I know all of this may sound confusing at first. But once you get the hang of it, this is the greatest way to make money since sliced bread.

I still have two positions left in my model trading portfolio, they are all deep-in-the-money, and about to expire in seven trading days. That opens up a set of risks unique to these positions.

I call it the “Screw up risk.”

As long as the markets maintain current levels, ALL of these positions will expire at their maximum profit values.

They include:

(TLT) 9/$155-$158 put spread

10.00%

(SPY) 9/$410-$420 call spread

10.00%

With the September 17 options expirations upon us, there is a heightened probability that your short position in the options may get called away.

If it happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money vertical options spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker telling you that your call options have been assigned away.

I’ll use the example of the S&P 500 (SPY) $410-$420 in-the-money vertical BULL CALL spread.

For what the broker had done in effect is allow you to get out of your call spread position at the maximum profit point days before the September 17 expiration date. In other words, what you bought for $8.90 on August 17 is now worth $10.00, giving you a near-instant profit of $1,210 or 12.35%!

All you have to do is call your broker and instruct them to “exercise your long position in your (SPY) September 17 $410 calls to close out your short position in the (SPY) September 17 $420 calls.”

You must do this in person. Brokers are not allowed to exercise options automatically, on their own, without your expressed permission. This is a perfectly hedged position, with both options having the same name and the same expiration date, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one options contract is exercisable into 100 shares.

Short positions usually only get called away for dividend-paying stocks or interest-paying ETFs like the (TLT). There are strategies out there that try to capture dividends the day before they are payable. Exercising an option is one way to do that.

Weird stuff like this happens in the run-up to options expirations like we have coming.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there that may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to blow it by writing shoddy algorithms.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

There is a further annoying complication that leads to a lot of confusion. Lately brokers have resorted to sending you warnings that exercises MIGHT happen to help mitigate their own legal liability.

They do this even when such an exercise has zero probability of happening, such as with a short call option in a LEAPS that has a year or more left until expiration. Just ignore these, or call your broker and ask them to explain.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

There may not even be an evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. In fact, I think I’m the last one they really did train.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Calling All Options!

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/Call-Options.png345522Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-08 09:02:082021-09-08 08:35:43A Note on Assigned Options, or Options Called Away

I am usually hiking at Lake Tahoe this time of year, doing the deep research, hiking ten miles a day, and the stripping down to jump into the lake at the end.

This year, climate change had other ideas.

So I am visiting a childhood haunt in Newport Beach, CA, where my late uncle used to live. Remember him? He was the former CFO of Penn Central Railroad in 1970 who made a fortune buying puts just before the company went bankrupt. I guess that was allowed back then.

He lived next door to John Wayne, and we kids used to wave at him, astonished at his bald head. I still miss The Duke.

I am still typing one finger at a time, my left wrist in a brace and elbow in a huge bandage. I told the doctor I couldn’t get to Reno for him to take the stitches out because of the wildfires, so I would do it myself with a pocketknife with Jack Daniels as a sterilizer. He said, “Knock yourself out.”

Traders are so frustrated waiting for the normal summer correction they are starting to call “The Endless Bid Market.” That has left them underweight, trying to catch up, which is why we didn’t get a drop of more than 4% this summer.

Of course, they are also getting rich with what they already have, but they all want to get richer. Greed is trouncing fear big time. Forget about investing.

You can’t buy the dip anymore because there are no dips. You simply use new cash flows to add to your winners, the more they have gone up, the better.

That’s why large-cap tech stocks have been on an absolute tear, hitting new all-time highs. Of course, I am just as guilty as the rest, with a retirement fund loaded with big tech. Google (GOOG) is now my largest position, not through savvy stock selection but purely because of price appreciation.

Of course, it helps that the higher stocks go, the cheaper they get.

Earnings are melting up maintaining the same price-earnings multiple and stock prices are simply following suit. There is nothing overheated about it.

Company profit margins are soaring to record highs as companies make enormous productivity investments to deal with chronic labor shortages. If you live here in Silicon Valley, you see this happening around you every day.

If you don’t, stock valuations are fantasies coming from a faraway land, therefore the surprise at market strength.

Haven’t you noticed how hard it is to get a human on the phone outside of the Philippines, where workers feel rich when they are making $300 a month?

If anything, the market is still undervaluing stocks rather than overvaluing relative to their upside earnings potential.

An S&P 500 target of $500 is now my easy target for 2022. Any credit crunch that could trigger a recession is years off, and one Fed governor away. A delta variant that won’t quit, or the upcoming Mu variant is another worry.

Consensus forecasts constantly lagging the market has the effect of leaving institutions and individuals under-invested and trying to get in, hence no real dips for almost a year.

Afghanistan proves the market could care less about any geopolitical surprise.

You heard it from me first. If the market can’t selloff over the next two weeks when poor seasonals start to fade away, the they wont for all of 2021.

