The U.S. 10-year Treasury bond ($TNX) has surged past the October 2022 high so what does that mean for tech stocks ($COMPQ)?

In short term, tech shares will be held back.

Tech stocks are the most exposed to collateral damage from surging interest rates because of the growth nature of the sector.

Funnily enough, much of this 2023 rally has been fueled by the notion of a Fed “pivot” coming down the pipeline.

It still hasn’t come, but now the pendulum has swung the other way and tech shares, even the biggest and best, and getting brutalized.

The people short tech stocks in 2023 couldn’t have been more wrong even if betting against the Fed doesn’t usually work.

Now, the inverse of the Fed pivot is taking place as the U.S. 10-year Treasury bond has hit highs of 4.32% demolishing last years’ peak.

Technically, once recent highs shatter, it is common for set algorithms to motion another wave of money to continue the trend.

The trend for yields is now higher.

It’s highly plausible that this bull market in bond yields picks up and pushes to 5%.

Why is this happening?

The surprisingly resilient US economy has meant the job market is on fire. Tech companies have become leaner, but have abstained from mass firings.

Also, Americans are spending like there is no tomorrow which has kept stocks going up for most of the year and the latest earnings season reinforces this trend.

The result will mean that inflation could remain stubbornly above the Fed’s target, leaving room for long-term yields to push even higher.

There is a remarkable repricing higher in longer-term rates and many traders have been caught off guard.

The market is coming more to the view that there is going to be long-term inflation pressures despite recent progress.

Macro uncertainty is going to remain the story for the next few years, and that requires greater compensation to own long-dated bonds.

But many now expect a soft landing that would leave inflation the dominant risk.

For much of the year, the market worked its way towards a hard landing/Fed pivot scenario which factors in lower inflation. Now the opposite is happening.

Broader economic shifts are also driving speculation that the low rates — and inflation — of the post-crisis period were an anomaly. Among them: surging wage costs, deglobalization, and corporates padding their net margins.

The U.S. is drowning in its own federal debt but must issue more to service the interest on this debt meaning the purchasing power in the United States is crashing.

The net net of this is very negative for technology stocks and it’s a tough pill to swallow after benefiting from the AI bubble and Fed pivot narrative for the first 7 months of the year.

It’s difficult to see another burst of hot money pouring into tech stocks for the rest of 2023.

If we are stuck with the soft landing and the higher for longer narrative, then markets will bid up higher inflation which will suppress tech stocks.

That is what the 4.33% in the 10-year is telling us and tech stocks in the near term will be negatively correlated with this yield moving into the last 3 months of the year.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-18 15:02:562023-08-31 12:42:20A Poor Omen

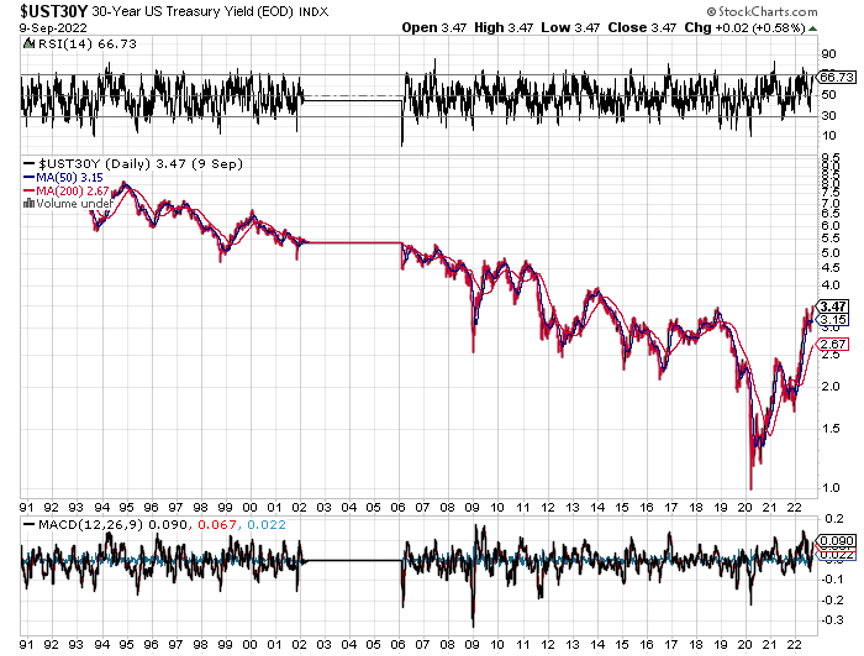

With ten-year US Treasury yields hitting 4.00% yesterday, it’s time to pay the piper for the last 15 years of the borrowing rampage of epic proportions.

This is not a new thing.

We are, in fact, becoming the United States of Debt.

That Washington is taking the lead in this frenzy of borrowing is undeniable. The last administration took the national debt from $23 trillion to $28 trillion during four years of prosperity that was entirely borrowed from the future.

The Biden administration will eventually take that figure up to an eye-popping $38 trillion. That will be the final bill for ending the pandemic, putting 25 million people back to work, and bringing the second Great Depression to a close.

The National Debt exceeded US GDP in 2016, taking the debt to GDP ratio to the highest point since WWII.

Treasury Secretary Janet Yellen recently confided to me that, “It’s the kind of thing that should keep you awake at night.”

It gets worse.

According to the Federal Reserve Bank of New York, total personal debt topped $19 trillion by the end of 2020. An overwhelming share of personal consumption is now funded by credit card borrowing.

