Going against the market consensus has been working pretty well lately.

When the world prayed for a Santa Claus rally, I piled on the shorts. When traders expected a New Year January crash, I filled my boots with longs.

That’s how you earn an eye-popping 19.83% profit in a mere nine trading says, or 2.20% a day.

The other day, someone asked me how it is possible to get mind-blowing results like these. It’s very simple. Get insanely aggressive when everyone else is terrified, which I did on January 3. I also knew that with the Volatility Index (VIX) falling to $18, pickings would quickly get extremely thin. It was make money now, or never.

To quote my favorite market strategist, Yankees manager Yogi Berra, “No one goes to that restaurant anymore because it’s too crowded.”

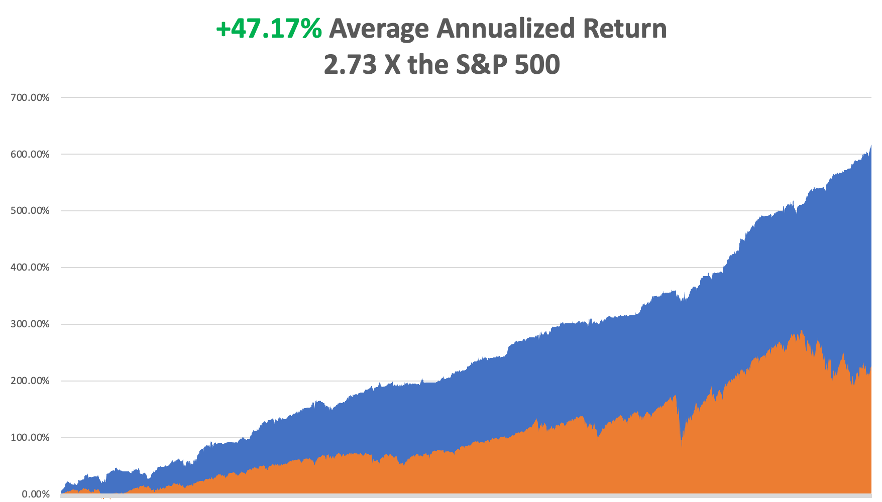

My performance in January has so far tacked on a welcome +19.83%. Therefore, my 2023 year-to-date performance is also +19.83%, a spectacular new high. The S&P 500 (SPY) is up +3.78% so far in 2023.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 15 years ago. My trailing one-year return maintains a sky-high +103.30%.

That brings my 15-year total return to +617.03%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +47.17%, easily the highest in the industry.

I took profits in my February bonds last week (TLT), taking advantage of a $5 pop in the market. All my remaining positions are profitable, including longs in (GOLD), (WPM), (TSLA), (BRK/B), and (TLT), with 30% in cash for a 10% net long position.

Since my New Year forecasts have worked out so well, I will repeat the high points just in case you were out playing golf or bailing out from a flood when they were published.

Buy Falling Interest Rate Plays, as I expect the yield on the ten-year US Treasury yield to fall from 3.50% to 2.50% by yearend. That means Hoovering up any kind of bond, like (TLT), (MUB), (JNK), and (HYG). Falling interest rates also shine a great spotlight on precious metals like (GLD), (SLV), (GOLD), and (WPM).

The US Dollar Will Continue to Fall. Commodities love this scenario, including (FCX), (BHP), and emerging markets (EEM).

Inflation Will Decline All Year and should go below 4% by the end of 2023. In fact, we have had real deflation for the past six months. Financials do well here, like (MS), (GS), (JPM), (BAC), (C), and (BRK/B).

Which creates another headache for you, if not an opportunity. We may have a situation where the main indexes, (SPY), (QQQ), and (IWM) go nowhere, while individual stocks and sectors skyrocket. That creates a chance to outperform benchmarks…and everyone else. There has been a lot of discussion among traders lately about the collapse of the Volatility Index ($VIX) to $18, a two-year low and what it means.

They are distressed because a ($VIX) this low greatly shrinks the availability of low risk/high return trading opportunities. A ($VIX) this low is basically shouting at you to “STAY AWAY!”

Does it mean that an explosion of volatility is following? Or are markets going to be exceptionally boring for the next six months?

Beats me. I’ll wait for the market to tell me, as I always do.

Consumer Price Index Falls 0.1% in December, continuing a trend that started in June. Stocks popped and bonds rallied. YOY inflation has fallen to 6.5%. “RISK ON” continues. Now we have to wait another month to get a new inflation number. The economy has now seen de facto deflation for six months. Gas prices led the decline, now 9.4%. We might get away with only a 0.25% interest rate hike at the February 1 Fed meeting.

Bond Default Risk Rises, as well as a government shutdown, as radicals gain control of the House. This is the group that lost the most seats in the November election. Bonds are the only asset class not performing today, and paper with summer maturities is trading at deep discounts. It certainly casts a shadow over my 50% long bond position. However, I don’t expect it to last more than a month and my longest bond maturity is in February.