Nonfarm Payroll Report bombs, coming in at only 235,000 versus an expected 720,000, a huge miss. The headline Unemployment Rate fell 0.2% to 5.2% a new post-pandemic low. Mysteriously, both stocks and bonds hated it. Manufacturing was up 37,000, while Leisure & Hospitality was zero and Retail at -28,000. Education LOST -25,000 during the back-to-school season. Average Hourly Earnings rose an astonishing 0.6% MOM, or 4.3% YOY. The U6 long term unemployment rate fell to 8.8%. Goodbye taper. A shortage of workers was to blame, but the economic data has been worsening for a while now. Delta is taking a bigger bite than we thought. Stocks hit new August highs the most in history, surpassing the 1929 record of 11 times. The only negative three-month period seen since 1929 are August, September, and October. Remember what happened in 1929? If that doesn’t scare the living daylights out of you, then nothing will. So, it seems we are in for some kind of correction, even if it’s just the 5% kind. Looks like the month end will be hot. Bitcoin leads crypto, but Ethereum is catching up. Cardano has doubled in a month making it the number three crypto and Avalanche has tripled. Newly minted online broker Robinhood (HOOD) says 60% of its option trading is now in crypto. MicroStrategy’s (MSTR) Michael J. Saylor sees a 50-fold increase in Bitcoin to a total market value of $100 trillion. That is five times the US M3 money supply of $20 trillion. It’s become a financial system of "get crypto or go home." Oil jumps on Hurricane IDA, with a sharp 8.9% rally. Some 91% of Gulf Production shut in, or 1.65 million barrels a day. Don’t expect it to continue. Sell into the rally on this future buggy whip industry. SEC is cracking down on Market Gaming by multiple apps aimed at Millennials. It’s shopping for a new set of market rules aimed at regulating those who foster runaway volatility in single stocks like (AMC). PayPal to enter stock trading, sending the stock up a ballistic $15 in two days. If they pull it off, it will open a huge new profit stream for them, possibly becoming another Robinhood (HOOD), cashing in on the retail trading boom. Earning: regulation costs a lot. Buy (PYPL) on dips.

S&P Case Shiller soars to new highs in June, the National Home Price Index jumping 18.6% YOY, breaking all records. Prices are now 41% higher than the bubble top in 2006. This is the sharpest gain in the 34-year history of the index. Prices in Phoenix leaped 29.6%, followed by San Diego at 27.1% and Seattle by 25.0%. Supply and demand will be seriously out of whack for years. Pending Home Sales drop for the second straight month on a signed contract basis, down 1.8% in July. Summer slowdown, delta slowdown, or market top? However, supply and demand are still far out of balance. Your next Apple purchase may be a satellite phone, bypassing local cell phone networks. A Chinese analyst made this prediction for the iPhone 13 out in 2022. The report says that the iPhone 13 includes a Qualcomm X60 baseband modem chip, which includes LEO satellite comms capabilities. If accurate, this means that the upcoming iPhone will have the hardware capability to act as a satellite phone. It certainly would upend the rush to build private satellite networks, like Viasat and Tesla’s Starlink. Enough investors believed the story to send the stock to a new all-time high. Buy (AAPL) on dips. Air Travel is falling off, with airport security screening dropping to only 1.35 million, the lowest since May 11. Delta is taking its toll, but back to school is a factor as well. Bond king Bill Gross says treasuries are trash. He sees ten-year yields hitting 2.00% sometime in 2022. The 77-year-old drove bond prices for a decade and also made a fortune collecting stamps. Sometimes Bill is early, but he is always right. One billion Asians to join middle class by 2030 on top of the existing 3.75 billion today. That will create a vastly larger market for all online services, which the stock market seems to be telling us today. Indonesia, Pakistan, and Bangladesh are expected to see the largest increases. There is a lot of “hope” in this number, i.e., no more covid, no ward, and no depressions. The next market correction won’t come until the Fed makes a mistake and that might be years off, says Wharton finance professor and long-term bull Jeremy Siegel. That will be when the Fed finds itself behind the inflation curve. Until then, the slow grind up continues. Stocks are the best defense against inflation. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a robust +9.31% gain in August. My 2021 year-to-date performance soared to 78.57%. The Dow Average was up 15.82% so far in 2021.

That leaves me 80% in cash at 20% in short (TLT) and long (SPY). Although we have maxed out the profits with these two positions, I’ll keep them as there is nothing else to do. I’m keeping positions small as long as we are at extreme overbought conditions. The “endless bid” market is not giving anyone entry points as long as the Volatility Index (VIX) remains at $16.

