Global Market Comments

December 11, 2020

Fiat Lux

FEATURED TRADE:

(DECEMBER 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (FXA), (FXE), (FXC), (UUP), (FXB), (ABNB), (DASH), (TAN), (TLT), (TBT), (NZD), (DKNG), (SNOW), (AAPL), (CRSP), (RTX), (NOC)

Global Market Comments

December 11, 2020

Fiat Lux

FEATURED TRADE:

(DECEMBER 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (FXA), (FXE), (FXC), (UUP), (FXB), (ABNB), (DASH), (TAN), (TLT), (TBT), (NZD), (DKNG), (SNOW), (AAPL), (CRSP), (RTX), (NOC)

Below please find subscribers’ Q&A for the December 9 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, NV with my guest and co-host Bill Davis.

Q: Is gold (GLD) about ready to turn around from here?

A: The gold bottom will be easy to call, and that’s when the Bitcoin top happens. In fact, we have a double top risk going on in Bitcoin right now, and we had a little bit of a rally in gold this week as a result. So, longer term you need actual inflation to show up to get gold any higher, and we may actually get that in a year or two.

Q: The US dollar (UUP) has been weak against most currencies including the Canadian dollar (FXC), but Canada has the same problems as the US, but worse regarding debt and so on. So why is the Canadian dollar going up against the US dollar?

A: Because it’s not the US dollar. Canada also has an additional problem in that they export 3.7 million barrels a day of oil to the US and the dollar value have been in freefall this year. Canada has the most expensive oil in the world. So, taking that out of the picture, the Canadian dollar still would be negative, and for that reason I've been recommending the Australian dollar (FXA) as my first foreign currency pick, looking for 1:1 over the next three years. Of the batch, the Canadian dollar is probably going to be the weakest, Australian dollar the strongest, and the Euro (FXE) somewhere in the middle. I don’t want to touch the British pound (FXB) as long as this Brexit mess is going on.

Q: Would you buy the IPO’s Airbnb (ABNB) and Dash (DASH)?

A: No on Dash. The entries to new competitors are low. Airbnb on the other hand is now the largest hotel in the world, and it just depends on what price it comes out at. If it comes out at a stupid price, like 50% over the IPO, I wouldn’t bother; but if you can get close to the IPO price, I would probably buy it for the long term. I think you would have another double if we got close to the IPO price, so that is worth doing. They have been absolutely brilliant in their management and the way they handled the pandemic; they basically captured all the hotel business because if you rent an apartment all by yourself, the COVID risk is much lower than if you go into a Hilton or another hotel. They also made a big push on local travel which was successful. They gave up long-distance travel, and they’re now trying to get you to explore your own area; and that worked beyond all expectations. Even I have rented some Airbnb’s out in the local area like in Carmel, Monterey, Mendocino, and so on and I came back disease-free.

Q: If the United States Treasury Bond Fund (TLT) goes to a 1.00% yield, what would that translate to in the (TBT) (2x short treasury ETF)?

A: My guess is probably about $18, which has been upside resistance for a long time, but it depends on how long it takes to get there. You have about a 3% a year cost of carry on the TBT that you don’t have in Treasuries.

Q: Should we buy China stocks when the current administration is so negative on China?

A: Yes, that’s when you buy them—when the current administration is negative on China; because when you get an administration that’s less negative on China, the Chinese stocks will all rocket. There’s an easy 20-30% in most of the headline Chinese stocks from here sometime in 2021. And I'm looking to add more Chinese stocks. I currently have Alibaba (BABA), and that’s working well. I want to pick up some more.

Q: What about the New Zealand currency ETF (NZD)?

A: It pretty much moves in sync with the Australian dollar, but it’s usually a few cents cheaper and more volatile.

Q: Legalized sports betting seems to be on the upswing. Where do you see DraftKings (DKNG) going?

A: I think it goes up. I think there’s going to be a recovery in all kinds of entertainment type activities. Draft Kings got a huge market share from the pandemic which they will probably keep.

Q: Do we use spreads when playing (FXA)?

A: Yes, you can probably do something like a $70-$72 here one month out and make some decent money.

