Below please find subscribers’ Q&A for the April 28 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA.

Q: There is talk of digital currencies being launched in the US. Is there any truth to that? How would that affect the dollar?

A: There is no truth to that; there is not even any serious discussion of digital currency at the US Treasury. My theory has always been that once Bitcoin works and is made theft-proof, the government will take it over and make that the digital US dollar. So far, Bitcoin has existed regulation-free; in fact, the IRS is counting on a trillion dollars in capital gains being taxed going forward in helping to address the budget deficit.

Q: If you have a choice, what’s the best vaccine to get?

A: The best vaccine is the one you can get the fastest. I know you’re a little slow on the rollout in Canada. Go for Pfizer (PFE) if you’re able to choose. You should avoid Moderna (MRNA) because 15% of people getting second shots have one-day symptoms after the second shot. But basically, you don’t get to choose, only kids get to choose because only Pfizer has done trials on people under the age of 21. So, if you take your kids in, they will all get Pfizer for sure.

Q: Should I buy Freeport McMoRan (FCX) here or wait for a bigger dip?

A: Freeport has just had a 25% move up in a week. I wouldn’t touch that. We put out the trade alert when it was in the mid $30s, and it's essentially at its maximum profit point now. So, you don't need to chase—wait for a bigger dip or a long sideways move before you get in.

Q: How do I trade copper if I don't do futures?

A: Buy (FCX), the largest copper producer in the US, and they have call options and LEAPS. By the way, if we do get another $5 dip in Freeport, which we just had, I would really do something like the (FCX) $45-$50 2023 LEAP. You can get 5 times your money on that.

Q: Time to buy oil stocks (USO) for the summer?

A: No, the big driver of oil right now is the pandemic in India. They are one of the world's largest consumers—you find out that most poor countries are using oil right now as they can’t afford the more expensive alternative sources of power. And when your biggest customer is looking at a billion corona cases, that’s bad for business. Remember, when you trade oil, you’re trading against a long-term bear trend.

Q: Would you buy Delta Airlines (DAL) at today’s prices?

A: Yes, I’m probably going to go run the numbers on today's call spread; I actually have 20% of cash left that I could spend. So that looks like a good choice—summer will be incredible for the entire airline industry now that they have all staved off bankruptcy. Ticket prices are going to start rising sharply with an impending severe aircraft shortage.

Q: What are your thoughts on the Buffet index which shows that stocks are more stretched vs GDP at any time vs 2000?

A: The trouble with those indicators is that they never anticipated A) the Fed buying $120 billion a month in US Treasury bonds, B) the Fed promising to keep interest rates at zero for three years, and C) an enormous bounce back from a once-in-a-hundred-year pandemic. That's why not just the Buffet Index but virtually all technical indicators have been worthless this year because they have shown that the market has been overbought for the last six months. And if you paid attention to your indicators, you were either left behind or you went short and lost your shirt. So, at a certain point, you have to ignore your technical indicators and your charts and just buy the damn market. The people who use that philosophy (and know when to use it, and it’s not always) are up 56% on the year.

Q: What trade categories are getting fantastic returns? It’s certainly not tech.

A: Well, we actually rotated out of tech last September and went into banks, industrial plays, and domestic recovery plays. And you can see in the stocks I just showed you in our model portfolio which one we’re getting the numbers from. Certainly, it was not tech; tech has only performed for the last four weeks and we jumped right back in that one also with positions in Microsoft (MSFT). So yes, it’s a constantly changing game; we’re getting rotations almost daily right now between major groups of stocks. The only way to play this kind of market is to listen to someone who’s been practicing for 52 years.

Q: I am 83 years old and have four grandchildren. I want to invest around $20,000 with each child. I was thinking of your bullish view on Tesla (TSLA) on a long-term investment. Do you agree?

A: If those were my grandchildren, I would give them each $20,000 worth of the ProShares Ultra Technology Fund (ROM), the 2x long technology ETF. Unless tech drops 50% from here, that stock will keep increasing at twice the rate of the fastest-growing sector in the market. I did something similar with my kids about 20 years ago and as a result, their college and retirement funds for their kids have risen 20 times. So that’s what I would do; I would never bet everything on a single stock, I would go for a basket of high-tech stocks, or the Invesco QQQ NASDAQ Trust (QQQ) if you don’t want the leverage.

Q: Do you like Amazon (AMZN) splitting?

A: I don’t think they’ll ever split. Jeff Bezos worked on Wall Street (with me at Morgan Stanley) and sees splits as nothing more than a paper shuffle, which it is. It’s more likely that he’ll break up the company into different segments because when they get to a $5 trillion market cap, it will just become too big to manage. Also, by breaking Amazon up into five companies—AWS, the store, healthcare, distribution, etc., —you’re getting a premium for those individual pieces, which would double the value of your existing holdings. So, if you hold Amazon stock, you want it to face an antitrust breakup because the flotation will double the value of your total holdings. That has happened several times in the past with other companies, like AT&T (T), which I also worked on.

Q: When is Tesla going to move and why is it going up with earnings up 74%?

A: Well, the stock moved up a healthy 46% going into the earnings; it’s a classic sell the news market. Most stocks are doing that this quarter and they did so last quarter as well. And Tesla also tends to move sideways for years and then have these explosive moves up. I think the next double or triple will come when they announce mass production of their solid-state batteries, which will be anywhere from 2 to 5 years off.

