Global Market Comments

April 1, 2021

Fiat Lux

Featured Trade:

(MARCH 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (ZM), ($INDU), (X), (NUE), (WPM), (GLD), (SLV), (KMI), (TLT), (TBT), (BA), (SQ), (PYPL), (JNP), (CP), (UNP), (TSLA), (GS), (GM), (F)

Global Market Comments

April 1, 2021

Fiat Lux

Featured Trade:

(MARCH 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (ZM), ($INDU), (X), (NUE), (WPM), (GLD), (SLV), (KMI), (TLT), (TBT), (BA), (SQ), (PYPL), (JNP), (CP), (UNP), (TSLA), (GS), (GM), (F)

Below please find subscribers’ Q&A for the March 31 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Would you buy Facebook (FB) or Zoom (ZM) right here?

A: Well, Zoom was kind of a one-hit wonder; it went up 12 times on the pandemic as we moved to a Zoom economy, and while Zoom will permanently remain a part of our life, you’re not going to get that kind of growth in stock prices in the future. Facebook on the other hand is going to new highs, they just announced they’re laying a new fiber optic cable to Asia to handle a 70% increase in traffic there. So, for the longer term and buying here, I think you get a new high on Facebook soon; there's maybe another 20-30% move in Facebook this year.

Q: I can’t really chase these trades here, right?

A: Correct; if you wait any more than a day or 2 on executing a trade alert, you’re missing out on all of the market timing value we bring to the game. So that's why I include an entry price and the “don’t pay more than” price. And we never like to chase, except last year, when we did it almost all the time. But last year was a chase market, this year not so much.

Q: How are LEAP purchase notifications transmitted?

A: Those go out in the daily newsletter Global Trading Dispatch when I see a rare entry point for a LEAP, then we’ll send out a piece and notify everybody. But it’s very unusual to get those. Of course, a year ago we were sending out lists of LEAPS ten at a time when the Dow Average ($INDU) is at 18,000. But that is not now, you only wait for those once or twice a year. On huge selloffs to get into two-year-long options trades, and that is definitely not now. The only other place I've been looking out for LEAPS right now are really bombed out technology stocks begging for a rotation. Concierge members get more input on LEAPS and that is a $10,000 a year upgrade.

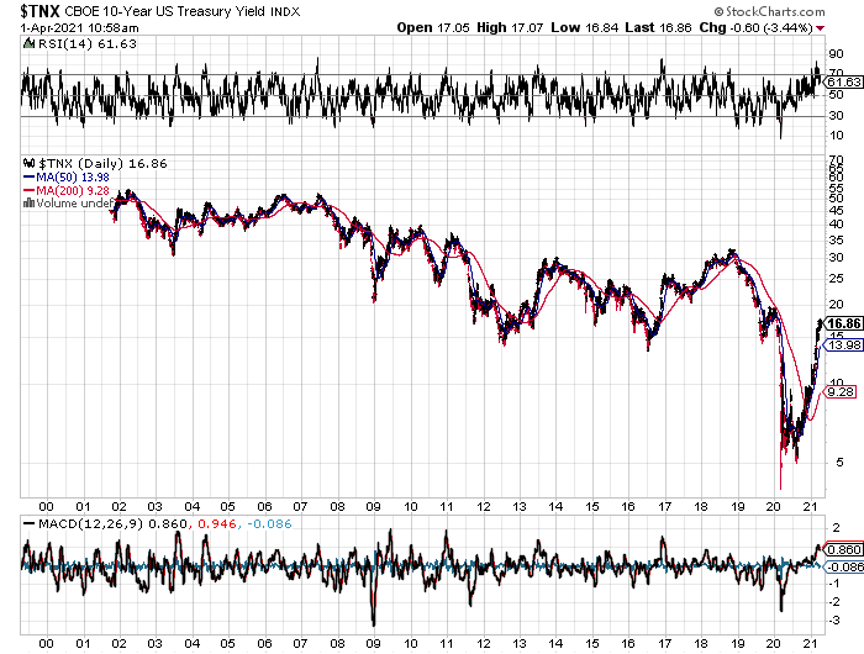

Q: What are your thoughts on silver (SLV) and long-term gold (GLD)?

A: I see silver going to $50 and eventually $100 in this economic cycle, but it's out of favor right now because of rising interest rates. So, once we hit 2.00% in the ten years, it’s not only off to the races for tech but also gold and silver. Watch that carefully because your entry point may be on the horizon. That makes Wheaton Precious Metals (WPM) a very attractive “BUY” right now.

Q: Are you going to trade the (TLT)?

A: Absolutely yes, but I’m kind of getting picky now that I’m up 42% on the year; and I only like to sell 5-point rallies, which we got for about 15 minutes last week. And I also only like to buy 5- or 10-point dips. Keep your trading discipline and you’ll make a ton of money in this market. Last year we made about 30% trading bonds on about 30 round trips.

Q: How much further upside is there for US Steel (X) and Nucor Corp. (NUE)?

A: More. There's no way you do infrastructure without using millions of tons of steel. And I kind of missed the bottom on US Steel because it had been a short for so long that it kind of dropped off the radar for me. I think we have gone from $4 to 27 since last year, but I think it goes higher. It turns out the US has been shutting down steel production for decades because it couldn't compete with China or Japan, and now all of a sudden, we need steel, and we don’t even make the right kind of steel to build bridges or subways anymore—that has to be imported. So, most of the steel industry here now is working for the car industry, which produces cold-rolled steel for the car body panels. Even that disappears fairly soon as that gets taken over by carbon fiber. So enough about steel, buy the dips on (X) and (NUE).

