Mad Hedge Biotech and Healthcare Letter

March 13, 2025

Fiat Lux

Featured Trade:

(THE 10,000 DAILY CONSULTATIONS YOU'LL NEVER SEE)

(HIMS), (TDOC), (GDRX), (NVO), (LLY)

Mad Hedge Biotech and Healthcare Letter

March 13, 2025

Fiat Lux

Featured Trade:

(THE 10,000 DAILY CONSULTATIONS YOU'LL NEVER SEE)

(HIMS), (TDOC), (GDRX), (NVO), (LLY)

Did you know that 100 years ago, the average American lifespan was just 54 years? Today, we're approaching 80.

But what's truly remarkable isn't just that we're living longer—it's that a 36-year-old former Tinder executive named Andrew Dudum is revolutionizing how we access healthcare.

His company, Hims & Hers (HIMS), has exploded from a niche men's health startup into a $1.5 billion healthcare powerhouse in just a few years.

What exactly does HIMS do?

HIMS is transforming healthcare with a tech-first approach. They began by solving embarrassing men's health problems like ED and hair loss through an online platform, but have since built a vertically integrated healthcare powerhouse.

Now they handle everything from virtual doctor's visits and AI-powered diagnostics to personalized medication compounding and doorstep delivery.

All without the patient ever leaving their couch or explaining their problems to three different receptionists. It's healthcare reimagined for the digital age—and patients are flocking to it.

The numbers don't lie. By the end of 2024, they hit 10,000 patient visits per day - that's more than some mid-sized hospitals.

Their subscriber base swelled to 2.2 million, up 45% year-over-year. Even more impressive is that 55% of those subscribers are using at least one personalized solution, not just generic treatments.

What makes HIMS so disruptive is their mastery of the tech playbook that Wall Street has been drooling over for years. They're capturing data at every patient touchpoint and have built one of healthcare's largest proprietary datasets.

My sources tell me they've got over 500,000 square feet of compounding pharmacies and fulfillment centers spread across Ohio, Arizona, and California. These aren't your father's drugstores.

Unlike Teladoc (TDOC) and GoodRx (GDRX), who dabble in AI for basic tasks, HIMS goes much deeper.

They're personalizing treatments, fine-tuning dosages, improving adherence, and creating custom supplement plans. Their AI chatbots handle everything from prescription refills to progress tracking.

I met a guy last week who manages a tech fund in Boston who put it best: "Each new subscriber makes their entire system smarter." That's a competitive moat that gets wider by the day.

Revenue has followed this growth trajectory like a heat-seeking missile. In 2024, the company raked in $1.5 billion, a staggering 69% increase year-over-year. Their Q4 revenue hit $481 million, nearly doubling with a 95% year-over-year increase.

But here's where it gets even more interesting. Their weight loss treatments have been absolute rocket fuel for growth.

Their oral-based offering reached a $100 million revenue run rate within just seven months of launch. And their GLP-1 offering (launched in Q2-24) generated more than $225 million in incremental revenue during 2024 alone.

My friend Janet at the Fed would be impressed by their margins, too.

Adjusted EBITDA margins reached 12% in 2024, with adjusted EBITDA increasing by 160% year-over-year to $54 million in Q4.

They hit their first full year of GAAP profitability with net income of $126 million and strong cash flow of approximately $200 million. That's what I call a healthy business.

But here's the rub. HIMS is betting big—perhaps too big—on weight loss treatments.

They generated $225 million from GLP-1 offerings in 2024 and project $725 million in 2025. That's a massive chunk of revenue hanging on one specialty.

The FDA isn't thrilled about compounded semaglutide, which HIMS relies on. If regulators clamp down, they're in trouble.

Worse, supply is controlled by Novo Nordisk (NVO) and Eli Lilly (LLY), creating a precarious position for HIMS. If insurance coverage expands for branded GLP-1s, patients might flee HIMS' alternatives.

They're trying to pivot to oral therapies and AI coaching, but it's a high-stakes gamble. As my hedge fund buddies would say, that's a lot of eggs in one regulatory basket.

