Global Market Comments

October 23, 2020

Fiat Lux

Featured Trade:

(11 SURPRISES THAT WOULD DESTROY THIS MARKET),

(SPY), (USO), (AMZN), (MCD), (WMT), (TGT)

Global Market Comments

October 23, 2020

Fiat Lux

Featured Trade:

(11 SURPRISES THAT WOULD DESTROY THIS MARKET),

(SPY), (USO), (AMZN), (MCD), (WMT), (TGT)

Global Market Comments

October 19, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

OR WHY THE NEXT TWO WEEKS ARE A WRITE-OFF)

(V), (SPY)

You can pretty much write off trading for the next two weeks.

The election has been decided. It’s going to be a scandal a day in the media, but everyone has already made up their minds. All attention will be devoted to politics at the expense of trading, investment, and research. In the end, the president will lose by more than 15 million votes. All that is left but the imprimatur of the Electoral College.

Yet the Democrats are not declaring victory, with the memory of the 2016 debacle too fresh, when overconfidence and complacency ruled.

The few who are trading are jockeying around to position for the 2021 market. That means keeping big tech and adding to positions in domestic recovery and industrial stocks, like banks, couriers, railroads, and drug companies.

Tech will keep rising because of the catapult into the future provided by the pandemic yet to be reflected by share prices. Domestic industrials will see a recovery that is normal when coming out of a tradition recession, or Great Depression.

But they are doing so hesitantly, with little conviction.

After all, there are national elections in two weeks.

As for me, I have limited myself to the cautious two positions, one long in Visa (V) and one short in the S&P 500 (SPY), both of which are making money.

So, it is a good time to do your research, build your short lists of stocks to buy, and gird your loins. The main event begins after November 3.

Markets jumped on stimulus hopes. Investors don’t really care if stimulus happens before or after a Biden win. They’re buying now. And Biden will almost certainly double up spending later in the year. No dips for latecomers. The post-election market melt-up has begun and new highs beckon. Fears of election disruption have vaporized.

Markets just entered the strongest six months of the year. It’s the inverse of sell in May and go away. October to May portfolios have yielded 64% annually for the past 20 years, while May to October investments yield exactly 4%. It traces back to America’s agricultural cycle of a century ago. Take every tailwind you can find.

The IMF predicted negative 4.4% growth for 2020, the worst since the Great Depression. Believe it or not, this is an upgrade from more dismal numbers. By comparison, the 2008-09 Great Recession brought only a 0.1% drawdown. If the US passes another stimulus package, it will recover its 2019 GDP in 2021 instead of 2022.

The new 5G iPhone is out! After a year of speculation, we get a better screen, improved camera, and magnetic charging for $999. The stock dumped on a classic “buy the rumor, sell the news.” Also out is a new mini iPhone for $699. Your neighborhood won’t have 5G for a year. Buy Apple (AAPL) on dips.

The US PC market saw best quarter in a decade, with millions of new home offices joining the fray. Some 71.4 million computers were shipped in Q3, up 3.6% YOY. Think enormous demand for new chips. Buy (AMD), (MU), and (NVDA) on dips.

Used car prices are soaring, jumping the most since 1969, and lifted the Consumer Price Index by 0.2% in September. It’s the fourth straight month of increasing inflation.

Ships are backed up in Los Angeles waiting to unload. America’s import boom and soaring trade deficit with China leaves no available dock space on the west coast. It’s another sign of a recovering economy.

US Producer Prices pop in September bringing the first YOY gain since March. They were up 0.4% following a 0.3% gain in August. Another sign of a recovering economy.

Weekly Jobless Claims ballooned to 898,000, now that California is reporting again. Not what you want to see going into an election. A slowing economy and spreading virus don’t help either. Some 25.5 million Americans are out of work.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch hit a new all-time high last week by staying 100% in cash. I was just as grateful for having no positions on the up 600-point days as I was on the down 600-point days. Safe to say that I will be an increasingly more aggressive buyer on ever smaller dips and a seller on bigger rallies. October has now reached to a welcome 1.61% profit.