Q: What stocks should I consider for the infrastructure project?

A: Well, US Steel (X) and Nucor Corp (NUE) would be good choices; but really you can buy anything because the infrastructure package, the way it’s been designed, is to benefit the entire economy, not just the bridge and freeway part of it. Some of it is for charging stations and electric car subsidies. Other parts are for rural broadband, which is great for chip stocks. There is even money to cap abandoned oil wells to rope in Texas supporters. All of this is going to require a massive upgrade of the power grid, which will generate lots of blue-collar jobs. Really everybody benefits, which is how they get it through Congress. No Congressperson will want to vote against a new bridge or freeway for their district. That’s always the case in Washington, which is why it will take several months to get this through congress because so many thousands of deals need to be cut. I’ve been in Washington when they’ve done these things, and the amount of horse-trading that goes on is incredible.

Q: Is it a good thing that I’ve had the United States Treasury Bond Fund (TLT) LEAPS $125 puts for a long time.

A: Yes. Good for you, you read my research. Remember, the (TLT) low in this economic cycle is probably around $80, so you probably want to keep rolling forward your position….and double up on any ten-point rally.

Q: Do you think we get a pop back up?

A: We do but from a lower level. I think any rallies in the bond market are going to be extremely limited until we hit the 2.00%, and then you’re going to get an absolute rip-your-face-off rally to clean out all the short term shorts. If you're running put LEAPS on the (TLT) I would hang on, it’s going to pay off big time eventually.

Q: If we see 3.00% on the 10-year this year, do you see the stock market crashing?

A: I don’t think we’ll hit 3.00% until well into next year, but when we do, that will be time for a good 10% stock market correction. Then everyone will look around again and say, “wow nothing happened,” and that will take the market to new highs again; that's usually the way it plays out. Remember, then year yields topped all the way up at 5.00% when the Dotcom Bubble topped in April 2020.

Q: Has the airline hospitality industry already priced in the reopening of travel?

A: No, I think they priced in the hope of a reopening, but that hasn’t actually happened yet, and on these giant recovery plays there are two legs: the “hope for it” leg, which has already happened, and then the actual “happening” leg which is still ahead of us. There you can get another double in these stocks. When they actually reopen international travel to Europe and Asia, which may not happen this year, the only reopening we’re going to see in the airline business is in North America. That means there is more to go in the stock price. Also coming back from the brink of death on their financial reports will be an additional positive.

Q: Do you think a corporate tax increase will drive companies out of the US again and raise the unemployment rate?

A: Absolutely not. First of all, more than half of the S&P 500 don’t even pay taxes, so they’re not going anywhere. Second, I think they will make these offshoring moves to tax-free domiciles like Ireland illegal and bring a lot of tax revenues back to the US. And third, all Biden is doing is returning the tax rate to where it was in 2017; and while the corporate tax rate was 35%, the stock market went up 400% during the Obama administration, if you recall. So stocks aren't really that sensitive to their tax rates, at least not in the last 50 years that I’ve been watching. I'm not worried at all. And Biden was up on the polls a year ago talking about a 28% tax rate; and since then, the stock market has nearly doubled. The word has been out for a year and priced in for a year, and I don't think anybody cares.

Q: What about quantum computers?

A: I’m following this very closely, it’s the next major generation for technology. Quantum computers will allow a trillion-fold improvement in computing power at zero cost. And when there's a stock play, I will do it; but unfortunately, it’s not (IBM), because we’re not at the money-making stage on these yet. We are still at the deep research stage. The big beneficiaries now are Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Q: Is it time to buy Chinese stocks?

A: I would say yes. I would start dipping in here, especially on the quality names like Tencent (TME), Baidu (BIDU), and Alibaba (BABA), because they’ve just been trashed. A lot of the selloff was hedge fund-driven which has now gone bust, and I think relations with China improve under Biden.

Q: Your timing on Tesla (TSLA) has been impeccable; what do you look for in times of pivots?

A: Tesla trades like no other stock, I have actually lost money on a couple of Tesla trades. You have to wait for things to go to extremes, and then wait two more days. That seems to be the magic formula. On the first big selloff go take a long nap and when you wake up, the temptation to buy it will have gone away. It always goes up higher than you expect, and down lower than you expect. But because the implied volatilities go anywhere from 70% to 100%, you can go like 200 points out of the money on a 3-week view and still make good money every month. And that’s exactly what we’re going to do for the rest of the year, as long as the trading’s down here in the $500-$600 range.

Q: Is Editas Medicine (EDIT), a DNA editing stock, still good?

A: Buy both (EDIT) and Crisper (CRSP); they both look great down here with an easy double ahead. This is a great long-term investment play with gene editing about to dominate the medical field. If you want to learn more about (EDIT) and (CRSP) and many others like them, subscribe to the Mad Hedge Fund Biotech & Healthcare Letter because we cover this stuff multiple times a week (click here).

Q: Is the XME Metals ETF a buy?

A: I would say yes, but I'd wait for a bigger dip. It’s already gone up like 10X in a year, but the outlook for the economy looks fantastic. (XME) has to double from here just to get to the old 2008 high and we have A LOT more stimulus this time around.

Q: What about hydrogen?

