Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)

Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)

If I had a dollar for every time someone told me the biotech sector was overvalued, I'd have enough to fund my own drug development program.

Yet here we are, watching the global immunology market rocket from $55 billion to $166 billion in just a decade, with the sector projected to hit $192 billion by 2028.

If you're wondering why big pharma keeps pouring billions into autoimmune research - and believe me, this question came up in every meeting last week - the answer is simple: we've barely scratched the surface.

Despite thousands of PhDs burning midnight oil in labs from Boston to Basel, we still don't have effective treatments for systemic lupus erythematosus, scleroderma, or even something as visible as vitiligo.

Want to see where the smart money is going? Look no further than the biosimilar stampede into AbbVie's (ABBV) Humira territory.

Like bargain hunters at a Black Friday sale, everyone's getting in line: Amgen (AMGN) with Amjevita, Sandoz (SDZNY) with Hyrimoz, Coherus (CHRS) with Yusimry, and Pfizer (PFE) with Abrilada.

And just when you thought the party was over, here comes Amgen's Wezlana challenging Johnson & Johnson's (JNJ) Stelara, followed by Alvotech (ALVO) and Teva's (TEVA) Selarsdi.

But here's where it gets interesting. I've identified four companies that are trading at valuations that would make Benjamin Graham smile.

First up is AbbVie, trading at 15.96x earnings (11.9% below sector median), with projected EPS growth to $15.21 by 2027.

Their dynamic duo of Rinvoq and Skyrizi is performing like a biotech version of Batman and Robin.

Rinvoq sales hit $1.61 billion in Q3 2024, up 45.4% year-over-year, while Skyrizi broke $3 billion, thanks to its mid-2024 FDA approval for ulcerative colitis.

