Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(WHAT THE HECK IS ESG INVESTING?),

(TSLA), (MO)

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(WHAT THE HECK IS ESG INVESTING?),

(TSLA), (MO)

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

I am always watching for market-topping indicators and I have found a whopper. The number of new IPOs from technology mega unicorns is about to explode. And not by a little bit but a large multiple, possibly tenfold.

Some 220 San Francisco Bay Area private tech companies valued by investors at more than $700 billion are likely to thunder into the public market next year, raising buckets of cash for themselves and minting new wealth for their investors, executives, and employees on a once-unimaginable scale.

Will it kill the goose that laid the golden egg?

Newly minted hoody-wearing millionaires are about to stampede through my neighborhood once again, buying up everything in sight.

That will make 2020 the biggest year for tech debuts since Facebook’s gargantuan $104 billion initial public offering in 2012. The difference this time: It’s not just one company but hundreds that are based in San Francisco, which could see a concentrated injection of wealth as the nouveaux riches buy homes, cars and other big-ticket items.

If this is not ringing a bell with you, remember back to 2000. This is exactly the sort of new issuance tidal wave that popped the notorious Dotcom Bubble.

And here is the big problem for you. If too much money gets sucked up into the new issue market, there is nothing left for the secondary market, and the major indexes can fall by a lot. Granted, probably only $100 billion worth of stock will be actually sold, but that is still a big nut to cover.

The onslaught of IPOs includes home-sharing company Airbnb at $31 billion, data analytics firm Palantir at $20 billion, and FinTech company Stripe at $20 billion.

The fear of an imminent recession starting sometime in 2020 or 2021 is the principal factor causing the unicorn stampede. Once the economy slows and the markets fall, the new issue market slams shut, sometimes for years as they did after 2000. That starves rapidly growing companies of capital and can drive them under.

For many of these companies, it is now or never. They have to go public and raise new money or go under. The initial venture capital firms that have had their money tied up here for a decade or more want to cash out now and roll the proceeds into the “next big thing,” such as blockchain, healthcare, or artificial intelligence. The founders may also want to raise some pocket money to buy that mansion or mega yacht.

Or, perhaps they just want to start another company after a well-earned rest. Serial entrepreneurs like Tesla’s Elon Musk (TSLA) and Netflix’s Reed Hastings (NFLX) are already on their second, third, or fourth startups.

And while a sudden increase in new issues is often terrible for the market, getting multiple IPOs from within the same industry, as is the case with ride-sharing Uber and Lyft, is even worse. Remember the five pet companies that went public in 1999? None survived.

Some 80% of all IPOs lost money last year. This was definitely NOT the year to be a golfing partner or fraternity brother with a broker.

What is so unusual in this cycle is that so many firms have left going public to the last possible minute. The desire has been to milk the firms for all they are worth during their high growth phase and then unload them just as they go ex-growth.

Also holding back some firms from launching IPOs is the fear that public markets will assign a lower valuation than the last private valuation. That’s an unwelcome circumstance that can trigger protective clauses that reward early investors and punish employees and founders. That happened to Square (SQ) in its 2015 IPO.

That’s happening less and less frequently: In 2019, one-third of IPOs cut companies’ valuations as they went from private to public. In 2019, that ratio has dropped to one in six.

Also unusual this time around is an effort to bring in more of the “little people” in the IPO. Gig economy companies like Uber and Lyft have lobbied the SEC for changes in new issue rules that enabled their drivers to participate even though they may be financially unqualified. They were all hit with losses of a third once the companies went public.

As a result, when the end comes, this could come as the cruelest bubble top of all.

Global Market Comments

March 6, 2018

Fiat Lux

Featured Trade:

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (TLT)

Global Market Comments

October 23, 2018

Fiat Lux

Featured Trade:

(WATCH OUT FOR THE UNICORN STAMPEDE IN 2019),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (MSFT)

I am always watching for market topping indicators and I have found a whopper. The number of new IPOs from technology mega unicorns is about to explode. And not by a little bit but a large multiple, possibly tenfold.

Six San Francisco Bay Area private tech companies valued by investors at more than $10 billion each are likely to thunder into the public market next year, raising buckets of cash for themselves and minting new wealth for their investors, executives, and employees on a once-unimaginable scale.

