Global Market Comments

December 6, 2019

Fiat Lux

Featured Trade:

(DECEMBER 4 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (TLT), (BABA), (CCI), (VIX)

Global Market Comments

December 6, 2019

Fiat Lux

Featured Trade:

(DECEMBER 4 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (TLT), (BABA), (CCI), (VIX)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader December 4 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: How do you see the markets playing out in 2020?

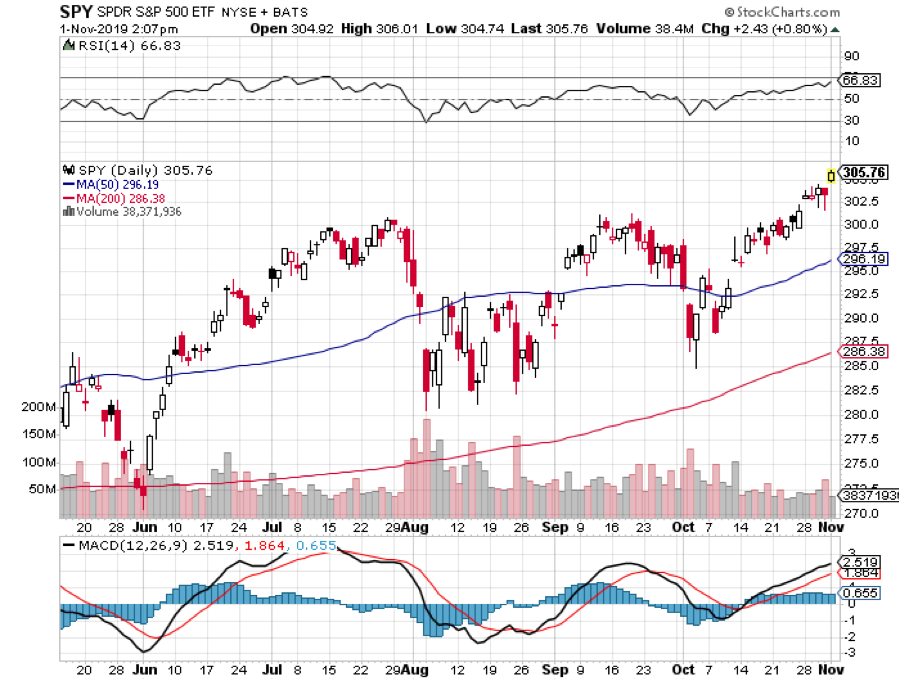

A: Well, I’m looking at small single-digit positive returns with a lot of volatility. Much of this year’s performance—30% in the S&P 500 (SPY), up 56% for the Mad Hedge Fund Trader—has already been pulled forward from 2020, thanks to super low interest rates and massive deficit spending. So, the more money we make now, the less money we make next year.

Q: How deep will the next recession be?

A: I’m looking for two quarters of small negative numbers like -0.1% or -0.2%, and then it’s off to the races again. That’s when the Golden Age of the Next Roaring Twenties starts, which I have already written a book about (click here).

And it’s possible we may not even see any negative numbers on a quarterly basis; we may just get close to zero, threatening it without actually breaking it. Of course, you could still get a 20% correction in the overall stock market if they only THINK we are going into recession, which has happened many times in the last 10 years.

Q: Are you expecting a market crash?

A: No; I do expect a meaningful pullback but frankly, right now, I do not see the conditions in place for that. None of the traditional causes of recessions, high-interest rates or high oil prices, are evident yet. The biggest threat to the market right now is the 2020 presidential election. And we are at a 14-year high in stock valuations.

Q: How bad will it get for car makers, and will the Tesla (TSLA) plant in Germany affect sales for European cars?

A: European carmakers have already been badly affected by Tesla, with Tesla taking over practically the entire luxury end of the market—that’s why companies like Mercedes, Audi and BMW are doing so badly with their shares, and they’re so far behind it’s unlikely they’ll ever catch up. The Berlin factory, I believe, is a battery factory, and after that, there will be a vehicle production factory, probably somewhere in eastern Europe where the cost basis is much lower.

Q: Double Line Capital’s CEO Jeff Gundlach says the US will get crushed in the next recession? Do you agree with him?

A: Well, my first advice to you is never take stock advice from a bond trader. Jeff Gundlach makes these spectacular forecasts, but the timing can be terrible. He can be wrong for 9 months before they finally turn. So, you can go out of business trading off of Jeff Gundlach’s stock advice, though his bond advice is valuable.

Q: Do you have any good recommendations for dividend stocks?

A: Yes, look at the entire cellphone towers REIT sector. That will be a growth sector next year with 5G rolling out and they have very high dividend yields. We’re going to get a significant increase in the number of cell towers thanks to 5G, and there are REITs specifically dedicated to cellphone towers. An example is Crown Castle (CCI), which has a generous 3.45% dividend yield.

Q: Are we in the final stages of a blow-off top for the stock market?

A: Yes, but blow-off tops can continue for many months, so don’t rush to sell short. However, next time the VIX gets down to 11, start buying six-month call options on the Volatility Index (VIX) at the $20 strike price. Go far out in the calendar to minimize time decay and far out of the money on strike prices to maximize your bang per buck.

Q: Gold had a nice day on Monday—is this the start of a reversal from the selling pressure?

