Mad Hedge Biotech and Healthcare Letter

March 22, 2022

Fiat Lux

Featured Trade:

(THE 800-POUND GORILLA IN THE GENE-SEQUENCING SECTOR)

(ILMN), (A), (TMO), (MRK), (RHHBY)

Mad Hedge Biotech and Healthcare Letter

March 22, 2022

Fiat Lux

Featured Trade:

(THE 800-POUND GORILLA IN THE GENE-SEQUENCING SECTOR)

(ILMN), (A), (TMO), (MRK), (RHHBY)

I’m a huge fan of the "razor and blades" business strategy, where the pricing and marketing model is designed to generate recurring, dependable income by ensuring that a customer is locked in onto a product or service for a long time.

The COVID-19 pandemic underscored the significance of DNA sequencing in improving and monitoring global health.

Thanks to DNA sequencing, we were able to identify the novel coronavirus and eventually developed vaccines and PCR-based tests. This also played a crucial role in detecting new strains and even transmission tracking.

To date, the top name in the DNA sequencing community is Illumina (ILMN).

In terms of competitors, the closest to Illumina’s dominance are Agilent Technologies (A) and Thermo Fisher Scientific (TMO). However, neither have developed their platforms enough to be directly comparable to Illumina.

Illumina has a notable installed base comprising approximately 20,000 machines owned by roughly 7,300 clients.

With the rising popularity of DNA sequencing, the demand for the company’s installation base is estimated to continue growing and along with it is the sale of consumables.

This is where the razor and blades business model comes in.

The consumables form a major part of Illumina’s strategy, with the instruments serving as “razors” and consumables as “blades.”

The cost of instruments can fall within the range of $20,000 to $1 million and are essential elements of expanding the company’s portfolio and locking in clients into long-term commitments.

Consumables typically represent 50% or more of the revenue of any DNA sequencing company. For Illumina, the number climbs to 80%.

Considering that the consumables also need repairs, this segment is expected to continue generating profits in services and contracts.

Evidently, 80% recurring revenue is highly indicative of a rock-solid business.

While the business model isn’t unique to Illumina, the company has attracted attention in Wall Street due to its exponential growth over the past years.

In the last five years, Illumina has practically doubled its revenue. During the COVID-induced economic slowdown, the company quickly recovered from a brief slump and accelerated its revenue growth at an even faster pace.

In the fourth quarter report for 2021, Illumina reported about $1.9 billion in revenue or an impressive 25% increase year-over-year.

As for 2022, the company is conservatively anticipating a 14% to 16% growth in its revenue.

Another step towards securing dominance in this field is Illumina’s decision to launch the TruSight Oncology Comprehensive test in Europe.

This is basically a cancer test that uses a single tissue sample to test for a broad range of tumor genes and biomarkers.

The goal is to create a “tumor profile” of patients with rare conditions to find a matching treatment option via precision technology. This doesn’t only cover available cancer therapies in the market but also clinical trials.

While this test focuses on the oncology sector, Illumina and its competitors are presumably working on more sophisticated genetic profile-based diagnostic tools for other conditions.

Although this has yet to be launched on a larger scale, Illumina is reported to seek collaborations with leading oncology treatment providers like Merck (MRK), Bayer (BAYN), and Roche (RHHBY).

Illumina has invested in seven new startups to further expand its pipeline: 4SR Biosciences; B4X; Cache DNA; CRISP-HR Therapeutics; NonExomics; Purpose Health; and Rethink Bio.

These focus on breakthrough therapies, DNA storage, mental wellness, sustainable food, and diagnostics.

Illumina has invested in 68 startups to date. This is a brilliant scheme to continue company growth and pipeline expansion for decades.

The DNA sequencing market was valued at $6.243 million in 2017 and is projected to hit $25.470 million by 2025.

Illumina’s remarkable execution of the razor and blades model, strong profit margins, and proactive profitability initiatives catapulted it to the top of the DNA sequencing sector.

Needless to say, Illumina is the 800-pound gorilla in the gene-sequencing sector—a dominance that is expected to go on for years.

