Global Market Comments

October 17, 2018

Fiat Lux

Featured Trade:

(WHO WAS THE GREATEST WEALTH CREATOR IN HISTORY?)

(FB), (AAPL), (GOOG), (AMZN),

(XOM), (BRKY), (T), (GM), (VZ), (CCA),

(WHY DOCTORS MAKE TERRIBLE TRADERS?)

Global Market Comments

October 17, 2018

Fiat Lux

Featured Trade:

(WHO WAS THE GREATEST WEALTH CREATOR IN HISTORY?)

(FB), (AAPL), (GOOG), (AMZN),

(XOM), (BRKY), (T), (GM), (VZ), (CCA),

(WHY DOCTORS MAKE TERRIBLE TRADERS?)

Mad Hedge Technology Letter

June 13, 2018

Fiat Lux

SPECIAL ACRONYM ISSUE

Featured Trade:

(FB), (AMZN), (GOOGL), (NFLX), (BABA), (BIDU), (TWTR), (SNAP), (INTC), (QCOM), (VZ), (T), (S)

The tech industry is infatuated with acronyms.

The two-, three- and four-letter acronyms of yore have been spruced up by a new wave of contemporary terms.

There are a lot more of them now and readers will need to absorb the meaning of each term to avoid our content seeming like a Grecian dialect.

The Mad Hedge Technology Letter will break down the relevant terminology that applies to the current tech sector.

This will aid readers in their pursuit of financial satisfaction.

FANG: Facebook (FB), Amazon (AMZN), Netflix (NFLX), and Google (now Alphabet) (GOOGL)

Jim Cramer, the host of CNBC's Mad Money, coined this term as this quartet became such a force to reckon with, that they deserved their own grouping. Financial commentators and analysts often refer to the FANGs that ultimately represent the developments and destiny of large cap tech. Apple is sometimes grouped in this bundle with analysts adding a second A inside the acronym.

AWS - Amazon Web Services

The cloud arm of Amazon is its cash cow. Amazon invented this business out of thin air in 2006. It offers the ability for Amazon to operate its e-commerce division close to cost by plowing profits from its thriving cloud arm. AWS is the backbone to the whole Amazon operation. Without it, Jeff Bezos would need to rethink another genius business model because current and future success hinges on this one subsidiary. AWS is the market leader in the cloud industry, carving out 33% of the total market. Microsoft is the runner-up and saw its market share surge from 10% to 13% in the latest quarter.

GDPR - General Data Protection Regulation

Europe has been a stickler concerning individual data protection, and the American companies running riot with Europeans personal data has reached its climax. On May 25, 2018, new European regulations were implemented to give the user more control of handing out their personal data. Penalties for non-compliance are steep. Companies risk being fined up to 20 million Euros or 4% of annual worldwide turnover, whichever is larger. Facebook's Mark Zuckerberg now has a reason to behave like an angel. The least regulated industry in the world is finally experiencing the bitter regulation pill most industries have felt for centuries.

SaaS - Software as a Service

A software distribution model licensing software on a subscription basis. Instead of installing many of these software programs, many of them are available through the Internet on the cloud. Most subscriptions work on an annual basis, and this recurring revenue model has carved out additional income from companies that were used to paying a one-off fee for software. This model has been highly successful. Even former legacy companies have deployed this business model to critical acclaim.

AI - Artificial Intelligence

An area of computer science that strives to deploy human intelligence into machine simulation. The four main tasks it carries out are speech recognition, learning, planning, and problem solving. A.I. has been identified as a cutting-edge tool to fuse with technology products boosting the underlying performance creating massive profits for the participants. This phenomenon is controversial with the prophecy that robots might advance rapidly and turn on their inventors. As each day passes, A.I. is starting to infiltrate deeper into our daily lives, and humans are becoming entirely reliant on their positive functions to carry out daily tasks.