The US Consumer is in Good Shape, according to JP Morgan’s Jamie Diamond. Spending is now 10% greater than pre covid, and balance sheets are healthy. No sign of an impending deep recession here.

Boeing Deliveries Soar from 340 to 480 in 2022, and 479 new orders. A sudden aircraft shortage couldn’t have happened to a nicer bunch of people. The 737 MAX has shaken off all its design problems after two crashes four years ago. Cost-cutting here can be fatal. Europe’s Airbus is still tops, with 663 deliveries last year. Don’t chase the stock up here, up 79% from the October lows, but buy (BA) on dips.

Small Business Optimism Hits Six-Month Low to from 91.9 to 89.8, adding to the onslaught of negative sentiment indicators, so says the National Federation of Independent Business (NFIB).

Copper Prices Set to Soar Further with the post-Covid reopening of China, according to research firm Alliance Bernstein. After a three-year shutdown, there is massive pent-up demand. Copper prices are at seven-month highs. Keep buying (FCX) on dips.

Australian Metals Exports Soar, as the new supercycle in commodities gains steam. Shipments topped $9 billion in November, 20% higher than the most optimistic forecasts. Keep buying copper (FCX), aluminium (AA), iron ore (BHP), gold (GLD) and silver (SLV) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, January 16, markets are closed for Martin Luther King Day.

On Tuesday, January 17 at 8:30 AM EST, the New York Empire State Manufacturing Index is out

On Wednesday, January 18 at 11:00 AM, the Producer Price Index is announced, giving us another inflation read.

On Thursday, January 19 at 8:30 AM, the Weekly Jobless Claims are announced. US Housing Starts and Building Permits are printed.

On Friday, January 20 at 7:00 AM, the Existing Home Sales are disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, the University of Southern California has a student jobs board that is positively legendary. It is where the actor John Wayne picked up a gig working as a stagehand for John Ford which eventually made him a movie star.

As a beneficiary of a federal work/study program in 1970, I was entitled to pick any job I wanted for the princely sum of $1.00 an hour, then the minimum wage. I noticed that the Biology Department was looking for a lab assistant to identify and sort Arctic plankton.

I thought, “What the heck is Arctic plankton?” I decided to apply to find out.

I was hired by a Japanese woman professor whose name I long ago forgot. She had figured out that Russians were far ahead of the US in Arctic plankton research, thus creating a “plankton gap.” “Gaps” were a big deal during the Cold War, so that made her a layup to obtain a generous grant from the Defense Department to close the “plankton gap.”

It turns out that I was the only one who applied for the job, as postwar anti-Japanese sentiment then was still high on the West Coast. I was given my own lab bench and a microscope and told to get to work.

It turns out that there is a vast ecosystem of plankton under 20 feet of ice in the Arctic consisting of thousands of animal and plant varieties. The whole system is powered by sunlight that filters through the ice. The thinner the ice, such as at the edge of the Arctic ice sheet, the more plankton. In no time, I became adept at identifying copepods, euphasia, and calanus hyperboreaus, which all feed on diatoms.

We discovered that there was enough plankton in the Arctic to feed the entire human race if a food shortage ever arose, then a major concern. There was plenty of plant material and protein there. Just add a little flavoring and you had an endless food supply.

The high point of the job came when my professor traveled to the North Pole, the first woman ever to do so. She was a guest of the US Navy, which was overseeing the collection hole in the ice. We were thinking the hole might be a foot wide. When she got there, she discovered it was in fact 50 feet wide. I thought this might be to keep it from freezing over but thought nothing of it.

My freshman year passed. The following year, the USC jobs board delivered up a far more interesting job, picking up dead bodies for the Los Angeles Counter Coroner, Thomas Noguchi, the “Coroner to the Stars.” This was not long after Charles Manson was locked up, and his bodies were everywhere. The pay was better too, and I got to know the LA freeway system like the back of my hand.

It wasn’t until years later when I had obtained a high-security clearance from the Defense Department that I learned of the true military interest in plankton by both the US and the Soviet Union.

It turns out that the hole was not really for collecting plankton. Plankton was just the cover. It was there so a US submarine could surface, fire nuclear missiles at the Soviet Union, then submarine again under the protection of the ice.

So, not only have you been reading the work of a stock market wizard these many years, you have also been in touch with one of the world’s leading experts on Artic plankton.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/john-thomas-peleliu-island-1975.png434628Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-17 09:02:252023-01-17 14:36:18The Market Outlook for the Week Ahead, or Going Against the Consensus

Passive investing, or piling all your money in major stock indexes like the S&P 500 (SPX) or the Dow Average (INDU), just got killed off by the bear market.

The days when you could just index and then go play golf for the rest of the day are gone for good.

Rest in Peace.

On a good day, your investments reliably underperformed the indexes, less management fees and hidden expenses. Even indexers have to work to earn a living.

That was fine as long as the indexes went up like clockwork, as they did almost every year for the last 12 years. Enter Covid-19. Many individual investors will instantly have heart attacks when they opened their annual pension fund and 401k statements.