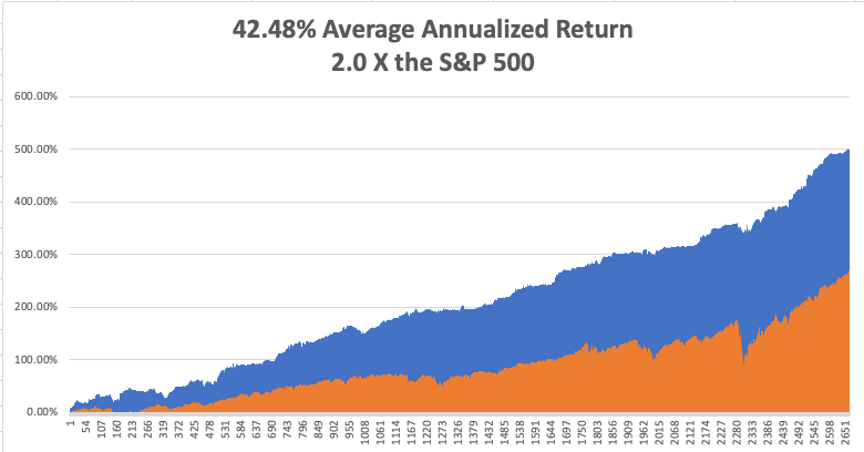

That brings my 12-year total return to 501.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.48%, easily the highest in the industry.

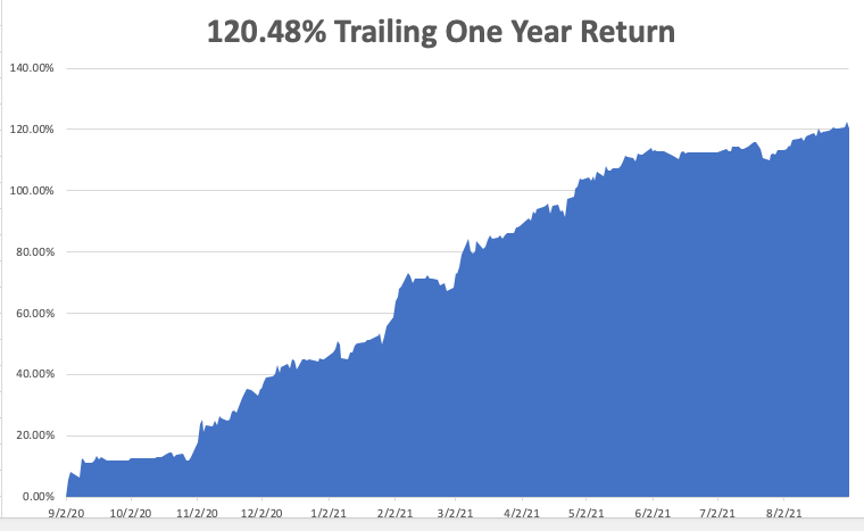

My trailing one-year return popped back to positively eye-popping 120.48%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 40 million and rising quickly and deaths topping 645,000, which you can find here.

The coming week will be slow on the data front.

On Monday, September 6 markets are closed for the US Labor Day. On Tuesday, September 7, there are no special data releases. Everyone will be recovering from hurricanes in the south and east, wildfires in the west, and Covid everywhere.

On Wednesday, September 8 at 9:30 AM, we get API crude oil stocks.

On Thursday, September 9 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, September 10 at 8:30 AM, we learn the Producers Price Index for August. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, a few years ago, I was visited in London by an old friend who had once served on the British Army staff of General Bernard Law Montgomery, the hero of Alamein, who was known to his friend as “Monty” (he had no friends).

I asked if there was anything I could do for him and he said, “Actually, I haven’t had a dish of moules mariniere (steamed mussels in white wine sauce) on the Grand Square in Brussels for a while. I said, “No problem, let’s go.”

We drove my Mercedes 6.0 to an old Battle of Britain hanger (one-inch-thick bombproof steel doors) on the outskirts of London where I kept a twin-engine Cessna 340 with turbocharged engines with a maximum speed of 225 kts. We landed in Brussels in an hour.

We savored the mussels on the square, as good as ever, the national dish of Belgium. The autumn air was brisk, tourists gawked, we drank, and everyone had a good time.

I left my fried there talking to some Belgian beauty for an early return to England. I wanted to park my plane at the grass airfield in Salisbury in Wiltshire, home of the tallest cathedral in England, which I nearly took out several time. The problem was that the runway had no lights.

Unfortunately, I ran into an Atlantic headwind and was running late, so I skipped a refueling stop at Ostend. When My instruments showed I was right over the airfield, I saw nothing but black.

I did, however, remember the radio frequency of the pub at the end of the field which constantly kept a speaker on. I radioed the pub, “if anyone will roll up some newspapers set them on fire and line the runway, I will buy them a pint of beer.”

The entire pub emptied out and within secondss I had a perfectly lighted runway on both sides. Landing was a piece of cake.

When I taxied up to the pub, the starboard engine ran out of gas. I walked in and made good on my promise, even buying a second round for my rescuers. I then crawled back into my airplane and went to sleep, waking up the next day with the worst hangover ever.

