Mad Hedge Technology Letter

December 18, 2019

Fiat Lux

Featured Trade:

(CYBER SECURITY IS STILL A BUY)

(SYMC), (PANW), (CSCO), (FTNT), (AAPL), (MSFT)

Mad Hedge Technology Letter

December 18, 2019

Fiat Lux

Featured Trade:

(CYBER SECURITY IS STILL A BUY)

(SYMC), (PANW), (CSCO), (FTNT), (AAPL), (MSFT)

What does the technology sector’s “last gasp up” mean for tech stocks?

At the Mad Hedge Lake Tahoe Conference in late October, I correctly identified that the tech sector would experience a last leg to the price appreciation that has been part of a broader 10-year bull market in American equities.

The past 7 weeks have been nothing short of spectacular for tech shares as not only have the heavy hitters delivered in spades, like Apple (AAPL) and Microsoft (MSFT), but tech growth shares have been released from the penalty box after a short-dated growth scare and joined the rally with zeal.

How long will the “last gasp up” last?

The bar was set exceptionally low in 2019 because senior management spun the trade war acrimony into the accounting calculus effectively offering CFOs a chance to lower expectations to the point of getting away with murder.

Even with earnings’ expectations reset at nadir data points, performance was a mixed bag.

Superior tech companies were able to jump over the pitiful expectations, then if that wasn’t enough, they pushed backwards any inklings of earnings growth by guiding as low as they possibly could.

An archetypal example is Palo Alto Networks (PANW) whose shares dipped more than 8.5% in pre-market trading after issuing their quarterly earnings report.

The company announced sales of $771.9 million with an adjusted EPS of $1.05 topping analysts' estimates.

Why did shares sully?

Palo Alto Networks tanked guidance by telling investors they expect sales between $838 million and $848 million in the second quarter.

The expectation represented a midpoint sales forecast of $843 million, which is lower than the consensus estimates of $845.12 million.

The adjusted EPS in the second quarter is estimated to be $1.11–$1.13, below the consensus earnings forecast of $1.30.

Palo Alto Networks is forecasting sales between $3.44 billion and $3.46 billion with an EPS between $4.9 and $5.0 for next year, compared to analyst projections of $3.46 billion in revenue and an EPS of $5.07 in 2020.

PANW accounts for a big piece of the pie in the cybersecurity trade comprising 16.2% in 2019.

Overall industry growth is strong at 10.4%, and PANW managed to increase its sales by 22.3% to $633.7 million.

This cybersecurity company is one of my favorite tech stalwarts and is as rock-solid as they come for a second-tier tech growth company.

Another trend that dovetails closely with the last gasp up thesis is buying growth.

At this stage in the tech cycle, the low hanging fruit has been plucked and tech companies are increasingly finding it hard to generate organic growth.

Companies are now resorting to inorganic growth with Palo Alto Networks announcing that it will acquire Aporeto for $150 million in an all-cash transaction.

This isn’t just a one-off for PANW, they have acquired four other companies in 2019 to plug into their growth puzzle.

They have also completed the acquisition of an IoT cybersecurity firm Zingbox.

Palo Alto Networks acquired two cloud security startups in July as well - Demisto to gain traction in the AI security segment and Twistlock, the leader in container security.

The other top players in this field are Cisco (CSCO), Fortinet (FTNT) and Symantec (SYMC).

The bullish secular trend in cybersecurity is watertight and comments from Nikesh Arora, CEO of Palo Alto Networks, only reconfirmed the strength in cybersecurity when he said, “As a growing number of organizations move their business to the cloud, developers increasingly rely on cloud-native technologies such as containers and serverless infrastructure to accelerate the development, testing, and deployment of modern applications and services.”

What’s next for investors?

Barring any exogenous shocks, the last gasp up continues and recent macro policy developments have supported this hypothesis as well as the tailwinds of an improving economy.

Palo Alto Networks is part of a high growth segment and many corporates are on record contemplating lower enterprise tech spending heading into 2020.

This sets up another incredibly low bar for cybersecurity companies to hop over next year and I believe the best in show such as PANW, Fortinet, Cisco, and Symantec will pass with flying colors.

The interesting acid test will occur at the end of 2020 when tech firms and sub-segments of tech such, as cybersecurity, release commentary on whether 2021 guidance could signal ensuing risk of being dragged into recessionary turbulence.

A 2021 tech sector recession is certainly not priced into current tech share valuations in this frothy period of asset appreciation.

Mad Hedge Technology Letter

April 10, 2019

Fiat Lux

Featured Trade:

(TAKE A 2020 RAIN CHECK WITH SYMANTEC)

(SYMC), (FTNT), (PANW),

If you said I am going to the well too many times with this enterprise software theme, I would say you are out of your mind.

Next up is Symantec Corp. (SYMC) who offers global cybersecurity products, services, and solutions, and will be a primary beneficiary of the acceleration of network security products that expanded 12.6% YOY in 2018 and a secondary beneficiary to the migration to enterprise software.

The uptick in gorging cybersecurity products helps reflect the strongest industry metrics since analytics started tracking cybersecurity figures.

As more corporations take the leap of faith and splurge on data centers to house digital secrets, cloud service providers will store corporate data on these massive server farms and perimeter protection software is needed to guard against trojan horses and other malware.

This development has led to a vibrantly healthy market for firewall products, a traditional cybersecurity tool applied to block access to portions of a corporate network from the outside internet.

Firewall products weren’t shy registering 16.3% YOY growth to $2.4 billion in Q4 2018.

