Her name is Goldilocks. The neighbors have been sneaking peeks at her through the curtains at night and raising their eyebrows because she is slightly older than my kids, or about 50 years younger than me.

I have no complaints. Suddenly, the world looks a brighter place, I’m getting up earlier in the morning, and there is a definite spring in my step. My doctor asks me what I’ve been taking lately.

It helps a lot too that the value of my stock portfolio is going up every day.

I don’t know how long Goldilocks will stay. The longer the better as far as I am concerned. After all, I’m a widower twice over, so anyone and anything is fair game. But two or three months is reasonable and possibly until the end of 2021.

That’s the way it is with these May-December relationships, or so my billionaire friends tell me, who all sport trophy wives 30 years younger.

At my age, there are no long-term consequences to anything because there is no long-term. I don’t even buy green bananas.

I have been expecting exactly this month’s melt-up for months and have been positioning both you and me to take maximum advantage. I am making all my pension fund and 401k contributions early this year to get the money into the stock market as fast as possible.

So far so good.

More money piled into stocks over the past five months than over the previous 12 years. And this pace is set to continue. Those who sold a year ago are buying back. $2 trillion in savings enforced by the pandemic are also going into stocks. And after all, there is nothing else to buy.

If all this sounds great, it’s about to get a lot better. Europe and Asia are still missing in action, thanks to a slower vaccine rollout. When they rejoin the global economy in the fall, it will further throw gasoline on the fire. Exports will boom.

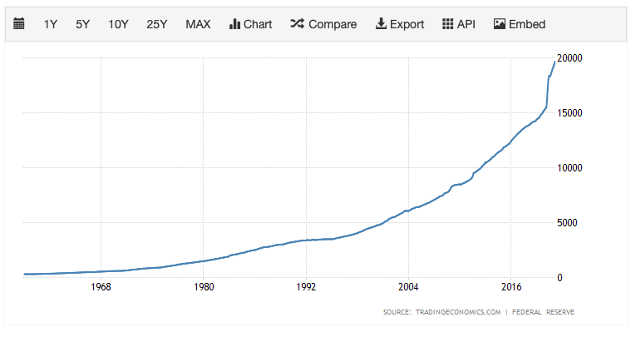

The money supply is growing at an astonishing 26% annual rate, thanks to QE forever and massive government spending. That’s the fastest rate on record. In ten years, a PhD will write a paper on how much of this ended up in the stock market. Today, I can tell you it is quite a lot.

In the meantime, make hay while the sun shines. What am I supposed to talk to about with Goldilocks at night anyway?

Do you suppose she trades stocks?

50 Years of Money Supply Growth is Going Vertical

A face-ripping rally is on for April, or so says Strategas founder Lee. A Volatility Index with a $17 handle is sending a very strong signal that you should be loading up on energy, industrials, consumer discretionary, and travel-related stocks. Avoid “stay at home” stocks like Covid-19, which are extremely overcrowded. I’m using dips to go 100% long.

It’s all about infrastructure, 24/7 for the next three months, or until the $2.3 trillion spending package is passed. It might have to take a haircut first. Biden has set a July 4 target to close thousands of deals and horse-trading. With the S&P 500 breaking out above $4,000 and the financial markets drowning in cash, the plan could be worth another 10% of market upside. Would your district like a new bridge? Maybe a freeway upgrade? The possibilities boggle the mind.

US Manufacturing hits a 37-year high in March, driven by massive new orders front-running the global economic recovery. The Institute for Supply Management publishes a closely followed index that leaped from 60.8 to 64.7. Buy before the $10 trillion hits the market.

US Services Industry hits record high, with the Institute of Supply Management Index soaring from 55.3 to 63.7 in March. The ending of Covid-19 restrictions was the major factor. Roaring Twenties here we come!

US Job Openings are red-hot, coming in at 7.4 million compared to an expected 7 million, according to the JOLTS report. It’s the best report in 15 months. It's a confirmation of the ballistic March Nonfarm Payroll report out on Friday.

