Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 4Global Strategy Webinar broadcast from Silicon Valley with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: If Trump figures out the trade war will lose him the election; will he stop it?

A: Yes, and that is a risk that hovers over all short positions in the market at all times these days because stocks will soar (INDU) when the trade war ends. We now have 18 months of share appreciation that has been frustrated or deferred by the dispute with China. The problem is that the US economy is already sliding into recession and it may already be too late to turn it around.

Q: Do you see the British pound (FXB) dropping more on the Brexit turmoil? Do you think the UK will stay in the EU?

A: If the UK ends Brexit through an election, then the pound should recover from $1.19 all the way back up to $1.65 where it was before Brexit happened four years ago. If that does happen, it will be one of the biggest trades of the year anywhere in the world, going long the British pound. This is how I always anticipated it would end. I was in England for the Brexit vote and I was convinced that if they held the election the next day, it would have lost. The only reason it won was because nobody thought it would— a lot like our own 2016 election. That brings Britain back into the EEC, saves Europe, and has a positive impact on markets globally. So, this is a big deal. Not to do so would be economic suicide for Britain, and I think wiser heads will prevail.

Q: Do you think it’s a good idea for Saudi ARAMCO to go public in Japan as reports suggest?

A: When the Arabs want to get out of the oil business (USO), (XLE), you want to also. That’s what the sale of ARAMCO is all about. They’re going to get a $1 trillion or more valuation, raising $100 billion in cash. And guess who the biggest investors in alternative energy in California are? It’s Saudi Arabia. They see no future in oil, nor should you. This is why we’ve been negative on the sector all year. By the way, bankruptcies by frackers in the U.S. are at an all-time high, another indicator that low oil prices can’t be tolerated by the US industry for long.

Q: Is it time to buy the ProShares Ultra Short 20 year Plus Treasury Bond Fund (TBT)?

A: No, not yet; I think we’re going to break 1.33% — the all-time low yield for the (TLT) will probably be somewhere just below 1.00%. We probably won’t go to absolute zero because we still have a growing economy. The countries that already have negative interest rates have shrinking economies or are already in recession, like Germany or Great Britain can justify zero rates.

Q: Are you going to run all your existing positions into expiration?

A: I’m going to try to—it’s only 12 days to expiration, and we get to keep the full profit if we do. As long as the market is dead in the middle here, there are no other positions to put on, no extreme low to buy into or extreme high to sell into. It’s a question of letting this sort of nowhere-trend play out, but also there's nothing else to buy, so there is no need to raise cash. So, we’re 60% invested now and we’re going to try running as many of those into expiration as we can. Looks like all the long technology positions are safe (FB), (AMZN), (MSFT), (DIS). The only thing we’re pressing here are the shorts in Walmart (WMT) and Russell 2000 (IWM).

Q: Do you think it’s a good idea for Tesla (TSLA) to build another Gigafactory in Shanghai, China during a trade war? Will this blow up in Elon’s face?

A: I don’t think so because the Chinese are desperate for the Tesla technology and they just gave Tesla an exemption on import duties on all parts that need to go there to build the cars. So, that’s a very positive development for Tesla and I believe the stock is up about $10 since that news came out.

Q: Will Roku (ROKU) ever pull back? Would you buy it up here?

A: No, we recommended this thing last year at $40; it’s now up to $165, and up here it’s just wildly overbought, in chase territory. Of course, the reason that’s happening is that the big concern last year was Amazon wiping out Roku, yet they ultimately ended up partnering with Roku, and that’s worth about a 400% gain in the stock. You know the second you get into this, it’s over. There are just too many better fish to fry in the technology area.

Q: What happens if our existing Russell 2000 (IWM) September 2019 $153-$156 in-the-money vertical BEAR PUT spread Russell 2000 position closes between $156 and $153?