Q: How do you feel about Snowflake (SNOW)?

A: I wanted to get into this from day one, but it doubled on the IPO, and then it doubled again. It’s one of the only technology stocks Warren Buffet has bought in the last several years besides Apple (AAPL). So, it’s just too popular right now, it’s hotter than hot. They have a dominant market share in their big data platform, so it’s a great place to be but it’s really expensive now.

Q: Do your options trade alerts have any risk of assignment?

A: Yes, they do, but when you get an assignment it’s a gift, because they’re taking you out of your maximum profit point, weeks before the expiration. All you do is tell your broker to use your long position to cover your short position, and you will get the 100% profit right then and there. I say this because the brokers always tell you to do the wrong thing when you get an assignment, such as going into the market to close out each leg separately. That is a huge mistake, and only makes money for the brokers. For more details, log in and search for “assignments” at www.madhedgefundtrader.com

Q: Congratulations on your great performance; what could derail your bullish prediction?

A: Well, we’ve already had a pandemic so obviously that’s not it, and then you have to run by your usual reasons for an out-of-the-blue crash; let’s say Donald Trump doesn't leave the presidency. That would be worth a few thousand points of downside. So would a major war. We could have both; we could have a major war before a disrupted inauguration. The president has essentially unlimited ability to go to war at any time, so there aren’t too many negatives on the near-term horizon, which is why everyone is super bullish.

Q: What’s your opinion on the solar area, stocks like First Solar (FSLR) and the Invesco Solar ETF (TAN)?

A: I’m bullish. Even though they're over 300% since March, we’re about to enter the golden age of solar. Biden wants to install 500,000 solar panels next year and provide the subsidies to accomplish that. This all looks extremely positive for solar. In California, a lot of people will go solar, because getting an independent power supply protects you from the power shut-offs that happen every time the wind picks up, in which response to wildfire danger. We had ten days of statewide power blackouts this year.

Q: What are your thoughts on lithium?

A: I’m not a big believer in lithium because there is no short supply. The key to producing lithium is finding countries with no environmental controls whatsoever because it’s a very polluting and messy process to mine. Better to let other countries mine your lithium cheap, refine it, and then send it to you in finished form.

Q: Since you love CRISPR (CRSP) at $130, what about shorting naked puts? The premiums are really high.

A: I never advocate shorting naked puts. Occasionally, I will at extreme market bottoms like we had in March, but even then, I do it only on a 1 for 1 basis, meaning don’t use any leverage or margin. Never short any more puts than you’re willing to buy the stock lower down. People regularly see the easy money, sell short too many puts, and then get a market correction and a total wipeout of their capital. And they won't have to do that liquidation themselves; their broker will do it for them. They’ll do a forced liquidation of your account and then close it because they don't want to be left holding the bag on any excess losses. You won’t find out until afterwards. So, I would not recommend shorting naked puts for the normal investor. If you want to be clever, just buy an in-the-money call spread, something like a $110-$120 out a couple of months. That's probably a far better risk reward than shorting a naked put. By the way, I came close to wiping out Solomon Brothers 30 years ago because my hedge fund was short too many Nikkei Puts. In the end, I made a fortune, but only after a few sleepless nights (remember that Mark?).

Q: What do you think about defense stock right now?

A: I’m avoiding defense stock because I don’t see any big increases in defense spending in the future administration, and that would include Raytheon (RTX), Northrop Grumman (NOC), and some of the other big defense stocks.

SEE YOU ALL IN 2021!

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 7, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or A DICEY LANDING)

(SPY), (TLT), (AMZN), (TSLA), (CRM), (JPM), (CAT), (BABA),

(FCX), (GLD), (SLV), (UUP), (FXE), (FXA), (FXB), (FXY), (FXI), (EWZ), (THD), (EPU)

Landing my 1932 de Havilland Tiger Moth biplane can be dicey.

For a start, it has no brakes. That means I can only land on grass fields and hope my tail skid catches before I run out of landing strip. If it doesn’t, the plane will hit the end, nose over, and dump a fractured gas tank on top of me. Bathing in 30 gallons of 100 octane gasoline with sparks flying is definitely NOT a good long term health plan.

