Global Market Comments

December 2, 2021

Fiat Lux

Featured Trade:

(A NOTE ON OPTIONS CALLED AWAY)

(GS), (TLT)

Global Market Comments

December 2, 2021

Fiat Lux

Featured Trade:

(A NOTE ON OPTIONS CALLED AWAY)

(GS), (TLT)

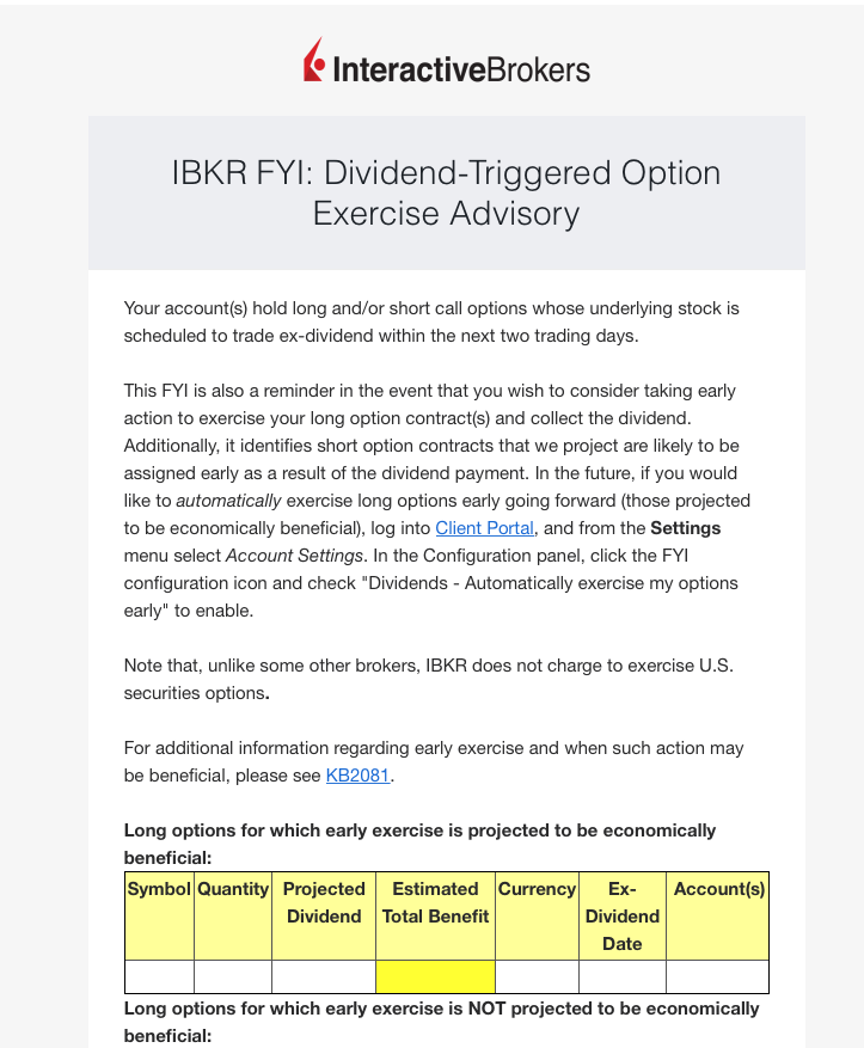

Goldman Sachs (GS) shares went ex-dividend yesterday, December 1 for a $2.00 quarterly dividend.

Anyone who has the (GS) December 2021 $340-$360 vertical bull call debit spread could potentially have their short positions in the $360 calls called away, or exercised against them by hedge fund seeking to capture the dividend.

Although the return for such a move is very small, some 0.51%, making this highly unlikely, it is not impossible. So it’s important to know how to handle these events.

If exercised, brokers are required by law to email you immediately and I know all of this may sound confusing at first. But once you get the hang of it, this is the greatest way to make money since sliced bread.

I call it the “Screw up risk.”

If it happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money vertical option spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker telling that your call options have been assigned away.

I’ll use the example of the Goldman (GS) $340-$360 in-the-money vertical BULL CALL spread.

