Below please find subscribers’ Q&A for the September 22 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: When’s the United States US Treasury bond fund (TLT) going to go down?

A: When J. Powell tapers, which will be either today or in 6 weeks. That's the time frame we’re looking at now, and people are positioning now for the taper—that's why financials are taking off like a rocket. Buy those financials and don't expect too much from your tech stocks for the next few months.

Q: What do you think of adding corporate or municipal bonds to my portfolio?

A: Don’t do that on pain of death please; you will lose money. Corporate bonds will get slaughtered the second interest rates turn because they have the most exposure from a credit point of view to any downgrades resulting from rising interest rates. Better to keep your money in cash than buy bonds here. It was a great idea 10 years ago, but a terrible idea today. Just buy cash or buy extremely deep-in-the-money LEAPS which will get you a 10-20% per year return.

Q: What are the chances that the government defaults?

A: Zero, because corporate profits this year will increase from $2 trillion to $10 trillion, spinning off massive tax revenues for the government. The deficit will come down substantially in the future as a result. Keep expecting upwards surprises in profits and taxable revenues. That may be why the (TLT) is staying so high.

Q: I need a customized LEAPS on a stock.

A: We do those for our concierge customers. If you’re interested, then email Filomena at customer support at support@madhedgefundtrader.com.

Q: What brand of shot did you get?

A: Pfizer (PFE).

Q: The Government is showing no sign of balancing a budget and the hole will only get deeper; what are your thoughts?

A: I agree, and that’s why I'm short the (TLT). All we need is a taper to really get some juice under that trade; we really don’t need that much. Ten-year US Treasury yields are now around 1.30% and we only need the yield to get up to about 1.70% for us to make a maximum profit on our positions. One taper hint and it could get us up to those levels.

Q: Why is Visa (V) dropping so much?

A: Fear of being replaced by Bitcoin. This is the big thing dragging all three credit card companies down, including American Express (AXP) and master Card (MA). That's why I have not added a Visa position among my financials in this go around.

Q: How can the Fed unwind their balance sheet and normalize interest rates to a historical average of 4-5%?

A: Quite easily: quit buying bonds. They’re still buying $120 billion/month worth. Technology has accelerated with the pandemic and we all know this is highly deflationary. I expect the next peak in interest rates to be only 3% or 3.5%, not the 6% we saw in the last peak in interest rates in the 2000s. So yeah, bonds are going to go down but not back to 2000’s level.

Q: Thoughts on the Johnson & Johnson (JNJ) shot?

A: No thank you. If you get to choose, Moderna (MRNA) is now producing the best immunity data on a year-to-date basis if you’re starting out from scratch. Some people are mixing, they start out with Pfizer and then get Moderna. They get a worse reaction because the Moderna initial reaction shot sees the Pfizer vaccine as a new virus, so you may get a small flu as a result of that.

Q: What is the put spread you’re recommending on the TLT?

A: The May 2022 $150-$155 vertical put spread. That is the sweet spot now on the short side on (TLT) LEAPS. You should earn a 115% profit in eight months on this trade if interest rates remain unchanged or fall.

Q: Do you expect the ProShares Ultra Short 20 year+ Treasury ETF (TBT) to make it to $20 this year?

A: Yes, I do; $16 to $20 isn’t that much of a move. Remember, the (TBT) is a two times short ETF.

Q: Are you recommending bank stocks?

A: Yes, Morgan Stanley (MS) and JP Morgan (JPM) are two of the best. They will lead the yearend rally starting from here.

Q: When do you expect the semiconductor shortage to end?

A: End of next year, or maybe even 2023, because what all the analysts keep underestimating is that the end of shortages is based on companies getting the chips they want today. The actual issue is that companies are designing billions of chips into their products at an exponential rate, and what they’ll need in a year from now is far higher than most people realize. The semiconductor shortage is much more structural than people realize—that's my theory. They don’t throw up a $2 billion fab overnight. So, this will keep going on for a while and be a drag on economic growth.

Q: Are you sure we won’t see $100 oil (USO)?

A: With oil, you're never sure about anything, although I highly doubt it. We’d have to have monster economic growth in China to get oil up to $100 a barrel. Right now, China is going the other way.

Q: What’s your view on the debt ceiling? Will it give us a good buying opportunity?

A: Probably not, our good buying opportunity was yesterday or Monday. These debt crises are always one minute before midnight solutions. They always get solved. Never underestimate the ability of Congressmen to spend money in their own district. So, I don’t think that would create a stock market crash like it might have done 20 years ago.

Q: What about Freeport McMoRan (FCX)?

A: It’s taking a dip here because of a possible real estate crash in China, and of course China is the world’s largest buyer of copper for apartment construction. I’m kind of taking a break here on Freeport McMoRan and US Steel (X) until we learn a little more about the China situation. They did move to start a bailout today. Let’s see if that continues.

Q: When will the airlines come back?

A: They’ll come back when business travel returns, which I think could be next year. If you eliminate the virus completely, these things double easily. That's the bet you’re making. Let’s see if the covid boosters work, the childhood shots work, and then you can take another look at Delta (DAL) and Alaska (ALK).

Q: If Bitcoin gains mass adoption, does that put banks out of business just like electric vehicles are making oil obsolete?

A: No, not if the banks go into the Bitcoin business. And the banks actually have the cash, resources, and infrastructure to take over the Bitcoin area once the technology matures. And the corollary to that is that the oil industry is that the majors have the infrastructure, the manpower, and the capital to take over the alternative energy business if they choose to do so and oil goes to zero, which it eventually will. The proof of that is the largest investor in all the Silicon Valley energy startups are Saudi Arabian venture capital funds. They’re huge investors in solar here. If Saudi Arabia has a lot of oil, they have even more solar. Believe me, I’ve been there.

Q: Will a lack of inventory and rising interest rates end the bidding wars on houses soon?