So, what about valuation? There's no getting around it—HIMS is trading at premium multiples: 3.76x forward EV/Sales versus the sector median of 3.19x, an EV/EBITDA of 29.69x compared to 12.12x, and a sky-high forward P/E of 65.96x against the sector's more modest 25.46x.

When you stack it up against competitors, the gap grows even wider. HIMS' forward P/E makes GoodRx (29.65x) seem downright affordable, and its EV/Sales ratio towers over both Teladoc (0.74x) and GoodRx (2.42x).

Is that premium justified? With revenue growth cruising at 69%, there's a case to be made—but investors should be cautious. I've watched this story unfold countless times: today's darling of Wall Street can easily turn into tomorrow's cautionary tale.

Still, for those with a strong stomach and the patience to see this through, HIMS is definitely worth a closer look. After all, we're witnessing one of the most significant transformations in healthcare in over a century.

Just think about it – In 1924, Americans relied on house calls and patent medicines. Today, personalized treatments arrive at our doorsteps after a five-minute video chat.

And the company leading this healthcare revolution? Founded by a guy who used to help people swipe right on Tinder.

From patent tonics to AI-prescribed pharmaceuticals in a century. Seems our approach to awkward health problems has evolved even faster than our lifespans.

Who knew swiping right would someday fix more than just your dating life?

Mad Hedge Biotech and Healthcare Letter

July 30, 2024

Fiat Lux

Featured Trade:

(RETAIL THERAPY, MEET RETAIL RX)

(HUM), (WMT), (WBA), (UNH), (CVS), (TDOC)

In my years of covering the markets, from the trading floors of Tokyo to the halls of power in Washington, I've seen my fair share of unexpected partnerships.

