Mad Hedge Bitcoin Letter

October 14, 2021

Fiat Lux

Featured Trade:

(WHAT’S NEW IN BIOTECH)

(CGTX), (BIIB), (LLY), (ABBV), (NVS), (TAK), (PYXS), (PFE),

(AZN), (GILD), (GSK), (IMGN), (ISO), (TMO), (BIO)

Mad Hedge Bitcoin Letter

October 14, 2021

Fiat Lux

Featured Trade:

(WHAT’S NEW IN BIOTECH)

(CGTX), (BIIB), (LLY), (ABBV), (NVS), (TAK), (PYXS), (PFE),

(AZN), (GILD), (GSK), (IMGN), (ISO), (TMO), (BIO)

As the biotechnology world is ever-evolving, with several companies going public every few months, let me share some of the most promising names that recently emerged.

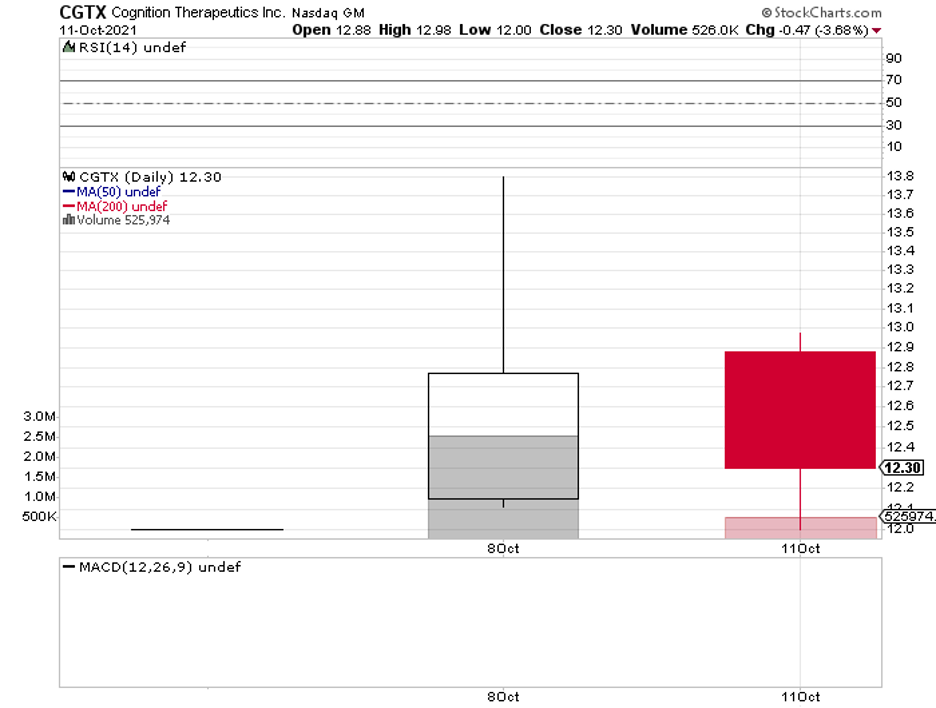

The first is Cognition Therapeutics (CGTX), a company working on treatments for Alzheimer’s disease and macular degeneration.

Its most promising candidate is an Alzheimer’s treatment called CT1812, which is currently under Phase 2 trials. Looking at the timeline, CGTX expects to release topline data by 2023.

With the expected growth of the aging population, focusing on treating various forms of Alzheimer’s is a promising direction for Cognition Therapeutics.

In fact, the global market for this neurodegenerative disease is projected to grow from $2.9 billion in 2018 to a whopping $10.5 billion by 2025.

So far, the major competitors of Cognition Therapeutics in this area include Biogen (BIIB), Eli Lilly (LLY), AbbVie (ABBV), Novartis (NVS), and Takeda (TAK).