For what the broker had done in effect is allow you to get out of your call spread position at the maximum profit point 12 days before the December 17 expiration date. In other words, what you bought for $16.00 on November 30 is now worth $20.00, giving you a near-instant profit $2,400, or 25.00% in 2 trading days!

All have to do is call your broker and instruct them to “exercise your long position in your (GS) December 17 $340 calls to close out your short position in the (GS) November 17 $360 calls.”

You must do this in person. Brokers are not allowed to exercise options automatically, on their own, without your expressed permission.

This is a perfectly hedged position, with both options having the same name and the same expiration date, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one options contract is exercisable into 100 shares.

Short positions usually only get called away for dividend-paying stocks or interest-paying ETFs like the (TLT). There are strategies out there that try to capture dividends the day before they are payable. Exercising an option is one way to do that.

Weird stuff like this happens in the run-up to options expirations like we have coming.

A call owner may need to buy a long (GS) position after the close, and exercising his long (GS) call is the only way to execute it.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there which may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to blow it by writing shoddy algorithms.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

There is a further annoying complication that leads to a lot of confusion. Lately, brokers have resorted to sending you warnings that exercises MIGHT happen to help mitigate their own legal liability.

They do this even when such an exercise has zero probability of happening, such as with a short call option in a LEAPS that has a year or more left until expiration. Just ignore these, or call your broker and ask them to explain.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

There may not even be an evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. In fact, I think I’m the last one they really did train.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Calling All Options!

Global Market Comments

December 1, 2021

Fiat Lux

Featured Trade:

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT SPREADS),

(TLT)

Global Market Comments

November 22, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WORST-CASE SCENARIO)

(BITO), (ETHE), (TLT), (TBT), (NVDA), (DE)

In the investment business, you’re only as good as your last trade. If that is the case, that makes me a pretty worthless person in the wake of a record four stop-losses at the November 19 option expiration.

Days before, the market closed with all ten of our positions profitable. But the pandemic lockdown in Austria on Friday morning shattered those plans. Fears of a new Covid wave and another mini-recession send bonds soaring and interest rates crashing. That trashed financial stocks, where I had a heavy exposure.

If you work in the business long enough, you see a black swan on an options expiration day every five or ten years. This was our turn. As a result, we traded a double-digit gain for November for a moderate loss. That still leaves us with a heroic 80% gain for 2021 and 15 consecutive profitable months.

There is nothing to do but pick yourself up, dust yourself off, and go on to the next trade. I wouldn’t be surprised to see all of the Friday losses reversed in the coming weeks. Banks are still outrageously profitable and the cheapest sector in the market. If you have a six-month to one-year view, the action on Friday changed nothing.

You live by the sword, you die by the sword.

There was a lot going on Friday than just another Covid wave. November option expirations used to be a snore. But this year, brokerage firms have stampeded so many retail investors into the options markets where they make the most money that they have become major events.

Some 70% of all options trading now takes place in securities with less than two weeks to expiration. In the meantime, professional traders limit their personal accounts to long term LEAPS which are the subject of the Mad Hedge Concierge Service. Instead of rolling the dice for a 10% profit in a month, you get a very safe 100% return in a year.

Of course, while financials were getting wrecked, falling interest rates were acting as a steroid for tech stocks. (MSFT) and Google (GOOG) hit new highs for the year. Concierge members in my (ROM) LEAPS were rolling in clover.

The barbell strategy wins again!

Infrastructure Bill is signed on Monday, injecting another $1.2 trillion into the economy today. This assured the economy will keep booming through 2024. The bond market hates it, down $6.00 in three days. It adds another 3% to GDP over the next five years. Keep selling (TLT) on rallies.

Bitcoin Forks for the first some since 2017, making it much more competitive with Ethereum. It enables the lead crypto to use defi and third party apps. Miner Marathon (MARA) is raising a $500 million bond issue to buy Bitcoin. Keep buying (BITO) and (ETHE) on dips.

US Retail Sales roar, up 1.7% in October compared to 0.8% in September, far more than expected. Receipts for all items are rising. Higher wages are immediately translating into increased spending.

