Mad Hedge Technology Letter

July 30, 2021

Fiat Lux

Featured Trade:

(THE BEST WAY TO STREAMLINE YOUR TECH PORTFOLIO)

(MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

Mad Hedge Technology Letter

July 30, 2021

Fiat Lux

Featured Trade:

(THE BEST WAY TO STREAMLINE YOUR TECH PORTFOLIO)

(MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

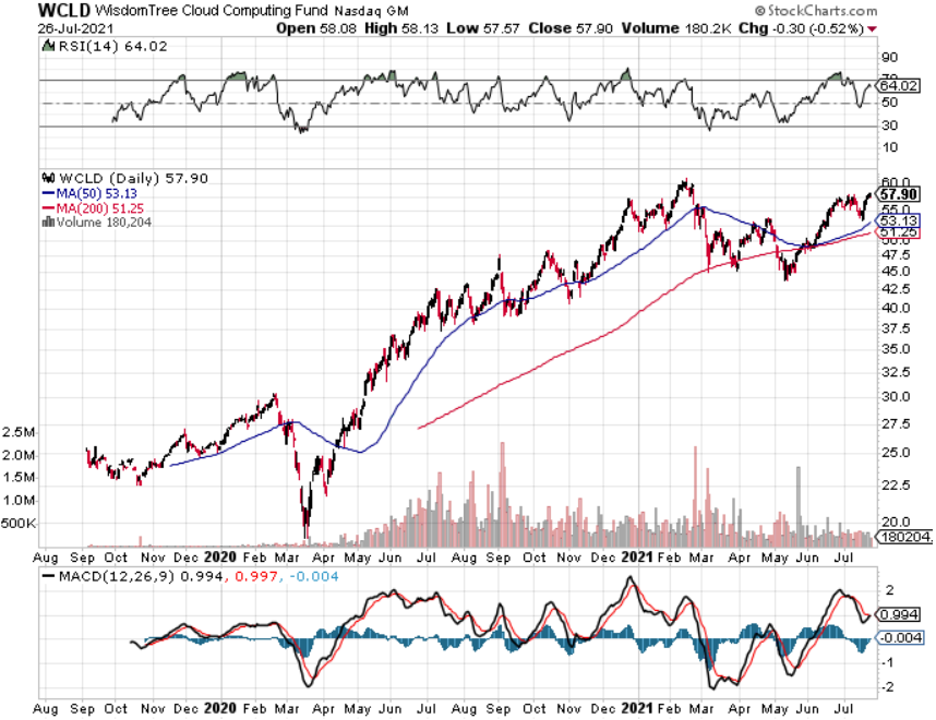

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance, and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

Mad Hedge Technology Letter

July 21, 2021

Fiat Lux

Featured Trade:

(THE TRUTH ABOUT AUTOMATION AND WALL STREET JOBS)

(AAPL), (SQ), (AMZN), (PYPL)

Mad Hedge Technology Letter

April 16, 2021

Fiat Lux

Featured Trade:

(SHOULD I BUY COINBASE TODAY?)

(COIN), (CRM), (ADBE), (PYPL), (SQ)

For all the cryptocurrency haters in the world, it’s getting harder to take that stand.

I’ll tell you why.

Coinbase (COIN) was the first major crypto business to go public in the U.S. when it began trading at $381 Wednesday morning on the Nasdaq and its IPO symbolizes the acceptance of an alternative digital asset class in technology.