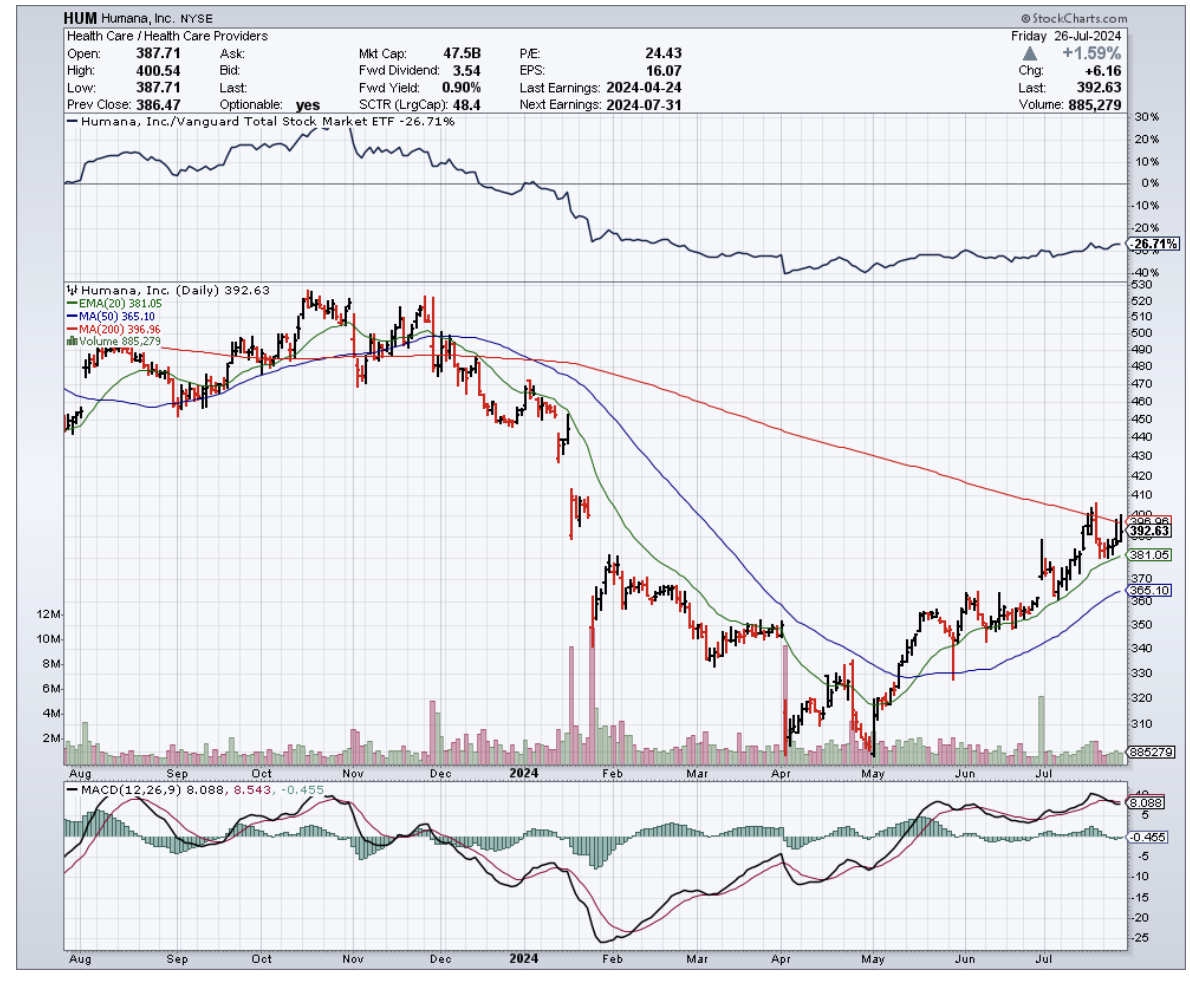

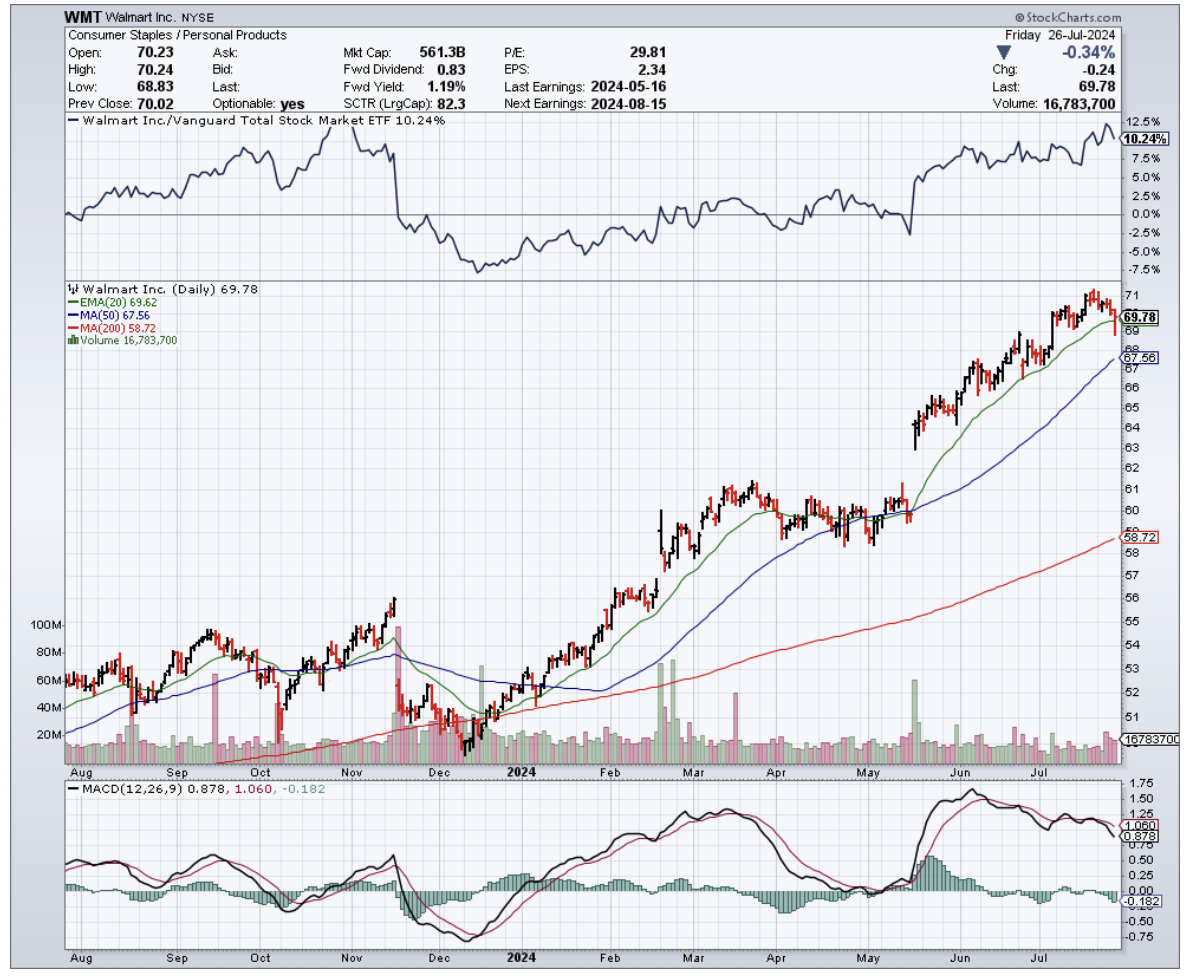

But the recent tie-up between Walmart (WMT) and Humana (HUM) has me sitting up and paying attention.

That’s right. Walmart, the king of rollbacks and home of the $1 hot dog, has found a new tenant for the vacant spaces that used to house its healthcare business: Humana's CenterWell health clinics.

Humana, as you know, is one of the biggest players in the Medicare Advantage game, and is setting up shop in 23 Walmart Supercenters across Florida, Georgia, Missouri, and Texas.

And they're not just dipping their toes in the water – they're diving in headfirst, with plans to have these clinics up and running by the first half of 2025.

Now, I know what you're thinking. "John, why should I care about some dusty old retail giant like Walmart getting into bed with a health insurance company?"

Let me tell you why.

Humana's Q1 2024 earnings were nothing to sneeze at, with revenues growing 11% year-over-year to a whopping $29.6 billion.

And while the company did revise its full-year EPS guidance downward, it maintained its outlook for adjusted EPS and even revised its membership growth in MA plans upward.

This is a big deal, folks. Medicare Advantage plans have been the bread and butter of Humana's business model, underpinning the company's phenomenal share price gains from $25 per share in 2010 to over $550 in late 2022.

With the population aging faster than fine wine, the demand for senior-focused healthcare services will only grow.

