Mad Hedge Biotech & Healthcare Letter

August 5, 2021

Fiat Lux

FEATURED TRADE:

(LET THE BIOTECH BUYOUTS BEGIN)

(TBIO), (SNY), (MRNA), (PFE), (BNTX), (ARCT), (GSK), (JNJ), (MRK), (BLUE), (CVAC)

Mad Hedge Biotech & Healthcare Letter

August 5, 2021

Fiat Lux

FEATURED TRADE:

(LET THE BIOTECH BUYOUTS BEGIN)

(TBIO), (SNY), (MRNA), (PFE), (BNTX), (ARCT), (GSK), (JNJ), (MRK), (BLUE), (CVAC)

One of my predictions for this year just came true: the biotechnology buyouts have begun.

In my letter last January, I forecasted that the growing popularity of the mRNA technology courtesy of the COVID-19 vaccines from Moderna (MRNA) and Pfizer (PFE / BioNTech (BNTX) would trigger acquisitions of smaller biotechnology companies this year.

I predicted that bigger players in the healthcare industry would scoop up smaller players to stake a claim in this quickly growing space.

Topping our list of buyout candidates is Translate Bio (TBIO)—the very same company hogging headlines in the past days following its $3.2 billion acquisition by Sanofi (SNY).

The all-cash deal values each TBIO share at $38, representing a premium of over 30% above the stock’s price. If all goes well, the deal should be completed by the third quarter of 2021.

This is one of the first major moves by Sanofi following the healthcare giant’s recent pivot into vaccines.

However, this isn’t the first time Sanofi and TBIO worked together.

The two companies have actually started collaborating back in 2018, working on a potential mRNA-based flu vaccine—a project that has Sanofi and TBIO ahead of the pack, with BioNTech and Arcturus Therapeutics Inc. (ARCT) trailing behind.

Sanofi and TBIO’s mRNA seasonal flu vaccine candidate is expected to commence with Phase 1 results expected to be out by the fourth quarter of this year.

Considering that Sanofi is one of the leading vaccine makers in the world with roughly $3 billion in sales in flu vaccines alone in 2020, it won’t come as a surprise if their candidate breezes through the trials.

Even prior to this acquisition, Translate Bio has been working on using its mRNA platform to develop vaccines and treatments for a broad range of diseases like liver and pulmonary ailments.

So far, its novel pipeline has 2 clinical-stage programs along with 7 pre-clinical work covering direct therapeutics and vaccines.

One of its lead candidates is MRT5005, which is an mRNA-based therapy for cystic fibrosis (CF).

This is a groundbreaking treatment because it takes advantage of mRNA’s capability to deliver proteins to lung cells. It’s also extremely non-invasive, as patients can simply inhale the mRNA drug into their bodies.

Other than helping with the treatment of CF, this inhalation delivery system can also open avenues for other pulmonary targets.

Most importantly, TBIO’s MRT5005 doesn’t only offer treatments. It actually is a cure for CF.

TBIO’s work on CF treatment is extremely important. This disease is terrible, recording a median age of death among patients in the US as 30.6 years old. In this country alone, over 30,000 people suffer from the condition, and more than 70,000 are recorded worldwide—and the numbers continue to climb each year.

In terms of the CF market, the global demand for treatments for this disease is expected to reach $16.3 billion by 2026, hitting roughly 16.8% in CAGR over the years.

With the acquisition of Translate Bio, Sanofi plows ahead of its competitors in the space, including Pfizer, GlaxoSmithKline (GSK), Johnson & Johnson (JNJ), and Merck (MRK), as the sole Big Pharma company with a wholly-owned in-house mRNA platform.

This is on top of Sanofi’s recent $470 buyout of another mRNA company, Tidal Therapeutics, to bolster its immuno-oncology and inflammatory diseases segments.

Apart from its aggressive buyout strategy, Sanofi also announced its plan to allocate roughly $476 million annually to a “vaccines mRNA Center of Excellence” with the goal of queuing at least six mRNA-based candidates in clinical trials by 2025.

Allotting $476 million to this plan is a telling move on the company’s future direction, as it comprises a substantial fraction of Sanofi’s $6.5 billion overall R&D budget.

These moves strongly signal that Sanofi’s going all-in on the mRNA platform, which could obviously pose a challenge to the likes of Moderna and, of course, BioNTech.

With smaller cap companies like bluebird Bio (BLUE) and CureVac (CVAC) still up for grabs, it’s only a matter of time before another big company decides to follow suit.

Mad Hedge Biotech & Healthcare Letter

January 28, 2021

Fiat Lux

FEATURED TRADE:

(WATCH OUT FOR THESE BUYOUT STOCKS)

(TBIO), (MRNA), (PFE), (BNTX), (SNY), (BLUE), (BMY)

Many predictions this 2021 probably won’t pan out. However, here’s a pretty safe bet: we will see a number of biotechnology company acquisitions this year.