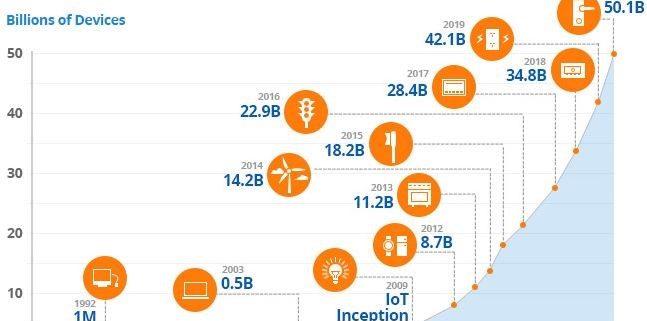

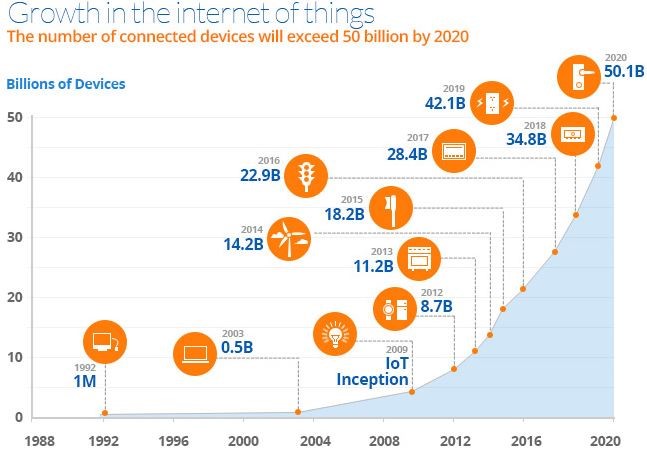

IoT - Internet of Things

Internet connectivity with things. This network will connect billions and billions of devices together. Your bathtub, thermostat, and razor will be armed with sensors and processors that reroute the performance data back to the manufacturer. Deploying the data, engineers will be able to enhance products with even more precision and high quality serving the end customer needs. 5G testing is ongoing in select American cities and new hyper-fast Internet speeds will make mass adoption of IoT products a reality.

5G - 5th generation wireless system

This is the successor to 4G and is poised to increase wireless Internet speeds up to 20 gigabits per second. Some of the traits will be low latency, high mobility, and will be able to accommodate high connection density. This technology is crucial to the development of the next generation of groundbreaking technology such as autonomous cars that need a faster Internet speed to run elaborate software. The war to develop this technology with the Chinese has turned into a heated standoff. China is stubbornly bent on becoming the global leader of technology in the future, and the communist government views 5G as the keys to the Ferrari. U.S. companies Verizon (VZ), AT&T (T) and Sprint (S) plan to roll out 5G in 2019. Other key companies are Huawei, Intel (INTC), Samsung, Nokia, Ericsson and Qualcomm (QCOM).

BAT - Baidu, Alibaba, and Tencent

This trio is the Middle Kingdom's answer to America's FANG. The nine-year domestic bull market has been led by large-cap tech, at the same time China's economy has been fueled by Baidu, Alibaba, and Tencent. Baidu and Alibaba are tradable through American depositary receipts (ADR). Tencent is public on Hong Kong's Hang Seng stock exchange, the third largest stock market in Asia. These companies are all a mix and mash of functionality that covers the same broad spectrum of the FANGs. They are the best companies in China and are on the cusp of every single cutting-edge technology from A.I. to autonomous vehicles. The Mad Hedge Technology Letter does not recommend these stocks to our subscribers because the Chinese government is on a nationalistic mission to delist Alibaba and Baidu from America and bring them back home. Initially, Alibaba wanted to list on the Hang Seng Hong Kong stock exchange, but draconian rules applied to dual-listing made the company flee to America.

NIMBY - Not In My Back Yard

Local opposition to proposed development in local areas. Although not a pure tech term, the epicenter of the NIMBY movement is smack dab in the middle of the San Francisco Bay Area where all the premium tech jobs are located. Local opposition has made it grueling for any developers to build.

What's more, the expensive cost of land has made any new building a tough proposition. This explains the 10-year drought where San Francisco experienced not a single new hotel built. The dearth of housing has caused San Francisco housing prices to skyrocket to a medium price of $1.61 million as of March 2018. Exorbitant housing prices have triggered a mass migration of Californians fleeing the Bay Area in droves. The shocking aftereffects have put highly paid Millennial tech workers spending the bulk of their salary on housing or living in dilapidated shacks. The extreme conditions we are now seeing are forcing schools around the Bay Area to close in unison as young families cannot afford to stay. Tech companies have become public enemy No. 1 in the Bay Area as locals are desperate to maintain their current lifestyle but are finding it more difficult by the day.