A: You lose money. You will get the Russell 2000 shares put to you, or sold to you at $153.00, which means you now own them, and you’ll get a big margin call from your broker for owning the extra shares. If ever it looks like we’re getting close to the strike price going into expiration, I come out precisely because of that risk. You don’t want random chance dictating whether you’re going to make money in your position or not going into expiration. If you’re worried about that, I would get out now and you can still come out with a nice profit. Or, you can always wait for another down day tomorrow.

Q: Is it time to get super aggressive shorting Lyft (LYFT) or Uber (UBER) when they openly admit that they won’t make a profit anytime in the near future?

A: The time to short Uber (UBER) and Lyft was at the IPO when the shares became available to sell. Down here I don’t really want to do very much. It’s late in the game and Uber’s down about one third from its IPO price. We begged people to stay away from this. It’s another example where they waited for the company to go ex-growth before it went public, but it didn’t leave anything for the public. It was a very badly mishandled IPO—it’s now at $31 against a $45 IPO price and was at a new all-time low just 2 days ago. You knew when they offered the drivers shares, the thing was in trouble. Sometime this will be a buy, but not yet. Go take a long nap first.

Q: Is the fact that rich people are hoarding cash a good indicator that a recession is approaching?

A: Yes, absolutely. Bonds yielding 1.45% is also an indication that the wealthy are hoarding cash from other investment and parking it in US treasury bonds. I went to the Pebble Beach Concourse d’ Elegance vintage car show a few weeks ago and all of the $10 million plus cars didn’t sell, only those priced below $100,000. That is always a good indicator that the wealthy are bailing ahead of a recession. If you can’t get a premium price for your vintage Ferrari, trouble is coming.

Q: Argentina just implemented currency controls; is this the start of a rolling currency crisis among emerging nations?

A: No, I believe the problems are unique to Argentina. They’ve adopted what is known as Modern Momentary Theory—i.e. borrowing and printing money like crazy. Unfortunately, this is unsustainable and results in a devalued currency, general instability, and the eventual hanging of their leaders from the nearest lamppost. This is exactly the same monetary policy that the Trump administration has been pursuing since he came into office. Eventually, it will lead to tears, ours, not his.

Q: Is the new all-electric Porsche Taycan a threat to Tesla?

A: No, it’s not. Their cheapest car is $150,000 and it gets one third less range than Tesla does. It’s really aimed at Porsche fanatics, and I doubt they will get outside their core market. In the meantime, Tesla has taken over the middle part of the electric market with the Model 3 at $37,000 a car. That’s where the money is, and Porsche will never get there.

Q: How will the US pull out of recession if the interest rates are at or below zero?

A: It won’t—that’s what a lot of economists are concerned about these days. With interest rates below zero, the Fed has lost its primary means to stimulate the economy. The only thing left to do is use creative means like feeding the economy with currency, which Europe has been doing for 10 years, and Japan for 30, with no results. That’s another reason to not allow rates to get back to zero—so we have tools to use when we go into a recession 12-24 months from now.

Q: What’s the best way to buy silver?

A: The ETF iShares Silver Trust (SLV) and, if you want to be aggressive, the silver miners with the Global X Silver Miners ETF (SIL).

Q: Have global central banks ruined the western economic system as we know it for future generations?

A: They may have—mostly by printing too much money in the last 10 years in order to get us out of recession. This hasn’t really worked for Europe or Japan, mind you, though who knows how much worse off they would be if they hadn’t. What it did do here is head off a Great Depression. If we go back to money printing in a big way, however, and it doesn’t work, we will not have prevented a Great Depression so much as pushed it back 10 or 15 years. That’s the great debate ongoing among economists, and it will eventually be settled by the marketplace.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/JT-with-snorkel-story-1-image-6-e1535059927176.jpg267350Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-06 04:02:202019-10-14 09:46:34September 4 Biweekly Strategy Webinar Q&A

Featured Trade: (ITALY’S BIG WAKE UP CALL), (TLT), ($TNX), (TBT), (SPY), ($INDU), (FXE), (UUP), (USO), (WELCOME TO THE DEFLATIONARY CENTURY), (TLT), (TBT),

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-31 10:06:422019-07-31 10:21:42July 31, 2019

Those planning a European vacation this summer just received a big gift from Mario Draghi, the outgoing president of the European Central Bank. His promise to re-accelerate quantitative easing in Europe has sent the Euro crashing and the US dollar soaring.