My flying these days is much more sedentary. The FAA requires me to do three take offs and landings every three months to keep my license current, and I usually bring along my kids for this chore. On the last landing, I always shut off my engine and glide in.

I warn the kids and they always say, “No dad, don’t,” but I do it anyway. I tell them it’s the only way to practice engine failures.

As I said before, I crash better than anyone I know.

I think I’ll watch the John Wayne classic “The Searchers” one more time tonight.

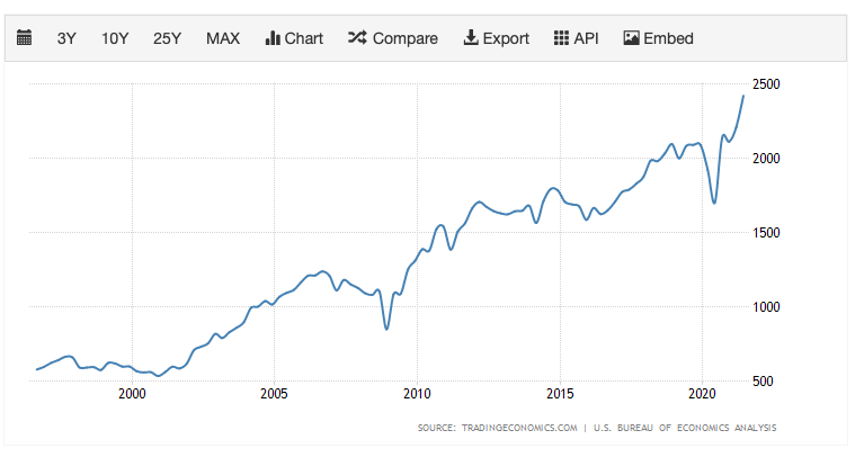

US Corporate Profits Through End 2020

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/US-corporate-profits-1.png466864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-07 09:02:342021-09-07 10:27:05The Market Outlook for the Week Ahead, or the “Endless Bid” Market

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE HIGHER WE GO THE CHEAPER WE GET),

(JPM), (BAC), (C), (GS), (MS), (BLK), (FCX), (X),

(WYNN), (MGM), (ALK), (LUV), (HAL), (SLB), (TLT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-30 09:04:272021-08-30 10:28:16August 30, 2021

I am sitting here holed up in my office in San Francisco.

Lake Tahoe is being evacuated as the Caldor fire is only ten miles away and the winds are blowing towards it. The visibility there is no more than 500 yards. The ski resorts are pointing their snow cannons towards their buildings to ward off flames.

Conditions are not much better here in Fog City. We are under a “stay at home” order due to intense smoke and heat. Even here, the fire engines are patrolling by once an hour.

The Boy Scout trip got cancelled this weekend, so the girls are having a cooking competition, chocolate chip waffles versus a German chocolate cake.

To make matters worse, I have been typing with only one finger all week, thanks to the elbow surgery I had on Tuesday. Next time, I’ll think twice before taking down a 300-pound steer. When I told the doctor how I incurred this injury, he laughed. “At your age?”

Which leaves me to contemplate this squirrelly stock market of ours. I have always been a numbers guy. But the higher the indexes rise, the cheaper stocks get. That’s not supposed to happen, but that is the fact.

We started out 2021 with an S&P 500 price earnings multiple of 25X. Now, we are down to a lowly 21X and the (SPY) is 20% higher, rising from $360 to $450.25.

The analyst community, ever the lagging indicator that they are, had S&P forward earnings for 2022 all the way down to $175. They have been steadily climbing ever since and are now touching $200 a share.

This is what 20/20 hindsight gets you. That and $5 will get you a cup of coffee at Starbucks. It takes a madman like me to go out on a limb with high numbers and then be right.

So what follows an ever-cheaper market? A more expensive one. That means stocks will continue to my set-in-stone target of $475 for the (SPY) for yearend, and (SPY) earnings of over $200 per share.

It gets better.

(SPY) earnings should hit $300 a share by 2025 and $1,400 a share by 2030. That makes possible my (SPY) target of $1,800 and my Dow Average target of 240,000 in a decade.

What are markets getting right that analysts and bears are getting wrong?

The future has arrived.

The pandemic brought forward business models and profitability by a decade. Technology is hyper-accelerating on all fronts.

Cycles are temporary but adoption is permanent. We are never going back to the old pre-pandemic economy. As a result, stocks are now worth a lot more than they were only two years ago.

So what do we buy now? There is a second reopening trade at hand, the post-delta kind. That means buying banks (JPM), (BAC), (C), brokers (GS), (MS), money managers (BLK), commodities (FCX), (X), hotels (WYNN), (MGM), airlines (ALK), (LUV), and energy (HAL), (SLB).

And what do we avoid like the plague? Bonds (TLT), which offer only confiscatory yields in the face of rising inflation with gigantic negative interest rates.

As for technology stocks, they will go sideways to up small in the aftermath of their ballistic moves of the past three months.

