Global Market Comments

April 16, 2019

Fiat Lux

Featured Trade:

(WHY YOU WILL LOSE YOU JOB IN THE NEXT FIVE YEARS,

AND WHAT TO DO ABOUT IT),

(BLK)

Global Market Comments

April 16, 2019

Fiat Lux

Featured Trade:

(WHY YOU WILL LOSE YOU JOB IN THE NEXT FIVE YEARS,

AND WHAT TO DO ABOUT IT),

(BLK)

Global Market Comments

April 15, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR QE IS BACK!),

(SPY), (TLT), (TSLA), (DIS), (FCX), (GOOG), (MSFT), (AMZN)

Let me warn you in advance that I am only going off drugs long enough to write this newsletter.

This year’s flu has finally laid me low and let me tell you it is a real killer. Perhaps it is my advanced age that has magnified its effects. Then I developed an allergic reaction to the flu medicine I was taking. For a couple of days there, I was looking like the Michelin Man.

However, I did have a lot of time to read research. And what I learned was sobering.

For a start, we are fully back to a quantitative easing market. In one fell swoop, the Fed went from an expectation of four interest rate hikes in 2019 to none. By ending quantitative tightening early, it has cut the amount of cash it is withdrawing from the financial system from $4.3 trillion to only $1.5 trillion.

The Fed is in effect reflating the bubble one more time. And what do you do in a QE-driven economy. YOU BUY EVERYTHING! This explains why stocks, bonds, commodities, and energy have all been marching upward in unison this year even though that is supposed to be theoretically impossible.

Yes, the decade long liquidity-driven bull market may have another leg up to go.

A higher high inevitably leads to a lower low. The trades you are executing now may be akin to picking up pennies in front of a steam roller. We are clearly planting the seeds of the next financial crisis. But for now, the pain trade is clearly to the upside.

Those of who who traded through the dotcom bubble are seeing déjà vu all over again. Huge money-losing tech companies are now floating IPOs on a daily basis. This too will end in tears, which is why I have recommended to followers to avoid all of them. This is a sucker’s game.

There is a cloud behind this silver lining. After a ballistic 21.43% move in the Dow Average in four months, markets are trading as if risk is a thing of the past. The euphoria is here and complacency rules. That means the number of new possible low risk/high return trades out there has fallen to zero.

There is another cloud to worry about. The more excess stimulus the Fed provides the economy now, the fewer resources it will have to get us out of the next recession, which might be only a year off. As a result, everyone is long but extremely nervous. They are still participating in the party but are standing next to the exit door. Pent up volatility is building like a volcano ready to explode.

The other great revelation is that markets have been trading extremely short term in nature, only one quarter ahead of what the real economy is doing. So, a stock market meltdown in Q4 2018 discounted a collapsing GDP growth in Q1 2019 of a 1% rate or less. That is down 80% from a year ago peak.

The ultra-strong market in Q1 is anticipating an economic rebound in Q2, After that, who knows?

That’s why I am moving both of my trading portfolios for Global Trading Dispatch and the Mad Hedge Technology Letter to 100% cash positions in the coming week.

Last week was the week when Walt Disney (DIS) morphed from being a has-been media stock hobbled by a failing holding in ESPN to a dynamic company that is suddenly taking over the world. The reward was an eye-popping 25% move in three weeks, which we caught.

Copper demand is rocketing, off of soaring global electric car production. Each vehicle needs 22 pounds of the red metal, and 4 million have been built so far. That number reached 5 million by June. Take a second bite of the apple with (FCX) as well.

General Electric got slaughtered again, with an earnings downgrade from Morgan Stanley. It will take years to sort out this mess. Avoid (GE).

The 30-year fixed rate mortgage plunged to 4.03% and may save the spring selling season for residential real estate.

Apple Topped $200. It looks like the market is finally buying the services story. Stand aside for the short term. It’s had a great run, up 42% from the December low. I’m waiting for 5G until I buy my next iPhone, probably next year.

The Mad Hedge Fund Trader hit a new all-time high briefly, up 15.46% year to date, and beating the pants off the Dow Average. Good thing I didn’t buy the bearish argument. There’s too much cash floating around the world. However, my downside hedges in Disney and Tesla cost me some money when I stopped out. I was late by a day.

We are taking profits on a six-month peak of 13 positions across the GTD and Tech Letter services and will wait for markets to tell us what to do next.

