Mad Hedge Biotech and Healthcare Letter

July 26, 2022

Fiat Lux

Featured Trade:

(ANOTHER TECH AND HEALTHCARE CROSSOVER)

(ONEM), (AMZN), (TDOC), (AMWL), (GOOGL), (AAPL), (MSFT), (CVS), (WBA), (UNH)

Mad Hedge Biotech and Healthcare Letter

July 26, 2022

Fiat Lux

Featured Trade:

(ANOTHER TECH AND HEALTHCARE CROSSOVER)

(ONEM), (AMZN), (TDOC), (AMWL), (GOOGL), (AAPL), (MSFT), (CVS), (WBA), (UNH)

The battle for telemedicine dominance might have just ended before it even began.

Amazon (AMZN) just announced its all-cash plan to acquire One Medical (ONEM) for $3.9 billion, paying $18 per share.

To date, this will be Amazon’s biggest step toward the healthcare world.

With the entry of Amazon into this telehealth segment, companies like Teladoc (TDOC) and Amwell (AMWL) would need to work overtime to match the resources of the e-commerce giant.

However, Amazon’s move isn’t exactly novel considering that other FAANG companies like Google (GOOGL), Apple (AAPL), and Microsoft (MSFT) have already acquired healthcare companies.

What this move simply indicates is that Amazon has finally turned serious in its bid for a bigger piece of the healthcare market.

This isn’t even the first time Amazon decided to go beyond its retail business. It has a pretty diverse portfolio including Amazon Web Services, a cloud infrastructure service, and even Whole Foods.

However, the decision to aggressively pursue the $800 billion healthcare industry might just be what Amazon needs to really move the needle.

In 2018, Amazon shelled out roughly $1 billion to buy an online pharmacy called PillPack which led to the launch of virtual Amazon Care clinics.

On that same year, the e-commerce company also pursued a joint venture, dubbed Haven, with Berkshire Hathaway and JPMorgan Chase. Unfortunately, that plan didn’t pan out and was eventually shut down.

Buying One Medical at a premium of 77%, Amazon beat other interested bidders including CVS (CVS), Walgreens (WBA), and UnitedHealth (UNH).

It’s still unclear what Amazon plans with One Medical. The e-commerce giant might add it to its Amazon Care brand or let it operate independently.

One Medical is a membership-based platform, which is backed by the Carlyle Group (CG) and managed under 1Life Healthcare.

Like most telehealth companies, it offers virtual healthcare services like virtual visits. What makes it different is that it also provides in-person checkups in accredited medical offices within the US.

One Medical’s app enables clients to schedule appointments, talk with their healthcare provider, and ask for prescriptions.

A key selling point is that the company guarantees that all the appointments start on time. Another notable feature is that users can gift a yearlong subscription to someone for $199.

Like Teladoc and Amwell, the company isn’t profitable yet. This case isn’t shocking for a relatively new field.

However, One Medical’s strategy has led to impressive revenue and membership growth.

The company’s revenue has consistently increased since its 2020 IPO. In 2021, its membership count climbed by 34% to reach 736,000.

In the first quarter of 2022, One Medical’s membership grew again by 28% and revenue jumped 109% to record over $254 million. So far, more than 8,000 companies provide One Medical services to their staff.

For 2022, One Medical projects its revenue to be between $831 million and $853 million.

Admittedly, these figures seem inconsequential when you compare them to the other sectors of Amazon’s business. For example, Amazon Web Services raked in $18.4 billion in sales in the first quarter of 2022.

Actually, One Medical’s revenue and membership growth might even look small and unimpressive compared to Teladoc, which recorded $565 million in the first quarter and has more than 54 million members in the US alone.

Undoubtedly, the healthcare market offers a mouthwatering opportunity for the likes of Amazon. It’s a lucrative industry, one of the handful that can truly make a difference in an already thriving business. Moreover, it has been highly profitable over the years.

Nonetheless, the acquisition of One Medical isn’t a foolproof plan for Amazon’s dominance in healthcare. So far, the e-commerce giant’s track record has been mixed. That doesn’t mean that the deal is a bad move. In fact, it indicates Amazon’s seriousness in making a play for the healthcare market.