Q: How can I renew my subscription?

A: You can call customer support at 347-480-1034 or email support@madhedgefundtrader.com and I guarantee you someone will get back to you.

Q: Top gene-editing stock after CRISPR Therapeutics (CRSP)?

A: There are two of them: one is Intellia (NTLA); it’s actually done better than CRISPR lately. The second is Editas (EDIT) and you’ll find out that the same professionals, including the Nobel prize winner Jennifer Doudna here at Berkeley, rotate among all three of these, and the people who run them all know each other. They were all involved in the late 2000's fundamental research on CRISPR, and they’re all frenemies. So yes, it's a three-company industry, kind of like the cybersecurity industry.

Q: What about PayPal (PYPL)?

A: I would wait for the earnings since so many companies are selling off on their announcements. See if they sell off 3-5%, then you buy it for the next leg up. That is the game now.

Q: Do you like any 3D printing stocks like Faro Technologies (FARO)?

A: No, that’s too much of a niche area for me, I’m staying away. And that's becoming a commodity industry. When they were brand new years ago, they were red hot, now not so much.

Q: Do you see the chip companies continuing their bull run for the next few months?

A: I do. If anything, the chip shortage will get worse. Each EV uses about 100 chips, and they’re mostly the low-end $10 chips. Ford (F) said production of a million cars will be lost due to the chip shortage. Ford itself has 22,000 cars sitting in a lot that are fully assembled awaiting the chips. Tesla alone has $300 worth of chips just in its inverters, and there are two inverters in every car. So, when you go from production of 500,000 cars to a million in one year, that's literally billions of chips.

Q: The airlines are packed; what are your thoughts?

A: Yes, one of the best ways to invest is to invest in what you see. If you see airlines are packed, buy airline stocks. If you can’t hire anyone, you know the economy is booming.

Q: What about the Russel 2000 (IWM)?

A: We covered it; it looks like it wants to break out to new highs from here. By the way, there are only 1,500 stocks left in the Russell 2000 after the pandemic, mergers, and bankruptcies.

Q: Are there other ways to play copper out there like (FCX)?

A: Yes; one is the (COPX)— a pure copper futures ETF. However, be careful with pure metal ETFs of any kind because they have huge contangos and you could get a 50% move up in your commodity while your ETF goes down 50% over the same time. This happens all the time in oil and natural gas, and to a lesser degree in the metals, so be careful about that. Before you get into any of these alternative ETFs, look at the tracking history going back and I think you'll see you're much better off just buying (FCX).

Q: How long do you typically hold onto your 2-year LEAPS? Based on my research, the time decay starts to accelerate after about 3 months to one year on LEAPS.

A: Actually, with LEAPS, the reason I go out to two years is that the second year is almost free, there's almost no extra cost. And it gives you more breathing room for this thing to work. Usually, if I get my timing right, my LEAP stocks make big moves within the first three months; by then, the LEAP has doubled in value, and then you have to think about whether you should keep it or whether there are better LEAPS out there (which there almost always are). So, you sell it on a double, which only took a 30% move in the stock, or you may be committed to the company for the long term, like a Microsoft or an Amazon. And then you just run it through the expiration to get a 400% or 500% profit in two years. That is how you play the LEAP game.

Q: Are these recorded?

A: Yes, we record these and we post them on the website after about 2 hours. Just log into the site, go to “my account”, then select your subscription type (Global Trading Dispatch or Technology Letter), and “webinars” will be one of the button choices.

Q: Can you also sell calls on LEAPS?

