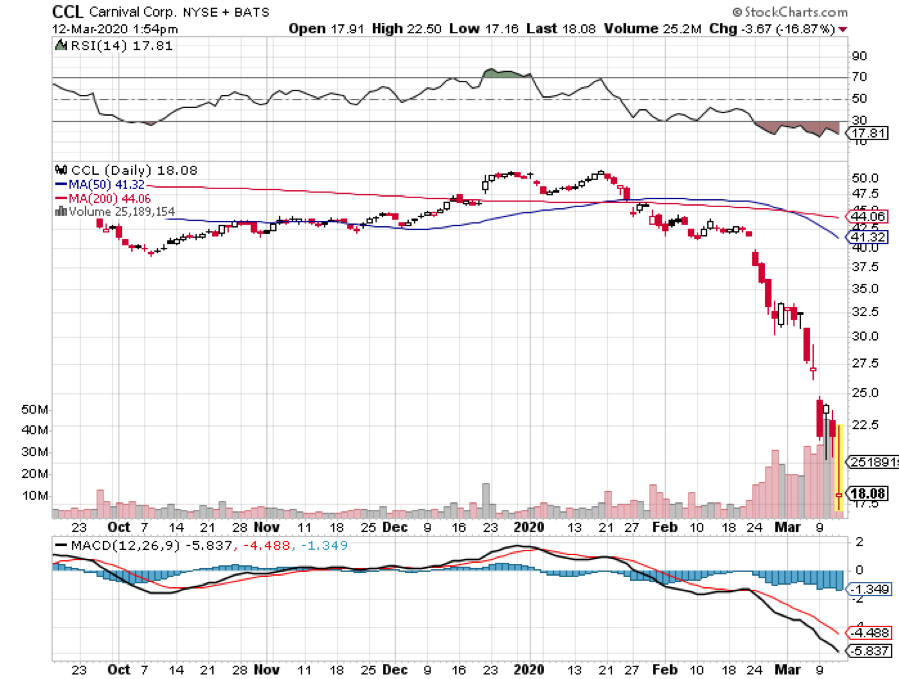

I took my hit of the year on Friday, losing 4.4% on my bond short. A 9-point gap move has never happened in the long history of the bond market. Fortunately, my losses were mitigated by a five-point dip I was able to use to get out, a hedge within my bond position, and three short positions in Corona related-stocks, (CCL), (WYNN), and (UAL), which cratered.

All eyes will be focused on the Coronavirus still, with deaths over 3,000. The weekly economic data are virtually irrelevant now. This is usually the weakest week of the month on the data front.

On Monday, March 9 at 10:00 AM, the Consumer Inflation Expectations is out.

On Tuesday, March 10 at 5:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, March 11, at 7:30 AM, the Core Inflation Rate for February is printed.

On Thursday, March 12 at 8:30 AM, Initial Jobless Claims are announced. Core Producer Price Index for February is also out.

On Friday, March 13 at 9:00 AM, the University of Michigan Consumer Sentiment Index is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll be shopping for a cruise this summer. I am getting offered incredible deals on cruises all over the world. Suddenly, every cruise line in the world is having sales of the century.

Shall it be a Panama Canal cruise for $99, a trip around the Persian Gulf for $199, or a voyage retracing the route of the HMS Bounty across the Pacific for $299. Of course, the downside is that I may be subject to a two-week quarantine on a plague ship on my return.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

![]()

Global Market Comments

March 2, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TRADING THE CORONA MARKET),

(SPX), (INDU), (AAPL), (VIX), (VXX), (AAPL), (MSFT), (AMZN)

It’s time to stockpile food, load up on ammo, and get ready to isolate yourself from the coming Corona Armageddon. If you rely on prescriptions to keep breathing, better lay in a three-month supply. Six months might be better.

At least, that’s what the stock market thinks. That was some week!

Thank goodness it wasn’t as bad as the 1987 crash, when we cratered 20% in a single day, thanks to an obscure risk control strategy called “portfolio insurance” that maximized selling at market bottoms.

In fact, we may have already hit bottom on Friday at Dow 24,681 and S&P 500 (SPX) 2,865.

There are a whole bunch of interesting numbers that converge at the 24,000 Dow Average handle. That is the level where we started the second week of 2019, so we have virtually given up that entire year. If you missed 2019, you get a second chance at the brass ring.