April is so far down -1.50%, as my downside hedges in Tesla (TSLA) and Disney (DIS) cost me some sofa change. My 2019 year to date return retreated to +13.92%, paring my trailing one-year return back up to +27.22%.

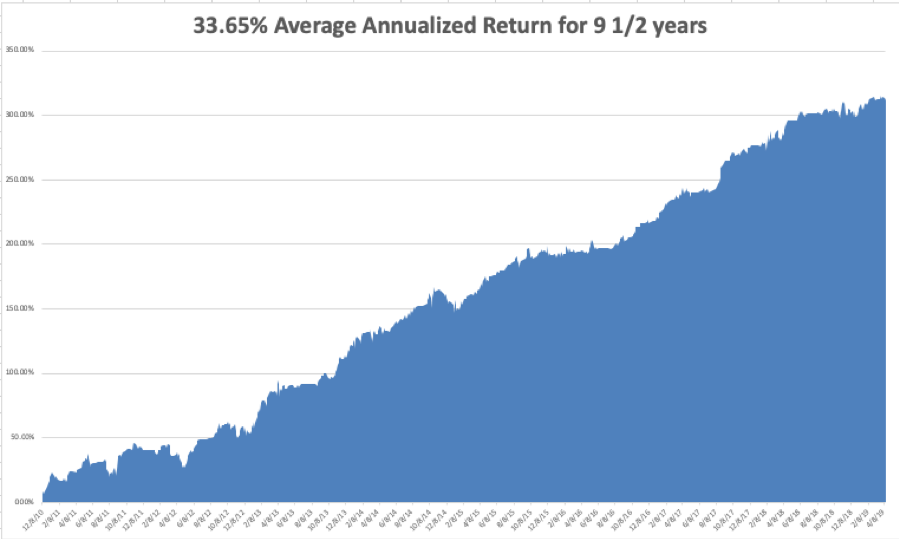

My nine and a half year return backed off to +314.06%. The average annualized return appreciated to +33.65%. I am now 100% in cash.

The Mad Hedge Technology Letter has gone ballistic, with an aggressive and unhedged 30% long which expires this week. It is maintaining positions in Microsoft (MSFT), Alphabet (GOOGL), and Amazon (AMZN), which are clearly going to new highs.

It’s going to be a dull week on the data front after last week’s fireworks.

On Monday, April 15 at 8:30 AM, we get the April Empire State Index. Citibank (C) and Goldman Sachs (GS) report.

On Tuesday, April 16, 9:15 AM EST, we learn March Industrial Production. Netflix (NFLX) and IBM (IBM) report.

On Wednesday, April 17 at 2:00 PM, we get the Fed Beige Book Indicators. Morgan Stanley reports (MS).

On Thursday, April 18 at 8:30 the Weekly Jobless Claims are produced. At 10:00 AM EST, we obtain the March Index of Leading Economic Indicators. American Express (AXP) reports.

On Friday, April 19 at 8:30 AM, the markets are closed for Good Friday.

As for me, I am staying planted in my bed reading up on research and watching HBO until I kick this flu. After that, I should be good for the rest of the year.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 8, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR THE FLIP-FLOPPING MARKET),

(SPY), (TLT), (TSLA), (BA), (LUV), (DAL)

Easy come easy go.

Flip flop, flip flop.

Up until March 25, the bond market was discounting a 2019 recession. Bonds soared and stocks ground sideways. Exactly on that day, it pushed that recession out a year to 2020.

For that was the day that bond prices hit a multiyear peak and ten-year US Treasury yields (TLT) plunged all the way to 2.33%. Since then, interest rates have gone straight up, to 2.52% as of today.

There was also another interesting turn of the calendar. Markets now seem to be discounting economic activity a quarter ahead. So, the 20% nosedive we saw in stocks in Q4 anticipated a melting Q1 for the economy, which is thought to come in under 1%.

What happens next? A rebounding stock market in Q2 is expecting an economic bounce back in Q2 and Q3. What follows is anyone’s guess. Either continuing trade wars drag us back into a global recession and the stock market gives up the $4,500 points it just gained.

Or the wars end and we continue with a slow 2% GDP growth rate and the market grinds up slowly, maybe 5% a year.

Which leads us to the current quandary besieging strategists and economists around the world. Why is the government pressing for large interest rate cuts in the face of a growing economy and joblessness at record lows?

