Mad Hedge Technology Letter

October 15, 2018

Fiat Lux

Featured Trade:

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

Mad Hedge Technology Letter

October 15, 2018

Fiat Lux

Featured Trade:

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

Interest rates triggered a tsunami wave of selling tearing apart the tech sector with a vicious profit-taking few trading days.

No doubt that asset managers are frantically locking in profits for the rest of the year and protecting ebullient performance from a year to remember.

This week shouldn’t deter investors from picking up bargains that were non-existent for most of the year because the bulk of the highest quality tech names churned higher with lurching momentum.

Here are the names of five of the best stocks to slip into your portfolio in no particular order once the madness subsides.

Apple

Steve Job’s creation is weathering the gale-fore storm quite well. Apple has been on a tear reconfirming its smooth pivot to a software-tilted tech company. The timing is perfect as China has enhanced their smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality. That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has their supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $100 billion in shares by the end of the year. Get into this stock while you can as entry points are few and far between.

Amazon

This is the best company in America hands down and commands 5% of total American retail sales or 49% of American e-commerce sales.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then oozing innovation and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft

The optics in 2018 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter and that is a good thing in 2018.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon-effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business.

Microsoft Azure grew 87% YOY last quarter. The previous quarter saw Azure rocket by 98%. Shares are cheaper than Amazon and almost as potent.

Square

CEO Jack Dorsey is doing everything right at this fin-tech company blazing a trail right to the doorsteps of the traditional banks.

The various businesses they have on offer makes me think of Amazon’s portfolio because of the supreme diversity. The Cash App is a peer-to-peer money transfer program that cohabits with a bitcoin investing function on the same smartphone app.

Square has targeted the smaller businesses first and is a godsend for these entrepreneurs who lack the immense capital to create a financial and payment infrastructure. Not only do they provide the physical payment systems for restaurant chains, they also offer payroll services and other small loans.

The pipeline of innovation is strong with upper management mentioning they are considering stock trading products and other bank-like products. Wall Street bigwigs must be shaking in their boots.

The recently departed CFO Sarah Friar triggered a 10% collapse in share price on top of the market meltdown. The weakness will certainly be temporary, especially if they keep doubling their revenue every two years like they have been doing.

Roku

Benefitting from the broad-based migration from cable tv to online streaming and cord-cutting, Roku is perfectly placed to delectably harvest the spoils.

This uber-growth company offers an over-the-top (OTT) streaming platform along with the necessary hardware and picks up revenue by selling digital ads.

Founder and CEO Anthony Woods owns 21 million shares of his brainchild and insistently notes that he has no interest in selling his company to a Netflix or Apple.

Roku’s active accounts mushroomed 46% to 22 million in the second quarter. Viewers are reaffirming the obsession with on-demand online streaming content with hours streamed on the platform increasing 58% to 5.5 billion.

The Roku platform can be bought for just $30 and is easy to set-up. Roku enjoys the lead in the over-the-top (OTT) streaming device industry controlling 37% of the market share leading Amazon’s Fire Stick at 28%.

The runway is long as (OTT) boxes nestle cozily in only 40% of American homes with broadband, up from a paltry 6% in 2010.

They are consistently absent from the backbiting and jawboning the FANGs consistently find themselves in partly because they do not create original content and they are not an off-shoot from a larger parent tech firm.

This growth stock experiences the same type of volatility as Square. Be patient and wait for 5-7% drops to pick up some shares.

Mad Hedge Technology Letter

October 8, 2018

Fiat Lux

Featured Trade:

