Global Market Comments

December 5, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD MARKET AND THE BAD MARKET)

(TLT), (XOM), (OXY), (TSLA), (SPY), (BABA), (BIDU), (KBH), (PHM), (LEN), (AAPL)

Global Market Comments

December 5, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD MARKET AND THE BAD MARKET)

(TLT), (XOM), (OXY), (TSLA), (SPY), (BABA), (BIDU), (KBH), (PHM), (LEN), (AAPL)

I usually write my Monday strategy letters in the middle of the night in my mind, from 2:00 AM to 3:00 AM, because my feet are too hot, too cold, or because my hip hurts. Then I go back to sleep. If I remember half of it the next morning, then I get a great letter.

I often like to refer to old proven market nostrums and show how true they really are. One of my favorites is the concept of the “good” market and the “bad” market.

The good market is the one for bonds. Vastly more research goes into bonds than stocks because that’s where the respectable, safe, widows and orphan money goes. Global bond markets are also far bigger, worth about $120 trillion. Bond traders usually began their journey at Harvard or Wharton, speak with clipped upper-class accents, and belong to exclusive private clubs that would never let you in for lunch, even with an invitation from a member.

Suffice it to say that the bond market is always right. Their relaxed lifestyle can be explained by the fact that they really only have two variables to look at, Fed policy and the actual supply and demand for money. Working in the bond market is almost like a sinecure, sending you a paycheck every month because you are entitled to it.

The stock market is the complete opposite.

While the bond market was polishing the teacher’s apple at the head of the class, the stock market was smoking cigarettes in the bathroom, endlessly catching detention. The stock market is also smaller, worth about $50 trillion. While bond traders are attending their Rotary meetings, stock traders binge drink and tear up the roads with their new Porsches and Ferraris.

Needless to say, stock traders are always wrong.

That’s because they face a hopeless dilemma. While bond traders have to contemplate only two variables, stock traders have to deal with millions. They have to cope with the hundreds of input variables per company that affect their earnings, and there are over 3,000 companies that trade in the US alone.

To illustrate the point, look at the recent market action.

Both markets have been driven by the same massive liquidity created by the government since 2009. The bond market peaked in August 2020 when it saw the free lunch of ultra-low interest rates soon ending. Stocks didn’t peak until January 2021, some 17 months later. It’s clear that stock traders suffer from a severe learning disorder.

And they’re doing it again.

After a 49% swan dive over two years plus, bonds bottomed on October 14. Stocks may not finally bottom until the spring, six months after bonds. Bonds are now betting that the recession has already begun, we just haven’t seen it in the data yet. Stocks are betting that the recession doesn’t start until 2023, if at all. That’s why it’s been going up.

As for me, I have traded both stocks AND bonds. That’s because before there were stocks, there were bonds as the only thing to trade. As you may recall, stocks were moribund in the 1970s. On top of that, you can add foreign exchange, precious metals, commodities, and volatility. There essentially isn’t anything I haven’t traded.

My performance in December has so far tacked on another robust +3.37%. My 2022 year-to-date performance ballooned to +87.05%, a spectacular new high. The S&P 500 (SPY) is down -13.61% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +104.88%.

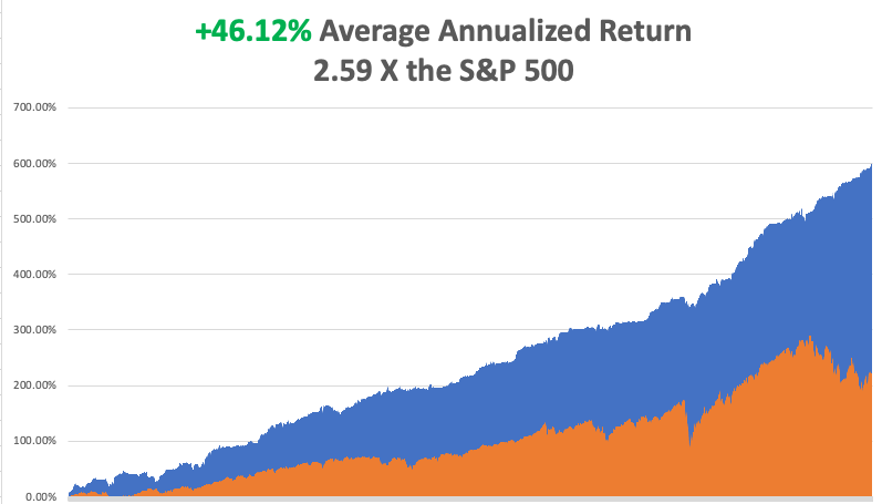

That brings my 14-year total return to +599.61%, some 2.60 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +46.12%, easily the highest in the industry.

I took profits in my triple weighting in bonds last week (TLT), booking some serious profits. All my remaining positions are profitable, shorts in (XOM), (OXY), (TSLA), (SPY), and one long in (TSLA), with 50% cash for a 30% net short position. We’ve just had a great run and the time to pay the piper is fast approaching.

With an +87.05% profit in hand this year, I don’t get a lot of complaints. However, I have been getting some lately because my trade alerts can be hard to get into.

Of course, it can be challenging to execute when 6,000 subscribers are trying to get into the same position at the same time. But when the entire world joins in, that raises the difficulty to a whole new level.

That is what happened with my trade alert to BUY the (TLT) on November 18. It was the trade alert around the world and the next day, bonds rocketed by $3.50. I laddered in with more positions with higher strike prices getting to a triple long in the bond market. When your trade alerts have a 95% success rate, that is what happens. It is the price of being right, which is better than the alternative.

When I first entered this trade, I thought the ten-year US Treasury yield would plunge from 4.46% to 2.50% by June 2023, taking the (TLT) from $91 to $120.

With the (TLT) at $108 on Friday and the ten-year yield at 3.50%, we are already halfway there. If I AM right and bond yields drop to 2.50%, the 30-year fixed mortgage rate will also drop below 4.00% and you can forget about any real estate crash. That's why the homebuilders (LEN), (KBH), and (PHM) are up 30%-40% since October.

With the ballistic moves in some Chinese stocks over the last two weeks (Alibaba (BABA) up 58%, Baidu ((BIDU) adding 47%, I have received a surge in inquiries about the prospects of the US going to war with the Middle Kingdom.

I have been asked this question continuously for the last 50 years, by several Presidents of the United States on down, and my answer is always the same.

There is not a chance.

The reason is very simple. The Chinese can’t feed themselves. They have not been able to do so for 100 years. With a population of 1.2 billion, the Chinese will never be able to feed themselves.

That means the Chinese are highly dependent on international trade to finance their food imports. When trade is vibrant, China prospers.

When it doesn’t, they start stacking up the bodies like cordwood for mass cremation, as happened when China suffered its last major famine. I know because I was there in the 1970s, and I’ll never forget that smell. As you quickly learn during a famine, there is no substitute for food.

So, what are the chances of China bombing their food supply? I’d say zero. A disruption of even a few months and people start to go hungry. Will they bluff, bluster, and obfuscate for domestic consumption? Every day of the year and that is what they are doing now.

As for buying Chinese stocks, I think I’ll pass for now. There are just too many great American ones on sale. The Chinese moves above are only taking place after horrific declines, 78% for (BABA), and 81% for (BIDU).

And before I go on to the data points, I want to recall a funny story.

One day in London 40 years ago, one of my junior traders at Morgan Stanley walked in with a big smile on his face. He had just gotten a great deal on a Ferrari Testarossa, which then retailed at $360,000, a lot of money for a 25-year-old East Ender in those days.

I thought to myself, “There are no great deals on Ferraris.”

A few months later, he totaled the Ferrari after a late night of binge drinking and racing on London’s damp streets, breaking the vehicle cleanly in half. The insurance company determined that his car was in fact two different Ferraris with two different VIN numbers that had been welded together. The car had split apart at the welds.

Some clever entrepreneur took the intact front end of a rear-ended car and the pristine back half of a car with destroyed hood and made one whole good Ferrari. Since my trader had only insured one car and not two, the insurance company refused to honor the claim.

All I can say is “Beware of friends bearing false Ferraris.”