Over the last two weeks, the Euro (FXE) has fallen by 2.5%. That $1,000 Florence hotel suite now costs only $975. Mille Gracie!

You can blame the political instability in the Home of Caesar, which has not had a functioning government since WWII. The big fear is that the extreme left would form a collation government with the extreme right that could lead to its departure from the European Community and the Euro. Think of it as Bernie Sanders joining Donald Trump!

In fact, Italy has had 62 different governments since WWII. They change administrations like I change luxury cars, about once a year. Welcome to European debt crisis part 27.

I can’t remember the last time markets cared about what happened in Europe. It was probably the first Greek debt crisis in 2011. As a result, German ten-year bunds have cratered from 0.60% to -0.40%. But they care today, big time.

Given the reaction of the global financial markets, you could have been forgiven for thinking that the world had just ended.

US Treasury Bond yields (TLT) saw their biggest plunge in years, off 120 basis points to 2.05%.

Even oil prices collapsed for an entirely separate set of reasons, the price of Texas Tea pared 20% since April on spreading global recession fears.

Saudi Arabia looks like it's about to abandon the wildly successful OPEC production quotas that have been boosting oil prices for the past year. Iran has withdrawn from the nuclear non-proliferation treaty, responding with an undeclared tanker war in the Persian Gulf, which I flew over myself only a few weeks ago. The geopolitical premium is back with a vengeance.

So if the Italian developments are a canard, why are we REALLY going down?

You’re not going to like the answer.

It turns out that rising inflation, interest rates, oil and commodity prices, the US dollar, US national debt, budget deficits, and stagnant wage growth are a TERRIBLE backdrop for risk in general and stocks specifically. And this is all happening with the major indexes at the top end of recent ranges.

In other words, it was an accident waiting to happen.

Traders are extremely nervous, global uncertainty is high, the seasonals are awful, and Washington is a ticking time bomb. If you were wondering why I was issuing so few Trade Alerts in July, these are the reasons.

This all confirms my expectation that markets could remain stuck in increasingly narrow trading ranges for the next six months until the presidential election begins in earnest.

Which is creating opportunities.

The global race towards zero interest has the US as the principal laggard. So you should keep buying every serious dip in the bond market.

Stocks are still wildly overvalued for the short term, so I’ll keep my low profile there. As for gold (GLD) and the currencies, I keep buying dips there as well.

So watch for those coming Trade Alerts. I’m not dead yet, just resting. The contest here is to make as much money as you can, not to see how many trades you can clock. That is a brokers' game, not yours.

Waiting for My Shot

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-15.png389489Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-31 10:04:572019-08-27 14:39:43Italy’s Big Wake Up Call

For many, one of the most surprising impacts of the administration’s tariffs on Chinese imports announced today has been a rocketing bond market.

Since the December $116 low, the iShares 20+ Year Treasury Bond ETF (TLT) has jumped by a staggering $16 points, the largest move up so far in years.

The tariffs are a highly regressive tax that will hit consumers hard in the pocketbook, thus reducing their purchasing power.

It will dramatically slow US economic growth. If the trade war escalates, and it almost certainly will, it could shrink US GDP by as much as 1% a year. A weaker economy means less demand for money, lower interest rates, and higher bond prices.

There is no political view here. This is just basic economics.

And while there has been a lot of hand-wringing over the prospect of China dumping its $1.1 trillion in American bond holdings, it is unlikely to take action here.