(A LONG-AWAITED BREATHER IN TECHNOLOGY),

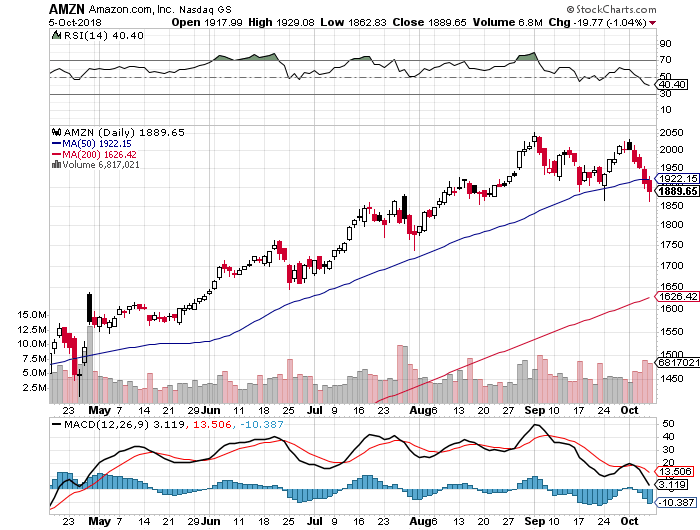

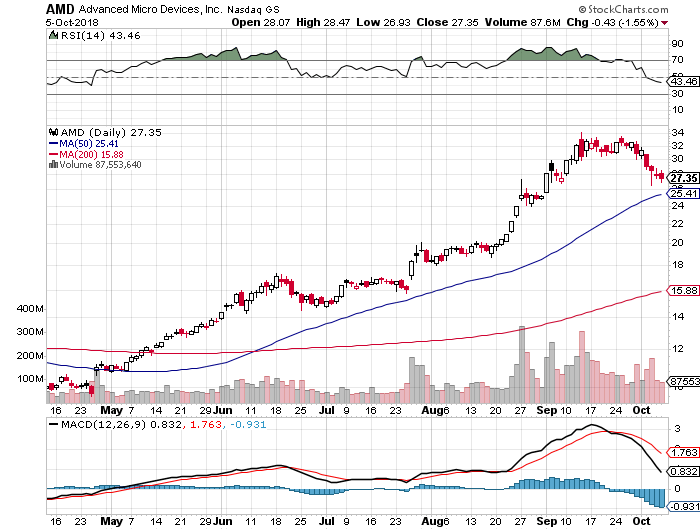

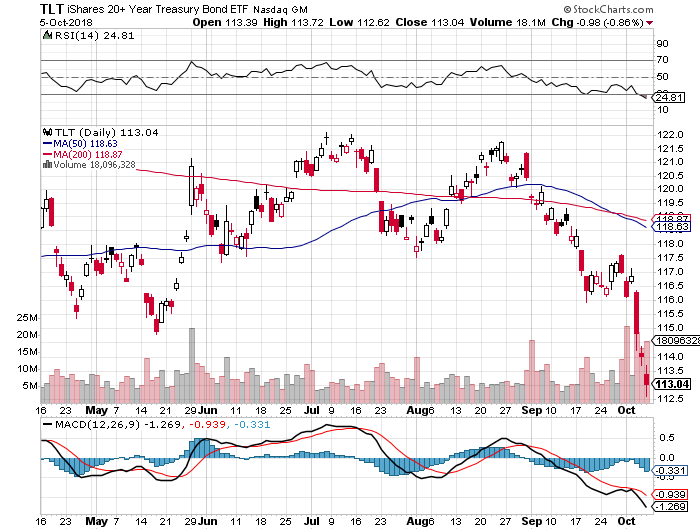

(AMZN), (TGT), (NVDA), (SQ), (AMD), (TLT)

Taking profits - it was finally time.

The Nasdaq has been hit in the mouth the last few days and rightly so.

It was the best quarter in equities for five years, and a quarter that saw tech comprise up to a quarter of the S&P demonstrating searing strength.

It would be an understatement to say that tech did its part to drive stocks higher.

Tech shares have pretty much gone up in a straight line this year aside from the February meltdown.

Even that blip only caused Amazon (AMZN) to slide around 10%.

After all the terrible macro news thrown on the market in spades – tech stocks held their own.

Not even a global trade war with the second biggest economy in the world which is critical to exporting products to America was able to knock tech shares off their perch.

At some point, 26% earnings growth cannot sustain itself, and even though the tech narrative is still intact, investors need to breathe.

Let’s get this straight – tech companies are doing great.

They benefit from a secular tailwind with every business pivoting to mobile and software services.

All that new business has infused and invigorated total revenue.

The negative reaction by technology stocks was based on two pieces of news.

Interest rates (TLT) surging to over 3.2% was the first piece of news.

The increase in rates reinforces that the economy is humming along at a breakneck speed.

Yields are going up for the right reasons and this economy is not a sick one indeed.

As rates rise, other asset classes become more attractive such as CD’s and bonds.

The whole world is looking at the pace of rate rises because this will affect the ability for tech behemoths to borrow money to invest in their expensive well-oiled machines.

Three things are certain - the economy is hot, the smart money is buying on the dip now, and Amazon will still take over your home.

Even in a rising rate environment, Amazon is fully positioned to outperform.

The second catalyst to this correction was Amazon’s decision to hike its minimum wage to $15 per hour.

This could lay the path for workers around the country to demand higher pay.

The move was a misnomer as it will eliminate stock awards and monthly bonuses lessening the burden that Amazon actually has to dole out.