Will it kill the goose that laid the golden egg?

Newly minted hoody-wearing millionaires are about to stampede through my neighborhood once again, buying up everything in sight.

That will make 2019 the biggest year for tech debuts since Facebook’s gargantuan $104 billion initial public offering in 2012. The difference this time: It’s not just one company, and five of them are based in San Francisco, which could see a concentrated injection of wealth as the nouveaux riches buy homes, cars and other big-ticket items.

If this is not ringing a bell with you, remember back to 2000. This is exactly the sort of new issuance tidal wave that popped the notorious Dotcom Bubble.

And here is the big problem for you. If too much money gets sucked up into the new issue market, there is nothing left for the secondary market, and the major indexes can fall, buy a lot.

The onslaught of IPOs includes ride-sharing firm Uber at $120 billion, home-sharing company Airbnb at $31 billion, data analytics firm Palantir at $20 billion, FinTech company Stripe at $20 billion, another ride-sharing firm Lyft at $15 billion, and social networking firm Pinterest at $12 billion.

Just these six names alone look to absorb an eye-popping $218 billion, and that does not include hundreds of other smaller firms waiting on the sidelines looking to tap the public market soon.

The fear of an imminent recession starting sometime in 2019 or 2020 is the principal factor causing the unicorn stampede. Once the economy slows and the markets fall, the new issue market slams shut, sometimes for years as they did after 2000. That starves rapidly growing companies of capital and can drive them under.

For many of these companies, it is now or never. The initial venture capital firms that have had their money tied up here for a decade or more want to cash out now and roll the proceeds into the “next big thing,” such as blockchain, health care, or artificial in intelligence. The founders may also want to raise some pocket money to buy that mansion or mega yacht.

Or, perhaps they just want to start another company after a well-earned rest. Serial entrepreneurs like Tesla’s Elon Musk (TSLA) and Netflix’s Reed Hastings (NFLX) are already on their second, third, or fourth startups.

And while a sudden increase in new issues is often terrible for the market, getting multiple IPOs from within the same industry, as is the case with ride-sharing Uber and Lyft, is even worse. Remember the five pet companies that went public in 1999? None survived.