Builder Sentiment jumps, up 3 points to 83, according to the National Association of Homebuilders. A decade-long structural shortage of housing is a huge tailwind. Good luck hiring a contractor right now. The Midwest and the south are the leaders in demand.

Dollar hits 16-Month High, on the strength of yesterday’s red hot Retail Sales. It means higher interest rates soon, which is great for the buck. Currencies with the fastest rising interest rates are always the strongest.

NVIDIA kills it, with revenues up 50% YOY and earnings up 60%. It’s well on the way to becoming the next trillion-dollar company. It’s another Mad Hedge 20 bagger. Buy (NVDA) on dips.

Biden may try an SPR Release to cap gasoline prices. There are 741 barrels in the Strategic Petroleum Reserve, enough for 21 days of US consumption. It’s sitting there costing money, essentially a government subsidiary for the energy industry. Why have it if the US is now a net energy exporter? The concern has been enough to drop oil prices by 10%.

Rents for single-family homes are up 10.2% YOY, and will continue to rise. Miami has the highest rent inflation in the country, and the highest-priced homes are seeing the fastest increases.

Weekly Jobless Claims drop to new post-pandemic low, to 268,000, just fractionally. There are 2 million continuing claims. The great resignation continues.

John Deere strike ends, with some of the best terms for workers in 40 years. It cost the company $2.5 billion. They get an immediate 10% raise and $7,500 bonus, larger out-year raises, and big performance bonuses. There is a lot of making up for 30 years of no real wage growth going on here. It points a loaded gun at the head of the “transitory” argument for inflation. Buy (DE) on dips.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the disastrous November options expiration, my November month-to-date performance plunged to -7.73%. My 2021 year-to-date performance took a haircut to 80.82%. The Dow Average is up 16.34% so far in 2021.

My entire portfolio expired on Friday, and I am 100% in cash. Of our ten positions, six made money and four lost. In addition, subscribers to the Mad Hedge Technology letter had another five winners, as tech stocks are still on a tear.

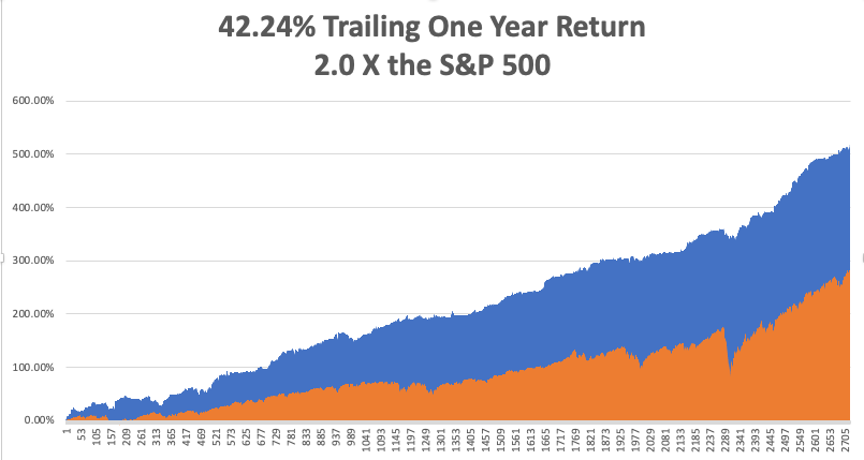

That brings my 12-year total return to 503.37%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 42.24%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 96.56%. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 48 million and rising quickly and deaths topping 772,000, which you can find here at https://coronavirus.jhu.edu.

The coming week will be all about the inflation numbers.

On Monday, November 22 at 7:00 AM, Existing Homes Sales for October are released.

On Tuesday, November 23 at 6.45 AM, the Flash Manufacturing PMI is announced.

On Wednesday, November 24 at 5:30 AM, US Q3 GDP second estimate is published. At 7:00 AM we get New Home Sales for October. Minutes from the last Fed meeting are printed at 2:00 PM.

On Thursday, November 25 markets are closed for Thanksgiving Day.

On Friday, November 26 at 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, when I was shopping for a Norwegian Fiord cruise for next summer, each stop was familiar to me because a close friend had blown up bridges in every one of them.