I have to admit that I was getting pretty sick of index investing. People like me would slave over their computers all day long in some years barely beating the returns of those who never lifted a finger. That is now ancient history.

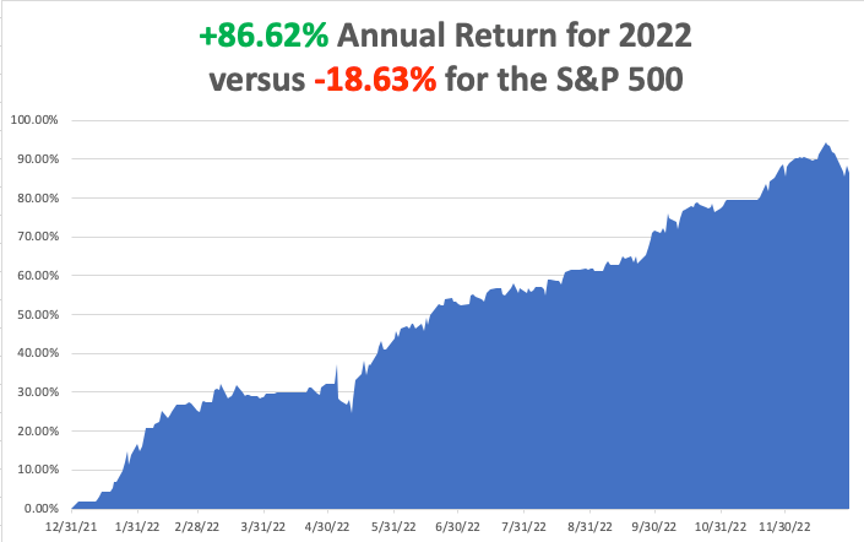

Look no further than my own performance year to date. Last year, I managed to clock an 86.62% gain, compared to a pitiful 18% for the Dow Average. 2023 could be another great year for me.

How will your index fund perform when US pandemic deaths hit over 1 million as reported by Johns Hopkins University?

The global pandemic is creating a brave new world on countless fronts, and management of your retirement funds is no different. Passive investing will be replaced by active investment whereby educated individuals pick winning stocks and judiciously avoid the awful ones.

The bad news is that you will have to work harder to oversee your nest egg. The good news is that you will make a lot more money. The difference between passive and active investment is now greater than at any time in history, and that chasm is set to increase.

While the bull market allowed all stocks to go up equally, the new one is totally different. There is about to be a huge differentiation between winners and losers like never seen before. The difference between the wheat and the chaff will be enormous.

Those who figure out the new game early will prosper mightily. Those who don’t will crash and burn.

I have been fighting a daily battle with some of my own subscribers, as they are arguing that the biggest gains will simply be made from buying the biggest losers.

I’m not buying that logic for a nanosecond. Many of the worst performers are never coming back to their former glory, such as airlines, cruise lines, hotels, movie theaters, restaurant chains, and casinos. Sure, they may have a brief dead cat bounce off the bottom for a trade. But the long-term outlook for these ill-fated industries is grim at best.

No, the future lies in buying Teslas and Rolls Royces at KIA prices. Come in today and these distressed levels and you may earn as much as 15% a year for the next decade.

You know the companies I am talking about, the ones I have been covering at great length in Global Trading Dispatch, The Mad Hedge Technology Letter, and the Mad Hedge Biotech & Healthcare Letter. If you are missing any of these publications, please feel free to pick them up at our store. Please note that all our prices are going up substantially soon.

This is going to lead to a very interesting future. Those who continue to index are looking at years of subpar performance. Those who go active and do it the right way are going to be looking pretty.

It’s going to be a fun decade. The Roaring Twenties have only just begun.

Good Luck and Good Trading,

John Thomas

Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/03/john-thomas-horse.png530404Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-05 10:02:042023-01-05 12:04:23The Death of Passive Investing

Below please find subscribers’ Q&A for the December 14 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Is it time to short the S&P 500 (SPY), or go into cash?

A: I vote for cash. Number 1. We’ve just had a tremendous run in the market. The 200-day moving average at $405 is proving to be massive resistance, and you could get a bunch of profit-taking in January on all the positions people bought up in October. They’ve made a ton of money on that, and they may be deferring to profit-taking, hoping for the Santa Clause rally to continue and to take advantage of all that time decay over the holidays—so, high risk. Risk-reward right now is terrible, so I don’t want to do anything. I’m 100% cash, and I’ll stay that way until the New Year unless something exceptional happens in the markets—you never know what might happen. And I watch markets 24/7, vacation or not because it's in my blood.

Q: What about Financials?

A: Wait until the next dip and then go for call spreads which deliver max profits in sideways markets. JP Morgan (JPM), Bank of America (BAC), Citigroup (C) and you might take a look at Wells Fargo (WFC) next time around, but they always seem to be getting into trouble.

Q: What do we do about interest rates here?