Although it’s not easy to accurately forecast which biotechnology companies will be involved in these deals, there is a handful that qualifies as prime acquisition targets.

One of the top biotech buyout candidates in my radar this year is Translate Bio (TBIO).

Thanks to the massive success of the COVID-19 programs of Moderna (MRNA), Pfizer (PFE), and BioNTech (BNTX), a spotlight has been cast on the benefits of the messenger RNA (mRNA) technology.

That’s why I wouldn’t be surprised if bigger players in the healthcare industry decide to scoop up smaller players to stake a claim in this quickly growing space.

Among all the small-cap biotechs in play, Translate Bio is easily one of the top prospects.

Before Moderna and BioNTech hogged the spotlight with their mRNA-based COVID-19 vaccines, Translate Bio was actually one of the strong contenders in the race. Unfortunately, it failed to keep up with its peers and is now lagging well behind the leaders.

On the flip side, the attention that mRNA technology has been getting these days seemed to have strengthened the confidence of investors in the technology – an effect that Translate Bio greatly benefited from in the past months.

Despite its lagging performance in the COVID-19 race, Translate Bio has been making significant progress with its work with partner Sanofi (SNY) on their own candidate, MRT5500. If all goes well, then the product should be out by the first quarter of 2021.

Apart from that, the two have been focusing on different vaccine candidates for other viral and bacterial diseases.

Translate Bio’s pipeline also includes treatments targeting another lucrative market using the same MRT platform technology as MRT5500: cystic fibrosis (CF).

The company’s CF treatment has been causing excitement among investors because instead of offering invasive therapy, this option offers patients an inhaled version of the mRNA drug as treatment.

Moreover, the MRT platform technology of Translate Bio could be expanded to cover more than just CF – a promising diversification that encouraged big investors like Sanofi to continuously pour money into collaborations with this Massachusetts-based biotech.

As mRNA technology gains more traction, Sanofi might even reevaluate its relationship with Translate Bio and decide that it wants more than just a collaboration.

With the smaller biotech company’s modest market capitalization of only a little over $1.7 billion, an acquisition could be on the table sooner rather than later.

Another potential buyout candidate is Bluebird bio (BLUE).

Unlike its contemporaries in the biotech space, Bluebird shares plunged by nearly 50% in 2020.

Although the company offers a promising upside potential, it can’t seem to generate sufficient enthusiasm to take part in the biotech sector’s rally last year.

In fact, Blue stock continued to hover near its 52-week low despite several gene and cell therapy tickers reaching all-time highs.

While that’s obviously bad news for Bluebird shareholders, I think this makes the company an even more attractive acquisition candidate.

I think it’s important to determine the reasons behind Bluebird’s abysmal 2020 performance.

The stock had a rocky start last year, with the COVID-19 pandemic exacerbating its overall meltdown.

One of Blue’s major roadblock was its failure to secure approval from the FDA for its multiple myeloma treatment, which it has been working on with Bristol Myers Squibb (BMY).

Then, it delayed its submission for approval of its sickle cell disease treatment LentiGlobin. This was initially set for the second half of 2021 but was pushed to late 2022.

The main takeaway from this streak of negative updates is that Blue still doesn’t have its act together when it comes to dealing with regulatory approval processes.

Regardless, the potential of this biotech’s pipeline remains impressive.

Apart from its work with Bristol and LentiGlobin, Bluebird has been working on a late-stage candidate for treatment of a rare metabolic disorder called cerebral adrenoleukodystrophy with Lenti-D.

Prior to its partnership with Bristol, Bluebird was actually partnered with Celgene.

When Celgene was bought by Bristol in 2019, the bigger company continued the collaboration with Blue and expanded the partnership to cover more genetic disorders and extend to oncology treatments.

Due to the setbacks, Bluebird’s market capitalization now hovers somewhere near $3 billion.

Given all these pipeline candidates and its future plans, I suspect it wouldn’t take long before a major player takes notice of this attractive valuation and puts this bird in a cage.

Overall, both Translate Bio and Bluebird are solid companies in the biotechnology space.

While the COVID-19 pandemic slowed down some of their progress, the products in their pipelines could yield substantial value to interested acquisition partners.

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

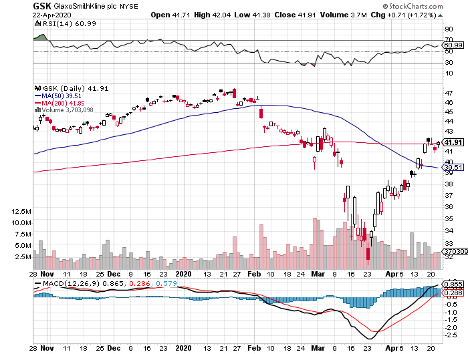

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but take advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but takes advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.