Global Market Comments

October 18, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD NEWS IS HERE)

(GS), (MS), (JPM), (BAC), (C), (BLK), (TLT), (BRKB), (SPY)

Global Market Comments

October 18, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD NEWS IS HERE)

(GS), (MS), (JPM), (BAC), (C), (BLK), (TLT), (BRKB), (SPY)

Here’s the good news.

You know those pesky seasonals that have been a drag of the market for the past five months? You know, that sell in May and go away thing?

It’s about to end, vanish, and vaporize.

We are only ten trading days away from when seasonals turn hugely positive on November 1.

On top of that, the pandemic is rapidly receding, the economy reaccelerating, and workers are returning to the workforce. The action Biden took with the west coast ports should unlock the logjam there. It all sounds like a Goldilocks scenario.

The ports issue has nothing to do with the pandemic. The truth is that with 6% GDP growth, the US economy is growing faster than it has ever done before. That means we are buying a lot more stuff, more than our antiquated infrastructure can handle. Unlock the ports, and growth could accelerate even further.

Bitcoin has been on fire as well, doubling since August 1. The focus has been on the launch of the first crypto futures ETF, which may happen as early as today. All of the trade alerts we issued in this space have been total home runs. (Click here for our Bitcoin Letter).

As a result, Bitcoin is within striking range of hitting a new all-time high at $66,000. Break that, and we could see a melt-up straight to $100,000.

Want another reason to be bullish? The Millennial generation is about to inherit $68 trillion by 2030. Guess where that is going? Bitcoin and all other risk assets, as younger investors tend to be more aggressive.

So, what to do about all of this?

Keep doing more of what’s working. Buy financials and Bitcoin and sell short bonds. Wait for tech to bottom out at the next interest rate peak, then load the boat there once again.

Make as much money as you can now because 2022 could be a year of diminished expectations. Stocks might rise by only 15% compared to this year’s 30% torrid rate.

As for Bitcoin, that is a horse of a different color.

CPI Hits 5.4%, and was up 0.4% in September, a high for this cycle. This time, it was food and energy that took the lead. Used car prices, which went ballistic last month, showed a decline. Supply chain problems are wreaking havoc and those with inventory can charge whatever they want. The Fed thinks this is transitory, the bond market doesn’t. Sell rallies in the (TLT).

Weekly Jobless Claims Plunge to 293,000, a new post-pandemic low. With delta in retreat, higher wages are luring people back to work to deal with massive supply chain problems. This may be the beginning of the big drop in unemployment to pre-pandemic levels. Stocks will love it. Buy stocks on dips.

Big Banks Report Blowout Earnings and are firing on all cylinders. The best is yet to come. Interest rates are rising, default rates are falling, profit margins expanding, and the economy is growing at a record rate. Buy (JPM), BAC), and (C) on dips.

The Nonfarm Payroll Bombs in September, coming in at only 194,000. That follows a weak 235,000 in August. The headline Unemployment Rate dropped to a new post-pandemic low of 4.8%, down from a peak of 22%. It’s not a soggy economy that’s causing this, but a shortage of people to hire. Some 10 million workers have gone missing from the American economy, and many may never come back.

Bitcoin Soars to $61,000, a five-month high, putting the previous $66,000 high in range. With ten crypto ETFs waiting in the wings for SEC approval, a flood of money is about to hit the sector. Several countries are now considering the adoption of Bitcoin as a national currency after El Salvador’s move. Keep buying Bitcoin dips. Mad Hedge Bitcoin Letter followers are making a fortune.

Oil (USO) Tops $80, after OPEC limits production increases to 400,000 barrels a day, dragging on the stocks market. Prices are approaching levels that will restrain growth. Pandemic under-investment and distribution problems have triggered a short squeeze. There will be many spikes on the way to zero.

Fed Minutes Show Taper to Start in November, as discussed in the September meeting. They may start with $15 billion a month in fewer bond purchases. The inflation boogie man is getting bigger with the 5.4% print on Tuesday. Sell rallies in the (TLT)

JOLTS Comes in at 10.4 million indicating that the labor shortage is getting more severe. Millions are still staying home for fear of catching covid. There is also a massive skills disparity resulting from decades of under-investment in education.

IMF Cuts Global Growth Forecast to 5.9%. Supply chains, delta, inflation worries, and vaccine access are to blame.

US Dollar (UUP) Hits One-Year High on rising interest rates. This will continue for the foreseeable future. Stand aside from the (UUP) as this is a countertrend trade. We may be only 15 basis points away from an interim peak in rates at 1.76% for the ten-year.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a heroic +8.91% gain so far in October. My 2021 year-to-date performance soared to 81.51%. The Dow Average was up 15.4% so far in 2021.

Figuring that we are either at, or close to a market bottom, and being a man of my convictions, I kept 90% invested in financial stocks all the wall until the October 15 options expirations. Those include (MS), (GS), (JPM), (BLK), (BRKB), (BAC), and (C).

The payday was big and more than covered earlier in the month stop-losses in (SPY) and (DIS). I quick trip by the Volatility Index (VIX) to $29, then back to $15 was a big help.

