Global Market Comments

November 16, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or RAIDING THE PIGGY BANK),

(SPY), ($INDU), (JPM), (CAT), (UNP), (UPS), (SLV), (TLT), (TSLA)

Global Market Comments

November 16, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or RAIDING THE PIGGY BANK),

(SPY), ($INDU), (JPM), (CAT), (UNP), (UPS), (SLV), (TLT), (TSLA)

I remember the last time that the market went up 10% in ten days.

In the fall of 1982, I was in the office of Carl Van Horn, the chief investment officer of JP Morgan Bank. I was interviewing him about the long-term prospects for the stock market with the Dow Average at 600 and gurus like Joe Granville predicting Dow 300 by yearend.

The odd thing about the interview was that he kept ducking out of the room for a minute at a time and then coming back in. I finally asked him what he was doing. He answered, “Oh, I had to go out and buy $100 million worth of stock.”

And that was back when $100 million actually bought you something!

Over the last two weeks, the Dow Average has tacked on a historic $4,000 points. For a few fleeting second, it actually touched 30,000. Cassandras everywhere are tearing their hair out.

The monster rally began a few days before the election and has continued unabated. In my view, this is the second leg of a 20-fold move that started in 2009 when the Dow was at 6,000 and will continue all the way up to 120,000 by 2029.

No wonder investors are so bullish! It seems that recently, quite a few have come over to my way of thinking.

And how could they not be so bovine-inclined?

The most contentious election in history over. The pandemic is about to end. In a year we’ll, all have our Covid-19 vaccinations, at least those who want them. I’m planning on getting all six.

The greatest burst of economic growth in history is about to be unleased. Consumption wasn’t destroyed, just deferred into 2021 and 2022, unless you’re in the cruise, airline, or restaurant business. The exponential profit growth unleashed by the pandemic isn’t even close to being discounted.

This hasn’t been just any old rally. Stocks left for dead years ago, the old-line industrials and cyclicals have sprung back to life. Union Pacific (UNP) has exploded. JP Morgan Chase (JNP) has gone off to the races. Caterpillar (CAT) is in orbit.

The great thing about these moves is that it is very early days. They could run for years. But where will the money come from to pay for these? How about raising the big tech piggy bank, which has been leading markets for years and is now wildly overvalued.

However, $4,000 points is a lot. So, we may get some back and fill and a sideways “time” correction before we attempt higher highs by yearend. The only thing that could upset this scenario is if Covid-19 cases explode, which they are now doing.

Where will the market care? Who knows, but like stock prices, US Corona cases have doubled in ten days to 160,000.

Covid-19 is cured! News that Pfizer (PFE) has discovered a Covid-19 vaccine that is 90% effective has sent stocks soaring to new all-time highs! The Dow futures were up $1,800 at the highs pre-market. The Great Depression is over. Recovery stocks like banks, cruise ships, restaurants, energy, and railroads are exploding to the upside, with stay-at-home stocks such as couriers, precious metals, and streaming companies in free fall. Some 500,000 health care workers have priority in getting the two-shot regime. The US Army will begin national distribution almost immediately, but you may not get it until the summer.

Market volatility crashed, with the Volatility Index (VIX) down from $41 last week to $18. Happy times are here again, at least says the market, this minute. I told you to go short last week!

Walt Disney is the best recovery play in the market. With theme parks, hotels, and cruise ships, it had the most exposure of any blue-chip company to the pandemic. It is also best positioned for any recovery. The stock was up 26% at the highs this morning. Only its rock-solid balance sheet gets this company alive. My 2021 target is $200 a share. Back to waiting in lines for hours, packing shoulder to shoulder on rides, and paying $20 for hamburgers.

The end of the depression may be in sight, but the US still faces a massive loan default wave that could erode confidence in the economy. A full economic recovery in a year will be too late for millions of businesses, especially small ones. The Fed says the risks are “severe,” and Disneyland is still laying off workers. Just when you think we are risk-free; we are not.

A big recovery in dividend stocks is coming after sitting in the doghouse for years while big tech hogged the limelight. Phillip Morris (PM) at a 6.7% yield? AbbVie (ABBV) at 5.5%? Williams Co (WMB) at 8.3%? They certainly will draw some buyers in this near-zero interest rate world. High yields REITs are also in for some joy now that a vaccine is on the horizon.