US Auto Sales surge in Q1, shaking off the 2020 Great Recession. It’s a solid data point for the recovery, despite a global chip shortage. General Motors (GM) was up 4%, thanks to recovering Escalade sales, and strong demand is expected for the rest of 2021. Toyota (TM) was up 22% and Fiat Chrysler 5%. “Pent-up demand” is a term you’re going to hear a lot this year. The Economic boom will run through 2023, says JP Morgan chairman Jamie Diamond, one of the best managers in the country. In his letter to shareholders, he says 10% of his workforce will work permanently from home. Zoom (ZM) is here to stay. Fintech is a serious threat to legacy banks, which is why we love Square (SQ) and PayPal (PYPL). Keep buying (JPM) on dips. Interest rates will rise for years, but not fast enough to kill the bull market.

IMF predicts 6.0% Global Growth for 2021, the highest in 40 years. China will grow at 8.4%. It’s a big improvement since their January prediction. The $1.9 trillion US Rescue is stimulating not just America’s economy, but that of the entire world. Expect a downgrade to the 3% handle in 2022, which is still the best in a decade.

Fed Minutes say Ultra Dove Policy to Continue, so say the minutes from the March meeting. Rates won’t be raised on forecasts, predictions, or crystal balls, but hard historic data. That’s another way of saying no rate hikes until you see the whites of inflation’s eyes. $120 billion of monthly bond buys will continue indefinitely. Bonds dropped $1.25 on the news. Sell all (TLT) rallies in serious size. It’s still THE trade of 2021.

Disneyland in LA to open April 30 after a one-year hiatus. It’s time to dust off those mouse ears. The last time the Mouse House was closed this long, antiwar protesters took to Tom Sawyer’s Island and raised the Vietcong flag (I was there). Some 10,000 cast members have been recalled. Only 15% capacity will be allowed to California residents only. The new Avengers Campus will open on June 4. The company is about to make back the 25% of revenues it lost last year, but with a much lower cost base. Buy (DIS) on dips.

Was that inflation? The Producer Price Index jumped by 1.0% in March compared to an expected 0.40%. It’s the second hot month in a row. Basically, the price of everything went up. The YOY rate is an astonishing 4.04% a near-decade high. If it looks like a duck and quacks like a duck….Stocks didn’t like it….for about 15 minutes.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 5.80% gain during the first nine days of April on the heels of a spectacular 20.60% profit in March.

It was a very busy week for trade alerts, with five new positions. Sensing an uncontrolled market melt-up for the entire month piled on aggressive long in Visa (V), JP Morgan (JPM), and Microsoft (MSFT). I also poured on a large short position in bonds (TLT) with a distant May expiration.

My now large Tesla (TSLA) long expires in 4 trading days. Half of my even larger short in the bond market (TLT) also expires then.

That leaves me 100% invested for the sixth time since last summer. Make hay while the sun shines.

My 2021 year-to-date performance soared to 49.89%. The Dow Average is up 11.60% so far in 2021.

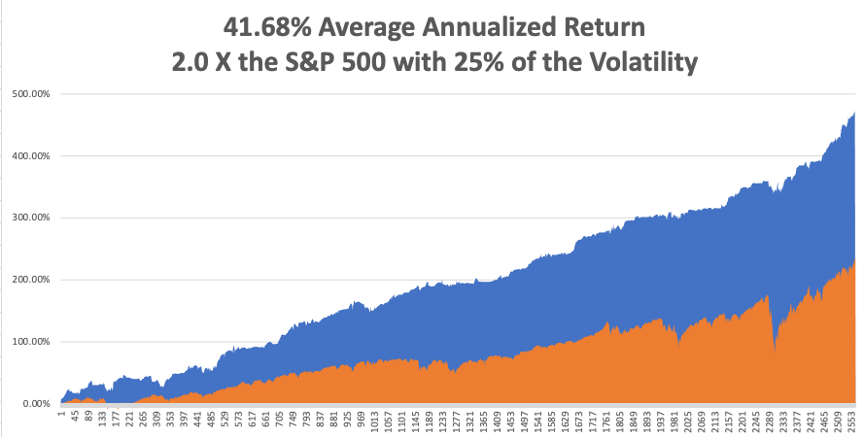

That brings my 11-year total return to 472.44%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.68%, the highest in the industry.