Call this a push – the rise in expenses won’t be material and realistically, Amazon can afford to push the wage bill by another order of magnitude, even though they will not.

This was also a way for Amazon founder Jeff Bezos to keep Washington off his back for a few months, and his generous decision was praised by government officials.

The wage hike underscores the strength of the ebullient American economy, and the consumer will benefit by recycling their wages back into Amazon and the wider economy.

Amazon makes up 50% of American e-commerce sales, and when workers are buying goods online, a good chance its coming from Amazon.

In an environment of full employment, the natural direction of wages is up, and this was due to happen.

You can also look at wage inflation as employees gaining at the expense of the corporation.

However, the massive deflationary trends of technology will also make this wage hike quite irrelevant over time as Amazon will automate more of their supply chain to make up for any wage hike that could damage revenue.

Amazon’s economies of scale give the Seattle-based company enough levers and buttons to push and pull to dilute expenses to make this a non-issue.

Each earnings call usually involves CFO of Amazon Brian Olsavsky explaining the acceleration of efficiencies in fulfilment centers bolstering the bottom line.

The stellar innovation in operational expertise moves up a level each quarter if not two levels.

Ultimately, though expensive on the surface, this won’t affect Amazon’s numbers at all, but more critically please the lower tier of workers who fight and scratch for their daily crust of bread.

This win-win scenario casts a positive image of Bezos in the public eye at a crucial time when he plans to recruit another legion of Amazon workers, as Amazon will shortly announce the location of their second American-based headquarter.

In fact, this turns the screws on the smaller retailers who must match the $15 per hour wage or confront a potential disaster of an entire workforce walking out and joining Amazon.

The mysterious Amazon-effect works in many shapes and sizes.

Big retailers like Target (TGT) have griped that it’s near impossible to find seasonal workers for the upcoming holiday season.

Moreover, if inflation remains moderate but contained – technology will power on.

And it will take more than a few prints of rising inflation to impress the Fed enough to expedite the raising of rates.

But it is safe to say that investors cannot expect the 100% up moves like in Amazon and Advanced Micro Devices (AMD) in one calendar year moving forward.

Technology has a plate full of challenges facing its share price as we move into the latter part of the fiscal year.

The challenges are two-fold - mid-term elections and navigating a smooth year-end.

Earnings should be good which is already baked into the pie, and the benefits of the tax cut have already worked itself through the system.

The furious pace of share buybacks will eventually subside too.

Management might finally bring out the spin doctors claiming the stronger dollar and worsening trade war is the reason to guide down.

At least tech companies doing business in China might follow this playbook.

Either way, tech shares are demonstrably sensitive right now and while the market needs tech to lead the way, the sector is exhausted from the burden of carrying the bulk of the load.

Freak-outs on rate surges have been a common experience for those old hands presiding over markets for decades.

These are all the staples of a 9th year bull market.

Typical late stage topping action is normal in economic cycles.

After the dust settles, the overreaction will give way to great buying opportunities at great prices, albeit it in the higher quality names.

The chip sector is still one to avoid unless the names are Advanced Micro Devices or Nvidia (NVDA).

Legacy companies have always been a no-go.

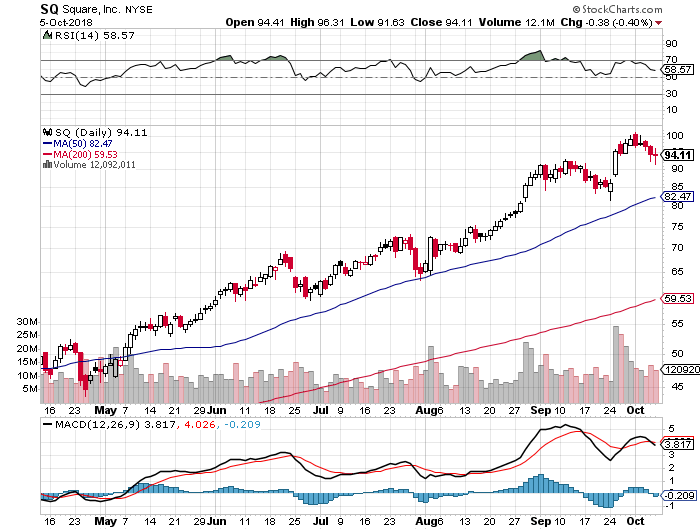

If you want hyper-growth, fin-tech name Square (SQ) would be an ideal candidate.

If buy and hold is your cup of tea, any 10% discount would be a great entry point in any of these quality companies.