A: Look for the 10-year Treasury bond (TLT) yield to drop to about 2.50% in 2023, about the first half of 2023—maybe by June or so. We did just have a round of profit-taking, but we’re adding on dips.

Q: What do you think about the US sending patriot batteries to Ukraine?

A: The problem is the MIM-104 Patriot SAM system is kind of old—about 41 years old—and it’s been outrun by the new technologies developed by the Ukraine war. Also, 1,000 drones at $1,000 each would be cheaper than 1 patriot missile for $4 million. Sending swarms of hundreds of super cheap drone bombs to attack targets has only been developed over the past six months and you only need one to get through to destroy the target for which the patriot would be useless. Patriot is really designed to shoot down incoming Russian intercontinental ballistic missiles with nuclear warheads with one hour of notice and highly predictable trajectories. We used them a lot in the Gulf War in 1991, and we gave many to Israel which used them to great effect when defending big cities. But they were only firing against slow WWII German-style V2 rockets which Saddam Hussein literally copied off of Wikipedia. If you want to see how effective the new drone strategy is, watch competitive drone racing (https://www.youtube.com/watch?v=HNRiMgNnuVE ), or robot wars (http://www.robotwars.tv ), or any of these other online programs where you have drones controlled by humans doing exactly what I’m talking about. Also, 1,000 drones at $1,000 each would be cheaper than 1 patriot missile for $ million.

Q: What’s your Rivian (RIVN) target by the January options expiration?

A: I have no idea, but Elon Musk has had the impact of destroying not only Tesla but the entire EV sector, so Rivian is a great company clearly being dragged down by Tesla. But also, a joint venture to make trucks in Europe was also put on hold with Mercedes. And of course, nobody wants to spend money ahead of a recession. Buy (RIVN) two-year LEAPS.

Q: Why is the US buying Natural Gas (UNG) in Massachusetts from Russia when we have so much already in this country?

A: The US does not have a national natural gas pipeline system, so you can have excesses in Texas where it’s produced meet shortages in Massachusetts where it’s consumed. Somebody found a loophole to get Russian gas into the US using offshore shell companies which I’m sure will be closed instantly once that delivery is made. Suffice it to say that the sanctions on Russia are tightening, are having a deeper effect and forcing them to pull out of Ukraine sooner than we expect. That may be the pivotal black swan of 2023—that Russia gives up on Ukraine, which would be a huge positive for all markets.

Q: When will we be using nuclear fusion?

A: I have been following nuclear fusion for 50 years, ever since I worked at the Nuclear Test Site in Nevada—it’s long been the holy grail for alternative energy. I talked to the teams every once in a while, since they live next door. The positive developments we saw in England last week are a big breakthrough, but you’re looking for at least 30 years until we get functional economic nuclear fusion power plants. So, we only have to stay alive for 30 more years (and keep climate change from killing us all off in the meantime) before we get carbon-free energy in an unlimited supply. Having said that, from the time they developed a functional commercial nuclear powerplant using Uranium in 1957 from the initial use of the atomic bomb in 1945, was only 12 years and that had to be equally as daunting. So, I may be wrong, and there may be other breakthroughs coming our way, but you don’t control 150 million degrees easily—that's what’s necessary with fusion. The amounts of power input required are also staggering, like all the power that San Francisco uses in a day, just to produce marginal bits of electricity. And the deuterium fuel needed (H2, or heavy hydrogen) in large quantities would not exactly be cheap either. But in 30 years every city should get its own min sun to provide unlimited electricity. So there’s your science lecture of the day, from a long-term fusion follower. For a more detailed explanation please click here at https://www.energy.gov/science/doe-explainsnuclear-fusion-reactions

Q: Is Tesla (TSLA) a buy here?

A: Absolutely, for the long term, but I would not be amazed to see $110 print first. Number one, there’s a major short play going on here too building huge amounts of buying power, and Number two, we’re flushing out a lot of long-term profit takers for tax loss selling as we go with the year-end to offset 2022 losses in other stocks. Buying Tesla at 27X earnings multiple, and next year’s 19X multiple when it was at 100X just a year ago is kind of unbelievable. An onslaught of new Tesla positives will hit the market in 2023. The new Cybertruck comes out and there is a two-year waiting list out the gate and deposits in hand for 100,000 vehicles. The company is generating such enormous cash flows that it is like to carry out $10 billion in share buybacks, especially with the price this low. There are no real competitors on the horizon, except for a handful with minimal production at big losses outside of China.

Q: Is the demise of FTX the end of crypto?

A: I would say yes, which is why we stopped producing our Bitcoin newsletter. It could take 30 years for this thing to recover. It’s another Japanese stock market type situation, where it literally takes three decades to recover, and by then new technologies will far surpass it. The confidence in anything crypto has been totally destroyed by the FTX scandal—it’s the final nail in the coffin. And there are better things to do—I’d rather be buying NVIDIA (NVDA) or Tesla (TSLA) than crypto. There are too many great trades after a bear market.