A: Only if you consider 10 years soon. That is how long it will take for the sizes of different generations to come into balance, the Millennials (85 million) versus the Gen Xers (45 million). That’s when the housing bubble will end, but that won’t be for another decade. We still have a structural shortage of new home construction (about 5 million units a year) because all the home builders who went bust in the financial crisis in 2008/2009 and never came back—all of that new construction is still missing. And the surviving ones haven’t increased production to meet that shortfall because they want to manage their risk. Eventually, they will and that probably will be the next top, but that’s really 2030 type business.

Q: What about Federal Express (FDX)?

A: Labor shortages. It's hitting (UPS), (FDX), the Post Office, and DHL too—all the couriers.

Q: When do you think gold (GLD) and silver (SLV) rise back to 2,000?

A: I am avoiding gold and silver as long as Bitcoin has buyers. The action in Bitcoin is 10x the movement you get in gold and that’s attracted all the speculative capital in the market, draining all interest from gold, which hit a new six-month low just last week.

Q: What’s your buy target for Apple (AAPL)?

A: I would say if you can get it at $135, that would be a gift. We did get close to $140 at the lows this week; that’s when you start nibbling, and then you double up again at $135. I doubt Apple is going down more than 10% in this cycle. There are too many people still trying to get into it. And they’re still the largest buyer of stock in the world. They only buy one stock, their own.

Q: I never got any IPath Series B S&P 500 VIX Short Term Futures ETN (VXX) alerts.

A: That's because we never sent any out. (VIX) has become an incredibly difficult game to play, accumulating positions for months and then trying to get out on a one-day spike that lasts a few minutes. The insiders have too much of a house advantage here, who only play from the short side. There are too many better fish to fry.

Q: What about the Apple electric vehicle?

A: I’ll believe it when I see it; I've been hearing about this for something like seven years. My guess is that Apple is more likely to supply consoles and parts to other EV makers and help them get into the game with software and so on. I think that will be Apple's role in all of this.

Q: How much has China Evergrande Group stock fallen?

A: It’s a really illiquid stock in China so we never got involved in it. I think it’s down more than half. Even the professional short-sellers like Jim Chanos and Kyle Bass, have been targeting that stock for 10 years are now screaming they’re vindicated. Of course, they lost fortunes in the meantime. So, I'll pass on that one.

Q: What about stop losses on LEAPS trades?

A: I don’t really run LEAPS portfolios or issue stop losses. The idea is to run these into expiration, and we’ve never had one expire out of the money, although I may break that record if TLT doesn’t turn around in the next three months.

Q: How would autonomous trucking impact rail transportation?

A: They’re two totally different things. Trucking companies like Yellow Corporation (YELL) carry smaller cargo for local deliveries or small long-distance deliveries. 7Some 70% of all railroad traffic is coal going to China, and the rest is bulk commodities like wood chips, iron ore, etc. Trucks don’t carry any of that, so they’re totally separate businesses. But, if we went totally autonomous on trucking, it would make all the main trucker companies massively profitable, as they get rid of their drivers. Right now, every trucking company in the US has a driver shortage.

Q: United Airlines (UAL) pilots are now ordered to get vaccinated.

A: I think within months to hold a job anywhere in the US, you will have to get vaccinated. They do not want you in the office without a vaccination. Jobs are not worth risking lives, and we hit 2,000 deaths again yesterday. The corporations are taking the lead, not the government. The exception will be the politically motivated companies, like the My Pillow Guy; I doubt they'll ever require vaccinations at My Pillow. And there are a few other companies such as Hobby Lobby that are also anti-vaxers. But all public transport companies, hospitals, etc., are going to say get vaccinated or get out—it’s very simple.

Q: Should I buy Berkshire (BRKB) here?

A: Yes, it’s a great entry point, even if you can't get my price. Go higher in the strikes or go farther out in maturity.

Q: Is copper metal (CPER) a buy here?

A: Probably long term, but short term will be subject to the whims of the Chinese real estate crisis if there is one.

Q: Won’t Natural Gas (UNG) outperform in the power grid since all EVs must be charged?

A: Not if the grid is 100% electric. Natural gas still has carbon in it, although only half as much as oil or gasoline. I think even natural gas eventually gets phased out because you can expect solar panels to improve by 80% over the next ten years. At that point, any other energy source won’t be able to compete—oil, natural gas, you name it. And that is why you don’t see any long-term money going into carbon energy sources.

Q: Iron ore has just gone from $200 to $100, why are you bullish?

A: Yes, Because it has just gone from $200 to $100. Eventually, China recovers, despite a short-term financial and housing crisis. Buy low, sell high—that’s my revolutionary new strategy.

Q: What are your thoughts on Bitcoin vs Ethereum?

A: I think Ethereum will outperform Bitcoin because it has a more modern technology. It’s only six years old, vs 12 years for Bitcoin. It’s also more efficient, using less energy in its production. In fact, we did get a double in Ethereum in August as opposed to only a 50% move in Bitcoin.

Q: Do you have any concerns on holding the financials through earnings in October?

A: No, I think the results will be fantastic, and I want to be long going into those.

Q: What does the current situation with China mean for Alibaba (BABA)?

A: Keep your stocks, you’ve already taken the hit—down 53%. The next surprise is that China quits beating up on capitalism and these things will all recover bigtime. However, any options you may have could expire before that happens. So, keep the stocks, get rid of the options, salvage whatever time value you can, and then wait for China to start doing the right thing.

Q: What are the best solar stocks?

A: First Solar (FSLR) and SunPower (SPWR), which have both done great.

Q: If bonds are a no-no, and governments are getting more indebted than ever, who will buy them?