Of course, you have to ask the question of “what does the president know that we don’t.” The only conceivable reason for a sharp cut in interest rates during “the strongest economy in American history” is that the China trade talks are not going as well as advertised.

In fact, they might not be happening at all. Witness the ever-failing deadlines that always seem just beyond grasp. The proposed rate cut might be damage control in advance of failed trade talks that would certainly lead to a stock market crash, the only known measure of the administration view of the economy.

This also explains why politicization of the Fed is moving forward at an unprecedented rate. You can include political hack Stephen Moore who called for interest rate RISES during the entire eight years of the Obama administration but now wants them taken to zero in the face of an exploding national debt. There is also presidential candidate Herman Cain.

Both want the US to return to the gold standard which will almost certainly cause another Great Depression (that’s why we went off it last time, first in 1933 and finally in 1971). The problem with gold is that it’s finite. Economic growth would be tied to the amount of new gold mined every year where supplies have been FALLING for a decade.

The problem with politicization of the Fed is that once the genie is out of the bottle, it is out for good. BOTH parties will use interest rates to manipulate election outcomes in perpetuity. The independence of the Fed will be a thing of the past.

It has suddenly become a binary world. It either is, or it isn’t.

Positive China rumors lifted markets all week. Is this the upside breakout we’ve been looking for? Buy (FXI). While US markets are up 12% so far in 2019, Chinese ones have doubled that.

The Semiconductor Index, far and away the most China-sensitive sector of the market, hit a new all-time high. Advanced Micro Devices (AMD), a Mad Hedge favorite, soared 9% in one day. It’s the future so why not? This is in the face of semiconductor demand and prices that are still collapsing. Buy dips.

Verizon beat the world with its surprise 5G rollout. It’s really all about bragging rights as it is available only in Chicago and Minneapolis and it will take time for 5G phones to get to the store. 5G iPhones are not expected until 2020. Still, I can’t WAIT to download the next Star Wars movie on my phone in only ten seconds.

US auto sales were terrible in Q1, the worst quarter in a decade, and continue to die a horrible death. General Motors (GM) suffered a 7% decline, with Silverado pickups off 16% and Suburban SUVs plunging 25%. Is this a prelude to the Q1 GDP number? Risk is rising. You have to wonder how much electric cars are eating their lunch, which now accounts for 4% of all new US sales.

Tesla (TSLA) disappointed big time, and the stock dove $30. Q1 deliveries came in at only 63,000 as I expected, compared to 90,700 in Q4, down 30.5%. I knew it would be a bad number but got squeezed out of my short the day before for a small loss. That’s show business. It’s all about damping the volatility of profits.

By cutting the electric car subsidy by half from $7,500 in 2019 and to zero in 2020, the administration seems intent on putting Tesla out of business at any cost. I hear the company has installed a revolving door at its Fremont headquarters to facilitate the daily visits by the Justice Department and the SEC. Did I mention that the oil industry sees Tesla as an existential threat?

The March Nonfarm Payroll Report rebounded to a healthy 196,000, just under the 110-month average. Weekly Jobless Claims dropped to New 49-Year Low. Whatever the problems the economy has, it’s not with job creation. But at what cost? Of course, we have to cut interest rates!

Boeing successfully tested new software, even taking the CEO for a ride. Maybe it will work this time. Airlines will love it. (BA) shares have already made back half their $80 losses since the recent crash and we caught the entire move. Buy (BA), (DAL), and (LUV).

The Mad Hedge Fund Trader hit a new all-time high briefly, up 15.46% year to date, and beating the pants off the Dow Average. Good thing I didn’t buy the bearish argument. There’s too much cash floating around the world. However, my downside hedges in Disney and Tesla cost me some money when I stopped out. I was late by a day.

We are taking profits on a six-month peak of 13 positions across the GTD and Tech Letter services and will wait for markets to tell us what to do next.

March turned positive in a final burst, up +1.78%. April is so far down -1.76%. My 2019 year to date return retreated to +13.69%, paring my trailing one-year return back up to +26.59%.