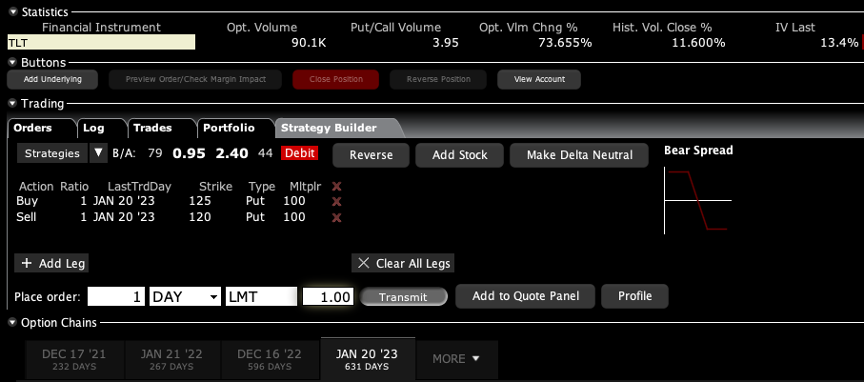

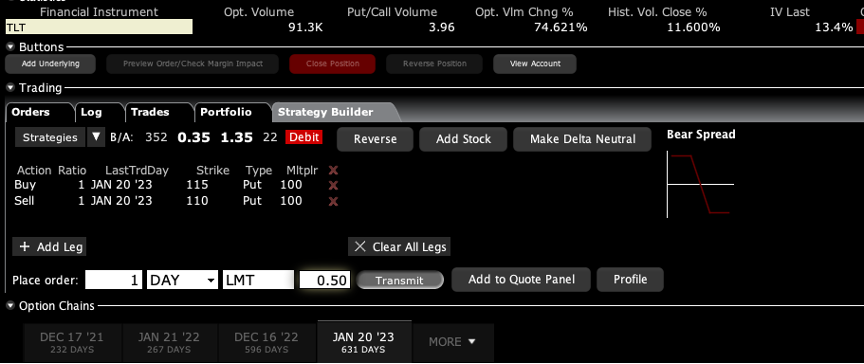

A: Yes and the only place to do that is the US Treasury market (TLT). There you either want to be short calls far above the market, out two years, or you want to be long puts. And by the way, if you did something like a $120-$125 put spread out to January 2023, then you’re looking at making about a 400% gain. That is a bet that 20-year interest rates only go up a little bit more, to 2.00%. If you really want to bet the ranch, do something like a $120-$122 and you might get a 1000% return.

Q: What is the best LEAP to trade for Microsoft (MSFT)?

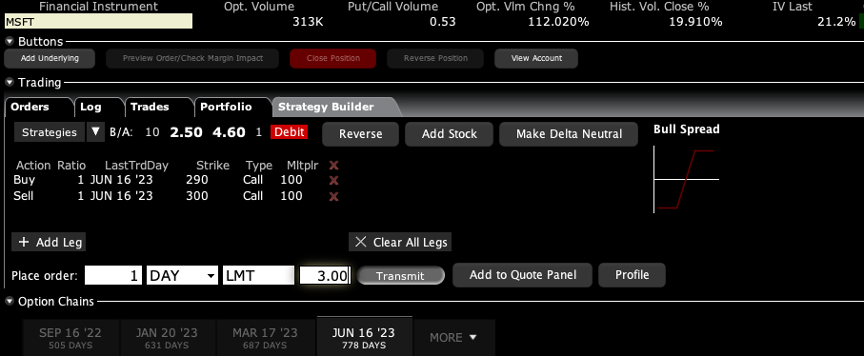

A: If you want to go out two years, I would do something like a June 2023 $290-$300 vertical bull call spread. There is an easy 67% profit in that one on only a 20% rise in the stock. I do front monthlies for the trade alert service, so we always have at least 10 or 20 trade alerts going out every month. And the one I currently have for is a deep in the money May $230-$240 vertical bull call spread which expires in 12 days.

Q: What is the best way to play Google (GOOG)?

A: Go 20% out of the money and buy a January 2023 $2,900-$3,000 vertical bull call spread for $20—that should make about 400%. If you want more specific advice on LEAPS, we have an opening for the Mad Hedge Concierge Service so send an email to support@madhedgefundtrader.com with subject line “concierge,” and we will reach out to you.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

I Think I See Another Winner

https://www.madhedgefundtrader.com/wp-content/uploads/2019/11/john-rifle.png700525Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-30 09:02:212021-04-30 12:12:05April 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the February 17 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Are we buying gold on dips?

A: Not yet. As long as you have a ballistic move in bitcoin going on, you don't want to touch gold. Eventually gold does get dragged up by the global bull market in commodities, but silver is more preferable since it moves up at twice the rate of gold in bull markets.

Q: Is it time to buy Amazon (AMZN) LEAPS?

A: Yes, I am looking for a move to $5,000 a share in Amazon with the onset of enormous GDP figures. Exploding consumer spending may be what breaks Amazon out of its current six-month range. I would do something like a two-year LEAP with the $3,600-$3,700 in Amazon. Be cautious and stay near the money. You should get like a 400% or 500% return on that LEAP at expiration, or sooner.

Q: What's your view on Tesla (TSLA)?

A: It looks tired—lower lows, lower highs. We’re in a short-term downtrend that could last several months. I’m holding off on buying Tesla until we find a bottom. I just have one $150 out-of-the-money call spread that expires in 20 days, and that’s it. We paired our position way back on Tesla. Wait for the market to come to you, if you can get Tesla under $700, that's a great time to buy LEAPS on Tesla.

Q: Are you still bearish on energy (XLE)?

A: Short term no, long term yes. You’re trying to catch a rally in a long-term bear market. Some people can do that, some people can’t. It’s the next buggy whip industry, the next American Leather, which completely vaporized.

Q: What about the calls for $100 oil (USO)?

A: Yes, after the markets went up $10 dollars in a day you always see calls for $100 oil. If the energy crisis in Texas shows us anything, it’s that we have to move away from oil as an energy source much faster than we thought because its distribution and production system freeze.

Q: Are you expecting a short-term correction (SPY)?

A: Yes but no more than 4%; there is still too much cash on the sidelines.

Q: Have airline leisure stocks run too far?

A: No, they are coming off of much lower lows so they can go to much higher highs. Almost all restrictions should be gone in six months—I’m trying to time my Australia trips and I think in six months may get to the point where, if you show proof of vaccination and submit to a 3 day test, they will let you into the country. But in six months you won’t be able to get an airline or hotel reservation.

Q: What about the AT&T (T) yield play and 5G play?

A: Yes, I still like AT&T and you should probably buy it about here. All these legacy telecom companies are going to have big moves once 5G accelerates allowing a vast expansion of streaming and other high-end services.

Q: Is CRISPR (CRSP) a good LEAP candidate?

A: Yes, and you can do something like the $200-$210 two years out because it’ll almost certainly get taken over before then.