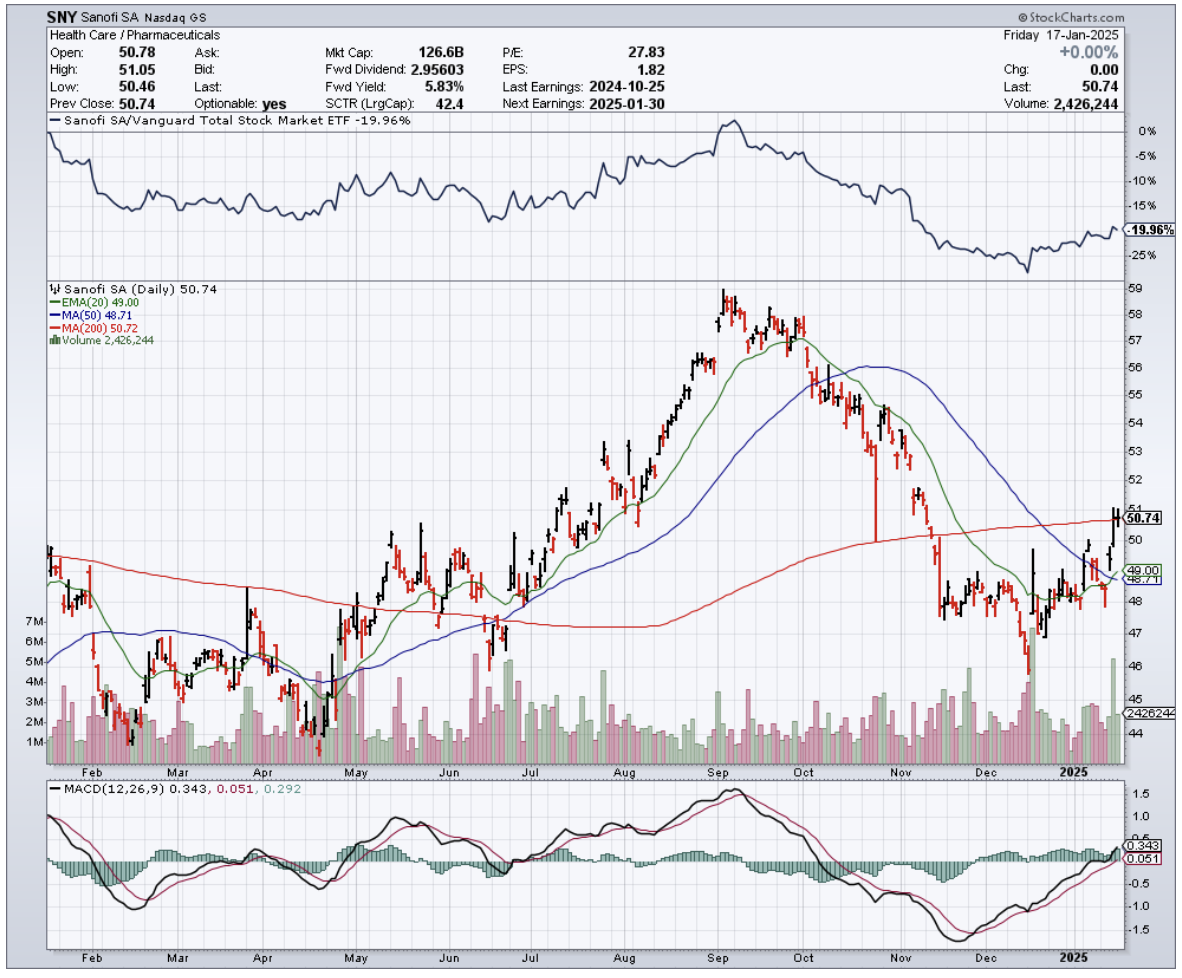

As for Sanofi (SNY)? Now we're talking value. At 11.7x earnings - 35.39% below sector median and 1.3% below its 5-year average - it's like finding a Ferrari priced like a Fiat.

Their star player Dupixent raked in 3.48 billion euros in Q3 2024, up 22.1% year-over-year and 5.2% quarter-over-quarter.

Then, there’s Teva Pharmaceuticals. Trading at a P/E ratio of 7.88x - that's 56.5% below the sector median - while projecting non-GAAP EPS growth to $3.6 by 2028.

But here's the kicker: their clinical trial data reads like a biotech investor's dream. Their new drug duvakitug achieved 47.8% clinical remission in ulcerative colitis patients versus 20.45% for placebo (p=0.003).

In Crohn's disease? Even better - 47.8% endoscopic response compared to 13% for placebo (p<0.001).

Finally, there's Bristol-Myers Squibb (BMY). Yes, it's trading at 47.5x earnings (162.1% above sector median), but here's where patience pays off - their P/E ratio is expected to drop to 8.82x by 2027.

Meanwhile, Zeposia sales jumped 19.5% year-over-year to $147 million in Q3 2024, while Sotyktu showed consecutive quarterly growth.

The cherry on top? These companies are paying you to wait. We're talking dividend yields from 3.8% to 4.41% - try getting that from your savings account.

Looking at these numbers reminds me of the tech sector in the late 1990s, but with one crucial difference - these companies are actually making money, lots of it.

They generate significant cash flow and have strong balance sheets, unlike many of the high-flying tech companies of the dot-com era that were burning through cash with no clear path to profitability.

While others are chasing the next meme stock or crypto moonshot, smart investors are quietly positioning themselves in companies that are literally changing the face of medicine.

Remember, buying umbrellas in the summer heat has always been my style.

Right now, the immunology sector is experiencing its own kind of summer, and these four stocks are your umbrellas.

The forecast? Growth storms ahead.

Mad Hedge Biotech and Healthcare Letter

August 1, 2024

Fiat Lux

Featured Trade:

(THE PLAYBOOK FOR A BIOTECH TRIPLE CROWN)

(ABBV), (TEVA), (PFE), (AMGN), (AZN), (BGNE), (LLY), (CERE)