A: Sorry, I am just not a believer in hydrogen. You have to find someone else to be bullish on hydrogen because it’s not me. I've been following the technology for 50 years and all I can say is: go do an image Google for the name “Hindenburg” and tell me if you want to buy hydrogen. Electricity is exponentially scalable, but Hydrogen is analog and has to be moved around in trucks that can tip over and blow up at any time. Hydrogen batteries are nowhere near economic. We are now on the eve of solid-state lithium-ion batteries which improve battery densities 20X, dropping Tesla battery weights from 1,200 points to 60 pounds. So “NO” on hydrogen. Am I clear?

Q: Why do you do deep-in-the-money call and put spreads?

A: We do these because they make money whether the stock goes up down or sideways, we can do them on a monthly basis, we can do them on volatility spikes, and make double the money you normally do. The day-to-day volatility on these positions is very low, so people following a newsletter don’t get these huge selloffs and sell at bottoms, which is the number one source of retail investor losses. After 13 years of trade alerts, I have delivered a 40.30% average annualized return with a quarter of the market volatility. Most people will take that.

Q: Is ProShares Ultra Short 20 Year Plus Treasury ETF(TBT) still a play for the intermediate term?

A: I would say yes. If ten-year US Treasury bonds Yields soar from 1.75% to 5.00% the (TBT) should rise from $21 to $100 because it is a 2X short on bonds. That sounds like a win for me, as long as you can take short term pain.

Q: What is the timing to buy TLT LEAPS?

A: The answer was in January when we were in the $155-162 range for the (TLT). Down here I would be reluctant to do LEAPS on the TLT because we’ve already had a $25 point drop this year, and a drop of $48 from $180 high in a year. So LEAP territory was a year ago but now I wouldn’t be going for giant leveraged trades. That train has left the station. That ship has sailed. And I can’t think of a third Metaphone for being too late.

Q: Would you buy Kinder Morgan (KMI) here?

A: That’s an oil exploration infrastructure company. No, all the oil plays were a year ago, and even six months ago you could have bought them. But remember, in oil you’re assuming you can get in and out before it crashes again, it’s just a matter of time before it does. I can do that but most of you probably can’t, unless you sit in front of your screens all day. You’re betting against the long-term trend. It works if you’re a hedge fund trader, not so much if you are a long-term investor. Never bet against the long-term trend and you always have a tailwind behind you. All surprises work to your benefit.

Q: If you get a head and shoulders top on bitcoin, how far does it fall?

A: How about zero? 80% is the traditional selloff amount for Bitcoin. So, the thing is: if bitcoin falls you have to worry about all other investments that have attracted speculative interest, which is essentially everything these days. You also have to worry about Square (SQ), PayPal (PYPL), and Tesla (TSLA), which have started processing Bitcoin transactions. Bitcoin risk is spread all over the economy right now. Those who rode the bandwagon up will ride it back down.

Q: Is Boeing (BA) a long-term buy?

A: Yes, especially because the 737 Max is back up in the air and China is back in the market as a huge buyer of U.S. products after a four-year vacation. Airlines are on the verge of seeing a huge plane shortage.

Q: What about Ags?

A: We quit covering years ago because they’re in permanent long-term downtrends and very hard to play. US farmers are just too good at their jobs. Efficiencies have double or tripled in 60 years. Ag prices are in a secular 150-year bear market thanks to technology.

Q: Is this recorded to watch later?

A: Yes, it goes on our website in about two hours. For directions on where to find it, log in to your www.madhedgefundrader.com account, go to “My Account,” and it will be listed under there, as are all the recorded webinars of the last 12 years.

Q: Would you buy Canadian Pacific (CP) here, the railroad?

A: No, that news is in the price. Go buy the other ones—Union Pacific (UNP) especially.

Q: What are your thoughts on Bitcoin?

A: We don’t cover Bitcoin because I think the whole thing is a Ponzi scheme, but who am I to say. There is almost ten times more research and newsletters out there on Bitcoin as there is on stock trading right now. They seem to be growing like mushrooms after a spring storm. There are always a lot of exports out there at market tops, as we saw with gold in 2010 and tech stock in 2000.

Q: What do you think about Juniper Networks (JNP)?

A: It’s a Screaming “BUY” right here with a double ahead of it in two years. I’m just waiting for the tech rotation to get going. This is a long-term accumulate on dips and selloffs.

Q: Did the Archagos Investments hedge fund blow threaten systemic risk?

A: No, it seems to be limited just to this one hedge fund and just to the people who lent to it. You can bet banks are paring back lending to the hedge fund industry like crazy right now to protect their earnings. I don’t think it gets to the systemic point, but this is the Long Term Capital Management for our generation. I was involved in the unwind of the last LTCM capital, which was 23 years ago. I was one of the handful of people who understood what these people were even doing. So, they had to bring me in on the unwind and huge fortunes were made on that blowup by a lot of different parties, one of which was Goldman Sachs (GS). I can tell you now that the statute of limitations has run out and now that it's unlikely I'll ever get a job there, but Goldman made a killing on long-term capital, for sure.

Q: Will Tesla benefit from the Biden infrastructure plan?

A: I would say Tesla is at the top of the list of companies the Biden administration wants to encourage. That means more charging stations and more roads, which you need to drive cars on, and bridges, and more tax subsidies for purchases of new electric cars. It’s good not just Tesla but everybody’s, now that GM (GM) and Ford (F) are finally starting to gear up big numbers of EVs of their own. By the way, I don't see any of the new startups ever posing a threat to Tesla. The only possible threats would be General Motors, Ford, and Volkswagen, which are all ten years behind.