Q: What’s a good LEAP for Tesla?

A: Wait for it to drop to $700 first and then buy something like the $900-$1000 two years out.

Q: What do you think of Apple?

A: Apple (AAPL) is taking a rest waiting for the 5G rollout to reaccelerate. Our target for Apple this year is $200.

Q: Do we sell in May and go away?

A: I would just go away and keep all your longs. The trouble is, trying to be ultra-smart and time all this stuff in a runaway bull market, you find it a lot harder to get in when you come back; you go “oh my gosh these things are up so much,” you don’t buy anything, and then it doubles. I’ve seen that a lot in the past, New York in 1971, Tokyo in 1987, Dotcom stocks in 1985, add US stocks in 2015.

Q: What do you think of Riot (RIOT) stock?

A: Wouldn't touch it with a ten-foot pole. If I didn’t want to buy bitcoin at $1, I'm not going to want to buy it at $51,000. Go elsewhere for your bitcoin advice, except you’ll hear the same thing: it will go up because it’s gone up. You should use it as a risk indicator. That’s essentially what all bitcoin analysts will tell you because there's nothing to analyze. There are no earnings, there's not even any physical presence anywhere to analyze, no customer support. If you can get seven 10 baggers like we did last year, with Zoom (ZM), Roku (ROKU), Tesla (TSLA), and Nvidia (NVDA) —why bother with cryptocurrencies?

Q: What are your thoughts on travel?

A: My take is that leisure travel is returning in mass but that the business travelers will shy away; and that will be true for this year but probably not next year. I think business travel will come back once it’s 100% safe and once all the companies are making money again and can afford travel.

Q: Is Trilogy Metals Inc. (TMQ) a good buy? It has Copper, Zinc, and some exposure to Gold and Silver.

A: Yes, it is a buy. Most commodity prices should double from these levels; and probably the smartest ones to buy are the ones that haven't moved yet—gold and silver, but silver especially. The world will come roaring back and it needs every possible metal it can get its hands on.

Q: What do you think of the cannabis stocks (TLRY), (ACB)?

A: That is one of several small bubbles in the markets that I don't want to touch at all. How hard is it to grow a weed? Barriers to entry are zero. Massive competition from the black market, as about 30% of the cannabis demand is still going to your local drug dealer who doesn’t have to pay taxes, whereas you get double taxed with a pot company—35% retail sales taxes and then taxes on the profits on top of that. So no thank you, Mary Jane.

Q: Do you think Warren Buffet is still the leading thought contributor to personal finance, or is he outdated?

A: Berkshire Hathaway is up 10% this year, and the Dow is up only 2.8%, so I would say he’s still pretty well in touch with the markets; and he has very heavy weightings in Coca Cola (KO), Financials (XLF), and Apple (AAPL), as well as some energy stocks. Good discipline and good strategy never go out of style.

Q: Is the Texas energy disaster going to set the US’ way on renewable energy faster?

A: Yes, it does force people to consider the move into alternative energy sources much faster, especially when the old energy sources go to zero and then have whole states lose their power sources. Look how the governor of Texas is blaming frozen windmills, which only account for 7% of the Texas energy supply. What a joke! I’ll lend him my hairdryer and they’ll work. Notice the propensity to immediately blame others for their own mistakes. That is terrible leadership. Texas is going to turn blue.

Q: Is climate change overhyped in the US stock market?

A: Absolutely yes, that’s why I haven’t been buying any of these. They tend to be smaller companies, and ever since Biden got the lead in the primaries and the polls last spring this whole sector, and ESG investing in general, has been on an absolute tear and is wildly expensive. I call these feel-good stocks; people buy them because they make them feel good but very few of these actually make real money. I prefer to stick to the real money plays of which there are more than enough around.

Q: Do you like rare earth such as the Van Eck Vectors Rare Earth/Strategic Metals ETF (REMX)?

A: I do like rare earths. You need them for practically anything electronic. China's been withholding supplies again, which they like to do from time to time just to rattle our cage because we need them for all our weapons systems. But this is also prone to bubbles, so be careful when you buy it that you’re not paying up too much. By the way, the (REMX) ETF was brought out at the absolute peak of the last rare earth bubble, which we covered extensively 11 years ago. We got people in at the very bottom of rare earth, and things went up ten times. Then we got everybody out and people said I was being bearish too soon, so I never got invited to conferences again. After that, it went down for eight straight years.

Q: Don’t you think frozen windmills and solar speak for more reliance on oil than less? Biden administration limits on oil will drive up prices.

A: You’re right on the second part; creating shortage of supply will cause price increases. But frozen windmills are a result of lack of capital investment and planning. It turns out all of the windmills in the northern part of the US have electric heaters, so they don’t freeze because it gets colder up there. They didn’t do that in Texas to save money, and now they have lost about 7% of the total Texas energy supply. So bad management was the issue there. Penny-wise and pound-foolish.

Q: Are commodities in general in play? What is the best ETF for commodities?

A: The trouble with commodities is there is no one big catch all commodity ETF. However, you can expect one soon; as things peak or have big runs, they tend to generate new ETFs like new children because the demand is there. In the commodities world, there are lots of individual 1x and 2x ETFs like the gold ETF (GLD), the silver (SLV), the copper (CPER), and so on. But there isn’t one good basket I’ve found. You can always create your own by buying small amounts of each of the leading companies, which is probably the best thing to do.