Mad Hedge Biotech and Healthcare Letter

February 8, 2022

Fiat Lux

Featured Trade:

(A NEW WAVE OF GENE-EDITING EXPERTS)

(NTLA), (REGN), (VRTX), (CRSP), (TMO), (SGMO), (EDIT), (MRK), (BIIB)

The gene-editing sector quietly achieved historical results in 2021. Last year, human trials of two in vivo CRISPR-centered treatments released promising data.

One study, conducted by Intellia Therapeutics (NTLA) and Regeneron Pharmaceuticals (REGN), worked on targeting the faulty gene responsible for transthyretin amyloidosis.

Using their new CRISPR-based therapy, they were able to record an impressive 96% decline in the transthyretin gene.

This is an impressive accomplishment not only for its high efficacy but also for the mere fact that no other work has managed to record any significant effect on the gene for almost a decade now.

The other study is by Vertex Pharmaceuticals (VRTX) and CRISPR Therapeutics (CRSP). Over the years, the two have been collaborating on coming up with treatments for various rare diseases.

In 2021, they recorded promising results in their clinical trials for sickle cell disease and beta-thalassemia. Aside from the potency of these treatments, there is a possibility that the effects would offer long-lasting improvements in the patients' lives.

While 2021 was clearly a remarkable year for the gene-editing sector, all signs indicate an even better 2022.

If the sector doesn’t deliver, there will be 2023 and the year after. After all, the gene-editing world is the kind of space that gets better with age.

More than that, this sector will keep evolving and attracting new players every year.

Hence, key players like Thermo Fisher Scientific (TMO), Sangamo Therapeutics (SGMO), Editas Medicine (EDIT), Merck (MRK), and Oxford Genetics cannot expect to be the top names in the industry forever.

Recently, some names have been making waves in the gene-editing industry.

One is Excision BioTherapeutics. Founded in 2015, this Philadelphia biotechnology company leverages its CRISPR-based platform to target viral infections.

Basically, they aim to snip the viral DNA out of the host genome.

To date, the company’s most advanced project is its HIV treatment: EBT-101. So far, Excision has managed to functionally cure its test animals of the infection by removing their HIV genomes.

Ultimately, Excision’s goal is to come up with a “one-and-done” therapy for viral diseases.

Apart from working on HIV treatments, the company is also looking into potential cures for herpes simplex, hepatitis B, and a rare brain infection called multifocal leukoencephalopathy.

If these treatments succeed, Excision’s therapies would be available in highly specialized treatment centers.

Another promising biotechnology company is California’s Scribe Therapeutics, which was founded in 2018.

Describing their approach to be guided with an “engineer first” philosophy, Scribe’s plans to use CRISPR-based gene-editing tools to achieve their goals.

Instead of using the conventional CRISPR-Cas9 methods, the company opts for modified versions of the RNA-guided genome editors or CasX enzymes.

Scribe has been developing these CasX enzymes to ensure that they acquire the qualities of the target for enhanced specificity.

That is, the company wants its “editor” to learn as much as possible about the characteristics of the system to deliver intentionally designed solutions.

Simply, Scribe aims to control all elements and eliminate the need to leave anything to chance or even nature.

Since its founding, Scribe has been actively developing solutions for unmet medical needs.

For instance, it has been working with Biogen (BIIB) to develop and eventually market CRISPR-based treatments that target an underlying genetic component of a nervous system disease called amyotrophic lateral sclerosis.

The agreement states that Scribe will get $15 million upfront and receive over $400 million in potential milestone payments.

The company has already started testing its technology in mouse models, focusing on neurological and neurodegenerative conditions.

Given their current trajectory, Scribe expects to release data by the third or fourth quarter of 2022 or early 2023.

All in all, gene-editing tools have evolved so much from the mid-twentieth century. Back in the 1970s and 1980s, the process of gene targeting was only possible in experiments on mice.

Since then, the ever-expanding world of science has pushed the sectors of gene analysis and manipulations to cover all kinds of cells and organisms.

Considering the increasing demand in this sector, it’s no wonder the gene-editing world has been growing at breakneck speed over the past years—a pace that won’t slow down anytime soon.