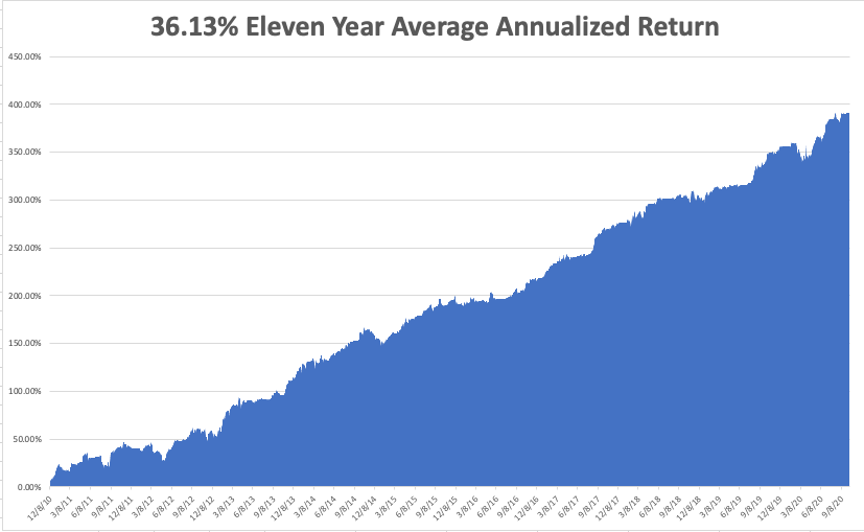

That keeps our 2020 year-to-date performance at a blistering +36.11%, versus a gain of 0.3% for the Dow Average. That takes my eleven-year average annualized performance back to +36.13%. My 11-year total return stood at a new all-time high at +392.02%. My trailing one-year return appreciated to +42.67%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 219,679, which you can find here.

On Monday, October 19 at 8:30 AM EST, the IMF/World Bank virtual annual meeting starts, so we can expect Fed speakers every day. (IBM) reports earnings.

On Tuesday, October 20 at 8:30 AM EST, Housing Starts for September are announced. Netflix (NFLX) reports earnings.

On Wednesday, October 21 at 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out. At 2:00 PM EST, the Fed Beige Book is published, a transcript of the Federal Open Market Committee meeting from six weeks ago. Tesla (TSLA) reports earnings.

change.

On Thursday, October 22 at 8:30 AM EST, the Weekly Jobless Claims are announced. At 10:00 AM EST Existing Home Sales for September are out. AT&T (T) reports.

On Friday, October 23, at 2:00 PM, we learn the Baker-Hughes Rig Count. American Express (AXP) reports earnings.

As for me, I saw a curious thing driving back from Lake Tahoe this weekend. Usually, I see a never-ending parade of out of state license plates moving to the Golden State.

This time, I saw telephone poles coming in by the truckloads, hundreds of them. These are to replace the many burned down in the horrific wildfires that incinerated an area the size of Connecticut. Apparently, California has run out of telephone poles.

Is there a public stock for a company that sells telephone poles?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 7, 2020

Fiat Lux

Featured Trade:

(THE ROARING TWENTIES HAVE JUST BEGUN),

(SPY), (TLT), (TBT), (VIX)

I just about fell out of my chair when the national election poll numbers were released over the weekend.

After remaining stuck at a 49% to 41% lead for the past year, Joe Biden picked up 5% to reach a commanding 54% to 39% lead. These are the most decisive polling numbers since the 1972 Nixon-McGovern contest, when the former carried 49 states in the Electoral College.

A blue wave is now a certainty, where the democratic party gains control of the White House and Congress for at least the next two years.

The enormous swing is no doubt a response to the president’s performance at last week’s debate, which most viewers found wanting. We now know that he was infected with Covid-19 at the time, which among its many symptoms include delusion and poor decision-making.

We don’t know Trump’s academic record because he has sued his alma mater to prevent their release. However, it is safe to say he failed his debate class. You never attack the moderator.