A: Governments. The only buyers of bonds now are non-economic buyers. Those would be governments, central banks, and banks who are required by law to own certain amounts of bonds to meet regulatory capital requirements. No individual in their right mind is buying any bonds here at all, nor is any financial advisor recommending them.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/tootsie.png331522Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-24 09:02:442021-09-24 11:19:08September 22 Biweekly Strategy Webinar Q&A

Global Market Comments September 20, 2021 Fiat Lux

Featured Trade:

(INTRODUCING THE MAD HEDGE BITCOIN PLATINUM SERVICE),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BATTLE OF THE 50-DAY),

(SPY), (TLT), (DIS), (BLOK), (MSTR), (QQQ), (EEM), (UUP)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-20 10:06:212021-09-20 10:30:05September 20, 2021

The next long-term driver of financial markets will be rising interest rates.

It’s not a matter of if, but when. Is it this month, or next month? One way or the other it’s coming.

Which means you should be rearranging your portfolio right now big time.

In a rising interest rate regime seven big things will happen:

1) Bonds (TLT) will collapse.

2) Domestic recovery and commodity stocks (FCX) will soar.

3) Technology stocks (QQQ) will move sideways to down 10%

4) The US dollar (UUP) craters

5) Foreign stock markets (EEM) do better than American ones.

6) Bitcoin (BLOK), (MSTR) and other cryptocurrencies go through the roof.

7) Residential real estate keeps appreciate, but at a slower rate.

These trends will continue for six months, or until long-term interest rates hit an interim peak, such as at 2.00%.

The delta variant gave us a secondary recession. Its demise will give us a secondary recovery, and the same sectors will prosper as with the first. According to the Johns Hopkins University of Medicine, this is happening right now.

The only caution here is that long-term investors should probably keep their technology stocks. Once rates hit the next interest rate peak again, it will be off to the races for tech once again. In the long term, tech always comes back, and tech always wins.

Of course, the major event of the coming week will be the Federal Reserve’s Open Market Committee meeting where interest rates are decided and the press conference with Jay Powell that follows.

Interest rates won’t move. It’s the press conference that is crucial, where we gain insights into the taper. What’s different this time is that the European Central Bank has already begun their taper with an economy far weaker than ours. Will Jay take the cue?

Far and away, the most reliable indicator for “BUY” timing since the presidential election has been the 50-day moving average for the S&P 500. Increasing stock weightings there and you were golden.

The problem now is that we have not seen the index close below the 50-day for two consecutive days for a record 221 days. This has not happened for 31 years.

We all know the reasons: Record low-interest rates making cash trash, seven years of quantitative easing, and a global liquidity glut. Exploding equity in homes and stock portfolios helps too. Still, 31 years is a long time to be this bullish.

I saw all this coming a mile off.

Since the election, I have relentlessly pursued this market with a super aggressive 100% weighting. Then I started paring back risk in June. In July and August, I cut back further to the bone, running minuscule 20% long weightings against a few shorts.

And this is how you manage your risk control.

When markets are rigged in your favor and the lunch is free, you bet the ranch. When they aren’t, you cower on the sidelines and watch others take insane risks.

But who am I to know? I’ve only been doing this for 51 years, and 58 years if you count the (IBM) shares I bought with my paperboy earnings.

Antitrust Comes Home to Roost at Apple, sending the stock down $9 in two days. A judge ruled that Apple will no longer be allowed to prohibit developers from providing links or other communications that direct users away from Apple in-app purchasing. Apple typically takes a 15% to 30% cut of gross sales. It’s a slap on the wrist, as Apple’s main revenue stream is still from iPhones. The judge ruled in favor of Apple on nine of ten other issues. It creates massive new opportunities for hundreds of other Silicon Valley start-ups. Still, if you were looking for an excuse to take profits, this is it. Buy (AAPL) on dips.

Tesla to get EV Tax Credit Restored in a new overhaul of alternative energy subsidies. Both Tesla (TSLA) and General Motors (GM) lost their $7,500 per car subsidies when sales topped 200,000. GM will get an extra $5,000 discount for union-made cars. Tesla is ferociously non-union. Maybe this explains the 36% rally since May. It should help (TSLA) get reach its million-vehicle target for 2021 if it can get enough chips. Buy (TSLA) on dips.

China Inflation Hits 13 Year High, up 9.5% YOY. Soaring commodity and coal prices are the issue. Coal is up 57% YOY, reflecting an energy shortage during the covid economic rebound. It predicts a hot CPI for the US on Tuesday.

The Consumer Price Index rose by 5.3% YOY and up 0.3% in August. It was a seven-month low, with delta clearly a drag. Food and energy came in lighter than expected. Prices for used cars, air tickets, and insurance fell. Stocks loved it, rising triple digits, and bond prices halved losses. St next week’s FOMC we’ll see how Jay really feels.

House Looking at a Top 26.5% Corporate Tax Rate, well up from the current 21% but not as high as the 28% that was feared. Capital gains would rise from 20% to 25%. The goal is to raise $2.5 trillion to get the $3.5 trillion spending package into law. It’s all a trial balloon for what might be possible. Stocks loved it.

Amazon to Hire 125,000 and boost wages to $18 an hour. They are also paying $3,000 signing bonuses and taking pay up to $22.50 in prime areas like New York and California. It’s all part of a strategy to make (AMZN) the “best employer in the world”. Buy (AMZN) on dips as its dominance on online commerce grows.

China Destroys Casino Stocks, threatening to increase oversight of their Macao operations. The concern is that China will pull the gaming licenses of foreign companies when they come up for renewal in June. Buy (WYNN) and (LVS) on the dip.

Weekly Jobless Claims Come in at 332,000, a new post-pandemic low. The previous week was revised down even lower, to 312,000. The end of pandemic unemployment benefits is no doubt a factor, driving people off of their couches and back to the salt mines. Is this the light at the end of the tunnel?

Bitcoin Charts are Showing a Golden Cross, which usually presages upside breakouts in the cryptocurrency. A golden cross is where the 50-day moving average pierces the 200-day to the upside. This is crucial because technicals are more important in crypto than in any other financial instrument. In the meantime, (AMC) has started accepting Bitcoin for online movie ticket purchases. Buy (MSTR) on dips.