Mad Hedge Bitcoin Letter

October 14, 2021

Fiat Lux

Featured Trade:

(WHAT’S NEW IN BIOTECH)

(CGTX), (BIIB), (LLY), (ABBV), (NVS), (TAK), (PYXS), (PFE),

(AZN), (GILD), (GSK), (IMGN), (ISO), (TMO), (BIO)

As the biotechnology world is ever-evolving, with several companies going public every few months, let me share some of the most promising names that recently emerged.

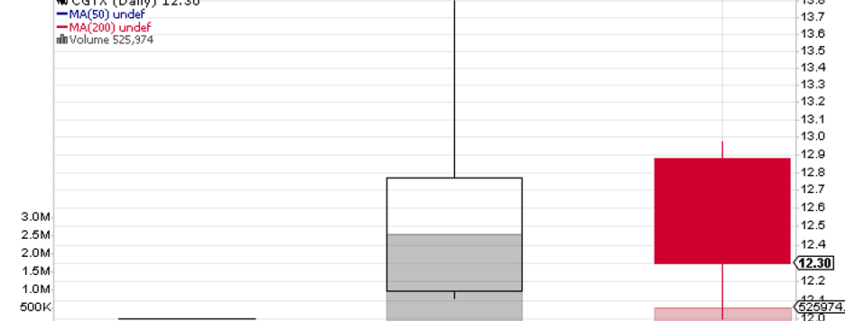

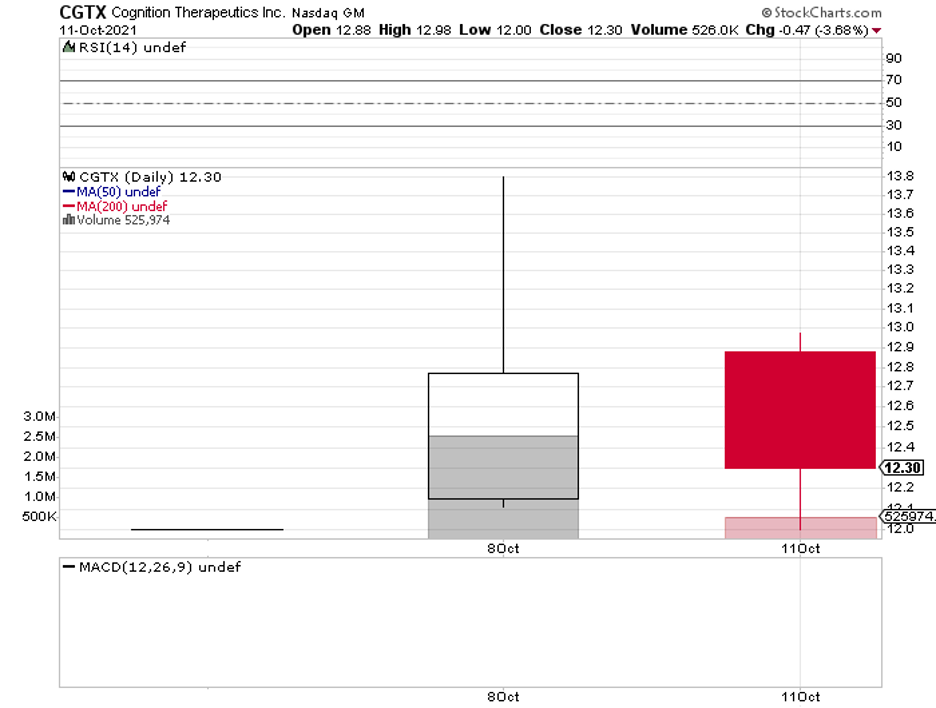

The first is Cognition Therapeutics (CGTX), a company working on treatments for Alzheimer’s disease and macular degeneration.

Its most promising candidate is an Alzheimer’s treatment called CT1812, which is currently under Phase 2 trials. Looking at the timeline, CGTX expects to release topline data by 2023.

With the expected growth of the aging population, focusing on treating various forms of Alzheimer’s is a promising direction for Cognition Therapeutics.

In fact, the global market for this neurodegenerative disease is projected to grow from $2.9 billion in 2018 to a whopping $10.5 billion by 2025.

So far, the major competitors of Cognition Therapeutics in this area include Biogen (BIIB), Eli Lilly (LLY), AbbVie (ABBV), Novartis (NVS), and Takeda (TAK).

