This week, I had to fly off to a party given by my biggest hedge fund client at the Penthouse Suite at the Bellagio Hotel in Las Vegas. And what a party it was!

The showgirls were flowing hot and heavy, roaming magicians performed magic tricks, and there was the odd fire-breather or two. For entertainment, we were treated to rock legend Lenny Kravitz who played his signature song, American Woman.

I managed to get a few hours in private with my client, one of the wealthiest men in the world whom you would all recognize in an instant, and this is what I told him.

SELL THE NEXT BIG RALLY IN STOCKS. IT MAY BE YOUR LAST CHANCE TO GET OUT AT THE TOP BEFORE THE NEXT BEAR MARKET. ANY STOCK YOU KEEP AFTER THAT YOU WILL HAVE TO OWN FOR AT LEAST TWO YEARS AND 4-5 YEARS TO GET BACK UP TO YOUR ORIGINAL COST!

The markets are coiled for a sharp year-end rally for the following 16 reasons:

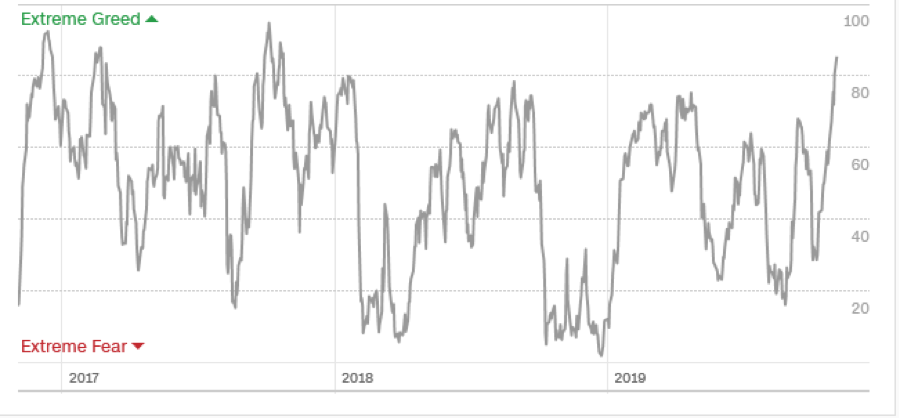

1) The S&P 500 (SPY) is more overbought than at any time in a decade, according to my Mad Hedge Marketing Timing Index at 90. Technology is the most oversold since the Dotcom bubble. We are in the early stages of the final melt-up.

2) The algorithms that drove the markets down so quickly and severely are now poised to flip to the upside.

3) Bear markets never started with real interest rates of zero (1.75% inflation rate – 1.75% ten year US Treasury yield).

4) Bear markets also don’t start with all-time high profits reported by the leading companies like Apple (AAPL), Amazon (AMZN), and Microsoft (MSFT)

5) We are now in the strongest seasonal period of market gains from November to May.

6) Sales during both Black Friday and Cyber Monday will do exceptionally well as the consumer is on fire.

7) At least $100 billion in corporate share buybacks have to kick end by yearend.

8) Risk Parity Traders, another new hedge fund strategy bedeviling the markets, are now in a position to strongly buy stocks, and sell bonds, which have gone nowhere.

9) Both month-end and year-end window-dressing purchases are not to be underestimated.

10) Much stock selling is being deferred to January when capital gains taxes are not payable for 16 months.

11) A lot of hedge fund shorts have to be covered by the end of 2019.

12) Global liquidity growth is slowing but is still enormous. There is nothing else to buy but US stocks. If you missed 2019, you get to do it all over again in 2020.

13) The collapse of oil prices from $77 to $50 a barrel has created a $200 billion surprise economic stimulus package for the US, especially for big energy consumers like transportation.

IT ALL ADDS UP TO A BIG FAT “BUY.”

I expect this rally to set up a classic head and shoulders top in the first quarter of 2019 (see chart below). Here’s where stocks fail, and we enter a new bear market. Here are ten reasons why:

1) Next year, S&P 500 earnings growth will sharply downshift from a 26% annual growth rate in 2018 to zero in 2020.

2) The upfront benefits of the corporate tax cuts will be all spent. With all the tax breaks in the world, companies won’t spend a dime if they believe the US is going into recession.

3) The massive expansion of government spending Trump brought us will be slowed by a Democratic-controlled House of Representatives, especially for defense.

4) The trade war with China will continue, cutting US growth. The Chinese are determined to outlast Donald Trump. The Middle Kingdom can take far more pain than the US, which has open elections.

5) The global synchronized recession worsens, dragging the US into the tar pit.

6) The Fed will cut interest rates any more in this cycle. You’re going to have to live on the hyper stimulus you have already received.

7) If the Fed had any doubts, they only need to look at the inflationary impacts of new duties on most imported goods.

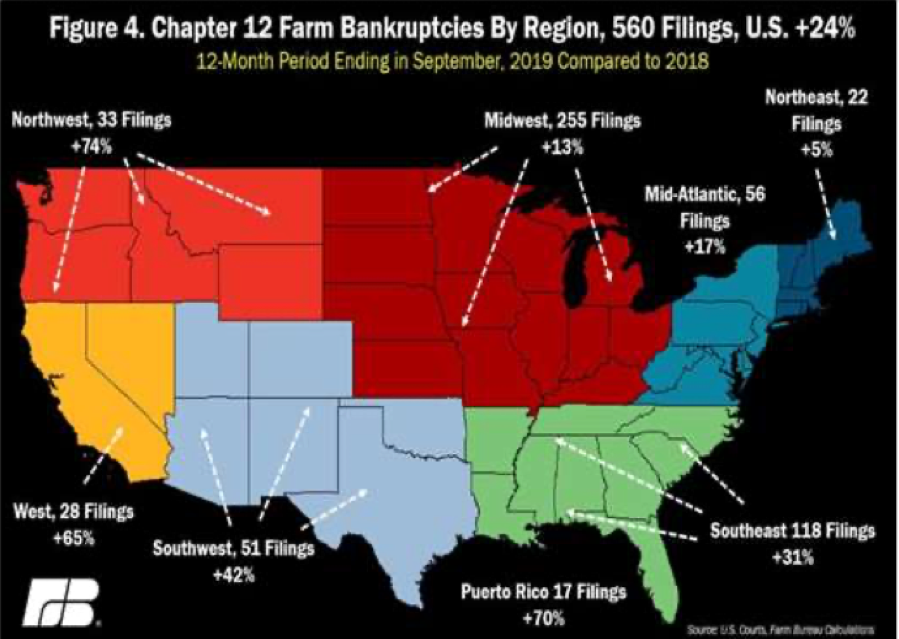

8) A continuation of the China trade war also will trigger depression in the agricultural sector which is suffering from a China boycott that has crushed prices. Millions of tons of crops rotting in storage silos. This will spill over into a regional banking crisis.

9) The mere age of this Methuselah-like bull market at 11 years is an issue. Too many people have made too much money too easily for too long.

This all adds up to a big “SELL” sometime in the spring.

I just thought you’d like to know.

To watch the video of Lenny Kravitz playing, please click here.