Q: What is the best property value right now?

A: That would be Mississippi; they have the lowest housing prices in the United States. Unfortunately, low cost of living, low tax states also have the worst education systems, which doesn’t matter of course if you don't have kids. In the end, you get what you pay for. It’s OK if you don’t mind dealing with stupid people every day, which I do. I can always tell when I’m dealing with customer support in the deep south because literacy falls off a cliff.

Q: Should we get a 10% correction soon?

A: Probably not; the last 10% correction needed a presidential election to scare the daylights out of you, and there's nothing like that on the horizon now. Maybe we’ll get another 5% correction on a game stop type incident, but there's just too many people trying to get into the stock market now. People who were selling last March/April are the same people who are buying now.

Q: Is there a bright future for hydrogen?

A: No, electricity is infinitely scalable, and hydrogen isn’t. It’s about as scalable as gasoline because you have to move it around in big tankers, keep it at 434.5 degrees Fahrenheit below zero, which is very expensive and has an unfortunate tendency to blow up. So, I never bought into the hydrogen thesis, except for local use of fleets where everyone gets all their hydrogen from a central facility.

Q: What will be the best performing sector in the next 1-3 months?

A: Your bond short and your financials. It’s the same trade. And it’s the one sector that no one asked about today.

Q: Do you think bitcoin is a bubble poised to pop at some point?

A: Yes, but who knows where that is; bubble tops are impossible to predict, especially when there are no valuation metrics. Bottoms can be measured with valuation metrics, but tops can’t because greed is an immeasurable quantity. However, it will certainly pop when they suddenly decide to increase the total outstanding number of bitcoins, which may seem unlikely now but is inevitable.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/john-thomas-tropics.png432324Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-19 10:02:082021-02-19 10:28:48February 17 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the January 6 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Incline Village, NV.

Q: Any thoughts on lithium now that Tesla (TSLA) is doing so well?

A: Lithium stocks like Sociedad Qimica Y Minera (SQM) have been hot because of their Tesla connection. The added value in lithium mining is minimal. It basically depends on the amount of toxic waste you’re allowed to dump to maintain profit margins—nowhere close to added value compared to Tesla. However, in a bubble, you can't underestimate the possibility that money will pour into any sector massively at any time, and the entire electric car sector has just exploded. Many of these ETFs or SPACs have gone up 10 times, so who knows how far that will go. Long term I expect Tesla to wildly outperform any lithium play you can find for me. I’m working on a new research piece that raises my long-term target from $2,500 to $10,000, or 12.5X from here, Tesla becomes a Dow stock, and Elon Musk becomes the richest man in the world.

Q: Won’t rising interest rates hurt gold (GLD)? Or are inflation and a weak dollar more important?

A: You nailed it. As long as the rate rise is slow and doesn't get above 1.25% or 1.50% on the ten-year, gold will continue to rally for fears of inflation. Also, if you get Bitcoin topping out at any time, you will have huge amounts of money pour out of Bitcoin into the precious metals. We saw that happen for a day on Monday. So that is your play on precious metals. Silver (SLV) will do even better.

Q: What are your thoughts on TIPS (Treasury Inflation Protected Securities) as a hedge?

A: TIPS has been a huge disappointment over the years because the rate of rise in inflation has been so slow that the TIPS really didn’t give you much of a profit opportunity. The time to own TIPS is when you think that a very large increase in inflation is imminent. That is when TIPS really takes off like a rocket, which is probably a couple of years off.

Q: Will Freeport McMoRan (FCX) continue to do well in this environment?

A: Absolutely, yes. We are in a secular decade-long commodity bull market. Any dip you get in Freeport you should buy. The last peak in the previous cycle ten years ago was $50, so there's another potential double in (FCX). I know people have been playing the LEAPS in the calendars since it was $4 a share in March and they have made absolute fortunes in the last 9 months.

Q: Is it a good time to take out a bear put debit spread in Tesla?

A: Actually, if you go way out of the money, something like a $1,000-$900 vertical bear put spread, with the 76% implied volatility in the options market one week out, you probably will make some pretty decent money. I bet you could get $1,500 from that. However, everyone who has gone to short Tesla has had their head handed to them. So, it's a high risk, high return trade. Good thought, and I will actually run the numbers on that. However, the last time I went short on Tesla, I got slaughtered.

Q: Any thoughts on why biotech (IBB) has been so volatile lately?

A: Fears about what the Biden government will do to regulate the healthcare and biotech industry is a negative; however, we’re entering a golden age for biotech invention and innovation which is extremely positive. I bet the positives outweigh the negatives in the long term.

Q: Oil is now over $50; is it a good time to buy Exxon Mobil (XOM)?

A: Absolutely not. It was a good time to buy when it was at $30 dollars and oil was at negative $37 in the futures market. Now is when you want to start thinking about shorting (XOM) because I think any rally in energy is short term in nature. If you’re a fast trader then you probably can make money going long and then short. But most of you aren't fast traders, you’re long-term investors, and I would avoid it. By the way, it’s actually now illegal for a large part of institutional America to touch energy stocks because of the ESG investing trend, and also because it’s the next American leather. It’s the next former Dow stock that’s about to completely disappear. I believe in the all-electric grid by 2030 and oil doesn't fit anywhere in that, unless they get into the windmill business or something.