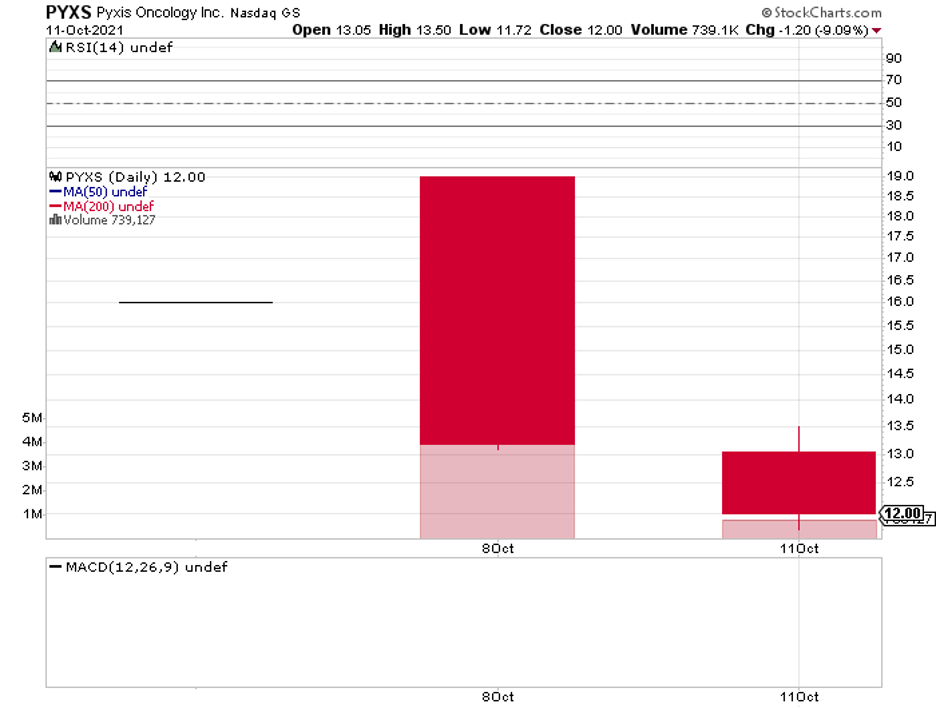

The second promising biotech company is Pyxis Oncology (PYXS), which is a spinoff from Pfizer (PFE).

Pyxis is focused on developing next-generation treatments targeting difficult-to-treat types of cancer.

Basically, the company’s goal is to create therapies that can directly kill tumor cells. It also wants to get rid of the underlying problems that lead to the uncontrollable spread of tumors and the weakening of the immune system.

To do this, Pyxis has come up with novel antibody drug conjugate (ACT) candidates and other monoclonal antibody (mAb) pipelines.

Its lead candidate is called ADC PYX-201, a potential treatment for non-small cell lung cancer and breast cancer.

The goal of ADC PYX-201 is to target actively multiplying tumors while boosting the immune response of the patient’s body. Pyxis plans to submit it as a non-small cell lung cancer treatment candidate by mid-2022.

If approved, then ADC PYX-201 will be under patent protection until 2037.

This holds great potential for Pyxis’ cashflow, as the market for non-small cell lung cancer worldwide is anticipated to rise from $6.2 billion in 2016 to over $12 billion by 2025.

With this potential of ADC treatments, Pyxis can expect competition from the likes of AstraZeneca (AZN), Gilead Sciences (GILD), GlaxoSmithKline (GSK), and ImmunoGen (IMGN).