Nonfarm Payroll Report Comes in Hot in November at 263,000, socking markets for 500 points. A December rate hike of 75 basis points has been firmly put back on the table. The Headline Unemployment Rate stays at a near-record high 3.7%. Average Hourly Earnings were up an inflationary 0.6%. Wages are up 5.1% YOY. The dollar soared on the prospect of higher rates for longer.

JOLTS Job Openings Report Comes in Weaker at 10.33 million in October, down 353,000 from September. High interest rates are finally taking their toll. There are still 1.7 job openings per applicant.

Key Inflation Read Drops, the Personal Consumption Expenditures Price Index falling 0.2% in October, excluding food and energy. It sets up a weak CPI on December 13, which would be very stock market positive.

Powell Turns Dovish, well, sort of, indicating that smaller interest rate hikes could start in December. The comments were made at a Brookings Institution meeting on Wednesday. Stocks rallied big on the news.

US to Ease Venezuela Sanctions, allowing Chevron to resume pumping there for six months after a three-year hiatus. It’s an out-of-the-blue big negative for oil prices. Venezuelan oil production has plunged from 2.1 million barrels a day to only 679, 000 thanks to gross mismanagement of the economy. But beggars can’t be choosers on the energy front. Good thing I’m running a double short in the sector. It’s the last think OPEC plus wanted to hear.

Don’t Expect a Housing Crash, as the financial system was vastly stronger than it was in 2008. A mild recession is already priced in, and bank balance sheets are rock solid. Buy the homebuilders on the next dips now coming off from horrific earnings, (KBH), (PHM), and (LEN).

Don’t Expect an iPhone 14 for Christmas, as pandemic-driven production shutdowns and Foxconn riots in China crimp supplies. It could be a longer wait if you want the new deep purple color. Avoid (AAPL) for now. I expect another big tech dive in 2023.

China Riots Tank Market, raising the specter of extended supply chain problems, especially for Apple (AAPL). Oil was especially hard hit as China is its largest buyer, hitting a two-year low and giving up all 2022 gains. China seems to be sacrificing its older generation, not giving them priority for vaccinations which don’t work anyway. This isn’t going away in a day. Transition to India will take a decade.

Case Shiller Plunges, the National Home Price Index Taking a 1.2% hit in September to 10.6%. Miami, Tampa, and Charlotte, NC showed the biggest YOY increases. You know the reasons why.

Home Rentals to Stay Sticky at Record Levels, with gains at 25-35% over the past 24 months. Homebuyers frozen out of the market by record-high interest rates are forced to rent at any price.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, December 5 at 8:00 AM EST, the ISM Nonmanufacturing PMI for November is out.

On Tuesday, December 6 at 8:30 AM, the Mad Hedge Traders & Investors Summit begins. Click here to register.

On Wednesday, December 7 at 7:30 AM, the Crude Oil Stocks are announced. It’s pearly Harbor Day.

On Thursday, December 8 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index for November.

On Friday, December 9 at 8:30 AM, the Producer Price Index for November. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, I am sitting here in front of the fire at my place in the Berkeley Hills and it is freezing cold and pouring rain outside. Heaven knows we need it.

I’m going to San Francisco later today to do some Christmas shopping. It’s not the ideal time but in my hopelessly busy schedule, this was the only day this year allocated for this chore.

For some reason, last night I recalled my days as an Ivy League Princeton professor, which I hadn’t thought about for decades.

When Morgan Stanley was a private partnership, before it went public in 1987, the firm represented the cream of the US establishment. There wasn’t anyone in business, industry, or politics you couldn’t reach through one of the company’s endless contacts. We referred to it as the “golden Rolodex.”

One day in the early 1980s, a managing director asked me a favor. Since he had landed me my job there, I couldn’t exactly say no. He had committed to teaching a graduate night class in International Economics at his alma mater, Princeton University, but a scheduling conflict had prevented him from doing so.

Since I was then the only Asian expert in the firm, could I take it over for him? If I had extra time to kill, I could always spend it in the Faculty Club.

I said “sure.”

So, the following Wednesday found me at Penn Station boarding a train for the leafy suburb about an hour away. On the way down, I passed the locations of several Revolutionary War battles. When we pulled into Princeton, I realized why they called these places “piles”. The gray stone ivy-covered structures looked like they had been there a thousand years.

My students were whip-smart, spoke several Asian languages, and asked a ton of questions. Many came from the elite families who owned and ran Asia. I understood why my boss took the gig.

I turned out to be pretty popular at the faculty Club, with several profs angling for jobs at Morgan Stanley. Rumors of the vast fortunes being made there had leaked out.

Princeton was weak in my field, DNA research. But as the last home of Albert Einstein, it was famously strong in math and physics. Many of the older guys had worked with the famed Berkeley professor, Robert Oppenheimer, on the Manhattan Project.

I was still a mathematician of some note those days, so someone asked me if I’d like to meet John Nash, the inventor of Game Theory, which won him a Nobel Prize in Economics in 1994. Nash’s work on partial differential equations became the basis for modern cryptography. I was then working on a model using Game Theory to predict the future of stock markets. It still works today and is the basis the Mad Hedge Market Timing Algorithm.

Weeks later found me driven to a remote converted farmhouse in the New Jersey countryside. On the way, I was warned that Nash was a bit “odd,” occasionally heard voices speaking to him, and rarely came to the university.

I later learned that his work in cryptography had driven him insane, given all the paranoia of the 1950s. Having worked in that area myself, that was easy to understand. His friends hoped that by arguing against his core theories, he would engage.

When I was introduced to him over a cup of tea, he just sat there passively. I realized that I was going to have to take the initiative so as a stock market participant, I immediately started attacking Game Theory. That woke him up and started the wheels spinning. It hadn’t occurred to him that game theory could be used to forecast stock prices.

His friends were thrilled.

I later went on to meet many Nobel Prize winners, as the Nobel Foundation was an early investor in my hedge fund. Whenever a member of the Swedish royal family comes to California, I get an invitation to lunch for the Golden State’s living Nobel laureates. It turns out that 20% of all the Nobel Prizes awarded since its inception live here. Last time, I sat next to Milton Friedman, and I argued against HIS theories.

The other thing I remembered about my Princeton days is my discovery of the “professor's dilemma.” Sometimes a drop-dead gorgeous grad student would offer to go home with me after class. I was happily married in those days with two kids on the way, so I respectfully declined, despite my low sales resistance.

No away games for me.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Nobel Prize

Global Market Comments

December 2, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(AMD), ($INDU), (TLT), (RCL), (VIX), (RIVN), (TSLA), (NVDA), (SLV), (GOLD), (USO), (XOM), (ALB), (SQM), (FMC), (CCI)

Below please find subscribers’ Q&A for the November 30 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: You keep mentioning December 13th as a date of some significance. Is this just because the number 13 is unlucky?

A: December 13th at 8:30 AM EST is when we get the next inflation report, and we could well get another 1% drop. Prices are slowing down absolutely across the board except for rent, which is still going up. Gasoline has come down substantially since the election (big surprise), which is a big help, and that could ignite the next leg up in the bull market for this year. So, that is why December 13 is important. And we could well flatline, do nothing, and take profits on all our positions before that happens, because whatever it is you will get a big move one way or another (and maybe both) on December 13.

Q: I’m a new subscriber, and I am intrigued by your structuring of options spreads. Why do you do debit spreads instead of credit spreads?

A: It’s really six of one and a half dozen of the other—the net profit is pretty much the same for either one. However, debit spreads are easier to understand than credit spreads. We have a lot of beginners coming into this service as well as a lot of seasoned old pros. And it’s easier to understand the concept of buying something and watching it go up than shorting something and watching it go down. Now, doing the credit spreads—shorting the put spread—gives you a slight advantage in that it creates cash which you can then use to meet margin requirements. However, it’s only a small amount of cash—only the potential profit in that position. And guess what? All the big hedge funds actually kind of like easy-to-understand trade alerts also, so that’s why we do them.

Q: I have a lot of exposure in NVIDIA (NVDA), so is it worth trading out of it and coming back in at a lower rate?

