Mad Hedge Technology Letter

May 22, 2023

Fiat Lux

Featured Trade:

(BUY EMERGING CHIP COMPANIES ON BIG DIPS)

(SWKS), (CRUS), (QRVO)

Mad Hedge Technology Letter

May 22, 2023

Fiat Lux

Featured Trade:

(BUY EMERGING CHIP COMPANIES ON BIG DIPS)

(SWKS), (CRUS), (QRVO)

So what about these small chip companies that attach themselves to Apple’s future?

The ones like Qorvo (QRVO), Skyworks Solutions (SWKS), and Cirrus Logic (CRUS).

Many refuse to invest in them because they are too reliant on Apple.

I would argue the exact opposite.

It’s exactly because they have strong relationships with Apple that readers need to invest in these stocks.

The issue is that they are highly volatile and missing the optimal entry point can mean the difference between a profit and a loss.

Apple can’t develop everything internally.

It’s just too much to do.

I don’t believe the tech giant could gradually replace most of its third-party components with first-party ones.

Furthermore, I do not see Apple abruptly swapping suppliers or canceling an existing supplier's orders with its competitors to secure lower prices.

As a result, most of Apple's suppliers can negotiate favorable terms.

For 2023, iPhone shipments appear stable as the market continues to recover from weak demand and ongoing macroeconomic challenges, but I believe this is just a short-term blip.

Cirrus Logic mainly sells audio converters and chips, but it also develops other mixed-signal processing chips for wireless headsets, wearables, augmented reality/virtual reality (AR/VR) headsets, notebook computers, and mobile devices. Apple installs Cirrus' audio chips and IC controllers in its iPhones, iPads, and Macs.

Skyworks produces a wide range of wireless chips for the mobile, automotive, home automation, wireless infrastructure, and industrial markets. Apple installs Skyworks' wireless chips in its iPhones, iPads, Macs, Apple Watches, and other devices.

Lumentum is a diversified supplier of optical chips for service providers, 3D-sensing chips which are used in mobile devices, cars, 3D printers, and other industrial machines, as well as commercial lasers for manufacturing various products. Apple uses Lumentum's 3D-sensing chips and lasers to power its Face ID features.

These companies bask in the glory of being connected to Apple when many other chip companies wish they were in the same position.

Cirrus relied on Apple for 79% of its revenue in 2022 and the gains from this contract are precisely why it is great to hold this company's stock.

Skyworks generated 58% of its revenue from Apple in fiscal 2022, while Lumentum generated 29% of its revenue from Apple in 2022.

The semiconductor industry has been prone to cycles. Periods of soaring demand are followed by periods of drought, causing some wild swings in many chip stocks. But some news reports predict that because of the demand for chips throughout the economy, these boom-bust cycles might be over.

Semiconductors are now going into various devices between 5G, cloud datacenters, phones, PCs, laptops, cars are using more and more semiconductors that the demand is becoming so diversified and that supply is becoming so expensive to bring on. It's going to be much more of a steadier business going forward, more like a steady growth business rather than a cyclical business with booms and busts.

Don’t believe the naysayers who urge investors to stay out of chip stocks because of overreliance. That is like saying Warren Buffet is too reliant on Apple which is false.

Wait for a big dip of 15% or 20% to invest in these small chip stocks.

Mad Hedge Technology Letter

January 29, 2019

Fiat Lux

Featured Trade:

(WHATS BEHIND THE NVIDIA MELTDOWN),

(QRVO), (MU), (SWKS), (NVDA), (AMD), (INTC), (AAPL), (AMZN), (GOOGL), (MSFT), (FB)

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.

Mad Hedge Technology Letter

January 14, 2019

Fiat Lux

Featured Trade:

(THE TECH DARLING OF 2019),

(TWLO), (MSFT)

Mad Hedge Technology Letter

January 10, 2019

Fiat Lux

Featured Trade:

(HERE’S THE CANARY IN THE COAL MINE FOR APPLE),

(AAPL), (SWKS), (AMZN), (TSLA)

A tech company in the jaws of the trade war dilemma is one to keep tabs on because this company leads Apple’s stock price.

Many industry analysts say that the market cannot recover unless Apple participates.