Mad Hedge Technology Letter

October 3, 2018

Fiat Lux

Featured Trade:

(OUR HOME RUN ON SQUARE),

(SQ), (V), (AMZN), (GRUB), (SPOT), (MSFT), (CRM), (AAPL)

Pat yourself on the back if you pulled the trigger on Square (SQ) when I told you so because the stock has just lurched over an intra-day level of $100.

It was me aggressively pushing readers into buying this gem of a fin-tech company at $49. To read that story, please click here (you must be logged in to www.madhedgefundtrader.com).

Since then, the price action has defied gravity levitating higher each passing day immune to any ill-effects.

The Teflon-like momentum boils down to the company being at the cross-section of an American fin-tech renaissance and spewing out supremely innovative products.

At first, Square nurtured the business by targeting the low hanging fruit– small and medium size enterprises in dire need of a strong injection of fin-tech infrastructure.

It largely stayed away from the big corporations that adorn billboards across the Manhattan skyline.

That was then, and this is now.

Square is going after the Goliath’s fueling a violent rise in gross payment volume (GPV).

Modifying themselves for larger institutions is the next leg up for Square.

They recently inaugurated Square for Restaurants for larger full-service restaurants.

Business owners do not need technical backgrounds to operate the software and integrating Caviar into this program emphasizes the feed through all of Square’s software.

Dorsey has built an ecosystem that has morphed into a one-stop shop for comprehensively running a business.

Migrating into business with the premium corporations offers an opportunity to augment higher margin business.

This is the lucrative path ahead for Square and why investors are festively lining up at the door to get a piece of the action.

The downside with an uber-growth company like Square are lean profits, but they have managed to eke out three straight quarters of marginal spoils.

However, the absence of profits can be stomached considering the total addressable market is up to $350 billion.

Grabbing a chunk of that would mean profits galore for this too hot to handle company.

Expenses are always a head spinner for Silicon Valley firms and attracting a dazzling array of engineers to spin out breathtaking profits can’t be done on the cheap.

The Cash app download figures are sizzling and is one of the most popular apps in the app store.

Square’s marketing strategy is also turning a corner getting out their name leading to sale conversions.

These are just several irons in the fire.

The last two years has seen this stock double each year, could we be in for another double next year?

If measured by growth, then I see why not.

Growth is the ultimate acid test deciding whether this stock will be dragged down into the quick sand or let loose to run riot.

Other second-tier tech firms in the middle of a sweet growth spot pack a potent punch like Spotify (SPOT) and Grubhub (GRUB) which are growing annual sales around 50-60%.

Material profits are also irrelevant for the aforementioned tech juggernauts.

Square is expanding at the same fervent pace too, and the hyper-growth only makes payment processors like Visa (V) quasi-jealous of such staggering numbers.

And when Square trots out numbers to the public like that with (GPV) shooting out the roof, the stock does nothing but go gangbusters.

Either way, Square has popularized making credit card payments through smartphones and that in itself was a tough nut to crack amongst tough nuts.

Square also has a line-up of impressive point-of-sales products such as Caviar.

In fact, merchant sellers are adopting an average of 3.4 Square software apps with invoices, loans, marketing, and payroll software being the most beloved.

Square also offers other software that can handle back office tasks and manage inventory.

The software and services business is on pace to register over $1 billion in sales in 2019.

The breadth of functions that can boost a company’s execution highlights the quality of software Dorsey has produced.

I always revert back to one key ingredient that all tech companies must wildly indulge in to fire up the stock price – innovation.

Innovation in bucket loads is something all the brilliant tech firms crave such as Microsoft (MSFT), Amazon, and Salesforce (CRM).

Overperformance starts from the top and trickles down to the people they hand pick to manage and run the businesses.

Jack Dorsey is right up there with the best of them and his influence cannot be denied or ignored.

His stewardship over his other company Twitter (TWTR) is sometimes worrisome because of a pure scheduling conflict, but it’s obvious which company is having a better year.

Square steers clear of the privacy and regulatory minefields handcuffing Twitter.

And it could be safely assumed that Dorsey enjoys his afternoons more at Square than his mornings across the street at Twitter where he is bombarded by heinous problems up the wazoo.

When you conjure up an up-and-coming company that could rattle the establishment, Square is one of the first companies that comes to mind.

Some analysts even argue this company deserves to be lifted into the vaunted Fang group.

I would say they are on their merry way but they just aren’t big enough to command a spot on the Fang roster.

I have immense conviction this stock will be a deep influencer of our time, and its diversified software offerings add limitless dimensions underpinning massive revenue streams.

In Q2, the subscription revenue grew 127% YOY underscoring the success the software team is having, crafting productive apps applicable to business owners.