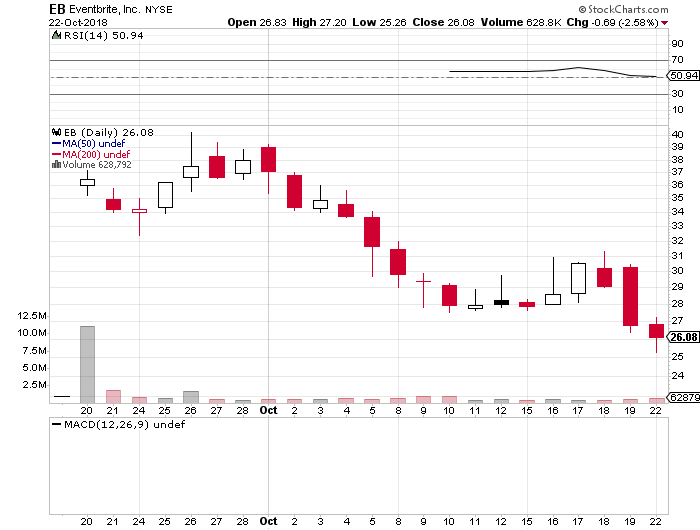

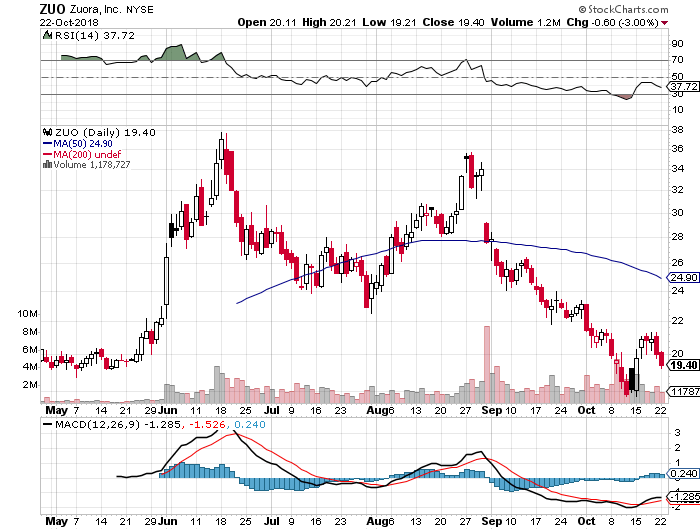

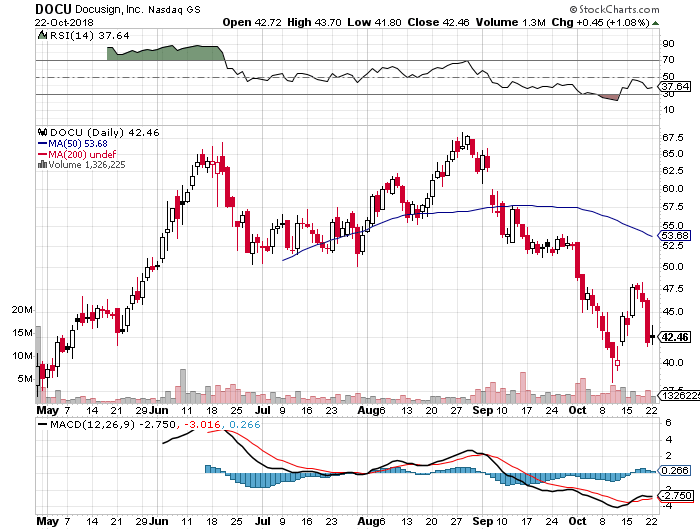

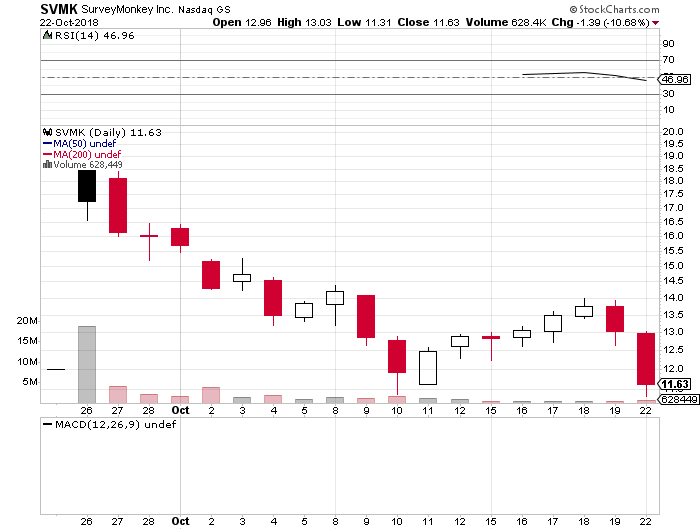

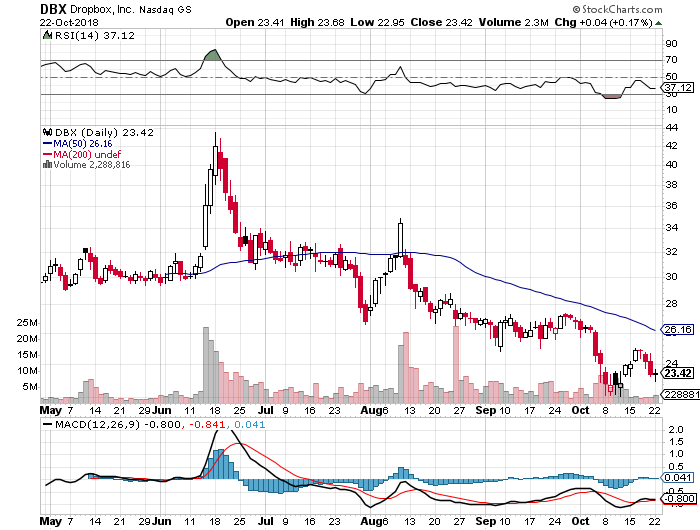

The move comes on the heels of an IPO market in 2018 that was a huge disappointment. While blockbuster issues like Dropbox (DB) and DocuSign (DOCU) initially did well, Eventbrite (EB), SurveyMonkey (SVMK), and Zuora (ZUO) have all been disasters.