Q: Would you put 10% of your retirement fund into cryptocurrencies?

A: Better to flush it down the toilet because there’s no commission on doing that.

Q: Is growing debt a threat to the economy? How much more can the government borrow?

A: It appears a lot more, because Biden has already indicated he’s going to spend ten trillion dollars this year, and the bond market is at a 1.70%—it’s incredibly low. I think as long as the Fed keeps overnight rates at near-zero and inflation doesn't go over 3%, that the amount the government can borrow is essentially unlimited, so why stop at $10 or $20 trillion? They will keep borrowing and keep stimulating until they see actual inflation, and I don’t think we will see that for years because inflation is being wiped out by technology improvements, as it has done for the last 40 years. The market is certainly saying we can borrow a lot more with no serious impact on the economy. But how much more nobody knows because we are in uncharted territory, or terra incognita.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 29, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT NEVER WAS),

(SPY), (TLT), (TBT), (TSLA), (CSCO), (ORCL), (INTC)

Of course, WWII historians know well the man who never was, the popular name for Operation Mincemeat.

In 1943, British intelligence found a homeless man who died on the streets of London, dressed him up as a Royal Marine Major William Martin, and released his body from a submarine off the coast of Spain, a German ally.

Handcuffed to his wrist was a briefcase with highly detailed plans for the allied invasion of Greece and the Balkans. The Germans shifted ten divisions to defend the region.

When the allies invaded Sicily instead, it came completely out of the blue. The invading American and British forces found the island almost undefended and inadequately manned and supplied by Italian troops. The allies planned for three months to capture Sicily. Instead, they did it in a mere 38 days. Allied losses came in at a tenth of those expected, thanks to Royal Marine Major William Martin.

The analogy here is that last week, we witnessed the market that never was. Stocks went down, then up. Bonds went up, then down. Even Tesla was virtually unchanged. It all ended up as a big fat zero for traders.

What all of this means for us investors is a subject of heated discussion among strategists. Of course, the Cassandras are always out there arguing that this is all proof that markets are peaking and that the mother of all stock market crashes is just ahead of us.

I take a different tack.

I think we are well into a long-overdue “time” correction whereby stocks go sideways for weeks or months before resuming their heroic assault on new highs. The timing will be dictated by the frantic reversal of the bond market at a ten-year Treasury yield of 2.00%.

Investors will rotate from the newly expensive recovery plays like banks into the newly cheap, such as technology stocks. Notice the sudden recent interest in legacy companies like Oracle (ORCL), Intel (INTC), and Cisco Systems (CSCO), which completely missed the great 2020 tech rally.

All of this sets up perfectly for the barbell portfolio which I have been advocating all year.

If there is a selloff, it will be by things that normal people don’t own. Those include SPACS, anything the Reddit crowd chases, stay-at-home stocks, and very high-priced tech stocks with no earnings.

Much focus has been placed on the Taiwanese-owned Ever Given stuck in the Suez Canal. As a Middle Eastern war correspondent for many years, I spent endless hours debating with my compatriots over what closure of the canal would mean.

What hasn’t been mentioned was that the accident was not caused by a Chinese captain, but Egyptian pilot ships are required to take on to raise revenues, and bribes, for the impoverished country. This all happened in the middle of a sandstorm where visibility is near zero.

I can tell you right now that they won’t get the Ever Given off there until they start to unload containers and lift off some weight so the 200,000-ton ship can rise of its own accord. Good luck with that in the middle of the Sinai Desert. Why not just sell all the contents on Amazon and have them deliver it for free as part of their prime membership?

This is a debacle that will last weeks, if not months, and will cost $9 billion a day in international trade until it’s over. In the meantime, commercial shippers have asked for protection from pirates from the US Navy as they navigate the unfamiliar water around the tip of Africa.

The Mad Hedge Summit Videos are Up, from the March 9,10, and 11 confab. Listen to 27 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here, click on CURRENT SUMMIT REPLAYS in the upper right-hand corner, and then choose the speaker of your choice.

Weekly Jobless Claims dive by 100,000, to 684,000, a one-year low. The decline was led by Illinois and Ohio. Labor shortages are popping up around the country in skilled areas, but bars and restaurants are still lagging severely.

Huge Office Cuts are coming, with execs planning a permanent 20% cut. Better to give the money to shareholders. Downtowns across the country will change beyond all recognition. How do you turn an office into an apartment?

CP Rail buys Kansas City Southern, for $25 billion, further concentrating the north American rail industry. It’s a steal because an economy entering a decade-long boom moves lots of stuff. It’s also a great North/South international trade play, which is recovering strongly with the exit of our last president. I used to ride box cars on the old Canadian Pacific back in the sixties (you can’t hitch hike where there are no cars), and occasionally the engineers would let me drive. It suddenly makes Norfolk South (NSC) and Union Pacific (UNP) look very tempting.

Another Tesla $3,000 Target was issued by Ark’s Cathie Wood, an early investor. Cathie’s Ark Innovation Fund ETF was up 180% last year largely on the strength of a massive Tesla (TSLA) holding. Her bear case is a low of $1,500 by 2025, nearly triple the current price. She has only one more triple to go to get to my own $10,000 forecast.

