The global bond markets have been screaming an ugly message at us loud and clear, and I’m afraid that it’s not a positive one.

Amazingly, US Treasury bonds have soared early this year, taking the (TLT) up a stunning 40 points.

In the meantime, stocks have suffered the sharpest crash in history, plunging ten times faster than the worst days of the 1929 crash, down 37%.

The implications for your investment portfolio are so momentous and far-reaching that I am going to have to list them one by one.

Read them and weep:

1) The US is in a severe depression.

2) The pandemic is not even close to ending. US deaths topped 85,000 yesterday and may triple from here.

3) The presidential election has become a major source of instability, and no one has any idea of how this will all end. Trump is currently trying to bankrupt the US Post Office to frustrate mail-in voting.

4) The immigration crisis is reaching a humanitarian crisis of epic proportions. It has become our Syria, which landed four million immigrants in Europe.

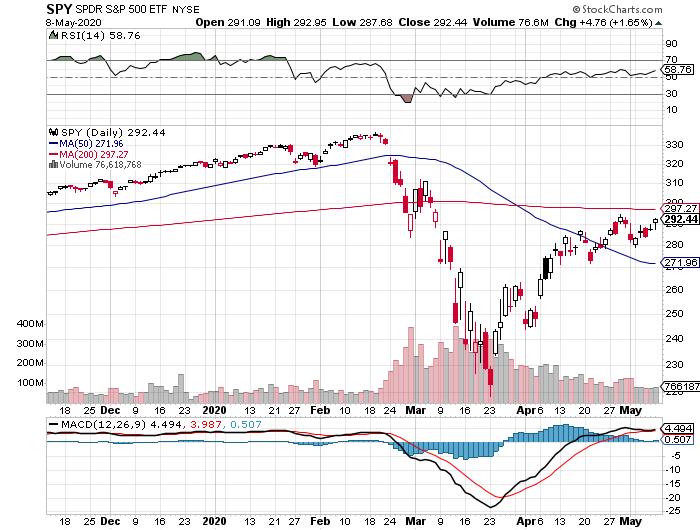

5) The stock market is in the process of crashing…. Again, failing dramatically at the 200-day moving average. That “Sell in May” thing may work big time this year.

6) The Trump trade is toast. Financials, commodity, energy, coal, and industrial stocks are leading the charge to the downside.

7) Oil (USO) is in free fall and may go negative again, another classic recession predictor. For the first time in history. Most small and medium-sized energy companies will go under. Coal has dropped to a historic low of 19% of US electricity production, less than total alternative sources, and is never coming back.

8) Bitcoin is rocketing, up an eye-popping 100% since the crash began. This has become the big hot money trade of 2020 in addition to that other great flight to safety trade, gold (GLD).

9) The US dollar (UUP) is flatlining, wiping out the growth of the foreign earnings of US multinationals. Foreign economies are collapsing even faster than ours, taking their interest rates and currencies lower at warp speed.

10) The unemployment rate, now at all-time lows, not bottom out for months. The great irony here is that while the president vociferously campaigned on an aggressive jobs program, he may well preside over the biggest job losses in history. The Fed is targeting total unemployment of 52 million, worst than the Great Depression.

For more on this, please read my recent piece, “Why You Will Lose Your Job in the Next Five Years and What to Do About It” by clicking here.

There is another alternative explanation to all of this.

A certain Monty Python sketch about a parrot comes to mind.

That all we saw a giant short squeeze in the hedge funds’ core short position in bonds for the umpteenth time, and that we are almost done.

Hedge funds have grown in size to where they are now the perfect contrary market indicator. It is the classic “Too many people in one side of the canoe” trade. A Yogi Berra quote comes to mind; “Nobody goes there anymore because it is too crowded.”

There are other structural factors at play here which are hard to beat. For more on this, please read my opus on “Why Are Bond Yields So Low” by clicking here.

Long Bonds are About to Take a Chainsaw to Your Portfolio

https://www.madhedgefundtrader.com/wp-content/uploads/2019/06/john-chain-saw.png399261MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2020-05-14 08:02:402020-06-15 12:09:57Ten More Ugly Messages from the Bond Market

I always get my best ideas when hiking up a steep mountain carrying a heavy backpack.

