Global Market Comments

January 15, 2025

Fiat Lux

Featured Trades:

(FRIDAY, JANUARY 31, 2025, SALT LAKE CITY, UTAH STRATEGY LUNCHEON)

(IT’S TIME TO PULL OUT THOSE OLD INFLATION PLAYS OUT OF THE DRAWER),

(GLD), (SLV), (TIPS)

Global Market Comments

January 15, 2025

Fiat Lux

Featured Trades:

(FRIDAY, JANUARY 31, 2025, SALT LAKE CITY, UTAH STRATEGY LUNCHEON)

(IT’S TIME TO PULL OUT THOSE OLD INFLATION PLAYS OUT OF THE DRAWER),

(GLD), (SLV), (TIPS)

Being an old do-it-yourself carpenter, I never throw anything away.

My garage is filled with ancient tools I bought 50 years ago and used only once.

Scraps of wood, odd lengths of wiring, and old coffee cans filled with loose nuts, screws, and nails are everywhere.

You KNOW that if you throw a tool out, you’ll desperately need it the next day.

The same is true of my investment approach. Nothing new ever happens in the financial market, plays that worked in past years just get endlessly recycled.

My inventory of ancient trading strategies includes instruments that were once incredibly profitable (Japanese equity warrant arbitrage?), but haven’t made money in decades.

So I was rooting around my trading toolbox the other day when I found just the ones I needed: inflation plays.

Some of the greatest trades of my half-century-long career in the trenches have been with inflation plays.

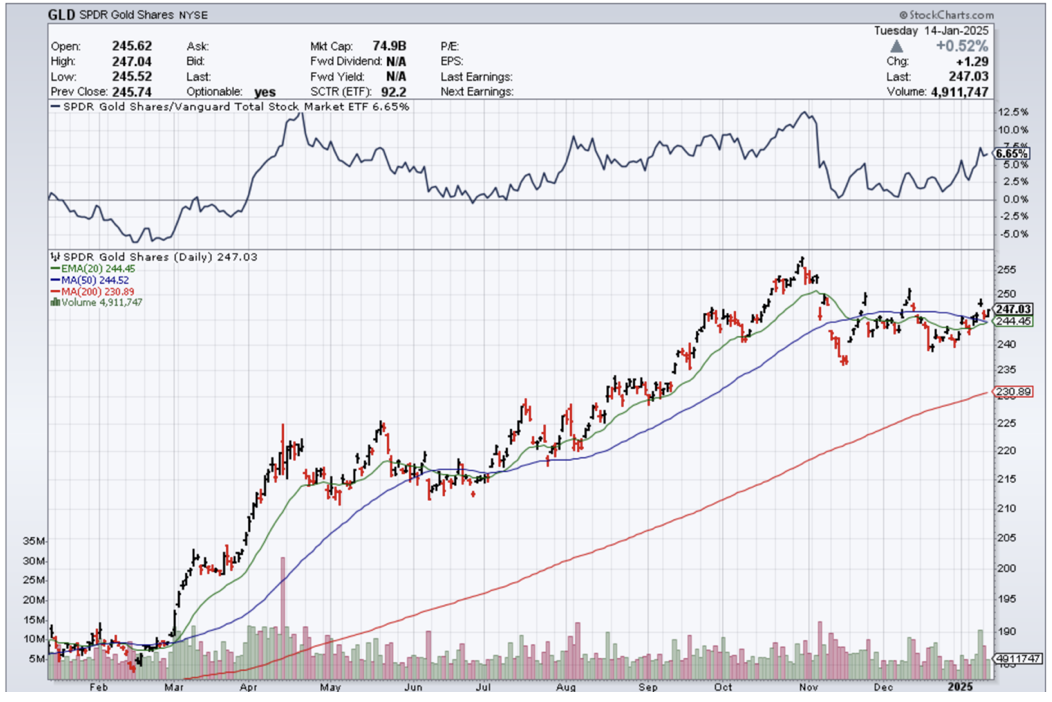

Of course, gold during the 1970s was the no-brainer after President Nixon took the US off the gold standard. I started buying in the barbarous relic in the mid-$30s and chased it all the way up to $900.

I made similar fortunes in that other great inflation hedge, residential real estate. Some of the properties I owned then in California have risen 100 times in value, thanks to inflation.