My Ten-Year View

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a modest +1.10% loss so far in September following a blockbuster 9.36% profit in August. My 2021 year-to-date performance soared to 77.47%. The Dow Average is up 13.02% so far in 2021.

That leaves me 70% in cash, 10% short in the (TLT), and 20% long in the (SPY) and (DIS). Both of our September option positions expired at max profits.

I’m keeping positions small as long as we are at extreme overbought conditions. However, a Volatility Index (VIX) above $20 shows there may be a light at the end of the tunnel.

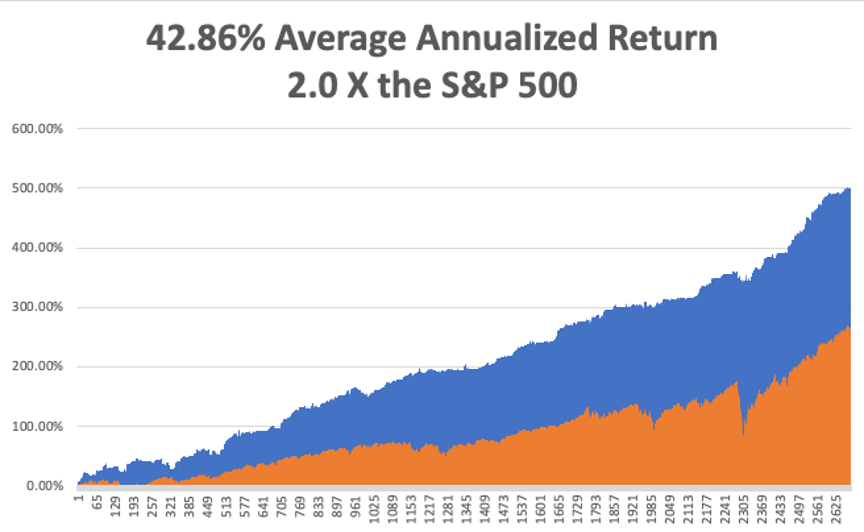

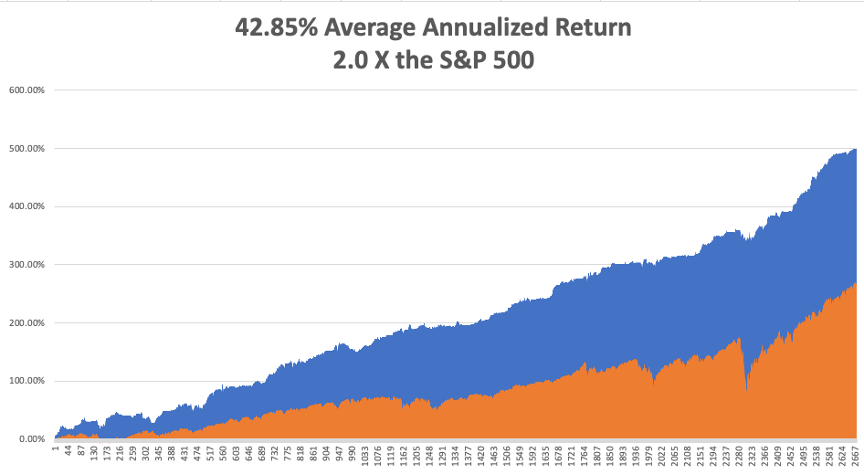

That brings my 12-year total return to 500.02%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.86%, easily the highest in the industry.

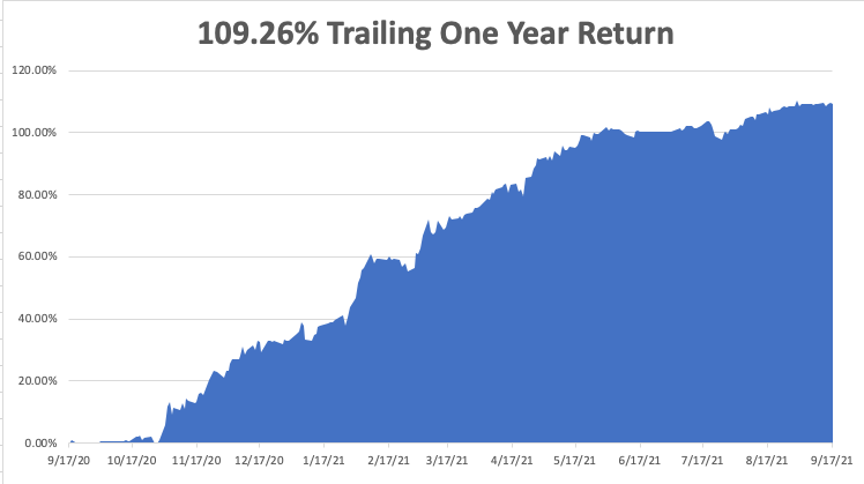

My trailing one-year return popped back to positively eye-popping 109.26%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 42 million and rising quickly and deaths topping 673,000, which you can find here.

The coming week will be all about the Fed meeting on Wednesday.

On Monday, September 20, at 11:00 AM, the NAHB National Housing Market Index for September is out.

On Tuesday, September 21 at 9:30 AM, Housing Starts for August are printed.

On Wednesday, September 22 at 11:00 AM, Existing Home Sales for August are announced. At 2:00 PM, the Fed interest rate decision is released and an important press conference about taper issues follows.

On Thursday, September 23 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, September 24 at 8:30 AM, we learn US Durable Goods for August. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, with the shocking re-emergence of Nazis on America's political scene, memories are flooding back to me of some of the most amazing experiences in my life.

I have been warning my long-term readers for years now that this story was coming. The right time is now here to write it.

I know the Nazis well.

During the civil rights movement of the 1960s, I frequently hitchhiked through the Deep South to learn what was actually happening.

It was not usual for me to catch a nighttime ride with a neo-Nazi on his way to a cross burning at a nearby Ku Klux Klan meeting, always with an uneducated blue-collar worker who needed a haircut.