The Beijing government isn’t going to do anything to damage the value of its own investments. The only time it actually does sell US bonds is to support its own currency, the renminbi, in the foreign exchange markets.

What it CAN do is to boycott new Treasury bond purchases, which it already has been doing for the past year.

The tariffs also raise a lot of uncertainty about the future of business in the United States. Companies are definitely not going to increase capital spending if they believe a depression is coming, which the last serious trade war during the 1930s greatly exacerbated.

While stocks despise uncertainty, bonds absolutely love it.

Those of you who are short the bond market through the ProShares Ultra Short 20+ Year Treasury ETF (TBT) have a particular problem that is often ignored.

The cost of carry of this fund is now more than 5% (two times the 2.10% coupon plus management fees and expenses). Thus, long-term holders have to see interest rates rise by more than 5% a year just to break even. The (TBT) can be a great trade, but a money-losing investment.

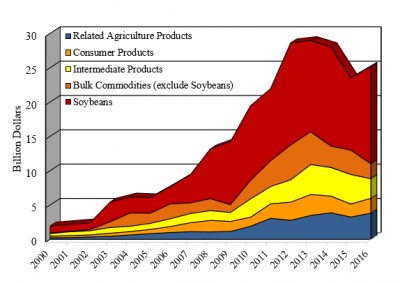

The Chinese, which have been studying the American economic and political systems very carefully for decades, will be particularly clever in its retaliation. And you thought all those Chinese tourists were over here just to buy our Levi’s?

It will target Republican districts with a laser focus, and those in particular who supported Donald Trump. It wants to make its measures especially hurt for those who started this trade war in the first place.

First on the chopping block: soybeans, which are almost entirely produced in red states. In 2016, the last full year for which data is available, the US sold $15 billion worth of soybeans to China. Which are the largest soybean producing states? Iowa followed by Minnesota.

A major American export is aircraft, some $131 billion in 2017, and China is overwhelmingly the largest buyer. The Middle Kingdom needs to purchase 1,000 aircraft over the next 10 years to accommodate its burgeoning middle class. It will be easy to shift some of these orders to Europe’s Airbus Industries.

This is why the shares of Boeing (BA) have been slaughtered recently, down some 13.5% from the top. While Boeing planes are assembled in Washington state, they draw on parts suppliers in all 50 states.

Guess what the biggest selling foreign car in China is? The General Motors (GM) Buick which saw more than 400,000 in sales last year. I have to tell you that it is hilarious to see my mom’s car driven up to the Great Wall of China. Where are these cars assembled? Michigan and China.

The global trading system is an intricate, finally balanced system that has taken hundreds of years to evolve. Take out one small piece, and the entire structure falls down upon your head.

This is something the administration is about to find out.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/03/China-chart-photo-2.jpg282400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-07-05 02:02:302019-08-05 17:45:34Why US Bonds Love Chinese Tariffs

Investors around the world have been confused, befuddled, and surprised by the persistent, ultra-low level of long-term interest rates in the United States.

At today’s close, the 30-year Treasury bond yielded a parsimonious 2.99%, the ten years 2.59%, and the five years only 2.40%. The ten-year was threatening its all-time low yield of 1.33% only three years ago, a return as rare as a dodo bird, last seen in the 19th century.