Q: With Amazon buying 11 planes, should we be going short United Parcel Service (UPS) and FedEx (FDX)?

A: Absolutely not. The market is growing so fast as a result of an unprecedented economic recovery, it will grow enough to accommodate everyone. And we have already had huge performance in (UPS); we actually caught some of this in one of our trade alerts. So again, this is also a stay-at-home stock. These stocks benefited hugely when the entire US economy essentially went home to go to work.

Q: Should we keep our stay-at-home stocks like DocuSign (DOCU), Zoom (ZM), and UPS (UPS)?

A: They are way overdue for profit-taking and we will probably see some of that; but long term, staying at home is a permanent fixture of the US economy now. Up to 30% of the people who were sent to work at home are never coming back. They like it, and companies are cutting their salaries and increasing their profits. So, stay at home is overdone for the short term, but I think they’ll keep going long term. You do have Zoom up 10 times in a year from when we recommended it, it’s up 20 times from its bottom, DocuSign is up like 600%. So way overdone, in bubble-type territory for all of these things.

Q: Are telecom stocks like Verizon (VZ) and AT&T (T) safe here?

A: Actually they are; they will benefit from any increase in infrastructure spending. They do have the 5G trend as a massive tailwind, increasing the demand for their services. They’re moving into streaming, among other things, and they had very high dividends. AT&T has a monster 7% dividend, so if that's what you’re looking for, we’re kind of at the bottom of the range on (T), so I would get involved there.

Q: Should we sell all our defense stocks with the Biden administration capping the defense budget?

A: I probably would hold them for the long term—Biden won’t be president forever—but short term the action is just going to be elsewhere, and the stocks are already reflecting that. So, Raytheon (RTX), United Technologies (UT), and Northrop Grumman (NOC), all of those, you don’t really want to play here. Yes, they do have long term government contracts providing a guaranteed income stream, but the market is looking for more immediate profits, or profit growth like you have been getting in a lot of the domestic stocks. So, I expect a long sideways move in the defense sector for years. Time to become a pacifist.

Q: Is it safe to buy hotels like Marriott (MAR), Hyatt (H), and Hilton (HLT)?

A: Yes, unlike the airlines and cruise lines, which have massive amounts of debt, the hotels from a balance sheet point of view actually have come through this pretty well. I expect a decent recovery in the shares, probably a double. Remember you’re not going to see any return of business travel until at least 2022 or 2023, and that was the bread and butter for these big premium hotel chains. They will recover, but that will take a bit longer.

Q: How about online booking companies like Expedia (EXPE) and Booking Holdings Inc, owner of booking.com, Open Table, and Priceline (BKNG)?

A: Absolutely; these are all recovery stocks and being online companies, their overhead is minimal and easily adjustable. They essentially had to shut down when global travel stopped, but they don’t have massive debts like airlines and cruise lines. I actually have a research piece in the works telling you to buy the peripheral travel stocks like Expedia (EXPE), Booking Holdings (BKNG), Live Nation (LYV), Madison Square Garden (MSGE) and, indirectly, casinos (WYNN), (MGM) and Uber (UBER).

Q: What about Regeneron (REGN) long term?

A: They really need to invent a new drug to cure a new disease, or we have to cure COVID so all the non-COVID biotech stocks can get some attention. The problem for Regeneron is that when you cure a disease, you wipe out the market for that drug. That happened to Gilead Sciences (GILD) with hepatitis and it’s happening with Regeneron now with Remdesivir as the pandemic peaks out and goes away.

Q: What about Chinese stocks (FXI)?

A: Absolutely yes; I think China will outperform the US this year, especially now that the new Biden administration will no longer incite trade wars with China. And that is of course the biggest element of the emerging markets ETF (EEM).

Q: Will manufacturing jobs ever come back to the US?

A: Yes, when American workers are happy to work for $3/hour and dump unions, which is what they’re working for in China today. Better that America focuses on high added value creation like designing operating systems—new iPhones, computers, electric cars, and services like DocuSign, Zoom—new everything, and leave all the $3/hour work to the Chinese.

Q: What about long-term LEAPS?

A: The only thing I would do long term LEAPS in today would be gold (GOLD) and silver miners (WPM). They are just coming out of a 5-month correction and are looking to go to all-time highs.

Q: What about your long-term portfolio?

A: I should be doing my long-term portfolio update in 2 weeks, which is much deserved since we have had massive changes in the US economy and market since the last one 6 months ago.

Q: Do you have any suggestions for futures?

A: I suggest you go to your online broker and they will happily tell you how to do futures for free. We don’t do futures recommendations because only about 25% of our followers are in the futures market. What they do is take my trade alerts and use them for market timing in the futures market and these are the people who get 1,000% a year returns. Every year, we get several people who deliver those types of results.

Q: Will people go back to work in the office?

A: People mostly won’t go back to the office. The ones who do go back probably won't until the end of the summer, like August/September, when more than half the US population has the Covid-19 vaccination. By the way, getting a vaccine shot will become mandatory for working in an office, as it will in order to do anything going forward, including getting on any international flights.

Q: What is the best way to short the US dollar?