Home Prices are soaring at the fastest rate in seven years. Ultra-low interest rates and a structural shortage create the perfect storm for higher prices. Houses are now seen as “safe” since they didn’t crash 40% like the stock market did in the spring. Mortgage brokers are so overloaded it takes three months to get a refi done. This could continue for another decade.

China’s “Single’s Day” breaks all records, bringing in an eye-popping $116 billion in sales for Alibaba (BABA). US customers were the biggest buyers, eclipsing our “Black Friday” by a huge margin. I told you (BABA) was a “BUY”.

Biden could lock down the economy for 4-6 weeks if new cases keep growing at their current rate. That would knock the pandemic on the nose for good, but is it worth the price? That is an idea making the rounds in the incoming Biden administration. Cases could be peaking at 250,000 a day right around the inauguration. I may not go this year.

Stocks may Go up for years. That’s is what the Volatility Index (VIX) is telling us down here at $22. If we break below $20 and stay there, then the long-term Bull market becomes a sure thing. Stocks are now discounting the end of the pandemic.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

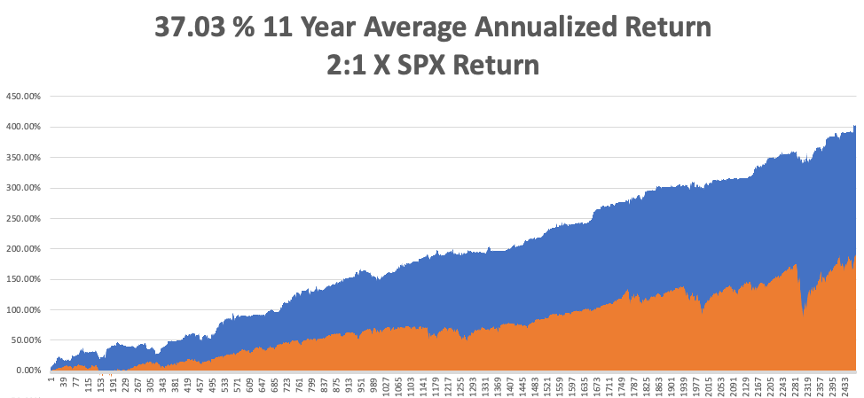

My Global Trading Dispatch exploded to another new all-time high last week. November is up 12.31%, taking my 2020 year-to-date up to a new high of 48.34%. That brings my eleven-year total return to 404.25% or double the S&P 500 over the same period. My 11-year average annualized return now stands at a new high of 37.03%.

It was a week of profit-taking on the fully invested portfolio I piled on just before the election. My one new long was in the silver ETF (SLV) and my one new short was in (TLT), both of which turned immediately profitable. I used the one dip of the week to cover a short in the (SPY) close to cost.

It worked in spades.

The coming week will be a sleeper compared to the previous one. We also need to keep an eye on the number of US Coronavirus cases and deaths, now over 10 million and 240,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, November 16 at 9:30 AM EST, the Empire State Manufacturing Index is out.

On Tuesday, November 17 at 9:30 AM, US Retail Sales are published.

On Wednesday, November 18 at 9:30 AM, US Housing Starts for October are released.

On Thursday, November 19 at 8:30 AM, the Weekly Jobless Claims are announced. At 11:00 AM, the big Existing Home Sales for October are announced.

On Friday, November 13, at 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I’ll be cleaning off the grime from the last Boy Scout trip of the year up to the giant redwoods of north Mendocino County. I haven’t been up there in 13 years and boy has it changed. The vineyards have ground enormous and entire new exurbs have been constructed. There are only a few apple farms left, where I picked up some nice cider, pie, and bags of fresh apples.

There are still a few bits of the old California left.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 9, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE ROARING TWENTIES HAVE JUST BEGUN),

(SPY), (TLT), (TSLA), (CAT), (JPM), (GOLD), (UNP), (UPS), (AMGN)

I have a prediction to make.

If you are unhappy about the election result, the world will still turn, the sun will rise in the east and set in the west, and the moon will continue to wax and wane every month.

There, I promise I won’t talk about politics for another four years unless it’s for the Official Incline Village, Nevada Bear Wrangler.