Business owners can even take out a loan through Square Capital which issues micro-loans to small business owners.

In need of financing? Ring up Dorsey’s company for a few quid.

Starkly contrasting Square in the payment processors space is Visa (V).

Visa is not a hyper-growth company going ballistic, but a stoic behemoth unperturbed.

The 3.283 billion visa cards that adorn its insignia represents scintillating brand awareness and efficiency.

When Tim Cook was asked if Apple (AAPL) plans to disrupt Visa, he smirked and said, “People love their credit cards.”

This is a prototypical steady as she goes-type of company.

They do not offer micro-loans to small businesses or dabble with any of the murky sort of products that can be found on the edge of the risk curve.

They are a safe and steady pure payment processor.

Its network can digest 65,000 transactions per second and is universally cherished as a brand around the world.

All of this led to an operating margin of 66% in 2017.

Square has identified other parts of the payment process to snatch and do not directly compete with Visa.

They partner with Visa and pay them a processing fee.

Subsequently, Square is paid a merchant fee after the payment is approved.

Visa has a monopoly and a moat around their business as wide as can be.

Square is a different type of beast – growing uncontrollably and hell-bent on spawning a revolutionary fin-tech paradigm shift.

The question is can Square eventually turn payment heavyweights like Visa on its head?

The path is fraught with booby traps and as Square generates the projected sales and bolsters its revenue, it could start to encroach on these legacy processors too.

Yet, it’s too early to delve into that threat yet.

Enjoy the ride with Square and better to lay off this potent stock until a better entry point presents itself.

This stock will go higher. Giddy-up!

Mad Hedge Technology Letter

September 18, 2018

Fiat Lux

Featured Trade:

(THE DANGERS OF PLAYING TECH SMALL FRY),

(FIT), (AAPL), (CRM), (FTNT), (SQ), (SNAP), (BBY)

The No. 1 complaint the Mad Hedge Fund Technology Letter receives is that I focus too much on the tech behemoths, and do not allocate much time for the needle-in-the-haystack inspirations aiming to disrupt the status quo.

Let’s get this straight – both are important.

And when a gem of a company riding the coattails of monstrous secular tailwinds comes to the fore, I do not hesitate to usher readers into the stock at a market sweet spot.

Fortunately, many of the lesser-known companies I have recommended have hit their stride such as Salesforce (CRM), Fortinet (FTNT), and Square (SQ), while I alerted readers to avoid Snap (SNAP) like the plague.

There are a lot of moving parts to say the least.

The most recent annual Apple (AAPL) product release event was emblematic of why I cannot go to the well and recommend the minnows of the tech world on a constant basis.

In 2017, Apple registered more than $229 billion in gross revenue. And under this umbrella of assets is a finely tuned operational empire that stretches like the Mongol empire of yore from best-in-class hardware to innovative software services.

Last year brought Apple a king’s ransom of profits to the tune of more than $48 billion.

Many of these upstart firms are fighting tooth and nail to surpass the $100 million gross sales mark, which is peanuts for the intimidating large tech companies.

In the process of expanding their dominion far and wide, the net they cast extends further by the day.

I hammer home the fact that these cash-rich stalwarts have an insatiable drive to initiate new businesses as a way to position themselves at the heart of each groundbreaking trend and capture fresh markets.

Some decisions are rued and some – brilliant.

At the very least, they can afford a few hits.

Algorithms, which suck up voluminous amounts of data, carry out the best decisions that software can buy.

Managers wield these finely tuned algorithms to make precise bets.

These myriads of algorithms are tweaked every day as the level of tech ingenuity snowballs incrementally with each passing day.

Enter Fitbit (FIT).

This company was first known as Healthy Metrics Research, Inc., a decisively less sexy name than its current name Fitbit.

Healthy Metrics Research, Inc. unglamorously began as did most tech companies - with little fanfare.

Its cofounders James Park and Eric Friedman identified the opportunity to jump into the sensor industry, as they saw a monstrous addressable market for future sensors in wearable smart devices.

They soon caught a bid and $400,000 flew into its coffers. They promptly marketed designs to potential investors with nothing more than a circuit board in a wooden box.

Oh, how the wearable smart device market has advanced since those early days…

All in all, the idea was good enough for some initial seed money.

At the first tech conference marketing their new sensors, they were hoping to eclipse 50 orders.

Fortuitously, the upstart firm received more than 2,000 pre-orders, and a reset upward in expectations.

With momentum at their backs, the cofounders now had the sticky situation of physically delivering the end-product to the end-user.