Either way, the clear winner would be One Medical. Since the announcement, the stock has risen 70%.

Moreover, even if Amazon falls victim to politicization or anti-trust issues involving the deal, One Medical still has a number of suitors lined up.

Basically, it’s a win-win for this emerging telehealth company.

When the sushi hits the fan – the sushi really does hit the fan.

We are at the beginning of a massive tech reckoning, and many will shed a tear because of the new changes.

The lavish era of artificially rock-bottom-priced interest rates that fueled an unconscionable tech bubble has now reached an end.

There wasn’t even a main street parade for the closing.

Many fortunes were christened over the past 13 years, mostly by the "Who’s Who" of Silicon Valley as founders and CEOs.

This meant that wild speculation was the flavor of the day which was a force that delivered the equity markets astronomically high tech valuations that we have never seen before.

Those likely won’t be back any time soon.

Many investors haven’t adjusted to the new normal yet.

Similar to 2009, the founders & executives that run VC-backed companies have been quick to figure it out.

They understand that the cost of capital is now exorbitantly high and that high cash burn rates are now impossible.

These artisanal tech companies with zero killer technology like Uber, Lyft, and Peloton are more or less screwed in this new environment.

Even though the executives and founders get what is going on, the same can’t be said on the field of play.

Tech employees who may have enjoyed higher than average success aren’t prepared to enter this new era where accountability and costs matter.

When I talk about employees, I am referring to the ones working in technology in the Bay Area.

Up until now, tech employees have been used to pretty much naming their benefits and compensation package and companies fighting over them.

A rude awakening meets them as tech companies who once showered stock options on new employees now wait in horror as that same method of payment is demonstrably less attractive to future employees with low stock prices.

Most employees have only experienced this amusement park-like setting in the Bay Area, which is what led to many employees dictating the work-from-home situation.

Unfortunately, they might now have to come into the office or get fired.

In many ways, this is not their fault. Excess capital led to excessive showering of employee benefits and heightened expectations.

Unfortunately, you can't ignore the fact that if your company isn't cash flow positive & capital is now expensive, you are living on borrowed time.

During the arbitrary societal lockdown, many companies experimented with remote workers, most from outside of the Bay Area.

Based on anecdotal conversations, this trend is likely to continue post-pandemic. This means the Bay Area employee is now competing with a broader set of alternatives.

In today's world, positive cash-flow matters & surviving requires outmaneuvering competitors.

You need teammates that are ready to grit it out and not whine like an adolescent teenager.

Sadly, we may have conditioned a contingent of employees in a way that is incongruent with this mindset.

As we enter the cusp of layoffs, the guy at the bottom is clearly hurt the most or the last one in is usually the first out.

There is nobody to blame for this situation.

The low rates encouraged that type of poor behavior because they could get away with it.

When everybody is making money, most companies don’t clamp down and top employees can’t get away with a lot.

Tech firms like Teledoc (TDOC) and DocuSign (DOCU) are in real trouble if the capital markets only offer them 10% cost of capital for the next few years.

As the greater economy looks to reset, the goalposts have narrowed in the technology sector and the firms considered “successful” from here on out will have a checkmark next to profitability.

Growth at all costs has now been substituted with survive at all costs in Silicon Valley, so get used to it.

Mad Hedge Technology Letter

May 11, 2022

Fiat Lux

Featured Trade:

TECH DESERVES WHAT IT DESERVES)

(RBLX), (ARKK), (ROKU), (TDOC), (ZM), (TSLA), (GM)

A bear market rally in tech would be an overwhelmingly healthy signal that the financial system is working in an orderly fashion.

Yet, as I say that, a looming recession inches closer.

How do I know that?

That was my first reaction when my eyes were stung by the headline of 8.3% inflation.

Sure, not a 10, but it is emblematic of the ongoing inflation concerns with items such as airplane tickets up 18% year over year in price.

Remember the consensus was that inflation pressures are trending towards peaking, potentially setting up for a nice bear market rally.

That narrative hit another catch-22, not as bad as it could have been, but clearly not great and prices biting at the backs of consumers.

The hope that inflation will be crammed back into the genie bottle is not going to happen until later this year and not for the right reasons.

Simply because comparables become easier to beat year over year.