A: No, as long as the market is pushing to new highs, which it seems to be doing—you don’t want to be anywhere near gold; wait for a better opening lower down.

Q: Are you sending Trade Alerts out on the Mad Hedge Biotech & Healthcare letter?

A: Not in the form that we see in Global Trading Dispatch or the Mad Hedge Technology Letter. Essentially, everything we’ve put out so far has been a long term buy. Most people know nothing about these sectors and we’re trying to get them into buyable names. So far, we’ve issued “BUYS” for 20 different companies; all of them have gone straight up. So, it’s really more of a long term buy-in hold situation. Since we’re in the very early days of the boom in biotech and healthcare stocks, you don’t want to leave money on the table with short term trade alerts for call spreads when there is a double or triple in the stock at hand. We are doing call spreads in the main market where most stocks are already at all-time highs in order to limit our risk.

Q: Fidelity just said that 50% of baby boomers who manage their own portfolio should rebalance it. What do you think is the best way to optimize my portfolio, as a baby boomer born in 1954?

A: You should always rebalance every year, especially when you get enormous moves in single sectors. The interesting thing this year is that everything went up, so you may not need to rebalance that much. When I say rebalance, I’m referring to rebalancing your weightings of stocks vs bonds. If you’re over 50, you want to have roughly a 50/50 ratio on those. That would suggest pairing back some of your equity weightings, increasing your bond weighting because stocks (SPY) (30% total return) have risen a lot more than bonds (TLT) (19% total return) this year.

Q: Marijuana stock Tilray (TLRY) has just had a pitiful year going from $100 to $20 and missed earnings targets for 4 for straight quarters. Could this go to zero?

A: Yes; after all, how hard is it to grow a weed? I never bought the story on the whole marijuana sector, not only because they are not allowed to participate in the financial sector. It’s an all-cash business; you hear about people moving around suitcases full of $100 bills doing deals in Oakland and Denver. I believe anybody can do this. My real estate agent is quitting his business to go into cannabis farming. Additionally, they’re getting a lot of competition from the black market where everybody used to buy their marijuana because it’s tax-free. There’s about a 40% price difference between the tax-paying legal form of marijuana and the tax-free black market where people used to get their marijuana. There’s no great value added there. It’s not like they’re designing a 96 stack microprocessor.

Q: What do you think about Ali Baba (BABA), the Chinese internet giant?

A: I love it long term. Short term, it will be subject to trade war gyration; so use the big dips to buy into it because long term we come out of this.

Global Market Comments

November 18, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE MELT UP IS ON)

(SPY), (AAPL), (UBER), (SCHW), (BA), (TSLA), (DIS), (NFLX), (TLT)

All of a sudden, and without warning, a buying panic has ensued in the stock market, breaking it out of a tedious two-year range.

The many concerns that kept investors out of stocks, like the trade war, interest rates, and a global economic slowdown, were shaken off like water off the back of a wet dog.

I could see all this coming. Even with my Mad Hedge Market Timing Index at 86, and trading as high as 91, screaming “SELL” I have been ignoring it. It usually has to spend 2-4 weeks at these elevated levels to make a real top anyway. Hedge fund compatriots who were sucked into selling too early by their own inferior in-house algorithms have been stopping out in great pain.

I’ll tell you the people who are really screwed by this move. Those who watched the economic data deteriorate all year, cut their equity allocations to the bone, and only started chasing the market upward once it broke new ground. It is a strategy that can only end in tears.

We here at Mad Hedge Fund Trader did a lot better. Followers of Global Trading Dispatch missed the breakout but bought every major dive of 2019. With double a good year’s performance in hand, we have no need to chase.

The newer Mad Hedge Technology Letter and Mad Hedge Biotech and Healthcare Letter have continued to go long pedal to the metal bringing in double-digit gains for all. Above all, we took profit on no less than four positions on Friday.

Can the market grind higher? Absolutely, yes. The world is awash in cash looking for any kind of return, and US stocks, with a (SPY) 1.81% dividend, are among the world’s highest yielding. In fact, the move could continue until the end of the year.

When will I come back in? After we get a substantial dip. Disciplines are useless unless you stick to them. In the meantime, while stocks are going crazy, there is fertile ground to harvest in other asset classes. I bought bonds (TLT) at the bottom last week and they are already performing nicely.

If you remember, I sold short, and then bought oil (USO) in September, taking advantage of a spate of volatility there. Such is the advantage of an all-asset class strategy I have been preaching and teaching for the past 12 years.

There will be no interest rate cuts in 2020, says Fed chairman Jay Powell, reading in between the lines. To do so would undermine our ability to get out of the next recession. We are still way below the 2.0% inflation target in this deflationary world.

The de-inversion of the yield curve is clearly driving stocks, with long term interest rates at last higher than short term ones. The markets are backing the recession out of the forecast. “Fear of missing out” is replacing just fear.

Consumer Prices rose faster than expected as tariffs feed into prices, up 0.4% in October. It’s going to take a lot more than that to move the needle on inflation. The YOY rate climbed to 1.8%. Also, US Producer Prices jumped, up 0.4% in October, a six-month high. It’s going to take a lot more than this to start ringing the inflation bell.