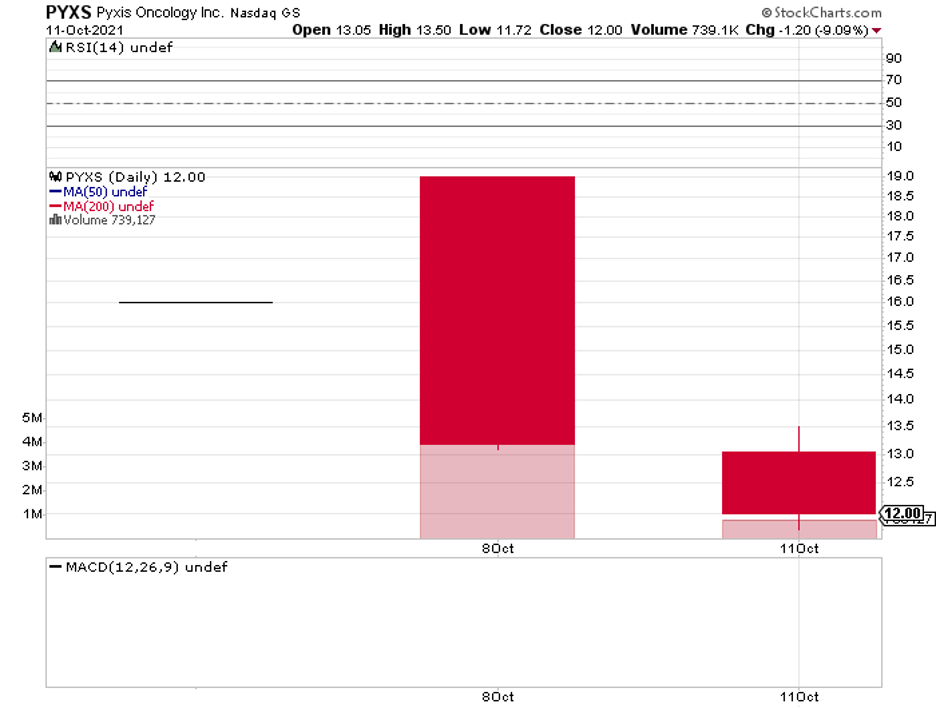

The second promising biotech company is Pyxis Oncology (PYXS), which is a spinoff from Pfizer (PFE).

Pyxis is focused on developing next-generation treatments targeting difficult-to-treat types of cancer.

Basically, the company’s goal is to create therapies that can directly kill tumor cells. It also wants to get rid of the underlying problems that lead to the uncontrollable spread of tumors and the weakening of the immune system.

To do this, Pyxis has come up with novel antibody drug conjugate (ACT) candidates and other monoclonal antibody (mAb) pipelines.

Its lead candidate is called ADC PYX-201, a potential treatment for non-small cell lung cancer and breast cancer.

The goal of ADC PYX-201 is to target actively multiplying tumors while boosting the immune response of the patient’s body. Pyxis plans to submit it as a non-small cell lung cancer treatment candidate by mid-2022.

If approved, then ADC PYX-201 will be under patent protection until 2037.

This holds great potential for Pyxis’ cashflow, as the market for non-small cell lung cancer worldwide is anticipated to rise from $6.2 billion in 2016 to over $12 billion by 2025.

With this potential of ADC treatments, Pyxis can expect competition from the likes of AstraZeneca (AZN), Gilead Sciences (GILD), GlaxoSmithKline (GSK), and ImmunoGen (IMGN).