But Humana isn't the only one benefiting from this partnership.

For Walmart, renting out these spaces to CenterWell allows them to recoup some of the infrastructure investments they made in building out their 51 Walmart Health clinics, which they recently shut down due to profitability challenges.

It's like finding a roommate to help pay the rent after your startup goes belly up.

But the healthcare industry is like a giant game of Jenga, with players constantly pulling out blocks and hoping the whole thing doesn't come crashing down.

Just look at Walgreens Boots Alliance (WBA), another retail giant that recently announced the closure of 150 of its in-store clinics due to profitability challenges. It's a stark reminder of how difficult it can be to make a buck in this business.

That's why Walmart's pivot to a partnership model with Humana is so intriguing.

By leasing out pre-equipped facilities to CenterWell, Walmart is essentially letting Humana handle the nitty-gritty of patient care while still maintaining a presence in the rapidly growing primary care industry.

It's like having your cake and eating it too, without having to worry about the pesky details of actually baking the cake.

As expected, Walmart and Humana aren't the only ones making moves in the healthcare space.

CVS Health (CVS) and UnitedHealth Group (UNH) are also betting big on primary care, with CVS acquiring Oak Street Health for $10.6 billion and UnitedHealth's Optum division going on an acquisition spree to expand its network of physicians and healthcare providers.