Yesterday, I was just passing through the 9,000-foot level on the Tahoe Rim Trail when suddenly, the fog lifted and the skies cleared. I was hit with an epiphany.

It was my “AHA” moment.

The next American Golden Age, the next Roaring Twenties, started on March 23.

However, you have to dive deep into investor psychology to reach that astonishing conclusion.

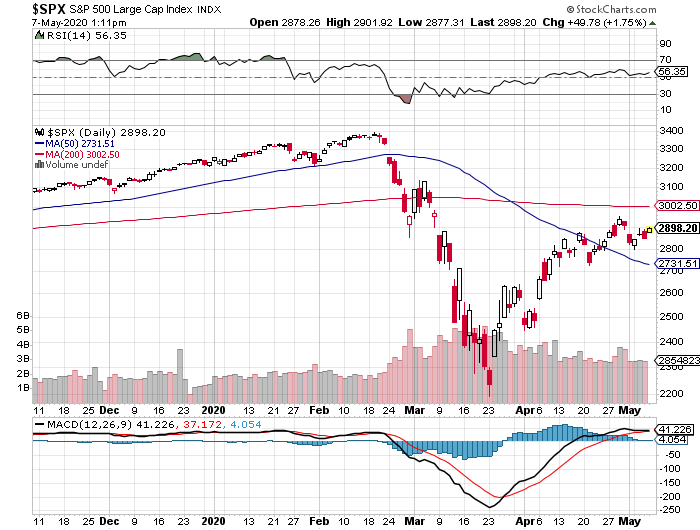

The conundrum of the day is why stocks are trading at a plus 30X multiple two months into a Great Depression. The economic data has been so horrific that the mainstream news has been reporting them.

Some 30 million unemployed on the way to 51 million? Those are Fed numbers, not mine (click here for the link ). Over 52% of small businesses going bankrupt in the next six months? A GDP that is shrinking at an amazing -40% annualized rate?

Yet, we have a Dow Average that has risen a breathtaking 38% in six weeks. The market has essentially dropped 38% and risen 38% over three months, with the Volatility Index (VIX) making a brief visit to the $80 handle.

To understand these massive contradictions, you have to understand what investors think they are buying. They are not hoovering up stocks that are cheap, offer value, or at the bottom of an economic cycle.

Instead, they are investing in a hope, a vision, an expectation that the coming decade will bring a major economic boom. Yes, they are buying my coming American Golden Age.

Only 10% of the value of a stock is reflected in current year earnings, according to Dr. Jeremy Siegal at the Wharton School of Economics (click here to go to the site). The other 90% is in the following nine years. Investors have written off this year’s earnings and are paying up for the following nine.

Long term followers of this newsletter are well aware of my approaching forecast of the next Roaring Twenties (click here for the link).

Except that this time we have a catapult, the pump-priming effects of the pandemic. The government has stepped in with $14 trillion worth of fiscal and monetary stimulus. Creative destruction is taking place at an exponential rate. Companies have to become hyper-efficient overnight or die.

It’s not rocket science. More than 85 million millennials are aging into their peak spending years, buying homes, cars, and all the luxuries of life. Every time this has happened for the past century, US economic growth leaped to 4%.

It happened in the 1920s, the 1960s, the 1990s, and is about to take place in the 2020s. And with each pop in growth, the stock market rises about 400%. Look at your long-term charts and you’ll see I’m dead right.

That takes us from the March 23 Dow Average low at 18,000 up to 72,000 by 2030, except that it’s a low number. Throw in the hyper-acceleration of innovation by the technology and biotech sectors, a Dow 120,000 is within reach.

You may recall that number from my marketing pitches, except that this time it’s happening. In a decade you are going to look like an absolute genius by following the recommendation of the Mad Hedge Fund Trader.

It also means that we may not see market corrections of any more than 10% this year. That would take us down to a Dow Average of 22,500, and an (SPX) of 2,600 in the coming months. That’s where you should jump in and buy with both hands. The only way I would be wrong is if the US epidemic explodes to unimaginable levels, which is not impossible.

Last week, U-6 unemployment rates exploding to a stratospheric 22.8%. The rate was far higher among high school graduates, but only 8% for college grads. Some 20.2 million lost jobs, ten times the previous record, and more than seen during the Great Depression. The BLS (click here) said the true figure was probably 5% higher due to counting anomalies and a huge backlog of data. And this is just the beginning. The good news is that next month, only 10 million jobs will be lost.