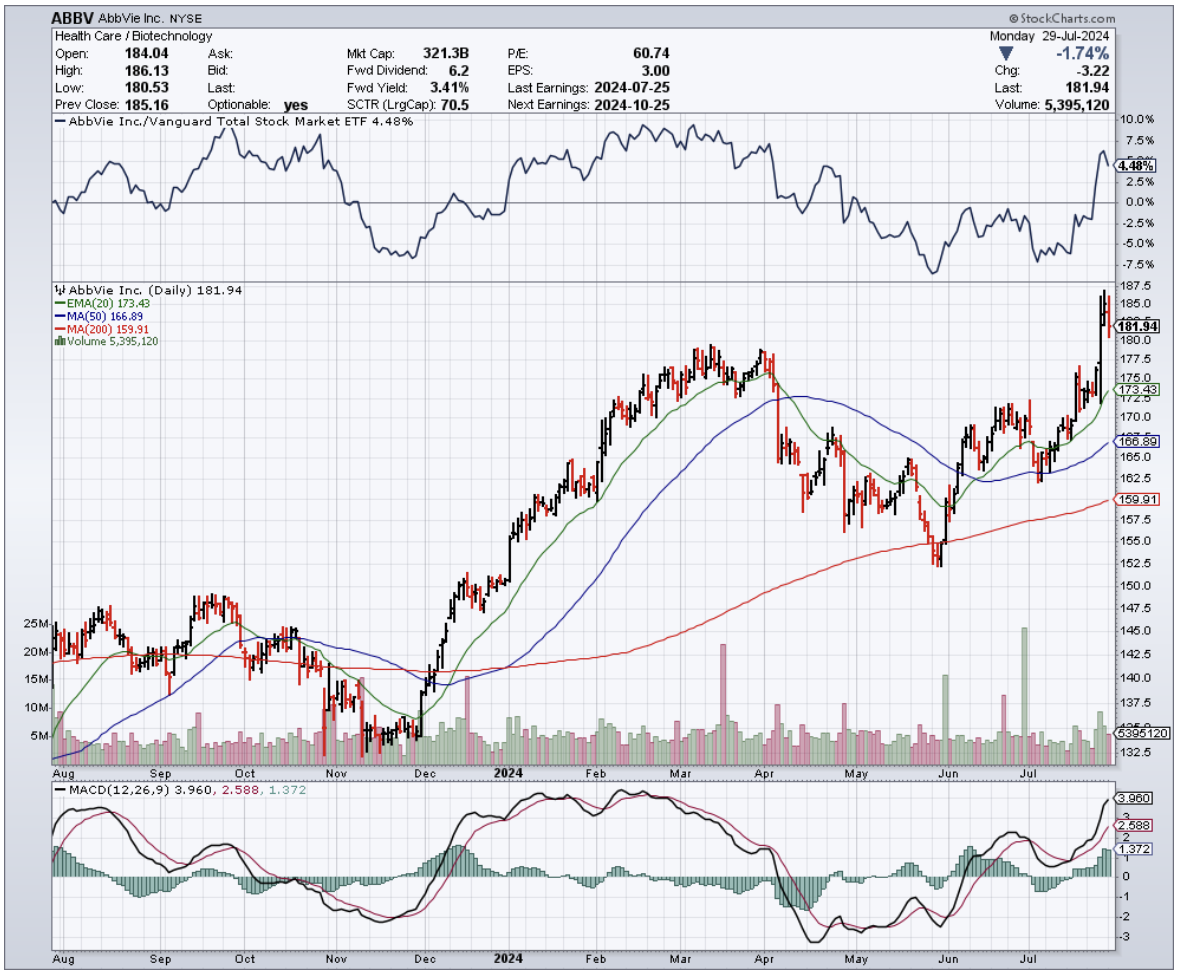

AbbVie (ABBV): A biotech stock that's been on my radar longer than most. If I could travel back to my UCLA biochem days, I'd tell young John to ditch the petri dishes and buy shares in this pharma giant. Why?

Because AbbVie isn't just another pharma play – it's a masterclass in diversification, innovation, and market-beating performance.

This is the stock that could turn a bright-eyed student into a savvy investor faster than you can say "immunology franchise."

In fact, if you've been paying attention to the market, you might have noticed that AbbVie's stock has been outperforming the broader U.S. market since mid-April, and for good reason.

This is a company that's been running at full throttle, posting some seriously impressive numbers in Q2 2024. We're talking $14.46 billion in revenue, a whopping 17.5% increase from the previous quarter and beating consensus estimates by a cool $430 million.

Earnings per share may have fallen just short of analysts' expectations, but they still climbed by a respectable 34 cents to $2.65.

But here's the thing: AbbVie's success isn't just a flash in the pan. This is a company with a diversified portfolio that's driving growth across multiple fronts.

I'm talking about their immunology, oncology, and neuroscience franchises, which together account for a staggering 75% of the company's total revenue.