A: NVIDIA is one of the single most volatile stocks in the market—it’s just come up 50%. But it could well test the lower limits again because it is so volatile, and the chip industry itself is the most volatile business in the S&P 500. If your view is short-term, I would take profits now, and look to go back in next time we hit a low. If you’re long-term, don’t touch it, because NVIDIA will triple from here over the next 3 years. I should caution you that if you do try the short-term strategy, most people miss the bottom and end up paying more to get back into the stock; and that's the problem with all these highly volatility stocks like Tesla (TSLA), NVIDIA (NVDA) and Advanced Micro Devices (AMD) unless you’re a professional and you sit in front of a screen all day long.

Q: Would you buy now and step in to make it long-term?

A: I think we get a couple more runs at the lows myself. We won’t get to the old lows, but we may get close. Those are your big buying points for your favorite stocks and also for LEAPS. And I’m going to hold back on new LEAPS recommendations—we’ve done 12 in the last two months for the Concierge members, and maybe half of those went out to Global Trading Dispatch before they took off again. So, that would be my approach there.

Q: How much farther can the Fed raise interest rates until they reverse?

A: 1%-2%, unless they get taken over by the data—unless suddenly the economy starts to weaken so much that they panic and reverse like crazy. I think that's actually what’s going to happen, which is why we went hyper-aggressive in October on the long side, especially in bonds (TLT). You drop rates on the ten-year from 4.5% to 2.5% in six months—that’s an enormous move in the bond market. That is well worth running a triple long position in it; I think that’s what's going to happen. That’s where we will make out the first 30% in 2023.

Q: Should I short the cruise lines here, like Royal Caribbean (RCL)?

A: They do have their problems—they have massive debts they ran up to survive the pandemic when all the ships were mothballed, so it is an industry with its major issues. The stock has already doubled since the summer so I wouldn’t chase it up here. I’m not rushing to short anything here right now though unless it’s really liquid or has horrendous fundamentals like the oil industry, which everyone seems to love but I hate—right now the haters are winning for the short term, until December 16, which is all I care about.

Q: Is the diesel shortage going to affect farmers and all other industries like the chip?

A: As the economy slows down, you can expect shortages of everything to disappear, as well as all supply chain issues, which is a positive for the economy for the long term.

Q: What about the 2024 iShares 20 Plus Year Treasury Bond ETF (TLT) 95—is that not a trade?

A: That’s a one-year position with a 100% potential profit. That is worth running to expiration unless we get a huge 20-point move up in the next 3 months, which is possible, and then there won’t be anything left in the trade—you’ll have 95% of the profit in hand at which point you’ll want to sell it. So, with these one-year LEAPS or two-year LEAPS, run them one or two years unless the underlying suddenly goes up a lot, and then grab the money and run; that's what I always tell people to do. Because if you sell your position, they can’t take the money away from you with a market correction.

Q: Is the current US economy the best economy in the world?

A: It is. If you look at any other place in the world, it’s hard to find an economy that's in better shape, and it’s because we have the best management in the world and hyper-accelerating technology which everyone else begs and borrows. Or steals. People who are predicting zero return on stocks for 10 years are out of their minds. You don’t short the best economy in the world. If anything, technology is accelerating, and that will take the stock market with it in the next year or so.

Q: Do you see the Dow ($INDU) outperforming the other indexes until the Fed positive pivots?

A: Absolutely yes, because the S&P 500 (SPY) has a very heavy technology weighting and technology absolutely sucks right now. That would probably be a good 3-month trade—buy the Dow, and short the S&P 500 in equal amounts. Easy to do—you might pick up 10% on a market-neutral trade like that.

Q: Do you see a Christmas rally this year?

A: Actually, I do, but it won’t start until we get the next inflation report on December 13, at which point I'm going 100% cash. I’ve made enough money this year, and this is a problem I had when I ran my hedge fund: when you make too much money, nobody believes it, so there's really no point in making more than 50% or 60% a year because people think it’s fake. This is true in the newsletter business as well. Markets also have a nasty habit of completely reversing in January; this year, we had one up day in January, and then it was bombs away and we just piled on the shorts like crazy, so you have to wait for the market to first give you the fake move for the year, and then the real one after that. The best way to take advantage of that is to be 100% cash, and that’s why I usually do.

Q: What indicators do you see that give you the most confidence that inflation has peaked?

A: There's one big one, and that’s real estate. Real estate is absolutely in a recession right now and has the heaviest weighting of any individual industry in the inflation calculation. If anybody thinks house prices are going up, please send me an email and tell me where, because I’d love to know. The general feeling is they’re down 10-15% over the last six months. New homes are only being sold with massive buydowns in interest rates and free giveaways on upgrades. It is an industry that is essentially shut down, with interest rates having gone from 2.75% to 7.5% in a year, so there’s your deflation, but unfortunately, real estate is also the slowest to price in in the Fed’s inflation calculation, so we have to go through six months of torture until the Fed finally sees proof that inflation is falling. So, welcome to the stock market because it's just one of those factors. Just for fun, I got a quote on financing an investment property. The monthly payment would have been double for half the house that I already have.

Q: Are LEAPS a buy with the CBOE Volatility Index (VIX) this low?

A: No, you want to look at stocks first, and then the VIX; and with all the stocks sitting on top of 30-50% rises, it’s a horrible place to do LEAPS. LEAPS were an October play—we bought the bottom in a dozen LEAPS in October, and those were great trades, except for Tesla (TSLA) and Rivian (RIVN) which still have two years left to run. Up here, you’re basically waiting on a big selloff before you go into these one to two-year options positions.

Q: Why does Biden keep extending student loans? Will this catch up at some point?

A: He’s going to take it to the Supreme Court, and if he loses at the Supreme Court, which is likely, then he’ll probably give up on any loan extensions. At this point, the loan extensions on student loans are something like 2 or 2.5 years. The reason he’s doing this is to get 26 million people back into the economy. As long as you have giant student loan balances, you can’t get credit, you can’t get a credit card, you can’t buy a house, you can’t get a home loan. Bringing that many new people into the economy is a huge positive for not only them but for everyone else because it strengthens the economy. That has always been the logic behind forgiving student loans—and by the way, the United States is virtually the only country in the world that makes students pay back their loans after 30 or 40 years. The rest give college educations away either for free or give some interest-free break on repayments until they can get a salary-paying job.

Q: Does the budget deficit drop impact the stock market?

A: Yes, but it impacts the bond market first and in a much bigger way. That’s one of the reasons that bonds have rallied $13 points in six weeks because less government borrowing means lower interest rates—it’s just a matter of supply and demand. This has been the fastest deficit reduction since WWII, and markets will discount that.

Q: Will the US dollar (UUP) crash?

A: Yes, it will. You get rid of those high interest rates and all of a sudden nobody wants to own the US dollar, so we have great trades setting up here against everything, except maybe the Yuan where the lockdowns are a major drag.

Q: Is silver (SLV) a buy now?

A: No, it’s just had a big 10% move; I would wait for any kind of dip in silver and gold (GOLD) before you go into those trades. And when/if you do, there are better ways to do it.

Q: How is the Ukraine war going?

A: It’ll be over next year after Ukraine retakes Crimea, which they’ve already started to do. Russia is running out of ammunition, and so are we, by the way. However, the United States, as everybody learned in WWII, has an almost infinite ability to ramp up weapons production, whereas Russia does not. Russia is literally using up leftover ammunition from WWII, and when that’s gone, they’ve got nothing left, nor the ability to produce it in any sizable way. All good reasons to sell short oil companies ahead of a tsunami of Russian oil hitting the market. By the way, oil is now down for 2022.

Q: What's the number one short in oil (USO)?

A: The most expensive one, that would be Exxon Mobile (XOM).

Q: What’s going to happen to the markets in January?

A: After this Christmas rally peters out, I’m looking for profit-taking in January.

Q: When is a good time to buy debit spreads on oil?

A: Now. Look at every short play you can find out there; I just don’t see a massive spike up in oil prices ahead of a recession. And by the way, if the war in Ukraine ends and Russian oil comes back on the market, then you’re looking at oil easily below $50.

Q: What is the best way to invest in iShares Silver Trust (SLV) in the long term?

A: A two-year LEAP on the Silver (SLV) $25-$26 call spread—that gets you a 100%-200% return on that.

Q: Is lithium a good commodity trade?

A: Lithium will move in sync with the EV industry, which seems to have its own cycle of being popular and unpopular. We’re definitely in the unpopular phase right now. Long term demand for lithium will be increasing on literally hundreds of different fronts, so I would say yes, lithium is kind of the new copper. Look at Albemarle (ALB), Societe Chemica Y Minera de Chile (SQM), and FMC Corp. (FMC).