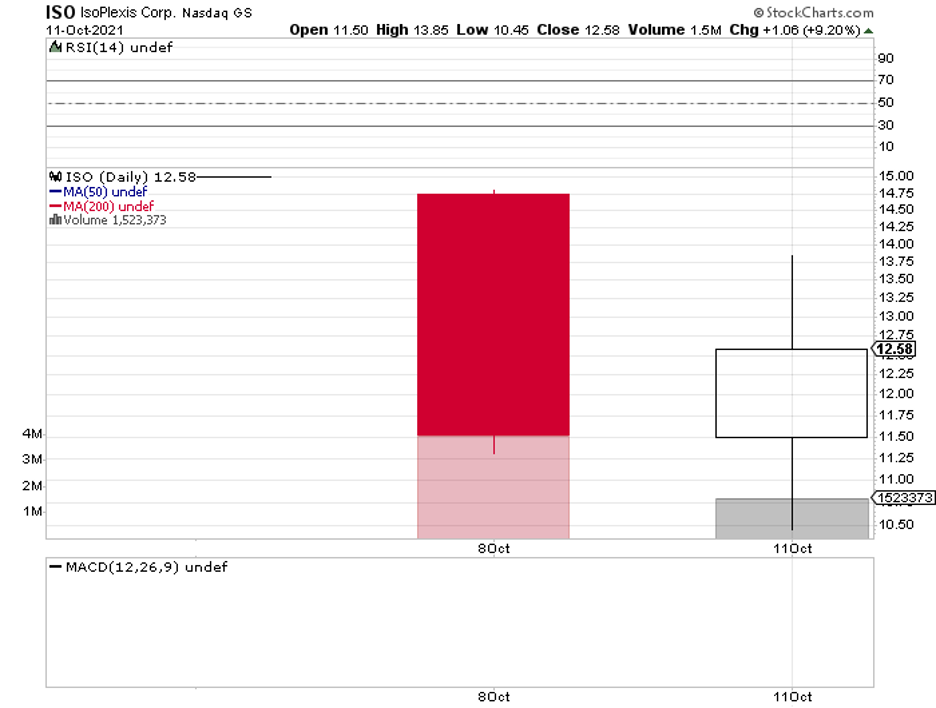

The last name on today’s list is IsoPlexis Corporation (ISO).

This company is the first to focus on dynamic proteomics and single-cell biology in an effort to develop “walk-away automation” products that aid in shortening the therapeutic development timelines by acquiring “multiplexed proteomics with very low sample volumes that reflect in vivo biology to clarify lead candidates.”

In layman’s terms, IsoPlexis is working on a technology that aims to identify every protein in the body to speed up the development of new therapies for rare diseases.

This is a lucrative business, with IsoPlexis targeting at least $34 billion in the total addressable market.

Considering that IsoPlexis is a pioneer in this field, it is possible for it to gain the lion’s share of the segment and position itself as an undisputed leader for years.

More importantly, IsoPlexis can use its patented technology, “Proteomic Barcoded,” to expand the use cases to cover other lucrative markets.

For example, IsoPlexis can apply its technology to cancer immunology and targeted oncology by predicting the progression of cancer cells in the body.

Adding cell therapies to the company’s pipeline is also a very realistic possibility since its technology can be utilized to create CAR-T cell therapies as well.

In fact, IsoPlexis’ approach is already being used in developing treatments for leukemia and melanoma.

Another profitable avenue for IsoPlexis’ technology is the vaccines sector.

Since the development of vaccines requires profiling the responses of the respiratory and immune systems, the company’s data would accelerate the entire process.

So far, the major rivals of IsoPlexis in this space include Thermo Fisher Scientific (TMO) and Bio Rad Laboratories (BIO).

While all these biotech companies offer promising products and technologies, they’re all still in the early stages of development.

This makes them high-risk investments and are likely suitable for those who are willing to invest in the long term.

For those who want to see movement faster and sooner, it might be best to watch these stocks from the sidelines.

Mad Hedge Biotech & Healthcare Letter

July 8, 2021

Fiat Lux

FEATURED TRADE:

(TURNING THE BIOHACKERS’ DREAM TO REALITY)

(NEO), (AZN), (GSK), (ABBV), (ILMN), (TMO), (TXG), (BLUE), (CRSP), (EDIT)

There is a huge possibility that the first person to ever live to a thousand years old has been born in our lifetime.

That’s according to experts on life longevity. They also say that sooner rather than later, we’ll simply be checking ourselves into hospitals or clinics once every decade.

Pretty much how you’d bring your car in for a service, that’s how we’ll keep our bodies working at peak condition for centuries.

As far-fetched as it sounds, it’s undeniable that dreams of achieving immortality are as old as mankind itself.