NASDAQ (QQQ) turned positive for 2020, and the followers who piled into tech LEAPS at the March bottom are eternally grateful. Tech and biotech are the only places to be. Everywhere else is a waste of time and money. The entire country is turning into a tech economy or going out of business. Buy tech on dips.

Warren Buffet sold all his airline shares, taking a major loss, including Delta (DAL), Southwest (LUV), American (AA) and United (UAL). The Fed’s $50 billion airline bailout blocked him from making a real killing. His Berkshire Hathaway (BRK/A) (click here) owned close to 10% of all of them. The complete collapse of tourism and business travel are the issues. He sees no recovery in the foreseeable future. They don’t call him the “Oracle of Omaha” for nothing.

US Auto Sales are down a mind-blowing -48% in April, the worst on record. Only 8.6 million cars were sold in the US against last year’s annual rate of 17 million. Toyota and Honda saw the biggest falls as their ships can’t unload due to lack of storage space.

The US Treasury will borrow $3 Trillion this Quarter to fund the massive bailout programs. Announced programs amount to 20 times the $789 billion 2009 rescue package, which Republicans opposed. I’m increasing my bond shorts. Sell short (TLT) again, even if we don’t get a decent rally. Oh, and Trump is threatening a default too. He doesn’t see the connection.

Bonds crashed on massive issuance, with the Treasury announcing a record 20-year bond floatation. Yields hit a one-month high. With the (TLT) down $18 from its recent high, I am taking profits on my bond shorts. I’ll be selling the next rally….again. This could be my core trade for the next decade.

Consumer Debt soared to $14.3 trillion in Q1, a new all-time high. A lot of people are living on their credit cards right now.

Trump threatens to cancel China trade deal, blaming them for Covid-19, sending stocks into a 400-point dive. The last time he did this, shares plunged 20%. It’s all part of an effort to divert attention from the administration’s disastrous handling of the pandemic. America’s Corona deaths are now 20 times China’s, and they are still an emerging nation. Just what we needed, a renewed trade war on top of a pandemic-caused Great Depression, as if the market needed more uncertainty. Sell rallies in the (SPY)

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years again, up a gob-smacking +6.46%. We are now only 0.65% short of a new all-time high.

My aggressive short bond positions came in big time on the back of theannounced $3 trillion in new debt issuance in Q2. Short bonds are far and away the better quality trade of buying stocks at these elevated levels.

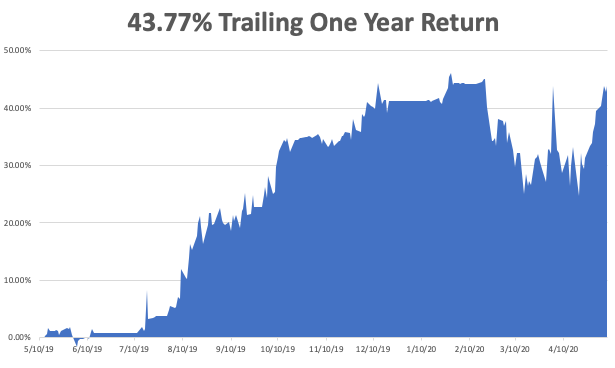

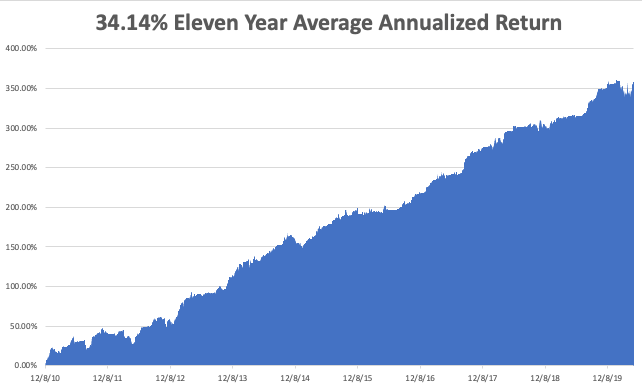

May is up +6.46%, taking my 2020 YTD return up to 2.59%. That compares to a loss for the Dow Average of -13.43% from the February top. My trailing one-year return exploded to 43.77%. My ten-year average annualized profit returned to +34.14%.