Like I have mentioned in past tech letters, high-growth tech stocks are most sensitive to the fluctuation in rates and investors should be nowhere near growth funds like Cathy Wood’s ARK Innovation ETF (ARKK).

Another head-scratching move was ARK’s Cathy Wood selling Tesla (TSLA) shares and rolling them into GM (GM).

This is for the lady who likes to tell us that we aren’t “doing the research.”

Betting against Elon Musk is a fool’s game.

When it comes to EVs, I would put money on Musk to defy any odds.

Tesla will outperform GM, especially amid a backdrop of lithium prices spiking and supply chain issues going haywire.

Musk is simply the anointed guy that knows how to work miracles.

He only developed the EV industry as he saw fit, invented reusable space rockets, cut the price of space exploration by 10, and reimagined tunneling construction technology.

And by the way, his Neuralink brain interface company is working on implanting chips in human brains so we don’t need to use our fingers on keyboard anymore.

I wouldn’t want to compete with this man and to believe that GM will be able to nimbly outmaneuver Musk who has the audacity to aggressively solve anything no matter how many people he pisses off is not an incremental bet on “innovation” that Wood likes to tout she is participating in.

Neither is the purchase of Roku (ROKU), Zoom (ZM), or Roblox (RBLX) which have all tanked since she put new money to work in them in late April.

Inflation at 8.3% means that the real rate of inflation is still -7.55% and until that’s addressed, any bear market rally will be viciously sold breaching further levels down below.

The carnage in the tech world is indicative at the dregs of the barrel.

Tech IPOs are toxic.

Market for new issues has been bereft throughout the first four-plus months of this year, and nothing that would move the needle is on the tech IPO radar for the duration of the second quarter.

Companies that were aiming to go out in the first half of 2022 have no appetite to continue down that path because there simply won’t be a bid.

Going public today would require a complete revaluation of their business and leave many late-stage investors and employees with out-of-money stock.

Grocery deliverer Instacart is the only company in that class that’s been forthright with its slowing valuation. In March, the company said it cut its valuation by about 40% to $24 billion.

That’s how bad it is out there at the bush league end of the tech sector and many of these stocks that are public such as Teladoc are down 80%.

I do believe that many of these loss-making growth techs are rightfully down 80%.

They had time to show a profit and they failed in the allotted amount of time they were given.

Every window closes and the market moves forward with or without them.

In the near term, I am bearish on the market but I do believe we are oversold which could feed into a dead cat bounce to sell on.

Mad Hedge Technology Letter

April 29, 2022

Fiat Lux

Featured Trade:

(TELADOC IMPLODES)

(ARKK), (SARK), (TDOC), (ROKU), (SHOP), (ZM)

The Cathie Wood circus keeps making new lows as digital doctor platform Teladoc (TDOC) recorded the biggest drop in shares since its IPO.

At one point, shares were down 45% and this was the day after buying another tranche of over $200 million worth of shares before the earnings came out.

TDOC was a pandemic darling and since then, the stock has done nothing but dive lower.

There is even an inverse ETF to jump on the anti-Cathie Wood bandwagon called Tuttle Capital Short Innovation ETF (SARK).

SARK is almost up 100% year to date showing that as market conditions distort, traders must distort with them.

To stay long tech growth is like throwing money off an apartment balcony.

The lack of understanding Cathie Woods exhibits about the stock market is hard to fathom.

Her go-to excuse is that others “aren’t doing the research.”

We were smack dab in a low-rate environment for a decade when even marginal tech companies would get the benefit of the doubt.

As the goalposts have moved and narrowed, Wood is still sticking to her 5-year time horizon and still explaining to investors that other analysts “aren’t doing their homework.”

This really is a case of the emperor having no clothes if I have ever seen it.

To add insult to injury, she has gone on public television to speak about how she believes the global economy is experiencing deflationary pressures.

No matter what changes to the trading environment, she sticks to her narrow story of deflation and her 5-year time horizon while her investors lose money.

If that’s not enough, she blames the market for not understanding her ARKK fund which is down more than 50% this year.

She claims that many people are “devaluing innovation” and just do not understand innovation like she does.

With an unrelenting belief in her growth strategy, miraculously, another $1.5 billion of inflows have juiced up her fund in 2022.