Q: Is Blackrock (BLK) in trouble?

A: Not in a million years, and I’d be buying it on any dip. They’re an incredibly well-run company, buy on dips. They have one gated REIT which thei disclosed well in advance that is drawing all the adverse publicity. In bear markets, traders always believe the worst.

Q: Why would you not sell Nvidia (NVDA)?

A: Well, we dumped all our tech stocks in January, so we did sell there. But I try not to go against long-term trends, and the long-term trends for Nvidia is a double or triple from here since they are the 8-pound gorilla in the high-end chip business.

Q: Why is cybersecurity (PANW), (CRWD) so unloved in this environment?

A: They are over-owned. When everybody owns something, you can have the greatest story in the world and it doesn’t go up because you need new buyers for things to go up, and the Cybersecurity story is pretty well known. That’s why it won’t go down either, people are not selling because they believe in the long-term story of cyber security—and quite correctly so, and I might add at the bottom of the ranges.

Q: Isn’t Warren Buffet’s age a worry regarding Berkshire Hathaway (BRKB)?

A: No, the replacement management team that has been there for 20 years, is generating great results. Warren is basically just the front-end mouthpiece for Berkshire Hathaway, just like I’m the front-end mouthpiece for the Mad Hedge Fund Trader and isn't really involved in day-to-day decisions. That’s how Berkshire was able to step up its technology exposure during the teens. When he goes, the stock might drop 5% from algorithm and uninformed sales, but no more.

Q: What do you think of the iShares 20 Plus Year Treasury Bond ETF (TLT) versus the ProShares UltraShort 20+ Year Treasury (TBT)?

A: Avoid the (TBT) because it’s a 2x—you have extra management fees, and extra dealing costs—it’s better just to buy (TLT) on a 2x margin than it is shorting the (TBT) which is already a 2x. I’m looking for $120-$130 in the (TLT) by mid-2023, which is also a great LEAPS candidate.

Q: Is the market rethinking technology multiples here which are IBIDTA based?

A: It has already rethought the technology multiples because they have collapsed. They have dropped, in Tesla’s case 100X to 19X, which looks like a pretty serious piece of rethinking to me, so yes absolutely. Where is the final level? My theory always has been that when tech falls to a market multiple, which for the S&P 500 right now is 18.5X, that is your final bottom in tech multiples which means they may have more to go down. And what might really happen is you may have a situation where the market multiples start to rise again and get back up to the 20’s, tech falls, and they meet somewhere in the low 20s. That’s your final bottom for tech, and then you buy it to own for the next 10 years.

Q: When do you think the Fed will start lowering rates?

A: It will be a second-half affair. First of all, they have to raise rates by 50 basis points on Wednesday, then raise them again in February by 50 and again in March by 25, and then leave them alone for 3 months. Then we will have a recession, or dramatically lower inflation by then, or both. And then they’ll have room to start cutting, which sets a calendar of about June where they start several 75 basis point CUTS. Remember, markets discount things 6-9 months in advance, which is why we had that $20 rally in the (TLT) that started in February. There’s your calendar. So far, it’s working.

Q: Will you give a buy signal on Tesla (TSLA)?

A: More like a Hail Mary on Tesla, hoping that it’s the bottom. When you get these capitulation selloffs, which is what we’re getting on Tesla, there is absolutely no way of predicting where the final number is, because you’re dealing with human emotions here, which are totally unpredictable and are panicking. I’d rather wait, give the first 10% of the move to the next guy, and then play the new trend from there. But I think Tesla could be one of the top performers of 2023. Especially if you get down to like $110 or so, something unbelievable—you know, get Tesla to market multiple, that means it’s got to drop another $30 essentially, and in this environment, it could do that. It could keep going down every day for the rest of this year because a lot of these big reversals tend to happen at year ends. When you get the last Tesla bull out of there, that’s when it goes up. After that, it’s all short covering.

Q: Do you think it will be 50 or 75 basis points?

A: It’s a coin toss for whether it’s 50 or 75. Knowing Jay Powell as I do, I’d go for 50, but with harsh talk. I think he wants to shock us, wants to kill off this stock market rally, wants to kill off any hope you can get one more price rise through the system before we hit a recession. A 50 basis points would be a real shocker and, by the way, would also give us easily a 1000-point selloff, which we could then use to buy into for the new year.

Q: Could Tesla reach $600?

A: Yes, I think it could. Remember, the fundamental story for Tesla is still on track. They are still growing at a 40% rate, while the rest of Detroit is going nowhere. All of their leads are overwhelming, and the really telling aspect for the future of Tesla is that Apple gave up on its autonomous driving program. Every other car company in the world is going to come to the same decision, except for maybe Google. So yes, the bull case is absolutely there, you just have to wait for the current capitulation to flush out, and then it becomes a buy for years.

Q: Does the adoption of a digital currency impact the economy?

A: No, I think anything digital money is on hold for the foreseeable future as the FTX disaster unfolds.