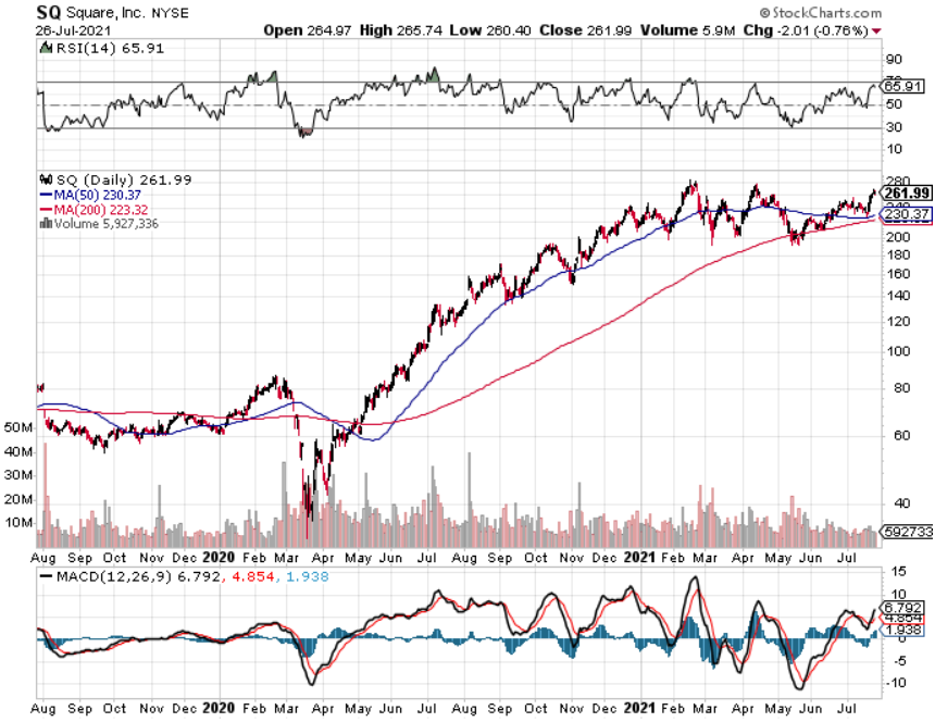

Prior to this watershed moment, the only way to play crypto was through second derivatives plays like PayPal (PYPL) and Square (SQ) who have been handsomely rewarded through higher share prices.

Now, we get the biggest U.S. cryptocurrency exchange trading publicly that will allow exposure to mainstream stock-market investors.

The event has also been tabbed as a catalyst that might drive the adoption of incremental digital assets.

At the very least, this lays down a marker for further crypto-related companies eyeing the Nasdaq after Coinbase’s blowout success.

This also shows that the cryptocurrency infrastructure is developing rapidly and its budding credibility is something that needs to be acknowledged.

The Coinbase IPO was also the catalyst in sending bitcoin prices to almost $65,000.

No doubt that the appreciating asset has been the most attractive use case for the incremental investor and cryptocurrency buyer.

Many early investors who got into bitcoin at 20 cents are now billionaires many times over.

After such stunning success, it’s hard to believe that any fintech or cryptocurrency start-up would ever consider doing their IPO anywhere else but New York.

New York has the liquidity, the US dollar, and the capacity to receive such type of growth companies in bulk.

This is not only an emphatic victory for digital assets, but also for the US tech sector and a stamp of validation for the Nasdaq market.

Ironically enough, even during this trade war, Chinese tech companies are clamoring to go public in New York and not mainland China for the above reasons.

Here are a few other highly positive data points to digest that were talking points in their S-1 filing.

The overall market capitalization of crypto assets grew from less than $500 million to $782 billion between December 31, 2012, and December 31, 2020, representing a CAGR (compound annual growth rate) of over 150%.

Over the same period, Coinbase retail users grew from less than 13,000 to 43 million, a 175% CAGR.

I believe the total market cap of crypto is now around $2 trillion in April 2021.

And more recently, Coinbase has experienced significant growth in the number of institutions on their platform, increasing from over 1,000 as of December 31, 2017, to 7,000 as of December 31, 2020.