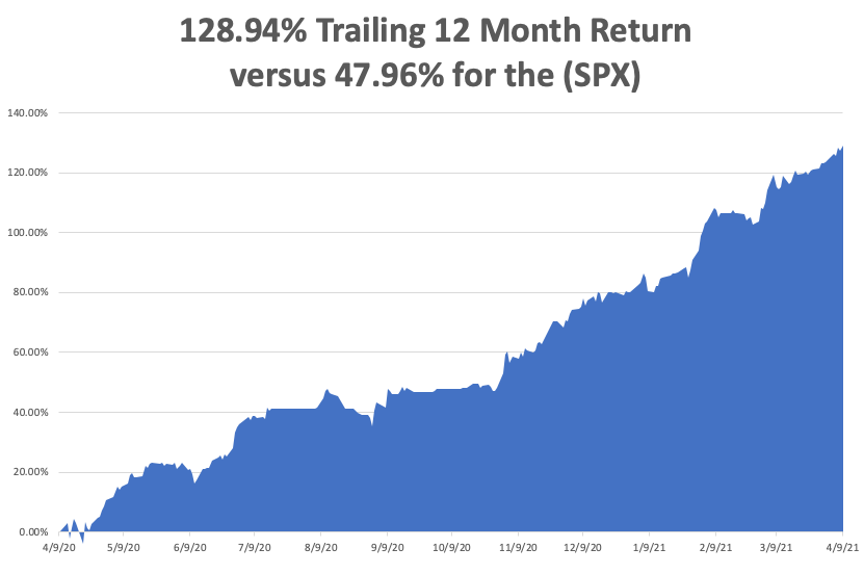

My trailing one-year return exploded to positively eye-popping 128.94%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives. Every time I think these numbers can’t be topped, that increases by another 10% during the following two weeks.

We need to keep an eye on the number of US Coronavirus cases at 30.6million and deaths topping 563,000, which you can find here.

The coming week will be dull on the data front.

On Monday, April 12, at 11:00 AM, the US Consumer Inflation Expectations for March is released.

On Tuesday, April 13, at 8:30 AM, US Core Inflation for March is published.

On Wednesday, April 14 at 2:00 PM, the Federal Reserve Beige Book is out. On Thursday, April 15 at 8:30 AM, the Weekly Jobless Claims are printed. We also learn US Retail Sales for March.

On Friday, April 16 at 8:30 AM, we get the Housing Starts for March. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, the whole Archegos blow-up reminds me that there are always a lot of con men out there willing to take your money. As PT Barnum once said, “There is a sucker born every minute.”

I’ll tell you about the closest call I have ever had with one of these guys.

In the early 2000s, I was heavily involved in developing a new, untried, untested, and even dubious natural gas extraction method called “fracking.” Only a tiny handful of wildcatters were even trying it.

Fracking involved sending dynamite down old, depleted wells, fracturing the rock 3,000 feet down, and then capturing the newly freed up natural gas. If successful, it meant that every depleted well in the country could be reopened to produce the same, or more gas than it ever had before. America’s gas reserves would have doubled overnight.

A Swiss banker friend introduced me to “Arnold” of Amarillo, Texas who claimed fracking success and was looking for new investors to expand his operations. I flew out to the Lone Star state to inspect his wells, which were flaring copious amount of natural gas.

Told him I would invest when the prospectus was available. But just to be sure, I hired a private detective, a retired FBI man, to check him out. After all, Texas is notorious for fleecing wannabe energy investors, especially those from California.

After six weeks, I heard nothing, so late on a Friday afternoon, I ordered $3 million sent to Arnold’s Amarillo bank from my offshore fund in Bermuda. Then I went out for a hike. Later that day, I checked my voice mail and there was an urgent message from my FBI friend:

“Don’t send the money!”

It turns out that Arnold had been convicted of check fraud back in the sixties and had been involved in a long series of scams ever since. But I had already sent the money!

I knew my fund administrator belonged to a certain golf club in Bermuda. So, I got up at 3:00 AM, called the club Starting Desk and managed to get him on the line. He said I had missed the 3:00 PM Fed wire deadline on Friday and the money would go out first thing Monday morning. I told him to be at the bank at 9:00 AM when the doors opened and stop the wire at all costs.

He succeeded, and that cost me a bottle of Dom Perignon Champaign, which fortunately in Bermuda is tax-free.

It turned out that Arnold’s operating well was actually a second-hand drilling rig he rented with a propane tank buried underneath that was flaring the gas. He refilled the tank every night to keep sucking in victims. My Swiss banker friend went bust because he put all his clients into the same project.

I ended up making a fortune in fracking anyway with much more reliable partners. No one had heard of it, so I bought old wells for pennies on the dollar and returned them to full production. Then gas prices soared from $2/MM BTU to $17. America’s gas reserves didn’t double, they went up ten times.

I sold my fracking business in 2007 for a huge profit to start the Diary of a Mad Hedge Fund Trader.

It is all a reminder that if it is too good to be true, it usually is.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-8.png422564Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-12 09:02:542021-04-12 14:11:44The Market Outlook for the Week Ahead, or The Melt Up is On!

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WILL HE OR WON’T HE?)

(INDU), (USO), (TM), (SCHW), (AMTD), (ETFC), (SPY), (IWM), (USO), (WMT), (AAPL), (GOOGL), (SPY), (C)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-07 03:04:222019-10-07 03:46:35October 7, 2019

Once again, the markets are playing out like a cheap Saturday afternoon matinee. We are sitting on the edge of our seats wondering if our hero will triumph or perish.

The same can be said about financial markets this week. Will a trade deal finally get inked and prompt the Dow Average to soar 2,000 points? Or will they fail once again, delivering a 2,000-point swan dive?

I vote for the latter, then the former.

Still, I saw this rally coming a mile off as the Trump put option kicked in big time. That's why I piled on an aggressive 60% long position right at last week’s low. Carpe Diem. Seize the Day. Only the bold are rewarded.

Or as Britain’s SAS would say, “Who dares, wins.”

It takes a lot of cajones to trade a market that hasn’t moved in two years, let alone take in a 55% profit during that time. But you didn’t hire me to sit on my hands, play scared, and catch up on my Shakespeare.

I think markets will eventually hit new all-time highs sometime this year. The game is to see how low you can get in before that happens without getting your head handed to you first.

Last week saw seriously dueling narratives. The economic data couldn’t be worse, pointing firmly towards a recession. But the administration went into full blown “jawbone” mode, talking up the rosy prospects of an imminent China trade deal at every turn.

This was all against a Ukraine scandal that reeled wildly out of control by the day. Is there a country that Trump DIDN’T ask for assistance in his reelection campaign? Now we know why the president was at the United Nations last week.

The September Nonfarm Payroll Report came in at a weakish 136,000, with the Headline Unemployment rate at 3.5%, a new 50-year low.

Average hourly earnings fell. Apparently, it is easy to get a job but impossible to get a pay raise. July and August were revised up by 45,000 jobs.

Healthcare was up by 39,000 and Professional and Business Services 34,000. Manufacturing fell by 2,000 and retail by 11,0000. The U-6 “discouraged worker” long term unemployment rate is at 6.9%.

The US Manufacturing Purchasing Managers Index collapsed in August from 49.7 to 47.9, triggering a 400-point dive in the Dow average. This is the worst report since 2009. Manufacturing, some 11% of the US economy, is clearly in recession, thanks to the trade war-induced loss of foreign markets. A strong dollar that overprices our goods doesn’t help either.

The Services PMI Hit a three-year low, from 53.1 to 50.4, with almost all economic data points now shouting “recession.” The only question is whether it will be shallow or deep. I vote for the former. Consumer Spending was flat in August. That’s a big problem since the average Joe is now the sole factor driving the economy. Everything else is pulling back. Consumer spending, which accounts for more than two-thirds of U.S. economic activity, edged up 0.1% last month as an increase in outlays on recreational goods and motor vehicles was offset by a decrease in spending at restaurants and hotels.

The Transports, a classic leading sector for the market, have been delivering horrific price action this year giving up all of its gains relative to the S&P 500 since the 2009 crash.

Oil (USO) got crushed on recession fears, down a stunning 19.68% in three weeks. The global supply glut continues. Over production and fading demand is not a great formula for prices.

Toyota Auto Sales (TM) cratered by 16.5% in September, to 169,356 vehicles in another pre-recession indicator. It’s the worst month since January during a normally strong time of the year. The deals out there now are incredible.

Online Brokerage stocks were demolished on the Charles Schwab (SCHW) move to cut brokerage fees to zero. TD Ameritrade (AMTD) followed the next day and was spanked for 23%, and E*TRADE (ETFC) punched for 17. These are cataclysmic one0-day stock moves and signal the end of traditional stock brokerage.

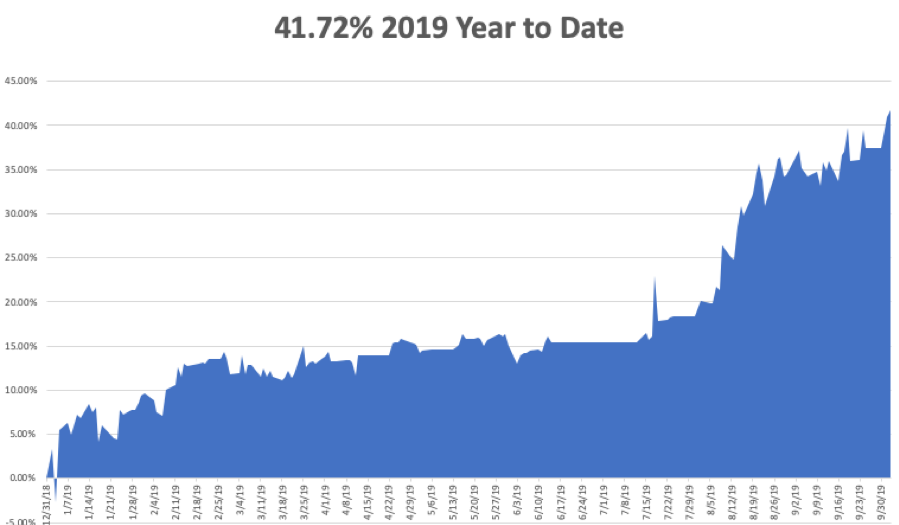

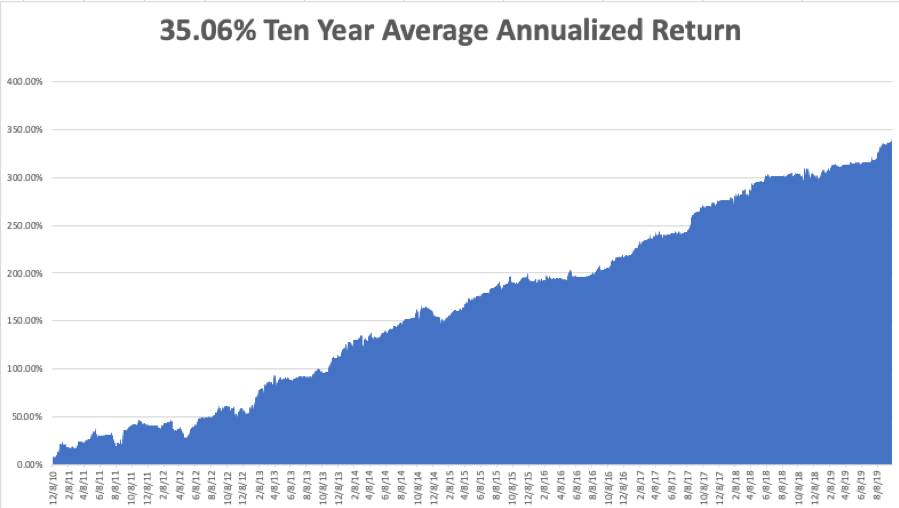

The Mad Hedge Trader Alert Service has blasted through to yet another new all-time high. My Global Trading Dispatch reached new apex of 341.86% and my year-to-date accelerated to +41.72%. The tricky and volatile month of October started out with a roar +5.40%. My ten-year average annualized profit bobbed up to +35.06%.

Some 26 out of the last 27 trade alerts have made money, a success rate of96.29%! Under promise and over deliver, that's the business I have been in all my life. It works.

I used the recession-induced selloff since October 1 to pile on a large aggressive short dated portfolio. I am 60% long with the (SPY), (IWM), (USO), (WMT), (AAPL), and (GOOGL). I am 20% short with positions in the (SPY) and (C), giving me a net risk position of 40% long.

The coming week is all about the September jobs reports. It seems like we just went through those.

On Monday, October 7 at 9:00 AM, the US Consumer Credit figures for August are out.

On Tuesday, October 8 at 6:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, October 9, at 2:00 PM, we learn the Fed FOMC Minutes from the September meeting.

On Thursday, October 10 at 8:30 AM, the US Inflation Rate is published. US-China trade talks may, or may not resume.

On Friday, October 11 at 8:30 AM, the University of Michigan Consumer Sentiment for October is announced.

The Baker Hughes Rig Count is released at 2:00 PM.

As for me, I’m still recovering from running a swimming merit badge class for 60 kids last weekend. Some who showed up couldn’t swim, while others arrived with no swim suits, prompting a quick foray into the lost and found.

One kid jumped in and went straight to the bottom, prompting an urgent rescue. Another was floundering after 15 yards. When I pulled him out and sent him to the dressing room, he started crying, saying his dad would be mad. I replied, “Your dad will be madder if you drown.”

I never felt so needed in my life.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/10/young-john-thomas.png497499Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-07 03:02:222019-10-07 03:46:23The Market Outlook for the Week Ahead, or Will He, or Won’t He?

Featured Trade:

(I HAVE AN OPENING FOR THE MAD HEDGE FUND TRADER CONCIERGE SERVICE), (DON’T MISS THE AUGUST 7 GLOBAL STRATEGY WEBINAR), (HAVE WE SEEN “PEAK AUTO SALES”),

(GM), (TM), (F), (HMC), (TSLA), (NSANY),

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-06 01:08:412019-08-05 17:35:33August 6, 2019

There is no limit to my desire to get an early and accurate read on the US economy, which at the end of the day is what dictates the future returns on our investments.

I flew over one of my favorite leading economic indicators only last week.

Honda (HMC) and Nissan (NSANY) import millions of cars each year through their Benicia, California facilities where they are loaded on to hundreds of rail cars for shipment to points inland as far as Chicago.

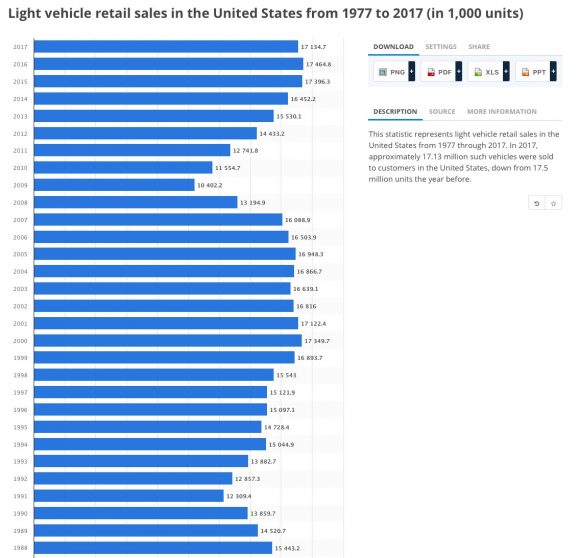

In 2009, when the US car market shrank to an annualized 8.5 million units, I flew over the site and it was choked with thousands of cars parked bumper to bumper in their white plastic wrappings, rusting in the blazing sun and bereft of buyers.

Then, “cash for clunkers” hit (remember that?). The lots were emptied in a matter of weeks, with mile-long trains lumbering inland, only stopping to add extra engines to get over the High Sierras at Donner Pass. The stock market took off like a rocket, with the auto companies leading.

I flew over the site last weekend, and guess what? The lots are full again. Not only that, the trains lined up to take them away are gone. US Auto Sales peaked in October 2017 when they fell just short of a 19 million annualized rate. As of the end of June this year, they had fallen to a 15.1 million annualized rate. July is looking worse still.

And this is what I’m worried about. Auto Sales may not only be peaking for this economic cycle. They may be peaking for all time.

This is my logic.

As they slowly age, Millennials are about to become the principal buyers of automobiles. The problem is that Millennials are purchasing cars at a far slower rate than previous generations.

This is because they have a much higher concentration in urban areas where the cost of car ownership is the most expensive in history. $40 for parking for an evening? Give me a break. But good luck finding free on-street parking, and if you do, your windows will probably get smashed.

In cities like San Francisco, public transportation, bicycles, and electric scooters are the preferred mode of transportation.

It doesn’t help that this generation is shouldering the burden of the bulk of $1.5 trillion in student loan debt. When you owe $2,000 a month in interest, there is little room for a car payment, and you probably don’t have the credit rating to buy a car anyway.

When they do buy cars, all-electric is their first choice, if they can get access to overnight charging. A lot of companies are making this easy by offering free charging for electric commuters in corporate parking lots. This explains why Tesla (TSLA) has taken deposits from 400,000 for their low-end Tesla 3, which has a two-year waiting list for new buyers.

When Millennials do drive, such as on business, for weekend trips or summer vacations, they either rent or “share.” Driving around the city, you see cars parked everywhere with bizarre names like Upshift, Getaround, Zipcar, Turo, and Casual Carpool.

Indeed, Detroit takes the car-sharing threat so seriously that the Big Three have all bought into the technology, with General Motors taking a stake in Maven. (GM) plans to start its own peer-to-peer car-sharing service this summer.

This is all a mystery for my generation, which grew up tearing apart old cars and putting them back together. I spent a year trying to put the engine on my 1955 Volkswagen back together. When I gave up, I towed the car and a big box full of greasy parts to a local mechanic, a German Army veteran. When he finished, even he had four parts left over.

Do you know who believes my rash, possible MAD theory? Investors in auto stocks, one of the worst-performing sectors of the stock market this year. Shares like those of General Motors (GM) keep breaking new valuation lows.

What was (GM)’s price earnings multiple today? Try a miserable zero since the company loses money, one of the lowest of all S&P 500 stocks. Hapless portfolio managers keep getting sucked into the shares, which have become one of the ultimate value traps.

It is all further evidence that my cautious view on the US economy is correct, that multiple crises overseas are ahead of us, and that the stock market could drop 5%-10% at any time. The auto industry should lead the charge to the downside, especially General Motors (GM) and Ford (F).

As for Tesla (TSLA), better to buy the car than the stock.

Sorry, the photo is a little crooked, but it's tough holding a camera in one hand and a plane's stick with the other while flying through the turbulence of the San Francisco Bay’s Carquinez Straight.

Air traffic control at nearby Travis Air Force base usually has a heart attack when I conduct my research in this way, with a few joyriding C-130s having more than one near miss.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/tesla.png222745MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-08-06 01:02:192019-09-04 13:22:00Have We Seen “Peak Auto Sales”?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.