Biden has $3 Trillion More to Spend on top of the just passed $1.9 trillion rescue package. It's all rocket fuel for the stock market, not so much for bonds. The money will be spent on a mix of old-line freeway and bridge repair along with new spending on decarbonizing the power grid and social measures. It will be financed by tax hikes on those earning over $400,000. Remember, Roosevelt hiked the maximum tax rate to 90% on the wealthy, where it stayed for 30 years, and Biden is old enough to remember.

Daily Air Travelers top 1.5 Million, for the first time in a year. The pandemic low was 200,000 a day. It’s an indication of how anxious Americans have become to travel, and how strong the imminent economic boom will be.

Intel to build two chip fabs for $20 billion in Arizona to address the current severe shortage. US construction is a positive as it helps reduce reliance on foreign supplies. Too bad it will still leave them five years behind (AMD), but it’s a major move in the right direction. It deals with everything investors wanted to hear and moves them solidly into the 10nm architecture market. Buy (INTC) on dips.

New Home Sales Dive, off 18.2% in February, now that the free money train has left the station. Weather was blamed as a factor, with giant snowstorms slamming much of the country. Shortage of supply is another big issue. Some big builders are basically out of inventory and are reduced to selling floor plans with extended completion dates.

US Dollar (UUP) hits a four-month high, with a major assist from rising US bond interest rates. Expect the rally to continue until ten-year yields hit 2.00%, then sell the daylights out of it. With the US money supply growing at a near exponential 30% annual rate, there’s no way the dollar strength can continue. When you increase the supply, you decrease the value, simple supply and demand. My first pick is to buy the Aussie (FXA) a call option on a global synchronized economic recovery.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000, here we come!

It’s amazing how well patience can help your performance. My Mad Hedge Global Trading Dispatch profit reached a super-hot 18.61% so far in March on the heels of a spectacular 13.28% profit in February.

It was a go-nowhere week in the market, so I limited myself to a single trade all week, a double short in the bond market (TLT) on top of a welcome $5 rally. The position turned immediately profitable.

I still have a deep in-the-money call spread Tesla (TSLA) that is profitable and expires in 14 trading days. That leaves me with 70% cash and a barrel full of dry powder.

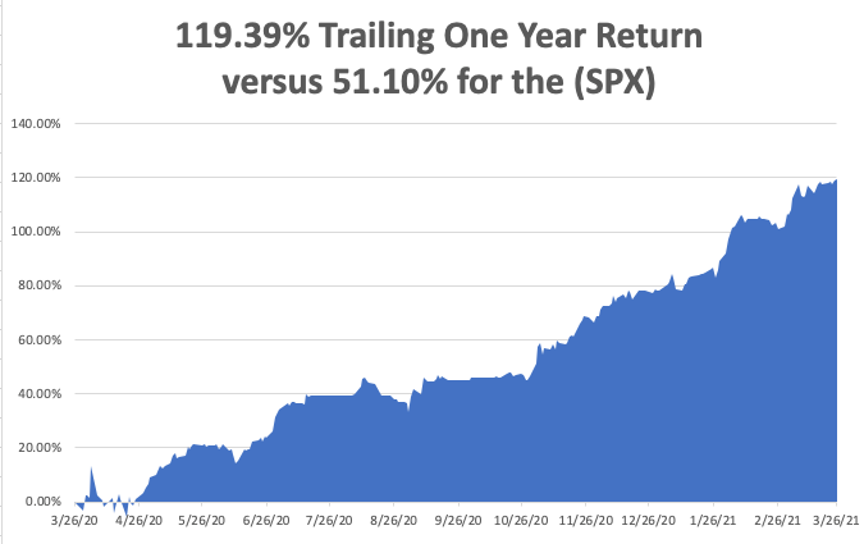

This is my fifth double-digit month in a row. My 2021 year-to-date performance soared to 42.10%. The Dow Average is up 9.9% so far in 2021.

That brings my 11-year total return to 464.65%, some 2.08 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.30%.

My trailing one-year return exploded to positively eye-popping 119.39%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Corona virus cases at 30.2 million and deaths topping 550,000, which you can find here.

Thankfully, death rates have slowed dramatically, but Obituaries are still the largest sector in the newspaper. At this point, some 47% of the US population has achieved immunity through vaccination or catching the disease. Herd immunity is near.

The coming week is a big one for jobs data.

On Monday, March 29, at 9:00 AM, the Dallas Fed Manufacturing Index for March is released.

On Tuesday, March 30, at 9:00 AM, the S&P Case Shiller National Home Price Index for January is published.

On Wednesday, March 31 at 8:15 AM, the ADP Challenger Private Employment Report for March is out. Pending Home Sales for February are indicated at 9:00 AM.

On Thursday, April 1 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, April 2 at 8:30 AM we get the Nonfarm Payroll Report for March. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, tax time is coming up and let me tell you, I have absolutely the best IRS story of all time.

It comes from my late, dear friend, Al Pinder, who I sat next to for ten years at the Foreign Correspondents of Japan in Tokyo, pounding away on antiquated Royal typewriters until our shoulders were as stiff as boards. Al then was the shipping correspondent for the New York Journal of Commerce newspaper.

Al was a colorful character, to say the least.

In the run up to WWII, Al took an extended vacation in Japan where he toured and photographed the country’s beaches, looking for the best landing sites for the US military in case war broke out.