There are many out there that still think she is a great money manager after her one call of Tesla going up was correct.

Investors have chosen to back her further even with mounting losses and that has now backfired as ETF ARK Innovation ETF (ARKK) appears as if the market has not recognized how smart Cathie Wood is.

ARKK is Teladoc’s largest shareholder with a 12% stake worth.

It’s not just TDOC, but other investments like Roku (ROKU), Zoom Video Communications (ZM), and Shopify (SHOP) whose shares have experienced cataclysmic meltdowns of epic proportions.

Why did TDOC shares perform so poorly?

Higher advertising expenses in the mental health market, as well as an “elongated sales cycle” in chronic conditions as employers and providers of healthcare plans evaluate strategies.

TDOC’s services aren’t as good as first thought.

TDOC also took a $6.6 billion charge for impairment of goodwill, a non-cash charge the company excluded from its adjusted results.

The competition also has increased significantly and many of these first-move advantages are not holding up like they used to in tech.

The recent performance has been met with a bevy of analyst downgrades and tech growth as a sub-sector will have a hard time recovering until a lower interest rate sentiment comes back to sweep up the market.

Still, not a peep out of Cathie Wood on modifying her controversial strategies and that’s when we are staring down a barrel of multiple 50 basis point interest rate rises.

She was photographed partying in the Bahamas at some beach parties the day before the TDOC debacle, apparently, she isn’t bothered that much by her followers losing generation wealth.

If readers want to get back into tech growth after an easing of credit conditions, avoid buying ARKK and just buy a collection of strong tech growth yourself.

Global Market Comments

April 11, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or WATCH OUT FOR THE RECESSION WARNINGS)

(TLT), (TSLA), (FB), (CRSP), (TDOC), (GILD), (EDIT), (SQ), (INDU), (NVDA), (GS)

The drumbeat of a coming recession is getting louder and louder.

There is no doubt that the traditional signals of a slowing economy are already flashing yellow, if not bright red.

Rocketing interest rates are the most obvious one, with ten-year US Treasury bonds yield soaring from 1.33% to 2.71% in a mere four months. This is why investors pulled a gut-punching $87 billion out of bond funds in Q1.

If the Fed continues with a quarter point rise at every meeting for the rest of the year, we might escape this cycle without a recession. If the Fed ramps up to a half point rate at every meeting as was discussed last week a recession becomes a sure thing.

Imminent positive real yields for the first time in a decade also threaten to draw money out of stocks and into bonds.

I happen to be in the non-recessionary camp and the reason is very simple. Companies are making too much damn money. This is especially true for technology companies, which account for some 75% of the profits made in the US. If anything, their profits are accelerating, although at a lower rate than seen in 2021.

Certainly, the tech companies themselves aren’t buying the recession scenario. They are hiring and investing as if the economic boom will continue forever. Tesla alone has completed two new factories in the past month, in Berlin, Germany and Austin, Texas, each capable of producing a half million vehicles a year. Tesla’s existing factories are all expanding capacity.

Sitting here in Silicon Valley, I can tell you that the job market is as hot as ever. Those who have jobs, like my own kids, are besieged with multiple job offers. It seems the standard time to keep a job these days is a year, after which one takes the next upgrade, promotion, and batch of stock options.

But the stock market seems hell-bent on discounting a recession anyway. You see this in the most economically sensitive sectors of the market, banks, semiconductors, and transport, which have just clocked a miserable month. If I am right (I’m always right), and there is no recession, these will be the sectors that lead the recovery.

Until the market makes up its mind, the disciplined among us will have to while away our time constructing lists of companies to buy for the rebound. That’s when the next leg of the bull market resumes.

We find out when this happens on Wednesday when the next batch of inflation data is released, which is likely to be diabolical.

Quantitative Tightening to Start as Soon as May, according to Fed Governor Brainard. That means our central bank will start selling its vast $9 trillion in bond holding in two months, a huge market negative. Bonds tanked. The Fed only quit quantitative easing in March.