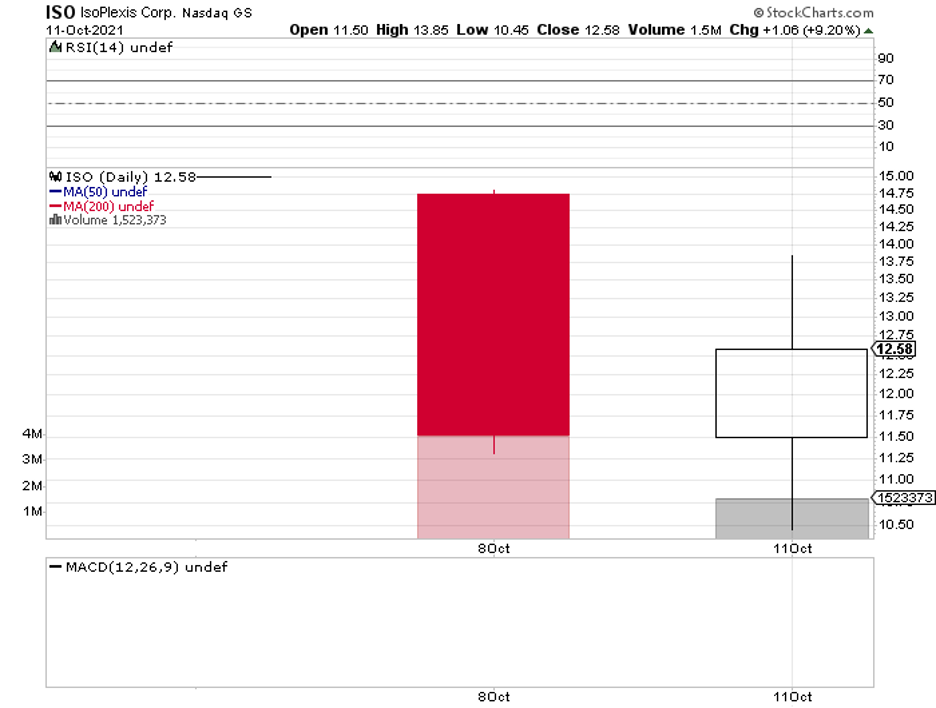

The last name on today’s list is IsoPlexis Corporation (ISO).

This company is the first to focus on dynamic proteomics and single-cell biology in an effort to develop “walk-away automation” products that aid in shortening the therapeutic development timelines by acquiring “multiplexed proteomics with very low sample volumes that reflect in vivo biology to clarify lead candidates.”

In layman’s terms, IsoPlexis is working on a technology that aims to identify every protein in the body to speed up the development of new therapies for rare diseases.

This is a lucrative business, with IsoPlexis targeting at least $34 billion in the total addressable market.

Considering that IsoPlexis is a pioneer in this field, it is possible for it to gain the lion’s share of the segment and position itself as an undisputed leader for years.

More importantly, IsoPlexis can use its patented technology, “Proteomic Barcoded,” to expand the use cases to cover other lucrative markets.

For example, IsoPlexis can apply its technology to cancer immunology and targeted oncology by predicting the progression of cancer cells in the body.

Adding cell therapies to the company’s pipeline is also a very realistic possibility since its technology can be utilized to create CAR-T cell therapies as well.

In fact, IsoPlexis’ approach is already being used in developing treatments for leukemia and melanoma.

Another profitable avenue for IsoPlexis’ technology is the vaccines sector.

Since the development of vaccines requires profiling the responses of the respiratory and immune systems, the company’s data would accelerate the entire process.

So far, the major rivals of IsoPlexis in this space include Thermo Fisher Scientific (TMO) and Bio Rad Laboratories (BIO).

While all these biotech companies offer promising products and technologies, they’re all still in the early stages of development.

This makes them high-risk investments and are likely suitable for those who are willing to invest in the long term.

For those who want to see movement faster and sooner, it might be best to watch these stocks from the sidelines.

Mad Hedge Biotech & Healthcare Letter

August 31, 2021

Fiat Lux

FEATURED TRADE:

(A CANCER PIONEER FOR THE BOOKS)

(SEGN), (MRK), (BMY), (PFE), (GILD), (RHHBY), (TAK), (GMAB)

When choosing a biotechnology company to invest in, a good sign to look out for is when management continuously looks for ways to expand its technology.

This means you’re looking at a stock that’s likely to appreciate multiple folds.

Seagen (SEGN) does this in spades.

Since it was founded in 1997, Seagen (SEGN) has reached almost $30.67 billion in market capitalization.

Reviewing its growth story, I think its powerful growth strategy is one of the key elements that help the company with its advancements.

That is, Seagen is aggressively developing and expanding its different labels for the approved drugs in its portfolio while also actively discovering innovative and new treatments and molecules.

Simply put, Seagen’s growth and expansion can be likened to a tree that keeps forming new additional branches.

Over the years, the company has experienced a remarkable transformation from a single-product firm to a diversified and ever-expanding player, particularly in the oncology medication market—a strategy that paid off.

After all, the market for cancer drugs isn’t the type to stand still.

This sector is renowned for its fast-paced demands and rapid growth. If you look at how much has been done, remember that several types of cancer that seemed incurable a mere 10 years ago are now no longer considered death sentences thanks to the innovative therapies discovered.

If roughly 15 years ago, the standard cancer treatment only involved chemotherapy and surgery, the recent years have granted us access to newer technologies like targeted therapy and immunotherapy.

Lately, CAR-T therapy has been hailed as the most effective means of treating blood cancer. Meanwhile, the likes of Merck’s (MRK) Keytruda and Bristol-Myers Squibb (BMY) Opdivo have made chemotherapy and surgery more effective as well.