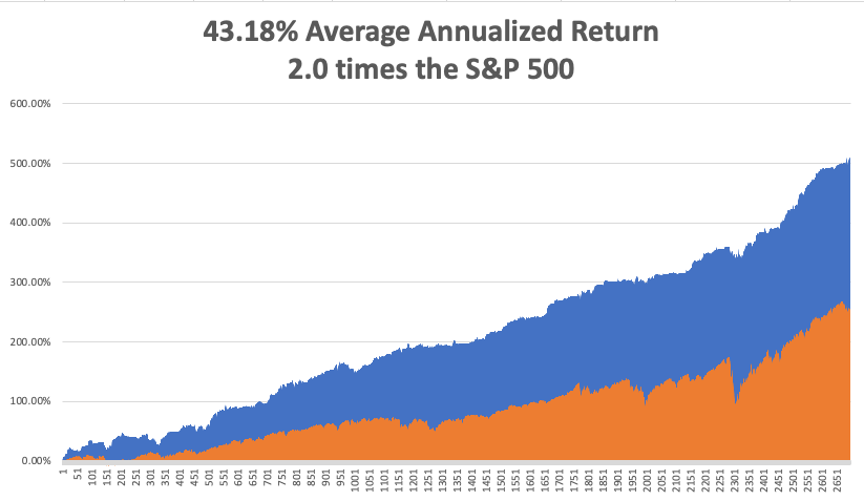

That brings my 12-year total return to 511.06%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 43.19%, easily the highest in the industry.

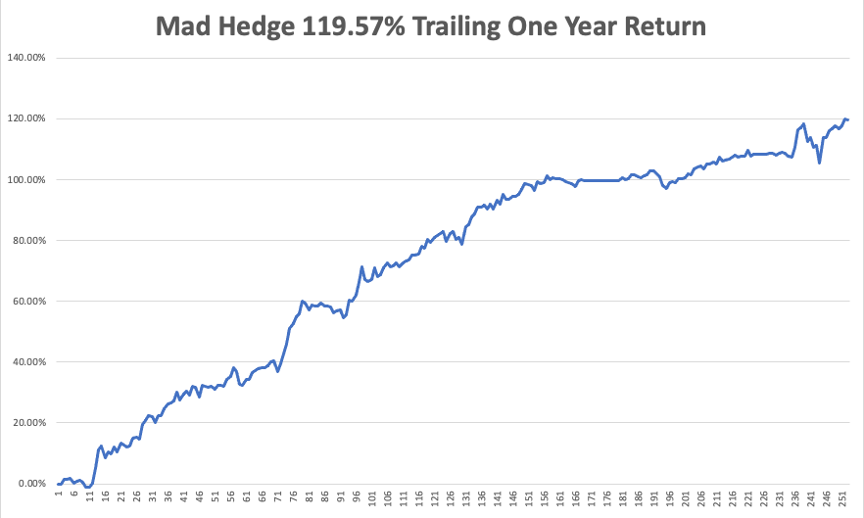

My trailing one-year return popped back to positively eye-popping 119.57%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 45 million and rising quickly and deaths topping 725,000, which you can find here.

The coming week will be slow on the data front.

On Monday, October 18 at 8:15 AM, Industrial Production for September is published. Johnson & Johnson (JNJ) reports.

On Tuesday, October 19 at 8:00 AM, the Housing Starts for September are released. Netflix (NFLX) reports.

On Wednesday, October 20 at 7:30 AM, Crude Oil Stocks are announced. Tesla (TSLA) and IMB (IBM) report.

On Thursday, October 21 at 8:30 AM, Weekly Jobless Claims are announced. At 10:00 AM, Existing Home Sales for September are printed. Alaska Air (ALK) and Southwest Air (LUV) report.

On Friday, October 22 at 8:45 AM, the US Markit Flash Manufacturing and Services PMI is out. American Express (AXP) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

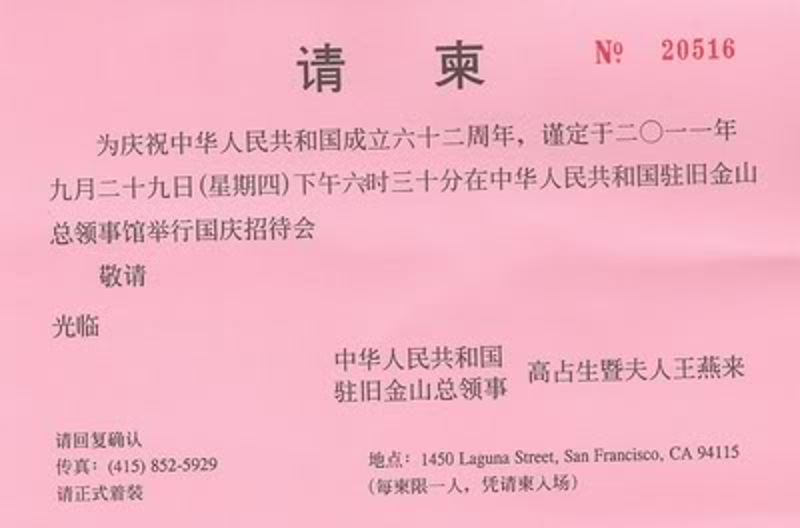

As for me, I normally avoid the diplomatic circuit, as the few non-committal comments and soggy appetizers I get aren’t worth the investment of time.

But I jumped at the chance to celebrate the 70th anniversary of the founding of the People’s Republic of China with San Francisco consul general Gao Zhansheng.

Happy Birthday, China!

When I casually mention that I survived the Cultural Revolution from 1968 to 1976 and interviewed major political figures like Premier Deng Xiaoping, who launched the Middle Kingdom into the modern era, and his predecessor, Zhou Enlai, modern-day Chinese are enthralled.

It’s like going to a Fourth of July party and letting drop that I palled around with Thomas Jefferson and Benjamin Franklin.