You all know that I am a history buff and there are particular periods of history that are starting to disturb me.

In August, we saw ten new intraday highs for the S&P 500 (SPY). That has not happened since 1987. Remember what happened in 1987?

We have not seen 11 new highs in August since 1929. The only negative three months seen since 1929 are August, September, and October. Remember what happened in 1929?

If that doesn’t scare the living daylights out of you, then nothing will. So, it seems we are in for some kind of correction, even if it’s just the 5% kind.

As for me, I’m looking forward to 2030.

The “Everything” Rally is on, according to my friend, Strategas founder Tom Lee. You can see it in the recent strength of epicenter stocks like energy, hotels, airlines, and casinos. It could run into 2022.

The Taper is this year and interest rate rises are later, said Jay Powell at Jackson Hole last week. Markets will be jumpy, especially bonds. Fed governor Jay Powell’s every word was parsed for meaning. Dove all the way. The larger focus will be on the August Nonfarm Payroll report out this week. Pfizer Covid vaccination gets full FDA approval, requiring millions more to get shots and bringing forward the end of the pandemic. All 5 million government employees will now get vaccinated, including the entire military. It’s the fastest drug approval in history. Some 37,000 new cases in one day. The stock market likes it. Take profits on (PFE) Bitcoin tops $50,000 after breaking several key technical levels to the upside. Next stop is a double top at $66,000. It helps that Coinbase is buying $500 million worth of crypto for its own portfolio. Buy (COIN) on dips. The US Dollar will crash in coming years, says Jeffry Gundlach and I think he is right. Emerging markets will become the next big play but not quite yet. Gold (GLD) will be a great hideout once it comes out of hibernation. China will soon return to outperforming the US. The dollars reserve currency status is at risk. The lumber crash is saving $40,000 per home, says Toll Brothers (TOL) CEO, Doug Yearly. Last year, lumber prices surged from $300 per board foot to an insane $1,700, thanks to a Trump trade war with Canada and soaring demand. It all flows straight through the bottom line of the homebuilders which should rally from here. Buy (TOL) on dips. China’s crackdown creates investment opportunities, says emerging investing legend Mark Mobius. He sees corporate governance improving over the long term. The gems are to be found among smaller companies not affected by Beijing’s hard-line. Mobius loves India too. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a healthy +7.62% gain in August. My 2021 year-to-date performance appreciated to 76.83%. The Dow Average was up 15.87% so far in 2021.

That leaves me 80% in cash at 20% in short (TLT) and long (SPY). I’m keeping positions small as long as we are at extreme overbought conditions.

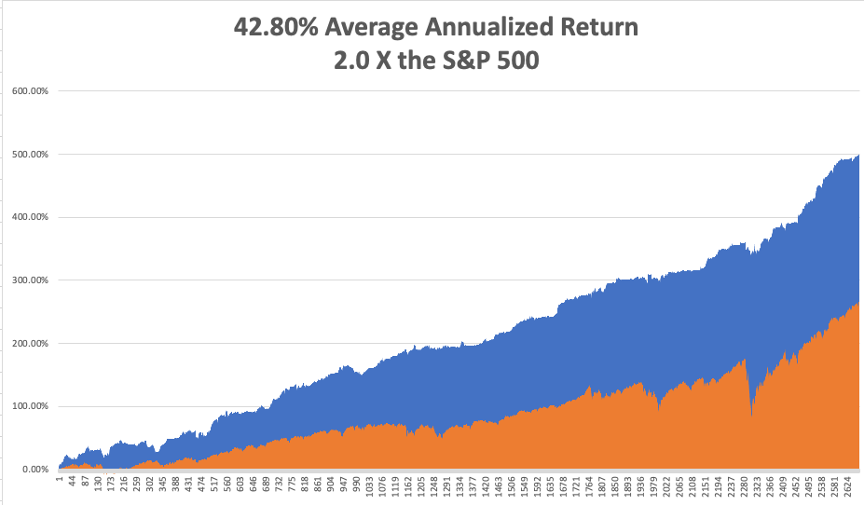

That brings my 12-year total return to 499.38%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.80%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 116.67%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 39 million and rising quickly and deaths topping 638,000, which you can find here.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 30 at 11:00 AM, Pending Home Sales are published. Zoom (ZM) reports.

On Tuesday, August 31, at 10:00 AM, S&P Case Shiller National Home Price Index for June is released. CrowdStrike (CRWD) reports.

On Wednesday, September 1 at 10:45 AM, the ADP Private Employment report is disclosed.

On Thursday, September 2 at 8:30 AM, Weekly Jobless Claims are announced. DocuSign (DOCU) reports.

On Friday, September 3 at 8:30 AM, the all-important August Nonfarm Payroll report is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

Oh and the German chocolate cake won, but please don’t tell anyone.

As for me, given the losses in Afghanistan this week, I am reminded of my several attempts to get into this troubled country.