This week, Q1 earnings reports continue, and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 11 at 10:00 AM, the April US Inflation Expectations are out. Caesar’s Entertainment (CZR) and Marriot International (MAR) report earnings.

On Tuesday, May 12 at 5:00 PM, the NFIB Small Business Optimism Index for April is released. Toyota Motors (TM) reports earnings.

On Wednesday, May 13 at 9:30 AM, the ever fascinating weekly Cushing Crude Oil Stocks is announced. Cisco Systems (CSCO) reports earnings.

On Thursday, May 14 at 8:30 AM, we get another blockbuster Weekly Jobless Claims. Advanced Micro Devices (AMD) reports earnings.

On Friday, May 15 at 7:30, AM the Empire State Manufacturing Index is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll continue my solo circumlocution of the 160 mile Tahoe Rim Trail every afternoon in ten-mile segments. Why solo? Do you know anyone else who wants to hike 160 miles at 10,000 feet in two weeks?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We Had a 3 Month Warning of the Pandemic and Did Nothing

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/john-hiking.png523432Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-11 09:02:132020-06-15 12:08:54The Market Outlook for the Week Ahead, or The Next Golden Age Has Already Started

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 6Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What broker do you use? The last four bond trades I couldn’t get done.

A: That is purely a function of selling into a falling market. The bond market started to collapse 2 weeks ago. We got into the very beginning of that. We put out seven trade alerts to sell bonds, we’re out of five of them now. And whenever you hit the market with a sell, everyone just automatically drops their bids among the market makers. It’s hard to get an accurate, executable price when a market is falling that fast. The important point is that you were given the right asset class with a ticker symbol and the right direction and that is golden. People who have been with my service for a long time learn how to work around these trade alerts.

Q: Is there any specific catalyst apart from the second wave that will trigger the expected selloff?

A: First of all, if corona deaths go from 2 to 3, 4, 5 thousand a day, that could take us back down to the lows. Also, the market is currently expecting a V-shaped recovery in the economy which is not going to happen. The best we can get is a U-shape and the worst is an L-shape, which is no recovery at all. What if everything opens up and no customers show? This is almost certain to happen in the beginning.

Q: How long will the depression last?

A: Initially, I thought we could get out of this in 3-6 months. As more data comes in and the damage to the economy becomes known, I would say more like 6-9, or even 9-12 months.

Q: In natural gas, the (UNG) chart looks like a bullish breakout. Does it seem like a good trade?

A: No, the energy disaster is far from over. We still have a massive supply/demand gap. And with (UNG), you want to be especially careful because there is an enormous contango—up to 50 or 100% a year—between the spot price and the one-year contract price, which (UNG) owns. Once I saw the spot price of natural gas rise by 40% and the (UNG) fell by 40%. So, you could have a chart on the (UNG) which looks bullish, but the actual spot prices in front month could be bearish. That's almost certainly what’s going to happen. In fact, a lot of people are predicting negative prices again on the June oil contract futures expiration, which comes in a couple of weeks.

Q: What about LEAPS on United (UAL) and Delta (DAL)?

A: I am withdrawing all of my recommendations for LEAPS on the airlines. When Warren Buffet sells a sector for an enormous loss, I'm not inclined to argue with him. It’s really hard to visualize the airlines coming out of this without a complete government takeover and wipeout of all existing equity investors. Airlines have only enough cash to survive, at best, 6-8 months of zero sales, and when they do start up, they will have more virus-related costs, so I would just rather invest in tech stocks. If you’re in, I would get out even if it means taking a loss. They don’t call him the Oracle of Omaha for nothing.

Q: Any reason not to do bullish LEAPS on a selloff?

A: None at all, that is the best thing you can do. And I’m not doing LEAPS right now, I’m putting out lists of LEAPS to buy on a selloff, but I wouldn't be buying any right now. You’d be much better off waiting. Firstly, you get a longer expiration, and secondly, you get a much better price if you could buy a LEAP on a 2,000 or 3,000 point selloff in the Dow Average (INDU).

Q: Would you add the 2X ProShares Ultra Short S&P 500 (SDS) position here if you did not get on the original alert?