Five minutes into the great hall, and I ran into my old friend Wen. She started out her career with the Chinese Intelligence Service and had made the jump to the Foreign Ministry, as all their best people did. Wen was passing through town with a visiting trade mission.

When I was touring China in the seventies as the guest of the Bank of China, Wen was assigned as my guide and translator, and we kept in touch over the years. I was assigned a bodyguard who doubled as the driver of a tank-like Russian sedan, a Volga.

The Cultural Revolution was on, and while the major cities were safe, we ran the risk of running into a renegade band of xenophobic Red Guards, with potentially fatal consequences.

By the time Wen married, China had already adopted its one-child policy. As much as she wanted more children, she understood the government’s need to adopt such a drastic policy. Without it, the population today would be 1.6 billion, not 1.2 billion, and all of the money that went into buying capital goods would have been spent on food imports instead.

The country would have stagnated at its 1980 per capita income of $100/year. There would have been no Chinese economic miracle. She was very proud of her one son, who was a software engineer at Microsoft (MSFT) in Beijing.

I asked if she recalled our first trip together and a dark cloud came over her face. We were touring a section of Fuzhou in southern China when three policemen marched up. They started shouting at Wen that we were in a restricted section of the city where foreigners were not allowed. They started mercilessly beating her with clubs.

I was about to intercede when my late wife, Kyoko, let go with a blood-curdling tirade in Japanese that froze them in their tracks. I saw from the fear in their faces that she had ignited their wartime fear of Japanese authority and the dreaded Kempeitai, or secret police, and they beat a hasty retreat.

To this day, I’m not exactly sure what Kyoko said. We took Wen back to our hotel room and bandaged her up, putting ice on the giant goose egg on her head. When I left, I gave her my paperback copy of HG Well’s A Short History of the World, which she treasured, as the book was then banned in China.

Wen mentioned that she was approaching the mandatory retirement age of 60, and soon would be leaving the Foreign Service. I suggested she move to San Francisco, which offered a thriving Chinese community.

She laughed. No matter how much prices had fallen, she could never afford anything here on a Chinese civil servant’s salary.

I asked Wen if she still had the book I gave her nearly five decades ago. She said it had become a treasured family heirloom and was being passed down through the generations.

As she smiled, I notice the faint scar on her eyebrow from that unpleasantness so long ago.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

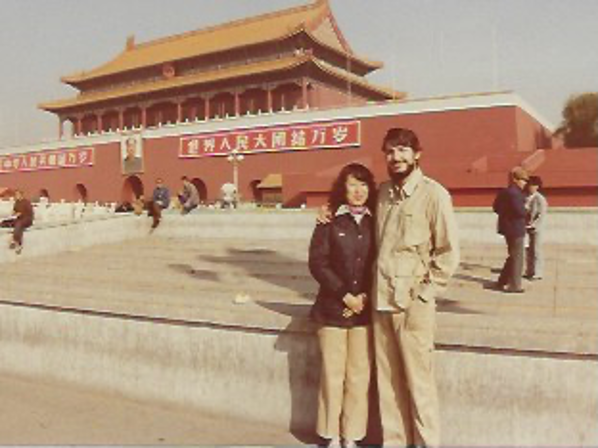

Kyoko and I in Beijing in 1977

Followers of the Mad Hedge Fund Trader alert service have the good fortune to own deep-in-the-money options positions that expire on Friday, October 15, and I just want to explain to the newbies how to best maximize their profits.

These involve the:

(SPY) 10/$410-$420 call spread 10.00%

(GS) 10/$320-$330 call spread 10.00%

(JPM) 10/$130-$140 call spread 10.00%

(BLK) 10/$770-$790 call spread 10.00%

(MS) 10/$85-$90 call spread 10.00%

(BRKB) 10/$255-$265 call spread 10.00%

(C) 10/$62-$65 call spread 10.00%

Provided that we don’t have another 2,000-point move down in the market this week, these positions should expire at their maximum profit points.

So far, so good.

I’ll do the math for you on our deepest in-the-money position, the Goldman Sachs (GS) October 15 $320-$330 vertical bull call spread, which I most certainly will run into expiration. Your profit can be calculated as follows:

Profit: $10.00 expiration value - $8.50 cost = $1.50 net profit

(11 contracts X 100 contracts per option X $1.50 profit per options)

= $1,650 or 17.65% in 24 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning, October 18 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration on Friday, October 15. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month-end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

Well done, and on to the next trade.

You Can’t Do Enough Research

Global Market Comments

October 11, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE SUMMIT VIDEOS ARE UP),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HAPPY DAYS ARE HERE AGAIN),

(GS), (MS), (JPM), (BAC), (C), (BLK), (TLT), (BRKB), (SPY)

Global Market Comments

October 7, 2021

Fiat Lux

Featured Trade:

(A NOTE ON ASSIGNED OPTIONS, OR OPTIONS CALLED AWAY)

(SPY), (TLT)

I know all of this may sound confusing at first. But once you get the hang of it, this is the greatest way to make money since sliced bread.

I still have a record ten positions left in my model trading portfolio, they are all deep-in-the-money, and about to expire in six trading days. That opens up a set of risks unique to these positions.

I call it the “Screw up risk.”

As long as the markets maintain current levels, ALL of these positions will expire at their maximum profit values.

They include:

(SPY) 10/$410-$420 call spread 10.00%

(GS) 10/$320-$330 call spread 10.00%

(JPM) 10/$130-$140 call spread 10.00%

(BLK) 10/$770-$790 call spread 10.00%

(MS) 10/$85-$90 call spread 10.00%

(BRKB) 10/$255-$265 call spread 10.00%

(C) 10/$62-$65 call spread 10.00%

With the October 15 options expirations upon us, there is a heightened probability that your short position in the options may get called away.