Tesla Blows Away Q1 Sales, shipping 310,000 vehicles, far above expectations. This is despite supply chain problems, soaring interest rates, and the Ukraine War. Sky-high gasoline prices helped a lot, which is driving buyers into Tesla showrooms in drives. All other competitors are falling farther behind, unable to obtain parts and commodities which Tesla locked up long ago. This puts Tesla well on its way to its 1.5 million production goal for this year. Keep buying (TSLA) on dips. My long-term target is $10,000 a share.

The Metaverse May be Worth $13 Trillion by 2030, says Citibank. The same is so for Web 3.0, which includes virtual worlds, like gaming and applications in virtual reality. Citi’s broad vision of the metaverse includes smart manufacturing technology, virtual advertising, online events like concerts, as well as digital forms of money such as cryptocurrencies like I’ll be looking for the best plays.

Biotech May Be Staging a Comeback, after spending a year in hell, taking some shares down 80%-90%. Investors are also nibbling at the sector as a recession and bear market plays, as these companies keep growing regardless of the economic cycle. Buy (CRSP), Teledoc (TDOC), Gilead Sciences (GILD), ad Editas Medicine (EDIT) on dips.

US Bonds Just Suffered their Worst Quarter in a Half Century, with yields rocketing from 1.33% to 2.71%, and Mad Hedge was triple short most of the way down. Bear LEAPS holders, which are many of you, made fortunes. We could stall around current levels until the Fed delivered both barrels of a shot gun, two back-to-back half point rate rises from the Fed.

30-Year Fixed Rate Mortgage Rates Top 5.00%, trashing the home builders. If you thought buying a home was tough, its worst now. So far, no impact on home prices.

US Dollar Hits New Two-Year High. It’s all about rising interest rates. Expect a stronger greenback to come before the turn. The coming QT will put a two-step turbocharger on the move.

German Battery Sales Soar By 67%, to residential buyers to cope with pending energy shortages. Germany already has 2.2 million solar installations out of a population of 83 million. It’s a very smart move as batteries powered by solar panels can remove you from the grid entirely, as I have amply proven with my own installation. It may be the permanent solution to over-dependence on Russian energy supplies.

Tesla Moving into Bitcoin Mining, in partnership with Blockstream and Block, formerly Square (SQ). Tesla will supply the electric power with its massive 3.8-megawatt solar array. That is the size of a large nuclear power plant. The mining facility is designed to be a proof of concept for 100% renewable energy bitcoin mining at scale. If Elon Musk likes Bitcoin maybe you should too.

The Bank of Japan Now Owns 7% of the Japanese Stocks Market. The central bank had to buy the shares after it had already bought all the bonds in the country to support the economy. So, what happens when the policy flips from QE to QT? How about unloading $371 billion worth of shares on the market. This would e a neat trick since so much of the country’s shares are locked up in corporate cross holdings. Methinks I’ll be steering clear of Japanese stocks for the foreseeable future.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

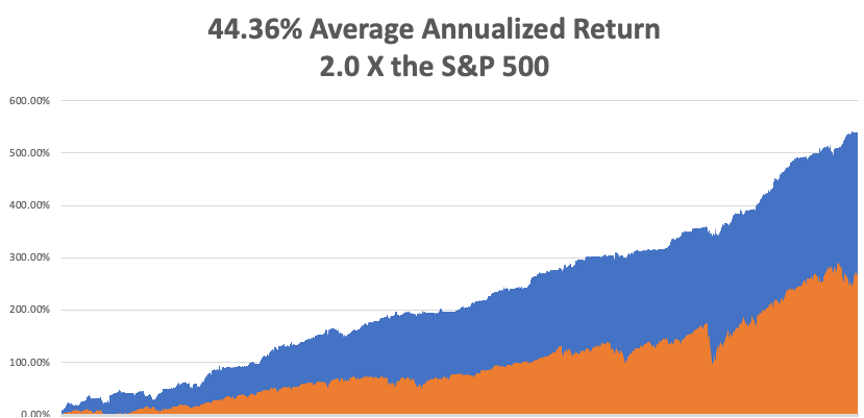

My March month-to-date performance retreated to a modest 0.38%. My 2022 year-to-date performance ended at a chest-beating 27.23%. The Dow Average is down -4.20% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 68.89%.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding long positions in technology, banks, and biotech. I am currently in a rare 100% cash position awaiting the next ideal entry point.