Paying homage to the sheer size of Apple is one thing, and the gargantuan size means that many other companies are positioned to feed off of Apple revenue model and rely on the iPhone maker for the bulk of their contracts.

Is this a dangerous game to play?

Yes.

But its better than having no business at all.

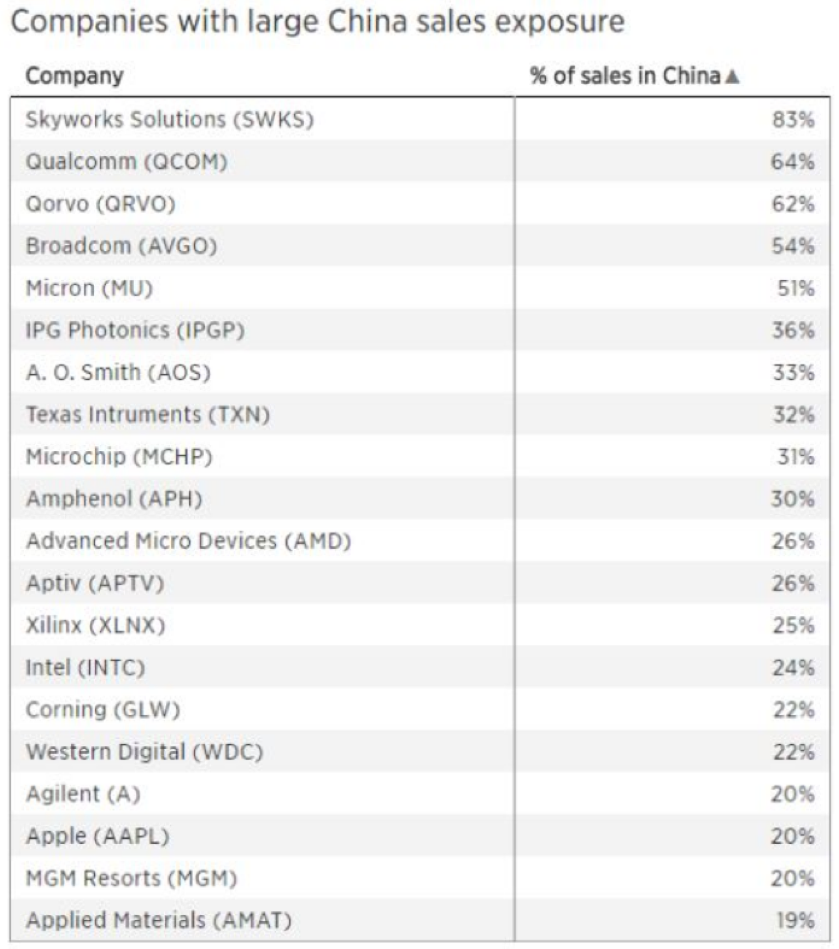

No stock epitomizes this strategic position better than niche chip stock Skyworks Solutions (SKWS) who extract 83% of total revenue from China.

Apple announced slashing production to its latest iPhone model by 10% in the first quarter due to weak sales.

Apple has also trimmed forecast for total iPhone production from about 48 million to between 40 and 43 million.

The company also failed to meet its latest projected forecast selling a disappointing 46.9 million in the fourth quarter of fiscal 2018, significantly lower than analysts’ expectation of 47.5 million units.

Then when you thought the bottom was in, President of the United States Donald Trump announced an escalation of tariffs from 10% to 25% on Chinese goods that could siphon off 10% of Apple’s revenue from China-produced iPhones.

All this means is that Skyworks Solutions (SWKS) is now the most oversold stock in the tech sector going from $123 about a year ago to about $63.

The avalanche of grumpy news has halted Apple in its track, but Skyworks Solutions is truly ground zero, the metaphorical canary in the coal mine.

The uncertainty that pervades this part of tech does what tech stocks abhor - puts a cap on Skyworks Solutions ceiling and the whole industry which peaked last year.

Containment is the absolute worst description of a tech because it tears apart any remnant of a growth narrative which tech firms need to justify the accelerating investment.