It was with those fond memories in mind that found myself looking for similar inflation plays to execute.

Let me stop right here.

The oldies are still the goodies.

In the next surge of inflation that the new administration is about to unleash, I expect gold to rise from today’s $2,703 an ounce to at least $5,000. After that, look out above!

Silver (SLV) should do double, eventually touching $100 an ounce from today’s $30.83.

Your home will also be a fantastic inflation hedge. Anything you own today should rise in value at least tenfold over the next 20 years.

However, in updating my research, I came across a few new wrinkles that are definitely worthy of your attention.

The big one is TIPS.

TIPS are US Treasury bonds that are indexed to inflation. If inflation rises, the value of your TIPS rises.

Specifically, TIPS are tied to the Consumer Price Index as calculated by the US Department of Labor Bureau of Labor Statistics.

Let me show you how they work.

Let’s say you bought $1,000 worth of TIPS with a 1% coupon. If the CPI comes in at zero, you will receive $10 that year in interest payments.

If the CPI rises 2%, your $1,000 in principal increases to $1,020. Your 1% coupon is then calculated off of this new, higher amount and jumps to $10.20, giving you a total return of $32.10.

Now here is the really fun part.

If the CPI rises to 15%, as it did in 1979, the value of your investment rises by 16.15% to $1,161.50.

Yes, I still have my bell bottoms from those days, although the waist is rather tight.

This explains why many high-net-worth individuals always have a few TIPS parked away in their portfolios, usually stuck in a folder behind the radiator.

TIPS are issued by the U.S. Treasury at recurring auctions as part of the government’s overall funding program.

Currently, the Treasury conducts monthly TIPS auctions: three per year for five-year TIPS, six for 10-year TIPS, and three for 30-year TIPS.

You can buy TIPS directly from the US government and bypass hefty third-party management and brokerage fees.

However, the semi-annual inflation adjustments of a TIPS bond are treated as taxable income by the IRS, even though investors won’t see that money until they sell the bond or it matures.

So it may be wise to buy your TIPS via a mutual fund or ETF or to only hold them in a tax-exempt IRA, 401k, or deferred benefit plan.

TIPS also have the additional benefit in that, like municipal bonds, they are exempt from state and local taxes.

Well-heeled residents of highly taxed California, New York, and Illinois absolutely love them.

Like many government programs, TIPS was first created in 1997 for a problem that didn’t exist: inflation. That year the CPI was only 1.7%.

The highest CPI since then was 3.4% in 2000, the year of the dotcom bubble top. For most of 2016, it hung around 1.6%.

Since the first issuance of tips, the US economy has been steadily battered by something no one predicted: deflation.

Thanks to the onslaughts of hyper-accelerating technology, flat wage growth, and global competition, prices worldwide have been heading ever lower.

For more than two decades, investors in TIPS were shortchanged. They accepted lower yields in return for protection against something that never happened. It was the fire insurance without the fire.

That is, no fire until January this year, when we saw an actual spark.

The CPI for that month came in at 0.6%, which works out to 2.5% annualized, the fastest pace of price appreciation in four years.

The TIPS explanation I have given you so far is the simple one. It gets much more complicated.

Seasoned bond pros have figured out ways to game this market six ways from Sunday using an array of sophisticated algorithms.

This enables them to add “alpha” by outperforming generic TIPS returns with aggressive high-turnover trading strategies.

Bond giant PIMCO and DoubleLine Capital are some of the more ardent practitioners of this approach.

These firms employ both top-down and bottom-up strategies, which can be broken down into the following:

Top-down strategies include:

Bottom-up strategies include:

If all of this gives you a headache and you just want to keep your life simple, you can just buy one of the many TIPS ETFs out there.

PIMCO has the Broad US TIPS Index ETF (TIPZ).

BlackRock has the iShares TIPS Bond ETF (TIP). Barclays has the SPDR 1-10 Year TIPS ETF (TIPX).

The only way these won’t work is if deflation, instead of ending, accelerates.

Artificial intelligence is only just starting to pervade our lives, and the productivity increases and cost savings it promises are enormous.

So is the potential job and wage destruction, the largest component of the CPI calculation.

If that is the case, then the CPI could turn negative, and sharply so. In that scenario, inflation-indexed TIPS will deliver losses instead of the promised gains.