That brings my 13-year total return to 539.79%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.36%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.3 million, up only 100,000 in a week and deaths topping 985,000 and have only increased by 2,000 in the past week. You can find the data here. Growth of the pandemic has virtually stopped, with new cases down 98% in two months.

On Monday, April 11 at 8:00 AM EST, Consumer Inflation Expectations are released.

On Tuesday, April 12 at 8:30 AM, the Core Inflation Rate for March is announced.

On Wednesday, April 13 at 8:30 AM, the Producer Price Index for March is printed.

On Thursday, April 14 at 7:30 AM, the Weekly Jobless Claims are printed. We also get Retail Sales for March.

On Friday, April 8 at 8:30 AM, NY Empire State Manufacturing Index for March. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, back in 2002, I flew to Iceland to do some research on the country’s national DNA sequencing program called deCode, which analyzed the genetic material of everyone in that tiny nation of 250,000. It was the boldest project yet in the field and had already led to several breakthrough discoveries.

Let me start by telling you the downside of visiting Iceland. In the country that has produced three Miss Universes over the last 50 years, suddenly you are the ugliest guy in the country. Because guess what? The men are beautiful as well, the decedents of Vikings who became stranded here after they cut down all the forests on the island for firewood, leaving nothing with which to build long boats. I said they were beautiful, not smart.

Still, just looking is free and highly rewarding.

While I was there, I thought it would be fun to trek across Iceland from North to South in the spirit of Shackleton, Scott, and Amundsen. I went alone because after all, how many people do you know who want to trek across Iceland? Besides, it was only 150 miles or ten days to cross. A piece of cake really.

Near the trailhead, the scenery could have been a scene from Lord of the Rings, with undulating green hills, craggy rock formations, and miniature Icelandic ponies galloping in herds. It was nature in its most raw and pristine form. It was all breathtaking.

Most of the central part of Iceland is covered by a gigantic glacier over which a rough trail is marked by stakes planted in the snow every hundred meters. The problem arises when fog or blizzards set in, obscuring the next stake, making it too easy to get lost. Then you risk walking into a fumarole, a vent from the volcano under the ice always covered by boiling water. About ten people a year die this way.

My strategy in avoiding this cruel fate was very simple. Walk 50 meters. If I could see the next stake, I proceeded. If I couldn’t, I pitched my tent and waited until the storm passed.

It worked.

Every 10 kilometers stood a stone rescue hut with a propane stove for adventurers caught out in storms. I thought they were for wimps but always camped nearby for the company.

I was 100 miles into my trek, approached my hut for the night, and opened the door to say hello to my new friends.

What I saw horrified me.

Inside was an entire German Girl Scout Troop spread out in their sleeping bags all with a particularly virulent case of the flu. In the middle was a girl lying on the floor soaking wet and shivering, who had fallen into a glacier fed river. She was clearly dying of hypothermia.

I was pissed and instantly went into Marine Corp Captain mode, barking out orders left and right. Fortunately, my German was still pretty good then, so I instructed every girl to get out of their sleeping bags and pile them on top of the freezing scout. I then told them to strip the girl of her wet clothes and reclothe her with dry replacements. They could have their bags back when she got warm. The great thing about Germans is that they are really good at following orders.

Next, I turned the stove burners up high to generate some heat. Then I rifled through backpacks and cooked up what food I could find, force-fed it into the scouts and emptied my bottle of aspirin. For the adult leader, a woman in her thirties who was practically unconscious, I parted with my emergency supply of Jack Daniels.

By the next morning, the frozen girl was warm, the rest were recovering, and the leader was conscious. They thanked me profusely. I told them I was an American “Adler Scout” (Eagle Scout) and was just doing my job.

One of the girls cautiously moved forward and presented me with a small doll dressed in a traditional German Dirndl which she said was her good luck charm. Since I was her good luck, I should have it. It was the girl who was freezing the death the day before.

Some 20 years later I look back fondly on that trip and would love to do it again.

Anyone want to go to Iceland?

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Iceland 2002

Mad Hedge Technology Letter

March 7, 2022

Fiat Lux

Featured Trade:

(SHORT TERM PAIN FOR SILICON VALLEY TECH)

(NFLX), (QQQ), (EPAM), (SNAP), (TDOC), (ARKK)