So, it wouldn’t be a surprise anymore if the technology in the oncology sector advances further in the years to come.

Another relatively fresh innovation is the antibody-drug conjugate (ADC) technology.

This takes and combines all the positive effects of chemotherapy and targeted therapy while simultaneously eliminating the adverse effects of chemotherapy on the patient’s body.

Unlike chemotherapy, ADCs specifically target and eliminate tumor cells and works to spare the healthy ones. Once the tumor cells are detected, a toxic drug is released to kill them.

Basically, it works like a “smart bomb” in that it annihilates only the enemies and protects the allies.

The first drug to be approved based on ADCs is Mylotarg from Pfizer (PFE), which was 20 years ago.

However, it was only in recent years that this technology finally gained traction and attracted commercial success.

So far, roughly 56 pharmaceutical companies are working on developing ADCs.

Aside from Pfizer, another pioneer in ADCs is Seagen. Unlike Pfizer, this company has chosen to continue focusing on the development of the treatment.

Other companies working on ADC technology include Immunomedics, which Gilead Sciences (GILD) acquired, and Roche (RHHBY).

However, Seagen’s work looks to be the most promising in this segment.

Its first ADC drug is Adcetris, which was approved in 2011 for Hodgkin’s lymphoma and made in cooperation with Takeda Pharmaceutical (TAK).

Its indication was later expanded to cover another white blood cell disease, Peripheral T-cell lymphoma (PTCL).

Seagen already holds roughly 45% of the market share in the Hodgkin’s lymphoma segment alone, and this is expected to rise to 50% by 2026.

In terms of projected sales in the US, Adceris is estimated to generate about $1.7 billion by 2026.

On top of that, Seagen also rakes in royalties from Adceris sales outside the US thanks to its Takeda partnership.

Riding the momentum of Adceris, Seagen expanded its ADC pipeline and later gained approval for Padcev in 2019.

This drug received the go signal to treat a fairly common disease in the oncology space: metastatic bladder cancer.

In the US, the average number of new cases of metastatic bladder cancer is 83,000. Given its market size and potential to become part of a combination therapy with the ever-popular Keytruda, Padcev is expected to generate at least $2.6 billion in sales by 2026.

Gaining more confidence in its expertise in the oncology sector, Seagen continued its expansion and gained regulatory approval for breast cancer treatment Tukysa.

Tukysa is expected to bring roughly $1 billion in annual sales in the US and European markets. This figure is projected to rise when it eventually also gains approval for colorectal cancer.

Another notable drug in Seagen’s pipeline is Tisotumab Vedotin (TV), which is a collaboration with Genmab (GMAB). TV is a cervical cancer treatment and is expected to gain approval by the end of 2021.

Shifting gears, let’s take a look at the upcoming growth of Seagen. Initially, its 2021 guidance put its annual sales at $1.28 billion for all the products.

However, Seagen has already exceeded expectations, with Adceris reporting $700 million in sales for a single quarter this year. Actually, both Adceris and Padcev are well on their way into becoming blockbusters in a year or two, thanks to their continuously expanding applications.

Overall, Seagen is an excellent long-term investment.

Aside from its work with giant biopharmaceutical companies like Merck and BMY, its current portfolio of treatments and pipeline programs present a myriad of opportunities for Seagen.

Moreover, its ability to develop powerful treatments and leverage the science of ADCs make Seagen one of the most promising oncology stocks in the market today.

Mad Hedge Biotech & Healthcare Letter

August 12, 2021

Fiat Lux

FEATURED TRADE:

(THE FUTURE OF REGENERATIVE MEDICINE)

(CRSP), (EDIT), (BLUE), (PFE), (AZN), (GSK), (TAK), (REGN)

As our bodies begin to show signs of aging and fatigue, exploring ways to regenerate our organs has become crucial in ensuring a hale and hearty lifespan.

This demand has given rise to a branch of biotechnology and healthcare, which could very well be on the brink of becoming the next big thing in the mainstream biopharmaceutical industry: regenerative medicine.

For example, experts at Gladstone Institutes is applying gene therapy to repair heart damage. Basically, their goal is to reprogram scar tissue and transform it into a new heart cell.

What they do is inject the genes into the damaged heart caused by a heart attack. Then, these “new” genes alter the scar cells, converting them into beating hearts.