Let's start with immunology. Now, I know what you're thinking - isn't that just Humira, AbbVie's blockbuster drug for Crohn's disease and ulcerative colitis? Well, yes and no.

While Humira has been facing some generic competition from the likes of Teva Pharmaceutical (TEVA), Pfizer (PFE), and Amgen (AMGN), resulting in a 30% year-over-year decline in global sales, AbbVie's got a couple of other tricks up its sleeve.

Enter Skyrizi and Rinvoq, two immunology drugs that are picking up the slack in a big way. Sales of these bad boys climbed 45% and 56%, respectively, in Q2 2024.

Skyrizi, in particular, has been an absolute beast, raking in $2.73 billion and growing 44.8% year-over-year. And with the FDA giving it the green light for moderate-to-severe ulcerative colitis in June 2024, the sky's the limit for this game-changer.

But AbbVie's not content to rest on its laurels. They're pushing the envelope with Rinvoq, a JAK inhibitor that's been approved for a wide range of indications and is showing some serious promise.

In Q2 2024, Rinvoq brought in $1.43 billion, a 30.8% quarter-over-quarter increase, thanks to strong demand in the U.S., excellent clinical trial results, and FDA approval for treating children with psoriatic arthritis and juvenile idiopathic arthritis.

And let's not forget about giant cell arteritis, a condition that AbbVie's been targeting with Rinvoq.

Recent trials have shown some impressive results, with 46% of adult patients taking Rinvoq 15 mg experiencing sustained remission, compared to just 29% of those on placebo.

No wonder AbbVie's been submitting applications left and right to get this drug approved for even more indications.

But it's not just immunology where AbbVie's making waves. Their oncology portfolio, bolstered by the acquisition of ImmunoGen in mid-February 2024, is also delivering the goods.

Sure, demand for Imbruvica may be declining due to newer BTK inhibitors from AstraZeneca (AZN), BeiGene (BGNE), and Eli Lilly (LLY), but Elahere, an antibody-drug conjugate for ovarian cancer, is quickly becoming a rising star.

In Q2 2024, Elahere sales jumped 65.4% quarter-over-quarter to $128 million, driven by increased marketing, growing awareness among physicians, and promising data from clinical trials.

Finally, let's not overlook AbbVie's neuroscience franchise, which generated a cool $2.16 billion in Q2 2024, a 14.7% year-over-year increase.

Headlining this portfolio are Qulipta and Ubrelvy for migraine treatment, and Vraylar for a range of psychiatric conditions.

Qulipta, specifically, has been a standout, with sales surging 56.3% year-over-year to $150 million, thanks to its convenient oral administration and long-term efficacy data.

Looking ahead, AbbVie's got even more irons in the fire. Their $8.7 billion acquisition of Cerevel Therapeutics (CERE) is set to close soon, bringing promising neuroscience candidates like emraclidine for schizophrenia and davapidon for Parkinson's into the fold.

With all these positive developments, it's no wonder AbbVie's feeling confident enough to raise its full-year adjusted EPS guidance to $10.71-$10.91, up from the previous range of $10.61-$10.81. Talk about a biochemistry experiment gone right!

So, there you have it. AbbVie: a healthcare powerhouse that's firing on all cylinders and poised for even greater success in the years to come. If only I could've shown this to my younger self back in those UCLA labs – he might've traded his test tubes for trading terminals a lot sooner.

Now, if you're ready to take a ride on this rocket ship, I suggest you buckle up and hang on tight. Because let me tell you, dissecting AbbVie's financial DNA has been more thrilling than any fracking adventure or hedge fund rodeo I've ever been on.

And if there's one thing I've learned in my years hopscotching from biochem labs to Wall Street, it's that the view from the top of a well-diversified, innovative pharma giant is always worth the climb. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

November 21, 2023

Fiat Lux

Featured Trade:

(A PRESCRIPTION FOR CAUTION)

(VTRS), (PFE), (JNJ), (LLY), (BMY), (TEVA), (ABBV), (CVS)

In the rollercoaster world of pharmaceutical stocks, 2023 has been like riding the Cyclone at Coney Island – thrilling for some, nauseating for others.

Take Pfizer (PFE), for instance. It’s seen its stock take a nosedive by 43.4%. That’s the kind of drop that makes you check if your wallet’s still there. Then there’s Johnson & Johnson (JNJ), trailing behind with a 16.4% decline. Not as dramatic, but still enough to make your stomach lurch.