As for the (SPX), as the week’s lows have pulled back exactly to the peaks of twin failed rallies of 2018, right where you would expect major technical support on the long term charts.

And here is something else that is really interesting. If you use the (SPX) price earnings multiple of 16X that prevailed when Trump became president and then add in the 38.62% earnings growth that has occurred since then, you come up with a Dow average of 24,000.

Yes, the market has plunged from a 20X multiple to 16X in a week.

Want more?

If you drop every stock in the market to its 200-day moving average, you get close to a Dow Average of 24,000. I’m talking Apple (AAPL) down to $240, Microsoft (MSFT) cratering to $145. Amazon (AMZN) hit the 200-day on Friday at $1,849.

This means we are well overdue for a countertrend short-covering rally of one-third to two-thirds of the recent loss, or 1,500 to 3,000. That could take the (VIX) back to $20 in a heartbeat. I’ll take any bounce I can get, even the dead cat variety.

What the market has done in a week is backed out the entire multiple expansion that has occurred over the last three years caused by artificially low interest rates and the presidential browbeating of the Federal Reserve.

The fluff is gone.

I have been warning for months that torrid stock market growth against falling corporate earnings growth could only end in tears. And so it did.

Whether the bottom is at 24,000, 23,000, or 22,000, you are now being offered a chance to get off your rear end and pick up at bargain prices the cream of the crop of corporate America, many of which have seen shares drop 20-30% in six trading days.

Stock prices here are discounting a recession that probably won’t happen. That’s what it always does at market bottoms. It’s not a bad time to dollar cost average. Put in a third of your excess cash now, a third in a week, and the last bit in two weeks.

You also want to be selling short the Volatility Index (VIX) big time. With a rare (VIX) level of $50, you can consider this a “free money” trade. Over the last decade, (VIX) has spent only a couple of days close to this level.

Even during the darkest days of the 2008 crash, (VIX) spent only quarter trading between $20 and $50, and one day at $90. That makes one-year short positions incredibly attractive. Get the (VXX) back to last week’s levels and you are looking at 100% to 200% gains on put options very quickly. That’s why I went to a rare double position on Friday.

And then there is the Coronavirus, which I believe is presenting a threat that is wildly exaggerated. If you assume that the Chinese are understating the number of deaths, the true figure is not 3,000 but 30,000. In a population of 1.2 billion that works out to 0.0025%.

Apply that percentage to the US and the potential number of deaths here is a mere 7,500, compared to 50,000 flu deaths a year. And most of those are old and infirm with existing major diseases, like cancer, pneumonia, or extreme obesity.

Thank goodness I’m not old.

Fear, on the other hand, is another issue. Virtually all conferences have been cancelled. A school is closed in Oregon. Most large corporations banned non-essential travel on Friday. Major entertainment areas in San Francisco have become ghost towns. If this continues, we really could scare ourselves into an actual recession, which is what the stock market seemed to be screaming at us last week.

You can forget about the vaccine. It would take a year to find one and another year to mass produce it. They may never find a Corona vaccine. They have been looking for an AIDS vaccine for 40 years without success. So, we are left with no choice but to let nature run its course, which should be 2-3 months. The stock market may fully discount this by the end of this week.

What's disgraceful is the failure of the US government to prepare for a pandemic we knew was coming. I just returned from a two-week trip around Asia and Australia and at every stop my temperature was taken, I was asked to fill out an extensive health questionnaire and was screened for quarantine. When I got back to the US there was nothing. I just glided through the eerily empty immigration.

Most American communities have no Corona tests and have to mail samples to the CDC in Atlanta to get a result. We probably already have thousands of cases here already but don’t know it because there has been no testing. When the stock market learns this, expect more down 1,000-point days.

Where is the bottom? That is the question being asked today by individuals, institutions, and hedge funds around the world. That’s because there are hundreds of billions of dollars waiting on the sidelines left behind by the 2019 melt-up in financial assets. It’s been the worst week since 2008. All eyes are on (SPX) 2,850, the October low and the launching pad for the Fed’s QE4, which ignited stocks on their prolific 16% run. Suddenly, we

have gone from a market you can’t get into to a market you can’t get out of.