The stock market is starting to remind me of landing that Tiger Moth. On Friday, all four main stock indexes closed at all-time highs for the first time since pre-pandemic January. A record $115 billion poured into equity mutual funds in November. This has all been the result of multiple expansion, not newfound earnings.

Yet, stocks seem hell-bent on closing out 2020 at the highs.

And there is a major factor that the market is completely ignoring. What if the Democrats win the Senate in Georgia?

If so, Biden will have the weaponry to go bold. The economy goes from zero stimulus to maybe $6 trillion raining down upon it over the next six months. That will go crazy, possibly picking up another 10%, or 3,000 Dow points on top of the post-election 4,000 points we have seen so far.

That is definitely NOT in the market.

The other big decade-long trend that is only just starting is the weak US dollar. Lower interest rates for longer were reaffirmed by the appointment of my former economics professor Janet Yellen as Treasury Secretary.

A feeble dollar brings us a fading bond market, as half the buyers are foreigners. A sickened greenback also provides the launching pad for all non-dollar assets to take off like a rocket, including commodities (FCX), precious metals (GLD), (SLV), Bitcoin, and the currencies (UUP), (FXE), (FXA), (FXB), (FXY), and emerging stock markets like China (FXI), Brazil (EWZ), Thailand (THD), and Peru (EPU).

All of this is happening in the face of a US economy that is clearly falling apart. Weekly jobless claims for November came in at 245,000, compared to a robust 638,000 in October, taking the headline unemployment rate down to 6.9%. The real U6 unemployment rate stands at an eye-popping 12.0%, or 20 million.

Some 10.7 million remain jobless, 900,000 higher than in February. Transportation and Warehousing were up 140,000, Professional & Business Services by 60,000, and Health Care 46,000. Retail was down 35,000 as stores shut down at a record pace.

OPEC cuts a deal, adding 500,000 barrels a day to the global supply. The hopes are that a synchronized global recovery can take additional supply. Texas tea finally busts through a month's long $44 cap, the highest since March. Avoid energy. I’d rather buy more Tesla, the anti-energy.

Black Friday was a disaster, with in-store shopping down 52%. Long lines and 25% capacity restrictions kept the crowds at bay. If you don’t have an online presence, you’re dead. In the meantime, online spending surged by 26%.

Amazon (AMZN) hires 437,000 in 2020, probably the greatest hiring binge since WWII, and is continuing at the incredible rate of 3,000 a week. That takes its global workforce to 1.2 million. Most are $12 an hour warehouse and delivery positions. The company has been far and away the biggest beneficiary of the pandemic as the world rushed to online commerce.

Tesla’s (TSLA) full self-driving software may be out in two weeks, instead of the earlier indicated two years. The current version only works on freeways. The full street to street version could be worth $8,000 a car in upgrades. Another reason to go gaga over Tesla stock.

Goldman Sachs raised Tesla target to $780, the Musk increased market share to a growing market. No threat from General Motors yet, just talk. Volkswagen is on the distant horizon. In the meantime, Tesla super bear Jim Chanos announced he is finally cutting back his position. He finally came to the stunning conclusion that Tesla is not being valued as a car company. Go figure. Short interest in Tesla has plunged from a peak of 35% in March to 6% today. It’s learning the hard way.

The U.S. manufacturing sector pauses, activity in the U.S. manufacturing sector barely ticked up in November as production and new orders cratered, data from a survey compiled by the Institute for Supply Management showed on Tuesday. The ISM Manufacturing Report on Business PMI for November stood at 57.5, slipping from 59.3 in October.

Salesforce (CRM) overpays for workplace app Slack, knocking its stock down 9%. This is worth a buy the dip trade in the short-term and this is still a great tech company which is why the Mad Hedge Tech Letter sent out a tech alert on Salesforce on the dip.

Weekly Jobless Claims dive, with Americans applying for unemployment benefits falling last week to 712,000 down from 787,000 the week before. The weakness is unsurprising as we head into seasonal Christmas hiring.