Meanwhile, there’s Eli Lilly (LLY), playing the hero as it rockets up by an extraordinary 66.8%, thanks to its new weight-loss drugs. At this point, investors are practically throwing ticker-tape parades.

However, even with Eli Lilly’s star performance, the S&P 500 Pharmaceuticals index still shows a downturn of 2.3%.

Now, as we've seen earnings reports trickle in, a trend has started to stick out: positive results aren’t shielding drugmakers from a sell-off. Look at Pfizer and Bristol Myers Squibb (BMY), both hovering near their 52-week lows.

Still, investors are giving the biotechnology and healthcare stocks the side-eye for several reasons.

The new Medicare drug-price negotiation program is like a strict parent setting a curfew – it’s potentially restricting pricing power for certain medications. Plus, as interest rates climb, the allure of high dividend yields is diminishing faster than my motivation to hit the gym.

In this skeptical market, however, there are some optimistic investors who are digging through the bargain bin, hoping to strike gold.

Enter Viatris (VTRS), trading at just 3.3 times earnings and boasting a 5.1% dividend yield. It sounds promising, but only a few brave souls are recommending a buy.

Basically, this situation with Viatris is pretty much like finding a designer shirt at a discount store – sure, it’s cheap, but will it fall apart after two washes? Let’s take a closer look.

Viatris’s backstory is a bit of a soap opera. Born from the merger of Mylan and Pfizer's Upjohn unit, it carries the baggage of Mylan's EpiPen pricing scandal.

Since rebranding, Viatris has been trying to find its footing. Despite a shiny new business plan, which involves selling off assets for a potential $9 billion, investor confidence remains shaky at best.

Notably, its decision to exit the biosimilars market, where heavy hitters like Teva Pharmaceutical Industries (TEVA) and AbbVie (ABBV) play ball, has been seen as a bold move. Considering the potential of that market, it felt like leaving a high-stakes poker game just when the chips were starting to stack up. And with CVS Health (CVS) eyeing this lucrative space, Viatris might find itself wishing it had stayed at the table.

These past months, investors have been capturing this drama through a meme – comparing 'adjusted Ebitda' to 'free cash flow' with images of Jennifer Aniston and Iggy Pop. It’s a cheeky way of saying that Viatris’s financial projections might be wearing rose-colored glasses.

Looking ahead, Viatris is aiming for $2.3 billion in free cash flow next year, buoyed by recent sales. But the big question is: can it turn these assets into growth, or will it continue its high-wire act?

Reviewing its recent moves and their effects on the market, the Viatris saga has turned into a cautionary tale for investors in the pharma world – it’s a reminder that sometimes the threat of a nosedive is as real as the thrill of a skyrocket.

So, what’s the takeaway for those of us with skin in the game?

It seems wise to keep our eyes peeled and not jump on any bandwagons too hastily. Viatris, amidst its strategic transformations and market challenges, is worth watching with a careful eye. While its cash flow looks steady through 2027, thanks to planned asset sales, the long-term picture is as clear as mud.

As we navigate the unpredictable waves of the pharmaceutical market this year, let’s remember – it’s not just about holding on for the ride. It’s about knowing when to get on, when to get off, and maybe, just maybe, when to enjoy the view from the sidelines with some popcorn in hand. I say hold off from buying Viatris shares at the moment.

Mad Hedge Biotech and Healthcare Letter

May 23, 2023

Fiat Lux

Featured Trade:

(HUNTING FOR OPPORTUNITIES IN HEALTHCARE STOCKS)

(LLY), (NVO), (VTRS), (OGN), (MRK), (TEVA), (GI), (CNC), (PFE), (GILD), (AMGN)

I've been riveted by the healthcare sector's most extravagant stocks lately.

Just look at Eli Lilly (LLY), with its jaw-dropping market value of $412 billion, making it the richest pure-play biopharma company ever. And right on its heels is Novo Nordisk (NVO), boasting a market value of $377 billion. It's enough to make your head spin.

But if you're on the hunt for value, these sky-high prices might leave you feeling a bit queasy. That's why I embarked on a mission to uncover some hidden gems in the healthcare sector.