During the 1970s, Afghanistan was the place to go for hippies, adventurers, and world travelers, so of course, I made a beeline for straight for it.

It was the poorest country in the world, their only exports being heroin and the blue semiprecious stone lapis lazuli, and illegal export of lapis carried a death penalty.

Towns like Herat and Kandahar had colonies of westerners who spent their days high on hash and living life in the 14th century. The one cultural goal was to visit the giant 6th century stone Buddhas of Bamiyan 80 miles northwest of Kabul.

I made it as far as New Delhi in 1976 and was booked on the bus for Islamabad and Kabul ($25 one-way). Before I could leave, I was hit with amoebic dysentery.

Instead of Afghanistan, I flew to Sydney, Australia where I had friends and knew Medicare would take care of me for free. I spent two months in the Royal North Shore Hospital where I dropped 50 pounds, ending up at 125 pounds.

I tried to go to Afghanistan again in 2010 when I had a large number of followers of the Mad Hedge Fund Trader stationed there, thanks to the generous military high-speed broadband. The CIA waved me off, saying I wouldn’t last a day as I was such an obvious target.

So, alas, given the recent regime change, it looks like I’ll never make it to Afghanistan. I won’t live long enough to make it to the next regime change. It’s just one more concession I’ll have to make to my age. I’ll just have to content myself reading A One Thousand and One Nights at home instead. The Taliban blew up the stone Buddhas of Bamiyan in 2001.

In the meantime, I am on call for grief counseling for the Marine Corps for widows and survivors. Business has been thankfully slow for the last several years. But I’ll be staying close to the phone this weekend just in case.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

India in 1976

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-india.png576864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-30 09:02:562021-08-30 10:27:35The Market Outlook for the Week Ahead, or The Higher We Go the Cheaper We Get

Below please find subscribers’ Q&A for the August 25 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from The Atlantis Casino Hotel in Reno, NV.

Q: How does a 2X ProShares Ultra Technology ETF (ROM) February 2022 vertical bull call spread on the ROM look? Would you do $110-$115 or $115-$120?

A: I would do nothing here at $112.50 because we’ve just gone up 10 points in a week. I’d wait for some kind of pullback, even just $5 or $10 points, and then I would do the $110-$115. I’m leaning towards more conservative LEAPS these days—bets that the market goes sideways to up small rather than going ballistic, which it has done for the last 18 months. Think at-the-money strikes, not deep out-of-the-money on your LEAPS from here on for the rest of this economic cycle. The potential profits are still enormous. The only problem with (ROM) is that the longest maturities on the options are only six months.

Q: How do you recommend entering your long-term portfolio?

A: I would use the one-third rule: you put on ⅓ now, ⅓ higher or lower later on, and ⅓ higher or lower again. That way you get a good average price. Long term, everything goes up until we hit the next recession, which is probably several years off.

Q: I keep reading that the Delta variant is a market risk, but I don’t think that investors will look through this. Is Delta already priced into the shares?

A: Yes, what is not priced into the shares is the end of Delta, the end of the pandemic—and that will lead to my “everything” rally that I’ve been talking about for a month now. And we have already seen the beginning of that, especially with the price action this week. So yes, Delta in: dead market; Delta out: roaring market.

Q: Do you think there will eventually be a rotation into emerging markets (EEM), or has the virus battered these markets too much to even consider it?

A: Sometime in our future—not yet—the emerging markets will be our core holding. And the trigger for that will be the collapse of the dollar, which is hitting an interim high right now. When the greenback rolls over and dies, you can expect emerging markets, especially China, to take off like a rocket. That’s going to be our next big trade. I don't know if it will be this year or next year but it’s coming, so start doing your emerging market research now, and keep reading my newsletter.

Q: Is the coming tax hike a problem for the stock market?

A: No, I don’t think so. First off, I don’t think they’re going to do a tax bill this year; they don’t want anything to interfere with the 2022 election, so it may be next year’s business. Also, any new taxes are going to be overwhelmingly focused on billionaires, carried interest, offshoring, and large corporations. The middle class, people who make less than $400,000 a year, will not see any tax hike at all, possibly even getting some tax cuts via restored SALT deductions. So, I don't really see it affecting the stock market at all.

Q: What do you think about Chinese stocks (FXI)?

A: Long-term they’re okay, short term possibly more downside. Interestingly, the bigger risk may not be China itself and how the government is beating up its own tech companies, but the SEC. It has indicated they don’t really like these offshore vehicles that have been listed on the New York Stock Exchange, and they may move to ban them. I’m not rushing into China right now, only because there are just so many better opportunities in the US stock market for the time being. I may go back in the future—it’s a case where I’d rather buy them on the way up than trying to catch a falling knife on China right now.

Q: Do you expect any market impact from the Jackson Hole meeting?

A: Yes, whatever J Powell says, even if he says nothing, will have a market impact. And it will have a bigger impact on the bond market than it will on the stock market, which is down a full point this morning. So yes, but not yet. I imagine we’ll hear something very soon.