A: Buy the (FXE), the (FXY), the (FXA), or the (UUP) basket.

Q: Silver LEAP set up?

A: I would do something like a $32-$35 vertical bull call spread on options expiring in 2023, or as long as possible, and that increases the chance you’ll get a profit. You should be able to get a 500% profit on that LEAP if silver keeps going up.

Q: What about agricultural commodities?

A: Ah yes, I remember orange juice futures well, from Trading Places, where I also once made a killing myself. Something about frozen iguanas falling out of trees was the tip-off. We don’t cover the ags anymore, which I did for many years. They are basically going down 90% of the time because of the increasing profitability and efficiency of US farmers. Except for the rare weather disaster or an out of the blue crop disease, the ags are a loser’s game.

Q: Can we view these slides?

A: Yes, we load these up on the website within two hours. If you need help finding it just send an email or text to our ever loyal and faithful Filomena at support@madhedgefundtrader.com and she will direct you.

Q: Do you have concerns about Democrats regulating bitcoin?

A: Yes, I would say that is definitely a risk for Bitcoin. It is still a wild west right now and there are massive amounts of theft going on. It is a controlled market, with bitcoin miners able to increase the total number of points at any time on a whim.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/02/john-thomas-old-plane.png358466Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-08 10:02:392021-01-08 10:51:48January 6 Biweekly Strategy Webinar Q&A

Elliott Management’s dive into tech can be used as a leading indicator of which tech companies are great fixer-uppers.

Truth be told, Elliott Management, the vulture hedge fund, has a knack for finding those rusted cloud gems and polishing them shiny.

They don’t do this for free either, and making a killing on each of these turnaround stories usually has the same ruthless strategy.

Some of the prey were well-known within particular tech sector niches, like BMC, Novell and Informatica, but none were giants or household names.

Billionaire Paul Singer, notched sale after sale, reaping gains from the associated premiums on the acquisitions.

Most recently, his tech aspirations have increased with the pedigree of the company dwarfing in size he did before with stakes in eBay (EBAY), SAP, and AT&T (T).

This year, Elliott has already feasted on Twitter (TWTR) and SoftBank.

Part of the reason for slaying bigger dragons is because tech has gotten expensive with multiples expanding rapidly, and successfully leveraging usually works by going bigger and not smaller.

How does Elliott influence the change needed to raise the share prices?

First, getting his guys on the board to make decisions for the company.

He does this by getting his most trusted confidante and deal maker Jesse Cohn in the mix and he leads Elliott’s technology transactions.

He now sits on the boards of both eBay and Twitter.

Rather than scorching the earth for public change, he has worked in tandem with management at both companies.

Cohn is also supported by Elliott’s in-house Internet analysts, software analysts, operation analysts, consultants and stable of installed board members to help make decisions.

A decision they were at the forefront of was possibly firing Jack Dorsey at Twitter after identifying him as not maximizing profitability and revenue at Twitter.

Ultimately, Dorsey earned himself another quarter as CEO, but that’s how things work at Elliott, they run a tight ship.

Twitter said in a securities filing that a board committee formed this spring recommended that the current management structure remains in place for the time being.

The announcement gives Mr. Dorsey a reprieve after his performance was heavily criticized by Cohn and Elliott Management.

Twitter and Elliott reached an agreement in March in which the company agreed to appoint two board members and commit to $2 billion in share buybacks.

The agreement also included the formation of the new committee to study Twitter’s leadership, which effectively created a probation period for Mr. Dorsey to prove himself to the new investors.

So, does Elliott’s aggressive strategy work or fail?

The proof is in the pudding with Twitter shares up about 40% since bottoming out in March.

Twitter has expanded its userbase by about 23% since the fourth quarter of 2019.

So what now for Elliott?

Elliott is now one of the biggest investors in F5 Networks (FFIV), a Seattle company with a market value of about $8.8 billion.

They have spoken to the software company’s management about ways to appreciate the underlying shares which has not gone up in the past 365 days.

Shares have seriously underperformed to similar-sized cloud companies.

F5 Networks provides multi-cloud application services for the availability, security, performance, and availability of network applications, servers, and storage systems.

So far, they have announced plans to repurchase $1 billion worth of stock through fiscal 2022.

The buyback plan includes the accelerated repurchase of $500 million worth of stock in fiscal 2021.

The company said it targets double-digit adjusted earnings per share growth over the next two years and revenue growth of 6% to 7%, including software revenue growth CAGR of 35% to 40%.

These moves will help the company arrive at an inflection point in the transformation story where operating margins are poised to expand and revenue will accelerate, leading to sustainable double-digit growth

Elliott has also investigated some dubious decisions by F5’s management such as the company’s recent acquisitions of Shape Security Inc. and Nginx Software Inc., unhappy F5 overpaid without a clear integration strategy.

Elliott’ roadmap typically involves sizeable stakes in tech firms giving them the authority to throw their weight around behind the scenes.

Stock buybacks, acquiring company board seats, reducing expenses, acquisitions, wholesale management changes are part of their recipe for raising the stock price.

I have no reason to believe that Elliott will fail this time around after their string of tech successes and that leads me to recommend F5 Networks as a great buy the dip tech story.

The first stage of the turnaround is usually the most dramatic and noticeable with the follow-through to the flagging share price.