MAU - Monthly Active Users

Favored by social media companies to measure growth trajectories. This is how Twitter (TWTR) analyzes the health of its user numbers delivering a narrative to potential investors by hyping up user growth. If investors value this metric, this allows companies to focus on driving growth at the expense of burning cash. Thus, emerging social media companies such as Snapchat (SNAP) run huge loss-making operations for the promise of future profits after scaling.

ARPU - Average Revenue Per User

Favored by maturing social media companies, particularly Facebook, which has already grown global usership to 2.2 billion. Once the emerging hypergrowth phase comes to an end, social media companies focus on extracting more income per user through targeted ads. Facebook and Alphabet have the best ad tech divisions in all of Silicon Valley. The business model has made Facebook an inordinate amount of money as advertiser's flock to this de-facto marketplace paying more for effective ads whose price is set at an auction. It's a vicious cycle that attracts more traditional advertisers because it is the only method of selling to Millennials who are addicted to social media platforms. Cord-cutting is accelerating this trend forcing advertisers to co-exist with the Mark Zuckerberg model.

There are many more acronyms in the tech world that need explaining and that is exactly what I will do. The Mad Hedge Technology Letter will be back with another slew of technical terms to help subscribers understand the tech universe.

_________________________________________________________________________________________________

Quote of the Day

"You can worry about the competition... or you can focus on what's ahead of you and drive fast," said Square and Twitter CEO Jack Dorsey.

Mad Hedge Technology Letter

May 29, 2018

Fiat Lux

Featured Trade:

(HERE ARE SOME EARLY 5G WIRELESS PLAYS),

(T), (VZ), (INTC), (MSFT), (QCOM), (MU), (LRCX), (CVX), (AMD), (NVDA), (AMAT)

How would you like to be part of the biggest business development in the history of mankind?

This revolution will increase business functionality up to 10 times while flattening costs by up to 90%.

Still interested?

Enter the Internet of Things (IoT).

The Internet of Things (IoT) can be boiled down to Internet connectivity with things.

Your luxury juice maker, hair removal kit, and multi-colored Post-its will soon be online.

No, you won't be able to have Tinder chats with the new connectivity, but embedded sensors, tracking technology, and data mining software will aggregate a digital dossier on how products are performing.

The data will be fed back to the manufacturing company offering a comprehensive and accurate review without ever asking a human.

The magic glue making IoT ubiquitous and stickier than a hornet's nest is the emergence and application of 5G.

4G is simply not fast enough to facilitate the astronomical surge in data these devices must process.

5G is the lubricant that makes IoT products a reality.

Verizon Communications (VZ) and AT&T (T) have been assiduously rolling out tests to select American cities as they lay the groundwork for the 5G revolution.

The aim is for these companies to deliver customers a velocious 1 Gbps (gigabits per second) wireless connection speed.

Delivering more than 10 times the average speed today will be a game changer.

America isn't the only one with skin in the game and some would say we are not even leading the pack.

China Mobile (CHL) is carrying out a bigger test in select Chinese cities, and Chinese telecom company Huawei can lay claim to 10% of the 5G patents.

Americans should start to notice broad-based adoption of 5G networks around 2020.

Once widespread usage materializes, watch out!

It will go down in history books as a transformational headline.

The IoT revolution will follow right after.

Until the 5G rollout is done and dusted, tech companies are licking their chops and preparing for one of the biggest shifts in the tech ecosphere affecting every product, service, and industry.

The worldwide IoT market is poised to mushroom into a $934 billion market by 2025 on the back of cloud computing, big data, autonomous transport technology, and a host of other rapidly emerging technology.

The arrival of 5G will have an astronomical network effect. Companies will be able to enhance product specs faster than before because of the feedback of data accumulated by the tracking technology and sensors.

The appearance of this flashy new technology will spawn yet another immeasurable migration to technological devices by 2020.

In just two years, the world will play host to more than 50 billion connected devices all pumping out data as well as consuming data.

What a frightful thought!

IoT's synergies with new 5G technology will have an unassailable influence on the business environment.

For instance, industrial products in the form of robots and equipment will be a huge winner with 5G and IoT technology.

The industrial IoT market is expected to sprout to $233 billion by 2023.