Q: Do you like Salesforce (CRM)?

A: Yes, long-term. It’s also in a capitulation “catch a falling knife” stage. Wait for that to finish—better to buy it on the way up than on the way down is all I can say.

Q: Will there be any restrictions on copper mining (FCX)?

A: Not that I can think of—we’re looking at an enormous shortage of copper going forward and a future copper shock. Most of this is produced in emerging markets that have no environmental restrictions, which is why it happens there, like Chile. So yes, looking for new copper sources will be one of the big plays of this decade.

Q: Do you think the market will bottom in 2023?

A: Yes, if it hasn’t already.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Peleliu in 1978 with a Japanese 8 Inch Gun

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/john-thomas-peleliu-island-1975.png434628Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-16 09:02:322022-12-16 14:32:18December 14 Biweekly Strategy Webinar Q&A

Last week, I spoke about the “smart” market and the “dumb” market.

Looking across asset class behavior over the last couple of years, it’s become evident, there is another major driver.

Liquidity.

Hedge fund legend George Soros was an early investor in my hedge fund because he was looking for a pure Japan play. But I learned a lot more from him than he from me.

No shocker here: it’s all about the money.

Follow the flow of funds and you will always know where to invest. If you see a sustainable flow of money into equities, you want to own stocks. The same is true with bonds.

There is a corollary to this truism.

The simpler an idea, the more people will buy it. One can think of many one or two-word easy-to-understand investment themes that eventually led to bubbles: the Nifty Fifty, the Dotcom Boom, Fintech, Crypto Currencies, and oil companies.

Spot the new trend, get in early, and you make a fortune (like me and Soros). Join in the middle, and you do OK. Join the party at the end and it always ends in tears, as those who joined crypto a year ago learned at great expense.

If I could pass on a third Soros lesson to you, it would be this. Anything worth doing is worth doing big. This is why you have seen me frequently with a triple position in the bond market, or the double short I put on with oil companies two weeks ago, clearly just ahead of a meltdown.

Which brings me back to liquidity.

There are only two kinds of markets: liquidity in and liquidity out. Liquidity was obviously pouring into markets from 2009. This is why everything went up, including both stocks and bonds. That liquidity ended on January 4, 2022. Since then, liquidity has been pouring out at a torrential rate and everything has been going down.

So, what happened on October 14, 2022?

The hot money, hedge funds, and you and I started betting that a new liquidity in cycle will begin in 2023 and continue for five, or even ten years. This is why we have made so much money in the past two months.

Notice that liquidity out cycles are very short when compared with liquidity in cycles, one to two years versus five to ten years. That’s because populations expand creating more customers, technology advances creating more products and services, and economies get bigger.

When I first started investing in stocks, the U.S. population was only 189 million, the GDP was $637 billion, and if you wanted a computer, you had to buy an IBM 7090 for $3 million. Notice the difference with these figures today: $25 trillion for GDP, a population of 335 million, and $99 for a low-end Acer laptop, which has exponentially more computer power than the old IBM 7090.

What did the stock market do during this time? The Dow Average rocketed by 54 times, or 5,400%. And you wonder why I am so long term bullish on stocks. The people who are arguing that we will have a decade of stock market returns are out of their minds.

Which reminds me of an anecdote from my Morgan Stanley days, in my ancient, almost primordial past. In September 1982, I met with the Head of Investments at JP Morgan Bank (JPM), Mr. Carl Van Horn. I went there to convince him that we were on the eve of a major long term bull market and that he should be buying stocks, preferably from Morgan Stanley.

Every few minutes he said, “Excuse me” and left the room to return shortly. Years later, he confided in me that whenever he left, he placed an order to buy $100 million worth of stock for the bank’s many funds every time I made a point. That very day proved to be the end of a decade-long bear market and the beginning of an 18-year bull market that delivered a 20-fold increase in share prices.

But there is a simpler explanation. Liquidity in markets are a heck of a lot more fun than liquidity out ones, where your primary challenge is how to spend your newfound wealth.

I vote for the simpler explanation.

Yes, this is how markets work.