Advanced threat protection products used to find more sophisticated and modern offshoots of malicious software exploded to $416 million in Q4 2018, up 19.1% YOY.

Where does it stop?

Nobody knows, but the internet is becoming more of a chaotic free-for-all, and corporations existing for the sheer purpose of maximizing shareholder value will need to dole out an extra layer or two of digital protection.

Remember executive careers can be ruined from corporate cyberespionage these days and being the guy who lets the North Korean cyber army through the front door to fleece proprietary data isn’t a great pitch for a future executive gig.

The thorny Huawei issue has also heightened awareness of this sensitivity of security issues demonstrating how American tech prowess can be looted in a zero-sum cross-border game.

Internet users have also experienced a sudden balkanization of the web by totalitarian governments ready to weaponize the internet where they see fit while clamping down on freedom of expression on expressions that aren’t favorable to the interests above.

The orange alert climate has forced corporations to rush into cybersecurity products and my two favorite companies in this sphere are Palo Alto Networks, Inc. (PANW) and Fortinet, Inc. (FTNT).

I cannot say that Symantec is a better company than these two, it wouldn’t be true because their model doesn’t have the super growth trajectory when you analyze them head to head.

But this year should be an improvement on last year and I see room to the upside.

Every important metric will improve, aided by a return to better-calibrated execution, stabilization in business mix, and the benefit of revenue already on the balance sheet.

Operating margins slightly beat guidance with a 32% upswing last quarter and strong cash flow from operations of $377 million in the third quarter meant the company is more profitable.

Enterprise Security chipped in with revenue of $616 million, $31 million above the high end of the guidance range, and after a turbulent first half of 2018, Enterprise Security is back to organic growth of 3%.

And the main reason this company won’t be a massive winner is because of the lack of top-line growth indicating expansion in fiscal 2019 of only 1.5% in total revenue comprising of relatively flat revenue for Enterprise Security and 3% growth for the Consumer Digital Safety division.

Not good enough in the tech world of today.

Remember that the Consumer Digital Safety division contributes 49% to the top line while Enterprise Security only makes up 15%.

I believe this amounts to serious weakness in their business model because it should be the other way around to take advantage of the fast-growing enterprise business market and the even better margins.

The sluggish growth has hit shares with the chart flat as a pancake if you string it out the past 5 years with undulation in between.

The top line growth from 2017 to 2018, went from $4.02B to $4.83B and was a revelation, yet management has begged for more time with its prognosis of flat revenue for 2019.

Symantec will compensate for the lack of revenue growth with slightly better profitability maintaining a 30% operating margin, and predicting cash flow from operations for fiscal year 2019 to be in the range of $1.25B to $1.35B, a nice bump from the total cash flows from operations of $950 million in fiscal year 2018.

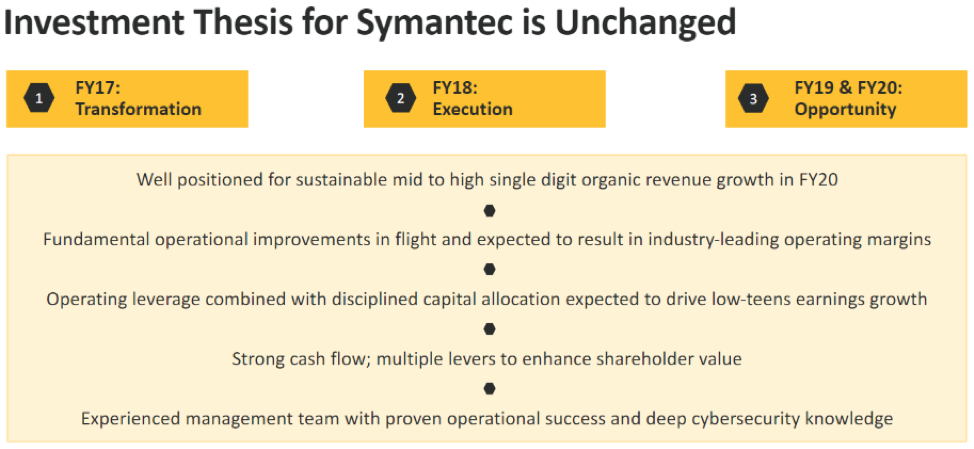

The catalyst to share appreciation is hidden in between the lines with management hyping up 2020 as the period when Symantec gets its mojo back with mid-single digit growth, with the Enterprise Security segment particularly benefiting from organic revenue expanding in the mid to high single digits from 2019.

A roll-off from existing contract liabilities will boost the Consumer Digital Safety segment but will not demonstrate any meaningful organic revenue growth projected to be unchanged at the low to mid-single digits YOY.

This sets up nicely for 2020 – the company expects a boost in operating margins to mid-30s and expected EPS growth in the low double digits with cash flow from operations benefitting from the 2019 restructuring, transition and transformation effort.

In short, they had a poor 2018 and Symantec’s management is telling investors to allocate downtime to fix the firm - growth will be missing this year, but they will be more profitable than last year, albeit with flat revenue.

The jury will be out in 2020 which is when they promised to have all their ducks in a row.

Even though they aren’t promising double-digit revenue growth in 2020, the high single-digit growth could see shares slowly grind up for the rest of this year.

This is another example of how legacy companies get stuck digging themselves out of a sinkhole before they can hyper-energize their profit model.

They are still in a holding pattern and I am neutral to slightly bullish on Symantec shares.