Q: If we do a LEAPS on Crown Castle Incorporated (CCI), you won’t get the dividend right?

A: No, you won’t, it’s a dividend-neutral trade because you’re long and short in a LEAPS. You have to buy the stock outright and become a registered shareholder to earn the dividend which, these days, is a hefty 4.50%. That said, if you’re looking for a high dividend stock-only play, buying the (CCI) down here is actually a great idea. For the stock-only players, this would be a really good one right now.

Q: Do you know people who are selling because of large capital gains?

A: The only people I know who are selling have giant tax bills to pay because of all the money they made trading options this year. I happen to know several thousand of those, as it turns out. So yes, I do know and that could affect the market in the next couple of weeks, which is why I went with the flatlined scenario for the next two weeks. Most tax-driven selling will be finished in the next two weeks, and after that, it kind of clears the decks for the markets to close on a high note at the end of the year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING or DISPATCH TECHNOLOGY LETTER as the case may be, then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 28, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LOOKING FOR BIG FOOT),

(NVDA), (VIX), (TLT), (TSLA), (XOM),

(OXY), (TSLA), (SPY), (MA), (V), (AXP)

On October 14, investors finally achieved the portfolios they long desired, not only individuals but institutional ones as well. They got rid of stocks and bonds that had been hobbling them all year and built their cash positions to decade highs.

What happened the next day?

Stocks and bonds went straight up for six weeks. Cash became trash.

For October 14 was the day that the stock market discounted the worst-case economic scenario for 2023, no matter how bad it may get. And it probably won’t get very bad. That’s barring a black swan-type event, like a brand-new global pandemic.

If you think your job can be frustrating, how about mine? If you run with the dumb crowd, the uninformed crowd, the loser crowd, you get your just desserts.

Fortunately, I saw these moves coming a mile off and loaded the boat. I’ve actually made more money on the parabolic move in bonds than some of the enormous moves in stocks. NVIDIA (NVDA) up 50%?

My performance in November has so far tacked on another robust +7.05%. My 2022 year-to-date performance ballooned to +82.42%, a spectacular new high. The S&P 500 (SPY) is down -16.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +94.61%.

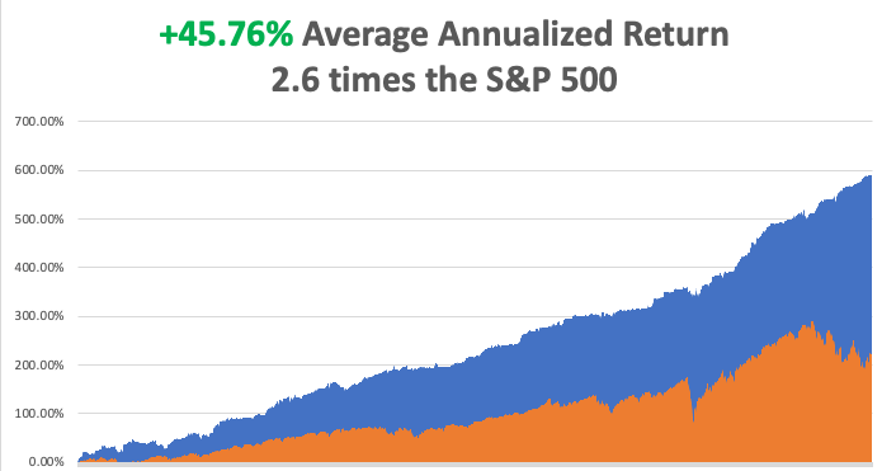

That brings my 14-year total return to +594.98%, some 2.60 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.76%, easily the highest in the industry.

I am going into the month-end surge with a fairly aggressive 40% long, (TLT), (TSLA), 40% short (XOM), (OXY), (TSLA), (SPY), with 20% crash for a totally market-neutral position. We’ve just had a heck of a run, and prices could well stall not far from here for the short term. The post-election rally happened, as predicted in this space.

Like Big Foot, the Yeti, and the Loch Ness Monster, the Fed pivot may soon actually make an appearance. I’m talking months, not years. That’s when our August central bank flips from the most severe tightening of interest rates in history, to a neutral, or one can only pray, an easing stance. This is what the 15% rally in stocks over the last six weeks has been all about.

And here is another old-time worn market nostrum. If investors sense that something is going to happen, they discount it fast, very fast.

Of course, there will be several false starts, denied rumors, and false flags, as there always are. After all, this is my 11th bear market. These will create sudden panic attacks, market selloffs, and Volatility Index (VIX) runs to $30 which are the license to print money for the Mad Hedge Fund Trader. Wait for the market to tell you when to trade. Ignoring it can prove expensive.

As we say here in the west, go off the reservation and you can get a lot of arrows stuck in your back.

How is this even remotely possible with the money supply only at $21.4 trillion, down 2% YOY? That’s a buzz cut from the +30% rate from a year ago.

The answer is that the money is out there, just hiding in different unrecognizable forms. Much of the $4 trillion in pandemic stimulus payments have yet to be spent. Inflation has added $2 trillion in new corporate profits through higher sales prices. Similarly, there is also another $1.5 trillion in pay increases bubbling through the system, also inspired by inflation.

You see this is booming credit card spending, much to the joy of Master Card (MA), Visa (V), and American Express (AXP) and their share price surges we have recently seen.

As I keep telling my Concierge customers on the phone, there is no playbook anymore. All the old ones have been rendered useless by the pandemic. To succeed and make windfall profits like me, you basically have to make it up as you go along.

The Fed Favors the Slowing of Rate Hikes, making a December increase of only 50 basis points a sure thing, according to minutes released on Wednesday for the prior meeting. Housing especially is taking a big hit. All interest rate plays, like bonds, rallied strongly.

Equities See Monster Inflows, some $23 billion in 35 weeks according to the Bank of America (BAC) flow of funds survey. There have been huge cash flows out of Europe looking for a stronger dollar, fleeing WWIII, and collapsing home currencies. The big chase is on. Time to go short? I am. It could be a big bull trap.

Leading Economic Indicators Dive, off 0.8% in October, double the decline expected and the weakest since the pandemic low in April 2020. There has only been one positive number in this data series in 2022. You have to go back to the financial crisis to find numbers this bad.

S&P Global Manufacturing PMI Takes a Hit in November, down to 47.6 from an estimate of 50. Services fell from 48 to 46.1. It’s another coincident recession indicator.

Existing Home Sales Plunge 5.9% in October to an annualized rate of 4.43 million units. It is the slowest sales pace in 11 years. It's not as bad as expected but is still down a horrific 28.4% YOY. Inventory fell to just 1.22 million units, only a 3.3-month supply, supporting prices in a major way. In fact, prices are still rising, up 6.6% annually to $379,100. Housing accounts for about 20% of the US economy, so here is your recession threat right here.

New Home Sales Come in Hot at 632,000, a real shocker with the 30-year fixed at 7.4%. Low-ball seller financing incentives must be a factor where they buy down rates to lower levels. Free upgrades, like those cherry wood cabinets, bonus rooms, and marble kitchen counters, also help. Prices are still up 15% YOY and inventories rose to a once unbelievable 8.9 months.

OPEC Plus Considering a 500,000 Barrels a Day Increase at their coming December meeting, which Saudi Arabia vehemently denied. The comments came out just as West Texas intermediate was barreling in on a new nine-month low. Saudi Arabia can talk all they want, but it’s tough to beat a coming recession, which every other hard asset class and commodity is now confirming.

Disney Axes Chairman, dumping Bob Chapek and bringing back Bob Iger from retirement. Losing $1.5 billion on the Disney Plus streaming service and losing its special tax status from the State of Florida has its costs. (DIS) is also not a stock to buy if we are going into recession. Avoid (DIS), despite the 10% move today. Let’s first see if Iger can cut costs.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 28 at 8:00 AM EST, the Dallas Fed Manufacturing Index for November is out.

On Tuesday, November 29 at 8:30 AM, the S&P Case Shiller National Home Price Index is released.

On Wednesday, November 30 at 8:30 AM, the ADP Private Employment Report for November is published. We also get a number on Q3 US GDP.