A: I would, I would just do a single 10% weighting. But don’t expect too much out of it, maybe you'll get a couple of points. And it’s also a good hedge for any longs you have.

Q: What happens if the second wave in the epidemic is smaller?

A: Second waves are always bigger because they’re starting off with a much larger base. There isn't a scientist out there expecting a smaller second wave than the first one. So, I wouldn't be making any investment bets on that.

Q: Pfizer (P) and others seem close to having a vaccine, moving on to human trials. Does that play into your view?

A: No, because no one has a vaccine that works yet. They may be getting tons of P.R. from the administration about potential vaccines, but the actual fact is that these are much more difficult to develop than most people understand. They have been trying to find an AIDS vaccine for 40 years and a cancer vaccine for 100 years. And it takes a year of testing just to see if they work at all. A bad vaccine could kill off a sizeable chunk of the US population. We’ve been taking flu shots for 30 years and they haven’t eliminated the flu because it keeps evolving, and it looks like coronavirus may be one of those. You may get better antivirals for treatment once you get the disease, but a vaccine is a good time off, if ever.

Q: Is this a good time to buy Boeing (BA)?

A: No, it’s too risky. The administration keeps pushing off the approval date for the 737 MAX because the planes are made in a blue state, Washington. The main customers of (BA), the airlines, are all going broke. I would imagine that their 1,000-plane order book has shrunk considerably. Go buy more tech instead, or a hotel or a home builder if you really want to roll the dice.

Q: How can the market actually drop to the lows, taking massive support from the Fed and further injections into account?

A: I don’t think we will get to new lows, I think we may test the lows. And my argument has been that we give half of the recent gains, which would take us down to 21,000 in the Dow and 2400 in the (SPX). But I've been waiting for a month for that to happen and it's not happening, which is why I've also developed my sideways scenario. That said, a lot of single stocks will go to new all-time lows, such as in retailers (RTF) and airlines (JETS).

Q: Would you stay in a Twitter (TWTR) LEAP?

A: If you have a profit, I would take it.

Q: What about Walt Disney (DIS)?

A: There are so many things wrong with Disney right now. Even though it's a great company for the long term, I'm waiting for more of a selloff, at least another $10. It’s actually rallying today on the earnings report. Around the low $90s I would really love to get into LEAPS on this. I think more bad news has to hit the stock for it to get lower.

Q: Are you continuing to play the (TLT)?

A: Absolutely yes, however, we’re at a level now where I want to take a break, let the market digest its recent fall, see if we can get any kind of a rally to sell into. I’ll sell into the next five-point rally.

Q: Any reason not to do calls outright versus spreads on LEAPS?

A: With LEAPS, because you are long and short, you could take a much larger position and therefore get a much bigger profit on a rise in the stock. Outright calls right now are some of the most expensive they’ve ever been. So, you really need to get something like a $10 or $15 rise in the stock just to break even on the premium that you’re paying. Calls are only good if you expect a very immediate short term move up in the stop in a matter of days. LEAPS you can run for two years.

Q: Is gold (GLD) still a buy?

A: Yes, the fundamental argument for gold is stronger than ever. However, it has been tracking one for one with the stock market lately. That's why I'm staying out of gold—I’d rather wait for a selloff in stocks to take gold down; then I’ll be in there as a buyer.

Q: Should I take profits on what I bought in April and reestablish on a correction?

A: Absolutely. If you have monster profits on a lot of these tech LEAPS you bought in the March/early April lows, then yes, I would take them. I think you will get another shot to buy these cheaper, and by coming out now and coming in later, you get to extend your maturity, which is always good in the LEAPS world.

Q: Would you buy casinos, or is it the same risk as the airlines?

A: I would buy casinos and hotels—they have a greater probability of survival than the airlines and a lot less debt, although they’re going to be losing money for years. I don’t know exactly how the casinos plan on getting out of this.

Q: Should we exit ProShares ultra short 20+ year Treasury Bond Fund (TBT) now?

A: No, that’s more of a longer-term trade. I would hang on to that—you could get from $16 to $20 or $25 in the foreseeable future if our down move in bond continues.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/john-guadalcanal.png354541Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-08 09:02:462020-06-08 12:15:20May 6 Biweekly Strategy Webinar Q&A

The most significant market development so far in 2020 has not been the epic stock market crash and rebound, the nonstop rally in tech stocks (NASDQ), the rebound of gold (GLD), or negative oil prices, although that is quite a list.