The end of the tunnel for Boeing (BA) as they bring to an end an awful 2020. Irish-based airline Ryanair Holdings placed a large order for a set of brand new Boeing 737 MAX aircraft, giving the plane maker a shot in the arm as the single-aisle jet comes off an unprecedented 20-month grounding.

Ryanair, Europe’s low-cost carrier, has 135 Boeing 737 MAX jets on order and options to bring the total to 200 or more. Hopefully, they won’t crash this time around. My fingers are crossed.

Dollar Hits 2-1/2 Year Low. With global economies recovering, the next big-money move will be out of the greenback and into the Euro (FXE), the Aussie (FXA), the Looney (FXC), the Japanese yen (FXY), the British pound (FXB), and Bitcoin. Keeping interest rates lower for longer will accelerate the downtrend.

When we come out the other side of this pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

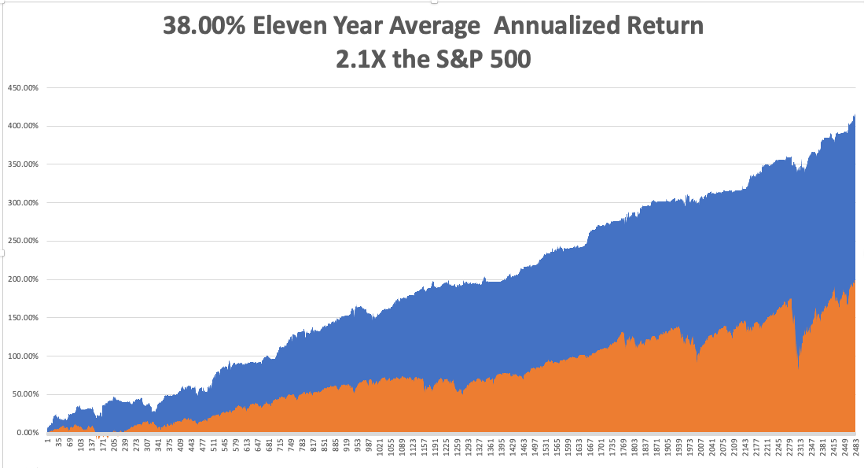

My Global Trading Dispatch catapulted to another new all-time high. December is up 5.34%, taking my 2020 year-to-date up to a new high of 61.78%.

That brings my eleven-year total return to 417.69% or double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.00%. My trailing one-year return exploded to 64.56%. I’m running out of superlatives, so there!

I managed to catch the 50%, two-week Tesla melt-up with a 5X long position, which is always nice for performance.

The coming week will be a slow one on the data front. We also need to keep an eye on the number of US Coronavirus cases at 14.5 million and deaths at 285,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, December 7 at 4:00 PM EST, US Consumer Credit is out.

On Tuesday, December 8 at 11:00 AM, the NFIB Business Optimism Index is published.

On Wednesday, December 9 at 8:00 AM, MBA Mortgage Applications for the previous week are released.

On Thursday, December 10 at 8:30 AM, the Weekly Jobless Claims are published. At 9:30 AM, US Core Inflation is printed.

On Friday, November 11, at 9:30 AM EST, the US Producer Price Index is announced. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, at least there is one positive outcome from the pandemic. Boy Scout Christmas tree sales are absolutely through the roof! We took delivery of 1,300 trees from Oregon for our annual fundraiser expected to sell them in two weeks. We cleared out our entire inventory in a mere six days!

We sold trees as fast as we could load them. With the scouts tying the knots, only one fell onto the freeway on the way home. An “all hands on deck” call has gone out to shift the inventory.

It turns out that tree sales are booming nationally. The $2 billion a year market places 21 million trees annually at an average price of $8 and are important fundraisers for many non-profit organizations. It seems that people just want something to feel good about this year.

Governor Gavin Newsome’s order to go into a one-month lockdown Sunday night inspired the greatest sales effort I have ever seen, and I worked on a Morgan Stanley sales desk! We shifted the last tree hours before the deadline, which was full of mud with broken branches and had clearly been run over by a truck at a well-deserved 50% discount.