This approach no longer demands any cloning to obtain an extra set of organs. The Gladstone Institutes’ use of gene therapy allows us to regrow our own set of organs right inside our bodies.

And in case you’re wondering whether this type of work actually has a future or just another trend that would quietly disappear in the future, I’m telling you that this industry has incredibly potential.

Just look at the $12 billion valuation of a biotechnology unicorn called Samumed in San Diego.

Founded in 2008, this company has spent most of its lifetime operating under the radar. It impressively came out of the shadows last 2016 and was quickly dubbed as an “anti-aging” company.

To them, though, they’re a “de-aging” company. That is, they believe that people should be brought back to their peak health conditions before they can even begin to restore youth.

This ideology is exhibited by the company’s lead program: a knee osteoarthritis cure called Lorecivivint.

As we know, osteoarthritis has no known treatment that works to reverse the damage to the joint.

That’s why the doctors focus on handling or managing the symptoms. They tell their patients to exercise and lose weight to boost muscle strength and decrease the burden on their joints.

They also prescribe various drugs like painkillers, some anti-inflammatory pills, and even cortisone shots. Other patients would eventually need to go through replacement surgery.

This is where Samumed comes in.

The company created Lorecivivint to repair the joint damage. That way, patients will no longer need to go through all the burden of managing the symptoms of knee osteoarthritis.

In their proof-of-concept report, Samumed shared that one year after getting injected with Lorecivivint, the X-rays of the knees of the patients showed that there was an increase in “medial compartment joint space width.”

In simpler terms, the knees grew cartilage after a single shot of Lorecivivint.

Other than working on a cure for knee osteoarthritis, Samumed is also looking into treating male pattern baldness.

Another impressive biotechnology company focused on regenerative medicine is Humacyte, which recently shifted from being a clinical-stage firm to a commercial one.

Humacyte’s core work is on Human Acellular Vessels (HAVs) or “implantable regenerative human tissue.”

A use case for this is when a patient has damaged blood vessels. Typically, there are three options to treat this: take a vessel from another part of the body, try to implant a donated vessel, or utilize a plastic tube.

The first one requires at least two surgeries and, of course, losing a vessel in another part of your body.

Meanwhile, the second and third options expose the patient to the possibility of an infection or the body rejecting the vessel or plastic tube.

Humacyte’s HAVs offer a fourth option.

Since the HAVs carry similar properties as the native tissues of the patient’s body, they significantly lower the risk of rejection.

Basically, they’re “growing” HAVs that won’t be rejected by the body.

More importantly, the company is creating engineered off-the-shelf replacement tissue that can be implanted to anyone without using immunosuppressive drugs.

This is impressive because immunosuppressants are staples in ensuring that the body does not reject the organs. However, the use of this can be dangerous because it increases the risk of infections.

So far, Humacyte has been working on coming up with safer and more effective treatments for hemodialysis patients since the current methods tend to expose them to higher risks of infections.

If everything goes according to plan, then the company will be able to file for FDA approval by 2022.

While the technologies offered in the regenerative medicine space have been discussed and even praised for years, it’s only recently that these became commercially viable.

For all the noise and hype surrounding these breakthrough and next-generation treatments, only a handful of patients have actually benefited from them.

However, 2021 might just mark the year that all these will change.

Other than the private firms and smaller biotechnology companies like CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), and bluebird Bio (BLUE), bigger names in the biopharmaceutical space, including Pfizer (PFE), AstraZeneca (AZN), GlaxoSmithKline (GSK), Takeda Pharmaceuticals (TAK), and Regeneron (REGN), are also starting to invest more aggressively into it.

Mad Hedge Biotech & Healthcare Letter

October 22, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS COVID-19 VACCINE OUTLIER ON THE FAST LANE?)

(NVAX), (PFE), (AZN), (JNJ), (SNY), (MRNA), (TAK)

It is not at all surprising that the biggest names in the healthcare industry are dominating the COVID-19 vaccine race.

After all, Big Pharmas such as Pfizer (PFE), AstraZeneca (AZN), Johnson & Johnson (JNJ), and Sanofi (SNY) are backed with vast resources that even media favorites like Moderna (MRNA) find challenging to compete against.

For months now though, going head to head with these big-name frontrunners is a clear outlier: Novavax (NVAX).

So far, there are only 10 COVID-19 vaccine candidates that have reached late-stage testing and Novavax’s NVX-CoV2373 has been performing at par (if not better) than its rivals—and the market has definitely noticed.