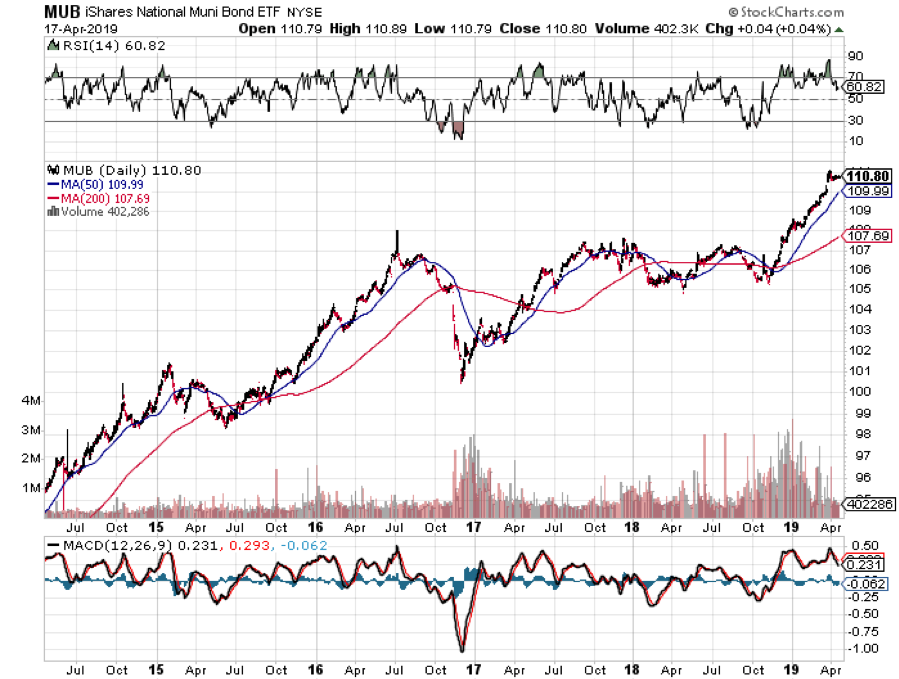

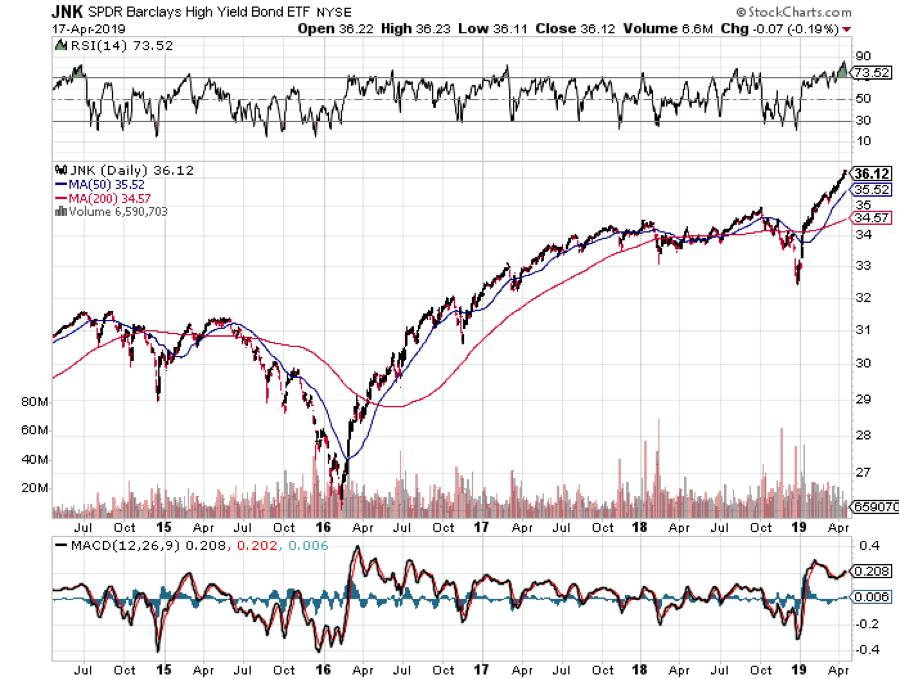

What’s more, yields across the entire fixed income spectrum have been plumbing new lows. Corporate bonds (LQD) have been fetching only 3.72%, tax-free municipal bonds (MUB) 2.19%, and junk (JNK) a pittance at 5.57%.