Robots will pervade deeply into economic provenance acting as the mule for brute strength heavy labor plus more advanced tasks as they become more sophisticated.

Total global spending related to IoT products will surpass 1.4 trillion dollars by 2021, according to the International Data Corporation (IDC).

IoT growth will become most robust in the thriving Asian markets fueled by a bonus tailwind of the fastest growing region in the world.

The advanced automation abilities of Germany and the U.K. will also give them a seat at the table.

Micron CEO Sanjay Mehrotra gushed about the future at Micron's investor day celebrating IoT and data as the way forward. Mehrotra explained that the explosion of IoT products will create a new tidal wave of "growing demand for storage and memory."

Chips are a great investment to grab exposure to the 5G, IoT, and big data movement.

Up until today, the last generation of technological innovation brought consumers computers and smartphones.

That world has moved on.

Open up your eyes and you will notice that literally everything will become a "data center on wheels or on feet."

To arrive at this stage, products will need chips.

As many high-grade chips as they can find.

Data centers are one segment in dire need of chips. This market will more than double from $29 billion in 2017 to $62 billion in 2021.

The general-purpose chip market for servers is cornered by Intel.

Industry insiders estimate Intel's market share at 98% to 99% of data center chips. Clientele are heavy hitters such as Amazon Web Services, Google, and Microsoft Azure along with other industry peers.

The only other players with data server chips out there are Qualcomm (QCOM) and Advanced Micro Devices Inc. (AMD).

However, there have been whispers of Qualcomm shutting down the 48-core Centriq 2400 chip for data centers that was launched only last November after head of Qualcomm's data center division, Anand Chandrasekher, was demoted via reassignment.

AMD's new data center chip, Epyc, has already claimed a few scalps with Baidu (BIDU) and Microsoft Azure promising to deploy the new design.

IoT integration is the path the world will take to adopting full-scale digitization.

Microsoft just announced at its own Build 2018 conference its plans to invest $5 billion into IoT in the next four years.

The Redmond, Washington-based company noted operational savings and productivity gains as two positive momentum drivers that will benefit IoT production.

Consulting firm A.T. Kearny identified IoT as the catalyst fueling a $1.9 trillion in productivity increases while shaving $177 billion off of expenses by 2020.

These cloud platforms give tech companies the optimal stage to win over the hearts and dollars of non-tech and tech companies that want to digitize services.

Many of these companies will have IoT products percolating in their portfolio.

Examples are rampant.

Schneider Electric in collaboration with Microsoft's IoT Azure platform brought solar energy to Nigeria by the bucket full.

The company successfully installed solar panels harnessing its performance using IoT technology through the Microsoft cloud.

Kohler rolled out a new lineup of smart kitchen appliances and bathroom fixtures coined "Kohler Konnect" with the help of Microsoft's Azure IoT platform.

Consumers will be able to remotely fill up the bathtub to a personalized temperature.

Real-time data analytics will be available to the consumer by using the bathroom mirror as a visual interface with touch screen functionality giving users the option to adjust settings to optimal levels on the fly.

Kohler's tie-up with Microsoft IoT technology has proved fruitful with product development time slashed in half.

To watch a video of Kohler's new budding relationship with Microsoft's Azure IoT platform, please click here.

It is safe to say operations will cut out the wastefulness using these new tools.

Look no further than legacy American stocks such as oil and gas producer Chevron (CVX), which wants a piece of the IoT pie.

Chevron announced a lengthy seven-year partnership with Microsoft's Azure platform.

The fiber optic cables inside oil production facilities generate more than 1 terabyte of data per day.

In the Houston, Texas, offices, sensors installed six miles below the surface shoot back data to engineers who monitor human safety and system operations on four continents from the Lone Star State.

The newest facility in Kazakhstan, using state-of-the-art technology, will produce more data than all the refineries in North America combined.

Using the aid of artificial intelligence (A.I.), computers will analyze seismic surveys. This pre-emptive technology customizes solutions before problems can germinate.

The new smart-work environment will multiply worker productivity that has been at best stagnant for the past generation.

To get in on the IoT action, buy shares of companies with solid IoT cloud platforms such as Microsoft and Amazon.

Buy best-of-breed chip companies such as Nvidia (NVDA), Intel (INTC), Advanced Micro Devices (AMD) and Micron (MU).