In fact, being a card-carrying white kid, I was often invited to come along.

I had a stock answer: "No thanks, I'm going to another Klan meeting further down the road."

That opened my driver up to expound at length on his movement's bizarre philosophy.

What I heard was chilling.

During 1968 and 1969, I worked in West Berlin at the Sarotti Chocolate factory in order to perfect my German. On the first day at work, they let you eat all you want for free.

After that, you get so sick that you never wanted to touch the stuff again. Some 50 years later and I still can’t eat their chocolate with sweetened alcohol on the inside.

My co-worker there was named Jendro, who had been captured by the Russians at Stalingrad and was one of the 5% of prisoners who made it home alive in 1955. His stories were incredible and my problems pale in comparison.

Answering an ad on a local bulletin board, I found myself living with a Nazi family near the company's Tempelhof factory.

There was one thing about Nazis you needed to know during the 1960s: They loved Americans.

After all, it was we who saved them from certain annihilation by the teeming Bolshevik hoards from the east.

The American postwar occupation, while unpopular, was gentle by comparison. It turned out that everyone loved Hershey bars.

As a result, I got free room and board for two summers at the expense of having to listen to some very politically incorrect theories about race. I remember the hot homemade apple strudel like it was yesterday.

Let me tell you another thing about Nazis. Once a Nazi, always a Nazi. Just because they lost the war didn't mean they dropped their extreme beliefs.

Fast-forward 30 years, and I was a wealthy hedge fund manager with money to burn, looking for adventure with a history bent during the 1990s.

I was mountain climbing in the Bavarian Alps with a friend, not far from Garmisch-Partenkirchen, when I learned that Leni Riefenstahl lived nearby, then in her 90s.

Attending the USC film school with a young kid named Steven Spielberg decades earlier, I knew that Riefenstahl was a legend in the filmmaking community.

She produced such icons as Olympia, about the 1932 Berlin Olympics, and The Triumph of the Will, about the Nuremberg Nazi rallies. It is said that Donald Trump borrowed many of these techniques during his successful 2016 presidential run.

It was rumored that Riefenstahl was also the onetime girlfriend of Adolph Hitler.

I needed a ruse to meet her since surviving members of the Third Reich tend to be very private people, so I tracked down one of her black and white photos of Nubian warriors, which she took during her rehabilitation period in the 1960s.

It was my goal to get her to sign it.

Some well-placed intermediaries managed to pull off a meeting with the notoriously reclusive Riefenstahl, and I managed to score a half-hour tea.

I presented the African photograph and she seemed grateful that I was interested in her work. She signed it quickly with a flourish.

I then gently grilled her on what it was like to live in Germany in the 1930s. What I learned was fascinating.

But when I asked about her relationship with The Fuhrer, she flashed, "That is nothing but Zionist propaganda."

Spoken like a true Nazi.

The interview ended abruptly.

I took my signed photograph home, framed it, hung it on my office wall for a few years. Then I donated it to a silent auction at my kids' high school.

Nobody bid on it.

The photo ended up in storage at my home, and when it was time to make space, it went to Goodwill.

I obtained a nice high appraisal for the work of art and then took a generous tax deduction for the donation, of course.

It is now more than a half-century since my first contact with the Nazis, and all of the WWII veterans are gone. Talking about it to kids today, you might as well be discussing the Revolutionary war.

By the way, the torchlight parade we saw in Charlottesville, VA in 2017 was obviously lifted from The Triumph of the Will, except that they didn't use tiki poolside torches in Germany in the 1930s.

Leni Riefenstahl

Olympia

Former Paperboy

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/leni-riefenstahl.png550400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-20 10:02:462021-09-20 10:30:20The Market Outlook for the Week Ahead, or The Battle of the 50-Day

Global Market Comments September 13, 2021 Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON FOR SEPTEMBER 14-16),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or VENTURING INTO THE METAVERSE

(SPY), (TLT), (VIX),

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-13 11:06:322021-09-13 12:52:21September 13, 2021

It refers to the virtual world where all things exist in a virtual world.

And here is the great thing about the metaverse. The real world can only grow at an analog rate and is finite. The virtual world can grow at an exponential, viral rate and is infinite.

Infinite markets with infinite customers? That is something that companies and share prices really like to hear about.

We’re getting a peek into the Metaverse right now with the movement of many companies to a virtual world triggered by the pandemic. With employees working at home, a headquarters at a PO Box in Montana to meet regulatory minimums, selling digital services to a digital market, these companies effectively exist only in terms of electrons and bytes.

But suddenly, costs have plunged by 40%, productivity has improved by 40%, and profits have increased tenfold. These are companies you want to own.

No wonder the stock market is going up almost every day. It’s because companies like this are worth more, a lot more overnight!

It's how Silicon Valley leaped from having 80 unicorns to 800 in the span of two years. The future is happening fast.

If you are an old fart who doesn’t want to bother with all this computer mumbo jumbo, invest a few minutes playing Facebook’s (FB) Oculus Rift with your grandkids. Then sit down and watch the 2018 science fiction/fantasy movie Ready Player One. There is a sequel in the works. The second sequel will be you and me.

We have now just suffered the worst trading week since February, with the (SPY) off by a mere $8.5, or 1.9%. We may have a shot at another long-awaited 5% correction this week. If we do, I’ll put half my cash in the market. I’ll put the rest in at a 10% correction.

I highly doubt that stocks will fall by more than that given the massive weight of liquidity in the financial system, even though it’s September. My $475 (SPY) target for end of 2021 still stands and I’m sticking to it. You’re going to have to pry my cold dead fingers off of my forecast.

The only question is which sectors will lead. My bet is on domestic recovery stocks like banks, brokers, hotels, casinos, airlines, cruise lines, and railroads. Delta peaked two weeks ago and is now falling precipitously, especially in the south.

That sets up a second post-Covid recovery trade with the same sector leading the first time.