The plywood has started coming down from storefronts in San Francisco, no doubt stored away for another day. Mass celebrations have broken out everywhere.

It is now back to the serious business of making money.

That is easy for me to do because I have just enjoyed the most profitable week in the 13-year history of the Mad Hedge Fund Trader. From the Thursday low last week, our 2020 year-to-date performance has rocketed by an eye-popping 11.46%. This was a once-in-a-decade setup and I struck while the iron was hot.

For only the third time this year, I went 100% fully invested right before the election, and every position dutifully made money across all asset classes. Stocks (SPY) and gold (GLD) soared, while the US Treasury bond market (TLT) and the US dollar (UUP) crashed. On the stock side, everything went up like the true quantitative easing, liquidity-driven market that it is.

My fundamental call on the market came true. It made no difference who won the election, the mere fact that it is over is a major positive for stocks.

With such a historic move last week, the major indexes have pulled forward performance from the rest of 2020 and possibly a piece of 2021 as well. So, I expect to see sideways chop for the next seven weeks with a slight upward bias.

I don’t need to remind the veterans out there that this is the perfect environment for vertical bull call spreads. We may stay fully invested for a while and shoot for a record performance for 2020.

The chance of a market crash now is effectively zero. If for some reason we do get a 5% pullback, for Heaven’s sake please dive in with both hands. The Roaring Twenties and the next American Golden Age have only just begun. Globalization resumes its inevitable course.

The only thing that would trigger a selloff is an exponential growth of the pandemic, which with 122,000 cases and 1,200 deaths yesterday has already started. I have believed all along that the third peak in cases will be the final hyperbolic one, with deaths eventually topping the 1919 Spanish Flu peak of 650,000.

So far, the stock market has chosen to ignore these grim numbers, preferring instead to focus on vaccine hopes. There is effectively no government in Washington until January 21, 2021 so there is no one to step in and stop it. When the market does notice, the next buying opportunity of the decade may be at hand.

Stocks started expecting a Biden Win on Monday when they exploded right out of the gate. The Volatility Index (VIX) will plunge from $40 to $24 in a heartbeat. This was the biggest post-election rally in 100 years, with a 65% voter turnout not seen since women first got to vote in 1918. Buy dips in the (SPY).

The flip side is that massive spending will create monster deficits. Abuse from Trump has prompted the world’s largest buyer of US Treasury Bonds (TLT), China, to cut back their holdings from $1.24 trillion to $1 trillion. If China won’t buy our debt, who will? Sell short the (TLT) on rallies.

The Senate is another story. If the Republicans win, it will block most Biden programs and gridlock government for two years. Gridlocked government is normally good for stocks, except when you have a global pandemic and a Great Depression. No bold action is possible.

Expect slower economic growth as a result, fewer trading opportunities, and less asset appreciation. The Senate’s main job now is to make sure Biden fails. However, if Biden takes Georgia, we won’t know for sure until two Senate runoff elections take place there in January.

Jay Powell isn’t going anywhere, so interest rates are staying at near zero for three more years, according to yesterday’s press conference. Quantitative easing is still the name of the game.

Gold has turned, with the standard 100-day correction over. New highs beckon. The drivers are US interest rates remaining near zero for years, stockpiling by foreign central banks, and a recovering US economy. Notice also that the correlation between US stocks and gold this year has been 1:11. Gold is just another quantitative easing asset class these days. I’m starting to look at silver too, which usually has much more upside volatility.

China’s PMI is up for eight months, to 51.6%, better than expected. The world’s first post-pandemic economic keeps powering on. Anything over 50 is showing expansion.

The US ISM Nonmanufacturing Index hit a two-year high in October, down from 57.5 estimated to 57.5. That’s a two-year high.

The Nonfarm Payroll Report surprises at 638,000 for October, taking the headline Unemployment Rate down to a still recessionary 6.9%. Some 268,000 government jobs were lost, including 147,000 census workers. The rest came from teachers laid off by cash-starved local governments. Leisure & Hospitality jumped by 271,000. There are still 10 million fewer employed than when the pandemic started. The news crushed the bond market, where I’m short. Keep selling rallies in the (TLT).

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch exploded to another new all-time high last week.