Q: September and October tend to be volatile; do you see us having a 5% or 10% pullback in those months?

A: I don’t see any more than 5%, with the hyper liquidity that we have in the system now. There just aren’t any events out there that could trigger a pullback of 10%—no geopolitical events, and the economy will be getting stronger, not worse. So yes, an “everything rally” doesn’t give you many long side entry points, so I just don’t see 10% happening.

Q: What about a Walt Disney (DIS) January 2022 $180-$220 LEAPS?

A: I would do the $180-$200. I think you can afford to be tighter on your spread there, take some more risk because I think it’s just going to go nuts to the upside once we get a drop in COVID cases. By the way, Disney parks are only operating at 70% capacity, so if you go back up to 100% that's a near 50% increase in profits for the company. And it’s not just Disney, but Netflix (NFLX), Amazon (AMZN), and everybody else that’s about to have the greatest number of blockbuster movies released of all time. They’re holding back their big-ticket movies for the end of the pandemic when people can go back into theaters. We’ll start seeing those movies come out in the last quarter of this year, and I’m particularly looking forward to the next James Bond movie, a man after my own heart.

Q: Are EV car charging companies like ChargePoint Holdings (CHPT) going to do as well as the car companies?

A: No. They’re low margin business, so it’s not a business model for me. I like high-profit margins, huge barriers to entry, and very wide moats, which pretty much characterizes everything I own. The big profits in EVs are going to be in the cars themselves. Charging the cars is a very capital-intensive, highly regulated, and low-margin business.

Q: Would a Fed taper cause a 10% pullback?

A: Absolutely not; in fact, I think a taper would make the market go up because Jay Powell has been talking it into the market all year. And that’s his goal, is to minimize the impact of a taper so when they finally do it, they say ho-hum and “okay you can take that risk out of the market.” That’s the way these things work.

Q: What is your yearend target for United States Treasury Bond Fund (TLT)?

A: $132. Call it bold, but I'm all about bold. I think the first stop will be at $144, then $138, then bombs away!

Q: What will it take for (TLT) to dip below $130?

A: Another year of hot economic growth, which Congress seems hell-bent on delivering us.

Q: What are your ProShares Ultra Short 20+ Year Treasury ETF (TBT) targets?

A: When we were at 1.76% on the 10-year bond, the (TBT) made it all the way back to 22 ½. Next year we go higher, probably to $25, maybe even $30.

Q: What’s your 10-year view on the (TBT)?

A: $200. That’s when you get interest rates back to 10% in 10 years on the 10-year bond. So yes, that’s a great long-term play.

Q: How long can we hold (TBT)?

A: As long as you want. Ten years would be a good time frame if you want to catch that $17 to $200 move. The (TBT) is an ETF, not an option, therefore it doesn’t expire.

Q: Are you working on an electrification stock list?

A: I am not, because it’s such a fragmented sector. It’s tough to really nail down specific stocks. I think it’s safe to say that the electric power grid is going to change beyond all recognition, but they won’t necessarily be in high margin companies, and I tend to prefer high-profit-margin, large-moat companies which nobody else can get into, like Apple (AAPL) or Google (GOOG).

Q: What about gas pipelines with high yields?

A: They have a high yield for a reason; because they’re very high risk. If you're going to a carbon-free economy, you don’t necessarily want to own pipelines whose main job is moving carbon; it’s another buggy whip-type industry I would avoid. I’ve seen people get wiped out by these things more times than I could count. If you remember Master Limited Partnerships, quite a few of them went bankrupt last year with the oil crash, so I would avoid that area. These tend to be very highly leveraged and poorly managed instruments.

Q: Best play on silver (SLV)?

A: Wheaton Precious Metals (WPM) is the highest leveraged silver play out there, and a great LEAPS candidate. Go out 2 years and triple your money.

Q: Geopolitical oil (USO) risks?

A: No, nobody cares about oil anymore—that’s why we’re giving up on Afghanistan. China is buying 80% of the Persian Gulf oil right now. We don’t really need it at all, so why have our military over there to protect China’s oil supply?

Q: What about Freeport McMoRan (FCX)?

A: I absolutely love it. Any big economic recovery can’t happen without copper, and you have a huge tailwind there from electric cars which need 200 pounds of copper each, as opposed to 20 pounds in conventional cars.

Q: I see AMC Entertainment Holdings (AMC) is up 20% today; should everyone be chasing this stock?

A: No, absolutely not. (AMC) and all the meme stocks aren’t investments, they’re gambling, and there are better ways to gamble.

Q: Should I buy the lumber dip?

A: Yes. I think the slowdown on housing is temporary because it will take 10 years for supply and demand in the housing market to come back into balance because of all the millennials entering the housing market for the first time. So, that would be a yes on lumber and all the other commodities out there that go into housing like copper, steel, and aluminum.