During the 1970s at the height of the Cold War, my late wife Kyoko flew a monthly round trip from Moscow to Tokyo as a British Airways stewardess. As she was checking out of her Moscow hotel, someone rushed at her and threw a bundled typed manuscript that hit her in the chest.

Seconds later a half dozen KGB agents dog-piled on top of her. It turned out that a dissident was trying to get Kyoko to smuggle a banned book to the West and she was arrested as a co-conspirator and bundled away to Lubyanka Prison.

I learned of this when the senior KGB agent for Japan contacted me, who had attended my wedding the year before. He said he could get her released, but only if I turned over a top-secret CIA analysis of the Russian oil industry.

At a loss for what to do, I went to the US Embassy to meet with ambassador Mike Mansfield, who as The Economist correspondent in Tokyo I knew well. He said he couldn’t help me as Kyoko was a Japanese national, but he knew someone who could. Then in walked William Colby, head of the CIA.

Colby was a legend in intelligence circles. After leading the French resistance with the OSS, he was parachuted into Norway with orders to disable the railway system. Hiding in the mountains during the day, he led a team of Norwegian freedom fighters who laid waste to the entire rail system from Tromso all the way down to Oslo. He thus bottled up 300,000 German troops, preventing them from retreating home to defend themselves from an allied invasion.

During the Vietnam war, Colby became notorious for running the Phoenix assassination program.

I asked Colby what to do about the Soviet request. He replied, “give it to them.” Taken aback, I asked how. He replied, “I’ll give you a copy.” Mansfield was my witness so I could never be arrested for being a turncoat. Copy in hand, I turned it over to my KGB friend, and Kyoko was released the next day and put on the next flight out of the country. She never took a Moscow flight again.

I learned that the report predicted that the Russian oil industry, its largest source of foreign exchange, was on the verge of collapse. Only massive investment in modern western drilling technology could save it. This prompted Russia to sign deals with American oil service companies worth hundreds of millions of dollars.

Ten years later, I ran into Colby at a Washington event, and I reminded him of the incident. He confided in me “You know that report was completely fake, don’t you?” I was stunned. The goal was to drive the Soviet Union to the bargaining table to dial down the Cold War. I was the unwitting middleman. It worked. That was Bill, always playing the long game.

After Colby retired, he campaigned for nuclear disarmament and gun control. He died in a canoe accident in the lake near his Maryland home in 1996.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 17, 2021

Fiat Lux

Featured Trade:

(HOW TO HANDLE THE FRIDAY, NOVEMBER 19 OPTIONS EXPIRATION),

(GS), (MS), (BAC), (TLT), (ROM), (BRKB)

Happy and newly enriched followers of the Mad Hedge Fund Trader Alert Service have the good fortune to own a record ten deep-in-the-money options positions that expire on Friday, November 19 at the stock market close in two days.

I have to admit that I traded like a Wildman this month, pedal to the metal, and 100% invested. This will take our 2021 year-to-date performance to over 100% for the first time in our 14-year history. I like to think that is the end result of my 53 years of investment in researching trading strategies.

Sometimes, overconfidence works.

It is therefore time to explain to the newbies how to best maximize their profits.

These involve the:

(GS) 11/$330-$350 call spread 10.00%

(GS) 11/$385-$395 call spread 10.00%

(MS) 11/$85-$90 call spread 10.00%

(MS) 11/$95-$98 call spread 10.00%

(BAC) 11/$37-$40 call spread 10.00%

(BAC) 11/$43-$46 call spread 10.00%

(TLT) 11/$150-$153 put spread 10.00%

(ROM) 11/$105-$110 call spread 10.00%

(BRKB) 11/$275-$280 call spread 10.00%

(BRKB) 11/$277.50-$282.50 call spread 10.00%

Provided that we don’t have another 2,000-point move down in the market in the next two days, these positions should expire at their maximum profit points.

So far, so good.

I’ll do the math for you on our deepest in-the-money position, the Goldman Sachs (GS) November 19 $330-$350 vertical bull call spread, which I almost certainly will run into expiration. Your profit can be calculated as follows:

Profit: $20.00 expiration value - $16.50 cost = $3.50 net profit

(6 contracts X 100 contracts per option X $3.50 profit per options)

= $2,100 or 17.65% in 24 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning November 22 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and make your broker find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration on Friday, November 19. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

Well done, and on to the next trade.