If it happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money vertical option spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker telling you that your call options have been assigned away.

I’ll use the example of the S&P 500 (SPY) $410-$420 in-the-money vertical BULL CALL spread.

For what the broker had done in effect is allow you to get out of your call spread position at the maximum profit point days before the October 15 expiration date. In other words, what you bought for $9.00 on September 17 is now worth $10.00, giving you a near-instant profit of $1,111 or 11.11%!

In the case of the S&P 500 (SPY) September 2021 $410-$420 in-the-money vertical BULL CALL, all have to do is call your broker and instruct them to “exercise your long position in your (SPY) October 15 $410 calls to close out your short position in the (SPY) October 15 $420 calls.”

You must do this in person. Brokers are not allowed to exercise options automatically, on their own, without your expressed permission.

This is a perfectly hedged position, with both options having the same name and the same expiration date, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one options contract is exercisable into 100 shares.

Short positions usually only get called away for dividend-paying stocks or interest-paying ETFs like the (TLT). There are strategies out here that try to capture dividends the day before they are payable. Exercising an option is one way to do that.

Weird stuff like this happens in the run-up to options expirations like we have coming.

A call owner may need to buy a long (SPY) position after the close, and exercising his long (SPY) call is the only way to execute it.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there that may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to blow it by writing shoddy algorithms.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

There is a further annoying complication that leads to a lot of confusion. Lately brokers have resorted to sending you warnings that exercises MIGHT happen to help mitigate their own legal liability.

They do this even when such an exercise has zero probability of happening, such as with a short call option in a LEAPS that has a year or more left until expiration. Just ignore these, or call you broker and ask them to explain.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

There may not even be an evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. In fact, I think I’m the last one they really did train.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Global Market Comments

September 27, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE SUMMIT VIDEOS ARE UP)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE YEAREND RALLY HAS BEGUN),

(DIS), (TLT), (SPY), (GS), (JPM), (BLK), (MS), (BRKB), (GOOG)

The calls started coming in as soon as the market closed.

More than a dozen subscribers called, emailed, and texted me on Thursday to say that they just had the best day in the market this year, and for some, their entire lives.

Holding fire until you saw the whites of their eyes worked. I used both visits to the (SPY) to $430 to load the boat with financial stocks, which then took off like a tribe of scalded chimps.

Mad Hedge made 5.6% on that day alone. One Concierge client reported a breathtaking $5.3 million profit after dumping a lot of his techs and piling into banks and brokers. Suffice it to say that I am very welcome in a well-to-do suburb of Seattle, Washington.

The washout was so dramatic and the recovery so rapid I think it is safe to say that our fall correction is over. We may get some small retracements and sideways chop from here. But the writing is on the wall. We are headed to new all-time highs in stocks by the end of 2022.

I received a lot of questions about how easily I was able to spot the bottom so easily. A Volatility Index (VIX) of $29 was a big help. So was the outflow of $34 billion from equity ETFs and mutual funds the previous week, the most in six months. And when the Mad Hedge Market Timing Index hits a rare low of 19, you don’t sit on your hands very long.

The $300 billion China Evergrande Group debt crisis gave us the crisis and the final flush we needed to establish a clear bottom.

Nothing else can stop this. New Covid cases are falling off a cliff, and childhood vaccinations out next month will accelerate this trend.

A massive infrastructure budget will pass in congress. It is almost irrelevant whether it’s a $3.5 trillion or $1.5 trillion. It will be more than can be spent in any reasonable amount of time.

In the meantime, the ultimate driver of share prices, the exponential growth of post covid corporate profits, continues unabated.

The wall of money keeps getting ever larger. The Fed reported that in Q2, Household Net Worth soared by $5.9 trillion is an incredible $141.7 trillion largely through the appreciation of stock and home prices. The Fed balance sheet has exploded from $4.1 trillion to $8.4 trillion in a mere 18 months.

This will continue for another decade. Keep piling on those leveraged long-term LEAPS. Flat is the new down.

Enjoy.

Four to six Interest RatesRises by 2024 which may start as early as 2024, says Fed governor Jay Powell. The taper could start in November. Bonds rose slightly on the news, but the writing is now definitely on the wall. The Fed now expects a stratospheric 5.9% GDP for 2021 and 3.8% for 2022. Sell all rallies in the (TLT) and buy all financial stocks.

Bonds Crash, down -$3.43 points after Jay Powell’s super bearish comments from Wednesday soak in. The 50-day moving average has been smashed and the next target is the 200-day at $1344.59. Watch the 50-day rollover from here on. My final target is a 1.76% yield on the ten-year US Treasury bond by January.

Back up the Truck, it’s time to load up on stocks on the back of yesterday’s 985-point swan dive. You especially want domestic recovery ones that benefit from rising interest rates, like banks, brokers, fund managers, commodities, and steel. The taper may be only weeks away and will drive stocks to new highs by yearend. You wanted a dip to buy, so buy the dip. Don’t expect much from technology stocks for a while.

China’s Largest Real Estate Developer Goes Bust, China Evergrande Group, with $300 billion in debt. The move smashed risk markets globally, opening the Dow Average down 650. Bitcoin plunged 10%. Is this China’s Lehman moment, or just another day at the office? It does take them another step back towards real communism.