It has been the recent peaking of the bond market (TLT), which a few weeks ago was probing all-time highs.

I love it when my short, medium, and long-term calls play out according to script. I absolutely hate it when they happen so fast that I and my readers are unable to get in at decent prices.

That is what has happened with my short call for the (TLT), which has been performing a near-perfect swan dive since April. The move has been enough to boost me back into positive numbers for 2020.

The yield on the ten-year Treasury bond has soared from 3.25% in 2018 to an intraday low of 0.31% in March.

Lucky borrowers who demanded rate locks in real estate financings at the end of January are now thanking their lucky stars. We may be saying goodbye to the 3% handle on 5/1 ARMS for the rest of our lives.

The technical damage has been near-fatal. The writing is on the wall. A 1.00% yield for the ten-year is now easily on the menu for 2020, if not 2.00% or 3.0%.

This is crucially important for financial markets, as interest rates are the well spring from which all other market trends arise.

Wiser thinkers are peeved that the promised bleeding of federal tax revenues is causing the annual budget deficit to balloon from a low of a $450 billion annual rate in 2016 to $1.2 trillion last year and over $5 trillion in 2020.

Add in the bond purchases from the Fed’s new promise of $8 trillion in quantitative easing and you get true government borrowing of $13 trillion for 2020. It will all end in tears for bond and US dollar holders.

And don’t forget the president, who recently threatened to default on US Treasury bonds, just as the Treasury was trying to float $3 trillion in new issues. It is a short seller’s dream come true.

As rates rise, so does the debt service costs of the world’s largest borrower, the US government. The burden will soar in a hockey stick-like manner, currently at 4% of the total budget.

What is of far greater concern is what the tax bill does to the National Debt, taking it from $24 trillion to $32 trillion over the next year, a staggering rise of 50%. Even Tojo and Hitler couldn’t get the US to buy that much. If we get the higher figure, then we are looking not at another recession, but at yet another 1930-style depression.

Better teach your kids to drive for UBER early, as they are the ones who are going to have to pay off this gargantuan debt. That is if (UBER) is still around.

So what the heck are you supposed to do now? Keep selling those bond rallies, even the little ones. It will be the closest thing to a rich uncle you will ever have, if you don’t already have one.

Make your year now because the longer you put it off, the harder it will be to get.

https://www.madhedgefundtrader.com/wp-content/uploads/2011/12/FatLady2-2.jpg248400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-06 08:02:402020-05-06 08:39:55Now the Fat Lady is REALLY Singing for the Bond Market

It was only a year ago that I was driving around New Zealand with my kids, admiring the bucolic mountainous scenery, with Herb Albert and the Tijuana brass blasting out over the radio. Believe me, the tunes are not the first choice of a 15-year-old.

Today, it is all a distant memory, with any kind of international travel now unthinkable. For me, that is like a jail sentence. It is all a reminder of how well we had it before and how bleak is the immediate future.

Stock traders have certainly been put through a meat grinder. The best and worst months in market history were packed back to back, down 39% and then up 37%. At the March 23 low, the Dow average had fallen by 11,400 in a mere six weeks. Those who lived through the 1929 crash have lost their bragging rights, if there are any left.

However, like my college professor used to say, “Statistics are like a bikini bathing suit. What they reveal is fascinating, but what they conceal is essential.”

Most of the index gains were achieved by just five FANG stocks. Virtually all of the gains were from “stay at home” companies taking in windfalls from cutting-edge online business models. The “recovery” had a good week, and that was about it.

The other obvious development is that if any business was in trouble before the health crisis, you can safely write them off now. That includes retailers like Sears (S), JC Penny’s (JCP), Macy’s (M), almost all brick-and-mortar clothing sellers, and the small and medium-sized energy industry.

The worst economic data points since the black plague are about to hit the tape. Some 30 million in newly unemployed is nothing to dismiss, and that number grows to 40 million if you include discouraged workers.

That is 25% of the workforce, the same as peak joblessness during the great depression. But $14 trillion in QE and fiscal stimulus is about to hit the market too.

Which brings us to the urgent question of the day: What to do now?