On Thursday, December 1 at 8:30 AM, the Weekly Jobless Claims are announced. US Personal Income and Spending for October is also out.

On Friday, December 2 at 8:30 AM, the Nonfarm Payroll Report for November is disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, by the 1980s, my mother was getting on in years. Fluent in Russian, she managed the CIA’s academic journal library from Silicon Valley, putting everything on microfilm.

That meant managing a team that translated over 1,000 monthly publications on topics as obscure as Artic plankton, deep space phenomenon, and advanced mathematics. She often called me to ascertain the value of some of her findings.

But her arthritis was getting to her, and all those trips to Washington DC were wearing her out. So I offered Mom a job. Write the Thomas family history, no matter how long it took. She worked on it for the rest of her life.

Dad’s side of the family was easy. He was traced to a small village called Monreale above the Sicilian port city of Palermo famed for its Byzantine church. Employing a local priest, she traced birth and death certificates going all the way back to an orphanage in 1820. It is likely he was a direct illegitimate descendant of Lord Nelson of Trafalgar.

Grandpa fled to the United States when his brother joined the Mafia in 1915. The most interesting thing she learned was that his first job in New York was working for Orville Wright at Wright Aero Engines (click here). That explains my family’s century-long fascination with aviation.

Grandpa became a tailer gunner on a biplane in WWI. My dad was a tail gunner on a B-17 flying out of Guadalcanal in WWII. As for me, you’ve all heard of plenty of my own flying stories, and there are many more to come.

My Mom’s side of the family was an entirely different story.

Her ancestors first arrived to found Boston, Massachusetts in 1630 during the second Pilgrim wave on a ship called the Pied Cow, steered by a Captain Ashley (click here).

I am a direct descendant of two of the Pilgrims executed for witchcraft in the Salem Witch Trials of 1692, Sarah Good and Sarah Osborne, where children’s dreams were accepted as evidence (click here). They were later acquitted.

When the Revolutionary War broke out in 1776, the original Captain John Thomas, who I am named after, served as George Washington’s quartermaster at Valley Forge responsible for supplying food to the Continental Army during the winter.

By the time Mom completed her research, she discovered 17 ancestors who fought in the War for Independence and she became the West Coast head of the Daughters of the American Revolution. It seems the government still owes us money from that event.

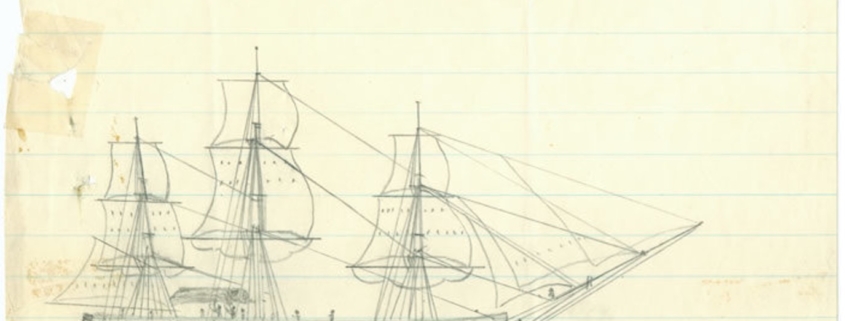

Fast forward to 1820 with the sailing of the whaling ship Essex from Nantucket, Massachusetts, the basis for Herman Melville’s 1851 novel Moby Dick. Our ancestor, a young sailor named Owen Coffin signed on for the two-year voyage, and his name “Coffin” appears in Moby Dick seven times.

In the South Pacific 2,000 miles west of South America, they harpooned a gigantic sperm whale. Enraged, the whale turned around and rammed the ship, sinking it. The men escaped to whaleboats. And here is where they made the fatal navigational errors that are taught in many survival courses today.

Captain Pollard could easily have just ridden the westward currents where they would have ended up in the Marquesas’ Islands in a few weeks. But these islands were known to be inhabited by cannibals, which the crew greatly feared. They also might have landed in the Pitcairn islands, where the mutineers from Captain Bligh’s HMS Bounty still lived. So the boats rowed east, exhausting the men.

At day 88, the men were starving and on the edge of death, so they drew lots to see who should live. Owen Coffin drew the black lot and was immediately shot and devoured. The next day, the men were rescued by the HMS Indian within sight of the coast of Chile, and returned to Nantucket by the USS Constellation.

Another Thomas ancestor, Lawson Thomas, was on the second whaleboat that was never seen again and presumed lost at sea. For more details about this incredible story, please click here.

When Captain Pollard died in 1870, the neighbors discovered a vast cache of stockpiled food in the attic. He had never recovered from his extended starvation.

Mom eventually traced the family to a French weaver 1,000 years ago. Our name is mentioned in England’s Domesday Book, a listing of all the land ownership in the country published in 1086 (click here). Mom died in 2018 at the age of 88, a very well-educated person.

There are many more stories to tell about my family’s storied past, and I will in future chapters. This week, being Thanksgiving, I thought it appropriate to mention our Pilgrim connection.

I have learned over the years that most Americans have history-making swashbuckling ancestors, but few bother to look.

I did.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Happy Thanksgiving from the Thomas Family

USS Essex

Global Market Comments

November 21, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SLOWING TO STALL SPEED),

(SPY), (TLT), (SLV), (WPH), (MAT), (NVDA), (MS), (GS)

I got a call from my daughter the other day, who is a Computer Science major at the University of California at Santa Cruz. The university was on strike and shut down, so she suddenly had a lot of free time on her hands.

The Teaching Assistants were only getting $12 an hour, which is not enough to live on in the San Francisco Bay Area by a mile. Some one-third were living in their cars, which can get chilly on the Northern California coast in winter.

Fast food workers in California will get $22 an hour from January, thanks to a bill passed in the recent election. The TAs, most of whom are working on master’s degrees and PhD’s in all kinds of advanced esoteric subjects, are simply asking to bring their pay in line with Taco Bell.

The entire UC system is on strike, affecting ten campuses, 17,000 TAs and 200,000 students. I have noticed that the most liberal universities often have the most draconian employment policies. It’s legalized slave labor. I speak from experience as a past victim, as I was once an impoverished work-study student at UCLA earning $1.00 an hour experimenting with highly radioactive chemicals.

What was my tuition for four years at the best public university in the world? Just $3,000, and I didn’t even pay that, as I was on a full scholarship, something about rocket engines I built when I was a kid. Werner Von Braun liked them. The 800 Math SAT score probably helped a tiny bit too.

UCSC is the feeder university for Silicon Valley. Graduates in Computer Science earn $150,000 a year out the door and $200,000 with a Master's degree. PhDs get offered founders’ stock in the hottest Silicon Valley startups.

I hope the TAs get their raise.

My daughter was calling me to apologize for her poor trading performance this year. I thought, “My goodness, did she just lose her entire college fund in some crypto scam?”

“How much did you lose,” I asked.

She answered that she didn’t lose anything and in fact was up 59% this year. She knew my performance was topping 78%, and that some subscribers had made up to 1,000%.

But she missed the October low because she had a midterm and was late on my (TLT) LEAPS because she was on a field trip. She promised to pay closer attention so she could earn the money to pay for her PhD.

My kids never ask me for money. If they need it, they just go into the markets and get it themselves. But then this is a family that discussed implied volatilities, chaos theory, and the merits of the Black Scholes equation over dinner every night. That’s what it’s like to have a hedge fund manager for a dad. Any extra money I have I give away to kids not as lucky as mine.

Then we talked about the most important issue of the day, how to cook the turkey this week. Brine, or no brine, with or without a T-shirt, or deep fat fry? She cautioned me to take it out of the freezer three days early to thaw. I bought my turkey a month ago because I knew prices would rise, and they have done so mightily. In case I get in over my head, I can always call the Butterball Thanksgiving Turkey Emergency Hotline at 844-877-3436.

But that’s just me.

Whenever making money gets too easy, I get nervous.

There’s a 90% chance we saw the bottom in this bear market on October 14. But how we proceed from here is the tricky part. Too much now depends on a single monthly data point, namely the Consumer Price Index, and that is a tough game to play. The next one is out on December 13.