This involved scouring Asia for reasonable suppliers for three-odd months with “7 near death experiences” mixed in the middle of it.

Highlighting the unglamorous nature of incubation stage firms were the cofounders once quick fix sticking a “piece of foam on a circuit board to correct an antenna problem."

Somehow and some way they debuted their product at the tail end of 2009, delivering 5,000 orders with a backlog of additional orders to boot, offering the company some stress relief.

Fitbit had the best product in an industry that barely existed, and everything was rosy at their headquarters in San Francisco.

Best Buy (BBY) even adopted its products, and Fitbit watches were flying off the shelves like hotcakes.

Margins were gloriously high. The lack of threats around the corner made the company the gold standard for smartwatches.

In short, the company was having its cake and eating it, too.

In 2011, Fitbit was furiously adding to the best smartwatch on the market installing an altimeter, a digital clock and a stopwatch to its premium product.

Then came embedded Bluetooth technology: able to track steps, distance, floors climbed, calories burned, and sleep patterns.

After being embroiled in several law quagmires over big data, momentum was still at their back, and Fitbit still managed to go public.

The IPO was a roaring success and then some.

The share price rocketed to almost $50, and the firm sat pretty in the middle of 2015.

Then the company’s shares fell to pieces in one fell swoop.

Fitbit’s stock cratered more than 50% in 2016. To inject new life into the company, CEO James Park trumpeted Fitbit’s imminent face-lift that would transform the young company from a "consumer electronics company" to a "digital healthcare company."

Bad news for Fitbit. Apple planned to do the same exact thing but do it better than Fitbit.

The readjustment to Fitbit’s grand plan was to combat the original Apple smartwatch that debuted on April 24, 2015 – three years ago.

The Apple smartwatch rapidly became the dominant smartwatch in the wearable industry, selling more than 4.2 million units in just one quarter alone.

Fitbit is now trading just a smidgen over $5 today, and the devastation is far from over.

Fitbit’s shares are down almost 1,000% from its 2015 peak, stressing the dangers that minnow tech companies face getting outgunned by companies that have superior talent, unlimited resources, and top-grade management.

Not only that, Apple can integrate any wearable device linking it with the rest of its ecosystem in a heartbeat.

Even better, it does not need to develop an operating system from scratch because it can use what it already has in place - iOS.

Even if it were to run into development troubles, it would be able to throw around a wad of capital to find someone to solve idiosyncratic issues that pop up.

Yes, Tim Cook has not been the second incarnation of Steve Jobs, but he has demonstrated a natural ability to become a trustworthy steward, advancing the interests of the company, its shareholders, and most importantly its lineup of ultra-premium products.

Fitbit was enjoying its beach promenade stroll and walked into a doozy of a tsunami with little warning.

Spearheading a revival is even more daunting.

For David to outdo Goliath takes an emphatic sum of capital and a master plan to go with it.

Fitbit has neither.

The most recent Apple product launch event introduced a gem of a smartwatch, and Fitbit’s shares once again are on life support.

With each passing Apple smartwatch iteration, Fitbit experiences a new dramatic leg down in the share price.

It is almost curtains for this company.

It will be unceremoniously laid to rest in what is now quite an expansive tech graveyard of futility.

The best-case scenario is possibly salvaging itself by drastic reinvention.

It is easier said than done.

Add this company to your list of small companies obliterated by the phenomenon known as FANG, and this story gives credence to investors trying to be cute with their tech investments.

On paper it looks great until the company becomes steamrolled.

And the paper Fitbit was written on doesn’t even look all that hot with Fitbit poised to lose money until 2021.

It sounds cliché, but the network effect cannot be underestimated.

Without this powerful effect, tech investors are exposed to a demonstrably higher level of risk.

The risk of extinction.

Stay away from Fitbit shares and any dead cat bounces that shortly arise.

The Apple watch series 5 could be the dagger that finishes the walking wounded.

As an endnote, the next potential Fitbit creeping closer to the eye of the FANG storm could be the smart speaker company Sonos (SONO).

Sometimes the calm before the storm can be awfully quiet.

________________________________________________________________________________________________

Quote of the Day

“The best way to predict the future is to create it,” said influential philosopher Peter Drucker.

Mad Hedge Technology Letter

September 6, 2018

Fiat Lux

Featured Trade:

(THE SMART PLAYS IN FINTECH),

(SQ), (PYPL), (JPM), (COF), (WFC), (BAC),

(MGI), (GRUB), (BABA), (NFLX)

Fintech is all the rage now, and it’s time for investors to grab a piece of the action.