This is evident in how CEO of Tesla (TSLA) Elon Musk ran his business. If he didn’t convince and mesmerize the public with his antics and chutzpah, he might not have cultivated the star power to have pushed through a loss-making enterprise for so long.

Now the loss-making enterprise is history and Musk is finally turning a profit.

Now let’s turn to the chip sector – sling and arrows have been fired with some direct hits.

Samsung reported earnings and scared off investors with a dud.

Management presides over a huge drop in earnings making China and weak sales as the scapegoats.

Samsung’s first profits decline for 2 years could be a sign of things to come.

Chip momentum and earnings are decelerating. There is no getting around that.

Investors will need management to flush out the chip glut and need confirmation that prices have bottomed to really flesh out a legitimate turnaround later this fiscal year.

Samsung curtailed sales estimates by 10% and expect operating profits to sink 28.7% in 2019.

The walking wounded Korean chaebol has also been the recipient of a massive price war against Chinese smartphones, the end result being that consumers are favoring lower-priced Chinese substitutes that match Samsung’s Galaxy 80% of the way.

Remember that when you battle China tech companies – it’s a fight against the Chinese state who subsidizes these behemoths and have access to unlimited loans at favorable interest rates.

Apple has had the same problem, as well as Huawei and Xiaomi, have started producing premium smartphones. Second tier Chinese smartphone makers Oppo and Vivo have also picked up market share at the marginal buyer level.

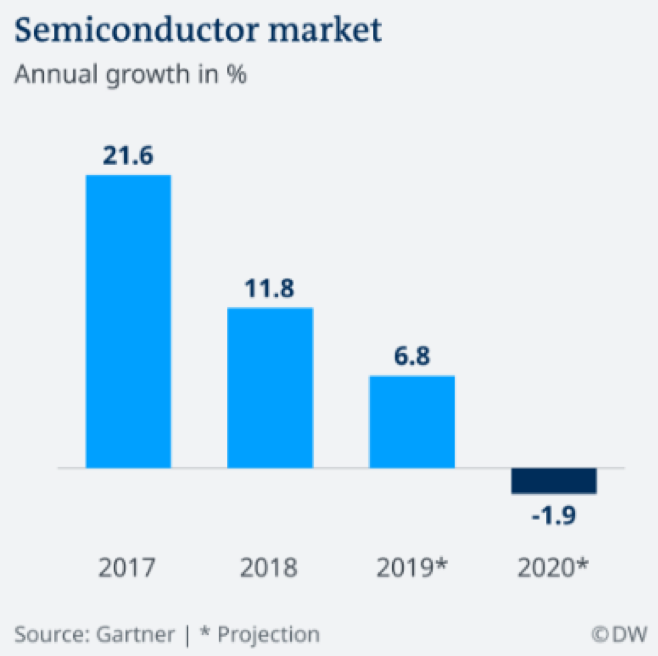

Semiconductor annual growth in 2018 held up quite well even though a far cry from 2017 when the semiconductor industry expanded 21.6%.

However, this year forecasts to only eke out 6.8% growth and then 2020 will turn negative with growth contracting 1.9%.

These dismal numbers could signal total revenue downshifting below total revenue numbers not seen since 2016.

In short, the chip industry is going backwards and backwards quickly.

I wouldn’t want to bet the ranch on any chip names now because the short-term prospects are grim.

The perfect storm of market saturation, overproduction, facetious geopolitics, weak demand, and unparallel competition is not a good cocktail of drivers towards accelerating earnings growth.

This is, in fact, a recipe for disaster.

And when you look at mobile, the phenomenon has been a true gamechanger and success but let’s face the facts, its already onto its 15th year and petering out.

There is only so much juice you can squeeze from a lemon.

Mobile will last for the time being until something better comes along which is absolutely what the tech markets are screaming for.

Tech companies have monetarily benefitted from this massive migration to mobile and there are still some hot croissants to take home from the bakery but I would estimate that 80% of the low-hanging fruit is off the tree.

That leads me to double down on my recent rant of a lack of innovation.

Google is still making most of its revenue from ad search and going 18 years strong, there will be no plans to stop even in year 30 and beyond.

Apple has been making iPhones for over 12 years.