Then, there’s the meteoric rise of telehealth during the pandemic. Companies like Teladoc Health (TDOC) saw their revenues skyrocket as patients turned to virtual care in droves.

While growth has slowed down since the height of the pandemic, telehealth is still a force to be reckoned with and could potentially disrupt traditional brick-and-mortar clinics.

So, what does all this mean for us?

Well, if you're an investor looking to get in on the action, you've got plenty of options. From established players like Humana and UnitedHealth to up-and-comers like Oak Street Health and Teladoc, there's no shortage of companies vying for a piece of the healthcare pie.

With an aging population, rising healthcare costs, and a growing focus on preventative care and chronic disease management, the demand for innovative healthcare solutions is only going to increase in the coming years.

And who knows, maybe one day we'll all be getting our annual check-ups at the local Walmart, with a side of low-priced toilet paper and a jumbo bag of Cheetos.

Stranger things have happened in the wild world of healthcare.

Mad Hedge Biotech and Healthcare Letter

July 20, 2023

Fiat Lux

Featured Trade:

(INNOVATION GENIUS OR INVESTORS’ QUAGMIRE?)

(TDOC), (MSFT)

Let's rewind to the inception of Teladoc (TDOC).

In the early 2000s, online medical appointments were as futuristic as a scene out of The Jetsons. Fast forward to today, and Teladoc's business model - a digital clinic where you see the doctor from your laptop - is as commonplace as ordering a latte from your phone.

In theory, it's a genius innovation - cut down the rigmarole of office visits, boost doctor efficiency, and slash overhead costs associated with physical appointments.

Unfortunately, the real world has been a tough nut to crack for Teladoc, with investors getting cold feet over the past few years.

Still, when the risk-averse tide returned in 2023 and investors started making a beeline for stocks that had taken a beating in 2022, Teladoc shareholders were also banking on a swift recovery from the lows.

Indeed, with a market shift towards greener pastures, the stock got a nearly 60% leg-up from its historical lows by early February. It looked like buyers were of the view that, despite some managerial slip-ups, the leader of the telehealth market seemed underpriced given its double-digit growth rates. The expectations also seemed tempered.

Then came another slap of reality with the quarterly reports.

Despite respectable Q4 figures, the outlook was nothing short of a letdown. After a 2022 slump in the telehealth market and Teladoc's 18% growth, one might have hoped for a more robust expansion within a burgeoning industry.

Instead, investors got a projection of lukewarm average increase of just 8.4%, GAAP profitability seemed like a distant dream, and even an EBITDA growth of 22% couldn't make the numbers shine.

The backlash was predictable. After Q1 numbers, the stock rallied before it stumbled again, nearing its all-time lows - even amidst a risk-on climate.

Diminishing growth, elusive profitability, mounting competition – Is this Teladoc's swan song, or can it claw back its glory?

Recent updates show that it seems like Teladoc is leaning on Microsoft (MSFT) for a lifeline.

The company declared an expanded alliance with Microsoft, aiming to harness the latter's state-of-the-art artificial intelligence (AI) technology. This uplifting news is a much-needed antidote for the digital health provider, whose recent journey had more in common with a bear market trudge than a bull run sprint.

The idea is for the telehealth company to basically plug in the Azure OpenAI Service, along with other Microsoft products, directly into its homegrown Teladoc Solo virtual care platform.

The endgame? Cut the red tape for overworked healthcare professionals by automating the grind of clinical documentation – applicable to virtual check-ups and in-person consultations.

That's not all. Teladoc is additionally introducing the "Nuance Dragon Ambient eXperience," or DAX, a sophisticated tool that effortlessly transforms patient-practitioner dialogues into comprehensive, specialty-specific clinical notes, all while sticking to the letter of documentation standards.

As expected, the stock enjoyed an initial sugar rush as investors toasted to the company's pivot towards AI.

For me, though, I have a more measured take on the announcement. While I recognize the positive thrust of the move, I can’t completely agree that this alliance is a game-changer. Let me share some of the reasons behind my reluctance.