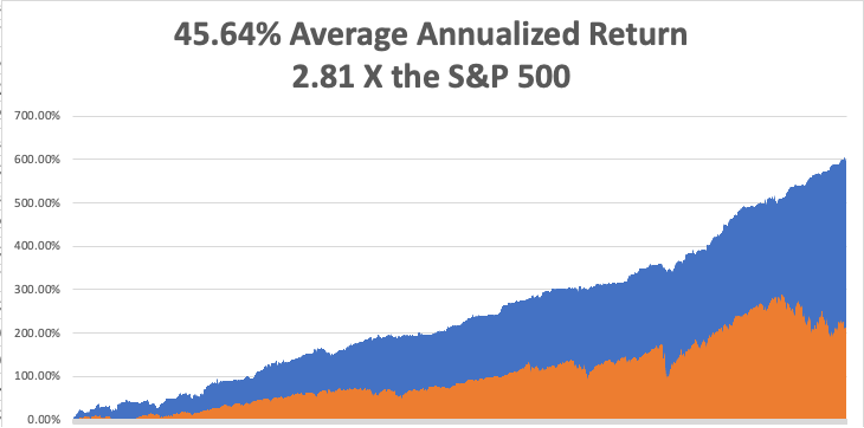

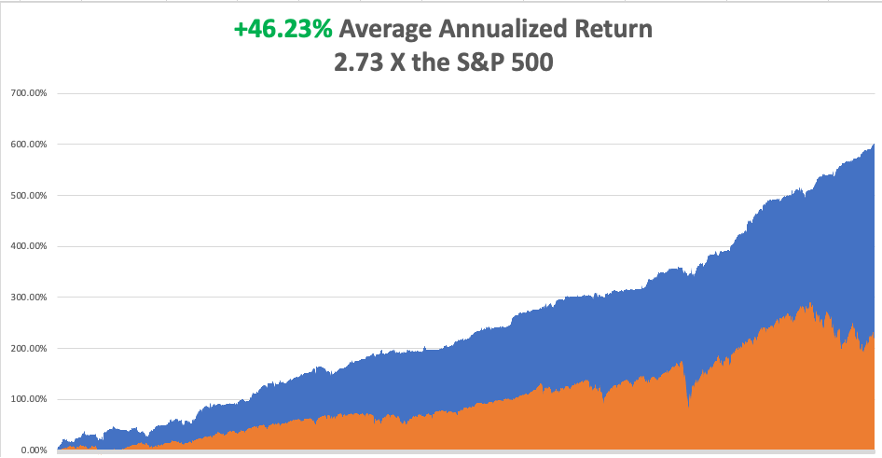

My performance in December has so far tacked on another robust +4.85%. My 2022 year-to-date performance ballooned to +88.53%, a spectacular new high. The S&P 500 (SPY) is down -17.0% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +92.92%.

That brings my 14-year total return to +601.09%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +46.23%, easily the highest in the industry.

I took profits in my oil shorts in (XOM), (OXY), (SPY), and (TSLA). I am keeping one long in (TSLA), with 90% cash for a 10% long position.

Producer Prices Come in High, up 0.3% in November, driven by rising prices for services. It sets up an exciting CPI for Tuesday morning.

Emerging Markets Saw Massive Inflows in November, some $37.4 billion, the most since June 2021. Chinese technology stocks were two big beneficiaries, down 80%-90% from their highs. This could be one of the big 2023 performers if the US dollar and interest rates continue to fall. Buy (EEM) on dips.

Oil is in Free Fall, with 57 fully loaded Russian tankers about to hit the market. Nobody wants it ahead of a recession. All mad hedge short plays in energy are coming home. When will the US start refilling the Strategic Petroleum Reserve?

Turkey Blocks Russian Oil at the Straights of Bosporus, checking insurance papers, which are often turning out to be bogus. Insurance Russian tankers are now illegal in western countries. Many of these tankers are ancient, recently diverted from the scrapyard and in desperate need of liability insurance. Oil spills are expensive to clean up. Just ask any Californian.

Tesla Cuts Production in China, some 20% at its Shanghai Gigafactory for its Model Y SUV, or so the rumor goes. The short sellers are back! These are the kind of rumors you always hear at market bottoms.

US Unemployment to Peak at 5.5% in Q3 of 2023, according to a survey from the University of Chicago Business School. A tiny handful expects a higher 7.0% rate. Some 85% of economists polled expect a recession next year. After that, the Fed will take interest rates down dramatically to bring unemployment back down. No room for a soft landing here.

Home Mortgage Demand Plunges in another indicator of a sick housing market, which is 20% of the US economy. New applications are down a stunning 86% YOY despite a dive in the 30-year rate to 6.41%, but nobody is selling. Refis are now nonexistent.

Gold Continues on a Tear, hitting new multi-month highs. With interest rates certain to plummet in 2023 as the Fed reacts to a recession, Gold could be one of the big trades for next year. Buy (GLD), (GDX), and (GOLD) on dips.

Services PMI Hits New Low for 2022 at a recessionary 46.2. Nothing but ashes in this Christmas stocking. It didn’t help bonds, which sold off two points yesterday.

Demand Collapse Hits China (FXI), with US manufacturing there down 40% and many factories closing early for the New Year. Container traffic from the Middle Kingdom is down 21% over the past three months, astounding ahead of Christmas.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, December 12 at 8:00 AM, the Consumer Inflation Expectations for November is published.

On Tuesday, December 13 at 8:30 AM EST, the Core Inflation Rate for November is out

On Wednesday, December 14 at 11:00 AM EST, the Federal Reserve Interest rates decision is announced. The Press Conference follows at 11:30.

On Thursday, December 15 at 8:30 AM EST, the Weekly Jobless Claims are announced. Retail Sales for November are printed.