The change in the election outlook has enormous implications for investors. It puts to rest and chance of a Trump win or a contested election. Biden’s lead is now so enormous that it is impossible to overturn through legal challenges, widespread voter suppression, or disabling of the US Post Office.

Differences in vote counts in the hundreds, as we saw in Florida in 2000, are fertile ground for challenges, extended outcomes, and uncertainty. Differences in the tens or hundreds of thousands aren’t.

Don’t take my word for it, listen to Mr. Market. The near three-point plunge in the bond market (TLT) yesterday tells us that good times are coming, demand for new funds will be unprecedented, and interest rates will rise. 2021 could see an unprecedented 10% US GDP growth rate.

As a result, the stock market now has before it the task of backing out a lot of fear and uncertainty that was priced in. Translation: stocks go up.

Horrendous multi thousand-point plunges are now a thing of the past. It is now unlikely that the S&P 500 (SPY) will even fall back to the 200-day moving average at $308, a near certainty only a week ago.

It’s time for you to step up your aggressiveness in returning to risk in general and the stock market specifically. We are about to see another tidal wave of cash to move into technology stocks. Rapid rotation into domestic recovery stocks, banks, and small caps will also ensue.

Your next entry point on the long side will be next Monday after Trump returns to the hospital as his Covid-19 peaks. That is supposed to be what happens 7-10 days after an initial infection. That should be worth 500 or a thousand points of downside.

The Roaring Twenties have just begun, if they hadn’t already last March. My forecast of another 400% gain over the next decade on top of the existing one just received another dollop of credibility.

Oh yes, and don’t forget to vote.

Global Market Comments

October 6, 2020

Fiat Lux

Featured Trade:

(HOW THE RISK PARITY TRADERS ARE RUINING EVERYTHING!),

(VIX), (SPY), (TLT),

(TESTIMONIAL)

I received a call from a hedge fund manager on Friday warning me of what was about to hit the market.

So much money had poured into "risk parity” strategies that it was starting a long-term secular trend up in market volatility (VIX). It was a classic case of too many people bunching up at one end of the canoe.

Witness last week’s failure of stimulus talks on every front. Even though stocks kept going up, the Volatility Index did, too. That is never a good sign.

Investment advisors everywhere are bemoaning the shenanigans of high-frequency traders, offshore hedge funds, and congress for the recent volatility of the market that has been scaring the living daylights out of their clients.

But they have a new enemy that few outside the trading community are aware of: "Risk Parity" managers.

Risk parity is being blamed for the September explosion of volatility that took it from 22% to 36% in a matter of days.

The industry is thought to have $400 billion to $600 billion in assets under management now, with hedge funds Bridgewater and AQR in the lead.

Potentially, they could unload as much as $100 billion worth of stocks in days.

What's more, the fun and games aren't confined to just equities. Risk parity strategies have spread like a pandemic virus to bonds (TLT), foreign exchanges, commodities, and even precious metals.

Risk Parity is an esoteric new investment strategy that targets a specific volatility level, rather than a return relative to a convention benchmark such as Treasury bonds or the S&P 500 (SPY).

When volatility (VIX) is low, they add risk, hoping to beat the returns of competitors. When volatility is high, they cut back positions, hoping they miss the losses of others.

The goal is to come out on top of the money manager league tables, sucking in tons of new assets and countless riches in management fees.

You can see right now where this is going.

In rising markets, they increase buying, and in falling ones, they greatly step up selling.

I'm sure there was a day several years ago when this approach made money hand over fist.

That was probably back when only its inventor was implementing it alone in a back room using an undisclosed hedge fund with a tiny amount of capital.

The problem with risk parity and all other strategies of its ilk is that they become victims of their own success. New capital pours in, returns fall until they inevitably dive into negative numbers.

I have seen this occur time and again, from the portfolio insurance of the 1980s (think October 1987 when the Dow plunged 20% in a single day), to Japanese warrant arbitrage, to high-frequency trading and the flash crashes.

The proof is in the pudding.