In the first part of 2023, Teladoc reported a top-line revenue of $629 million, while carrying a net loss of $69 million. On the surface, the balance between the top and bottom lines seems skewed.

However, taking a step back, Teladoc took a considerable hit last year with a sizeable goodwill impairment charge. But spring 2023 brings a new twist, with an $8.1 million expense for restructuring.

Based on the 10-Q filing, these costs were tied to "kissing goodbye to excess leased office spaces." We might assume this is a one-off, and quite frankly, it's a move I admire for a company currently in the red.

But let’s flip the script a bit and talk about operating expenses.

While the company managed to cut back on Sales and Technology and Development, they seemed to have thrown caution to the wind, with General and Administrative costs up by 9% and Advertising and Marketing expenses skyrocketing by 32%.

I’m not talking about an occasional splurge here. The 2022 report shows a 50% annual increase in Advertising and Marketing costs. This figure is critical, as it gives us a peek into the company's customer acquisition costs. More money spent on marketing translates to longer customer retention needed to turn a profit.

To provide you with a sense, for every dollar Teladoc made in Q1 2023, 28 cents went to marketing, a noticeable bump from 24 cents per dollar in Q1 2022.

Now, Teladoc hints at some seasonality in their operations, with the first and last quarters typically reflecting weaker operating income as the pace of new customer acquisitions and revenue growth lags behind marketing expenses. But let's not let this divert our attention from the discrepancy between revenue growth and marketing costs.

As an investor, you'd obviously want to know how well the company is retaining its customers with these rising acquisition costs.

Here's the deal: Teladoc's customer churn rate isn't increasing, but it's not dropping either. As for the customer retention rates, the company’s executives describe the figures as "stable."

Notably, the company already casts a wide net, claiming that "over 80 million individuals in the U.S. have access to one or more of our products and services." If that's true, Teladoc already has its hooks in nearly a quarter of the U.S. population.

So, the million-dollar question for investors: If Teladoc can't turn a profit with this massive reach, then when will it?

In the digital healthcare universe, Teladoc once promised to be a shooting star. Yet, amidst stalled growth, daunting losses, and controversial investments, it appears more like a black hole absorbing investor optimism.

The recent alliance with Microsoft injects a ray of hope, aiming to automate and optimize operations through AI. But the questions remain: Is this the life-saving maneuver that rights Teladoc's trajectory, or just a brief flash in the pan?

As investors, we're left to wonder, in the dance of innovation and investment, will Teladoc waltz or wobble? Only time will play the music.

Mad Hedge Technology Letter

March 22, 2023

Fiat Lux

Featured Trade:

(IF BITCOIN THEN GROWTH TECH TOO)

(COIN), (MSTR), (BTC), (DOCU), (TDOC)

We are closing in on $27,000 and that’s quite the performance for the digital gold Bitcoin (BTC).

It just was last year when Bitcoin was down in the dumps.

I am not here flogging crypto but tech investors should take heed of what is happening in the riskier parts of the asset markets.

Yes, tech growth is quite volatile, but bitcoin even more so.

The price of Bitcoin is already up 72% this year and that will beat most tech growth stocks including the Teledocs and DocuSigns of the world.

This last strong surge is correlated with global banking contagion with even very liberal-based CNBC stating that Switzerland has become a financial “banana republic.”

Bitcoin is often advertised as the alternative asset class to fiat banking precisely because fiat banking has a history of going to zero.

The blowups at Silicon Valley Bank, First Republic, and Credit Suisse offer credible evidence that the strength of the fiat money banking system is trending down rather than up.

Hence the monster rally and this will just make banking more expensive for the unbanked and give the big banks more power and more “too big to fail” status.

Narratives are more powerful in crypto in generating real price movements than any other asset class and no matter what your thoughts on how powerful that narrative is, people actually believe this.

Cryptocurrency initially attracted interest from a niche group of investors following bank failures and government rescues.

While its popularity has grown among speculative investors in the roughly decade-and-a-half since, it has retained a status among some as being an asset more removed from the banking system than stocks and government bonds.