You Can’t Do Enough Research

Global Market Comments

November 16, 2021

Fiat Lux

Featured Trade:

(A NOTE ON OPTIONS CALLED AWAY)

(GS), (TLT)

Global Market Comments

November 15, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or PROFITING FROM INFLATION),

($INDU), (TLT), (TBT), (MS), (GS), (BAC), (BRKB), (TSLA)

Worried about inflation?

I’m not. That’s because I know how to trade inflation, which we had in spades during the 1970s when it reached a horrific 18% rate. Those who figured out the game early made fortunes. Those who didn’t got killed.

And what is the best protection against inflation? You own stocks and homes, as much as you can get your hands on.

That’s because in an inflationary environment, companies can raise their prices faster than the inflation rate, which they have been doing since the summer. That’s why we have just seen the best earnings quarter in recent memory and all-time high stock indexes.

Homes do well because there are still 85 million millennials chasing a housing stock that is easily short ten million homes and are given free money to chase prices upward.

I asked a local real estate agent when home prices would slow down and she answered, “it might slow down on Christmas eve and Christmas day, and after that, it will take off again.”

I think home prices will continue to rise for another decade, but not at this year’s ballistic rate.

What about impending rising interest rate, you may ask? They will rise but not enough to hurt either stocks or homes. The pandemic vastly accelerated technology, which we all know is the greatest price destroyer of all time. So, inflation will go up, but from zero to 3%-4%, not the 18% of yore.

And yes, prices are rising for the working classes, those least able to pay them. But the same minimum wage workers are getting the biggest pay hikes in history, up to 100% in some cases, more than offsetting inflation.

And while stocks and homes see rising inflation, bonds don’t. My feeling is that the bond market will stumble across it in the dark some nights and prices will crash. Bonds will keep ignoring inflation until they can’t. The bond vigilantes will then return with a vengeance and are doing their stretching exercises as we speak.

One of the odder things about the past week is that each of the three announcements heralding sharply higher inflation trigger sharp moves up in bonds when they were supposed to go down. That worked until Thursday when the worst 30-year Treasury bond auction since 1990 prompted a $5.00 selloff.

Another bizarre development is that call options are trading at greater premiums than put options, an exceedingly rare event. That means that the consensus for stocks is now almost universally up.

It also means that the at-the-money long-dated LEAPS call option spreads I have been pelting my Concierge members with have become massively profitable. Six months out you can earn eye-popping 100% returns, and 200% in some of the more volatile names, like (ROM) and (MSTR).

The bottom line is that goldilocks is moving in for the long term and might advance to senior citizenship on this watch.

That works for me, so I’m going on a long hike.

The $1.2 Trillion Infrastructure Budget Passes, adding another 6% in GDP growth for the next two years. Construction detours are about to break out all over the country, and the domestic recovery play is on fire. Lost along the way was $550 million in social spending. No increase in corporate taxes sets up a perfect storm for stocks the next several months. Stay fully invested as I begged you to do weeks ago.

The US Reopens, provided you have two Covid shots and a test within the last three days. Got to keep those pesky diseased foreigners out! Hotels, airlines, casinos, and cruise lines took off like a scalded chimp, taking the indexes to new all-time highs. Buy (ALK) and (LUV) on dips.

The Bitcoin Rally Continues, with new all-time highs for both (BITO) and (ETHE). Concerns about the monetary health of the US are rising ahead of a major debt ceiling fight in Congress in December.

Inflation Soars with a Red Hot 6.2% CPI Print in October, the highest in 31 years. Energy, rent, and car costs led the gains. Bitcoin (BITO) and Ethereum (ETHE) jumped to new all-time highs in response. This is only going to get better. You can now count on a Fed interest rate hike in June.

The Disappearing Worker Trend Continues, with a record 4.4 million quitting in September. Workers are taking advantage of the labor shortage to switch jobs for higher wages. This will get worse before it gets better. Good luck trying to hire anyone.