On Friday, December 16 at 8:30 AM EST, the S&P Global Composite Flash PMI for December is disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, in 1978, the former Continental Airlines was looking to promote its Air Micronesia subsidiary, so they hired me to write a series of magazine articles about their incredibly distant, remote, and unknown destinations.

This was the only place in the world where jet engines landed on packed coral runways, which had the effect of reducing engines lives by half. Many had not been visited by Westerners since they were invaded, first by the Japanese, then by the Americans, during WWII.

That’s what brought me to Tarawa Atoll in the Gilbert Islands, and island group some 2,500 miles southwest of Hawaii in the middle of the Pacific Ocean. Tarawa is legendary in the US Marine Corps because it is the location of one of the worst military disasters in American history.

In 1942, the US began a two-pronged strategy to defeat Japan. One assault started at Guadalcanal, expanded to New Guinea and Bougainville, and moved on to Peleliu and the Philippines.

The second began at Tarawa, and carried on to Guam, Saipan, and Iwo Jima. Both attacks converged on Okinawa, the climactic battle of the war. It was crucial that the invasion of Tarawa succeed, the first step in the Mid-Pacific campaign.

US intelligence managed to find an Australian planter who had purchased coconuts from the Japanese on Tarawa before the war. He warned of treacherous tides and coral reefs that extended 600 yards out to sea.

The Navy completely ignored his advice and in November 1943 sent in the Second Marine Division at low tide. Their landing craft quickly became hung up on the reefs and the men had to wade ashore 600 yards in shoulder-high water facing withering machine gun fire. Heavy guns from our battleships saved the day but casualties were heavy.

The Marines lost 1,000 men over three days, while 4,800 Japanese who vowed to keep it at all costs, fought to the last man.

Some 35 years later, it was with a sense of foreboding that I was the only passenger to debark from the plane. I headed for the landing beaches.

The entire island seemed to be deserted, only inhabited by ghosts, which I proceeded to inspect alone. The rusted remains of the destroyed Marine landing craft were still there with their twin V-12 engines, black and white name plates from “General Motors Detroit Michigan” still plainly legible.

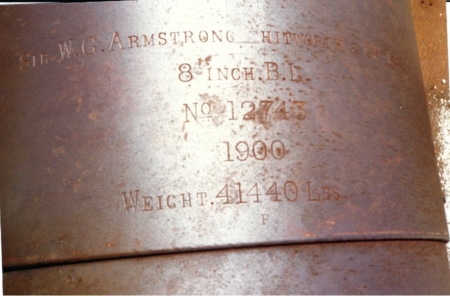

Particularly impressive was the 8-inch Vickers canon the Japanese had purchased from England, broken in half by direct hits from US Navy fire. Other artillery bore Russian markings, prizes from the 1905 Russo-Japanese War transported from China.

There were no war graves, but if you kicked at the sand human bones quickly came to the surface, most likely Japanese. There was a skull fragment here, some finger bones there, it was all very chilling. The bigger Japanese bunkers were simply bulldozed shut by the Marines. The Japanese are still in there. I was later told that if you go over the area with a metal detector it goes wild.

I spend a day picking up the odd shell casings and other war relics. Then I gave thanks that I was born in my generation. This was one tough fight.

For all the history buffs out there, one Marine named Eddie Albert fought in the battle who, before the war, played “The Tin Man” in the Wizard of Oz. Tarawa proved an expensive learning experience for the Marine Corps, which later made many opposed landings in the Pacific far more efficiently and with far fewer casualties. And they paid much attention to the tides and reefs, developing Underwater Demolition Teams, which later evolved into the Navy Seals.

The true cost of Tarawa was kept secret for many years, lest it speak ill of our war planners, and was only disclosed just before my trip. That is unless you were there. Tarawa veterans were still in the Marine Corps when I got involved during the Vietnam War and I heard all the stories.

As much as the public loved my articles, Continental Airlines didn’t make it and was taken over by United Airlines (UAL) in 2008 as part of the Great Recession airline consolidation.

Tarawa is still visited today by volunteer civilian searchers looking for soldiers missing in action. Using modern DNA technology, they are able to match up a few MIAs with surviving family members every year. I did the same in Guadalcanal.

As much as I love walking in the footsteps of history, sometimes the emotional price is high, especially if you knew people who were there.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tarawa November 1943

Broken Japanese Cannon

Armstrong 8-Inch Cannon 1900

US Landing Craft on the Killer Reef

How to Get to Tarawa

Roving Foreign Correspondent on Tarawa in 1978

Second Marine Division WWII Patch

https://www.madhedgefundtrader.com/wp-content/uploads/2022/12/japanese-cannon-e1670867621973.jpg305450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-12 10:02:252022-12-12 15:43:55The Market Outlook for the Week Ahead, or How Markets Work

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD MARKET AND THE BAD MARKET)

(TLT), (XOM), (OXY), (TSLA), (SPY), (BABA), (BIDU), (KBH), (PHM), (LEN), (AAPL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-05 09:04:592022-12-05 13:01:09December 5, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.