The Friday prior to election week, I picked up new longs in the (SPY), (TSLA), and (CAT). Then on Monday, I bet the ranch, going 100% “RISK ON,” throwing the dice on a post-election melt-up and adding the (TLT), (JPM), (GOLD), (UNP), (UPS), and (AMGN).

It worked in spades.

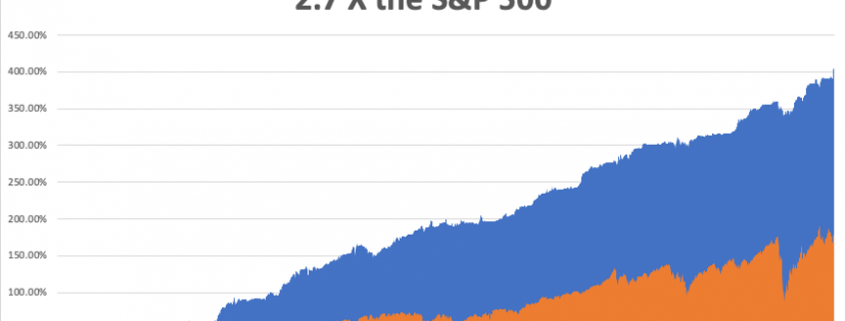

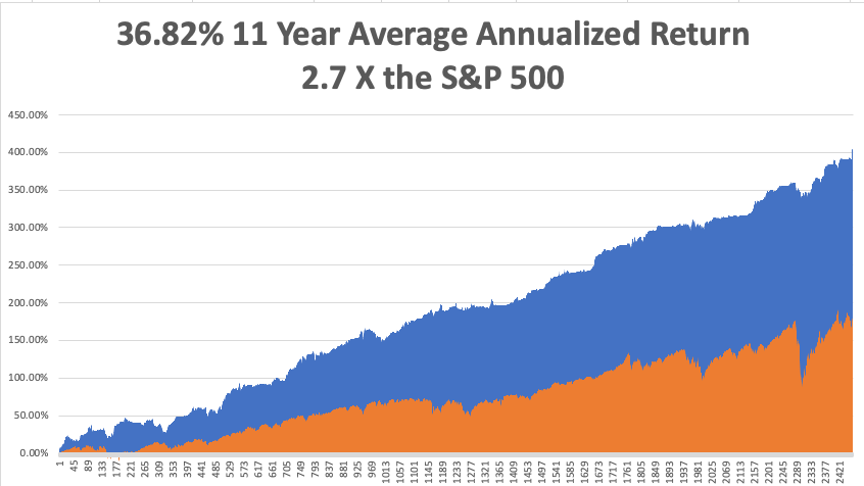

That keeps our 2020 year-to-date performance at a blistering +44.16%, versus a LOSS of -.06% for the Dow Average. That takes my 11-year average annualized performance back to +36.82%. My 11-year total return stood at new all-time high at +401.96%. My trailing one-year return appreciated to +52.23%.

The coming week will be a sleeper compared to the previous one. We also need to keep an eye on the number of US Coronavirus cases and deaths, now over 10 million and approaching 240,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, November 9 at 12:00 PM EST, US Consumer Inflation Expectations for October are out.

On Tuesday, November 10 at 7:00 AM EST, we get the NFIB Business Optimism Index for October.

Wednesday, November 11 is Veterans Day and I’ll be leading the local parade. The stock market is still open.

On Thursday, November 12 at 8:30 AM EST, the Weekly Jobless Claims are announced. At 9:30 AM EST, the US Inflation Rate for October is released.

On Friday, November 13, at 9:30 AM EST, the US PPI for October is printed. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, driving back from Lake Tahoe, I couldn’t help but sadly notice what a terrible wreck the country is in.

Stores everywhere are shuttered and schools are closed down. Many of my favorite businesses and restaurants are gone for good. Parts are unobtainable because someone in the supply chain either went out of business or died. You can’t go anywhere without being swathed in masks and hand sanitizer.

The new president has a big job ahead of him.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 5, 2020

Fiat Lux

FEATURED TRADE:

(A NOTE ON OPTIONS CALLED AWAY),

(SPY), (UNP), (TSLA), (CAT), (JPM), (GOLD), (UPS), (AMGN), (TLT)

Global Market Comments

November 2, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE ELECTION IS HERE!)