Oracle is still selling the same dinosaur database software that has barely changed for a generation, except for the prettified front end.

Amazon is the only company that is brimming with innovation and that is the very reason why all companies must react to the Amazon threat because they set the terms of engagement.

The pipeline is fertile to the point its hard to keep track of all the new products coming out of the company.

Bezos has stayed head and shoulders ahead of the competition because the competition has gotten comfortable, content with above average market positioning, and gobbling up the profits.

Once companies start behaving this way, it is the beginning of the end.

Then there is Skyworks Solution.

Can you imagine if Apple ever announced a ground-breaking new product that would see them stop making iPhones?

Skyworks Solution would go out of business.

This elevated existential risk has nudged up the beta on this stock and it trades accordingly.

Apple’s price action lags Skyworks Solution’s, but the chip companies' booms and busts are more exaggerated.

On cue, Skyworks Solutions announced a cut in guidance from $1 billion in revenue to $970 million in 2019.

EPS would drop from an estimated $1.91 to $1.81-$1.84.

Skyworks president and CEO Liam Griffin said they were “impacted by unit weakness across our largest smartphone customers.”

A bottom looks to be forming unless the trade war turns for the worse again.

The silver lining is that Skyworks Solutions is in queue for some hefty 5G contracts for the upcoming network upgrade.

This would be Skyworks Solutions' chance to jump out of the ring of fire and attach themselves to alternative revenue that doesn’t shred their share price in a growing piece of the tech industry.

If Skyworks Solutions manages to successfully pivot to 5G and specifically IoT products, management will finally be able to wipe away the sweat bullets because welding yourself to Apple’s story hasn’t been heavenly as the global smartphone market has calcified.

Mad Hedge Technology Letter

December 20, 2018

Fiat Lux

Featured Trade:

(MICRON TECHNOLOGY BOMBS AGAIN)

(MU), (FDX), (UPS), (AAPL), (QRVO), (SWKS), (NXPI), (CRUS), (LITE),

If there was ever a canary in the coal mine, we got one with chipmaker Micron (MU) delivering weak earnings results missing on the top line but squeaking through a one-cent beat on the bottom line.

Love them or hate them, chip companies are susceptible to the boom-bust cycle that is a hallmark of the chip industry.

The beginning of the bust stage of the cycle is upon us with management detailing an “inventory adjustment” that put a damper on revenue.

Micron followed that up by reducing capex for next year and it will take 2-3 quarters to work off this bloated inventory channel.

The perpetrator to the inventory backlog is the smartphone industry.

President and CEO of Micron Sanjay Mehrotra particularly noted “high-end smartphones” as the malefactor tugging down the demand.

This is another damming testament to the prospects of Apple’s (AAPL) suppliers Quorvo (QRVO), Skyworks Solutions (SWKS), NXP Semiconductors (NXPI), Cirrus Logic (CRUS), and Lumentum Holdings (LITE) who can’t catch a break.

The last six months have fired a barrage of poison-tipped arrows at their core business and these stocks are squarely in the no-fly zone until Apple and the trade war can conjure up some good news.

To say these shares are oversold is an understatement, but we are in an extreme trading environment with volatility shooting up the wazoo.

Further reducing the glimmer, Chinese tariffs took up a worrying amount of the conference call dialogue. Investors found out that tariffs pinged half a percent of gross margins.

I have been outright bearish the chip industry from the middle part of the year and Micron is heavily reliant on China for about half of its revenues which is a death sentence in December 2018.

As the China risks have spiked after each head fake détente, so have the execution risks to chip companies with an overly reliant manufacturing process in China.

Not only has the execution risk ratcheted up, but the regulatory risk through costly tariffs is now eroding Micron’s margins.

If you thought that was a downer, then FedEx (FDX) made sure the nail was in the coffin by its ghastly earnings report.

The stock sold off hard confirming fears that global growth is decelerating.

Management did not mince their words about the state of the world and investors usually listen because FedEx is a reliable yardstick of the bigger global economy.

CEO of FedEx Fred Smith offered an olive branch painting a picture of a “solid” US economy, but the conundrum is that the US economy and any other country don't exist in a vacuum and that has been highly evident in Britain who is engaging in economic suicide by disengaging from the globalized world.