And buy tech companies that produce wafer fab equipment such as Applied Materials (AMAT) and Lam Research (LRCX).

_________________________________________________________________________________________________

Quote of the Day

"Don't be afraid to change the model." - said cofounder and CEO of Netflix Reed Hastings.

Mad Hedge Technology Letter

May 25, 2018

Fiat Lux

Featured Trade:

(WHERE 5G CONNECTIVITY WILL TAKE US),

(T), (VZ), (INTC), (TSLA), (AAPL), (GOOGL)

AT&T (T), Verizon (VZ), and the other telecom heavies are in the process of investing $30 billion to make sure that fifth-generation wireless, or 5G, will roll out on time in 2020.

What 5G will do is improve the functionality of IoT (Internet of Things) by 10 times at one-tenth the cost, bringing a 100X increase of functionality over price.

The last time I saw a leap that great was when Intel (INTC) brought out its groundbreaking 8008 8-bit microprocessor chip in 1972. I remember it like it was yesterday.

The news that gravitational waves were discovered, as well as wrinkles in the space-time continuum, was big news in my family. 5G will be of that order.

Of course, we knew it was coming. It was just a matter of when.

I have 11- and 13-year-old girls (I can't help it if the plumbing still works!). Whenever we drive somewhere, we carry out what Einstein called "thought experiments."

They will come up with scientific questions, and I then direct them into finding their own answers through a series of prodding and hopeful questions.

It is much like how the children of royalty were tutored during the Middle Ages.

So they asked, "When will we get driverless cars?" which they had heard about on TV.

I answered in about two years, but that I had friends who run Tesla (TSLA) who already have them now.

And you know the interesting thing they discovered? After two years of beta testing, the cars are starting to develop their own personalities.

Each car has highly advanced learning software. When the mapping software requires one to take a difficult sharp left turn, the vehicle may miss it the first time.

It will then make the next legal U-turn, and then nail that turn every time in the future.

The cars are all programmed to drive like little old ladies. It will never speed, break the law, and always lets other cars cut in front. Over time, some are becoming cautious, while others are getting more aggressive depending on each individual's driving experience.

In other words, experience is turning them into "people."

I asked my daughters, "What would the world be like if everyone had driverless cars?" which will occur in about 30 years, or during their middle age.

They pondered for a moment. Then my older daughter shouted out, "There won't be car accidents anymore!" "Right!" I answered.

"But what will that mean?" I asked.

They puzzled over this.

A few seconds passed. Then it came. "The people who fix cars won't have anything to do!"

"You got it," I replied.

In fact, about 1 million people in the car repair industry will lose their jobs. A small group of vintage car fanatics will survive, much like horse and buggy hobbyists do today.

I pointed out that this is already happening because electric cars don't require any maintenance. You just rotate the tires every 6,000 miles (because electric batteries are so heavy).

I moved on. "Who else will lose their jobs when cars become self-driving?" They hit a brick wall. Then I asked "What else breaks when cars have accidents?"

A few seconds later it came. "People!"

"For sure," I shot back.

Actually, about 35,000 people die in car accidents every year in the United States, and another 500,000 are injured.

This means the demand for doctors, hospitals, and ambulances will go down. Say goodbye to another 1 million jobs.

"So, what else will self-driving cars do?" I was relentless.

My older girl was first: "If cars are driven by computers, it means they can drive closer together." I said, "That was true, but what was the consequence of that?"

The mountain scenery whizzed by. Then they got it.

"There won't be traffic jams anymore."

"Yes!" I blurted out. If a car can drive 70 miles per hour, but only needs to remain one car length behind the one in front of it, that effectively increases the capacity of freeways seven times.

We will never need to build another freeway again. Another 1 million jobs go down the drain.

"What else will self-driving cars do?" I carried on.

They hit a dead end. So, I gave a hint. "What do you see in cities?" After going through buildings, parks, roads, lots of cars, and bridges, I finally got the answer I wanted: "Parking lots."

I then posed the conundrum, "What's the connection between self-driving cars and parking lots?"

Now they were getting into the spirit of the thing. "They won't need them." I replied, "Absolutely."

Self-driving cars won't need to park. They'll just be able to drop you off and drive around the block until you are ready to go home.

This will be economical because after three decades of battery and solar improvements, energy will effectively be free, like air is today.