(INDU), (SPY), (TLT), (CAT), (TSLA), (GOLD), (JPM), (VIX), (VXX)

That was a great lead into Halloween last week, where frightening share price movements scared the living daylights out of all of us. The Dow Average dove by 7.0% last week and is down 8.9% from the September 1 peak. It was the worst performance in seven months.

Of course, I saw it all coming a mile off, predicting a selloff going into the November 3 presidential election and a rally once the great uncertainty is removed. That’s why I have run several short positions over the past month, all of which proved successful, and am long flipping to the long side.

The next generational peak at 120,000 is now only 93,499 points away. Time to get moving.

Of course, technical analysts who were eternally bullish at the market top are now wringing their hands over the double top on the charts that even a two-year-old can spot. It’s only giving us a better entry point for longs that will carry us through to yearend.

The stock market has priced in a contested election. If that doesn’t happen, and the winning candidate takes the White House by a landslide, markets will have to immediately back out that dire scenario. Stocks could soar by 1,000 points immediately on the first whiff of a challenge0-proof victory margin.

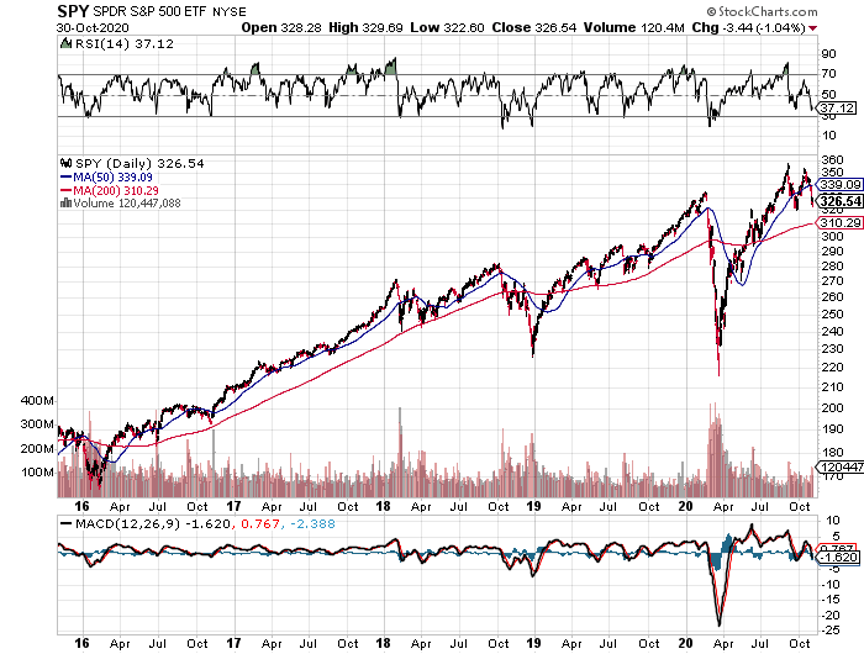

This time, we have the luxury of trading against a line in the sand at a (SPY) of $310, the 200-day moving average. Look at the chart below and you’ll see that this was not only close to the highs in 2018 and 2019 and a recent bottom in 2020. As if driven by the force of gravity, the market seems strangely driven to the $310 level.

It’s almost impossible to lose money on call spreads bought at market bottoms when the Volatility Index (VIX) is over 40%, as it was on Thursday and Friday. It’s time to strike while the iron is hot, and other investors are jumping off of bridges.

I’ll be piling into domestic recovery stocks like banks, construction, couriers, railroads, and gold and selling short bonds and the US dollar.

The election has already taken place, as 85 million votes have been cast in early voting. Many states have already seen double their 2016 turnouts. We just don’t know the outcome yet. It’s likely that new Covid-19 infections could top 100,000 on election day.

I’ll be up all night on Tuesday watching the results come in and keeping a hawk-eye on the overnight futures trading in Asia, the only open markets. Watch for Florida and North Carolina to report first.

One of the great ironies of trading last week was that after delivering the best earnings performance in stock market history, we saw one of the worst share price performances.

That’s because all of the great stimulants for the economy in recent months, the prospect of a massive stimulus package, declining Covid-19 cases, and plunging interest rates, will take a three-month vacation while the United States changes governments.