I can’t wait until next year!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

December 3, 2020

Fiat Lux

FEATURED TRADE:

(WHATEVER HAPPENED TO THE GREAT DEPRESSION DEBT?),

($TNX), (TLT), (TBT),

Global Market Comments

November 30, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SANTA COMES EARLY),

(SPY), (TLT), (TSLA), (JPM), (CAT), (BABA)

Everyone has been expecting a Santa Claus rally this year, but it looks like the jolly old man arrived early.

The holiday-shortened month was the best for stocks in 37 years. If you owned Tesla, like we did, it was even better. Elon Musk’s miracle creation shot up an incredible 60% this month.

At $600 a share, the company’s market capitalization expanded by an eye-popping $363 billion to $580 billion, the fastest wealth creation in history. The gain alone would rank it as the 55th largest company in the S&P 500. Similarly, Elon himself earned $100 billion this year, or $17 million an hour, the speediest wealth accumulation since capitalism begin.

These are numbers for the ages.

It’s all proof that if you live long enough, you see everything. OK, all of you who thought the Dow would soar by 12,000 points, or 67% in eight months, please raise your hands. Yes, I didn’t think I’d see many.

Which all raises some concerns for me. But then I’m always concerned. That’s why I’m still alive. That’s why I still have two nickels to rub together. My Mad Hedge Market Timing Index shouting “EXTREME SELL” urges further caution.

Rising at this meteoric pace, the market is pulling forward a big chunk of gains from 2021. Make hay while the sun shines because we may suffer long periods of boredom next year, when the Volatility Index (VIX) drops down to $10 and stays there.

It all reminds me of the Plaza Accord in 1987, when Japan agreed to a doubling of the yen against the US dollar in exchange for continued access to the US car market.

We all knew this would eventually demolish the Japanese stock market, but not for a while. I remember at the time, an old Japanese folk expression became popular. “The fool may be dancing, but the greater fool is watching.” The Nikkei Average doubled in three years before it crashed. Portfolio managers who only watched were left to pull rickshaws for a living. (This was before Uber).

This is why I have been urging followers to realize their biggest profits, as in Tesla, so they have dry powder with which to buy the next inevitable dip. And you don’t want to be left pulling a rickshaw.

The US Treasury delivered a hit for stocks, as outgoing Secretary Mnuchin cancels all remaining stimulus programs, sucking $459 billion out of the economy. It has so far prompted a $740-point dive in the Dow Average and a $7 rally in the TLT. It’s the ultimate scorched earth strategy that will prolong the recession. Use this move to buy more stocks (SPY) and sell short more bonds (TLT).

Janet Yellen was appointed the new Treasury Secretary in the incoming Biden administration. My old Berkeley economic professor wins again. She is probably the most qualified secretary ever appointed and as academic and former Fed governor. It looks like I may serve as an informal consultant on financial and monetary affairs like I did last time. I drove by her house last week and the vans were already loading up. The markets love her, with the Dow up 500 points and hitting 30,000. Janet is the Queen of Ease and the Master of QE, running a hyper-accommodative policy for five years.

Money is pouring into Asia. First into the pandemic, China was first out. With the most draconian lockdown yet seen, the Middle Kingdom was able to cap total deaths at 4,000. The US is now losing that number of people every two days….with one fourth the population. As a result, China now has the world’s strongest economy, growing at a 6.6% annual rate. The incoming Biden administration will lead to a major improvement in trade relations, bringing us back to a return of globalization. All of this is hugely positive for China.

Tesla tops $580 billion in market cap with a ballistic 37% move since its S&P 500 listing was announced two weeks ago. Look like Elon is due for another $20 billion bonus. Mad Hedge went into this with an aggressive 40% long weighting, making it the best trade of 2020, if not the decade. Tesla is my next trillion-dollar company.

Bitcoin crashed, down nearly $4,000 in 24 hours, or almost 20%. As is always the case with an asset with no fundamentals, nobody knows why as the cryptocurrency tests $16,000, down from $20,000. Fears of increased US regulation may be a factor.