Some 80% of all IPOs lost money this year. This was definitely NOT the year to be a golfing partner or fraternity brother with a broker.

What is so unusual in this cycle is that so many firms have left going public to the last possible minute. The desire has been to milk the firms for all they are worth during their high growth phase and then unload them just as they go ex-growth.

The ramp has been obvious for all to see. In the first nine months of 2018, 44 tech IPOs brought in $17 billion, according to Dealogic. That’s more than tech IPOs reaped for all of 2016 and 2017 combined.

Also holding back some firms from launching IPOs is the fear that public markets will assign a lower valuation than the last private valuation. That’s an unwelcome circumstance that can trigger protective clauses that reward early investors and punish employees and founders. That happened to Square (SQ) in its 2015 IPO.

That’s happening less and less frequently: In 2017, one-third of IPOs cut companies’ valuations as they went from private to public. In 2018, that ratio has dropped to one in six.

Also unusual this time around is an effort to bring in more of the “little people” in the IPO. Gig economy companies like Uber and Lyft are lobbying the SEC for changes in new issue rules that will enable their drivers to participate even though they may be financially unqualified.

As a result, when the end comes, this could come as the cruelest bubble top of all.

Mad Hedge Technology Letter

October 10, 2018

Fiat Lux

Featured Trade:

(DON’T BUY SURVEYMONKEY ON THE DIP),

(SVMK), (GOOGL), (CRM)

If a company takes almost 20 years and still isn’t profitable - it probably never will.

Granted, tech firms are given a Rapunzel-length leash to collect users, scale out the product, refine algorithms to industry standard, and build up the engineering team.

I know this takes time – it doesn’t happen in one day.

After whipping up a frenzy of momentum and venture capitalists claiming stakes, tech stocks usually go public.

This is the common process of what it takes to construct a Silicon Valley tech firm, and there are no shortcuts to this long hard slog.

And if after almost 20 years, amid a nine-year bull market, a tech firm in the most dominating sector in the world cannot figure how to be in the black, investors should stay away from this company in droves.

SurveyMonkey (SVMK), who recently achieved a blockbuster IPO, were the rock stars of the tech world for one day and one day only.

The stock peaking after the first trading day is a ghastly signal and ominous sign.

Their fifteen minutes of fame is all they will get because this practically ex-growth company has no indicators of a rosier future.

The company went public at $12 per share and even that was too generous.

The stock took off like a banshee, on the verge of overshooting the $20 level before falling back to grace.

The stock is now trolling around $13, and on the verge of heading to the purgatory of single digits.

What caused such a swan dive after such a promising start?

On the surface, everything looks like peaches and daffodils – a growing Silicon Valley cloud company even with Facebook spin doctor Sheryl Sandberg on the board.

The optics pass all the marks.

But wait a second, looking at the nuts and bolts, it’s crystal clear why this stock has been throttled back.

The first half of 2018, SurveyMonkey presided over a tepid 3% of paid user growth.

Yes, SurveyMonkey is growing, but not by much.

In this same period, the company lost $27.2 million and this was after an annual 2017 loss of $24 million.

Profitability isn’t exactly their forte.

The 14% of revenue growth the company secured was done after taking a machete and gutting margins to appear pretty for the IPO.

And it’s painfully obvious that SurveyMonkey is failing at converting the freemium users into paid converts.

The online survey doesn’t exactly have the highest barriers of entry.