When 2020 started, Novavax’s market capitalization was less than $130 million and traded at roughly $4 per share.

Ten months into the pandemic, this small biotechnology company’s market cap grew to over $6.5 billion and has been trading at $110 per share—and that is already after a price decrease in the past weeks.

Given the disparity in its size and resources compared to its competitors, it’s safe to say that Novavax has been punching way above its weight class particularly in terms of landing supply agreements for its COVID-19 program.

Novavax first received a CEPI grant in March worth $4 million, which was immediately dwarfed by the $384 million the biotech company got in May.

In a matter of months, Novavax joined the major league players and secured a $1.6 billion funding courtesy of the US government’s Operation Warp Speed program.

In exchange, the biotech company will supply 100 million doses of NVX-CoV2373 to the US upon approval.

Novavax also inked an agreement with the UK for 60 million doses and another with Canada for 76 million doses.

Novavax has also landed deals with Japan through Takeda Pharmaceutical (TAK) and India via the Serum Institute of India.

As expected, the grants and supply agreements were perceived as votes of confidence on Novavax’s work and the company reaped the rewards.

In March, the prices started moving from less than $10 per share to almost $50.

By May, the price moved up to roughly $80 per share.

After its Operation Warp Speed contract in July, Novavax’s price per share soared all the way to $189 before eventually falling to $110 this October.

Novavax has only conducted late-stage testing in the UK. But, Phase 3 is expected to begin in the US soon as well.

Admittedly, a lot is riding on NVX-CoV2373.

However, the company has actually offloaded the majority—if not all—of its financial risks linked to the program.

Riding the momentum of its COVID-19 vaccine candidate, Novavax has been working on a related influenza vaccine called Nanoflu.

Given the market size for this, Nanoflu is estimated to rake in an annual revenue somewhere between $550 million and $1.7 billion.

Another potential blockbuster is respiratory syncytial virus (RSV) vaccine ResVax, which is projected to reach peak sales of $2 billion.

Novavax is also working on a vaccine candidate for the Ebola virus, the Middle East Respiratory Syndrome (MERS-CoV), and Severe Acute Respiratory Syndrome (SARS).

While NVX-CoV2373 is anticipated as Novavax’s moneymaker in the coming years, the biotech company can only realistically expect massive sales from this until 2023.

Looking at the company’s manufacturing partnerships and the aggressive timeline it has taken, Novavax is expected to produce 2 billion doses of its COVID-19 vaccine by mid-2021.

This is great news for its investors because of Novavax’s smaller market capitalization compared to its competitors.

Since the biotech company is projected as one of the first companies—if not the first—to offer a vaccine, then it can cover a substantial market share before its bigger rivals take over the market.

Even if Novavax prices its COVID-19 vaccine cheaply, say, $10 per dose, it can still generate $20 billion in annual sales.

Moreover, the late-stage success of NVX-CoV2373 will definitely cause Novavax’s stock price to skyrocket.

Despite this potential though, it’s important to keep in mind that this biotech company still has a way lower market cap than its rivals.

That means its share price will move a lot higher compared to the stocks of the other vaccine leaders.

Therefore, Novavax’s small size is not a negative for its investors—it is actually an advantage.

So for biotech investors who are searching for a promising COVID-19 vaccine stock, there’s nothing cheaper and more promising than Novavax.

Mad Hedge Biotech & Healthcare Letter

June 23, 2020

Fiat Lux

Featured Trade:

(WHY SEATTLE GENETICS IS ON FIRE)

(SEGN), (MRK), (TAK), (GSK), (BGNE), (RHHBY), (NVS), (PFE), (IMG)

It’s not all about the Coronavirus

Though the COVID-19 pandemic has claimed the lives of over 120,000 people and is causing the suffering of almost 1.3 million patients in the United States alone, cancer and heart disease remain the leading causes of death in the country.

The American Cancer Society journal estimates that there will be around 1.8 million cancer cases this year, with 606,520 of those resulting in deaths.

Needless to say, the continuously increasing incidence of this deadly disease has prompted a number of companies in the biotechnology and healthcare sectors to invest substantially in creating and developing drugs for cancer treatment.

Buoyed by this demand, biotechnology company Seattle Genetics (SEGN) has gained 40.1% in 2020 so far primarily thanks to its cancer drugs.