New Home Sales exploded, up 41% YOY to 999,000, and gaining 1.5% in October. It’s the hottest since 2006. Homes sold but still under construction are up 60% YOY. Inventories plunged to 3.5 months and prices are rising due to shortages of labor and materials. This is where inflation begins.

Weekly Jobless Claims leaped to 778,000. The Coronavirus is felling people in the labor force in large numbers. Workers are losing jobs, benefits, and health care just as the pandemic goes exponential.

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

This has been the best week, month, and year in the 13-year history of the Mad Hedge Fund Trader, and the week was only three and a half days long!

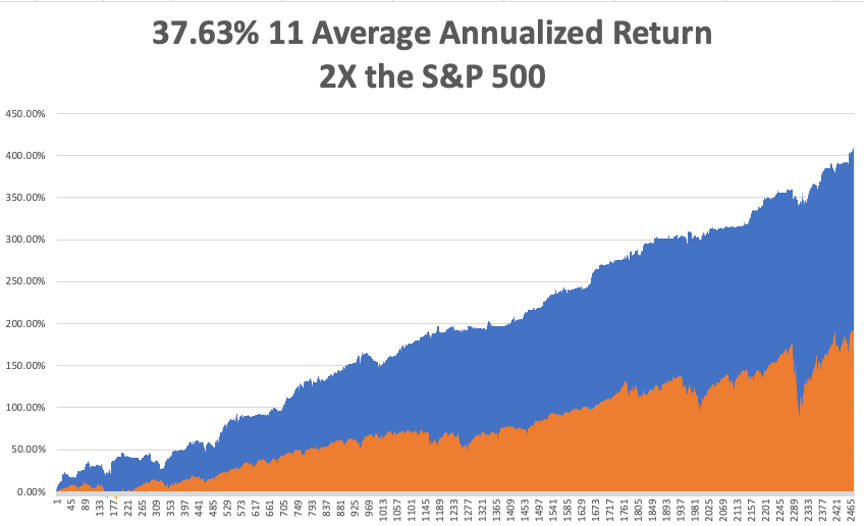

My Global Trading Dispatch catapulted to another new all-time high. November is up 22.06%, taking my 2020 year-to-date up to a new high of 58.09%.

That brings my eleven-year total return to 414.00% or double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 37.63%. My trailing one-year return exploded to 64.91%. I’m running out of superlatives, so there!

I managed to catch the 50%, two-week Tesla melt-up with a rare quadruple long position, which is always nice for performance.

The coming week will be all about jobs. We also need to keep an eye on the number of US Coronavirus cases at 13 million and deaths 270,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, November 30 at 11:00 AM EST, Pending Home Sales for October are released.

On Tuesday, December 1 at 11:00 AM, The ISM Manufacturing Index for November is out.

On Wednesday, December 2 at 9:15 AM, the ADP Private Employment Report is printed.

On Thursday, December 3 at 9:30 AM, the Weekly Jobless Claims are published.

On Friday, December 4 at 8:30 AM, the Nonfarm Payroll Report for November is called. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, it’s Christmas tree season for the Boy Scouts again, so I just spent the morning unloading 700 conifers from a semi-truck that just arrived from Corvallis, Oregon. The scouts sell them to raise money for camping trips for the upcoming year. Some of the trees were 12 feet high and two men had to struggle to get them in place.

Last week, I took the scouts to Hendy State Park in northern Mendocino county. We were the only ones camping among the 2,000 year old giant redwoods, but all the RV sites were full. I realized then that tens of thousands are riding out the pandemic and the Great Depression in the California State Park system, rotating locations every two weeks to keep from being kicked out. These are our modern-day “Hooverville’s.”

It’s a sign of the times.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 23, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE VACCINE PUT IS IN),

($INDU), (SPY), (TLT), (GLD), (TSLA)

You’ve all heard of the Fed Put which has put a floor under stock markets for the past decade, although it didn’t work so well this year.

Now, we have the Vaccine Put. Traders and investors have been more than willing to look through the pandemic to the other side, when multiple vaccines bring an end to the pandemic next summer.