We really do work in a “what have you done for me lately” industry.

It was all about tech earnings last week, with Amazon (AMZN), Alphabet (GOOGL), and Microsoft all reporting. We have to wait until next week for Apple (AAPL). They all knocked the cover off the ball. Only Apple (AAPL) disappointed on a 20% YOY sales drop.

It seems everyone was waiting for the iPhone 12. Stock was off $10. Sales in China also took a big hit. Expect a massive resurgence in Q4. iPhones are selling faster than Apple can make them. Buy (AAPL) on dips. The stock jumps 8%. Forget about the DOJ antitrust suit. Buy (GOOGL) on dips.

Crashing bond prices show that a recovery is imminent, with ten-year US Treasury yields ($TNX) jumping 20 basis points in a month to a four-month high. Buy (SPY) on dips and sell short (TLT) on rallies.

Existing Home Sales soared by 9.4% in September, up a staggering 20% YOY. Inventories fell to a record low 2.7 months. Median prices are up an astounding 14.8% YOY to $311,800. Zillow believes this madness will continue for at least another year. Sales were strongest in the Northeast, with most of the action in single-family homes. Homes over $1 million have doubled, and vacation homes are up 35%.

Q3 GDP exploded with a 33.1% rate, double the highest on record and in line with expectations. All cylinders are firing, except for the 20% of the economy that went bankrupt during the pandemic. The stock market fully discounted this on September 1 when stocks peaked. The US won’t recover its 2019 GDP until 2023. With Corona cases now soaring, are we about to go back into the penalty box?

Weekly Jobless Claims posted at 751,000, an improvement, but still near a record high. It’s the lowest report since pre-pandemic March 14. I think a lot of these losses are structural….and permanent.

The World’s Biggest ETF is bleeding funds, with the (SPY) losing $33 billion this year. Massive selling at market tops has been a major factor. Most of the selling was in February and March when the pandemic started, and the money never came back. It also belies the widespread shift into tech stocks this year. Out with the boring, in with the exciting. Dry powder for the coming Roaring Twenties?

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch hit another new all-time high last week. October closed out at a moderate 1.51% profit.

I took a big hit on a long in Visa (V), thanks to a surprise prosecution from the Department of Justice over their Plaid merger. I more than offset that with short positions in the (SPY) and (JPM). Then on Friday, I leaned into the close, picking up new longs in the (SPY), (TSLA), and (CAT) betting on a post-election rally.

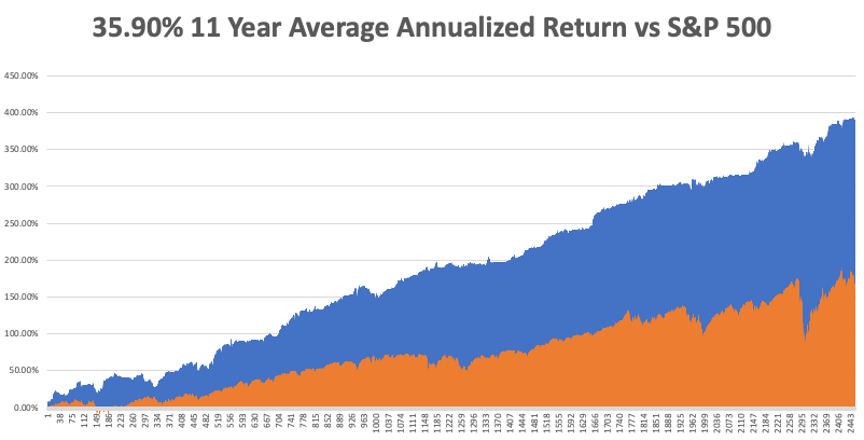

That keeps our 2020 year-to-date performance at a blistering +36.03%, versus a LOSS of -7.5% for the Dow Average. That takes my 11-year average annualized performance back to +35.90%. My 11-year total return stood at a new all-time high at +391.94%. My trailing one-year return appreciated to +42.48%.

The coming week will be one of the most exciting in history as election results trickly out Tuesday night. As if we didn’t have enough to worry about, it is also jobs week. We also need to keep an eye on the number of US Coronavirus cases and deaths, now over 9 million and 232,000, which you can find here.