Smith cited Europe as a stumbling block and blamed the bulk of weak guidance on “bad political choices”, a thinly veiled dig at the poor level of governance carried out around the world lately.

I might chime in that it is quite strange when political parties and sovereign nations adopt the game of chicken as the leading political strategy applying it to everything and anything.

The side effects to business have been startling with management unable to assuage investor sentiment and business plans shredded apart because of impulsive policy moves.

Politicians aren’t grasping fully that stock market moves are inherently tied to the news cycle and the overwhelming volume of bad news that shouldn’t be as bad as it should be, has a multiplier effect on the stock market algos that go haywire.

It truly is the world of the algos and humans are living in their world and not the other way around.

The most important takeaway from FedEx is what they didn’t say.

Early development of the de-facto Amazon Airlines has already cost FedEx up to 3% of total volume growth.

And this is just the beginning.

Amazon is still feeling around for the rocks at the bottom while it tries to cross the river.

Once it masters logistics, expect a radical swivel towards the integration of their own airline into the bulk of Amazon.com’s package deliveries.

And when FedEx’s management claims that the market has gotten it wrong about the Amazon threat, that means the market is completely correct.

The market is always right.

Amazon’s master plan is to vertically integrate every last process down to the last mile, the doorbell, and now the microwave as Amazon has rolled out a myriad of smart home products.

FedEx management has to be blind to understand this won’t damage future sales.

It is materially false if FedEx thinks Amazon is not competing with them, and the sad part of this is there is not much FedEx can do about it.

The shipping giant cut its 2019 earnings forecast between $15.50 and $16.60 per share — from $17.20 to $17.80 a share.

FedEx’s goal of eclipsing $1.5 billion in operating income by fiscal 2020 has been shelved disappointing investors. FedEx cratered 12% on a day that saw the Fed do its best body slam imitation on the market.

The first phase of the logistics swivel is taking delivery of 40 planes and constructing a hub that will be able to operate 100 planes, then it will do as Amazon does with everything – scale it to the hills.

FedEx and UPS have a few years to figure out how to counteract this existential crisis and not decades.

Technology moves that fast now in this interconnected world.

Domestic volume comprises 17% of revenues at UPS and 19% at FedEx, management won’t be able to hide this problem under the carpet as the drag becomes highly visible like a sore thumb.

Analysts expect Amazon Air to offer more than slim savings to its business model saving between $2 to $4 per package next year.

The annual savings add up from $1 billion to $2 billion or 3% to 6% of its global shipping costs.

It is spot-on to admit that over the last few years, the explosion of packages during the holiday shopping season has put higher levels of stress on the U.S. Postal Service, UPS (UPS), and FedEx.

Even though overloaded with business, all three carriers have posted record levels of on-time deliveries and they appear to be handling the surge in volume.

But there will come a moment in time when an inflection point will give Amazon the keys to the car.

They will suddenly stop offering their e-commerce packages to these three carriers and business will drop off a cliff for them.

That is the future these three are confronted with and there is nothing they can do unless they build their own Amazon.com which is a pie in the sky dream at this point.

Amazon is out to prove they can execute the logistic part of their business cheaper and faster than anyone else because of the superior management and mountain of data they can act on.

I believe it will happen.

Part of stretching themselves with a new army of minions in Washington D.C., New York, and Nashville is partly about fulfilling the job of comprehensively and vertically integrating their e-commerce platform.

It will take a horde of workers to make this happen.

If the prophecy from FedEx management comes true and the global economy indeed softens next year, the stock will bear the brunt of the downside momentum and UPS too.

Stay away from the trio of deliverers. There are healthier fishes in the sea.

And as for the chip sector and Apple, wait on the sidelines for some good news.

Mad Hedge Technology Letter

November 13, 2018

Fiat Lux

Featured Trade:

(NO BIWEEKLY STRATEGY WEBINAR FOR WEDNESDAY NOVEMBER 14)

(WHY I HATE CHIP STOCKS)

(AAPL), (CY), (TXN), (LRCX), (KLAC), (LITE), (QCOM), (MU), (SWKS), (LSCC)