An index of 17 risk parity funds tracked by JP Morgan has fallen by 8.2% since the beginning of May. More losses are to come. It sounds like the great unwind of risk parity assets has already started.

Like all investment fads that promise great, risk-free returns, this one will come and go.

In the meantime, fasten your seat belt.

Global Market Comments

October 5, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IS HISTORY REPEATING ITSELF?)

(SPY), (INDU), (DIS), (TLT)

In 1919, President Woodrow Wilson traveled to Europe to negotiate the end of WWI and the Versailles Treaty. Midway through the talks, he suffered a major stroke and was hustled back to the US in an American battleship, the USS George Washington.

The Spanish Flu pandemic was underway, killing millions, so it was thought best to keep the whole matter secret. The president’s wife essentially ran the country for the last three years of Wilson’s administration, claiming to represent the president’s wishes.

This was the history that flashed through my mind when I learned of President Trump’s Covid-19 infection on Thursday night. The presidential election is now effectively over. All fundraising has ceased. It is now an open question whether Trump can even live until the November 3 election. He is, after all, a high-risk patient. Any remaining public campaign events on which the president thrived is out of the question.

The minute the president got sick, media coverage has been wholly devoted to Covid-19. That was not in the Trump plan. Not at all.

The London betting markets soared from a 60% chance of a Biden win to 90% minutes after the Covid-19 news broke. The only question is the extent of the landslide. This election won’t go anywhere near the courts or the Supreme Court, as the stock market has been pricing in. If there is another big gap down, you should be picking up stocks by the bucket load as fast as you can.

Fund managers who thought Trump had a chance of returning will spend this weekend pouring over Biden’s economic policies. All investment decisions will now be made based on the assumption that these will be the policies in force for the next 4, 8, or 12 years.

Think:

higher taxes

more economic stimulus

big infrastructure spending

more quantitative easing

grants to state and local municipalities

no inflation

low-interest rates

more alternative energy subsidies

the return of the Paris Climate Accord

more regulation of the oil industry

end of the trade wars

rejoining the NATO alliance

Oh, and the huge technological advancements and the burgeoning profit opportunities that have emerged in response to the pandemic? We get to keep those.

That is great news for long-term investors. All of this combined is very pro-investment and pro stock market. It firmly solidifies my own Dow target of 120,000 in a decade and another Roaring Twenties and coming American Golden Age. Now, we even have the trigger.

That explains why the market made back a hefty 500 points in hours, even turning positive on the day for a few fleeting moments. On a six-month view, the upside risks are far greater than the downside ones. An S&P 500 of $3,500-$3,700 by yearend is within range, up 6%-12% from here.

The September Nonfarm Payroll Report bombed, coming in at 661,000, well below expected. The headline Unemployment Rate is at a historically high 7.9%. The U-6 real “discouraged worker” jobless rate is at 12.6%. Leisure & Hospitality was the big winner at 318,888, Healthcare gained 107,000, and Retail posted 142,000. Local Government lost a staggering 232,000 jobs and towns run out of money.

US Q2 GDP came in at a horrific negative 31.4% in the final read, the worst in US history. It’s a tough economic record to run for office on. The first Q3 GDP read will not be released until October 29, five days before the presidential election, and should be up huge.

US Capital Goods hit a six-year high, up 1.8% in August. July was revised upward as well. The boost may be short-lived as stimulus money runs out.

Office Rents won’t recover until 2025, says commercial real estate leader Cushman & Wakefield. Some 215 million square feet of demand has been lost due to the pandemic. Many knowledge-based workers are never coming back to the office.

Pending Homes Sales hit a record high in August, up a mind-blowing 8.8% from July and a staggering 24.5% YOY. Hot housing markets are seeing 11%-20% YOY price increases. The northeast saw the biggest gains. This trend has another decade to run. Buy before they run out of stock.

Case Shiller rose 4.8% in July as its National Home Price Index shows. Phoenix (9.2%), Seattle (7.0%), and Charlotte (6.0%) were the price leaders. A stampede to the suburbs fueled by record-low interest rates is the main driver. Look for these trends to continue for years.

Consumer Confidence soared in September, from 84.8 last month to 101.8. Those who have money are spending it. Those who don’t are waiting in lines at food banks, disappearing from the economy. New York bankruptcies surged 40%. If you haven’t spent the past decade investing in your online presence or yourself, you’re toast.

Disney (DIS) laid off 28,000 to stem hemorrhaging losses at its theme parks, hotels, and cruise line. It will take a year to come back. Clearly, their recent $78.3 billion purchase of 21st Century Fox movie and TV studios last year was poorly timed, just before the pandemic, and they borrowed massively to close it. And they had a major presence in China! It’s one of the biggest mass layoffs since Corona began to decimate the economy.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch pushed through to a new all-time high last week on the strength of a position that I kept for a single day. All I needed was the 700-point dive in the Dow Average in 24 hours to realize half the maximum profit in my short (SPY) position. When the market offers me a gift like that, I take it, no questions asked. I am back to a rare 100% cash position, waiting for a bigger dump to buy.

The risk/reward in the market now is terrible. I believe we have to test the 200-day moving averages before it’s safe to go back in with the indexes and single stocks.

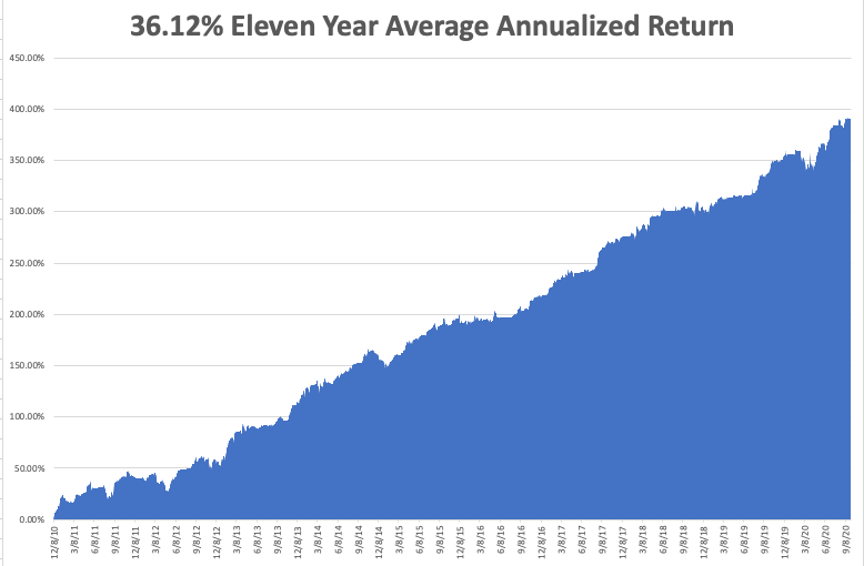

That takes our 2020 year-to-date performance back up to a blistering +35.46%, versus a loss of 2.87% for the Dow Average. October shot out the gate at +0.96%. That takes my 11-year average annualized performance back to +36.12%. My 11-year total return returned to another new all-time high at +391.37%. My trailing one-year return popped back up to +51.82%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 210,000, which you can find here.

On Monday, October 5 at 10:00 AM, the ISM Non-Manufacturing PMI Index for September is released.

On Tuesday, October 6 at 9:00 AM EST, the JOLTS Job Openings for August is published.

On Wednesday, October 7 at 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out. At 2:00 PM EST, the Fed Minutes from the last Open Market Committee Meeting six weeks ago are disclosed.

On Thursday, October 8 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, October 9, at 2:00 PM The Bakers Hughes Rig Count is released.

As for me, I’m headed up to Lake Tahoe again to escape the thick clouds of choking smoke in the San Francisco Bay Area. Also, the polls for the presidential election in Nevada open on October 17 and I have to VOTE!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 28, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DID THE ELECTION OR COVID JUST HIT THE STOCK MARKET?),

(SPY), (TLT), (GLD), (TSLA), (UUP)