On Monday, November 2 at 8:00 PM EST, US Vehicle Sales for October are released. Alibaba (BABA) and Sanofi (SNY) report earnings.

On Tuesday, November 3, we get the US Presidential Election. Early results in Florida will start coming out at 7:30 PM EST. TV networks, makers of campaign tchotchke and bumper stickers, and talking heads will go into mourning. Coca-Cola (K) reports earnings.

On Wednesday, November 4 at 9:15 AM EST, the ADP Private Employment Report is out. QUALCOMM (QCOM) and Wynn Resorts (WYNN) report earnings.

On Thursday, November 5 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, November 6 at 8:30 AM EST, the October Nonfarm Payroll Report is announced. Barrick Gold (GOLD) reports earnings. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I went to San Francisco for dinner with an old friend last night and I couldn’t believe what I saw. Storefronts were boarded up, the streets vacant, with only the homeless ever present. The cable cars have quit running.

We ate outside at my favorite Italian restaurant Perbacco on Market Street where the heat lamp blasted away. The restaurant is owned by my transplanted Venetian friend Umberto Gibin. He was running it at 50% capacity with 25% of the staff just to break even.

I hope he makes it.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 30, 2020

Fiat Lux

Featured Trade:

(OCTOBER 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(INDU), (VIX), (AMZN), (TSLA), (FEYE), (HACK), (PANW), (V), (TLT), (FXA), (FXC), (ZM), (DOCU), (RTX), (LMT), (NOC), (GD)

Below please find subscribers’ Q&A for the October 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you think if Trump contests the election, it will be bad for stocks?

A: Yes, count on that knocking another 10% off of stocks. The market has spent the last six months pricing in a Biden win. Take that away and you have to price that back out again, about 6,000 Dow Average points (INDU). We’ve already dropped 2,500 points so that leaves another 3,500 points of downside t0 go in the event of a Trump win.

Q: Will that result in a crash?

A: Yes. At least 1,000 points in the overnight session following.

Q: Do you think it’s going to happen?

A: No. According to the polls, Trump will lose by at least 15 million votes. While the polls missed the Electoral College result last time, they were dead on with the popular vote, with Hillary Clinton winning by 3 million votes. If the margin were only a few hundred or thousand votes in a single battleground state, Trump might win a court fight. But he can’t win if the margin is in ten states and tens of millions of votes. That is too much to fudge. That is how markets react: they hate surprises, and a second Trump win would be the surprise of the century.

Q: With all of the earnings positive, do you think markets will stay positive?

A: Earnings aren’t important right now. Everyone knew earnings would be great because we were coming off of hundred-year lows caused by the pandemic. So yes, we knew they’d be up 50%, 100%, 150%; that's not the surprise. The bigger issue is what the pandemic is going to do, and of course, only biochemists know that—most stock traders have no idea, which is reflected in these gigantic swings we’re seeing in the market both on the upside and the downside. As a biochemist, I can tell you that this is our final wave that's coming up and it could last several months. After that, we get a vaccine or herd immunity. When it's done, you have the bull market of a lifetime—up 400% in ten years from these levels. Dow 120,000 here we come!

Q: Do you see a tax selloff if Biden gets in? Should we get short?

A: Definitely; there will be a tax selloff. Past ones have only lasted a week or two and those were the last two weeks of December, so it really won’t be that bad. It’s not like it’s a surprise that Biden is ahead in the polls, because he has been for 6 months. Nor is it a surprise that he is going to raise taxes on the wealthy. I wouldn’t get short though. The short play was last week and the week before; and I did manage to get out three shorts but didn't want to get too big in front of an election. So those all worked. I'm out of all of them now, and now we’re looking only at long plays. And with the Volatility Index (VIX) over $40, you can go 20% or 30% in-the-money on these call spreads and still look to make 10%-20% profit on the position in a month.

Q: Isn’t the pandemic great for Amazon (AMZN)?

A: Yes, Amazon was taking over the world anyway, and forcing everyone to an online-only economy which couldn’t be better for them. A lot of this shifting is permanent and won’t be going back to the way it was before the pandemic with brick and mortar shops and malls. So yes, we love Amazon and I would buy on the dips. There’s a double from here.

Q: Do you have long term names I can buy to sit on?