One of the leading experts on this is the Human Longevity, Inc., which has leading genomics expert J. Craig Venter and billionaire Peter Diamandis as its founders.

Although it’s still not yet a publicly-traded company, Human Longevity, Inc. has been collaborating with cancer diagnostics firm Neogenomics (NEO).

Admittedly, NEO’s $5.32 billion market capitalization doesn’t really boost that much confidence in this company.

However, Human Longevity’s work with a Big Pharma company like AstraZeneca (AZN), which holds a market cap of $158.14 billion, definitely backs up its claims.

Moreover, AstraZeneca and Human Longevity are already halfway through their 10-year agreement that dates back to 2016.

Basically, what Human Longevity does is sequence an individual’s DNA and combine the information with an extensive list of tests to figure out how long that person will live and what steps can be taken to extend his or her life.

More impressively, the company can use the data to predict a budding disease, such as cancer, even before it exhibits symptoms.

And how much will that cost you?

Right now, the company is charging $25,000 for a comprehensive set of tests and a full profile.

In the end, you’d be given medical information about yourself that amounts to roughly 1 petabyte. For context, that’s 1,000 terabytes or 1 million GB worth of data.

While the cost is definitely high, it’s a good preventive measure to consider if you can spare the cash.

This is because the company can detect the slightest hint of diseases, which are typically at their most treatable phase.

Since the company is founded on the belief that we are all “DNA software-driven species,” it can also determine the disease-producing genes in our systems and use them as “pharmaceutical targets, so that people with those genetic changes don’t die.”

Aside from Human Longevity, another company working on this nice is called Life Biosciences, which was founded in 2017.

Since its launch, Life Biosciences has been acquiring companies left and right to boost its pipelines.

So far, it has at least 6 subsidiaries focused on developing treatments to fight the human aging process.

What makes Life Biosciences different is that it doesn’t focus on the leading causes of death, such as cardiovascular diseases or cancer.

Instead, it tries to figure out what are the underlying causes of the body’s aging. This includes stem cell exhaustion, cellular senescence, chromosomal instability, and even our metabolism.

At their core, Life Biosciences’ belief is that aging itself should not be considered a natural biological result of the passage of time.

Rather, it should be understood as a medical condition—the kind that can be treated in the same way we’d try to find medications or cures for diseases.

While Life Biosciences’ work has yet to earn any FDA approval, the involvement of GlaxoSmithKline (GSK) in its aging research seems to boost confidence in the company’s work.

Apart from GSK, a number of tech billionaires have expressly backed these efforts in the anti-aging field.

The most visible ones include Calico, which is backed by Google and AbbVie (ABBV), and Unity Biotechnology, supported by Jeff Bezos.

While Human Longevity and Life Biosciences have yet to go on IPO, there are already companies working on fields related to life longevity.

The first names that come to mind are the frontrunners of the genome sequencing market, such as Illumina (ILMN), Thermo Fisher Scientific (TMO), and 10x Genomics (TXG).

Smaller companies in this field include bluebird Bio (BLUE), CRISPR Therapeutics (CRSP), and Editas Medicine (EDIT).

Inasmuch as this is difficult to grasp at this stage, there is a massive market for this industry. In fact, the global longevity segment is projected to reach $27 trillion in 2026, which accounts for roughly 20% of the global GDP.

Meanwhile, the global market for human aging is estimated to reach at least $55 billion by 2023.

And those are just conservative estimates.

Making the public accept the idea behind longevity science has not been easy. Even with Big Pharma names backing these innovative companies, people are still wary of the concept.

After all, surveys show that most people would refuse medical treatments to slow their aging and allow them to live up to 120 or older. It’s not surprising why.

Those respondents probably witnessed how their older grandparents and parents spent their final years in pain and were subjected to invasive medical procedures. That makes the entire idea of living so long horrific to them.

However, the future imagined by these companies is different. Through their research, people can live long and still enjoy active and healthy lifestyles.

At this point, the longevity science space remains a playground dominated by a handful of transhumanists and even biohackers.

Nonetheless, the entry of the most respected researchers and the support from the biggest biopharmaceutical companies across the globe give hope that the promises the industry holds will become a reality soon.