China Bans Crypto, triggering a 7% plunge in Bitcoin. Financial systems the government can’t control are forbidden in the Forbidden City. It’s all part of a flight out of a restricted Yuan into unrestricted crypto by wealthy Chinese. China used to account for 99% of all Bitcoin mining and now it is at zero. The business will flock to the US, Canada, and any other country with cheap electricity. It’s a short-term negative for crypto but a long term positive. Buy Bitcoin and Ethereum on the dip.

Pfizer Boosters for over 65 were approved by the FDA for immediate distribution. Those younger will have to wait. It turns out that the Pfizer effectiveness drops from 99% to 66% in eight months. That puts older recipients, like me, at risk. Under 12 kids to come in October. See you at Costco! Buy (PFE) on dips.

Pandemic Tops 1918 US Death Toll at 675,000, although on a per capita basis we are still only a third of the Spanish Flu. We are not even close to this ending yet. We need vaccinations for kids and booster shots for all to be dome with this, getting national immunity up to 90%.

Housing Starts for August up 3.9% with apartment buildings the big driver. Single family homes fell. Building Permits are up 6.0% and are a 50% increase from the summer lows.

Existing Home Sales Drop, by 2% in August to 5.88 million units annualized according to a signed contract basis. Only 1.29 million homes are for sale, a 2.6-month supply, down 13% YOY. The Median Price rose to an eye-popping $356,700, up 14.9% YOY. Million-dollar homes are up 40% YOY.

Google (GOOG) Buys $2.1 Billion in New York Office Space, which is why I love this company. You can forget about those end of New York City stories. Always follow the money, where companies are putting their money, and you will find great stock. Or so the chairman of JP Morgan Bank taught me 40 years ago. Buy (GOOG) on dips.

Weekly Jobless Claims Pop to 351,000 last week, up 16,000. Leading Economic Indicators jump in August, coming in at 0.9%. March saw the high for the year at 1.3%. Getting a lot of noisy and conflicting economic data points this week as delta works its way through the system.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a robust +6.63% gain so far in September. My 2021 year-to-date performance soared to 85.20%. The Dow Average was up 13.60% so far in 2021. September 23 saw my biggest up day of the year, some 5.61%

I held fire until the Dow Average 1,000-point washout, then loaded the boat with financial stocks, writing the trade alerts as fast as I could. That leaves me 70% long financial stocks, 10% in cash, and 20% in short (TLT).

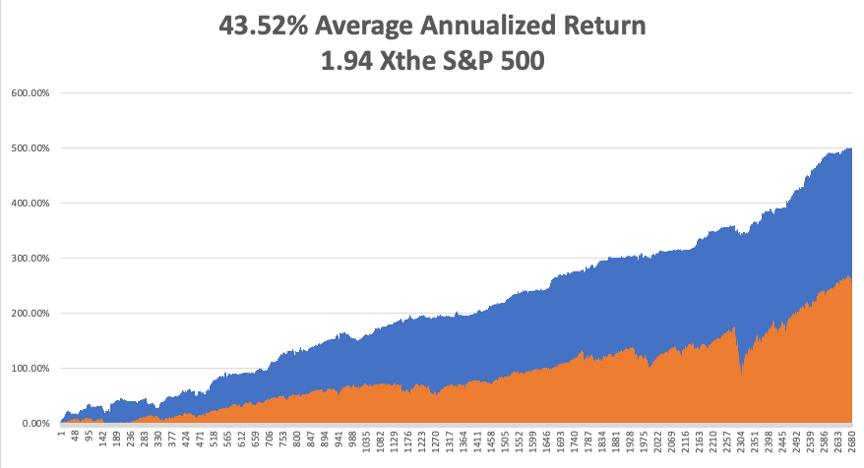

That brings my 12-year total return to 507.75%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 43.52%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 117.34%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 43 million and rising quickly and deaths topping 685,000, which you can find here.

The coming week will be slow on the data front.

On Monday, September 27 at 8:30 AM, Durable Goods are for August are reported.

On Tuesday, September 28 at 9:00 AM, The S&P Case Shiller National Home Price Index for July is published.

On Wednesday, September 29 at 10:00 AM, we get Pending Home Sales for August.

On Thursday, September 30 at 8:30 AM, Weekly Jobless Claims are announced. The final report of the Q2 US GDP is disclosed.

On Friday, October 1 at 8:30 AM, we learn Personal Income and Spending for August. The September Nonfarm Payroll Report is not out for another week due to the first day of the month rule. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, when I first met Andrew Knight, the editor of The Economist magazine in London 45 years ago, he almost fell off his feet. Andrew was well known in the financial community because his father was a famous WWII Battle of Britain Spitfire pilot from New Zealand.

At 34, he had just been appointed the second youngest editor in the magazine’s 150-year history. I had been reporting from Tokyo for years, filing two stories a week about Japanese banking, finance, and politics.

The Economist shared an office in Tokyo with the Financial Times, and to pay the rent, I had to file an additional two stories a week for them as well. That’s where I saw my first fax machine, which then was as large as a washing machine even though the actual electronics would fit in a notebook. It cost $5,000.

The Economist was the greatest calling card to the establishment one could ever have. Any president, prime minister, CEO, central banker, or war criminal were suddenly available for a one-hour chat about the important affairs of the world.

Some of my biggest catches? Presidents Gerald Ford, Jimmy Carter, Ronald Reagan, George Bush, and Bill Clinton, China’s Zhou Enlai and Deng Xiaoping, Japan’s Emperor Hirohito, terrorist Yasir Arafat, and Teddy Roosevelt’s oldest daughter, Alice Roosevelt Longworth, the first woman to smoke cigarettes in the White House in 1805.