The way the pandemic ends is that the US gets to 90% immunity, where Covid becomes an annual flu shot. California is already there with 80% of the population vaccinated and 10% getting the disease. Alabama may get there with 60% vaccinations and 30% getting sick. But in a year, the whole country will be at 90%.

Then, we can get on with the rest of our lives.

The August Nonfarm Payroll Report Bombs, coming in at only 235,000 versus an expected 720,000, a huge miss. The headline Unemployment Rate fell 0.2% to 5.2%, a new post-pandemic low. Mysteriously, both stocks and bonds hated it. Manufacturing was up 37,000, while Leisure & Hospitality was zero and Retail at -28,000. Education LOST -25,000 during the back-to-school season. Average Hourly Earnings rose an astonishing 0.6% MOM, or 4.3% YOY. The U6 long-term unemployment rate fell to 8.8%. Goodbye taper. A shortage of workers was to blame, but the economic data has been worsening for a while now. Delta is taking a bigger bite than we thought.

JOLTS comes in at a blockbuster 10.9 million in July, a new record high. This is the number of job openings in the private sector. Anyone who wants a job can get a job. Blame the education gap. The problem is that there is demand for 10.9 million website designers, computer programmers, and internet marketers, and an endless supply of waiters and other restaurant workers.

The Fed says growth downshifted during the summer, thanks to delta and a worker shortage according to the Beige Book release. We already knew that, and a five-point selloff in bonds is telling us that Covid is declining and growth is back on.

Europe tapers, cutting back monthly Eurobond purchases 160-170 billion a month. Governor Christine Lagarde believes any inflation is temporary and the time for emergency stimulus is over. Can the Fed be far behind?

Seven million lose Unemployment Benefits. This should make available more workers whose shortage have been a drag on the economy. Accelerating growth can only be good for stocks.

El Salvador launches Bitcoin as a national currency, creating a national wallet, and offering every citizen $30 to open an account. Most of the accounts will be accessed via cell phones. The central bank bought 400 bitcoins worth $20 million as part of the rollout. The country’s president is helping to sort out technical glitches. Is Bitcoin the next global currency? Bitcoin dropped 10% on the news.

Tesla to make its own whips in a dramatic response to a structural global chip shortage that could last years. The news was good for a $30 pop in the stock this morning. Tesla is already one of the world’s largest chip users, and their needs are expected to jump 50-fold in the next ten years. The move justifies a much larger premium for the stock. It’s all about training the neural network.

Will a Bitcoin ETF approval spike the Market? There are a dozen applications with SEC for the first US-approved crypto ETF. When approved, billions of new cash will pile into Bitcoin off the back of the new improved legitimacy. Buy before the IPO, it’s a classic trading strategy. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch is down 1.09% in September, thanks to a shortage of low-risk/high-return trading opportunities. My 2021 year-to-date performance soared to 77.48%. The Dow Average was up 13.10% so far in 2021.

That leaves me 60% in cash at 40% in short (TLT), and long (SPY) and (DIS). My last two positions expire in four trading days.

Although we have maxed out the profits with these two positions, I’ll keep them as there is nothing else to do. I’m keeping positions small as long as we are at extreme overbought conditions. The Volatility Index (VIX) now over $20 shows that an entry point may be near.

That brings my 12-year total return to 500.03%, some 2.00 times the S&P 500 (SPX) over the same period and a new all-time high. My 12-year average annualized return now stands at a new high of 42.85%, easily the highest in the industry.

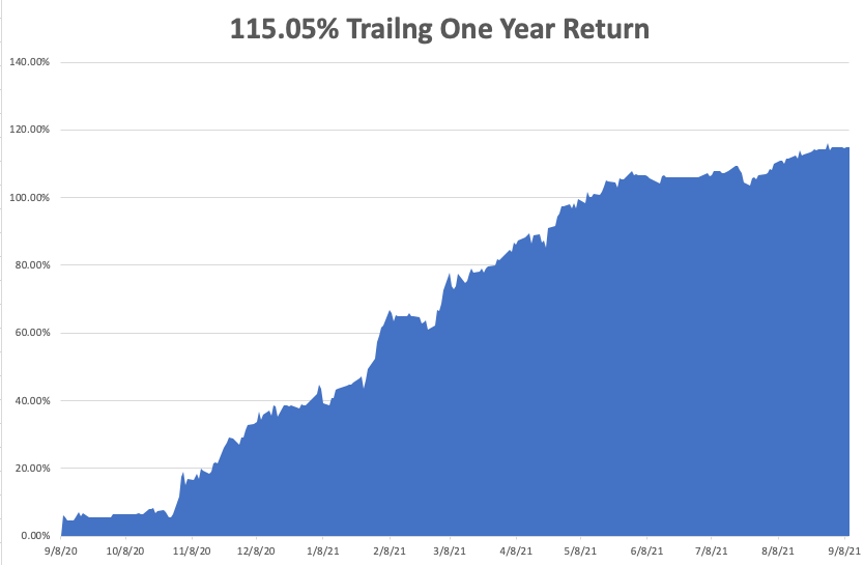

My trailing one-year return popped back to positively eye-popping 115.05%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 41 million and rising quickly and deaths topping 670,000, which you can find here.

The coming week will be slow on the data front.

On Monday, September 13, at 12:00 noon, US Inflation Expectations are released.

On Tuesday, September 14, at 8:30 AM, US Core Inflation is published, now the second biggest number of the month.

On Wednesday, September 15 at 9:15, Industrial Production for July is disclosed. At 9:30 AM, we get the New York Empire State Manufacturing Index for September.

On Thursday, September 16 at 8:30 AM, Weekly Jobless Claims are announced. We also get Retail Sales for August.

On Friday, September 17 at 8:30 AM, we learn the University of Michigan Consumer Sentiment for September. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, one of the great shortcomings of San Francisco is that we only have a theater district with two venues and it is in the Tenderloin, the worst neighborhood in the city, an area beset with homeless, drug addicts, and prostitution.