Oh, and at least 100,000 parking attendants might as well start joining the unemployment lines now.

It gets better.

Entrepreneurs now are developing apps for cars so they never need to park.

In an iteration of the sharing economy, and in a club or membership type format, your car will just drive person to person, selling rides, until you are ready to go home.

Think of it as Uber, without the drivers, that pays you.

Today, parking lots occupy about 15% of the land area of large cities. Self-driving cars will free up a lot of that space for other uses, such as housing and parks.

Then I asked the really big question. "What do all of these changes have in common?"

My 11-year-old picked up on this immediately. "A lot of people are going to lose their jobs!"

"For sure," I bubbled. Notice that every new technology improvement creates a lot of job losses. I went on.

"The trick for you girls is to always stay ahead of the technology curve so your job doesn't get lost, too." This is why I have been sending them to Java development school since they were 8 and 9.

They looked daunted.

And this is what 11- and 13-year-olds were able to figure out. Granted, they were MY kids.

Imagine what Google (GOOGL), Apple (AAPL), and Tesla are doing with this idea. It has become a hot bottom "next big thing." Silicon Valley is now rife with rumors of breakthrough developments and the poaching of staff.

The U.S. military and the Defense Advanced Research Projects Agency (DARPA) are involved in self-driving vehicles in a big way as well, holding regular contests with big prize money and the prospect of mammoth government contracts.

More and more generals and admirals are telling me that the wars of the future will be fought with software.

The bottom line is that things are happening much faster than we imagined possible only a few years ago.

Then my oldest daughter piped up.

"Dad, can I get my driver's license before all the cars are self-driving?" I said, "Sure. What kind of car do you want?"

"A red one."

My first car was a red 1957 Volkswagen Beetle.

On our next trip we will cover gravitational waves, Einstein's Theory of Relativity, and the significance of the clock tower in Bern, Switzerland.

By the way, these girls will be graduating from college in 2026 and 2027 and will be looking for jobs.

Just let me know. :-)

_________________________________________________________________________________________________

Quote of the Day

"Homo sapiens, the first truly free species, is about to decommission the natural selection, the force that made us," said E.O. Wilson, a Harvard University biology professor.

Mad Hedge Technology Letter

May 4, 2018

Fiat Lux

SPECIAL SPACE X ISSUE

Featured Trade:

(WILL SPACE X BE YOUR NEXT TEN-BAGGER?)

(EBAY), (TSLA), (SCTY), (BA), (LMT)

Mad Hedge Technology Letter

May 3, 2018

Fiat Lux

Featured Trade:

(THE INCREDIBLE SHRINKING TELEPHONE INDUSTRY)

(TMUS), (S), (NFLX), (T), (VZ), (CHTR), (CMCSA)

Talk is cheap.

Do not believe half-truths that go against economic convention.

This was the case when T-Mobile (TMUS) CEO John Legere and Sprint (S) CEO Marcelo Claure popped up on live TV promoting affordability, elevated competition, and massive 5G infrastructure investments if the two companies joined forces in a $26.5 billion deal.

This was a case of smoke and mirrors. The speculative claim of adding 3 million workers and investing $40 billion into 5G development is just a line pandering toward President Trump's nationalistic tendencies.

They want the deal to move forward any way possible.

Jack Ma, founder and executive chairman of Alibaba (BABA), met President Trump at Trump Towers before his term commenced and promised to add 1 million jobs in order to curry favor with the new order.

Where are those jobs?

If this merger came to fruition, market players would shrink from 4 to 3 - a newly reformulated T-Mobile plus Verizon (VZ) and AT&T (T).

Pure economics dictate that shrinking competition by 25% would create pricing leverage for the leftover trio.

Industry consolidation is usually met with accelerated profit drivers because companies can get away with reckless price increases without offering more goods and services.

Being at the vanguard of the 4G movement, America overwhelmingly benefited from lucid synergistic applications that fueled domestic job growth and economic gains.

Japanese and German players were hit hard from missing out in leading the new wave of wireless technology.

T-Mobile and Sprint wish to be insiders of this revolutionary technology and this is their way in.

In the past, T-Mobile jumped onto the scene with aggressively twisting its business model to fight tooth and nail with Verizon and AT&T.

It was moderately successful.

T-Mobile even offered affordable plans without contracts offering customers optionality and advantageous pricing.