In fact, Seattle Genetics welcomed 2020 with a newly approved drug called Padcev, which the company developed alongside Tokyo-based Astellas Pharma to treat the most common type of bladder cancer.

Despite the pandemic, Padcev sales have been exceeding expectations and analysts are jacking up the sales estimates for this potent bladder cancer product.

Initially pegged to rake in roughly $10 million in quarterly sales, Padcev managed to beat the estimates by four- to fivefold with $34.5 million in the first quarter of 2020.

Since then, peak sales prediction for this drug has been increased to a whopping $2 billion, with its 2020 sales target to be around $221 million.

Approximately 80,000 new bladder cancer cases are diagnosed every year in the United States. Among these patients, 90% suffer from the urothelial type -- the kind that Padcev is formulated to address.

Adding to that, Padcev’s success can also be attributed to the fact that it’s the only FDA-approved product for this particular patient set.

Riding on the momentum of Padcev’s unchallenged success in the bladder cancer field, Seattle Genetics and Astellas are now looking to expand the drug’s indication to cover an even larger patient set.

If this works out, then Padcev opens a whole new slew of possibilities to the tune of an additional $5.8 billion to its revenue.

At the moment, Padcev is also not prescribed to patients in the earlier stages of the disease - a demand that Seattle Genetics aims to address with its collaboration with Merck (MRK) via the immuno-oncology’s powerhouse drug Keytruda.

Aside from its bladder cancer drug, Seattle Genetics is also actively making a name for itself in another field.

In April 2020, Seattle Genetics received another positive news from the FDA.

The company’s breast cancer drug Tukysa, which was expected to gain approval by August this year, received the green light four months earlier instead.

Tukysa is another potential blockbuster drug for Seattle Genetics, with the product’s peak sales estimated to reach $1.2 billion by 2030.

All these are actually pretty impressive considering that Seattle Genetics was a one-product biotechnology company just a year ago.

Its single product, Hodgkin lymphoma drug Adcetris, had a specially impressive 2019 because of label expansions.

The drug posted a 32% jump in net sales to reach $627.7 million in the US and Canada. For 2020, Adcetris’ sales is expected to grow somewhere between 8% and 12%.

Apart from expanding the use of both Adcetris and Padciv, Seattle Genetics is also looking into developing new antibody treatments specifically for patients with solid tumors and lymphomas.

It currently has several candidates undergoing clinical trials, with some of these potential treatments expected to go head-to-head against active competitors in the space, including Roche (RHHBY), Novartis (NVS), Takeda Pharmaceutical (TAK), Pfizer (PFE), and Immunogen (IMG).

Prior to the approval of Padcev and Tukysa, the major growth driver that augmented Adcetris’ earnings was the company’s royalty revenue.

In the fourth quarter of 2019, the biotechnology company raked in $72.3 million in royalty revenue. This is actually triple the amount it earned in the same period in 2018.

The main source of its royalty revenue at the time is the $40 million in milestone payment it received from Takeda.

The payment was triggered by the annual net sales of Adcetris that went beyond $400 million in Takeda’s territory.

The total royalty revenue was also supplemented by a milestone payment from GlaxoSmithKline (GSK) and an upfront payment from Seattle Genetics’ work with Beijing-based company BeiGene (BGNE).

In the first quarter of 2020, royalty revenues jumped to $20 million compared to the $16 million the company earned during the same period in 2019.

Once again, this growth was attributed to Adcetris’ sales and boosted by royalties from the company’s collaboration with Roche (RHHBY) on the latter’s lymphoma drug Polivy.

Seattle Genetics has consistently grown its revenue since 2011 when its first-ever drug Adcetris received approval. With the recent additions of potential blockbusters Padcev and Tukysa, the company’s financial picture looks brighter than ever.

One of the key factors in its success is that the company addresses significant patient sets, providing its investors with the confidence that it can attract physicians and patients on board.

The Hodgkin lymphoma drug market, which Adcetris has covered, is anticipated to grow by roughly $1.24 billion from 2019 through 2023.

The urothelial cancer drug market, where Padciv is currently king, is estimated to hit $3.6 billion by 2023, with a 23% compound annual growth rate.

Tukysa addresses another patient set with high demand as well, with reports showing that the spending on HER2-positive cancer is anticipated to jump by 54% to hit $9.89 billion by 2025.