If the Fed decides to slow down the pace of interest rate hikes this is highly bullish for the crypto and tech growth sector.

Crypto investors have been particularly sensitive to regulatory and interest-rate developments.

They tend to pull money from long-bitcoin funds while adding to short-bitcoin products after the Federal Reserve announces interest-rate increases and regulators take action against crypto companies.

Since regulators started to crack down on some of the biggest crypto players, investors have pulled about $424 million from global exchange-traded products.

It’s been a terrible year to short bitcoin as that trade was last year’s rich uncle.

An important part of investing is to avoid searching for that boat that has left the dock.

Investors betting against crypto exchange, Coinbase (COIN), and bitcoin-buying software intelligence firm, MicroStrategy (MSTR), were down 76% and 62%, respectively, this year.

Some investors remain cautiously optimistic about the trajectory of bitcoin’s price, especially as it has surged against the backdrop of a banking crisis.

Although there could be a vicious pullback from the epic surge so far this year, Bitcoin will likely do well along with tech growth stocks in a paused or lower rate interest environment.

Throw in the bank contagion as a supercharger and 2023 is shaping up to be a great year to buy bitcoin and growth tech on the dips.

Mad Hedge Technology Letter

August 24, 2022

Fiat Lux

Featured Trade:

(ZOOMING TO FAILURE)

(ZM), (MSFT), (TDOC)

Let’s call it what it is – a one-hit wonder.

Zoom Video Technologies (ZM) was the darling of 2020 as we idled in our homes and succumbed to digital use if we liked it or not.

ZM became the hot item because they had an edge in the video conferencing product and their stock price boomed as we were all hooked on their software.

Fast forward to today and ZM CEO Eric Yuan wishes conditions were similar to 2020 so he can somehow combat the growth of Microsoft Teams which is essentially the same product as ZM but offered for free from competitor Microsoft (MSFT).

Teams keeps adding new features and when the inflationary monster disrupts the balance sheet too much, enterprises stop paying for ZM.

ZM is having a tough time battling it out with free software.

The company also cut its annual revenue forecast, saying it’s losing sales from consumers and small business faster than anticipated.

Zoom’s breakneck growth during the pandemic has cooled considerably as offices reopen and other software copycats take shape.

Online sales to consumers and small businesses are expected to decline 7% to 8% this year, Chief Financial Officer Kelly Steckelberg said on a conference call.

Zoom has responded by intensifying its focus on larger enterprise clients and pitching an expanded line of products such as software for customer contact centers.

In June, the company unveiled a new service bundle, Zoom One, to highlight offerings like internet-connected phones and physical conference rooms.

I’m not positive on these secondary offerings, particularly Zoom Phone, and see few use cases for it moving forward.

Sales to enterprise customers are expected to grow by more than 20% this year.

The company also reduced its annual sales forecast to about $4.4 billion from its May projection of as much as $4.55 billion. About $115 million of the cut is due to the “broader economic environment” and $35 million is due to the stronger US dollar.

ZM has effectively glamorized Facetime on the computer and the bad news is that there is no moat around this proprietary technology.

Zoom Phone is literally Facetime with no computer.

Good luck finding the incremental client.

This is the reason for big tech catching up to ZM so quickly and after relinquishing their first mover advantage, there has been no second act or even 1.5 act. It’s a quickly eroding wasteland for the ZM brain trust.

Then the company referenced the “broader economic environment” as to reasons for a lower forecast confirming what many people already know that we are barreling straight into a 2023 recession and ZM will be a discretionary service that gets cut with ease.

Not even the newly crowned federal student loan forgiveness group will spend their new bonuses on this unneeded software.

To be fair, it hasn’t only been ZM that has been body slammed, the other lockdown darling Teladoc (TDOC) which specializes in remote health consultations is trading at 5-year lows.

The stock is almost 10X lower than at its point in February 2021.

Even if there’s an apocalypse, users won’t gravitate to ZM highlighting the outsized risks of a one-trick pony with no competitive advantage.

Stay away from this stock.