Q: Should I put money into Canadian Junior Gold Miners (GDX)?

A: No, I would rather go out and take a long nap first. These are just so high risk, and they often go bankrupt. The liquidity is terrible, and the dealing spreads are wide. I would stick with the bigger precious metal plays like Newmont Mining (NEM), Barrick Gold (GOLD), and Wheaton Precious Metals (WPM).

Q: Is Boeing (BA) a buy here?

A: Yes, we’re back at the bottom end of the trading range for the stock. It’s just a matter of time before they get things right, and the 737 Max orders are rolling in like crazy now that there’s an airplane shortage.

Q: What do you think about Robinhood (HOOD)?

A: I like it quite a lot; I got flushed out of my long position on Friday with a 10% down move. Of course, 90% of my stop losses end up expiring at their maximum profit points, but I have to do it to keep the volatility of the portfolio down. So yes, I’ll try to buy it again on the next dip. The trouble is it’s kind of a quasi-meme stock in its own right, hence the volatility; so I would say on the next 10% down day, you go into Robinhood, and I probably will too.

Q: How are the wildfires around Tahoe?

A: They’re terrible and there are three of them. I did a hike two days ago there, and out of a parking lot with 100 spaces, I was the only one there. It’s the only time I’d ever seen Tahoe deserted in August. With visibility of 500 yards, it's just terrible. Fortunately, I was able to hike without coughing my guts out—it’s not so thick that you can’t breathe.

Q: What do you think of US Steel (X)?

A: I like it, I think the whole industrial commodity complex rallies like crazy going into the end of the year.

Q: As a new member, where is the best place to start? It’s just kind of like drinking from a fire hose.

A: Wait for the trade alerts; they only happen at sweet spots and you may have to wait a few days or weeks to get one since we only like to enter them at good points. That’s the best place to enter new positions for the first time. In the meantime, keep reading all the research, because when these trade alerts do come out, they’re not surprises because I’m pumping out research on them every day, across multiple fronts. Be patient— we are running a 93% success rate, but only because we take our time on entering good trades. The services that guarantee a trade alert every day lose money hand over fist.

Q: If they do delist Chinese stocks, will US investors be left holding the bag?

A: Yes, and that will be the only reason they don’t delist them, that they don’t want to wipe out all current US investors.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (whichever applies to you), then select WEBINARS and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-wine-1.png812562Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-27 10:02:412021-08-27 11:03:48August 25 Biweekly Strategy Webinar Q&A

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on February 2, 2021. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing and you don’t want to remain glued to a screen all day, these are the investments you can make. Then don’t touch them until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red on the spreadsheet.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, the click on the “Long Term Portfolio” button, then “Download.”

Changes

Biotech

Pfizer (PFE) has nearly doubled in six months, while Crisper Therapeutics (CRSP) has almost halved. Since the pandemic, which Pfizer made fortunes on, is peaking and we are still at the dawn of the CRISPR gene editing revolution, the natural switch here is to take profits in (PFE) and double up on (CRSP).

Technology

I am maintaining my 20% in technology which are all close to all-time highs. I believe that Apple (AAPL), (Amazon (AMZN), Google (GOOGL), and Square (SQ) have a double or more over the next three years, so I am keeping all of them.

Banks

I am also keeping my weighting in banks at 20%. Interest rates are imminently going to rise, with a Fed taper just over the horizon, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, keep Morgan Stanley (MS), Goldman Sachs (GS), JP Morgan (JPM), and Bank of America, which will profit enormously from a continuing bull market in stocks. They are also a key part of my” barbell” portfolio.

International

China has been a disaster this year, with Alibaba (BABA) dropping by half, while emerging markets (EEM) have gone nowhere. I am keeping my positions because it makes no sense to sell down here. There is a limit to how much the Middle Kingdom will destroy its technology crown jewels. Emerging markets are a call option on a global synchronized recovery which will take place next year.

Bonds

Along the same vein, I am keeping 10% of my portfolio in a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis so go read Global Trading Dispatch. Eventually, massive over-issuance of bonds by the US government will destroy this entire sector.

Foreign Exchange

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). Eventually, the US dollar will become toast and could be your next decade-long trade. The Aussie will be the best performing currency against the US dollar.

Australia will be a leveraged beneficiary of the synchronized global economic recovery through strong commodity prices which have already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

Precious Metals

As for precious metals, I’m keeping my 0% holding in gold (GLD). From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

I am keeping a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles. The arithmetic is simple. EV production will rocket from 700,000 in 2020 to 25 million in 2030 and each one needs two ounces of silver.

Energy

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

The Economy

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade after this year’s superheated 7% performance.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 700% or more from 35,000 to 240,000 in the coming decade. The American coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again. If I forget, please remind me.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-19 10:02:182021-08-19 12:09:09My Newly Updated Long-Term Portfolio

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

Calling All Options!

Calling All Options!