Andrew thought that the quality of my posts was so good that I had to be a retired banker at least 55 years old. We didn’t meet in person until I was invited to work the summer out of the magazine’s St. James Street office tower, just down the street from the palace of Prince Charles.

When he was introduced to a gangly 25-year-old instead, he thought it was a practical joke, which The Economist was famous for. As for me, I was impressed with Andrew’s ironed and creased blue jeans, an unheard-of concept in the Wild West.

The first unusual thing I noticed working in the office was that we were each handed a bottle of whisky, gin, and wine every Friday. That was to keep us in the office working and out of the pub next door, the former embassy of the Republic of Texas from pre-1845. There is still a big white star on the front door.

Andrew told me I had just saved the magazine.

After the first oil shock in 1972, a global recession ensued, and all magazine advertising was cancelled. But because of the shock, it was assumed that heavily oil-dependent Japan would go bankrupt. As a result, the country’s banks were forced to pay a ruinous 2% premium on all international borrowing. These were known as “Japan rates.”

To restore Japan’s reputation and credit rating, the government and the banks launched an advertising campaign unprecedented in modern times. At one point, Japan accounted for 80% of all business advertising worldwide. To attract these ads, the global media was screaming for more Japanese banking stories, and I was the only person in the world writing them.

Not only did I bail out The Economist, I ended up writing for over 50 business publications around the world in every English-speaking country. I was knocking out 60 stories a month, or about two a day. By 26, I became the highest-paid journalist in the Foreign Correspondents’ Club of Japan and a familiar figure in every bank head office in Tokyo.

The Economist was notorious for running practical jokes as real news every April Fool’s Day. In the late 1970s, an April 1 issue once did a full-page survey on a country off the west coast of India called San Serif.

It warned that if the West coast kept eroding, and the East coast continued silting up, the country would eventually run into India, creating serious geopolitical problems.

It wasn’t until someone figured out that the country, the prime minister, and every town on the map was named after a type font that the hoax was uncovered.

This was way back, in the pre-Microsoft Word era, when no one outside the London Typesetter’s Union knew what Times Roman, Calibri, or Mangal meant.

Andrew is now 82 and I haven’t seen him in yonks. My business editor, the brilliant Peter Martin, died of cancer in 2002 at a very young 54, and the magazine still awards an annual journalism scholarship in his name.

My boss at The Economist Intelligence Unit, which was modelled on Britain’s MI5 spy service, was Marjorie Deane, who was one of the first women to work in business journalism. She passed away in 2008 at 94. Today, her foundation awards an annual internship at the magazine.

When I stopped by the London office a few years ago, I asked if they still handed out the free alcohol on Fridays. A young writer ruefully told me, “No, they don’t do that anymore.”

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 20, 2021

Fiat Lux

Featured Trade:

(INTRODUCING THE MAD HEDGE BITCOIN PLATINUM SERVICE),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BATTLE OF THE 50-DAY),

(SPY), (TLT), (DIS), (BLOK), (MSTR), (QQQ), (EEM), (UUP)

The next long-term driver of financial markets will be rising interest rates.

It’s not a matter of if, but when. Is it this month, or next month? One way or the other it’s coming.

Which means you should be rearranging your portfolio right now big time.

In a rising interest rate regime seven big things will happen:

1) Bonds (TLT) will collapse.

2) Domestic recovery and commodity stocks (FCX) will soar.

3) Technology stocks (QQQ) will move sideways to down 10%

4) The US dollar (UUP) craters

5) Foreign stock markets (EEM) do better than American ones.

6) Bitcoin (BLOK), (MSTR) and other cryptocurrencies go through the roof.

7) Residential real estate keeps appreciate, but at a slower rate.

These trends will continue for six months, or until long-term interest rates hit an interim peak, such as at 2.00%.

The delta variant gave us a secondary recession. Its demise will give us a secondary recovery, and the same sectors will prosper as with the first. According to the Johns Hopkins University of Medicine, this is happening right now.

The only caution here is that long-term investors should probably keep their technology stocks. Once rates hit the next interest rate peak again, it will be off to the races for tech once again. In the long term, tech always comes back, and tech always wins.

Of course, the major event of the coming week will be the Federal Reserve’s Open Market Committee meeting where interest rates are decided and the press conference with Jay Powell that follows.

Interest rates won’t move. It’s the press conference that is crucial, where we gain insights into the taper. What’s different this time is that the European Central Bank has already begun their taper with an economy far weaker than ours. Will Jay take the cue?

Far and away, the most reliable indicator for “BUY” timing since the presidential election has been the 50-day moving average for the S&P 500. Increasing stock weightings there and you were golden.

The problem now is that we have not seen the index close below the 50-day for two consecutive days for a record 221 days. This has not happened for 31 years.

We all know the reasons: Record low-interest rates making cash trash, seven years of quantitative easing, and a global liquidity glut. Exploding equity in homes and stock portfolios helps too. Still, 31 years is a long time to be this bullish.

I saw all this coming a mile off.

Since the election, I have relentlessly pursued this market with a super aggressive 100% weighting. Then I started paring back risk in June. In July and August, I cut back further to the bone, running minuscule 20% long weightings against a few shorts.

And this is how you manage your risk control.

When markets are rigged in your favor and the lunch is free, you bet the ranch. When they aren’t, you cower on the sidelines and watch others take insane risks.

But who am I to know? I’ve only been doing this for 51 years, and 58 years if you count the (IBM) shares I bought with my paperboy earnings.