The tech sectors’ stellar performance in 2018 is a little taste of things to come as every industry forcibly pushes toward software and artificial intelligence to enhance products and services.

Bull markets don’t die of old age and some of these tech stalwarts are truly defying gravity.

The fintech sector is no exception.

Square (SQ) led by tech visionary Jack Dorsey has been a favorite of the Mad Hedge Technology Letter practically from the newsletter’s inception.

But another company has caught my eye that most of you already know about – PayPal (PYPL).

PayPal, a digital payments company, has extraordinary core drivers and a splendid growth trajectory.

Its arsenal of services includes digital wallets, money transfers, P2P payments, and credit cards.

It also has Venmo.

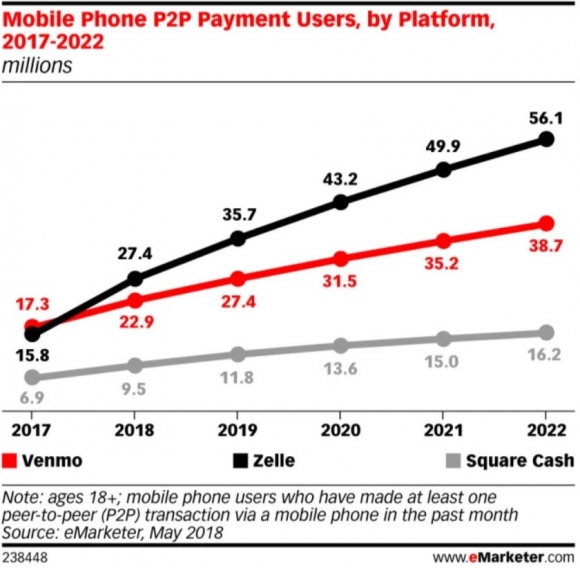

Venmo, a digital payment app, is the strongest growth lever in PayPal’s umbrella of assets right now, and was the first meaningful digital payment app in America.

It was established by Andrew Kortina and Iqram Magdon-Ismail, who were roommates at the University of Pennsylvania, and the company was bought out by PayPal for $800 million in 2014, marking a new chapter in PayPal’s evolution.

Funny enough, Venmo’s original use was to buy mp3 formatted songs via email in 2009.

Venmo is wildly popular with tech savvy millennials. A brief survey conducted illustrates how fashionable Venmo is by recording higher user statistics than Apple Pay.

The app is commonly used for ordering pizza through Uber Eats or Grubhub (GRUB), or even shelling out for monthly rent.

If you want to stir up your imagination even more, Venmo has a prominent social feed where users can view other Venmo users’ purchases.

Financial models suggest Venmo could contribute $300 million to the PayPal top line in 2021. If Venmo executes perfectly, revenue could surpass the $1 billion mark in 2021, with much higher operating margins than PayPal’s core products.

Even though management declines to speak specifically about Venmo, the dialogue in the earnings call usually provides some color into what is going on underneath the hood.

Xoom, a digital remittance distributor app with offices in San Francisco and Guatemala City owned by PayPal, along with Venmo grew payment volume by 50% YOY, surging to $33 billion annually.

Of that $33 billion in volume, $19 billion was contributed by Venmo and Xoom chipped in with $14 billion.

More than 60,000 new merchants joined PayPal’s array of platforms, adding up to more than 19.5 million total merchants.

All in all, PayPal locked in $3.86 billion of sales last quarter, which was a 23% YOY jump in revenue, at a time where widespread acceptance of fintech platforms is brisk.

PayPal raised its end-of-year forecast and rewarded shareholders with authorization of a $10 billion buyback.

Upward margin expansion, expanding market share, multiple revenue stream, and untapped pricing power is the recipe to PayPal’s meteoric rise.

PayPal’s share price has climbed higher from a base of $73 at the beginning of the year to an all-time high of more than $90.

Offering more proof fintech is alive and kicking is Jack Dorsey’s Square’s dizzying rise of more than 200% YOY in its share price.

The company is exceeding all revenue growth expectations and is poised to ramp up subscription revenue.

As with the Venmo app, Square’s Cash app has unrealized potential and will be one of the outperforming profit drivers going forward.

Square hopes to be the one-stop-shop for all types of digital payment needs including consumer finance, equity purchases, possibly international transfers, and cryptocurrency.

All of this is happening amid a robust secular story that could have seen traditional banks swept into the dustbin of history.

Rewind a few years ago, perusing the data about the movement to digital payments must have frightened the living daylights out of the executives from major Wall Street mainstays.

Digital wallets assertive migration into mainstream money payment services could have detached traditional banks’ core businesses.