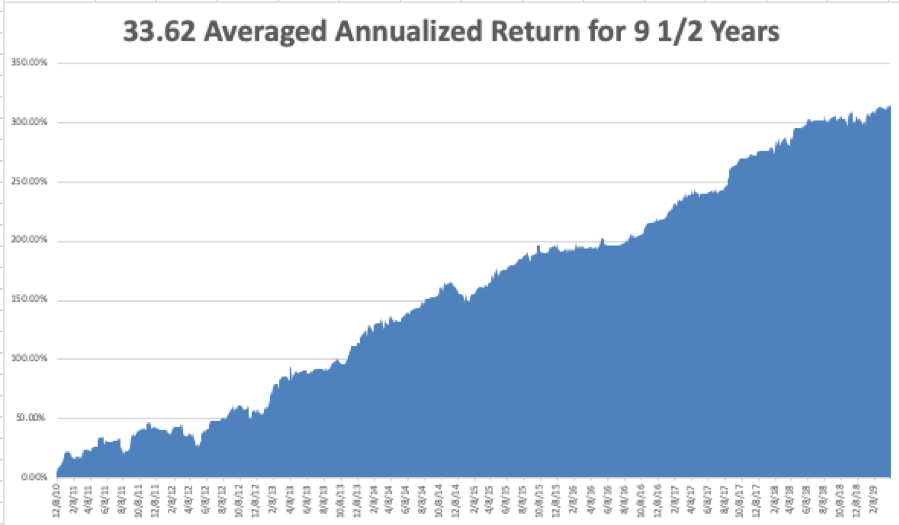

My nine and a half year return recovered to +313.83%, pennies short of a new all-time high. The average annualized return appreciated to +33.62%. I am now 80% in cash and 20% long, and my entire portfolio expires at the April 18 option expiration day in 9 trading days.

The Mad Hedge Technology Letter has gone ballistic, with an aggressive and unhedged 40% long, rising in value almost every day. It is maintaining positions in Microsoft (MSFT), Alphabet (GOOGL), and PayPal (PYPL), and Amazon (AMZN), which are clearly going to new highs.

It’s going to be a dull week on the data front after last week’s fireworks.

On Monday, April 8 at 10:00 AM, February Factory Orders are released.

On Tuesday, April 9, 6:00 AM EST, the March NFIB Small Business Optimism Index is published.

On Wednesday, April 10 at 8:30 AM, we get the March Consumer Price Index.

On Thursday, April 11 at 8:30 AM EST, the Weekly Jobless Claims are announced. The March Producer Price Index is printed at the same time.

On Friday, April 12 at 10:00 AM, the April Consumer Sentiment Index is published.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I have two hours until the next snow storm pounds the High Sierras and closes Donner Pass. So I have to pack up and head back to San Francisco.

But I have to get a haircut first.

Incline Village, Nevada is the only place in the world where you can get a haircut from a 78-year-old retired Marine Master Sargent, Louie’s First Class Barbers. Civilian barbers can never grasp the concept of “high and tight with a shadow”, a cut only combat pilots are entitled to. He’ll regale me with stories of the Old Corps the whole time he is clipping away. I wouldn’t miss it for the world.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 5, 2019

Fiat Lux

Featured Trade:

(APRIL 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (VIX), (TSLA), (BA), (FXB), (AMZN), (IWM), (EWU)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: I’ve gotten a lot of newsletters but not many trades. Why is that?

A: Perfect trades do not happen every day of the year. They happen a few times a year and they tend to bunch up. Most time in the market is spent waiting for an entry point and then piling on 5 or 10 trades rapidly. We’re letting our profits run and waiting for new trades to open up, so just be patient and we’ll get you more trades than you can chew on.

If you have to ask this question, you are probably overtrading. The goal is to make yourself rich, not your broker. The other newsletters that offer a trade alert every day don’t publish their performance as I do and lose money for their followers hand over fist.

Q: Are we on track for a market peak in May?

A: Yes; if we keep climbing up, eventually hitting new highs this month, then we are setting up perfectly for a pretty sharp pullback around May 10th. That would be a good time to get rid of all your longs and put on some short positions, certainly deep in the money put spreads—we’ll be knocking quite a few of those out in the end of April/beginning of May.

Q: Are you worried about the Russell 2000 (IWM) climb?

A: I’m not. If you look at the chart, every up move has been weak, and every down move has been strong. Looking at the chart, it’s still in a clear downtrend dragging all the other markets, and this is because small-cap stocks do poorly in recessions or market pullbacks.

Q: How severe and how long do you see the coming bear market being?