US Consumer Sentiment Hits Ten-Year Low, down from 71.7 to 68.6 in October, according to the University of Michigan. Inflation at a 30-year high 6.2% is starting to hit consumers hard.

Elon Musk Tesla Sales Top $5.1 billion, to pay off Uncle Sam. That must be one hell of a tax bill. At this rate, the market is rapidly running out of the sole seller. Buy (TSLA) on dips.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a massive +8.95% gain in October, followed by a decent 4.42% so far in November. My 2021 year-to-date performance moved to a new high of 92.97%. The Dow Average is up 18.00% so far in 2021.

After the recent ballistic move in the market, we got a week of consolidation which brought some generalized bitching, moaning, and wining.

I am continuing to run my longs in. Those include (MS), (GS), (BAC), (BRKB), and a short in the (TLT). The (TLT) short brought some hair-raising moments when we got a $3.00 spike up in the wake of the red hot 6.2% CPI release. I knew it was a complete BS move and successfully stared it down, watching it all reverse the next day. I don’t do this very often.

All positions are now approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 4 trading days and capture all the accelerated time decay.

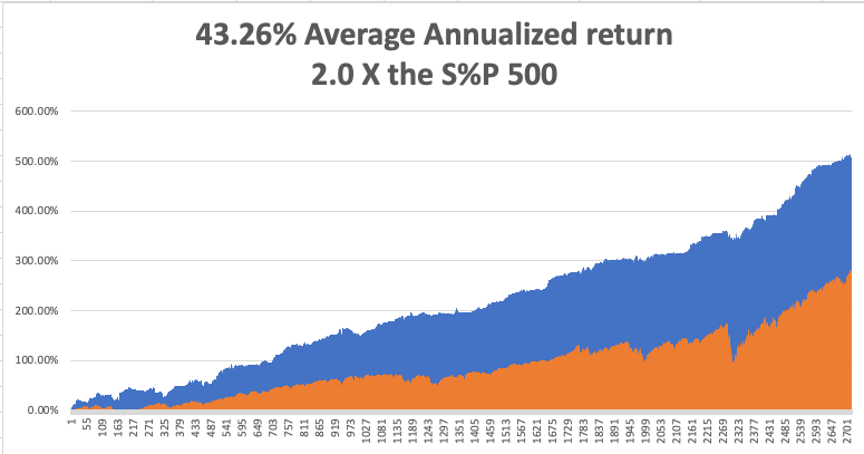

That brings my 12-year total return to 515.52%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 43.26%, easily the highest in the industry.

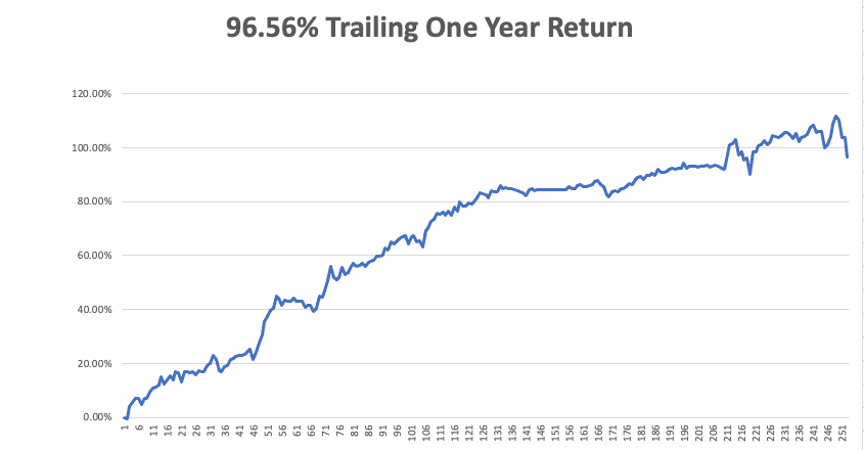

My trailing one-year return popped back to positively eye-popping 112.08%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 47 million and rising quickly and deaths topping 763,000, which you can find here.

The coming week will be all about the inflation numbers.

On Monday, November 15 at 9:00 AM, the New York Empire State Manufacturing Index for November is released. WeWork reports.