Spreads over Treasuries are approaching new all-time lows. The spread for junk over of ten-year Treasuries is now below an amazing 3.00%, a heady number not seen since the 2007 bubble top. “Covenant light” in borrower terms is making a big comeback.

Are investors being rewarded for taking on the debt of companies that are on the edge of bankruptcy, a tiny 3.3% premium? Or that the State of Illinois at 3.1%? I think not.

It is a global trend.

German bunds are now paying holders 0.05%, and JGBs are at an eye-popping -0.05%. The worst quality southern European paper has delivered the biggest rallies this year.

Yikes!

These numbers indicate that there is a massive global capital glut. There is too much money chasing too few low-risk investments everywhere. Has the world suddenly become risk averse? Is inflation gone forever? Will deflation become a permanent aspect of our investing lives? Does the reach for yield know no bounds?

It wasn’t supposed to be like this.

Almost to a man, hedge fund managers everywhere were unloading debt instruments last year when ten-year yields peaked at 3.25%. They were looking for a year of rising interest rates (TLT), accelerating stock prices (QQQ), falling commodities (DBA), and dying emerging markets (EEM). Surging capital inflows were supposed to prompt the dollar (UUP) to take off like a rocket.

It all ended up being almost a perfect mirror image portfolio of what actually transpired since then. As a result, almost all mutual funds were down in 2018. Many hedge fund managers are tearing their hair out, suffering their worst year in recent memory.

What is wrong with this picture?

Interest rates like these are hinting that the global economy is about to endure a serious nosedive, possibly even re-entering recession territory….or it isn’t.

To understand why not, we have to delve into deep structural issues which are changing the nature of the debt markets beyond all recognition. This is not your father’s bond market.

I’ll start with what I call the “1% effect.”

Rich people are different than you and I. Once they finally make their billions, they quickly evolve from being risk takers into wealth preservers. They don’t invest in start-ups, take fliers on stock tips, invest in the flavor of the day, or create jobs. In fact, many abandon shares completely, retreating to the safety of coupon clipping.

The problem for the rest of us is that this capital stagnates. It goes into the bond market where it stays forever. These people never sell, thus avoiding capital gains taxes and capturing a future step up in the cost basis whenever a spouse dies. Only the interest payments are taxable, and that at a lowly 2.59% rate.

This is the lesson I learned from servicing generations of Rothschilds, Du Ponts, Rockefellers, and Gettys. Extremely wealthy families stay that way by becoming extremely conservative investors. Those that don’t, you’ve never heard of because they all eventually went broke.

This didn’t use to mean much before 1980, back when the wealthy only owned less than 10% of the bond market, except to financial historians and private wealth specialists, of which I am one. Now they own a whopping 25%, and their behavior affects everyone.