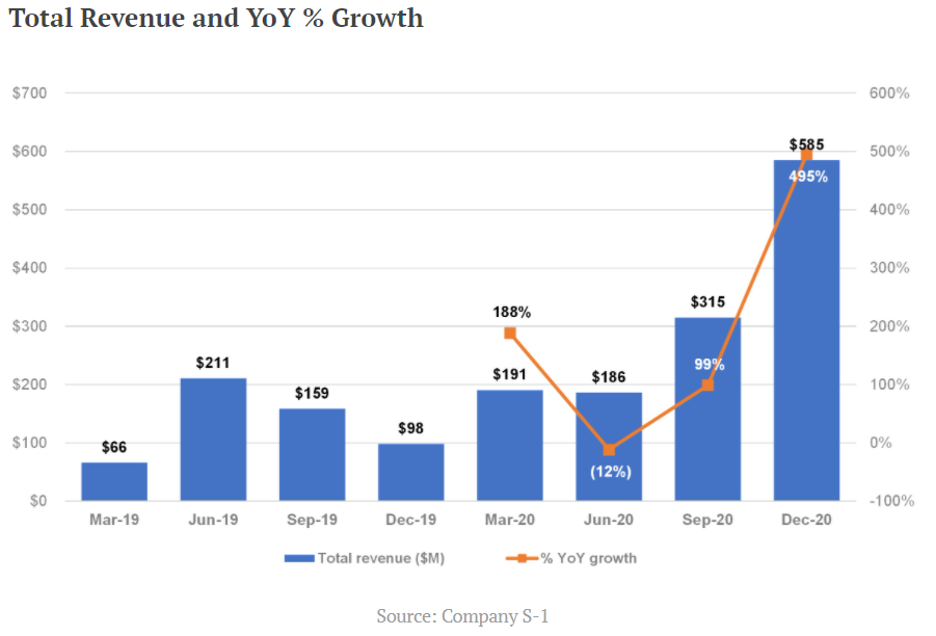

Bitcoin reported a nine-fold increase in Q1 revenue, to $1.8B, up from $190.6M the previous year.

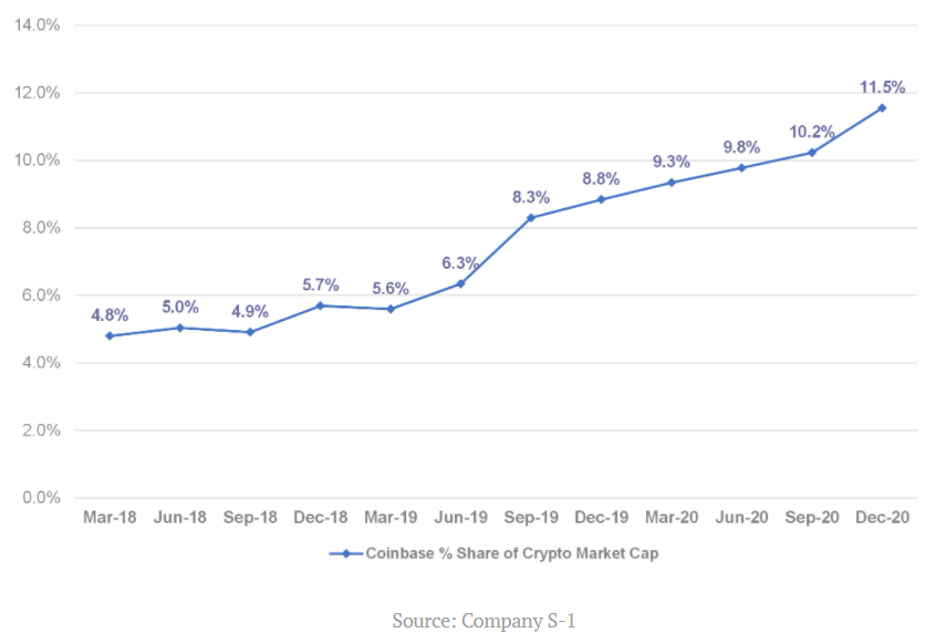

Just like Google and Facebook benefit from a duopoly, Coinbase will benefit from being the only pure cryptocurrency option on the Nasdaq and that will put a floor under shares in the short-term.

The growth metrics of the company are also robust via a helping hand by the increasingly expensive price of bitcoin.

No doubt that this company’s prospects are tied to the hip with the prices of cryptocurrencies.

If the price of bitcoin retraces to $30,000, which it could because of the high volatility of it, expect Coinbase shares to dive with it.

This for all intents and purposes is a bet on the health and price trajectory of bitcoin for better or worse until other crypto-based choices are introduced which would give more layers and complexity to this sub-sector.

Bitcoin calls out Binance which they state as a competitor and Kraken is another exchange that is large and vying for the same capital.

I believe these two companies have a chance to go public and that is when you will really see the institutions jump on this crypto bandwagon.

More options and a foundational investment base will also promote stability in this new technology sub-sector.

Should you buy Coinbase today?

No.

I understand Coinbase’s growth metrics are off the charts with revenue growing 900%, but it’s not worth $100 billion market cap on just $1.8 billion of quarterly sales.