A: If history repeats itself, then it’s going to be rather shallow. The last move down was only three months long and that stunned a lot of people who were expecting a more extreme pullback. I don’t see conditions in place that indicate a radically deep pullback—25% at most and 6-12 months in duration, which won’t be enough to liquidate your portfolio and justify the costs of getting out now and trying to get back in later. They key thing is that there are no systemic threats to the market other than the exploding levels of government borrowing.

Q: If you had the Tesla (TSLA) April $310-$330 vertical bear put spread, would you keep it?

A: Probably, yes, because you have a $15 cushion against a good news surprise and a lot less at risk. I got out of my Tesla (TSLA) April $300-$320 vertical bear put spread because my safety cushion shrank to only $5 and the risk/reward turned sharply against me.

Q: Should we be buying the Volatility Index (VIX) here for protection?

A: Not yet; we still have enough momentum in the stock market to hit all-time highs. After that, you really want to start looking at the VIX hard, especially if we get down to the $12 level. So good thinking, just not quite yet—as we know in the market, timing is everything.

Q: Are you getting nervous about the short Disney (DIS) calls?

A: I’m always nervous, every day of the year about every position, and yes, I’m watching them. You are paying me to be nervous so you can go play golf. We may take a small hit on the calls if the stock keeps rising, but that will be offset by a bigger gain on the call spread we’re long against.

Q: When is the quarterly option expiration?

A: It was on March 15 and the next one is June 21. This is an off-month expiration coming up on April 18th, and that’s only 12 trading days away.

Q: If you get a hard Brexit (FXB) in the next few weeks, what will happen to the pound?

A: It’s risen about 10% in the last few weeks on hopes of a Brexit outright failure. If that doesn't happen, the pound will get absolutely slaughtered.

Q: If China (FXI) is stimulating their economy, will that eventually help the U.S.?

A: Stimulus anywhere in the world always gets back to the U.S. because we’re the world’s largest market. So, yes, it will be positive.

Q: Would you consider trading UK stocks under Brexit fail?

A: Yes, and there is a UK stock ETF, the iShares MSCI United Kingdom ETF(EWU) and you’re looking at a 20%-25% rise in the British stock market if they completely give up on Brexit or just have another election.

Q: What are your thoughts on the China trade war?

A: The Chinese are in no rush to settle; that’s why we keep missing deadline after deadline and all the positive rumors are coming from the U.S. side. It’s looking more like a photo op trade deal than an actual one.

Q: If we get a top in stocks in May, how far do you expect (SPY) to go?

A: Not far; maybe 5% or 10%, you just have to allow all the recent players who got in to get out again, and if the economy slows to, say, a 1% rate in Q1, that’s not a panicky type market. That’s a 10% correction market and what we’ll probably get. If the economy then improves in Q2 and Q3, then we may go back up again to new highs. We seem to have a three quarter a year stock market and therefore, a three quarter a year stock market. Q1 is always a write off for the economy.

Q: Do you still like Amazon (AMZN)?

A: Absolutely, yes—it’s going to new highs. And it’s also starting to make a move on the food market, cutting prices at Whole Foods, which it owns, for the 3rd time this year. So, it’s moving on several fronts now, including healthcare. There’s at least a double in the company long term from these levels, and a triple if they break the company up.

Q: If you bought the stock in Boeing (BA) instead of the option spread, would you stay long?

A: I would, yes. It’s a great company and there's an easy 10% move in that stock once they get the 737 MAX back off the ground again which they should do within the month.

Q: What do you think about food stocks with big name brands like Hershey (HSY)?

A: I’ve never really liked the food industry. It’s really a low margin industry. You’re looking at 2% a year earnings growth against the big food companies vs 20% a year growth in tech which is why I stick with tech. My advice is always to focus on the few sectors that are the best 5% of the market and leave the dross for the index funds.

Q: With the current bullish wave in the market (SPY), what sector/stocks do you think have the most momentum to break out another 10% to 15% gain in the next one to three months?

A: The next 10% to 15% in the market will only happen after we drop 5-10% first. I believe this is the last 5% move of the China trade deal rally and after that, markets will fall or go to sleep for six months.

Q: Do you expect 2019 to be more like 2018 or 2017? We know you are predicting the (SPX) will hit an all-time high of 3000 in 2019. Do you think it zooms up to a blow-off top in Q2/Q3 and then pulls back in Q4, like 2018? Or, do you expect a steadier ascent with minor pullbacks along the way (like 2017), closing at or near the year's highs on Dec 31? This guidance will really help.