Now, don't get me wrong. These stocks may be cheap for a reason, and it's crucial to exercise caution. When it comes to investment opportunities, it's essential to separate the diamonds in the rough from the fool's gold.

Enter Viatris (VTRS), a rising star in the generic drug manufacturing arena that has caught the attention of savvy investors seeking long-term holdings. But is it the real deal, or just another flash in the pan?

Viatris shows potential with solid revenue from branded generics like Lipitor, Viagra, and EpiPens. These household-name medicines have a lasting market demand. Plus, its generous 5.2% dividend yield surpasses the market average.

But here's the catch: Viatris is currently undervalued and has yet to prove its growth potential. Its stock price took a hit, and sales in the core generic and branded segments dipped. However, there's hope in the pipeline.

With a range of injectable generic medicines awaiting approval, Viatris could be at the forefront of the market.

By 2027, these programs could yield over $1 billion in annual revenue. While not a game-changer for the company's overall revenue, it sets the stage for future earnings growth.

At this stage, I don’t see Viatris as a slam-dunk investment. However, monitoring their strategic plan to reduce debt, improve efficiency, and drive growth is prudent. It's a work-in-progress worth monitoring for future opportunities.

Another company that caught my attention is Organon (OGN), a recent spinout from Merck (MRK) that focuses on women's health and biosimilars. This hidden gem trades at an attractive valuation of just 4.8 times earnings.

Organon & Co. is a pioneering developer and provider of prescription therapies and medical devices catering to contraception and fertility needs.

The female contraceptive market is projected to experience robust growth, with a compound annual growth rate (CAGR) of 8.5% from 2022 to 2027. Notably, Organon is among the top 5 major corporations addressing the demands in this market segment.

But that's not all.

Organon boasts a diverse portfolio that extends beyond women's health. They also offer biosimilar immunology products, two oncology treatments, hypertension therapies, respiratory solutions, dermatology products, non-opioid pain management pills, and cures for male pattern hair loss.

On its first day of official existence, June 3, 2021, Organon's management proudly announced a lineup of over 60 drug products to enhance female health, along with Merck's (MRK) former biosimilars portfolio.

The biosimilars market is projected to soar to $44.7 billion by 2026, showing an impressive CAGR of 23.5%.

As expected, the biosimilars arena has become a bustling hub with both established and emerging companies eagerly entering the space. For instance, Teva Pharmaceutical Industries Limited (TEVA) has high hopes for its biosimilar drug targeting arthritis treatment, expecting it to boost Teva's revenue significantly.

Organon has already witnessed promising revenue growth from its biosimilar drugs, with a remarkable 17% increase amounting to $116 million.

Several drug sales have experienced a surge of over 30% in the United States, Canada, and Brazil. Moreover, Organon's brands have shown strong performance in China and the Asia Pacific/Japan region.

Investing in women's health is not only a wise choice; it's a strategic move that can yield significant rewards for individual investors and portfolios. With Organon's innovative solutions, broad product portfolio, and forward-thinking approach, it stands out as a compelling opportunity in the market.

Now, let's take a look at some intriguing names that have found their way onto the list.

We have health insurance behemoth Cigna Group (GI), trading at a mere 9.9 times earnings, alongside the health insurer Centene (CNC) at 10.3 times earnings. Not to mention the presence of renowned drugmakers Pfizer (PFE), Gilead Sciences (GILD), and Amgen (AMGN) gracing this list of bargain stocks.

These seemingly cheap healthcare stocks warrant close attention for the savvy investor seeking hidden gems. Sure, the term "cheap" can sometimes be misleading, but within these underappreciated names lies the potential for hidden value waiting to be discovered.

Mad Hedge Biotech and Healthcare Letter

May 2, 2023

Fiat Lux

Featured Trade:

(QUANTUM COMPUTING IN BIOTECH)

(MRNA), (IBM), (PFE), (NVS), (ILMN), (TEVA), (NVO), (RHHBY), (GOOGL)

When you think of the pioneering biotech, Moderna (MRNA), artificial intelligence (AI) and quantum computing might not be the first things that come to mind. Instead, you might associate Moderna more with its work in traditional laboratory research and as a leading coronavirus vaccine manufacturer.

However, Moderna has taken significant strides into the realm of AI. In fact, the biotech utilized AI during the early stages of developing its coronavirus vaccine and has also implemented the technology for other business purposes.