Investors would need solid tailwinds such as bitcoin passing $100,000 in 2021 for this company to be worth $100 billion and I just don’t see it.

Then also understand the cybersecurity and possible regulations are two risks that could blow up the business model at any moment which would take down the premium in the stock.

Yes, the meteoric rise of crypto at the start of 2021 has turned heads, but as the economy reopens, I do believe money will rotate from crypto back into traditional technology that is underpinned by cash cow businesses.

Highly profitable companies that aren’t FANGs are also set to deliver share appreciation to shareholders such as Salesforce (CRM) or a company like Adobe (ADBE) who earn profits of $5.27 billion on $13 billion of annual revenue.

I acknowledge that Coinbase’s IPO was the perfect time to go public.

They are taking advantage of easy money and low rates while the acceptance of this alternative asset class has never been higher.

However, I don’t see any more incremental growth in the short term and the stock is more than fully priced today.

The risk-reward is not favorable to pile into this stock now unless you have a bullish 50-year view on crypto and can’t wait.

This stock will go through volatility because of the inherent dynamics they are tied to and I would seriously look at buying Coinbase only on a massive sell-off.

Don’t go chasing unicorns.

At the end of the day, this is a real company with real revenue growth of 900% year-over-year. Slice it up anyway, and these numbers are numbers that attract investors, but the stock is too expensive right here.

Mad Hedge Technology Letter

April 7, 2021

Fiat Lux

Featured Trade:

(THE DISAPPEARING U.S. RETAIL STORE)

(SQ), (PYPL)

As vaccine shots hit a peak of 4 million on Easter Weekend, this means the return of the mall and retail, right?

Surely, a reopening bounce for retail is in the cards?

Think again.

A new report from a major bank suggests that 80,000 retail stores will close in the U.S. over the next few years.

This is not a wild guess or speculative bet on what will happen, this is starting to become a consensus.

By 2026, the worst-case scenario is 200,000 stores closing and by 2030, the worst-case scenario entails 300,000 stores closing highlighting the impactful nature of the situation.

As I took a fine-tooth comb to the latest earnings’ data, I can’t help but see that every tech CFO sees the accelerated digital transformation as one of the legacies of the pandemic.

But it will not be an invisible virus keeping shoppers away from the mall in the future, consumers are just satisfied with ordering from home and this economic behavior will become embedded in the new post virus world.

In 2020, 17 major retailers filed for bankruptcy – including Lord & Taylor, Century 21 and Brooks Brothers.

Countless are on the verge of defaults underscoring the pitiful shape of many retailers.

On the other side of the pandemic, blighted malls and unpaid rental payments is what will be left for much of retail.

Many of these malls won’t be able to rent out spaces for pennies on the dollar.

Many stores have gone 100% digital, even restaurants, that haven’t been able to offer dine-in options.

Online retail’s market share of the full retail landscape climbed from 14% in 2019 to 18% in 2020, and by 2025, that number will grow close to 30.

Average household spending online has grown the past five years from $5,800 to $7,100 from 2019 to 2020 highlighting how U.S. shoppers are increasingly comfortable ordering volume online.

Now armed with more stimulus money, I highly doubt there will be a renaissance in brick-and-mortar retail.

One possibility in the future is that many brick-and-mortar stores will double dip, both selling and fulfilling online orders from the same location.

Also, some goods simply aren’t made for click, order, and collect at home like shoes and dresses but others are such as home improvement, grocery, and auto parts.

The silver lining is awfully thin for the retail sector and odds are, if retailers don’t have a digital footprint by now, they are already toast.

The mall vacancy rate rose to 10.5% in the fourth-quarter 2020 from 10.1% in the third quarter and 9.7% a year ago.

This is unlikely to reverse in the short, medium, or long term and another concept for malls will need to be carefully thought out.

Considering further deterioration of non-digital retail, this should directly lead many investors to conclude that pouring money in ecommerce and fintech companies is the right thing to do.

It absolutely is.

The thesis for outperformance is so obvious that many tech investors need to seriously capture part of this sustainable megatrend.

On top of my list of fintech firms are Square (SQ) and PayPal (PYPL).

Square expanded sales 141% year-over-year last quarter and have been profitable for the past two quarters with EPS growing 39% year-over-year last quarter.