It’s a vexing issue because this is not your father’s stock market. This is not even the market we’d grown used to only six months ago. All I can say is that the virology course I took 50 years ago today is worth its weight in gold.

I think you would be mad not to count a second Covid-19 wave into your calculations. This could occur in weeks, or in months, after the summer respite. This makes a second run at the lows a sure thing. I don’t think we’ll make it, but a loss of half the recent gains is entirely possible.

That takes us back down to a Dow Average of 21,000, or an S&P 500 (SPX) of 2,400.

If you are a long term investor looking to rebuild your retirement nest egg, there are only two sectors left in the market, Tech and Biotech & Healthcare. Looking at anything else is both risky and speculative. So, if we do get another meltdown, these are the only areas you should target.

If I am wrong, the market will probably bounce along sideways in a narrow range for months. That is a dream scenario if you pursue a vertical bull and bear call and put option spread strategy that I have been offering up to followers for the past decade.

Pending Home Sales Were Down a Staggering 20.8% in March and off 16.3% YOY. The worst is yet to come. The West, the first into shelter-in-place, was down a monster 26.8%. Prices still aren’t moving because nobody can buy or sell. The way homebuilder stocks like (LEN) and (KBH) are trading, I’d say your home will be worth a lot more in a year when the huge demographic push resumes. I’m not selling.

The 60,000 peak in deaths proposed by the administration only weeks ago is now looking wildly optimistic. Their worst-case scenario of 200,000 deaths, the announcement of which set the March 23 bottom of the Dow Average at 18,200, is now likely.

It will take place when the epidemic peaks in the southern and midwestern states that never sheltered in place or went in late and are coming out early. That second wave may well create a second bottom in stock prices, and that is the one you jump into and buy with both hands.

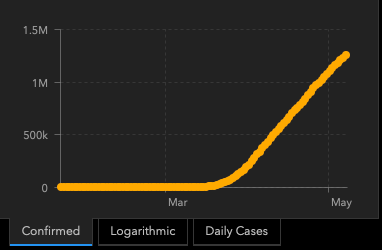

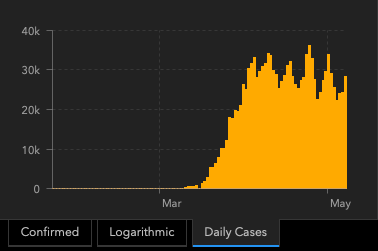

US Corona Deaths topped 66,000 last week, more than we lost after a decade of the Vietnam War. Total cases exceed one million.

Bank of America sees negative 30% GDP this quarter annualized, so says CEO Brian Moynihan. His economists expect negative 9% in Q3 and plus 30% in Q4. Suffice it to say, this is the ultra-optimistic case. Q4 doesn’t include the millions of businesses that will disappear because the Paycheck Protection Plan is failing so badly. Most government aid will take three to six months to hit the economy.

US GDP crashed 4.8% in Q1, the worst quarter since the depths of the 2008 Great Recession. Q2 will be far worse. We are now officially in recession, which should last 3-4 quarters. But is it already in the price? Next week’s April Nonfarm Payroll report should be a real humdinger.

Ford (F) lost $5 billion in Q2, and there is no guidance about the future. Avoid (F) on pain of death. Late to electric, they may not make it this time. They’re still in the buggy whip business.

Weekly Jobless Claims topped 3.8 million, bringing the six-week total to a staggering 30 million, more than those lost at the peak of the Great Depression. Florida, California, and Georgia led with applications. This implies a U-6 Unemployment rate of 25% with next week’s April Nonfarm Payroll Report. And the Dow Average is up 37% since March 23?

The Bond Market crashed on a Trump threat to default on US Treasury bonds, of which China owns $900 billion. It’s Trump’s retaliation for the Middle Kingdom spawning the Coronavirus, which he calls the “Chinese virus.” The (TLT) dropped three points on the news. Good thing I am triple short a market that is about to get crushed by massive government borrowing.

A glut of imported autos is parked at sea, steaming in circles, awaiting a recovery in the US economy. They are no doubt finding company with imported oil tankers. So many unwanted cars coming in the land-based storage areas were overflowing. It’s tough to see (F) and (GM) recovering from this. Keep buying made in the USA (TSLA) on dips, which is headed to $2,500 a share.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years, up a blistering +8.05%. We are now only 6.67% short of a new all-time high. The 100 new subscribers who came in the previous week are sitting pretty and must think I’m some sort of guru.