Now, Moderna is taking things a step further by partnering with International Business Machines (IBM) to explore the potential of AI and quantum computing in enhancing its messenger RNA research.

Needless to say, this innovative collaboration could potentially revolutionize the biotech industry.

To understand Moderna's recent developments in AI and quantum computing, it's important to first have a grasp of its mRNA technology.

Unlike traditional vaccine production that involves growing viruses in a lab, Moderna produces mRNA that provides the body with instructions to treat or prevent a particular illness. This innovative process is already faster than traditional vaccine production methods. But AI has played a significant role in making the process even faster.

Moderna has been able to leverage AI and automation to scale up mRNA production significantly. In fact, the company's mRNA production for experiments went from about 30 per month to 1,000 per month thanks to AI. Additionally, AI has contributed to the generation of more effective mRNA sequence designs, saving researchers considerable time.

Let's now take a closer look at the implications of Moderna's partnership with IBM.

One of the primary areas of focus is IBM's generative AI for therapeutics, which has the potential to provide Moderna researchers with a deeper understanding of molecular behavior, facilitating the development of new molecules for therapeutics.

Moreover, IBM's expertise in quantum computing could prove invaluable in speeding up the discovery of new treatments, enabling Moderna to push the boundaries of medical research and improve patient outcomes.

Quantum computing differs from traditional computing in its use of a system that allows for states beyond the binary 1s and 0s. Quantum computers can understand information as 1, 0 or something in-between, offering the potential for individual bits to be in multiple states at the same time. This characteristic may be beneficial in modeling the dynamic interactions among drugs, enzymes, cells, and proteins that are continuously changing.

The use of advanced systems in molecular modeling has been challenging for earlier generations of hardware. However, the incorporation of quantum computing could revolutionize the way biotech companies solve these complex problems.

As a starting point, Moderna will be part of IBM's enterprise accelerator program, which provides a platform for "quantum curious" companies to invest in building their expertise in emerging areas. This program gives access to IBM's network of computing systems and specialized training on the use of quantum computing for life sciences research.

As part of this collaboration, Moderna will gain access to MoLFormer, a powerful AI model that can accurately predict a molecule's properties. This tool will prove particularly valuable in Moderna's efforts to improve the lipid nanoparticles that encapsulate its mRNA treatments.

Additionally, the partnership includes investments in generative AI programs that will assist in the design of innovative mRNA-based treatments and vaccines, helping Moderna to further cement its position as a leader in the biotech industry.

IBM had previously attempted to make a name for itself in AI-powered drug discovery, offering services through its Watson platform.

However, these offerings were ultimately discontinued in 2019. Despite once partnering with major names in cancer research such as Pfizer (PFE), Novartis (NVS), Illumina (ILMN), as well as Teva (TEVA) for drug repurposing, IBM has shifted its focus to other areas of the life sciences industry.

As quantum computing technology continues to evolve, however, its potential applications have begun to attract some of the biggest names in biotech.

Companies like Novo Nordisk (NVO), Roche (RHHBY), and Boehringer Ingelheim have partnered with industry giants like Google (GOOGL) to explore the possibilities of this cutting-edge field, which is quickly moving from the realm of science fiction into a scientific reality.

As for the question of whether these moves can be a game-changer for Moderna, the answer is likely yes.

Moderna has already experienced significant benefits from AI in its processes, both in and out of the lab. With access to IBM's platforms, there is potential for further improvements in the company's research and development of new treatments and vaccines.

Efficiency, speed, and precision are crucial factors in drug and vaccine development, and any improvement in these areas could have a significant impact on Moderna's success. Although the results of the IBM partnership may not be immediately visible, Moderna's investments in AI and quantum computing could pay off in the long run.

With continuous innovation and portfolio expansion, Moderna is well-positioned to capitalize on market opportunities presented by mRNA technology and achieve substantial revenue growth in the years ahead.

Therefore, investors should not be overly concerned about short-term stock price fluctuations or declines in revenue from coronavirus vaccines. After all, Moderna has a robust pipeline and has demonstrated significant potential with promising clinical trial results.

Hence, investors should consider Moderna as a long-term investment opportunity, making it a valuable addition to any investment portfolio.