The truth is that even with overnight interest rates at 4.75%-5.00% , the economy is holding up far better than anyone imagined possible. Some sectors, like financials, are positively booming. And while housing is weak, we really have not seen any major price falls that could threaten a financial crisis. Consumers are in good shape with savings near record levels.

There isn’t going to be a hard landing. There isn’t even going to be a soft landing. In fact, we may not have a landing at all, with the economy continuing to motor along, albeit at a slower rate just above stall speed.

Which begs me to repeat that the next new trend in interest rates will be down, and that this will be the principal driver of all your investment decisions going forward. Bonds may make the initial move up, as last week’s trade alerts suggested. But I have no doubt that equities will have a big move in 2023 as well.

Producer Price Index Fades, up only 0.2%, half of what was expected. That’s a big decline from 8.4% to 8.0% YOY. It’s another bell ringing that inflation has topped. Stocks rallied 500 on the news.

Bonds Continue on a Tear, with the (TLT) up a breathtaking eight points from the October low. It could reach $120 in 2023. Keep buying (TLT) calls, call spreads, and LEAPS on dips.

FTX Keeps Getting Worse, as it is looking like it’s a Bernie Madoff X 10, or an Enron X 20. A new CEO has been appointed by the bankruptcy court, John Ray, the former liquidator of Enron and a distant relative of mine. This will spoil investment in most digital coins and tokens for good, which are now worthless, and coins unless they are guaranteed by JP Morgan (JPM) or Goldman Sachs (GS). FTX never had a CFO, and Sam Bankman-Fried is blaming it all on his girlfriend, not exactly what creditors want to hear. In any case, Bitcoin has been replaced by Taylor Swift tickets.

A Massive Silver Shortage is Developing, with demand up 16% in 2023 to 1.21 million ounces. With EV production increasing from 1.5 million to 20 million units a year within the decade, its share of the market will rise from 5% to 75%. Solar panel demand is also rising. Buy (SLV) and (WPM) on dips. My next LEAPS will be for silver on the next dip.

NVIDIA Sales Rise, but profits dip, taking the stock up 3%. Games sales dropped a heartbreaking 50% and crypto took a big hit. The company expects $6 billion in sales in Q4 and is still operating at an incredible 53.6% gross margin. The company is creating a new line of dumbed-down products to comply with China export bans. Keep buying (NVDA) on dips. We caught a 50% move in the past month.

Retail Sales Rise 1.3% in October, causing analysts to raise Q4 GDP forecasts. Rising prices are a major factor. Where is that darn recession?

Who Has the World’s Worst Inflation? Not the US, where price gains have been relatively muted. Venezuela leads with 21,912%, followed by Zimbabwe at 2019%, Lebanon at 1071%, Argentina at 194%, Turkey at 124%. Even Russia is at 25%. Who has the lowest? Japan at 1.0%, but their currency has just collapsed by 40%.

The 60/40 Portfolio is Back, after a 15-year hiatus. JP Morgan Chase says that keeping 60% of your money in stocks and 40% in bonds should deliver a 7.2% annual return. I believe the balanced portfolio return will be much higher, as everything will go up in 2023 and fixed income is now yielding 5% or better. 2022 saw the worst 60/40 return in 100 years.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 21 at 8:00 AM, the Chicago Fed National Activity Index for October is out.

On Tuesday, November 22 at 8:30 AM, the Richard Fed Manufacturing Index is released.

On Wednesday, November 23 at 8:30 AM, Durable Goods for October is published. At 11:00 AM, the FOMC minutes from the previous meeting are out. Weekly Jobless Claims are announced. New Homes Sales for October are out.

On Thursday, November 24, Markets are closed for Thanksgiving.

On Friday, November 25, stock markets close early at 1:00 PM. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I have dated a lot of interesting women in my lifetime, but one who really stands out is Melody Knerr, the daughter of Richard Knerr, the founder of the famed novelty toy company Wham-O (click here). I dated her during my senior year in high school.

At six feet, she was the tallest girl in the school, and at 6’4” I was an obvious choice. After the senior prom and wearing my cheap rented tux, I took her to the Los Angeles opening night of the new musical Hair.

In the second act, the entire cast dropped their clothes onto the stage and stood there stark naked. The audience was stunned, shocked, embarrassed, and even gob-smacked. Fortunately, Melody never revealed the content of the play to her parents, or I would have been lynched.

In a recurring theme of my life, while Melody liked me, her mother liked me even more. That enabled me to learn the inside story of Wham-O, one of the great untold business stories of all time.

Richard Knerr started Wham-O in a South Pasadena garage in 1948. His first product was a slingshot, hence the company name, the sound you make when firing at a target. Business grew slowly, with Knerr trying and discarding several different toys.

Then in 1957, he borrowed an idea from an Australian bamboo exercise hoop, converted it to plastic, and called it the “Hula Hoop.” It instantly became the biggest toy fad of the 20th century, with Wham-O selling an eye-popping 25 million in just four months. By 1959, they had sold a staggering 100 million.

The Hula Hoop was an extremely simple toy to manufacture. You took a yard of cheap plastic tubing and stapled it together with an oak plug, and you were done. The markup was 1,000%. Knerr made tens of millions and bought a mansion in a Los Angeles suburb with a stuffed lion guarding his front door which he had shot in Africa.

The company made the decision to build another 50 million Hula Hoops. Then the bottom absolutely fell out of the Hula Hoop market. Midwestern ministers perceived a sexual connotation in the suggestive undulating motion to use it and decried it the work of the devil. Orders were cancelled en masse.

Whamo-O tried to stop their order for 50 million oak plugs, which were made in England, but to no avail. They had already shipped. So, to cut their losses Whamo-O ordered the entire shipment dumped overboard in the North Atlantic, where they still bob today. The company almost went bankrupt.

Knerr saved the company with another breakout toy, the Frisbee, a runaway success which is still sold today. Even Incline Village, Nevada has a Frisbee golf course. The US Army tested it as a potential flying hand grenade. That was followed by other monster hits like the Super Ball, the Slip N Slide, and the Slinky.

Richard Knerr sold his company to toy giant Mattel (MAT) for $80 million in 1994. He passed away in 2008 at the age of 82.

As for Melody, we lost touch over the years. The last I heard she was working at a dive bar in rural California. Apparently, I was the high point of her life. The last time I saw her I learned the harshest of all lessons, never go back and visit your old high school girlfriend. They never look that good again.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Hula Hoop Inventor Chuck Knerr

Global Market Comments

November 14, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TOP FIVE TECHNOLOGY STOCKS OF 2023),

(RIVN), (ROM), (ARKK), (PANW), (CRM), (FXE), (FXY), (FXA), (LEN), (KBH), (DHI), (TLT), (UUP), (META), (TSLA), (BA), (JNK), (HYG), (BRKB), (USO)

The year 2022 has been driven by rising interest rates, a strong dollar, a weak economy, a bear market in stocks.

A massive reversal is about to take place. 2023 will gain the benefit of gale force macroeconomic tailwinds for the right stocks.

So far this year, Mad Hedge earned an astounding 77.20% profit cashing in on this year’s trends. We could earn the same return taking advantage of next year’s trends.

If you want to ride along on my coattails next year, that is fine with me. But it requires you to take a leap of faith.

I refer you to the motto of Britain’s Special Air Service: “Qui audet adipiscitur,” or “Who dares wins.”

For it only makes sense that the worst stocks of 2022 will be the best performers of 2023.

I have no doubt that tech stocks will bottom out sometime in 2023. Those who get in early will build some of the largest fortunes of this century. Those who miss the boat will spend their retirement years working at Taco Bell.

The reasons are very simple.

*Ultra-high interest rates will force a mild recession in early 2023. Then suddenly, inflation will plummet. We know this has already started because the largest element in the inflation calculation is housing costs, which are in free fall.

*The Fed will panic and deliver 2023 the sharpest DECLINE in interest rates in American history.

*Plunging interest rates will bring a crash in the US dollar.

*Foreign currencies like the Euro (FXE), the Japanese Yen (FXY), and the Australian dollar (FXA) will soar.

*And guess who gets the bulk of their earnings from abroad, sometimes up to two-thirds? The technology industry.

Kaching!

If you think I’m out of my mind, just look at the top performers of the historic stock market rally last week.