I was walking to a parking lot after a show one evening when I passed a doorway. Three men were violently attacking a blond woman. Never one to miss a good fight, I dove in, knocking two unconscious in 15 seconds (thank you Higaona Sensei!). Unfortunately, number three jumped to my side, pulled a knife, and stabbed me.

The attacker and the woman ran off, leaving me bleeding in a doorway. I drove over the Golden Gate Bridge to Marin General Hospital, bleeding all over the front seat of my car, where they sewed me up nicely and put me on some strong drugs.

The doctor said, “You shouldn’t be doing this at your age.”

I responded that “good Samaritans are always rewarded, even if the work is its own reward.”

Fortunately, I still had my Motorola Flip Phone with me, so I called Singapore from my hospital bed for a market update. I liked what I saw and bought 100 futures contracts on Japan’s Nikkei 225. This was back in 1999 when anything you touched went straight up.

Then, I passed out.

An hour later, I woke up, called Singapore again and bought another 100 futures contracts, not remembering the earlier buy. This went on all night long.

The next morning, I was awoken by a call from my staff who excitedly told me that the overnight position sheets had just come in and I had made 40% on the day.

Was there some mistake?

Then I got a somewhat tense call from my broker. I had a margin call. I had also exceeded the exchange limits for a single contract and owned the equivalent of $200 million worth of Nikkei. I told them to sell everything I had at market and go 100% cash.

That was exactly what they wanted to hear.

That left me up 60% on the year and it was only May.

I then called all of the investors in my hedge fund. I told them the good news, that I wouldn’t be doing anymore trades for the fund until I received my performance bonus the following January and was taking off on a long vacation. With a 2%/20% payout in those days, that meant I was owed 14% of the underlying assets of the fund at a very elevated valuation.

They said that’s great, have fun, by the way, how did you do it?

I answered, “Great drug selection.” No further questions were asked.

Then I launched on the mother of all spending sprees.

I flew to Germany and picked up a new Mercedes S600 V12 Sedan at the factory in Stuttgart for $160,000. I then immediately road-tested it on the Autobahn at 130 mph. I made it to Switzerland in only two hours. After all, my old car needed a new seat.

Next, I bought all new furniture for the entire house, each kid selecting their own unique style.

Then, I took the family to Las Vegas where we stayed in the “Rain Man Suite” at the Bellagio Hotel for $10,000 a night, where both the 1988 Rain Man and 2009 The Hangover were filmed.

I bought everyone in the family black wool Armani suits, plus a couple of Brioni’s for myself at $8,000 a pop. For good measure, I chartered a helicopter for a tour of the Grand Canyon the next day.

At the end of the year, I sold my hedge fund based on the incredible strength of my recent performance for an enormous premium. I then left the stock market to explore a new natural gas drilling technology I had heard about called “fracking.”

Four months later, the Dotcom Crash ensued in earnest.

I still have the scar on my right side, and it always itches just before it rains, which is now almost never. But it was worth it, every inch of it.

It’s all true, every word of it and I’ll swear to it on a stack of bibles.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/john-thomas-family-picture.png560712Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-13 11:02:092021-09-13 12:53:33The Market Outlook for the Week Ahead, or Venturing Into the Metaverse

Below please find subscribers’ Q&A for the September 8 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: Do you think we’ll see the under $130 in the United States Treasury Bond Fund (TLT) before January 2022?

A: I don’t think so; I think we could go below $140, maybe below $135. But $130 would be a brand new low in the move and would be a stretch. We basically lost 4 months on this trade due to the countertrend rally, which just ended. I would come out of your (TLT) $130-$135 vertical bear put spreads right here while they still have time value, but keep the $135-$ 140s, the $140-$145’s, and especially the $150-$155’s. The idea was that you just keep averaging up and up until the market turns, and then you make back any loss. We move into accelerated time decay on those deep out of the money put spreads in December, so I would take the money and then offset it with the gains you made in those positions.

Q: Does Palantir (PLTR) look like it’ll hit $100 by year-end?

A: No, the stock has been dead, and management has not been doing anything to promote it. We did get a move up to $45 but it failed. It’s still a great long-term idea as they are growing at 50% a year. Also, they did buy $50 million worth of gold bars as a hedge. But as a short-term trader, Palantir isn’t working. If you have an options position on that I would probably get out of it or roll it forward to 2023.

Q: PayPal (PYPL) is fluctuating up and down with Bitcoin. Do you like PayPal?

A: Absolutely, but it obviously is being dragged down by Bitcoin. It is a temporary down move caused by a one-time-only event in El Salvador. Buy the dip in PayPal. It is a leader in the whole move into a digital financial system.

Q: When is Freeport McMoRan (FCX) likely to move up?

A: As soon as we shift out of the tech trade into the domestic recovery trade, which could be in weeks or months at the latest. We’ll switch from one side of the barbell to the other.

Q: Where do you see Tesla (TSLA)?

A: It keeps going up, so my guess is we top $800 by the end of the year, and maybe $850. The big news here is that Tesla has gone into the chip business, making its own chips in-house which is easy for them to do in Silicon Valley. But it does make them the first global car maker that is also a chip maker, and therefore the stock deserves a higher premium. The stock went up $30 on the news and is great for all Tesla holders. I hope you have the 2023 LEAPS.

Q: Too late to buy Tesla LEAPS?

A: Unless you’re really deep in the money, with something like a $600-$650; but the return on that will only be about 50% in 2 years.

Q: The Biden administration just set a goal of 45% solar by the end of 2050. Which solar stock should I buy here?

A: The problem with solar is as soon as Biden started winning primaries, every solar stock took off like a rocket, figuring he’d win, which he did. All of them went up 6-fold or more as a result of that, then gave up one-third of their gains and are now moving sideways. So if you look at the charts, the classic one to buy here is the Invesco Solar ETF (TAN), a basked of the top solar companies. All of these peaked in February and have been doing sideways “time” corrections since then, which means they eventually want to go higher. The other two that have charts that look like they’re finally starting to break out to the upside are First Solar (FSLR) and SunPower (SPWR) after 8 months of consolidation.