It was able to take market share from Sprint, which is the monumental laggard in this group and the butt of jokes in this foursome.

The average cost of wireless has slid 19% in the past five years, and traditional wireless Internet companies are sweating bullets as the future is murky at best.

The bold strategy to merge these two wireless firms derives from an urgent need to combat harsh competition from the two titans Verizon and AT&T.

The merger is in serious threat of being shot down by the Department of Justice (DOJ) on antitrust grounds.

History is littered with companies that became complacent and toppled because of monopolistic positions.

Case in point, the predominant force in the American and global economy was the American automotive industry and Detroit in the 1950s.

Detroit had the highest income and highest rate of home ownership out of any major American city at that time.

Flint, Michigan, oozed prosperity, and the top three car manufacturers boasted magnanimous employee benefits and a tight knit union.

During this era of success, 50% of American cars were made by GM and 80% of cars were American made.

The car industry could do no wrong.

This would mark the peak of American automotive dominance, as local companies failed to innovate, preferring stop-gap measures such as installing add-ons such as power steering, sound systems, and air conditioning instead of properly developing the next generation of models.

American companies declined to revolutionize the expensive system put in place that could produce new models because of the absence of competition and were making too much money to justify alterations.

It's expensive to make cars but neglecting reinvestment yielded future mediocrity to the detriment of the whole city of Detroit.

The tech mentality is the polar opposite with most tech firms reinvesting the lion's share of operational profit, if any, back into product improvement.

Sprint got burned because it skimped on investment. It is in a difficult predicament dependent on T-Mobile to haul it out of a precarious position.

GM, Ford, and Chrysler met their match when Toyota imported a vastly more efficient way of production and the rest is history.

Detroit is a ghastly remnant of what it used to be with half the population escaping to greener pastures.

A carbon copy scenario is playing out in the mobile wireless space and allowing a merger would suppress any real competition.

To add confusion to the mix, fresh competition is growing on the fringes desiring to disrupt this industry sooner than later by cable providers such as Charter (CHTR) and Comcast (CMCSA) entering the fray offering mobile phone plans.

Google also offers a mobile phone plan through the Google Fi division.

The fusion of wireless, broadband, and video is attracting competition from other spheres of the business world.

The paranoia served in doses originates from the Netflix (NFLX) threat that vies for the same entertainment dollars and eyeballs.

Remember that AT&T is in the midst of merging with Time Warner Cable, which is the second largest cable company behind Comcast.

The top two in the bunch - AT&T and Verizon - are under attack from online streaming business models, and the Time Warner merger is a direct response to this threat.

There are a lot of moving parts to this situation.

AT&T hopes to leverage new video content to extract digital ad revenue capturing margin gains.

Legere and Claure put on their fearmongering hats as they argued that this deal has national security implications and losing out to Chinese innovation is not an option.

This argument is ironic considering T-Mobile is a German company and Sprint is owned by the Japanese.

Sprint have been burning cash for years and this move would ensure the businesses survives.

Sprint's crippling debt puts it in an unenviable position and this merger is an all or nothing gamble.

Sprint has not invested in its network and is miles behind the other three.

AT&T has outspent Sprint by more than $90 billion in the past 10 years.

This is the last chance saloon for Sprint whose stock price has halved in the past four years.

However, T-Mobile sits on its perch as a healthier rival that would do fine on a stand-alone basis.

Consolidation of this great magnitude never pans out for the consumer as users' interests get moved down the pecking order.

Wireless stocks were taken out and beaten behind the wood shed on the announcement of this news as the lack of clarity moving forward marked a perfect time to sell.

There will be many twists and turns in this saga and any capital put to use now will be dead money while this imbroglio works itself out.

If the deal doesn't die a slow death and finds a way through, the approval process will be drawn out and cumbersome.

The ambitious deadline of early 2019 seems highly unrealistic even with the most optimistic guesses.

The outsized winner from a deal would be AT&T, Verizon, and the newly formed T-Mobile and Sprint operation.

If this new wave of consolidation becomes reality, pricing pressure on the business model would ease for the remaining players, particularly allowing more breathing room for the leaders.

Stay away from this sector until the light can be seen at the end of the tunnel.

_________________________________________________________________________________________________

Quote of the Day

"Everything is designed. Few things are designed well." - said radio producer Brian Reed