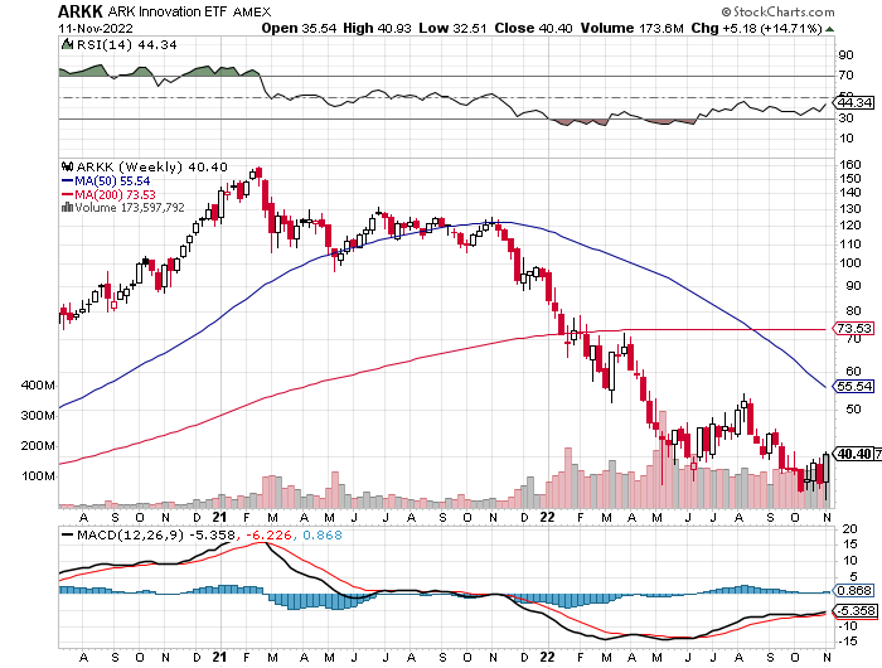

All the interest rate-sensitive sectors caught on fire. Technology stocks took off like a scalded cat, with Cathie Woods’ Ark Innovation Fund (ARKK) up an astounding 14% in a single day.

Bank shares soared. Homebuilders (LEN), (KBH), (DHI) caught a strong bid for the first time in ages. Junk bonds went bid only. US Treasury Bonds had their best day in 20 years (TLT), while the greenback (UUP) had its worst.

The bottom line here is so clear that I’ll write it on a wall for you. Falling interest rates will be the primary driver of stock prices for 2023 and 2024.

Of course, there is a better way to play this than buying the first technology index you stumble across.

So, let me boil this strategy down to just five names, close your eyes, and buy them.

Rivian (RIVN) – ($34) - Rivian is widely believed to be the next Tesla (TSLA). Some 25% owned by its largest customer, Amazon (AMZN), Rivian produces three types of EVs: the R1T pickup truck, the R1S SUV, and Amazon's EDV (electric delivery van). Its R1 vehicles start at under $70,000 and can travel more than 300 miles on a single charge. To learn more about Rivian, please click here.

To say that Rivian is the hot car of the day would be a vast understatement. New cars are trading for double list on the grey market. Owners complain of getting mobbed with gawkers whenever they hit the beach or the ski slopes. The buzz has led to an outstanding order book of an impressive 98,000, or four years of current production. The obvious cool factor allows enormous pricing power.

And here is the key to buying Rivian at this time. At 25,000, it is right at the mass production point where Tesla shares went ballistic all those years ago. And it already has an 80% decline in the price, in the rear-view mirror.

In 2024, Rivian plans to open its second plant in Georgia. After it fully expands its Illinois plant, it expects its annual production capacity to reach 600,000 vehicles.

Inflation Reduction Act passed this summer greatly accelerated rollout of the entire EV industry, which created a $7,500 per vehicle tax credit on top of state benefits.

Yes, this company offers venture capital-type risks. But it offers venture capital-type returns as well, up 10X-50X from here.

Ark Innovation Fund (ARKK) – ($40) – Cathie Woods’ high-tech fund was the proverbial red-headed stepchild of this bear market. It fell a gut-punching 80% from the 2021 top until last week. Just to get back to its old high, likely over the next five years, it has to rise by 400%. Its largest holdings are a real rollcall of the severely abused, Tesla (TSLA), Roku (ROKU), Exact Sciences (EXAS), Intellia (INTL), and Teladoc Health (TDOC), which Woods actively trades. But they are also a valuable insight into the future, EVs, CRISPR technology, robotic surgery, and molecular diagnostics. To learn more about the Ark Innovation Fund, please click here.

ProShares Ultra Technology ETF (ROM) – ($27) – This is a 2X long technology ETF that gives you an extremely aggressive position across the tech sector. It has 19% of its holdings in Apple (AAPL), 16% in Microsoft (MSFT), 10% in Alphabet (GOOGL) and Google (GOOG), at 3.5% in NVIDIA (NVDA), and 120 other smaller names. (ROM) shares are down a breathtaking 67% just in the past year. To learn more about the (ROM), please click here.

Palo Alto Networks (PANW) - $165 – Hacking is one of the fastest-growing sectors in technology, it is recession-proof and immune to the economic cycle. As a result, spending on the defense against hacking is absolutely exploding. Palo Alto Networks, Inc. is an American multinational cybersecurity company with headquarters in Santa Clara, California. Its core products are a platform that includes advanced firewalls and cloud-based offerings that extend those firewalls to cover other aspects of security. I have already earned a tenfold return over the past decade and expect to make another 10X in the coming years. You won’t find any dips in this stock as too many people are trying to get into it. To learn more about the Palo Alto Networks, please click here.

Salesforce (CRM) - $157 – The baby of tech genius Mark Benioff, this company is the dominant player in customer relationship management. If you want to do any business in the cloud, and almost all big companies do, you are up to your eyeballs in customer relationship management. Salesforce is the largest San Francisco-based cloud-oriented software company with virtually all of the Fortune 500 as its customer list. It provides customer relationship management software and applications focused on sales, customer service, marketing automation, analytics, and application development. Salesforce shares have been the target of a haymaker, down 55% in a year. To learn more about Salesforce, please click here.

You know what? I can do better than this.

I can create customized options LEAPS for you that will deliver a tenfold return on whatever performance these ultra-high beta stocks deliver. If the shares of one of my picks rise by 100%, you will make 1,000%.

This is an investment strategy that will enable you to retire early, real early. Tired of punching a time clock or logging into the next Zoom meeting on time?

Those will become a distant memory if you pursue my Mad Hedge Investment strategy for 2023.

As a result, my November month-to-date performance went off to the races, already achieving a hot +2.20%.

That leaves me with a very rare 100% cash position. With midterm election results out on Wednesday and the next report on the Consumer Price Index on Thursday, that sounds like a prudent place to be.

My 2022 year-to-date performance ballooned to +77.57%, a new high. The Dow Average is down -11.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +75.53%.

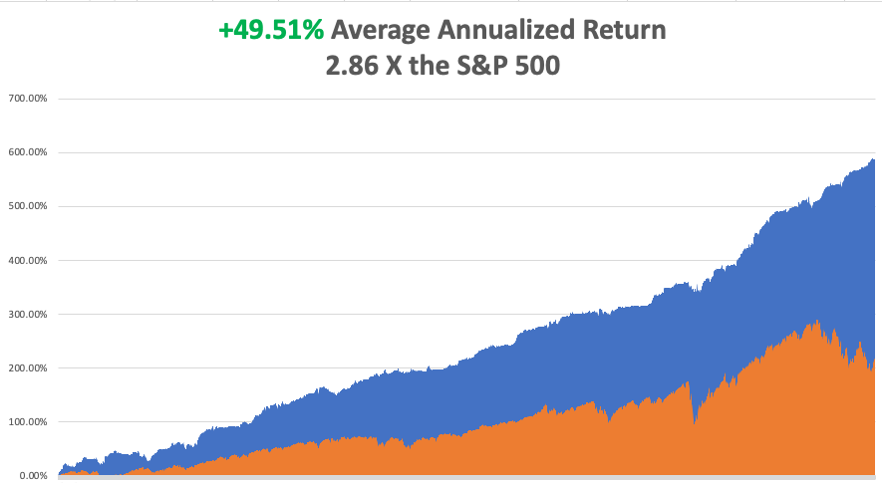

That brings my 14-year total return to +590.13%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +49.51%, easily the highest in the industry.