To sneak the top-secret pictures out of the country, he bought a large steamer trunk and placed them a false bottom. Then he went to Tokyo’s red-light district in Yoshiwara, bought a dubious sex toy, an inflatable life-sized Japanese doll, and placed it on top.

When the trunk was searched, the customs officials found the doll, had a good laugh and passed him on. Al’s photos were the basis of Operation Olympic, the 1945 US invasion of Japan, made unnecessary by the dropping of the atomic bomb.

When the war broke out, Pinder parachuted into western China, where he acted as the liaison with Mao Zedong’s guerilla forces in Hunan province. In 1944, Al received a coded message from headquarters ordering him to intercept a top-secret airdrop from a DC3 in the middle of the night.

Knowing he would be mercilessly tortured by the Japanese if caught, he set up three signal fires in a triangle in a remote part of the desert and managed to find the parachute. Dodging enemy patrols all the way, he returned to his hideout in a mountain cave and opened the package.

In it was a letter from the IRS asking why he had not filed a tax return for the past three years.

I told this story at Al’s wake a few years ago and everyone had a good laugh. Al went on to run CIA operations in Japan during the fifties and sixties. When he passed away, there was a frantic search for a safe deposit box by American intelligence officials containing records of all CIA payoffs to Japan’s leading conservative party.

When the box was finally found, there was an enormous sigh of relief at the embassy. I still miss Al.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 19, 2021

Fiat Lux

Featured Trade:

(MARCH 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(JPM), (TLT), (TBT), (SQ), (MMM), (SIL), (QQQ), (WMP), (CCIV), (TSLA), (USO), (CRSP), (PLTR), (HYG), (FCX), (XME)

Below please find subscribers’ Q&A for the March 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: I’ve heard that the COVID-19 cases are being understated by 16 million. Do you think this is true?

A: Yeah, I've always argued that the previous government's numbers were vastly underestimating the true number of cases out there for political purposes, but we are on the downslide regardless, so that’s good.

Q: When are tech stocks going to bottom out and when can I buy them?

A: I knew I would get this question. This is the question of the day. Picking bottoms is always tough because these are momentum plays and not valuation plays. I’ll give you a couple of levels though. The tech (QQQ) multiple is now at 25X earnings and the S&P 500 (SPY) is at 22X, so your first bottom will be down about 10% from here, or a 22X multiple. And I don’t think we will get much lower than that because tech stocks are growing at 20-25% a year, versus the (SPY) growing at maybe 10%, and I don’t think tech goes to much of a discount in that situation. So, you’re just waiting for interest rates to top out and start to go down, which will be the other indicator of a tech bottom. We had a slowdown in the rise of rates for just a couple of days this week, and tech stocks took off like a rocket. Those are your two big signals.

Q: With the Fed announcement, are you still in the Invesco QQQ Trust NASDAQ ETF (QQQ) bear put spread?

A: Yes, one of them expires in two days so that’s a piece of cake. The other one expires in a month, but it is way out-of-the-money—the April $240-$245 bear put spread, so I’ll keep that for a real meltdown day. But if it looks like we’re getting a breakout, I will come out of that short position so fast it will make your head spin.

Q: Do you like Palantir (PLTR)?

A: Absolutely yes—screaming LEAP candidate. It traded all the way down to $20 two weeks ago and is trading around $25 now. It’s a huge data firm, lots of CIA and defense work, huge government contracts extending out for years, cutting edge technology, and run by a nut job, so yes screaming buy at this level.

Q: Freeport McMoRan (FCX) is taking some pain here, is this still a buy and hold?

A: Yes, it’s taking the pain along with all the other domestic stocks, which is natural. In their case though, it’s up almost 10x from its bottom a year ago where we recommended it, so yeah I'd say time for a rest. So I’m still a buyer of the metals and (FCX) on dips, but like all other metals, it did get overextended. EV manufacturing is doubling this year, which uses a ton of copper. The same is true with solar panels and Chinese industrial recovery. When all your major markets are doubling in size, it’s usually good for the stock. I peaked at $50 in the last cycle and could touch $100 in this one.

Q: What are your thoughts about the Lucid EV SPAC, Churchill Capital IV (CCIV)?

A: Don’t touch it with a ten-foot pole. They only have 1 or 2 concept vehicles for high-end investors to test drive. The rumor is that their main factory will be in Saudi Arabia where the bulk of the seed capital came from. They’ll never catch up with Tesla (TSLA) on the technology. There's always going to be a few niche $250,000 cars out there, and they have no proof they can actually make these things. When they get to a million vehicles a year, then I might be interested. But they haven't done the hard part yet, which is mass-producing battery packs for a million cars. They've only done the easy part which is designing one sexy prototype to raise money. So, stay away from Lucid, I don’t think they’re going to make it.

Q: What about oil?

A: I am avoiding oil plays like the plague.

Q: When do you anticipate your luncheons to be back?

A: Maybe in 2023. I don’t want to scare off my customers by inviting them to a lunch where they all get COVID-19. If I did have a lunch, I’d have a vaccine requirement and a temperature gun to hit them at the door like everywhere else. I really miss meeting subscribers in person.

Q: Should I buy banks like JP Morgan (JPM) at this level?

A: I would say no. That ship has sailed. Wait for a steeper selloff or just let it run. We’ve already had an enormous move and you don’t want to chase it with a low discipline trade, which is what that would be.

Q: What do you think of silver (SLV)?