On Tuesday, November 16 at 8:30 AM, US Retail Sales for October are printed. Home Depot (HD) and Walmart (WMT) report.

On Wednesday, November 17 at 8:30 AM, the Housing Starts and Building Permits for October are published. NVIDIA (NVDA) and Cisco Systems (CSCO) report.

On Thursday, November 18 at 8:30 AM, Weekly Jobless Claims are announced. The Philadelphia Fed Manufacturing Index is printed. Macy's (M) and Alibaba (BABA) report.

On Friday, November 19 at 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, I am sitting in the Centurion Lounge in San Francisco Airport waiting for a United flight to Las Vegas where I have to speak at an investment conference. I have time to kill so I will reach back into the deep dark year of 1968 in Sweden.

My trip to Europe was supposed to limit me to staying with a family friend, Pat, in Brighton, England for the summer. His family lived in impoverished council housing.

I remember that you had to put a ten pence coin into the hot water heater for a shower, which inevitably ran out when you were fully soaped up. The trick was to insert another ten pence without getting soap in your eyes.

After a week there, we decided the gravel beach and the games arcade on Brighton Pier were pretty boring, so we decided to hitchhike to Paris.

Once there, Pat met a beautiful English girl named Sandy, and they both took off for some obscure Greek island, the ultimate destination if you lived in a cold, foggy country.

That left me stranded in Paris.

So, I hitchhiked to Sweden to meet up with a girl I had run into while she was studying English in Brighton. It was a long trip north of Stockholm, but I eventually made it.

When I finally arrived, I was met at the front door by her boyfriend, a 6’6” Swedish weightlifter. That night found me bedding down in a birch forest in my sleeping bag to ward off the mosquitoes which hovered in clouds.

I started hitchhiking to Berlin, Germany the next day. I was picked up by Ronny Carlson in a beat-up white Volkswagen bug to make the all-night drive to Goteborg where I could catch the ferry to Denmark.

1968 was the year that Sweden switched from driving English style on the left to the right. There were signs every few miles with a big letter “H”, which stood for “hurger”, or right. The problem was that after 11:00 PM, everyone in the country was drunk and forgot what side of the road to drive on.

Two guys on a motorcycle driving at least 80 pulled out to pass a semi-truck on a curve and slammed head on to us, then were thrown under the wheels of the semi. The driver was killed instantly, and his passenger had both legs cut off at the knees.

As for me, our front left wheel was sheared off and we shot off the mountain road, rolled a few times, and was stopped by this enormous pine tree.

The motorcycle riders got the two spots in the only ambulance. A police car took me to a hospital in Goteborg and whenever we hit a bump in the road, bolts of pain shot across my chest and neck.

I woke up in the hospital the next day, with a compound fracture of my neck, a dislocated collar bone, and paralyzed from the waist down. The hospital called my mom after booking the call 16 hours in advance and told me I might never walk again. She later told me it was the worst day of her life.

Tall blonde Swedish nurses gave me sponge baths and delighted in teaching me to say Swedish swear words and then laughing uproariously when I made the attempt.

Sweden had a National Healthcare system then called Scandia, so it was all free.

Decades later, a Marine Corp post-traumatic stress psychiatrist told me that this is where I obtained my obsession with tall, blond women with foreign accents.

I thought everyone had that problem.

I ended up spending a month there. The TV was only in Swedish, and after an extensive search, they turned up only one book in English, Madame Bovary. I read it four times but still don’t get the ending.

The only problem was sleeping because I had to share my room with the guy who lost his legs in the accident. He screamed all night because they wouldn’t give him any morphine.

When I was released, Ronny picked me up and I ended up spending another week at his home, sailing off the Swedish west coast. Then I took off for Berlin to get a job since I was broke.

I ended up recovering completely. But to this day whenever I buy a new Brioni suit in Milan, they have to measure me twice because the numbers come out so odd. My bones never returned to their pre-accident position and my right arm is an inch longer than my left. The compound fracture still shows upon X-rays.

And I still have this obsession with tall, blond women with foreign accents.

Go figure.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Brighton 1968

Ronny Carlson in Sweden