Bonds Clock Best Day in Years, taking the ten-year US Treasury bond fund up $3.64. All low interest rate plays had monster days. Junk bond ETFs (JNK) and (HYG) were up two points. 30-year fixed rate mortgages dropped 60 basis points to 6.60%, the biggest drop in history. Long bonds will be THE big trade of 2023.

US Dollar has Worst Day in 20 Years, driven by plunging interest rates. Big tech, which gets a major share from overseas sales, rocketed. Apple alone was up $12. Cathy Wood’s Ark Innovation Fund (ARKK) was up an incredible 14%. It vindicates my view that tech will turn when interest rates and the dollar fall.

Oil Companies (USO) Book Record $200 Million Profit this year, using the Ukraine War to double your cost of gasoline. If we have a recession next year, or the war ends, energy share prices should be peaking around here. Even if they don’t, the risk-reward here is terrible. It means we will have to pay a much higher price to decarbonize the economy at a later date.

Wells Fargo Gets Hit with $1 Billion Fine for its many regulatory transgressions over the last decade. Looting of customer accounts with bogus fees has been a recurring problem. Use any selloffs to buy (WFC) on dips.

Berkshire Hathaway's 20% Profit Increase YOY and buys back another $1 billion worth of stock. However, they did take a $10 billion loss on stocks in Q3 during the market meltdown. Keep buying (BRKB) stock and LEAPS on dips.

$1.5 trillion in Homeowners Equity Lost Since May, thanks to interest rates at 20-year high and a shrinking money supply. Since July, the median home price has dropped by $11,560. The average borrower has lost $30,000 in equity. It’s not a great time to rent either as prices there are soaring. Residential housing could remain weak for another 12-24 months, compared to the six-year drawdown we had from 2006.

Boeing Orders Rise in October, but deliveries fall. The company is finally out of the penalty box, up 40% since October 1. Don’t buy (BA) up here.

The Red Wave Fails to Show, with control of congress still too close to call. Republican House control has shrunk from an expected 60 seats six months ago to maybe two today. Donald Trump threw the election for his party, picking unelectable extremist candidates and campaigning where he wasn’t wanted. A pro-life Supreme Court brought out millions of women voters across the country. If the Republicans can’t win with inflation at 8.7%, they are toast in 2024 when it drops back down to 2%.

Market Dives 646 Points on Democratic Win, with technology stocks taking the biggest hit. The red wave no-show was a black swan traders were not looking for. Energy was the worst performing sector because they aren’t getting the air cover they paid for with a red wave. The result was much as I expected, which is why I went into November 8 with a rare 100% cash position waiting to buy the next low. It turns out that rights are more important than prices.

Elon Musk Sells More Tesla Shares and Warns of a Twitter Bankruptcy, some $3.9 billion worth, bringing this year’s total to $36 billion. Musk is raising money to head off a bankruptcy of Twitter now that major advertisers are fleeing en masse. This certainly is a distress sale. If Musk was looking to build a real business, re-tweeting fringe conspiracy theories was the worst thing he could have done. Endorsing the Republican party will cost him half of his customers. Is this Musk’s Waterloo, or his Dien Bien Phu?

Facebook to Lay Off 11,000, about 13% of its total employees. Zuckerberg admits the error of pushing the company into the metaverse too far too fast. With the stock down 77%, there are not a lot of happy campers at One Hacker Way. Avoid (META) for now, but it may be a 2023 play when we get closer to a new final product.

FTX Becomes an Epic Bankruptcy, with $9.5 billion missing from its balance sheet, in one of the biggest blowups of the crypto age. Losses are expected to reach $50-$60 billion, with the bankruptcy of 130 affiliated companies. It is also a potential Dept of Justice target. All affiliated tokens and coins have gone to zero. So, placing your money with a fresh-faced kid in the Bahamas wearing baggy shorts and with no financial background was not such a great idea after all. It’s amazing how many serious people were sucked in on this one. At least Sam Bankman-Fried said he was sorry.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 14 at 8:00 AM, the Consumer Inflation Expectations for October are released.

On Tuesday, November 15 at 8:30 AM, the Producer Price Index for October is released.

On Wednesday, November 16 at 8:30 AM, Retail Sales for October are published.

On Thursday, November 17 at 8:30 AM, Weekly Jobless Claims are announced. Housing Starts and Permits for October are also out.

On Friday, November 18 at 10:00 AM, the Housing Starts for October are printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I am often told that I am the most interesting man people ever met, sometimes daily. I had the good fortune to know someone far more interesting than myself.

When I was 14, I decided to start earning merit badges if I was ever going to become an Eagle Scout. I decided to start with an easy one, Reading Merit Badge, where you only had to read four books and write one review.

I was directed to Kent Cullers, a high school kid who had been blind since birth. During the late 1940s, the medical community thought it would be a great idea to give newborns pure oxygen. It was months before it was discovered that the procedure caused the clouding of corneas and total blindness. Kent was one of these kids.

It turned out that everyone in the troop already had Reading Merit Badge and that Kent had exhausted our supply of readers. Fresh meat was needed.

So, I rode my bicycle over to Kent’s house and started reading. It was all science fiction. America’s Space Program had ignited a science fiction boom and writers like Isaac Asimov, Jules Verne, Arthur C. Clark, and H.G. Welles were in huge demand. Star Trek came out the following year, in 1966. That was the year I became an Eagle Scout.

It only took a week for me to blow through the first four books. In the end, I read hundreds to Kent. Kent didn’t just listen to me read. He explained the implications of what I was reading (got to watch out for those non-carbon-based life forms).

Having listened to thousands of books on the subject, Kent gave me a first class education and I credit him with moving me towards a career in science. Kent is also the reason why I got an 800 SAT score in math.

When we got tired of reading, we played around with Kent’s radio. His dad was a physicist and had bought him a state-of-the-art high-powered short-wave radio. I always found Kent’s house from the 50-foot-tall radio antenna.

That led to another merit badge, one for Radio, where I had to transmit in Morse Code at five words a minute. Kent could do 50. On the badge below the Morse Code says “BSA.” In those days, when you made a new contact, you traded addresses and sent each other postcards.

Kent had postcards with colorful call signs from more than 100 countries plastered all over his wall. One of our regular correspondents was the president of the Palo Alto High School Radio Club, Steve Wozniak, who later went on to co-found Apple (AAPL) with Steve Jobs.

It was a sad day in 1999 when the US Navy retired Morse Code and replaced it with satellites. However, it is still used as beacon identifiers at US airfields.

Kent’s great ambition was to become an astronomer. I asked how he would become an astronomer when he couldn’t see anything. He responded that Galileo, the inventor of the telescope, was blind in his later years.

I replied, “good point”.

Kent went on to get a PhD in Physics from UC Berkely, no mean accomplishment. He lobbied heavily for the creation of SETI, or the Search for Extra Terrestrial Intelligence, once an arm of NASA. He became its first director in 1985 and worked there for 20 years.

In the 1987 movie Contact written by Carl Sagan and starring Jodie Foster, Kent’s character is played by Matthew McConaughey. The movie was filmed at the Very Large Array in western New Mexico. The algorithms Kent developed there are still in widespread use today.

Out here in the west aliens are a big deal, ever since that weather balloon crashed in Roswell, New Mexico in 1947. In fact, it was a spy balloon meant to overfly and photograph Russia, but it blew back on the US, thus its top secret status.

When people learn I used to work at Area 51, I am constantly asked if I have seen any spaceships. The road there, Nevada State Route 375, is called the Extra Terrestrial Highway. Who says we don’t have a sense of humor in Nevada?

After devoting his entire life to searching, Kent gave me the inside story on searching for aliens. We will never meet them but we will talk to them. That’s because the acceleration needed to get to a high enough speed to reach outer space would tear apart a human body. On the other hand, radio waves travel effortlessly at the speed of light.

Sadly, Kent passed away in 2021 at the age of 72. Kent, ever the optimist, had his body cryogenically frozen in Hawaii where he will remain until the technology evolves to wake him up. Minor planet 35056 Cullers is named in his honor.

There are no movies being made about my life…. yet. But there are a couple of scripts out there under development.

Watch this space.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

![]()

![]()