A: It’s a buy long term, short term it’s in the grim spiral of death along with the other precious metals, which absolutely hate rising interest rates. A silver long here is the equivalent of a bond (TLT) long. When you do go into silver, buy Wheaton Precious Metals (WPM) for the leveraged long play.

Q: Is 3M (MMM) going to extend the upside?

A: Probably yes, that's a classic American industrial play and a great company. I have friends who work there. How could we live without Post-it notes, Scotch Tape, and Covid-19 N-95 masks?

Q: What about Square (SQ)?

A: I love it in the long term, buy on the dips and buy it through LEAPS (long term equity anticipation securities).

Q: Should I unwind my leveraged financial ETF?

A: I’d say take a piece off, yeah; you never get fired for taking a profit. And they have had a tremendous move. Plus of course, the flip side of taking profits on domestic recovery stocks is to buy tech with that money. And eventually, that's what the entire market will do, it just may still be a little bit early.

Q: What’s a good target for LEAPS for CRISPR (CRSP) and Palantir (PLTR)?

A: Put your first strike 30% higher than today’s stock price and go 2 years out in maturity. I noticed on some names, the June 2023’s are starting to trade, but they’re highly illiquid. But if you put a bid in there and you get a market meltdown, you will get hit.

Q: If the long-term future for oil (USO) is so bad, why is it $65?

A: A few reasons. #1, huge short covering action. #2, economy recovery faster than people expected because of the stimulus. #3, a lot of people, mostly in Texas, Oklahoma, and Louisiana, don’t believe that there will be an all-electric grid in 20 years and think that oil will be in demand forever, including the entire oil industry, so they’re in there buying. And #4, the Saudis have held back with production increases to push the price up, so they’re letting it run so they can sell at a higher price. When they do sell, oil crashes again.

Q: Can we re-watch this presentation?

A: Yes, we post it about 2 hours later on the website so all our people in about 135 countries can access it whenever they like. Just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Q: How often do you have these webinars?

A: Every two weeks, and if you need help accessing it on your account page, email customer support at support@madhedgefundtrader.com.

Q: Is it time to initiate short positions on oil companies?

A: Not yet but keep it in the back of your mind. When some of the super-hot economic data come out after Q2, that may be your short in oil—then we may get into the $70’s a barrel. But not yet, there’s still too much upward momentum.

Q: Do you think we will see the 30-year fix below a 3.00% yield again?

A: Yes, in the next recession, which may be 5 or 10 years off because we’re starting at such a low base.

Q: Regarding copper, EV motors require a ton of copper. Doesn’t that make the metals a BUY?

A: That is true, and why we recommended Freeport McMoRan at $4 a year ago and recommended buying every dip. Each one of these rotor motors on each wheel of a Tesla weighs about 100 lbs—I’ve lifted them. Remember I tore apart a Tesla once just to see what made it tick, and they’re really heavy, and they use a lot of copper, and silver as well. So that has always been the bull market case for copper, as well as the fact that China re-emerged as a major buyer for their industrial buildout. That’s why we had a long in the SPDR S&P Metals and Mining ETF (XME).

Q: Do you foresee a good opportunity to go heavy into margin again?

A: Maybe if we get a decent selloff this summer, but you’ll never get the opportunity we had a year ago when you really wanted to put 100% of your portfolio into 2-year LEAPS. The people who did that made many tens of millions of dollars, which is why I get a free bottle of Bourbon every month. That was a once in 20 years event.

Q: What is your 2021 target for the S&P 500 (SPX)?

A: $4,860. It’s in my strategy letter which I sent out on January 6th, and that is all still posted on the website, click here for it.

Q: How do I renew my subscription with your company, and how do I figure out what I bought?

A: Email customer support at support@madhedgefundtrader.com and they will answer you immediately.

Q: Do you follow the iShares IBoxx High Yield Corporate Bond ETF (HYG)?

A: Yes, that is the high yield junk bond fund, but I have been avoiding long bond plays, as you may have noticed with my screaming short of the past year. We list (HYG) in these slides in the Bonds section.

To watch a replay of this webinar, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (as the case may be), then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 23, 2021

Fiat Lux

Featured Trade:

(THE UNITED STATES OF DEBT),

(TLT), (TBT), ($TNX)

Global Market Comments

January 25, 2021

Fiat LuxFeatured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE COMES THE SUPERHEATED ECONOMY),

(SPY), ($INDU), (TLT), (TBT), (TSLA)

The US economy is in the worst condition in a century. The U6 Unemployment rate stands at 20 million today. Main streets everywhere are boarded up. Millions of businesses have gone under. Some 4,500 people a day are dying from a dreaded virus.

All of this means that you should rush out and buy and stocks, as many as possible, with both hands, and by the bucket load. It’s time to take out that home equity loan and pour it into stocks, damn the torpedoes.

For things are about to get better for the US economy, a whole lot better, better beyond anyone’s wildest imagination, and for you individually.

Speaking to CEOs, fund managers, and hedge fund strategists, it is clear that most are wildly underestimating the strength of the 2021 recovery. People haven’t really added up all the stimulus and quantitative easing that is about the hit, which could reach $20 trillion. The total market value of US stock markets is only $51 trillion.

I hate to engage in some simplistic calculations here, but if you increase the amount of capital going into the economy by nearly 50% in two years, stocks just might go up by nearly 50% in two years. It’s no more complicated than that.