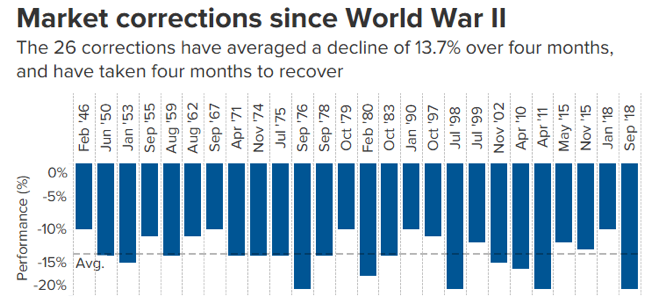

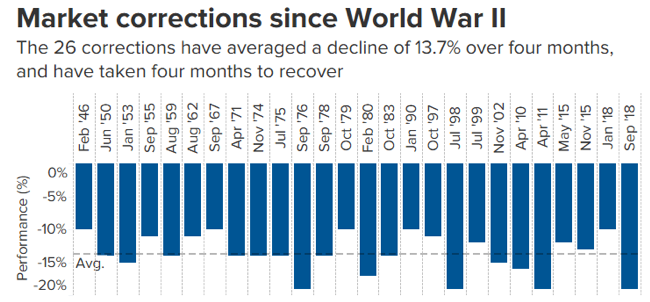

How long is this correction? The post-WWII average is four months, but we have covered so much ground so fast that this one may be quicker. We haven’t seen one since Q4 2018, which was one of the worst.

Corona does have a silver lining. Air pollution in China is the lowest in decades, with coal consumption down 42% from peak levels. It’s already starting to return as Chinese workers go back on the job. Call it the “Looking out the Window” Index.

Consumer Confidence was weak in February, coming in at 130.7, less than expected. Corona is starting to sneak into the numbers. Yes, imminent death never inspired much confidence in me.

International Trade is down 0.4% year on year for the first time since the financial crisis. It’s the bitter fruit of the trade war. The coasts were worst hit where trade happens. Trade is clearly in free fall now, thanks to the virus.

The helicopters are revving their engines, with global central banks launching unprecedented levels of QE to head off a Corona recession. Futures market is now pricing in three more interest rate cuts this year, up from zero two weeks ago. Hong Kong is giving every individual $1,256 to spend to stimulate the local economy. The plunge protection team is here! At the very least, markets are due for a dead cat bounce.

Bob Iger Retired from Walt Disney as CEO and will restrict himself to the fun stuff. The stock is a screaming “BUY” down here, with theme parks closing down from the Corona epidemic. Oops, they’re also in the cruise business!

Will the virus delay the next iPhone, and 5G as well? Like everything else these delays, it depends. Missing market could become the big problem. Missing customers too. I still want to buy (AAPL) down here in the dumps down $90 from its high.

The IEA says the energy outlook is the worst in a decade. Structural oversupply and the largest marginal customers mean that we will be drowning in oil basically forever. Avoid all energy plays like the plague. Don’t get sucked in by high yielding master limited partnerships. Don’t confuse “gone down a lot” with “cheap”.

Why is the market is really going down? It’s not the Coronavirus. It’s the Fed ending of its repo program in April, announced in the Fed minutes on February 19. No QE, no bull market. The virus is just the turbocharger. The Fed just dumped the punch bowl and no one noticed. This may all reverse when we get the next update on the Coronavirus.

A surprise Fed rate cut may be imminent, with a 25-basis point easing coming as early as tomorrow. There is no doubt that the virus is demolishing the global economy.

Investment Spending is Falling off a Cliff, with the Q4 GDP Report showing a 2.3% decline. Consumer spending, the main driver for the US economy, is also weakening as if economic data made any difference right now.

I could see the meltdown coming the previous weekend and was poised to hit the market with short sales and hedges. But when the index opened down 1,000, it was pointless. The best thing I could do was to liquidate my portfolio for modest losses. Two days later, that was looking a stroke of genius. This was the first 1,000 dip in my lifetime that I didn’t buy.

I then piled on what will almost certainly be my most aggressive position of 2020, a double weighting in selling short the Volatility Index at $50. Within 30 minutes of adding my second leg, the (VIX) had plunged to $40, earning back nearly half my losses from the week.

The British SAS motto comes to mind: “Who Dares Wins”.