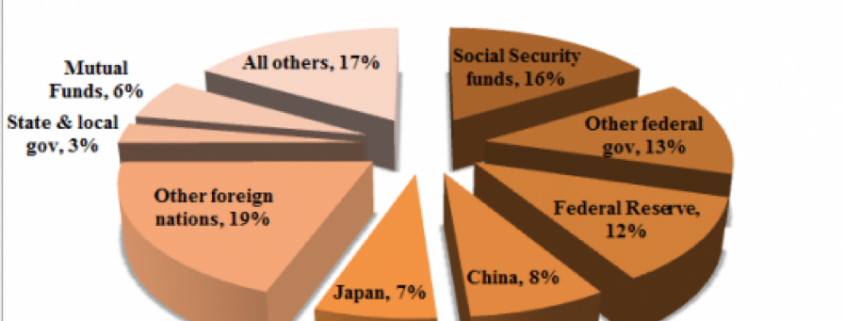

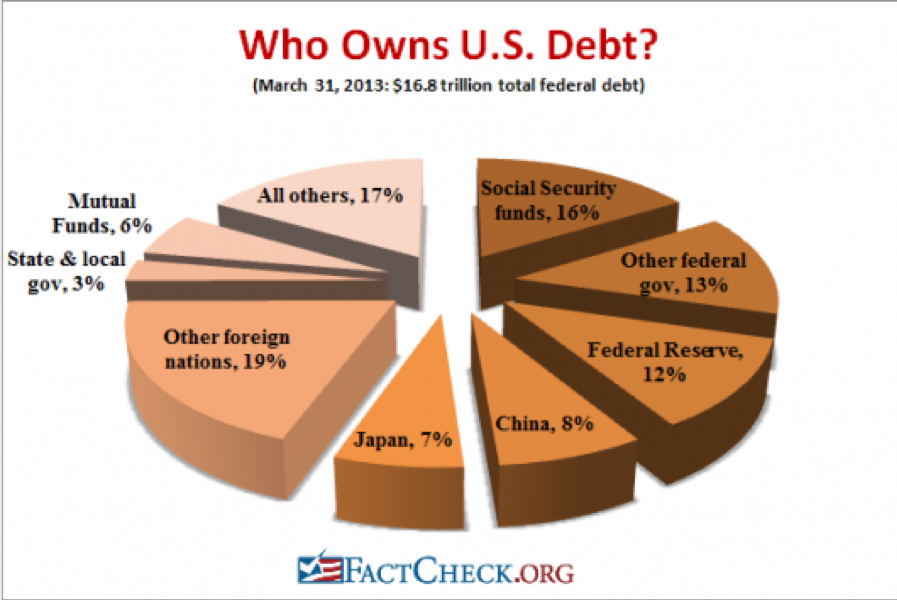

Who has been the largest buyer of Treasury bonds for the last 30 years? Foreign central banks and other governmental entities which count them among their country’s foreign exchange reserves. They own 36% of our national debt with China in the lead at 8% (the Bush tax cut that was borrowed), and Japan close behind with 7% (the Reagan tax cut that was borrowed). These days they purchase about 50% of every Treasury auction.

They never sell either, unless there is some kind of foreign exchange or balance of payments crisis which is rare. If anything, these holdings are still growing.

Who else has been soaking up bonds, deaf to repeated cries that prices are about to plunge? The Federal Reserve which, thanks to QE1, 2, 3, and 4, now owns 13.63% of our $22 trillion debt.

An assortment of other government entities possesses a further 29% of US government bonds, first and foremost the Social Security Administration with a 16% holding. And they ain’t selling either, baby.

So what you have here is the overwhelming majority of Treasury bond owners with no intention to sell. Ever. Only hedge funds have been selling this year, and they have already done so, in spades.

Which sets up a frightening possibility for them, now that we have broken through the bottom of the past year’s trading range in yields. What happens if bond yields fall further? It will set off the mother of all short-covering squeezes and could take ten-year yield down to match 2012, 1.33% low, or lower.

Fasten your seat belts, batten the hatches, and down the Dramamine!

There are a few other reasons why rates will stay at subterranean levels for some time. If hyper accelerating technology keeps cutting costs for the rest of the century, deflation basically never goes away (click here for “Peeking Into the Future With Ray Kurzweil” ).

Hyper accelerating corporate profits will also create a global cash glut, further levitating bond prices. Companies are becoming so profitable they are throwing off more cash than they can reasonably use or pay out.

This is why these gigantic corporate cash hoards are piling up in Europe in tax-free jurisdictions, now over $2 trillion. Is the US heading for Japanese style yields, of zero for 10-year Treasuries?

If so, bonds are a steal here at 2.59%. If we really do enter a period of long term -2% a year deflation, that means the purchasing power of a dollar increases by 35% every decade in real terms.

The threat of a second Cold War is keeping the flight to safety bid alive, and keeping the bull market for bonds percolating. You can count on that if the current president wins a second term.

Why Are They So Low?

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/US-debt-owners.png600897Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-24 02:07:262019-04-24 01:29:21Why Are Bond Yields So Low?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.