In fact, economic conditions are about to improve so fast that the Federal Reserve may have to break its promise about not raising interest rates for three years and instead start nudging them up by the end of 2021.

Needless to say, this is terrible news for the bond market (TLT), where I am lining up to go from a double to a triple short.

You are already starting to see other analysts ratchet up their overcautious yearend S&P 500 target. By November, they may reach my own outsized goal of 4,800, bringing in a total gain in stocks of 35%.

All of this explains why stocks just absolutely refuse to go down, even a little bit. Each one-day decline seems to be met with a wall of buying. The memo is out: you absolutely have to get into this market, whether you are an individual, hedge fund, institution, or outright bet the ranch gambler.

Of course, if you think I’m so bullish because I made 90% on my money since the April bottom, you’d be right.

Just keep your discipline and observe the basic rules of trading: 1) Don’t buy a position that is so big that it can’t handle a normal 10% correction, 2) Don’t accumulate a position that is so big that you can’t sleep at night, 3) No calling John Thomas in the middle of the night and asking “I have a 3X position in this and their trading down in Asia, what should I do?”

If you have to ask the question, your position is too big.

Biden’s economic plan boosts growth forecasts, according to Goldman Sachs. Prospects have jumped from 6.4% to 6.6%, the highest in a half-century, on the back of a massive Covid-19 package.

Treasury Secretary Janet Yellen says “GO BIG” or go home to the Senate Finance Committee. She was there to get confirmation and push for Biden’s $1.9 trillion stimulus package. Markets are underestimating the extent of the stimulus headed our way, which could reach $10 trillion in addition to another $10 trillion in quantitative easing. Buy dips.

Index Funds are getting trashed, substantially trailing the S&P 500, as single-story stocks dominate the market. It’s become a stock pickers market in the extreme, with no more obvious example that (TSLA), up 1,000% in 9 months. Small caps, IPOs, and cyclical are getting all the action, leaving the (SPX) in the dust.

Tesla delivered its first Chinese Model Y, which will add 250,000 units to sales in 2021. It’s all part of Elon’s quest to take over the global automobile market. He plans to boost sales from 500,000 last year to 20 million in a decade. If so, the stock today still looks cheap. But is the quality the same?

Tesla Q4 registrations soar by 63%, in California, its largest market. It’s due to the runaway success of the Model Y small SUV. The stock is taking a long-overdue rest with a sideways “time” correction. It’s still true that if you buy the stock, you get the car for free.

Weekly Jobless Claims are still sky-high at 900,000. It’s a decline on the week but still horrifically high. The stock market may be starting to notice, with stocks moving sideways for two weeks.

Existing Home Sales soared to a 15-year high, up an amazing 22% YOY in December to a seasonally adjusted 6.76 million units. In the meantime, inventories hit all-time lows at only 1.9 months as they can’t build them fast enough. Sales of $1 million-plus homes are up an incredible 94%. The hottest markets were in Austin, TX, Tampa, FL, and Phoenix, AZ. New York was the worst, followed by San Francisco. The market is on fire and could continue for another decade. Pending tax breaks from the new tax bill will give homeownership another big push.

US Housing Starts jump 5.8%, to 1.7 Million units. Single-family homes are up 12% YOY, driven by the pandemic. Notice the enormous supply/demand gap which assures that home prices will keep rising for years. Rising mortgage interest rates so far have had no effect.

US Manufacturing PMI hits 14-Year high, according to Markit, their index jumping from 57.1 to 59.1. The performance would have been better if it weren’t for rampant parts shortages nationwide. It’s another argument for the long-term bull case.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch shot out of the gate with an immediate 7.25%so far in January. That is net of a 4% loss on a Tesla short which I added one day too soon. Given the great heights of the market, I have trimmed my book to just a long in Tesla and a Short in US Treasury bonds.

That brings my eleven-year total return to 430.30% double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.80%. My trailing one-year return exploded to 74.44%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 90% since the March low.

The coming week will be a big one for big tech earnings.

We also need to keep an eye on the number of US Coronavirus cases at 25 million and deaths at 420,000, which you can find here. We are now running at a staggering 4,500 deaths a day.

When the market starts to focus on this, we may have a problem.

On Monday, January 25 at 9:30 AM EST, we get the Chicago Fed National Activity Index for December. Phillips (PSX) and Kimberly Clark (KMB) report.

On Tuesday, January 26 at 10:00 AM, we learned the new S&P Case Shiller National Home Price Index. Microsoft (MSFT), Johnson & Johnson (JNJ), and American Express (AMEX) report.

On Wednesday, January 27 at 10:00 AM, US Durable Goods for December are published. Apple (AAPL), Facebook (FB) and Tesla (TSLA) report.

On Thursday, January 28 at 9:30 AM, the first look at US GDP for Q4 is announced. McDonald’s (MCD), American Airlines (AA), and Visa (V) report.

On Friday, January 29 at 9:30 AM, US Personal Income and Spending for December is published. Ely Lilly (LLY) and Caterpillar (CAT) report. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I have never been big on the “meme” thing, but you have to love the one that has been circulating about Bernie Sanders. Suddenly, he showed up on every transit system in the country. Clearly, the country was dying for a laugh. I include several pictures below. Hopefully, I won’t end up like him someday.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 18, 2021

Fiat LuxFeatured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHAT WOULD KILL THIS MARKET?)

($INDU), (TLT), (TBT), (GLD), (GOLD), (WPM), (TESLA)