I wouldn’t be shocked if shares are up 25% from current prices in Q1 2021.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-11 12:02:282020-11-15 15:46:41The Vultures at Elliott Management

It will be inevitable – the 5G shift in 2020 will be delayed.

Last year, 5G was available on only about 1% of phones sold in 2019 and demand has cratered this year because of exogenous variables.

Up to just recently, Apple (AAPL) was the bellwether of the success of tech with wildly appreciating shares due to the expected ramp-up to a new 5G phone later this year.

Well, things are more complicated now.

I will be the first one to say it - the new Apple 5G iPhone will be delayed until 2021 – the project has been thrown into doubt because of a demand drop off and headaches with the supply chain in China.

The phenomenon of 5G cannot blossom until consumers can upgrade to 5G devices.

Concerning all the media print of China Inc. going back to work, don’t believe a word of it.

People of the Middle Kingdom are sitting at home just like you and me by navigating around top-down government edicts.

Instead of the perilous commute in a country of 1.4 billion people, Chinese workers are fabricating attendance figures per my sources.

Overall data is grim - global smartphone shipments dropped 38% year-over-year during February from 99.2 million devices to 61.8 million - the largest fall ever in the history of the smartphone market and that is just the tip of the iceberg.

The new data point underscores the magnitude of how the coronavirus is sucking the vitality out of the tech ecosystem in China and thus the end market for global consumer electronics.

The statistic also foreshadows imminent trouble in the smartphone market as other regions have now shut down not only in China but the manufacturing hubs of South East Asia.

The outbreak squeezes both supply and demand.

Factories in Asia are unable to manufacture phones as usual because of obligatory government shutdowns and complexities securing critical components from the supply chain.

5G has been hyped up as the great leap forward for wireless technology that will usher in unprecedented new use cases supercharging global GDP — from driverless transport to robotic automation to smart football stadiums.

And coronavirus is just that Godzilla destroying 5G momentum down.

Mass quarantines, social distancing, remote work, and schooling have been instituted in American cities, meaning that the current network carriers are swamped and overloaded with a surge in data usage.

The Verizon’s (VZ) and the AT&T (T) Broadbands of America are currently focused on maintaining their current core customers, adding extra broadband to handle the increased load, and making sure the health of the network stays intact.

This is a poor climate to upsell products to beleaguered Americans who have just lost income and possibly their house because they cannot pay mortgages.

Services such as YouTube and Netflix (NFLX) have even decreased the quality of streaming on their platforms to handle the dramatic spike in extra usage in Europe with the whole continent locked down.

The Chinese consumer was the Darkhorse catalyst to ramp up the global economic expansion during the last economic crisis, picking up world spending in 2009.

On the contrary, this group of super spenders is less inclined to save the global economy this time around because they are saddled with domestic debt.

Just as unhelpful to Silicon Valley revenues, the technology relationship at the top of the governments are poised to worsen because of the health scare.

The U.S. administration has already banned the use of Chinese components in the U.S. 5G network amid suspicions the devices would be used for espionage.

Back stateside, I believe the U.S. telecoms will explicitly detail a sudden slowdown in the 5G network rollout during their next earnings report.

The telecom companies have been able to successfully handle the extra incremental load, but it has had to allocate resources to service the extra volume.

In the meantime, companies will shift to doing infrastructure and site preparation in anticipation of the re-build up to 5G, but that could be next to be put on ice if crisis management moves to the forefront.

Considering every 5G base station is being manufactured in Asia, one must be naïve in believing all is well and they will probably need to do what the 2020 Tokyo Olympics will shortly do – postpone it.

It’s not business as usual anymore.

This time it’s different.

The world just isn’t ready to digest such a shift in global business as 5G until the fallout of the coronavirus is in the rear-view mirror.

The 5G phenomenon underlying effect is to supercharge globalization into smaller networks of interconnectivity and that is not possible during a black swan event like the coronavirus which is the antithesis of globalization and interconnected business.

Just take the situation across the Atlantic Ocean in Europe, UBS Group AG, and Credit Suisse Group AG required clients to post additional collateral, and money managers in New York are preparing term sheets for ultra-rich Americans to urgently meet margin calls.

Many people are scurrying back to their doomsday’s shelter and that does not scream global business.

If you thought gold was the safe haven – wrong again – it experienced back-to-back weekly losses as margin pressures force fire sales of gold to raise cash.

Another glaring example are the assets of Eldorado Resorts Inc., controlled by the founding Carano family, which burned $28.7 million of stock in the casino entity to meet a margin call to satisfy a bank loan.

Things are that bad now!

Sure, telecom players might argue that a sudden influx of workers from home necessitates more investment in 5G, but if they have no income, all bets are off.

The capacity of 4G home broadband has proved it is good enough for today’s demands and it means the last stage of 4G will be a high data consumption longer phase before business lethargically pivots to 5G in 2021.

Verizon’s CEO Hans Vestberg said last year that half the U.S. will have access to 5G by the end of 2020, and I will say that is now impossible.

This sets up a generational buy in the Silicon Valley chip names involved in 5G after coronavirus troubles peak such as Nvdia (NVDA), Xilinx (XLNX), Qorvo (QRVO), and QUALCOMM Incorporated (QCOM).

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-03-23 15:02:082020-05-11 13:21:14The Corona Drag on 5G

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.