Weekly Jobless Claims soared by 14,000 to 225,000. It’s the first big jump in many months. Is the employment top in? Is this the end of the beginning or the beginning of the end?

Charles Schwab (SCHW) trading accounts soared 31%, in the wake of the commission cut to zero. What happens when you lower the price? You sell more of them. It’s a classic law of supply and demand.

Uber founder dumped stocks, as Travis Kalanick unloads $700 million worth of shares. He’s not selling because he can’t think of new ways to spend the money. It’s not exactly a “BUY” recommendation, is it? Avoid (UBER) like the plague.

Apple hit a new all-time high at $264, on three broker upgrades, with the high end reaching $290. The market capitalization tops $1.2 trillion, making it the world’s largest publicly-traded company. It looks like I’m going to have to increase my own target from a conservative $200. I made this prediction when the newsletter started a decade ago and the share traded under $20. People said I was nuts, except Steve Jobs.

The Tesla Model 3 returns to “reliable” list, from Consumer Reports. They had been taken off due to pieces falling off new cars and failing transmissions exactly at the 44,000-mile mark. It was all covered by warranty, of course. Looks like Elon is figuring out how to put these things together and stay that way. It follows an onslaught of good news about the company that has wiped out the shorts. Who is last on the quality list now? Cadillac. Buy (TSLA) on dips.

US short interest falls 1.6%, to 16.8 billion shares, as hedge funds scramble to limit losses. It’s got to be at least half the current net buying.

Disney launched its streaming service, Disney Plus, at $6.99 a month. The site crashed from overwhelming demand. It’s a problem I wish I had. Netflix (NFLX) won’t go under but their growth will be clearly impaired. Let the streaming wars begin! Buy (DIS) on dips.

US Productivity plunged sharply, down 0.3% in Q3. It’s completely a result of the trade war-induced freeze on capital spending by US businesses this year. It means we’re eating out seed corn to grow.

This was a week for the Mad Hedge Trader Alert Service to stay level. With only one position left, a bargain long in (TLT), not much else was going to happen. My long position in Boeing (BA) expired on Friday at its maximum profit point.

By the way, running out of positions at a market top is a good thing.

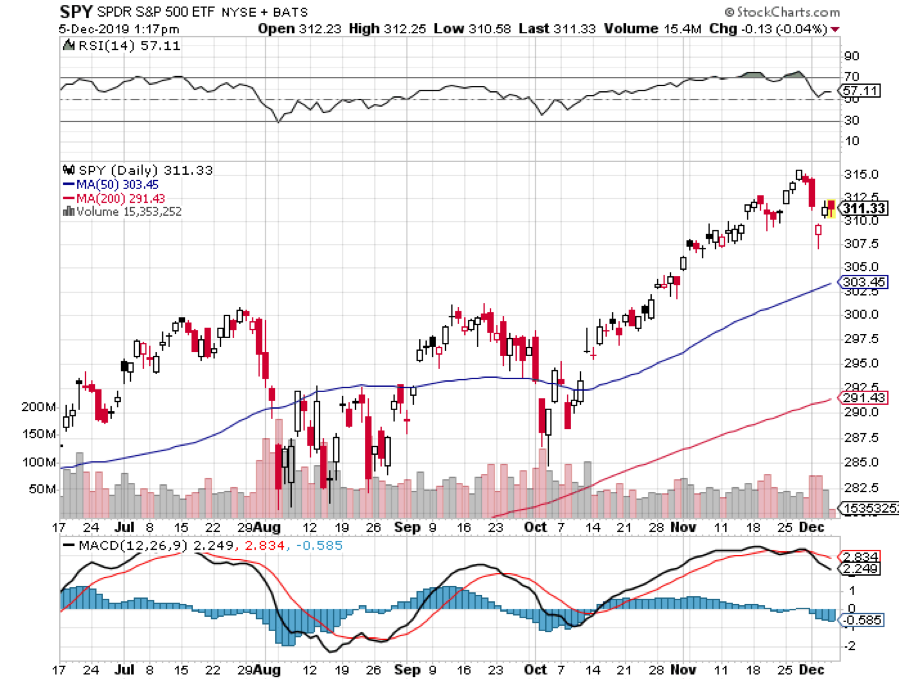

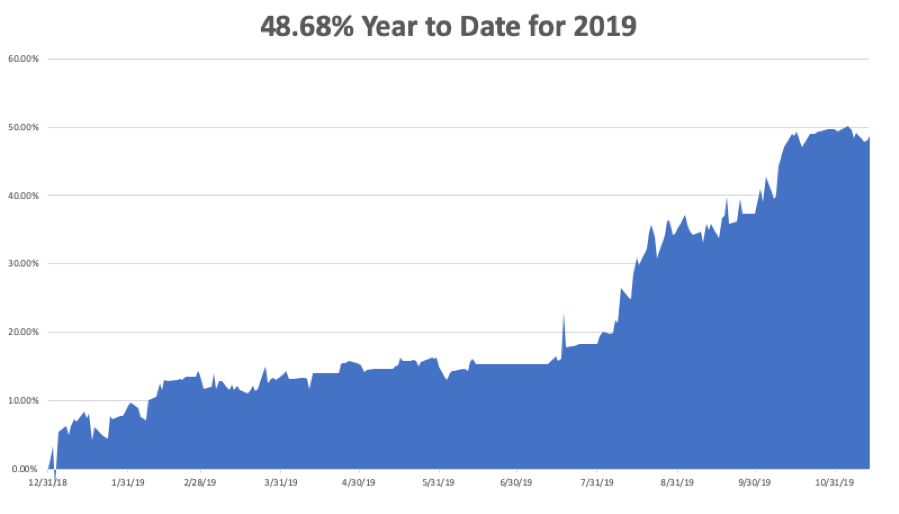

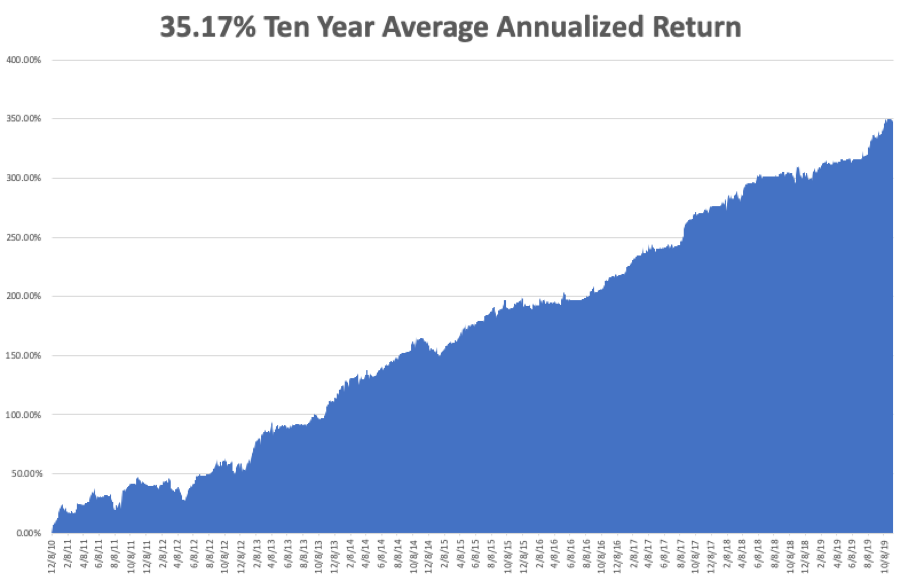

My Global Trading Dispatch performance held steady at +349.38% for the past ten years, pennies short of an all-time high. My 2019 year-to-date leveled out at +48.68%. So far in November, we are down a miniscule -0.31%. My ten-year average annualized profit held steady at +35.17%.

With my Mad Hedge Market Timing Index sitting around the sky-high 86 level, it is firmly in “SELL” territory and at a three-year high. The markets have been up in a straight line for 2 ½ months.

The coming week is pretty non-eventful of the data front after last week’s fireworks. Maybe the stock market will be non-eventful as well.

On Monday, November 18 at 11:00 AM, the US NAHB Housing Market Index for November is out.

On Tuesday, November 19 at 9:30 AM, US Housing Starts for October are released.

On Wednesday, November 20 at 2:00 PM, the Fed’s FOMC Minutes for their October meeting are published.

On Thursday, November 7, at 8:30 AM, Weekly Jobless Claims come out. At 11:00 AM the October Existing Home Sales are announced.

On Friday, November 8 at 11:00 AM, the University of Michigan Consumer Sentiment is out.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am going to see the latest Harry Potter play on Saturday, Harry Potter and the Cursed Child. It’s a reward for two kids who got straight A’s on their report cards. They seem to be strangely good at math. Maybe the apple doesn’t fall far from the tree.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 15, 2019

Fiat Lux

Featured Trade:

(NOVEMBER 13 BIWEEKLY STRATEGY WEBINAR Q&A),

(FCX), (TSLA), (FXI), (SPY), (AAPL), (M), (BA), (TLT)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader November 13 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Has the multiyear decline in commodities ended, such as for Freeport McMoRan (FCX)?

A: Yes, for the short term. However, we will almost certainly have another recession scare—or even election scare—sometime next year. That will cause a retest of the recent lows in commodities. The volatility will continue, but the long-term trend is up. The next recession will likely be so short that people will start discounting the recovery now. If you’re only looking for a 2-quarter recession and have a long-term view of your stocks, you probably want to use any kind of dips to buy now. A lot of the recent buying in Tesla (TESLA), by the way, has been of that nature.

Q: Will the US eventually drop all tariffs on Chinese imports (FXI), or do you see the US raising them?

A: I think eventually they will solve the trade war next year, right in front of the election—maybe June/July/August—so that Trump has something to run on. It’s too early to solve it now for political purposes. The whole trade war was essentially designed to depress the economy and then bring in Trump as the savior right before the election, and that has all tariffs disappearing sometime next year. By the way, some of the buying in the market now is discounting the end to the uncertainty of the trade war. So, either that or it ends when Trump leaves office—in either case, that’s 15 months off. Many big institutions think in timeframes much longer than that.

Q: Can the US consumer bring us through the holiday season to have equities (SPY) finish at all-time highs?

A: Yes, they can; I thought we might get a dip to trade off of in Oct/Nov, but we haven't gotten it. It’s looking more and more like a melt-up into year-end, even though it’s a slow-motion melt-up of 50 or 100 points a day.

Q: Will Apple (AAPL) keep going up every day forever?

A: No, don’t forget that Apple can have 40% pullbacks at any time without warning. Usually, they happen with new product launches. I would think we’re getting overextended here. If we somehow get a 10% or 20% pullback in Apple next year, I’d be jumping back into that for the product launch next September when we’ll likely hit $200, which has been my target for Apple for a very long time.

Q: Is it time to make a short term buy of beaten-down retail names like Macy’s (M)?

A: No, I am a person who trades with the long-term trend at all times. Most people are not agile or smart enough to do counter-trend trades and make money, and the risk/reward is also terrible—you make a mistake, you get killed on those. I think this company’s having a going-out-of-business sale, unless we enter a major increase in economic growth in this country, which is nowhere in the cards. If anything, I’m looking for a sharp rally to sell into. Macy’s might want to test that 200-day moving average up there at $20 at some point; that would be a great selling place. But no, we don’t want to touch the retailers right here, and retailers have been very kind to us this year on the short side.

Q: Do you see the United States US Treasury Bond Fund (TLT) as a safe-haven buy at today’s prices, or are bonds overpriced?

A: I think we’re getting the safe-haven bid as a hedge against stocks selling off. Wildly overbought Mad Hedge Market Timing Indexes are also great places to buy bonds because when you finally get the correction in the stock market, money piles into bonds, and you want to be buying the (TLT) before it does that.

Q: Is Boeing (BA) a short for the next 6 months?

A: No, I think the short play on Boeing is over. If we do get another run down to $325, take it as a gift and load the boat. I think the next major move in Boeing is to $400. Buy the dips.

Q: Do you think the Fed will cut one more time before the year is over, or will they hold off?

A: They will hold off—Powell said as much in this morning’s speech. He really said that not only will there be no more cuts this year, but next year as well, because we are essentially eating our seed corn when it comes to the next recession if we do cut rate because that means there will be no tools with which to get out of the recession.

Q: Are you seeing stocks rising to the end of the year, into the first of next year? If so, will there be a pullback during November before a final rise?

A: Yes we are seeing stocks rise to the end of the year; and you would think we will see some kind of pullback, but we have so much liquidity chasing so few stocks now, any pullbacks may be limited.

Q: (TLT) is called the iShares Barclay 20+ year bond fund. In your trade alerts, you talk about 10-year yields. How are the 10-year yields linked to the (TLT)?

A: There isn't a liquid 10-year bond ETF. There are ETFs but they’re fairly illiquid, so I put everyone into the 20-year (TLT) purely for liquidity reasons.

Q: What about going outright long on the (TLT)?

A: That’s not a bad option; the only problem with outright longs is you make no money if we grind sideways for a while, whereas with the options trade, you get in all the time decay. And we only did the December's, which have about 27 days left in them in trading time.

Q: Tesla just announced it will open a Berlin factory—what does this mean for Tesla and the share providers?

A: Well, it creates the means by which Tesla can increase its production from 400,000 cars this year to 5,000,000 cars a year in 10 years. And it’s just one other factory; expect more to come. Interestingly, their first choice was actually Great Britain, but Brexit scared them out of there.

Q: Do you think Silicon Valley should be a judge on political advertising?

A: I think Silicon Valley should not allow publication of obviously false content which they do now. That’s something the mainstream media are not allowed to do or they will get fined by the Federal Communications Commission. That ban does not apply to social media companies like Facebook (FB) and Twitter (TWTR) but should be as they are vastly more powerful than conventional media. Without it, you'll continue to see massive amounts of false information put out on the Internet. I can see the fake info clearly, but most can’t. I saw a statistic yesterday saying that roughly 50% of all information you read on the internet is false.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

This week, I had to fly off to a party given by my biggest hedge fund client at the Penthouse Suite at the Bellagio Hotel in Las Vegas. And what a party it was!

The showgirls were flowing hot and heavy, roaming magicians performed magic tricks, and there was the odd fire-breather or two. For entertainment, we were treated to rock legend Lenny Kravitz who played his signature song, American Woman.

I managed to get a few hours in private with my client, one of the wealthiest men in the world whom you would all recognize in an instant, and this is what I told him.

SELL THE NEXT BIG RALLY IN STOCKS. IT MAY BE YOUR LAST CHANCE TO GET OUT AT THE TOP BEFORE THE NEXT BEAR MARKET. ANY STOCK YOU KEEP AFTER THAT YOU WILL HAVE TO OWN FOR AT LEAST TWO YEARS AND 4-5 YEARS TO GET BACK UP TO YOUR ORIGINAL COST!

The markets are coiled for a sharp year-end rally for the following 16 reasons:

1) The S&P 500 (SPY) is more overbought than at any time in a decade, according to my Mad Hedge Marketing Timing Index at 90. Technology is the most oversold since the Dotcom bubble. We are in the early stages of the final melt-up.

2) The algorithms that drove the markets down so quickly and severely are now poised to flip to the upside.

3) Bear markets never started with real interest rates of zero (1.75% inflation rate – 1.75% ten year US Treasury yield).

4) Bear markets also don’t start with all-time high profits reported by the leading companies like Apple (AAPL), Amazon (AMZN), and Microsoft (MSFT)

5) We are now in the strongest seasonal period of market gains from November to May.

6) Sales during both Black Friday and Cyber Monday will do exceptionally well as the consumer is on fire.

7) At least $100 billion in corporate share buybacks have to kick end by yearend.

8) Risk Parity Traders, another new hedge fund strategy bedeviling the markets, are now in a position to strongly buy stocks, and sell bonds, which have gone nowhere.

9) Both month-end and year-end window-dressing purchases are not to be underestimated.

10) Much stock selling is being deferred to January when capital gains taxes are not payable for 16 months.

11) A lot of hedge fund shorts have to be covered by the end of 2019.

12) Global liquidity growth is slowing but is still enormous. There is nothing else to buy but US stocks. If you missed 2019, you get to do it all over again in 2020.

13) The collapse of oil prices from $77 to $50 a barrel has created a $200 billion surprise economic stimulus package for the US, especially for big energy consumers like transportation.

IT ALL ADDS UP TO A BIG FAT “BUY.”

I expect this rally to set up a classic head and shoulders top in the first quarter of 2019 (see chart below). Here’s where stocks fail, and we enter a new bear market. Here are ten reasons why:

1) Next year, S&P 500 earnings growth will sharply downshift from a 26% annual growth rate in 2018 to zero in 2020.

2) The upfront benefits of the corporate tax cuts will be all spent. With all the tax breaks in the world, companies won’t spend a dime if they believe the US is going into recession.

3) The massive expansion of government spending Trump brought us will be slowed by a Democratic-controlled House of Representatives, especially for defense.

4) The trade war with China will continue, cutting US growth. The Chinese are determined to outlast Donald Trump. The Middle Kingdom can take far more pain than the US, which has open elections.

5) The global synchronized recession worsens, dragging the US into the tar pit.

6) The Fed will cut interest rates any more in this cycle. You’re going to have to live on the hyper stimulus you have already received.

7) If the Fed had any doubts, they only need to look at the inflationary impacts of new duties on most imported goods.

8) A continuation of the China trade war also will trigger depression in the agricultural sector which is suffering from a China boycott that has crushed prices. Millions of tons of crops rotting in storage silos. This will spill over into a regional banking crisis.

9) The mere age of this Methuselah-like bull market at 11 years is an issue. Too many people have made too much money too easily for too long.

This all adds up to a big “SELL” sometime in the spring.

I just thought you’d like to know.

To watch the video of Lenny Kravitz playing, please click here.

Global Market Comments

November 4, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE SUMMIT)

(GM), (BA), (MSFT), (SPY), (TLT), (TSLA), (AMZN)

In 1976, I joined the American Bicentennial expedition to climb Mount Everest led by my friend and mentor, Jim Whitaker. Since I was a late addition, there was no oxygen budget for me which, in those days, was very heavy and expensive.

Still, I was encouraged to climb as far as I could without it, which turned out to be up to Base Camp II at 21,600 feet. At that altitude, you couldn’t light a cigarette as the matches went out too quickly. There just wasn’t enough oxygen.

Out of 700 men on the team, including 600 barefoot Nepalese porters, only two made it to the top. By the time I made it back to Katmandu 150 miles away, I had lost 50 pounds, taking my weight down to a scarecrow 125.

You can see the metaphor coming already.

Here I am at my screen looking at 27,500 in the Dow Average and not only am I gasping for oxygen, I am ready to pass out. My Mad Hedge Market Timing Index hit a new high for 2019 at an acrophobic 85. All of this is happening in the face of slowly eroding fundamentals and a global economic slowdown.

Could the market go higher? You betcha! At least a couple percent more by yearend. Market bottoms are easy to identify when valuations hit decade lows. Market tops are impossible to gauge because greed is unquantifiable and knows no bounds.

I’ll give you a perfect example. The US and Japan signed the Plaza Accord in 1985 calling a doubling of the value of the yen against the dollar and the eventual transportation of half of Japan’s auto production capacity to the US. We all knew this would eventually destroy the Japanese economy. Yet the Nikkei Average rose for five more years until it finally crashed.

Of course, the impetus for all of this are artificially low-interest rates, which dropped 25 basis points again last week for the third time this year.

There were with two dissents, while the December rate cut futures fall to 20%. If we get Japanese levels of interest rates, we might get a Japanese type 30-year stagnant economy.

US Q3 GDP came in at 1.9% in its most recent report, better than expected, but we are still in a serious downtrend. The economy is most likely running at a lowly 1.5% rate now. Weakness is a sure thing, now the government has run out of money for special projects. Don’t count on more with a Democratic house. It’s not the bed of roses I was promised.

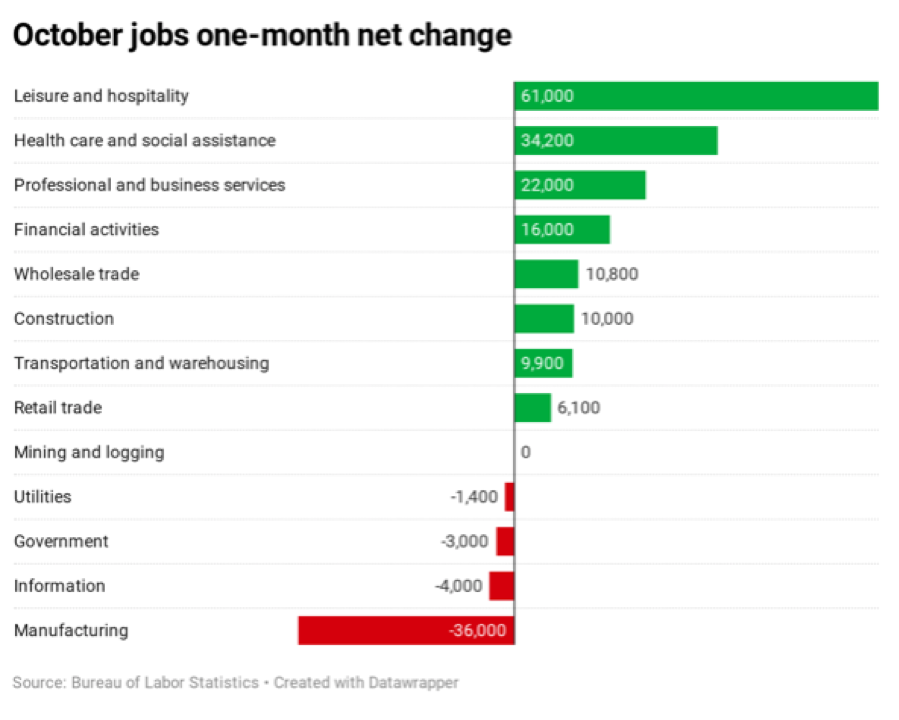

However, if there is trouble, you won’t see it in the employment data. The October Nonfarm Payroll Report surprised to the upside, at 128,000. Many expected much worse in the aftermath of the GM (GM) strike and Boeing (BA) grounding.

The headline Unemployment Rate ticked up 0.1% to 3.6%. The big gains were in Hospitality and Leisure, up a stunning 61,000, Health Care & Social Assistance, up 31,000, and Professional and Business Services, up 22,000. Manufacturing lost 36,000 jobs, a ten-year high. 20,000 temporary jobs were lost from the 2020 census wind down.

August and September were revised up by an unbelievable 95,000. The market loves these numbers.

Tesla shocked, bringing in a profit for only the third time in company history, and causing the stock to soar $55. The 100,000-unit production target within yearend looks within reach. Most importantly they opened up a new supercharger station in Incline Village, Nevada!

Tesla is now America’s most valuable car maker, beating (GM). The ideological Exxon-financed shorts have been destroyed once and for all. Buy (TSLA) on dips. There’s still a ten bagger in this one.

Amazon put out a gloomy Christmas forecast on the back of a disappointing earnings report, crushing the shares by 7%. Looks like the trade war might cause a recession next year. Q3 revenues were great, up 24% to an eye-popping $70 billion.

Good thing I took profits on the last option expiration. Poor Jeff Bezos, the abandoned son of an alcoholic circus clown, dropped $7 billion in net worth on Thursday. Buy (AMZN) on the dips.

The safest stock in the market, Microsoft (MSFT), says it’s all about the cloud. Azure revenues grew a stunning 59% in Q3. (MSFT) is now up 37% on the year. Keep buying every dip, if we ever get another one.

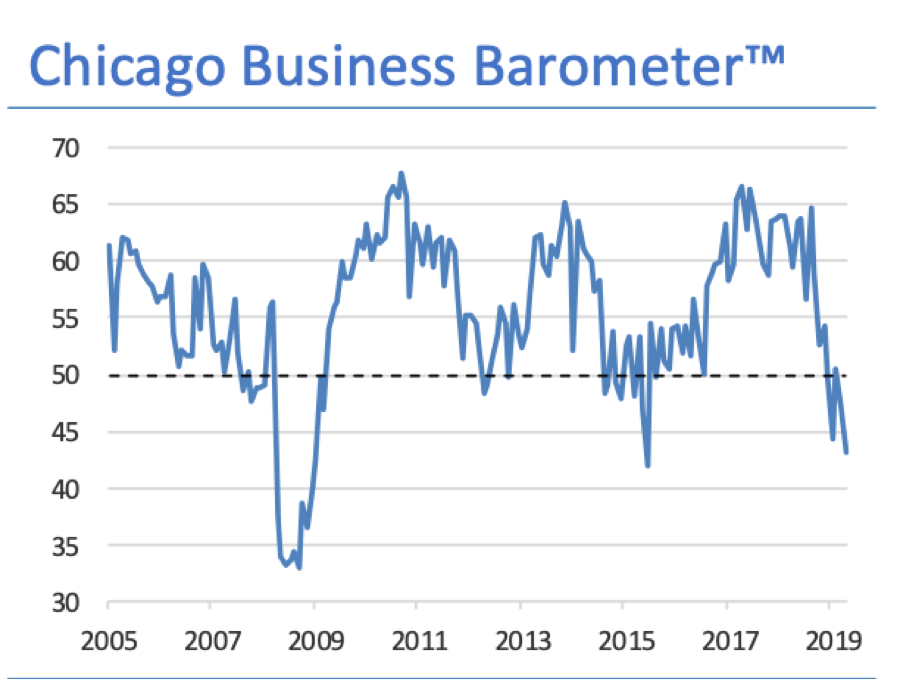

The Chicago PMI crashed, plunging from to 43.2, a four-year low. This horrific number was last seen during the recession scare of 2015. New orders have virtually disappeared, or order backlogs have vaporized. Inventories are soaring. This is the worst economic report this year and will cause a lot of economists’ hair to catch on fire.