That explains the ballistic $3,800 point rally in the Dow Average that launched in the run-up to the election. At 200,000 new cases and 2,000 deaths a day, we are losing the battle, but the cavalry is on the way and we can even hear the bugles.

That’s why I have recently been more aggressive in the market than usual, breaking all of my 13-year performance records. I don’t expect a market correction of more than 6% from here, or $1,800 Dow points. All of my current positions are geared to handle such a hit. After that, the market runs to new all-time highs.

We have ample reasons to see that 6% drawdown. While the pandemic rages, the president plays golf. Treasury Secretary Steven Mnuchin has moved to cancel the stimulus program in progress, despite vociferous Fed opposition. It was enough to prompt a $300 point selloff in the Dow and a near $2.00 spike in the bond market (TLT).

It is a scorched earth policy the Russians would be proud of. Trump is attempting to saddle Biden with a deeper depression and worse pandemic that will take longer to get out of. You and I will pay the price. In the meantime, there is a bull market in refrigerator trucks.

But if you believe that the Dow is headed for $120,000 in a decade as I do, why bother selling to avoid a mere $1,800 correction? You’d probably miss the bottom and the next leg up.

American Consumers are loaded with cash, after enduring a spending diet that is approaching a year. No business travel, no vacations, no shopping. Debt service ratios are also at decade lows, thanks to ultra-low interest rates. It all sets up a new American Golden Age starting in 2021.

Moderna announces 94.5% effective vaccine, triggering another monster rally in stocks for the second week in a row. The vaccine seems to block all of the most severe cases. Seniors may be able to get it by April. Mad Hedge Biotech Letter subscribers made a killing, getting into (MRNA) a year ago, pre-pandemic. Keep buying (MRNA) on dips. As for me, I’m running out of longs as they have all worked.

Mass tourism will return this summer after we all get our shots, says the CEO of Expedia, Peter Kern. The discount airline ticket reseller has been hanging on by its fingernails for the past nine months and just announced horrific earnings. Hint: this is not Rome’s first plague. A lot of travel businesses will get under, then resurface under new ownership. Summer booking is already picking up.

Tesla joins the S&P 500 and at a $480 billion market cap is the largest new entrant ever to do so. The stock was up a mind-blowing $108, or 27% on the news. This opens up new categories of institutional investors for Elon Musk’s dream come true, such as the $4.5 trillion in (SPX) index funds, which are now required by law to buy it. It gives the (SPX) more of a technology bent.

S&P finally got past the issue that most of the company’s profits come from ZEV, or green credits. Goldman Sachs figures that this will generate at least $9 billion of net buying of Tesla shares when there are no sellers. At this point, Tesla is the largest position of most Mad Hedge followers, primarily through capital appreciation.

Warren Buffet is pouring money into big pharma, and maybe you should too. It’s the cheapest sector in the market. AbbVie (ABBV), Bristol Myers (BMY), Merck (MRK), and Pfizer (PFE) were his biggest picks, according to regulatory filings, all names well known to the subscribers of the Mad Hedge Biotech & Healthcare Letter. It’s not all about Covid-19. Every major human disease will be cured in the next decade, spinning of billions in profits.

Homebuilders Sentiment Index breaks new record, at 90. The residential real estate market is on fire. After a great run, the homebuilders are still getting fabulous data. Builders are seeing supply shortages everywhere. Buy (LEN), (DHI), and (KBH) on dips. This trend has another decade to run.

Housing Starts rocket in October to a staggering 1.53 million, the highest since the last housing bubble top in 2007. Good luck finding something for sale. Which vacation destination resort is seeing the highest growth in sales? Good old Incline Village, NV, up 87% YOY. Many are buying homes after simply looking at zoom videos. Could housing be presaging what the entire economy is going to do in 2021? Buy everything on dips!

The Boeing 737 MAX flies again, with the beleaguered company regaining FAA certification after a 20-month break. It’s amazing this company is still alive after the grounding of its main product and thousands of order cancellations from the pandemic. Taking their debt from $9 billion up to an eye-popping $63 billion is what did it. American Airlines (AA) will be the first to take the troubled aircraft back to the skies. Buy (BA) on dips.