A: I think we have made most of the gains for 2019. Only the tag ends are lifted. We have already hit the upside targets for most strategists, and mine is only 7% higher. After that, there is a whole lot of boring ahead of us for 2019 and the (VIX) should drop to $9. After complaining about horrendous market volatility in December, traders will beg for volatility.

Good Luck and Good Trading

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Global Market Comments

April 4, 2019

Fiat Lux

Featured Trade:

(TEN REASONS WHY STOCKS CAN’T SELL OFF BIG TIME),

(SPY)

(SCAM OF THE MONTH CLUB)

Global Market Comments

March 25, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR GAME CHANGER)

(SPY), (TLT), (BIIB), (GOOG), (BA), (AAPL), (VIX), (USO)

“When the facts change, I change. What do you do sir?” is a famous quote from the great economist John Maynard Keynes which I keep taped to the top of my monitor and constantly refer to.

The facts certainly changed on Wednesday when the Federal Reserve announced a change in the facts for the ages. Not only did governor Jay Powell announce that there would be no further rate increases in 2019.

He also indicated that the Fed would end its balance sheet unwind much earlier than expected. That has the effect of injecting $2.7 trillion into the US financial system and is the equivalent of two surprise interest rate CUTS.

The shocking move opens the way for stocks to trade up to new all-time high, with or without a China trade deal. Only the resumption of all-out hostilities, like the imposition of new across the board 25% tariffs, would pee on this parade.

As if we didn’t have enough to discount into the market in one shot. I held publication of this letter until Sunday night when we could learn more about the conclusion of the Mueller Report. There was no collusion with Russia and there will be no obstruction of justice prosecution.

However, the report did not end the president’s legal woes as it opened up a dozen new lines of investigation that will go on for years. The market could care less.

At the beginning of the year, I listed my “Five Surprises for 2019”. They were:

*The government shutdown ended and the Fed makes no move to raise interest rates

*The Chinese trade war ends

*The US makes no moves to impeach the Trump, focusing on domestic issues instead

*Britain votes to rejoin Europe

*The Mueller investigation concludes that he has an unpaid parking ticket in

NY from 1974 and that’s it

Notice that three of five predictions listed in red have already come true and the remaining two could transpire in coming weeks or months. All of the above are HUGELY risk positive and have triggered a MONSTER Global STOCK RALLY

Make hay while the sun shines because what always follows a higher high? A lower low.

The Fed eased again by cutting short their balance sheet unwind and ending quantitative tightening early. It amounts to two surprise interest rate cuts and is hugely “RISK ON”. New highs in stocks beckon. This is a game changer.

Bonds soared and rates crashed taking ten-year US Treasury bond yields down to an eye-popping 2.42%, still reacting to the Wednesday Fed comments. This is the final nail in the bond bear market as global quantitative easing comes back with a vengeance. German ten years bonds turn negative for the first time since 2016.

Interest rates inverted with short term rates higher than long term ones for the first time since 2008. That means a recession starts in a year and the stock market starts discounting that in three months.

Interest rates are now the big driver and everything else like the economy, valuations, and earnings are meaningless. Foreign interest rates falling faster than ours making US assets the most attractive in the world. BUY EVERYTHING, including stocks AND bonds.

Biogen blew up canceling their phase three trials for the Alzheimer drug Aducanumab. This is the worst-case scenario for a biotech drug and the stock is down a staggering 30%. Some $12 billion in prospective income is down the toilet. Avoid (BIIB) until the dust settles.

Europe fined Google $1.7 billion, in the third major penalty in three years. Clearly, there’s a “not invented here” mentality going on. It's sofa change to the giant search company. Buy (GOOG) on the dip.

More headaches for Boeing came down the pike. What can go wrong with a company that has grounded its largest selling product? Answer: they get criminally prosecuted. That was the unhappy news that hit Boeing (BA), knocking another $7 off the shares. It can’t get any worse than this, can it? Buy this dip in (BA).

Indonesia canceled a massive 737 order for 49 planes, slapping the stock on the face for $9. Apparently, they are unwilling to wait for the software fix. Buy the dip in (BA).

Oil prices hit a new four-month high at $58 a barrel as OPEC production caps work and Venezuela melts down. At a certain point, high energy prices are going to hurt the economy. Buy (USO) on dips.