Antitrust Comes Home to Roost at Apple, sending the stock down $9 in two days. A judge ruled that Apple will no longer be allowed to prohibit developers from providing links or other communications that direct users away from Apple in-app purchasing. Apple typically takes a 15% to 30% cut of gross sales. It’s a slap on the wrist, as Apple’s main revenue stream is still from iPhones. The judge ruled in favor of Apple on nine of ten other issues. It creates massive new opportunities for hundreds of other Silicon Valley start-ups. Still, if you were looking for an excuse to take profits, this is it. Buy (AAPL) on dips.

Tesla to get EV Tax Credit Restored in a new overhaul of alternative energy subsidies. Both Tesla (TSLA) and General Motors (GM) lost their $7,500 per car subsidies when sales topped 200,000. GM will get an extra $5,000 discount for union-made cars. Tesla is ferociously non-union. Maybe this explains the 36% rally since May. It should help (TSLA) get reach its million-vehicle target for 2021 if it can get enough chips. Buy (TSLA) on dips.

China Inflation Hits 13 Year High, up 9.5% YOY. Soaring commodity and coal prices are the issue. Coal is up 57% YOY, reflecting an energy shortage during the covid economic rebound. It predicts a hot CPI for the US on Tuesday.

The Consumer Price Index rose by 5.3% YOY and up 0.3% in August. It was a seven-month low, with delta clearly a drag. Food and energy came in lighter than expected. Prices for used cars, air tickets, and insurance fell. Stocks loved it, rising triple digits, and bond prices halved losses. St next week’s FOMC we’ll see how Jay really feels.

House Looking at a Top 26.5% Corporate Tax Rate, well up from the current 21% but not as high as the 28% that was feared. Capital gains would rise from 20% to 25%. The goal is to raise $2.5 trillion to get the $3.5 trillion spending package into law. It’s all a trial balloon for what might be possible. Stocks loved it.

Amazon to Hire 125,000 and boost wages to $18 an hour. They are also paying $3,000 signing bonuses and taking pay up to $22.50 in prime areas like New York and California. It’s all part of a strategy to make (AMZN) the “best employer in the world”. Buy (AMZN) on dips as its dominance on online commerce grows.

China Destroys Casino Stocks, threatening to increase oversight of their Macao operations. The concern is that China will pull the gaming licenses of foreign companies when they come up for renewal in June. Buy (WYNN) and (LVS) on the dip.

Weekly Jobless Claims Come in at 332,000, a new post-pandemic low. The previous week was revised down even lower, to 312,000. The end of pandemic unemployment benefits is no doubt a factor, driving people off of their couches and back to the salt mines. Is this the light at the end of the tunnel?

Bitcoin Charts are Showing a Golden Cross, which usually presages upside breakouts in the cryptocurrency. A golden cross is where the 50-day moving average pierces the 200-day to the upside. This is crucial because technicals are more important in crypto than in any other financial instrument. In the meantime, (AMC) has started accepting Bitcoin for online movie ticket purchases. Buy (MSTR) on dips.

My Ten-Year View

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a modest +1.10% loss so far in September following a blockbuster 9.36% profit in August. My 2021 year-to-date performance soared to 77.47%. The Dow Average is up 13.02% so far in 2021.

That leaves me 70% in cash, 10% short in the (TLT), and 20% long in the (SPY) and (DIS). Both of our September option positions expired at max profits.

I’m keeping positions small as long as we are at extreme overbought conditions. However, a Volatility Index (VIX) above $20 shows there may be a light at the end of the tunnel.

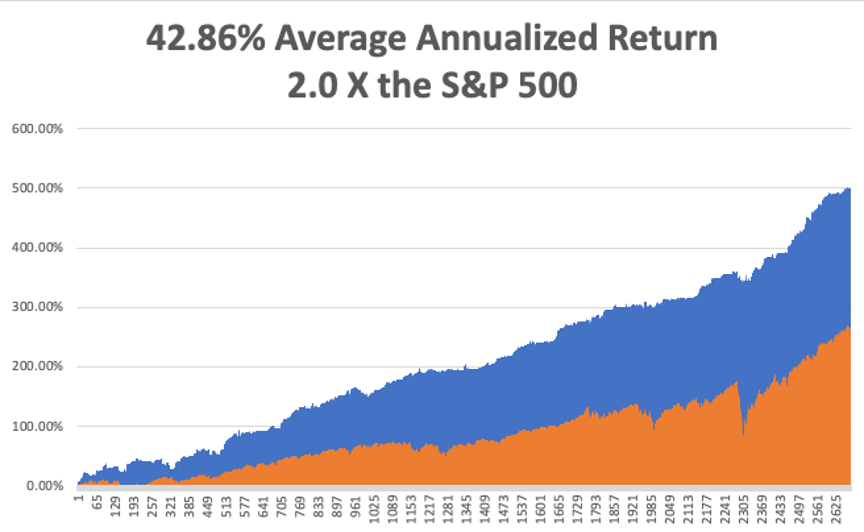

That brings my 12-year total return to 500.02%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.86%, easily the highest in the industry.

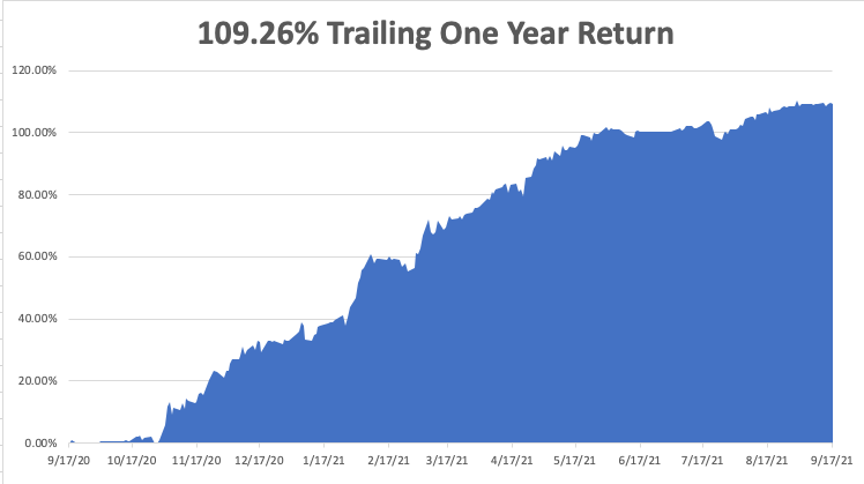

My trailing one-year return popped back to positively eye-popping 109.26%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 42 million and rising quickly and deaths topping 673,000, which you can find here.

The coming week will be all about the Fed meeting on Wednesday.

On Monday, September 20, at 11:00 AM, the NAHB National Housing Market Index for September is out.

On Tuesday, September 21 at 9:30 AM, Housing Starts for August are printed.

On Wednesday, September 22 at 11:00 AM, Existing Home Sales for August are announced. At 2:00 PM, the Fed interest rate decision is released and an important press conference about taper issues follows.

On Thursday, September 23 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, September 24 at 8:30 AM, we learn US Durable Goods for August. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, with the shocking re-emergence of Nazis on America's political scene, memories are flooding back to me of some of the most amazing experiences in my life.

I have been warning my long-term readers for years now that this story was coming. The right time is now here to write it.

I know the Nazis well.

During the civil rights movement of the 1960s, I frequently hitchhiked through the Deep South to learn what was actually happening.

It was not usual for me to catch a nighttime ride with a neo-Nazi on his way to a cross burning at a nearby Ku Klux Klan meeting, always with an uneducated blue-collar worker who needed a haircut.

In fact, being a card-carrying white kid, I was often invited to come along.

I had a stock answer: "No thanks, I'm going to another Klan meeting further down the road."

That opened my driver up to expound at length on his movement's bizarre philosophy.

What I heard was chilling.

During 1968 and 1969, I worked in West Berlin at the Sarotti Chocolate factory in order to perfect my German. On the first day at work, they let you eat all you want for free.

After that, you get so sick that you never wanted to touch the stuff again. Some 50 years later and I still can’t eat their chocolate with sweetened alcohol on the inside.

My co-worker there was named Jendro, who had been captured by the Russians at Stalingrad and was one of the 5% of prisoners who made it home alive in 1955. His stories were incredible and my problems pale in comparison.

Answering an ad on a local bulletin board, I found myself living with a Nazi family near the company's Tempelhof factory.

There was one thing about Nazis you needed to know during the 1960s: They loved Americans.

After all, it was we who saved them from certain annihilation by the teeming Bolshevik hoards from the east.

The American postwar occupation, while unpopular, was gentle by comparison. It turned out that everyone loved Hershey bars.

As a result, I got free room and board for two summers at the expense of having to listen to some very politically incorrect theories about race. I remember the hot homemade apple strudel like it was yesterday.

Let me tell you another thing about Nazis. Once a Nazi, always a Nazi. Just because they lost the war didn't mean they dropped their extreme beliefs.

Fast-forward 30 years, and I was a wealthy hedge fund manager with money to burn, looking for adventure with a history bent during the 1990s.

I was mountain climbing in the Bavarian Alps with a friend, not far from Garmisch-Partenkirchen, when I learned that Leni Riefenstahl lived nearby, then in her 90s.

Attending the USC film school with a young kid named Steven Spielberg decades earlier, I knew that Riefenstahl was a legend in the filmmaking community.

She produced such icons as Olympia, about the 1932 Berlin Olympics, and The Triumph of the Will, about the Nuremberg Nazi rallies. It is said that Donald Trump borrowed many of these techniques during his successful 2016 presidential run.

It was rumored that Riefenstahl was also the onetime girlfriend of Adolph Hitler.

I needed a ruse to meet her since surviving members of the Third Reich tend to be very private people, so I tracked down one of her black and white photos of Nubian warriors, which she took during her rehabilitation period in the 1960s.

It was my goal to get her to sign it.

Some well-placed intermediaries managed to pull off a meeting with the notoriously reclusive Riefenstahl, and I managed to score a half-hour tea.

I presented the African photograph and she seemed grateful that I was interested in her work. She signed it quickly with a flourish.

I then gently grilled her on what it was like to live in Germany in the 1930s. What I learned was fascinating.

But when I asked about her relationship with The Fuhrer, she flashed, "That is nothing but Zionist propaganda."

Spoken like a true Nazi.

The interview ended abruptly.

I took my signed photograph home, framed it, hung it on my office wall for a few years. Then I donated it to a silent auction at my kids' high school.

Nobody bid on it.

The photo ended up in storage at my home, and when it was time to make space, it went to Goodwill.

I obtained a nice high appraisal for the work of art and then took a generous tax deduction for the donation, of course.

It is now more than a half-century since my first contact with the Nazis, and all of the WWII veterans are gone. Talking about it to kids today, you might as well be discussing the Revolutionary war.

By the way, the torchlight parade we saw in Charlottesville, VA in 2017 was obviously lifted from The Triumph of the Will, except that they didn't use tiki poolside torches in Germany in the 1930s.

Leni Riefenstahl

Olympia

Former Paperboy