Global Debt to hit $227 trillion by end of 2020, thanks to the pandemic. Governments accounted for half of the increase. US Debt jumped from $71 in 2019 to $80 trillion. Sounds like a short to me! Sell (TLT) on every five-point rally.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

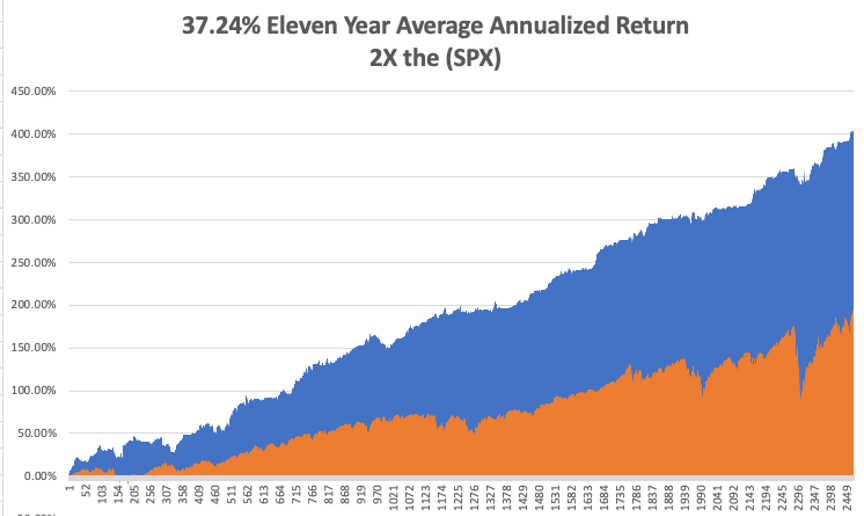

My Global Trading Dispatch exploded to another new all-time high last week. November is up 14.70%, taking my 2020 year-to-date up to a new high of 50.73%. That brings my eleven-year total return to 406.64% or double the S&P 500 over the same period. My 11-year average annualized return now stands at a new high of 37.24%. My trailing one-year return exploded to 58.48%.

It was a week of profit-taking on my November expiring positions and rolling forward to a new batch of December options. I managed to catch the Tesla melt-up with a double long position, which is always nice for performance.

My only hickey of the week was a short in the (SPY) which I was forced out of in the tag ends of this rally. Four days later, they expired at their maximum profit point.

The coming week will be a sleeper thanks to the national holiday. We also need to keep an eye on the number of US Coronavirus cases and deaths, now over 11.5 million and 250,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, November 23 at 9:30 AM EST, the Chicago Fed National Activity Index for October is released.

On Tuesday, November 24 at 10:00 AM EST, the S&P Case Shiller National Home Price Index for September is announced.

On Wednesday, November 25 at 9:30 AM EST, the Weekly Jobless Claims are announced a day early because of the holiday. The Q3 US GDP second estimate is printed at the same time.

On Thursday, November 26 Americans celebrate Thanksgiving Day. All markets are closed.

On Friday, November 27, no data points are released.

As for me, thanks to the pandemic I have been watching a lot more TV lately. I have started watching The Crown on Netflix, which is fascinating for me because I personally knew most of the royal family.

I’ll never forget the chief of protocol loudly calling out my name, “Captain John Thomas”, at the Buckingham Palace garden party where I met Queen Elisabeth and Lady Diana.

I also knew many of the postwar prime ministers, including the Iron Lady, Margaret Thatcher. She despised my macroeconomic press conference questions at a time when UK unemployment rate was a sky-high 14% and the pound was in free fall. Still, she toughed it out.

During the Falklands War, I was the Washington Bureau Chief for The Economist magazine. One day, an unusual message came through from London which I was asked to personally take to my old friend, CIA Director William J. Casey. It was a list of 10,000 military items which the British military needed delivered to the South Atlantic in 24 hours! And you know what? They did it!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 16, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or RAIDING THE PIGGY BANK),

(SPY), ($INDU), (JPM), (CAT), (UNP), (UPS), (SLV), (TLT), (TSLA)