The CBOE suspended bitcoin futures due to low volume and weak demand. It could be a fatal blow for the troubled cryptocurrency. Avoid bitcoin and all other cryptos. They’re a Ponzi scheme.

Equity weightings hit a 2 ½ year low as professional institutional money managers sell into the rally. They are overweight long defensive REITs and short European stocks. Watch out for the reversal.

December stock sellers are now March buyers. Expect this to lead to a higher high, then a lower low. Volatility is coiling. Don’t forget to sit down when the music stops playing.

Volatility hits a six-month low with the $12 handle revisited once again down from $30. (VIX) could get back to $9 before this is all over. Avoid (VIX) as the time decay will kill you.

Weak factory orders crush the market, down 450 points at the low. Terrible economic data is not new these days. But it ain’t over yet. Buy the dip.

The Mad Hedge Fund Trader was up slightly on the week. That’s fine, given the horrific 450 point meltdown the market suffered on Friday. We might have closed unchanged on the day but for rumors that the Mueller Report would be imminently released.

March is still negative, down -1.54%. My 2019 year to date return retreated to +11.74%, boosting my trailing one-year return back up to +24.86%.

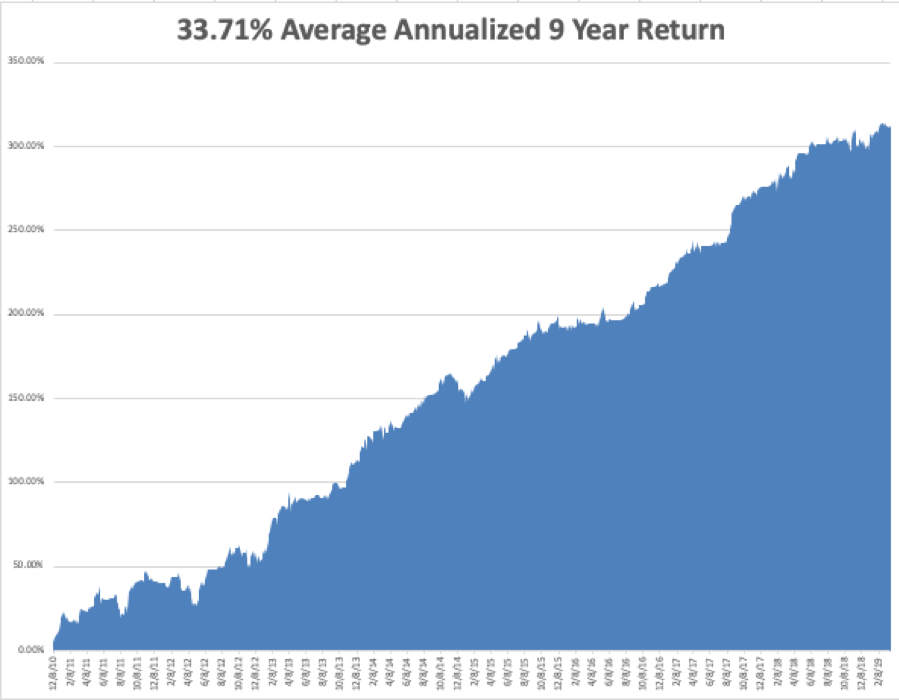

My nine-year return recovered to +311.88%. The average annualized return appreciated to +33.71%. I am now 40% in cash, 40% long and 20% short, and my entire portfolio expires at the April 18 option expiration day in 14 trading days.

The Mad Hedge Technology Letter used the weakness to scale back into positions in Microsoft (MSFT), Alphabet (GOOGL), and PayPal (PYPL), which are clearly going to new highs.

The coming week will be a big one for data from the real estate industry.

On Monday, March 25, Apple will take another great leap into services, probably announcing a new video streaming service to compete with Netflix and Walt Disney.

On Tuesday, March 26, 9:00 AM EST, we get a new Case Shiller CoreLogic National Home Price index which will almost certainly show a decline.

On Wednesday, March 27 at 8:30 AM, we get new Trade Deficit figures for January which have lately become a big deal.

Thursday, March 28 at 8:30 AM EST, the Weekly Jobless Claims are announced. We also then get another revision for Q4 GDP which will likely come down.

On Friday, March 29 at 10:00 AM, we get February New Home Sales. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’m praying that it stops snowing in the High Sierras long enough for me to get over Donner Pass and spend the spring at Lake Tahoe. We are at 50 feet for the season, the second highest on record.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader