Mad Hedge Technology Letter

August 21, 2020

Fiat Lux

Featured Trade:

(THE THINKING BEHIND RAY DALIO)

(ZLAB), (TME)

Mad Hedge Technology Letter

August 21, 2020

Fiat Lux

Featured Trade:

(THE THINKING BEHIND RAY DALIO)

(ZLAB), (TME)

Every time I watch an interview with the Bridgewater hedge fund manager Ray Dalio, what he doesn’t say really paints the picture of who he really is.

Yes, it’s undeniable that he is incredibly wealthy, successful, and has returned shareholder profits continuously, but his support for the Chinese communist party has to be called out.

Dalio necessarily isn’t anti-American, but he loves to trot out propaganda that America is a “weakening” power confronting a “rising” power.

I would argue this isn’t true and that China is just a paper Tiger with infinite more problems than the U.S. and has been hit infinite times harder economically because of this pandemic.

China is hoping to solve the issue from going from the world’s growth engine to 250 million unemployed Chinese on the streets, thanks to the city of Wuhan.

His response is almost automatic at this point in regard to China as he skirts around specifics and issues general statements to avoid criticizing the land of Chairman Xi Jinping.

Why does Ray Dalio give a free pass to China?

The easiest way to understand is to look where he deploys his money.

It’s well known that criticizing the Chinese government is a red line for the communist party and they will sabotage, swindle, destroy anyone that steps over this line, and even more so for a foreigner.

Ray Dalio doesn’t want his capital nicked in China where he would have zero chance of navigating through the corrupt judicial system successfully in a land that has zero rule of law.

As long as Dalio has meaningful investments in Chinese tech companies, he will never say anything bad about China. He is part of the problem that has spread through the U.S. system of self-censored Americans who have a financial interest in China.

What does he own?

Tencent Music Entertainment (TME).

Offering one-stop music services and solutions designed to create a complete music entertainment ecosystem, Tencent Music Entertainment has solidified its status as the biggest online music company in China by monthly active users (MAUs).

Dalio has upped his holdings by a staggering 858% in TME, Bridgewater has pulled the trigger on 620,000 shares in Q2. At 692,262 shares, the total position is valued at $9,318,000.

TME added 4.4 million subscribers in the quarter versus 2.8 million in Q1, and subscriber average revenue per user also grew 8% year-over-year.

What about the direction of the company?

The company renewed the Universal Music Group (UMG) licensing deal.

Additionally, it organized nine TME Live performances in Q2 and long-form audio licensed titles increased 300% year-over-year, with penetration of 9.4% compared to 4.6% last year.

What other Chinese investments does Dalio own? You would think an American billionaire would help the U.S. health industry find solutions against a global health crisis, but no, Dalio is investing in Chinese health companies.

What does he own?

Zai Lab Ltd. (ZLAB)

Zai Lab offers transformative medicines for cancer, autoimmune, and infectious diseases to patients in China.

Dalio's Bridgewater made a splash with a new position buying 63,837 shares. The value of this holding? It lands at $5,243,000.

The firm has performed well driven by Zejula's second-line ovarian cancer (OC) launch in China. Total sales from China, Hong Kong, and Macau reached $13.8 million.

The Chinese government is already requesting applications for the National Drug Reimbursement List (NDRL) for this year. ZLAB is expected to apply for Zejula's second line OC indication, with the results potentially coming in November 2020 and driving upside.

As for its other launch, Optune became commercially available at the end of June. Optune is priced like a premium therapeutic and would be with a list price of $19,000 and a net price around $11,000. This is at a modest discount price of that of the U.S. list price of around $20,000. Most patients in China are self-paying for this innovative device.

Why invest in Chinese tech firms when the U.S. has a perfectly operating tech industry that has seized even more market share from the broader economy?

Growth.

Watching Dalio’s interview, it’s clear to me that he is a numbers guy. The genesis of his logic originates from the debt cycle and how investments and payments function derive from this concept.

It’s hard for Wall Streetists to ignore the growth numbers in China and Chinese tech firms have the best growth numbers in any industry in an otherwise faltering Chinese economy.

Chinese tech firms have the best growth numbers out of any tech industry in the world, that is, if you believe them.

Dalio has put his money where his mouth is and clearly believes in Chinese tech and makes sure his toes are set squarely behind the Chinese communist line.

I just would remind Ray Dalio that he is one investigative report away from losing his money because industry experts agree that no number out of China is even close to accurate.

I again strongly urge readers to never deploy capital in any mainland Chinese tech firm, simply because there are too many great tech firms in the U.S., and also from the risk control perspective.

Do not follow Dalio down this path where you need to drink the same Kool Aid as him.

We are entering into the golden age of U.S. tech and there will be vast amounts of opportunity moving forward.

We are just scratching the surface here as technology will become a bigger part of our lives, it’s up to you if you want to be a participant or not.

Mad Hedge Technology Letter

January 15, 2019

Fiat Lux

Featured Trade:

(THE BALKANIZATION OF THE INTERNET),

(AAPL), (FB), (CTRP), (PDD), (BABA), (JD), (TME)

The Mad Hedge Technology Letter has a front-line seat to the carnage wrought by the balkanization of technology that is swiftly descending across all corners of the tech universe.

In technology terms, this is frequently referred to as “splinternet.”

A quick explanation for the novices can be summed up by saying splinternet is the fragmenting of the Internet causing it to divide due to powerful forces such as technology, commerce, politics, nationalism, religion, and interests.

The rapid rise of global splinternet news stories will have an immediate ramification on your tech portfolio and it’s my job to untangle the knots.

What investors are seeing is the bifurcation of the global tech game into a binary world of Chinese and American tech.

Most recently, Central European country Poland, who was thought to be siding with the Chinese because of the growing presence by large-cap Chinese tech in Warsaw, announced government security had arrested a Huawei employee, Chinese national Wang Weijing, for allegedly spying on behalf of the Chinese state.

For all the naysayers that believe the administration’s hope of curtailing the theft of western technology was a bogus endeavor, this recent event buttresses the notion that Chinese state-funded tech companies are truly running nefariously throughout the world.

In fact, Poland has little to gain from this maneuver if you take the current status quo as your guidebook, and I would argue it is a net negative for Poland because Chinese tech is deeply embedded inside of the Poland tech structure bestowing profits and internet capabilities on multiple parties.

Making the case stronger against China, Poland has no flagship tech communications company that would serve as competition to the Chinese or could directly gain from this breach of trust.

The fringe of the Eurozone Central European nations and Eastern European countries bordering Russia running developing economies rely on Huawei and other low-cost Chinese tech suppliers like ZTE to offer value for money for a populace who cannot afford $1000 Apple (AAPL) iPhones and exorbitant western European telecommunications infrastructure equipment.

The Chinese beelining to this burgeoning area in Europe has given these less developed countries high-speed broadband internet for $10-$15 per month and 4G mobile service for $7 per month, a smidgeon of what westerners fork out for the same monthly service.

Poland rebuffing Huawei is an ominous sign for Chinese tech doing business in the Czech Republic and Hungary as European countries are moving towards denying Huawei in unison.

The last few years saw China create the same recipe of success for fueling economic expansion mimicking the American economy.

The tech sector led the way with outsized gains boosting productivity while analog companies transformed into digital companies to take advantage of the efficiencies high-tech provides.

At the same time, Beijing has initiated a muscular response to the accelerated growth of local tech companies.

The foul play of American tech in Europe has given impetus to Beijing to launch a power grab on local tech structures such as Baidu, Alibaba, and Tencent.

This couldn’t be more evident at Tencent who has failed to secure any new gaming licenses for their best gaming titles.

PlayerUnknown’s Battlegrounds (PUBG), a battle royale multiplayer, has been deprived of massive revenue because of Tencent’s inability to win a proper gaming license from the Chinese authorities to sell in-game add-ons.

In total, lost revenue has already cost Chinese video game companies over $2 billion in revenue since May 2017.

Beijing wants to temper the growing clout of private tech companies who were the recipient of the Chinese consumer’s gorge on technology in the last 20 years.

These companies have never been more infiltrated by the communist party and this can be mainly attributed to the acknowledgment by Beijing that Chinese tech companies are too powerful for their own good now and are a legitimate threat to the powers above.

That is what the sudden retirement of Founder of Alibaba Jack Ma told us who infuriated Chairman Xi because Ma was the first Chinese of note to meet American President Donald Trump at Trump Towers pledging to create a million jobs in America.

Ma later rescinded that statement and was put out to pasture by Beijing.

What does this all mean?

As the broad-based balkanization spreads like wildfire, Chinese and American tech companies’ addressable markets will shrink hamstringing the drive to accelerate revenue.

The potential loss of Europe for the Chinese could give way to Nokia, Siemens, and other western telecommunication companies to move in hijacking a bright spot for Huawei.

If Apple isn’t punching above their weight in China, well that almost certainly means that local tech companies aren’t having a cake walk in the park as well.

The winter sell-off turned the screws on tech first and then the rest of equities obediently, Chinese tech could have a similar domino effect to the Chinese economy boding badly for Chinese ADRs listed on the New York Stock Exchange (NYSE).

Last year, the Shanghai index was one of the worst performing stock markets in the world.

And if the trade wars are really ravaging a few key limbs from local Chinese tech firms, then companies exposed to the Chinese consumer such as Alibaba (BABA), JD.com (JD), Pinduoduo (PDD), Ctrip.com International (CTRP) and Tencent Music Entertainment (TME) could fall off a cliff.

This has already been in the works.

These companies are a good barometer of the health of the Chinese consumer and have had an abysmal last six months of price action.

The vicious cycle will repeat itself with worsening Chinese data drying up the demand for Chinese tech services and the Chinese consumer tightening their purse strings as they try to save money from a cratering economy.

It could become a self-fulfilling prophecy and that is what other indicators such as negative automobile sales and a rapidly failing real estate market are telling us.

The 65 million ghost apartments dotted around China don't help.

This could be the perfect opportunity to instigate wide-ranging reforms to open up the financial, insurance, a tech market to the west, something many analysts thought China would do after joining the World Trade Organization (WTO).

However, Beijing’s retrenchment preferring to pedal mercantilism and cold-blooded power grabs could offer Chairman Xi the prospect of further consolidating his authority by sticking his fingers deeper into the local tech structures giving the state even more control.

I would guess this is a false dawn.

American tech will confront balkanization headwinds of its own evidence in Vietnam as the government blamed Zuckerberg’s Facebook (FB) for failing to root out anti-government rhetoric which is illegal in the communist-based country.

If you haven’t figured it out yet – there is an underlying suitability issue with western tech services that tie up with authoritarian governments.

It many times leads the western tech companies to be a pawn in a political game that later turns into a bloody mess.

The weak rule of law has spawned a convenient practice of blaming western tech to distract from internal disputes strengthening the nationalist case of a purported western tech firm gone rogue.

This could lead Facebook to be removed in Vietnam, and the $238 million in ad revenue that will vanish.

Headaches are sprouting up across Europe with Facebook clashing with more stringent data privacy rules through General Data Protection Regulation (GDPR).

German’s largest national Sunday newspaper Bild am Sonntag claimed from sources that the Federal Cartel Office will summon Facebook to halt collecting some user data.

This could take a machete to ad revenue in a critical lucrative market for Facebook, and this experience is being echoed by other American tech companies who are running full speed into complicated regulatory quagmires outside of America.

Adding benzine to the flames, Deputy Attorney General Rod Rosenstein speaking at a cybercrime symposium at Georgetown University’s Law Center in Washington added to the tech misery explaining that to “secure devices requires additional testing and validation—which slows production times — and costs more money.”

This is not bullish to the overall tech picture at all.

Hamstringing tech is not ideal to promoting economic growth, but the decades of unchecked growth is finally reverting back to the mean with regulation rearing its unpretty head and the balkanization of tech forcing countries to pick between China or America.

The silver lining is that the American economy remains resilient taking the body blows of a government shutdown, interest rate drama, and trade war uncertainty in full stride.

The net-net is that American and Chinese tech firms could experience decelerating revenue growth far dire than any worst-case scenario forecasted by industry analysts.

Therefore, I forecast that American tech shares have limited upside for the next 6-10 weeks and Chinese tech is dead money in that same time span.

Any rally is ripe for another sell-off if there are no meaningful breakthroughs in the trade war and if China’s economic data continues to falter.

The global growth scare could actually come home to roost.

The supposed narrowing of trade differences has been nothing more than tactical, and procuring any fundamental victories is a hard ask in the short term.

In an ideal world, China would open the floodgates and allow the world to join them in an economic détente, however, based on Chairman Xi’s record of purging his mainland enemies and the military, slamming the gates shut and padlocking them seems more likely at this point.

Seizing the rights to an untimed Chairmanship term has its perks – this is one of them and he is using the entire assortment of options available to him.

Traders should look at deep in-the-money vertical bear put spreads on any sharp rally to specific out-of-fashion tech names saddled with regulatory and data balkanization headwinds, or tech firms with a large footprint in mainland China.

Mad Hedge Technology Letter

December 17, 2018

Fiat Lux

Featured Trade:

(WHY TENCENT WILL REMAIN TRAPPED IN CHINA)

(TME), (SPOT), (IQ), (GOOGL), (FB)

So you thought that Tencent Music Entertainment (TME), the Spotify (SPOT) of China, going public at $13 a share on the New York Stock exchange would mean the music streaming giant would potentially tyrannize the Western music streaming market.

Relax, it will never happen, China’s personal data laws are analogous to Facebook’s (FB) lax data guidelines multiplied by a factor of 10.

There is no possible scenario in which a Chinese content service constructed at the magnitude of Tencent Music Entertainment Group would ever get the thumbs up from American regulators.

The ongoing trade war has effectively barred any Chinese capital’s ability to snap up key American technological firms, as well as stymieing any Chinese tech unicorns dishing out streaming content in participating in a monetary relationship with the American consumer.

In August, the Department of the Treasury which chairs the Committee on Foreign Investment in the United States (CFIUS) rolled out an expansionary pilot program widening CFIUS’ jurisdiction to review foreign non-controlling, non-passive investments in companies that produce, design, test, manufacture, fabricate, or develop “critical technologies” within certain industries deemed paramount to national security.

Even though the amendment does not specify China, it means China.

If you had a hunch that Tencent would take over the music streaming world, then the better question is to ask yourself if Tencent Entertainment is equipped to take over the Chinese streaming world and monetize the product efficiently.

What really is (TME)?

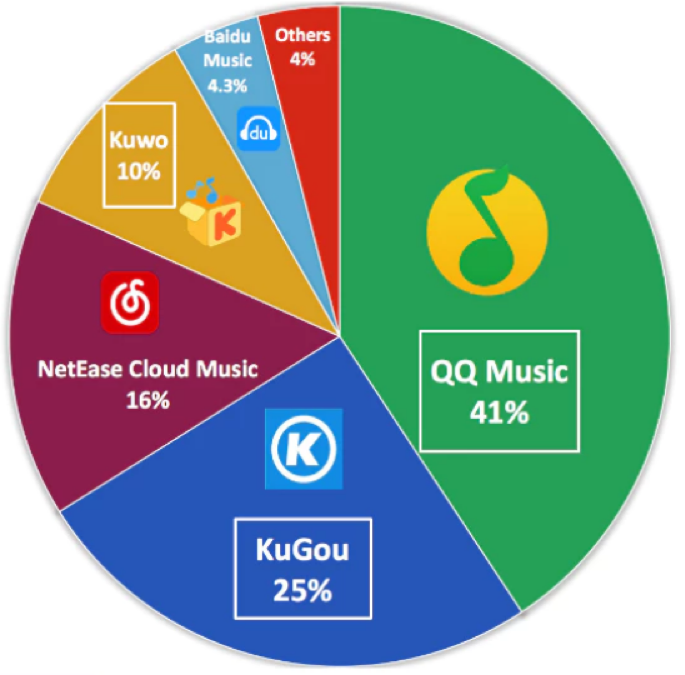

(TME) is the Tsar of Chinese music streaming with apps that allow users to stream music, sing karaoke, and watch musicians perform live. (TME) dominates this sphere of Chinese tech with a combined 800 million monthly active users.

(TME) is a concoction of services including QQ Music, Kugou, Kuwo, and karaoke app WeSing making up over 70% of the music streaming industry in China.

Its daily active users (DAUs) spend over 70 minutes per day on the platform and have inked exclusive deals with elite Western artists.

Tencent Music's revenue nearly doubled YOY to $2 billion during the first nine months of 2018, and its net income more than tripled to $394 million.

The social entertainment services aspect has been a massive revenue driver for them including income from virtual gifts on WeSing, a platform where fans gift virtual items to favorite singers, and sign up for premium memberships giving users access to exclusive concerts.

This collection of clever services mixed with social media has been successful, and the reason why it comprises 70% of total revenue.

Paid membership has grown 24% YOY to 9.9 million while paid users only make up 4.4% in China. This is a huge change in the tech climate from the past when Chinese netizens would never pay for internet content. This has allowed the average revenue per user (ARPU) to creep up to $17.22 per paid user.

The other 30% of revenue can be attributed to its ad-less music service which is not ad-less for free users.

So, in fact, the 30% of the business that mirrors Spotify is its Achilles heels echoing the painstaking task of monetizing pure music content.

No company has ever shown that a pure music streaming internet model can be profitable, the music streaming graveyard is littered with the failed attempts of companies from the past.

The unit registered a mere $1.24 in average revenue per paid user during the third quarter, paltry compared to (TME)’s social media products.

(TME)’s combination of social media and music entertainment weighted towards virtual gifts’ income is a weak business model in the west and would not extrapolate in the western world.

It is a supremely China model only unique to China and other Asian countries.

Therefore, I would point out that even if this arm of Tencent could migrate to America, management knows better than to put square pegs in round holes.

That being said, its potential in China is its long runway and most Chinese content companies haven’t been able to crack the western market.

The only types of Chinese companies that have had any remnant of success in the west are hardware companies and look what happened to telecommunication equipment companies Huawei and ZTE recently – taken out by the western regulatory sledgehammer.

It’s crystal clear that the Chinese understanding of personal data and IP regulation simply don’t marry up with western standards, and that is why I suggested that these two massive tech worlds are in for a hard splintering dividing these two competing models.

There has been some intense jawboning going on behind the scenes as Huawei, who is in the lead to develop 5G technology, still needs Qualcomm’s radio access technology to make 5G a reality.

The scenario of a hard fork between western and Chinese 5G becomes more real each passing day.

Part of Tencent Music’s ability to perform revolves around its swanky position installed in the center of the most popular chat app in China called WeChat.

Using this position as a fulcrum, Tencent Music plans to invest 40% of the capital raised from its IPO on expanding its music library, 30% on product development, 15% on marketing, and the last 15% on M&A.

For right now, there is an elevated emphasis on growing the number of paid users and converting its free users to premium subscriptions.

Ironically enough, Spotify has a 9% stake in Tencent Music and Tencent has a 7.5% holding in Spotify. Just by having stakes in each other is enough reason to avoid migrating into the same competitive markets with each other.

If you read between the lines, the stakes seem more a pledge of trading expertise in developing each other’s business as you see traces of each other in both unicorns.

Would I invest in Tencent Music?

One word – No.

There are almost 1,000 pending lawsuits alleging copyright infringement, not a huge surprise here.

Tencent concedes around 20% of the music content is not licensed.

Pouring fuel on the fire, a Tencent Music executive is also being sued by a seed investor claiming he was bullied into selling his stake ahead of its IPO.

There are question marks surrounding this company and that might have been part of the justification of tapping up the American public markets to prepare for this next stage of uncertainty.

As it is, Spotify cannot make money because of the elevated royalty costs eroding its business model, (TME) probably can if it steals most of its music, but that is a suicide mission waiting to happen.

Fortunately, Tencent is a hybrid mix of not only pure music streaming but of social media fused with music apps through gift giving gimmicks and karaoke-themed services.

These higher margin drivers are the reason why Tencent is profitable and Spotify is not, plus the giant scale of servicing 800 million Chinese users that give credence to the freemium model.

However, it’s entirely feasible that Tencent Music could use a good portion of the $1.1 billion from the IPO to battle the slew of pending lawsuits waiting around the corner.

Would you want to invest in a company that went public just to fund their legal defense?

Definitely not.

Look at its streaming cousin iQIYI (IQ), shares peaked over $40 in June after its IPO and have swan-dived ever since going down in a straight line and is trading around $17 today.

In general, most Chinese tech stocks have been collateral damage of a wider trade war pitting the maestros of crude geopolitical strategies against each other.

This year has not been kind to Chinese tech shares, and considering most of Tencent’s music library has been stolen, investors would be crazy to invest in this company.

I am surprised this company held up as well as it did on IPO day because the timing of the IPO couldn’t have been worse in a segment of tech that is awfully difficult to become profitable in a country whose economy is softening by the day in an insanely volatile stock market.

And to be honest, I would have stopped listening about this company after knowing they face pending lawsuits of up to 1000.

As for Spotify, yes, they are the industry leader in music streaming but investors need concrete proof they can become profitable. I like the direction of increasing operating margins, but that all goes to naught if it’s in a perpetual loss-making enterprise. I would sit out on both these stocks with a much negative bias towards its ticking time bomb Chinese music version.

Regulation and the trade war have taken a huge swath of tech off the gravy trade such as semiconductors, Google, social media, hardware, American tech who possess supply chains in China and I would smush in Chinese tech ADR’s on that list too.

Stay away like the plague.