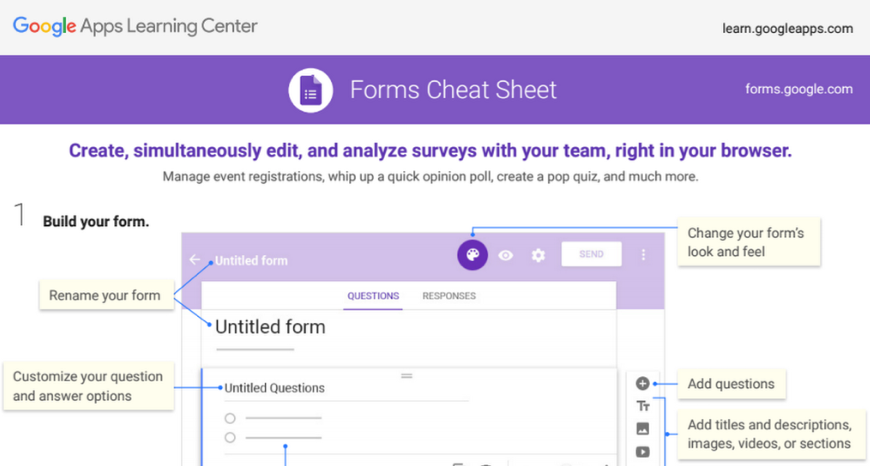

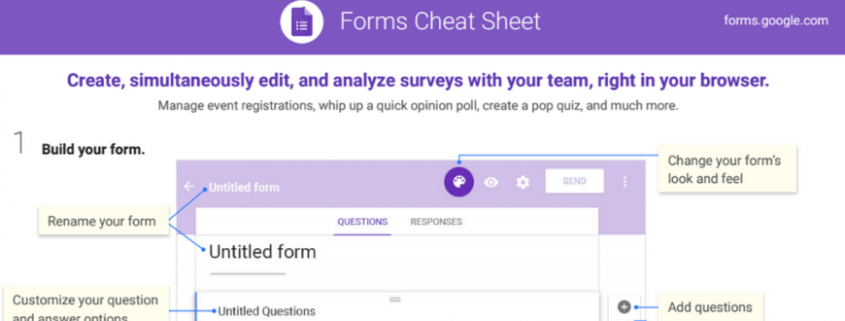

Google (GOOGL) Forms is the competitor in this space offering straightforward free surveys with basic analysis.

The tool is highly functional.

The pricing structure to SurveyMonkey’s individual membership is presented as a luxury service like the US postal service.

The individual service costs $384 per year and rises all the way up to the bloated price of $1,188 per year.

Any individual paying $1,188 per year for this needs to check themselves into a mental hospital.

Google Forms could easily undercut this pricing model by offering survey tool packages for a fraction of this amount.

The “team plan” is also laughable by charging $75 per month for up to three users, and this type of plan is capped at an exorbitant $225 per month.

Let’s remember that Microsoft offers Microsoft Office 365 Personal for an annual total of $59.99 and is million times more useful.

This annual subscription comes with premium versions of Word, Excel, PowerPoint, OneDrive, OneNote, Outlook, Publisher, and Access.

The OneDrive cloud service includes 1 terabyte (TB) of cloud storage.

Just by this simple comparison, it is easy to see which service is of value and which service is building castles in the sky.

With the explosion of service-as-a-software (SaaS) apps flooding desktops, I imagine the paid version of SurveyMonkey would be first on the chopping block due to its overly ambitious pricing.

In this strategy, the company is more concerned about milking as much as they can from each existing paid user instead of juicing up the core user base.

Effectively, this is a poor management decision, and the company is harming the growth of the potential paid usership base by robbing all incentive to convert to the paid version.

As Netflix masterfully proved, draw in the eyeballs at a lower price, build up the service to an optimum quality level, and subscribers never leave.

The opposite strategy is an indirect way of management believing the product is not good enough or the niche is too small to perpetualize a solid relationship.

And since growth numbers aren’t accelerating, there is infinitesimal reason to even consider investing in this fading company.

SurveyMoney has also racked up the debt - $317 million of it to be precise putting its debt $100 million over total revenue in 2017.

They were burning cash quickly and only had $43 million left in the coffers.

Part of the rationale for going public was a way to pay down debt.

Another chunk of proceeds from the IPO will be used to pay taxes.

The company has no innovative roadmap going forward and using the cash to pay down existing obligations shows the anemic level of intent from this company.

The silver lining in this company is that the losses of $76.4 million in 2016 were pared back in 2017.

In the IPO prospectus, SurveyMonkey noted that most unpaid customers do not become paid customers.

Even though the product is useful and it’s a long-time favorite of mine, the stock is a different animal.

There was not much meat in the prospectus and most of it were dry bones.

The IPO day was buoyed by the $40 million in stock venture-capital arm of Salesforce (CRM) pocketed, but that short-term boost has faded quickly as investors have dissected this company in every which way.

Use their free survey tools but avoid paying for the paid version and don’t buy the stock.

There are many other fishes in the sea.