Slogging your way to a physical bank to put in a wire transfer was not appealing.

Archaic methods of business are painful to see, and traditional banks were still operating this way as of 2015.

Time is money and technology has crashed the traditional waiting time to almost zero.

The way these tech companies operate is simple.

They compete to hire a hoard of advanced computer developers or shortcut the process using the time-honored tradition of poaching the competition’s best talent.

Then snatch market share at all costs and grow like crazy.

Banks badly needed introducing some functions to their array of services such as linking with third-party payment APIs to facilitate online payments and enabling cross-platform digital payments.

Other functions such as establishing modern peer-to-peer payment systems or adopting QR code technology that are wildly popular in East Asia could enhance optionality as well.

These are several instruments they could have amalgamated into their arsenal of fintech technology that could have freshened up these dinosaur institutions.

Harmonizing banking tasks with mobile functionality was fast coming and would be the standard.

Anyone not on board would sink like the Titanic.

Ultimately, banking institutions needed to up their game and acquire one of these digital wallet processors or watch from the sidelines.

They chose the former when a consortium called Early Warning Services (EWS) jointly created by behemoth American banks, including JPMorgan Chase & Co. (JPM), Capital One (COF), Bank of America (BAC), and Wells Fargo (WFC) to “prevent fraud and reduce detection risk” made a game-changing decision.

(EWS) acquired digital payment app Zelle in 2016, and this was its aggressive response to Square Cash and PayPal’s Venmo.

Results have been nothing short of breathtaking.

Leveraging the embedded base of existing banking relationships, Zelle took off like a scalded chimp and never looked back.

In a blink of an eye, Zelle had already signed up more than 30 banks and over 100 financial institutions to its platform.

Banks couldn’t bear being left out of the fintech party.

With hearty conviction, Zelle is signing up users at a pace of 100,000 per day, and the volume of payments in 2017 eclipsed $75 billion.

Zelle projects to expand more than 73% in 2018, integrating 27.4 million new accounts in the U.S., head and shoulders above Venmo’s 22.9 million and Square Cash due to add 9.5 million more users.

Make no bones about it, Zelle was in prime position to convert existing relationships into digital converts. The banks that do not have an interest in Zelle have an uphill climb to stay relevant.

The United States is rather late to this secular growth story. That being said, already 57% of Americans have used a mobile wallet at least once in their lives.

Innovative ideas bring supporters galore and even more adoptees.

That is why the strong pivot into technological enhanced ideas bear unlimited fruit.

Using a mobile platform to just open an app then send funds within a split second with minimal costs is appealing for the Netflix (NFLX) crazed generation that can hardly get off the couch.

Ironically, it’s those in the emerging parts of the world leading this fintech revolution by skipping the traditional banking experience completely and downloading digital wallet apps on their mobile devices.

It’s entirely realistic that some fresh-faced youth have never been present at a physical banking branch before in India or China.

Download an app and your fiscal life commences. Period.

The volume of funds passing through the arteries of Chinese digital wallet apps surpassed $15 trillion in 2017.

And by 2021, 79.3% of the Chinese population are projected to use digital wallets as their main source of splurging Chinese yuan.

America lags a country mile behind China, but the Chinese progress has offered American tech companies a crystal-clear blueprint to springboard digital payment initiatives.

Chinese state banks are already starting to become marginalized, and the Wall Street banks are not immune to the same fate.

Devoid of a digital strategy will be a death knell to certain banking institutions.

Compare the pace of adoption and some must question why American adoption is tardy to a fault.

Highlighting the lackadaisical pace of American fintech integration was Alibaba’s (BABA) smash-and-grab attempt at MoneyGram International Inc. (MGI), as it sought to gain a foothold into the American fintech market.

The attempt was rebuffed by the federal government.

The nascent state of the digital payment world in America must alarm Silicon Valley experts. And the run-up in Square and PayPal includes calculated bets that these two standouts will leapfrog into the future with guns blazing along with Zelle.

The parabolic nature of Square’s mystifying gap up means that a moderate pullback is warranted to put capital to work in this name.

Investors should wait for a timely entry point into PayPal as well.

These two stocks have overextended themselves.

As the fintech pie extrapolates, there will be multiple victors, and these victors are already taking shape in the form of Zelle, PayPal, and Square.

![]()

________________________________________________________________________________________________

Quote of the Day

“In the not-too-distant future, commerce is just going to be commerce. It won't be online commerce or offline commerce. It's just going to be commerce. And that will happen because of the phone,” – said CEO of PayPal Dan Schulman.