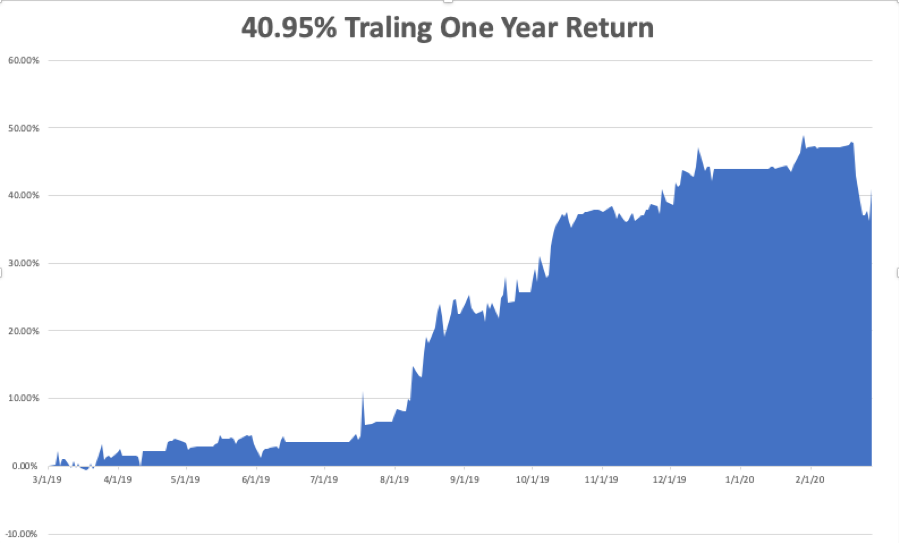

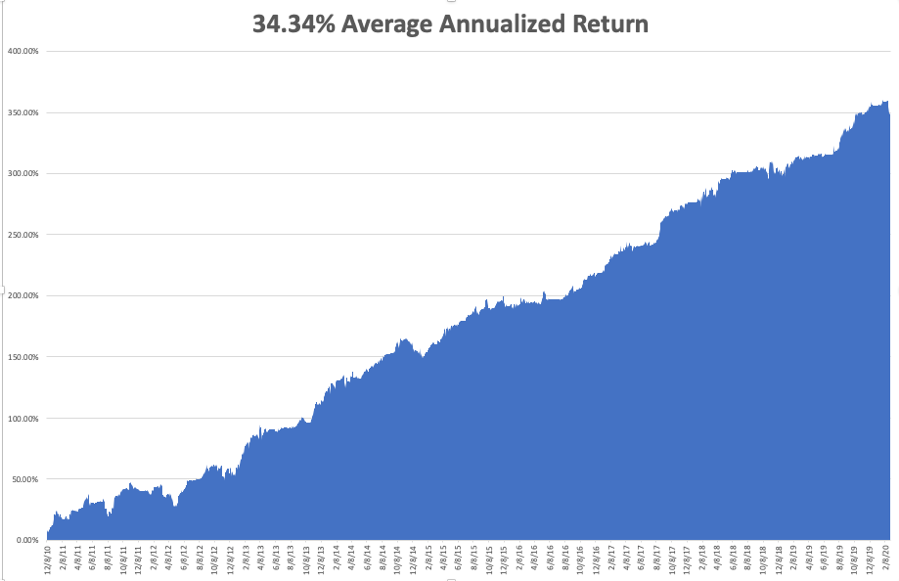

My Global Trading Dispatch performance pulled back by -6.19% in February, taking my 2020 YTD return down to -3.11%. My trailing one-year return is stable at 40.95%. My ten-year average annualized profit ground back up to +34.34%.

With many traders going broke last week or running huge double-digit losses, I’ll take that all day long in the wake of a horrific 4,500 point crash in the Dow Average.

All eyes will be focused on the Coronavirus still, with deaths over 3,000. The weekly economic data are virtually irrelevant now. However, some important housing numbers will be released.

On Monday, March 2 at 10:00 AM, the US Manufacturing PMI for February is out.

On Tuesday, March 3 at 4:00 PM, US Auto Sales for February are released.

On Wednesday, March 4, at 8:15 PM, the ADP Report for private sector employment is announced.

On Thursday, March 5 at 8:30 AM, Weekly Jobless Claims are published.

On Friday, March 6 at 8:30 AM, the February Nonfarm Payroll Report is printed. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, we have just suffered the driest February on record here in California, so I’ll be reorganizing my spring travel plans. Out goes the skiing, in come the beach trips.

Such is life in a warming world.

That’s it after I stop at Costco and load the car with canned food.

John Thomas

CEO & Publisher

Global Market Comments

January 6, 2019

Fiat Lux

2020 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trades:

(SPX), (QQQQ), (XLF), (XLE), (XLY),

(TLT), (TBT), (JNK), (PHB), (HYG), (PCY), (MUB), (HCP)

(FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

(FCX), (VALE), (AMLP), (USO), (UNG),

(GLD), (GDX), (SLV), (ITB), (LEN), (KBH), (PHM)

Global Market Comments

October 18, 2019

Fiat Lux

Featured Trade:

(OCTOBER 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (C), (GM), (IWM), ($RUT), (FB),

(INTC), (AA), (BBY), (M), (RTN), (FCX), GLD)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 16 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: How do you think the S&P 500 (SPX) will behave with the China trade negotiations going on?

A: Nobody really knows; no one has any advantage here and logic or rationality doesn’t seem to apply anymore. It suffices to say it will continue to be up and down, depending on the trade headline of the day. It’s what I call a “close your eyes and trade” market. If it’s down, buy it; if it’s, upsell it.

Q: How long can Trump keep kicking the can down the road?

A: Indefinitely, unless he wants to fold completely. It looks like he was bested in the latest round of negotiations because the Chinese agreed to buy $50 billion worth of food they were going to buy anyway in exchange for a tariff freeze. Of course, you really don’t get a trade deal unless you get a tariff roll back to where they were two years ago.

Q: Did I miss the update on the Citigroup (C) trade?

A: Yes, we came out of Citigroup a week ago for a small profit or a break-even. You should always check our website where we post our trading position sheet every day as a backstop to any trade alerts you’re getting by email. Occasionally emails just go completely missing, swallowed up by the ether. To find it go to www.madhedgefundtrader.com , log in, go to My Account, Global Trading Dispatch, then Current Positions. You can also find my newly updated long-term portfolio here.

Q: How much pain will General Motors (GM) incur from this standoff, and will they ever reach a compromise?

A: Yes, the union somewhat blew it in striking GM when they had incredibly high inventories which the company is desperate to get rid of ahead of a recession. If you wonder where all those great car deals are coming from, that's the reason. All of the car companies want to go into a recession with as little inventory as possible. It's not just GM, it’s everybody with the same problem.

Q: When does the New Daily Position Sheet get posted?

A: About every hour after the close each day. We need time to process our trades, update all the position sheets before getting it posted.

Q: What do you think about Bitcoin?

A: We hate it and don’t want to touch it. It’s unanalyzable, and only the insiders are making money.

Q: Are you predicting a repeat of Fall 2018 going into the end of this year to close at the lows?

A: No, I’m not. A year ago, we were looking at four interest rate increases to come. This year we’re looking at 1 or 2 more interest rate cuts. It’s nowhere near the situation we saw a year ago. The most we’re going to get is a 7% selloff rather than a 20% selloff and if anything, stocks will rise into the yearend then fall.

Q: Why are we trading the Russell 200 (IWM) instead of the ($RUT) Small Cap Index? We pay less commissions to brokers.

A: There's more liquidity in the (IWM). You have to remember that the combined buying power of the trade alert service is about $1 billion. And that’s harder to do with smaller illiquid ETFs like the ($RUT), especially the options.

Q: If this is a “Don’t fight the Fed” rally for investors, where else is there to go but stocks?

A: Nowhere. But it’s happening in the face of an oncoming recession, so it’s not exactly a great investment opportunity, just a trading one. 2009 was a great time not to fight the Fed.

Q: Do you want to buy Facebook (FB) even though there are so many threats of government scrutiny and antitrust breakups?

A: The anti-trust breakups are never going to happen; the government can't even define what Facebook does. There may be more requirements on disclosures, which means nothing because nobody really cares about disclosures—they just click the box and agree to anything. I was actually looking at this as a buy when we had the big selloff at the end of September and instead, I bought four other Tech stocks and (FB) had moved too far when we got around to it. I think there’s upside potential for Facebook, especially if we can move out of this current range.

Q: Would you sell short European banks? It seems like they’re cutting jobs right and left.

A: I always get this question after big market meltdowns. European banks have been underpricing risks for decades and now the chickens are coming home to roost. Some of these things are down 80-90% so it’s too late to sell short. The next financial crisis is going to be in Europe, not here.

Q: Is it time to short Best Buy (BBY) due to the China deal?

A: No, like Macys (M), Best Buy is heavily dependent on imports from China, and the stock has gotten so low it’s hard to short. And the problem for the whole market in general is all the best sectors to short are already destroyed, down 80-90%. There really is nothing left to short, now that all the bad sectors have been going down for nearly two years. There has been a massive bear market in large chunks of the market which no one has really noticed. So, that might be another reason the market is going up—that we’ve run out of things to short.

Q: Do you like Intel (INTC)?

A: Yes, for the long term. Short term it still could face some headwinds from the China negotiations, where they have a huge business.

Q: Would you buy American Airlines (AA) on the return of Boeing 737 MAX to the fleet?

A: Absolutely, yes. The big American buyers of those planes are really suffering from a shortage of planes. A return of the 737 MAX to the assembly line is great news for the entire industry.

Q: Do you like Raytheon (RTN)?

A: No, Trump has been the defense industry’s best friend. If he exits in the picture, defense will get slaughtered—it will be the first on the chopping block under a future democratic administration. And, if you’re doing nothing but retreating from your allies, you don't need weapons anyway.

Q: Will Freeport McMoRan (FCX) benefit from a trade war resolution?

A: Yes, the fact that it isn't moving now is an indication that a trade war resolution has not been reached. (FCX) has huge exposure to traditional metal bashing industries like they still have in China.

Q: Would you go long or short gold (GLD) here?

A: No, I'm waiting for a bigger dip. If you can get in close to the 200-day moving average at $129.50, that would be the sweet spot. Longer term I still like gold and it is a great recession hedge.

Good Luck and Good Trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There is a method to my madness, although I understand that some new subscribers may need some convincing.

Whenever I change my positions, the market makes a major move or reaches a key crossroads, I look to stress test my portfolio by inflicting various extreme scenarios upon it and analyzing the outcome.

This is second nature for most hedge fund managers. In fact, the larger ones will use top of the line mainframes powered by $100 million worth of in-house custom programming to produce a real-time snapshot of their thousands of positions in all imaginable scenarios at all times.

If you want to invest with these guys feel free to do so. They require a $10-$25 million initial slug of capital, a one year lock up, charge a fixed management fee of 2% and a performance bonus of 20% or more.

You have to show minimum liquid assets of $2 million and sign 50 pages of disclosure documents. If you have ever sued a previous manager, forget it. The door slams shut. And, oh yes, the best performing funds are closed and have a ten-year waiting list to get in. Unless you are a major pension fund, they don’t want to hear from you.

Individual investors are not so sophisticated, and it clearly shows in their performance, which usually mirrors the indexes less a large haircut. So, I am going to let you in on my own, vastly simplified, dumbed down, seat of the pants, down and dirty style of risk management, scenario analysis, and stress testing that replicates 95% of the results of my vastly more expensive competitors.

There is no management fee, performance bonus, disclosure document, lock up, or upfront cash requirement. There’s just my token $3,000 a year subscription fee and that’s it. And I’m not choosy. I’ll take anyone whose credit card doesn’t get declined.

To make this even easier, you can perform your own analysis in the excel spreadsheet I post every day in the paid-up members section of Global Trading Dispatch. You can just download it and play around with it whenever you want, constructing your own best case and worst-case scenarios. To make this easy, I have posted this spreadsheet on my website for you to download by clicking here.

Since this is a “for dummies” explanation, I’ll keep this as simple as possible. No offense, we all started out as dummies, even me.

I’ll take Mad Hedge Model Trading Portfolio at the close of October 29, the date that the stock market bottomed and when I ramped up to a very aggressive 75% long with no hedges. This was the day when the Dow Average saw a 1,000 point intraday range, margin clerks were running rampant, and brokers were jumping out of windows.

I projected my portfolio returns in three possible scenarios: (1) The market collapses an additional 5% by the November 16 option expiration, some 15 trading days away, falling from $260 to $247, (2) the S&P 500 (SPY) rises 5% from $260 to $273 by November 16, and (3) the S&P 500 trades in a narrow range and remains around the then current level of $260.

Scenario 1 – The S&P 500 Falls 5%

A 5% loss and an average of a 5% decline in all stocks would take the (SPY) down to $247, well below the February $250 low, and off an astonishing 15.70% in one month. Such a cataclysmic move would have taken our year to date down to +11.03%. The (SPY) $150-$160 and (AMZN) $1,550-$1,600 call spreads would be total losses but are partly offset by maximum gains on all remaining positions, including the S&P 500 (SPY), Salesforce (CRM), and the United States US Treasury Bond Fund (TLT). My Puts on the iPath S&P 500 VIX Short Term Futures ETN (VXX) would become worthless.

However, with real interest rates at zero (3.1% ten-year US Treasury yield minis 3.1% inflation rate), the geopolitical front quiet, and my Mad Hedge Market Timing Index at a 30 year low of only 4, I thought there was less than a 1% chance of this happening.

Scenario 2 – S&P 500 rises 5%

The impact of a 5% rise in the market is easy to calculate. All positions expire at their maximum profit point, taking our model trading portfolio up 37.03% for 2018. It would be a monster home run. I would make back a little bit on the (VXX) but not much because of time decay.

Scenario 3 – S&P 500 Remains Unchanged

Again, we do OK, given the circumstances. The year-to-date stands at a still respectable 22.03%. Only the (AMZN) $1,550-$1,600 call spread is a total loss. The (VXX) puts would become nearly a total loss.

As it turned out, Scenario 2 played out and was the way to go. I stopped out of the losing (AMZN) $1,550-$1,600 call spread two days later for only a 1.73% loss, instead of -12.23% in the worst-case scenario. It was a case of $12.23 worth of risk control that only cost me $1.73. I’ll do that all day long, even though it cost me money. When running hedge funds, you are judged on how you manage your losses, not your gains, which are easy.

I took profit on the rest of my positions when they reached 88%-95% of their maximum potential profits and thus cut my risk to zero during these uncertain times. October finished with a gain of +1.24. By the time I liquidated my last position and went 95% cash, I was up 32.95% so far in 2018, against a Dow average that is up 2% on the year. It was a performance for the ages.

Keep in mind that these are only estimates, not guarantees, nor are they set in stone. Future levels of securities, like index ETFs, are easy to estimate. For other positions, it is more of an educated guess. This analysis is only as good as its assumptions. As we used to say in the computer world, garbage in equals garbage out.

Professionals who may want to take this out a few iterations can make further assumptions about market volatility, options implied volatility or the future course of interest rates. And let’s face it, politics was a major influence this year.

Keep the number of positions small to keep your workload under control. Imagine being Goldman Sachs and doing this for several thousand positions a day across all asset classes.

Once you get the hang of this, you can start projecting the effect on your portfolio of all kinds of outlying events. What if a major world leader is assassinated? Piece of cake. How about another 9/11? No problem. Oil at $150 a barrel? That’s a gimme.

What if there is an Israeli attack on Iranian nuclear facilities? That might take you all of two minutes to figure out. The Federal Reserve launches a surprise QE5 out of the blue? I think you already know the answer.

Now that you know how to make money in the options market, thanks to my Trade Alert service, I am going to teach you how to hang on to it.

There is no point in being clever and executing profitable trades only to lose your profits through some simple, careless mistakes.

So I have posted a training video on Risk Management. Note: you have to be logged in to the www.madhedgefundtrader.com website to view it.

The first goal of risk control is to preserve whatever capital you have. I tell people that I am too old to lose all my money and start over again as a junior trader at Morgan Stanley. Therefore, I am pretty careful when it comes to risk control.

The other goal of risk control is the art of managing your portfolio to make sure it is profitable no matter what happens in the marketplace. Ideally, you want to be a winner whether the market moves up, down, or sideways. I do this on a regular basis.

Remember, we are not trying to beat an index here. Our goal is to make absolute returns, or real dollars, at all times, no matter what the market does. You can’t eat relative performance, nor can you use it to pay your bills.

So the second goal of every portfolio manager is to make it bomb proof. You never know when a flock of black swans is going to come out of nowhere, or another geopolitical shock occurs, causing the market crash.

I’ll also show you how to use my Trade Alert service to squeeze every dollar out of your trading.

So, let’s get on with it!

To watch the Introduction to Risk Management, please click here.