Mad Hedge Biotech & Healthcare Letter

June 17, 2021

Fiat Lux

FEATURED TRADE:

(VALUE CREATOR STOCK OPERATING UNDER THE RADAR)

(TECH), (AMGN), (ABT), (TMO)

There’s a wildly underrated and undercovered biotechnology stock despite its track record of creating long-term value and ability to outstrip its projected operational performance in the past years.

This stock is Bio-Techne (TECH).

Historically, Bio-Techne has reported impressively good margins, which could partly be attributed to the company’s incredibly strong intellectual property position.

While Bio-Techne originally concentrated on offering biotechnology solutions, it eventually embraced a diversification strategy thanks to all the dealmaking it has been doing over the years.

Back in the 1990s, Bio-Techne struck deals with promising biotechnology companies like Amgen (AMGN) and even Genzyme to acquire sections of their research departments.

Borrowing Warren Buffett’s expression, Bio-Techne’s value can be seen on the “owner earnings” it has been reporting. Thanks to a change in management in 2013, this sleepy high-margin company has been reinvigorated through various strategic acquisitions.

So far, Bio-Techne has three very active divisions.

It has its biotechnology division, which comprises 65% of its revenue and sells proteins, reagents, and antibodies right out of the freezer.

It has its protein platforms, which market instruments that push the use of the products sold by its biotechnology sector.

Lastly, it has its diagnostics sector that supplies equipment, such as those used for protein analysis, to other companies, including Thermo Fisher Scientific (TMO) and Abbott Laboratories (ABT).

Meanwhile, Bio-Techne has been making progress in stem cell research and Car-T immunotherapy, along with other kinds of cancer research.

Sales have been climbing steadily, increasing by an average of 15.7% over the last five years, with room for margins to pick up as Bio-Techne continues to integrate acquisitions.

To continue expanding its business, Bio-Techne recently shared its decision to buy diagnostics company Asuragen for $215 million.

Founded in 2006, Texas-based Asuragen develops and produces test kits for cancer and genetic carrier testing.

Estimated to contribute $30 million in revenue, Bio-Techne is actually paying only a mere 7 times its sales multiple—with the potential to jump to about 10 times as future contingent payments could boost the purchase price by an additional $105 million.

Even if that happens though, Bio-Techne will still be pumping sales at an extremely favorable multiple compared to its current multiple.

Another major acquisition of Bio-Techne is its 2018 deal with Advanced Cellular Diagnostics, which was executed to boost its diagnostics portfolio.

At the time, Advanced Cellular Diagnostics’ top line was already growing by 40% to 50%.

One of the most exciting products this acquisition added to Bio-Techne’s lineup is a tumor diagnostic test.

For context, current diagnostic tests are only 75% accurate. In comparison, Advanced Cellular Diagnostics’ test is 95% accurate. This makes the latter an extremely attractive product in the industry.

The company also has solid patent protection for new products focusing on gene and gene fragment probes.

Overall, the lineup from Advanced Cellular Diagnostics is estimated to bring in at least $50 million in additional yearly revenue for Bio-Techne.

The fact that it’s growing by 50% annually makes the acquisition one of the best buys of this biotechnology company.

Since being founded back in 1976, Bio-Techne has established itself as a steady value creator.

Needless to say, Bio-Techne is a highly profitable business, with earnings anticipated to increase by 15% annually.

Looking at the recurring nature of the company’s revenue, its consistent earnings, the potential of its Advanced Cellular Diagnostics purchase, and its prospects for more accretive acquisitions, Bio-Techne should be able to hold its mid-30s multiple to owner earnings.

Despite the pandemic’s effect on the biotechnology and healthcare sector in 2020, Bio-Techne still reported a 45% growth in its annual sales to reach $739 million last year.

So far, Bio-Techne is on track for its goal to become an over $30 million type portfolio. In terms of its five-year outlook, the company is targeting to reach $1.5 billion in the next few years.

Surprisingly, it’s still operating under the radar of the majority of investors, even in the biotechnology sector.

For biotechnology investors on the lookout for a value creator stock, it’s wise to keep an eye on Bio-Techne. Simply checking its bolt-on M&A strategy combined with its steady organic growth rate, this company has the potential to provide long-term returns.