Q: Why is the second half of September almost always bad? Is it due to institutional repositioning?

A: Not really, the cash comes into the market at certain times of the year, like end of the year, beginning of the year, and end of each quarter. September seems like the month where they kind of just run out of money. But there's actually also a historical reason for that. For most of American history, we had an agricultural economy. Farmers were more than half the population, and the period of maximum distress for farmers is September, where they put all the money into seed and fertilizer and labor into the field, but they haven't harvested it yet. So, traditionally, they always did a lot of borrowing in September, which caused a cash squeeze and interest rate spike, and a stock market panic as a result. So that's the history behind weak Septembers and Octobers. Once the farmers get the crops in and sell them, that resolves the cash squeeze, interest rates fall, and it’s straight up for stocks for the rest of the year most of the time.

Q: SPACs (Special Purpose Acquisition Companies) seem to be losing interest. Do you recommend any or stay away?

A: Stay away—they’re all rip-offs and are simply a means by which managers can increase their fees from 2% to 20%. That's what they did with virtually all of them. This will end in tears.

Q: What's your feeling about satellite internet phone service replacing current internet cell service in the future?

A: It’s in the future, but it may be 10 years off in the future. If it happens sooner, it’s because Elon Musk was able to deliver cheap rocket service. He already has 20,000 satellites in the sky for his own Starlink global cell phone service for internet access.

Q: How does one buy a Bitcoin stock?

A: Well first of all, I highly recommend you buy the Mad Hedge Bitcoin Letter, which you can get in our store. But there's also the Greyscale Bitcoin Trust (GBTC) which allows you to buy a Bitcoin proxy very easily. I’ll even honor the discounted $995 price for my Bitcoin Letter for another day by clicking here.

Q: Is Warren Buffet and his value philosophy something I should be following, or is he outdated?

A: I have to say, buying stocks cheap with high cash flow will never go out of style. Currently, Warren’s big holdings are domestic industrials, banks, and Apple. All of those look like they will do well moving forward. Buffet’s Berkshire Hathaway (BRKB) has a built-in barbell element to it and is the subject of one of our LEAPS recommendations which has already been hugely successful.

Q: Is Home Depot (HD) at $330 a bargain?

A: Well, we just had a selloff and it bounced hard, and now we’re waiting for the domestic post delta recovery. It's hard to imagine both Home Depot and Lowes not doing well in this scenario.

Q: What will happen to tech when interest rates rise?

A: My bet is they go sideways to down small until you get another peak in interest rates (the next peak will be at 1.76% in the ten year US Treasury bond, the 2021 high) and once you hit that, then tech will take off like a rocket again, and in the meantime, you play the domestics while interest rates are rising. That is the game and will continue to be the game for a couple of years.

Q: Should I buy IBM (IBM) on a turnaround story?

A: No, I've been waiting for IBM to turn around for 10 years. They just don’t seem to get it. What they do is whenever a division starts to make money, they sell it and get cash like they did with the PC division and this year with its infrastructure business called Kyndryl. So, they’re not leaving any growth for the actual IBM holders.

Q: Do you like Square (SQ) at $256?

A: Yes, and that would be a great 2023 LEAPS candidate. All of the digital settlement payment systems are going to do well in the Bitcoin future. They also own quite a lot of Bitcoin. They are leading the charge into a digitized financial system.

Q: What’s a good Ethereum ETF?

A: The Greyscale Ethereum Trust (ETHE) is just the ticket.

Q: So you avoid energy, meaning oil and gas?

A: Yes, alternative energy we like, but it’s had an enormous run already so after a 7-month time correction it’s probably safe to get into solar. Traditional oil and gas (USO) is in a long-term secular bear market that started 13 years ago and will eventually go to zero. Last year’s visit to negative futures prices is just a start. Since 2020, the energy market weighting has gone from 15% to 2%.

Q: Is Natural Gas the only rational core fuel for the grid?

A: No, natural gas (UNG) still produces carbon even though it’s only half the amount of oil. This all gets replaced by solar in the next ten years. That’s why I tell people to stay away from energy like the plague. Would you rather buy natural gas at $4.50/btu or get solar electricity for free? Those are basically going to be the choices in ten years.

Q: Who is the biggest Aluminum producer?

A: Alcoa (AA) which we are a buyer on dips. By the way, if we do have to build 200,000 miles of long-distance transmission lines to cover the electrification of the US energy supply, all of that has to be made of aluminum. You don't use copper for long distances, you use aluminum (aluminum for you Brits).

Q: Would you buy Uber (UBER) at $40 today?

A: Probably, yes; it had a nice 40% correction. However, you are buying into the battle over gig workers—whether they should be treated as full-time or part-time workers. That is going to be a continuing drag on the stock until they win.

Q: What do you think of meme stocks?

A: You're better off buying a lottery ticket. Even with a low payoff, you get a 1:10 chance of winning on a $1 lottery ticket. Meme stocks could double or go to zero with no warning whatsoever—there’s no logic to this market at all.

Q: What do you think of Uranium?

A: Three words come to mind: Chernobyl, Fukushima, and Three Mile Island. I think uranium's time has passed, even though China is building a hundred nuclear power plants. It’s just too expensive to compete against solar on a large scale and impossible to insure. If you still like Uranium though, the Uranium Royalty Corp. (UROY) has had a nice pop recently. But the issue is that nuclear technologies can’t keep up with solar and digital. And they blow up.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/john-thomas-roller-coaster.png696424Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-10 10:02:392021-09-10 12:21:53September 8 Biweekly Strategy Webinar Q&A

(A NOTE ON ASSIGNED OPTIONS, OR OPTIONS CALLED AWAY)

(SPY), (TLT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-08 09:04:502021-09-08 08:34:31September 8, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.