PayPal has a much bigger business meaning the law of numbers start to work against them.

They expanded sales 23% year-over-year last quarter and improved EPS by 30% year-over-year.

These two fintech stocks should be considered on every substantial dip because profitability increases have a clear path for the foreseeable future and the robustness of in-house products have not disappointed over time.

Mad Hedge Biotech & Healthcare Letter

April 1, 2021

Fiat Lux

FEATURED TRADE:

(A RULE MAKER IN HEALTHCARE)

(TDOC), (SQ), (SHOP), (ROKU), (TSLA)

Monopolies. In any industry, they’re typically called rule breakers.

For healthcare, these are rule-making stocks that ultimately rise to dominance that they eventually win government-sanctioned monopolies and establish massive networks.

For biotechnology and healthcare investors who like to err on the side of caution but still want to take a dip on monopoly-like players, one stock stands out: Teladoc Health (TDOC).

Teladoc, which currently has a market capitalization of $30 billion, is one of those groundbreaking companies that use technology to disrupt the way we live.

The company’s potential is actually getting compared to the likes of other tech movers such as (SQ), Shopify (SHOP), Roku (ROKU), and Tesla (TSLA).

So far, Teladoc stock has gone up 144% over the past 12 months.

On a year-over-year basis, the total number of visits for Teladoc more than doubled from 4.14 million to reach a whopping 10.59 million. Even the international visits rose by 71%.

As expected, the COVID-19 pandemic served as a major boon to its already thriving business.

Although it wasn’t as popular at the time, the company’s operating model offered a myriad of benefits for the healthcare industry.

For one, telehealth visits are way more convenient for the patients. Since the visits won’t take as much time and effort from their end, the patients would be more motivated to regularly check in with their doctors.

In turn, the doctors would be able to offer higher-quality care since the cooperation of the patients means they can also monitor the symptoms and progress better.

Best of all, the patients are typically billed at cheaper rates compared to office visits.

I think the last one makes Teladoc an attractive winner in the eyes of practically all health insurers.

Teladoc is the biggest telehealth services provider in the United States, and one of the major steps that the company took to cement its reputation as a virtual health leader is its splashy $18.5 billion merger with Livongo in 2020.

If you haven’t heard of Livongo, this company was growing incredibly faster than Teladoc even before the merger.

Basically, Livongo collects copious amounts of information from patients. Using artificial intelligence, the company then sends personalized tips and reminders to their enrolled members with the goal to improve their overall quality of life.

Most of the patients suffer from chronic conditions, which means they would require regular nudges to ensure that they take the proper medications on time.

For example, some of Livongo’s users have diabetes. The company monitors them via wireless glucose meters, guiding the users to follow a positive lifestyle when their blood sugars begin to spike.

At the time of the merger, Livongo has already secured over 500,000 enrolled members for its diabetes platform.

This is impressive as it represents roughly 2% of the entire diabetes pool in the United States.

Aside from diabetes, Livongo has also been working on other chronic conditions like hypertension and weight management.

Considering that hypertension accounts for 7.6 million deaths per year worldwide and the extensive list of health problems associated with obesity, such as coronary heart disease and end-stage renal disease, I think Livongo has developed a highly sustainable business model that’s perfect for the “new normal.”

More importantly, the combination of Livongo and Teladoc will now allow the two companies to cross-sell their services to their users.

As for those who think that Teladoc is only a pandemic play, the company didn’t really need the pandemic for its business model to succeed.

Prior to COVID-19, its sales have been growing by an average of 75% per annum since 2013.

With its merger with Livongo, I think Teladoc has developed a stronger all-weather model for growth.

Teladoc is a rule maker and a first-mover, with the company moving the multi-trillion dollar healthcare industry to the internet.

At this point, it is the dominant name in the arena and the undisputed leader in telehealth. With everything it has to offer, I believe Teladoc is a long-term investing opportunity and it would be a good idea to buy on the dip.

Global Market Comments

April 1, 2021

Fiat Lux

Featured Trade:

(MARCH 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (ZM), ($INDU), (X), (NUE), (WPM), (GLD), (SLV), (KMI), (TLT), (TBT), (BA), (SQ), (PYPL), (JNP), (CP), (UNP), (TSLA), (GS), (GM), (F)