This was a week for the Mad Hedge Trader Alert Service to stay level at an all-time high. With only two positions left, in Boeing (BA) and Tesla (TSLA), not much else was going to happen.

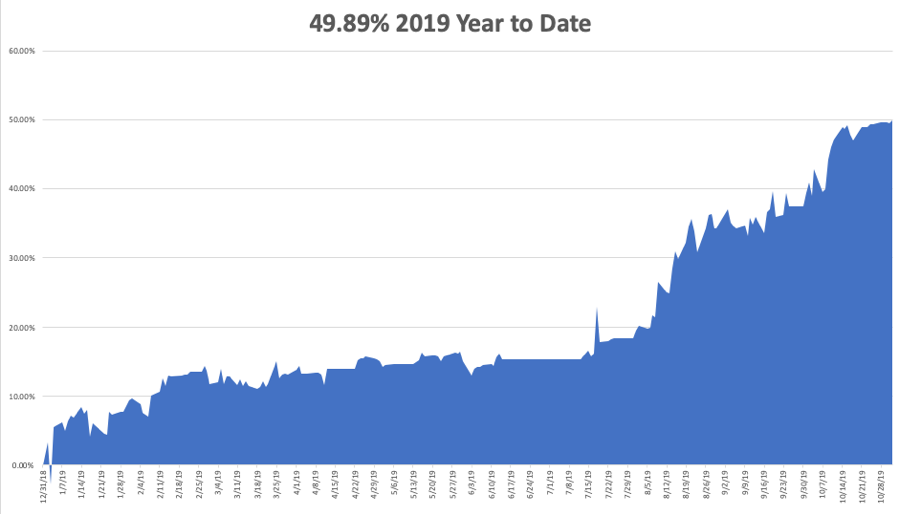

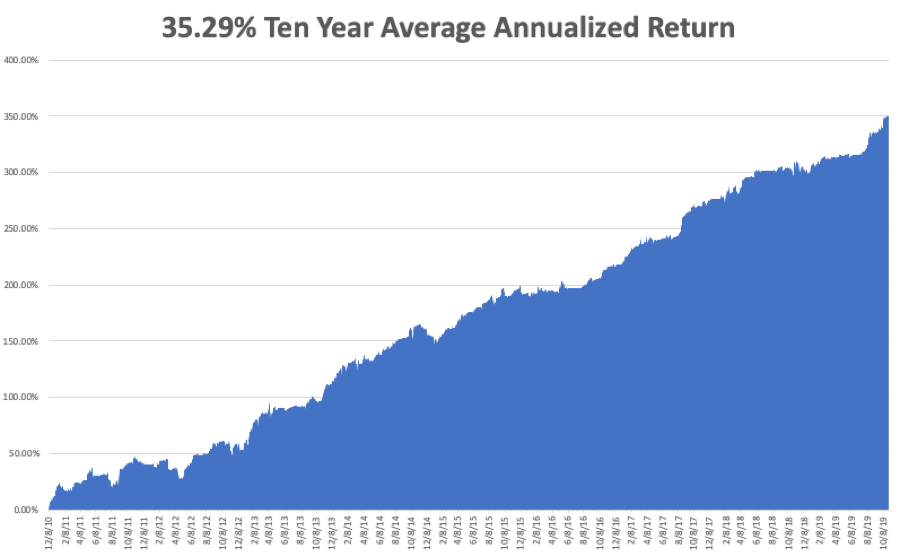

My Global Trading Dispatch reached new pinnacle of +350.03% for the past ten years and my 2019 year-to-date accelerated to +49.89%. The notoriously volatile month of October finished at +12.23%. My ten-year average annualized profit held steady at +35.29%.

The coming week is pretty non eventful of the data front after last week’s fireworks. Maybe the stock market will be non-eventful as well.

On Monday, November 4 at 8:00 AM, US Factory Orders for September are out. Uber (UBER) and Under Armor (UAA) report.

On Tuesday, November 5 at 8:00 AM, the October ISM Nonmanufacturing Index is published. US API Crude Oil Stocks are released at 2:30 PM EST. Peloton (PTON) reports.

On Wednesday, November 6, we get a raft of Fed speakers unrestrained by any impending meetings. QUALCOM (QCOM) and Humana (HUM) report.

On Thursday, November 7, there are a heavy duty series of bond auctions. Walt Disney (DIS) and Zoetis (ZTS) Report.

On Friday, November 8 at 8:00 AM, the University of Michigan Consumer Sentiment Indicator is learned.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am heading for Santa Cruz, California for the weekend to get out of the smoke and do some serious backpacking. I might even try to squeeze in a surfing lesson there. I’ll never give up.

By the way, several guests at the Tahoe conference remarked on the prominent scar on the side of my nose. That was caused by an ice ax that plunged straight through it in a fall while climbing Mount Rainer in 1967. Who patched it up and got me back down to the bottom? My friend Jim Whitaker.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 21, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE FORK IN THE ROAD),

(SPY), (TLT), (WMT), (GM), (FXI), (NFLX)