My aggressive triple weighting in short bond positions came in big time when Trump threatened to default on US debt. My shorts in the S&P 500 (SPY) helped. I took profits on my last long there the previous week. (SDS), another short play, clawed back some losses.

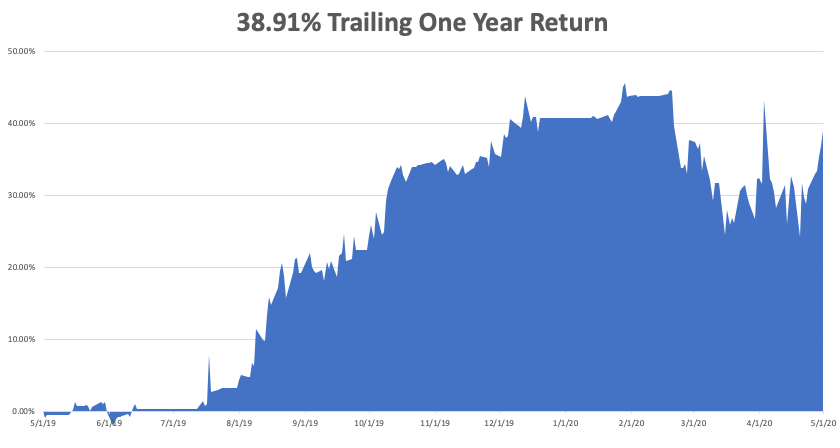

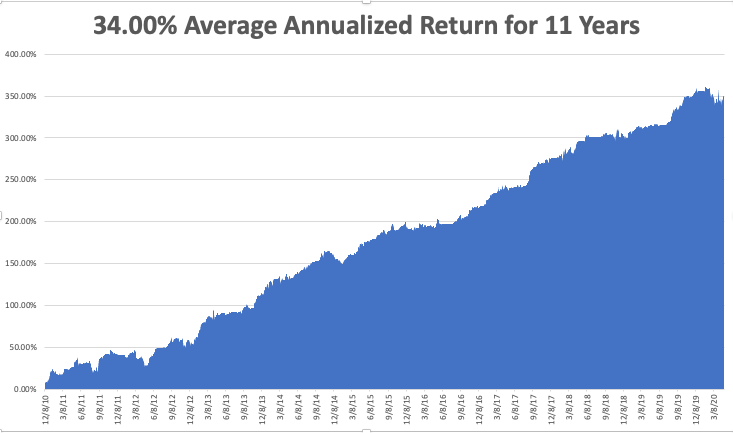

We closed out up a blockbuster +4.55% in April and May is up +2.11%, taking my 2020 YTD return up to only -1.75%. That compares to a loss for the Dow Average of -18.20% from the February top. My trailing one-year return returned to 38.91%. My ten-year average annualized profit returned to +34.00%.

This week, Q1 earnings reports continue and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 4 at 9:00 AM, the US Factories Orders for March are out and are expected to be disastrous. Berkshire Hathaway (BRK/B) and Eli Lilly (LLY) report.

On Tuesday, May 5 at 11:00 AM, the US Crude Oil Stocks are published and will be another bomb. Netflix (NFLX) and Coca-Cola (KO) report.

On Wednesday, May 6, at 7:15 AM, API Private Sector Employment Report is released. Lan Research (LRCX) and Electronic Arts (EA) announce earnings.

On Thursday, May 7 at 8:30 AM, another horrible Weekly Jobless Claims are out. Bristol Myers Squibb (BMY) reports.

On Friday, May 8, the April Nonfarm Payroll Report is printed, the worst unemployment rate since the Great Depression. AbbVie (ABBV) reports.

As for me, to battle cabin fever, I am setting up a tent in my back yard and staying there tonight, just to change the scenery. The girls need one more campout to qualify for camping merit badge, an important Eagle Scout one, and this will qualify.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/john-thomas.png665725Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-04 09:02:502020-06-08 12:27:48The Market Outlook for the Week Ahead, or The Next Bottom is the One You Buy

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-03-06 07:04:122020-03-06 07:23:08March 6, 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.