A: Yes, we actually do have a long-term portfolio posted on the website. It would be listed under your subscription area once you log in—we rebalance that twice a year. And of course, we had a 10% holding in Tesla (TSLA) which went up ten times, so the performance of the long-term portfolio is through the roof. To find the long-term portfolio, please click here.

Q: Do you record this webinar?

A: Yes, we post it on the www.madhedgefundtrader.com site in two hours.

Q: Do you still like the Internet security stocks like FireEye (FEYE)?

A: Yes. Hacking is growing faster than the Internet itself. You should also look at Palo Alto Networks (PANW) and the ETF (HACK).

Q: Should we hold on to the Visa (V) spread hoping it will come back after the election drop?

A: Hope is not an investment strategy. I always stop out of positions when they hit a 2% loss. The only time I have 4% losses is when we get these gigantic gap moves overnight, which tend to happen once every one or two years. In this case, Visa got hit with a surprise antitrust suit from the Department of Justice that knocked $10 off of the stock. So no, I will not hold on to it in the hope that it does better; I will try to minimize my losses, get out, and get into the next winning position. Hope is what turns a 4% loss into a complete 10% write off.

Q: What’s your view on the Canadian dollar (FXC)?

A: I like it, but it’s not as good as the Australian dollar (FXA) because Canada has a major oil exposure, and actually the worst kind of oil exposure—tar sands in northern Alberta. The outlook for oil is poor and that will be a drag on the currency in the form of fewer exports. Buy the (FXA). No oil troubles here. Kangaroos are another story.

Q: Will you be looking to sell short on the United States Treasury Bond Fund (TLT)?

A: Yes, if we can just get a little bit higher. We’re looking at an economic recovery next year, so we’d expect the (TLT) to be lower by at least $20 points in 2021.

Q: Do you think the San Francisco and New York housing markets will return to what they were before with so many people are moving out of the city?

A: Yes, they will come back, I’ve been through many of these cycles in San Francisco over the past 50 years; it always comes back. Once the pandemic is over, people will say, “Oh my gosh, I can’t believe you can get a two-bedroom apartment in San Francisco for only $2 million.” That's probably another year or two off after a vaccine is in widespread distribution.

Q: Is real estate in a bubble?

A: Absolutely, but real estate bubbles can go on for a long time, like ten years. The bubble in Australia has been going on for 30 years. Ultimately, real estate prices are driven by the earnings power of the local economy which, in the case of San Francisco, is huge. This time around, we have a record large millennial generation looking for real estate. There are 85 million millennia buyers with only 65 million Gen X-er’s selling homes. So, we have to make up a shortfall of 20 million houses at some point. That’s why building permits are through the roof every month.

Q: Zoom (ZM) and DocuSign (DOCU) are the darling stocks of COVID 2020—what do you think about them at these high prices?

A: Very high risk. If you bought these a year ago when we first started covering them, good for you as they're up ten times. However, there are better fish to fry than chasing these big pandemic winners at all-time highs.

Q: If Biden wins, what happens to defense stocks like Raytheon Technology (RTX)?

A: They go down. It turns out a lot of the defense business is in very long term contracts that can’t be broken. They have to supply so many planes a year to the government for a decade or more. However, the sentiment on these sectors sours under democratic administrations because they are not initiating new weapons systems where the big money is made. Lockheed Martin (LMT), Northrop Grumman (NOC), and General Dynamics (GD) all have the same problem. I grew up with these companies. They were the FANGs of their day.

Q: How does a Biden win affect Tesla (TSLA)?

A: Then $2,500 a share for Tesla looks cheap (it’s now at $410). Biden will do everything he can to slow climate change and accelerate alternative energy. Tesla is front and center on that. Under current law, car manufacturers are limited on the number of units they can sell to get the $7,500 tax break per vehicle. Tesla used up all their subsidies five years ago. My bet is that the limits will be eliminated and that leads to a huge surge in Tesla sales in the U.S., which is why the stock has gone up 10 times in the last year. Tesla has promised to drop their car price to $25,000 in three years. If you throw in $10,000 in federal and state tax subsidies you get the car for free. Then you can write off General Motors (GM) and Ford (F).

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 26, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MIXED MESSAGES)

(SPY), (TLT), (UUP), (FCX)