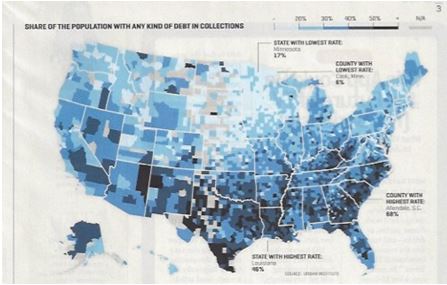

Some 33% of Americans now have debts in some form a collection, and that figure reaches an astonishing 50% in many southern states (see map below). Call it the Confederate States of Debt.

Corporations have also been visiting the money trough with increasing frequency, taking their debt to $6.1 trillion, up by 39% in five years, and by 85% in a decade.

The debt to capital ratio of the top 1,000 companies has ballooned from 35% to 54% and is now the highest in 20 years.

Another foreboding indicator is that corporate debt is rising faster than sales, with debt rising by a breakneck 8.5% annualized compared to 4.6% for sales over the past decade.

Automobile debt now tops $1 trillion and with lax standards has become the new subprime market.

And remember that other 800-pound gorilla in the room?

Student debt now exceeds $1.6 trillion and is rising, as is the default rate. Provisions in the last tax bill eliminate the deductibility of the interest on student debt, making lives increasingly miserable for young borrowers. And you wonder why the US birth rate is so low.

Of course, you can blame the low interest rates that have prevailed for the past decade. Who doesn’t want to borrow when the inflation adjusted long-term cost of money is FREE?

That explains why Apple (AAPL), with $270 billion in cash reserves held overseas, borrowed last year via ultra-low coupon 30-year bond issues, even though it doesn’t need the money. Many other major corporations have done the same.

And while everything looks fine on paper now, what happens if interest rates ever rise and stay high?

The Feds will be in dire straight very quickly. Raise short term rates to the 6% seen at the peak of the last cycle, and the nation’s debt service rockets from 4% to over 10% of the total budget. That’s when the sushi really hits the fan.

You can expect the same kind of vicious math to strike across the entire spectrum of heavily leveraged borrowers going forward, including big borrowers like cruise line, airlines, you, and me.

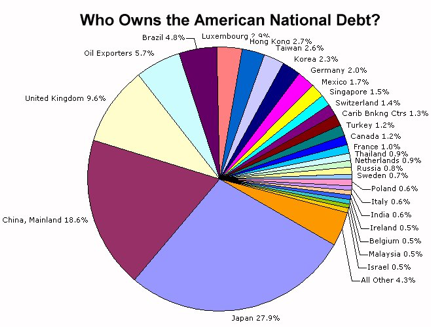

We are also witnessing the withdrawal of the Chinese as major Treasury bond buyers, who along with other sovereign buyers historically took as much as 50% of every issue. Threaten a war on your largest lender and it plays hell with you cash flow.

Rising supply against fewer buyers sounds like a recipe for eventually much higher interest rates to me.

Just watch this space for the next Trade Alert regarding when to get back in for the umpteenth time.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/02/american-debt.jpg285447Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-29 10:02:592022-09-29 12:12:42The United States of Debt

When I was a little kid during the early 1950s, my grandfather used to endlessly rail against Franklin Delano Roosevelt.

The WWI veteran, who was mustard gassed in the trenches of France and was a lifetime, died in the wool Republican, said the former president was a dictator and a traitor to his class, who trampled the constitution with complete disregard.

Republican presidential candidates Hoover, Landon, and Dewey would have done much better jobs.

What was worse, FDR had run up such enormous debts during the Great Depression that, not only would my life be ruined, so would my children’s lives.

As a six-year-old, this disturbed me deeply, as it appeared that just out of diapers, my life was already going to be dull, brutish, and pointless.

Grandpa continued his ranting until a three pack a day Lucky Strike non-filter habit finally killed him in 1977.

He insisted until the day he died that there was no definitive proof that cigarettes caused lung cancer, even though during his war, they referred to them as “coffin nails.”

He was stubborn as a mule to the end. And you wonder whom I got it from?

What my grandfather’s comments did do was spark in me a lifetime interest in the government bond market, not only ours, but everyone else’s around the world.

So, what ever happened to the despised, future destroying Roosevelt debt?

In short, it went to money heaven.

And here I like to use the old movie analogy. Remember, when someone walked into a diner in those old black and white flicks? Check out the prices on the menu on the wall. It says “Coffee: 5 cents, Hamburgers: 10 cents, Steak: 50 cents.”

That is where the Roosevelt debt went.

By the time the 20 and 30-year Treasury bonds issued in the 1930’\s came due, WWII, Korea, and Vietnam happened, and the great inflation that followed.

The purchasing power of the dollar cratered, falling roughly 90%. Coffee is now $1.00, a hamburger at McDonald’s is $5.00, and a cheap steak at Outback cost $12.00.

The government, in effect, only had to pay back 10 cents on the dollar in terms of current purchasing power on whatever it borrowed in the thirties.

Who paid for this free lunch?

Bond owners who received minimal and often negative real inflation-adjusted returns on fixed income investments for three decades.

In the end, it was the risk avoiders who picked up the tab. This is why bonds became known as “certificates of confiscation” during the seventies and eighties.

This is not a new thing. About 300 years ago, governments figured out there was easy money to be had by issuing paper money, borrowing massively, stimulating the local economy, creating inflation, and then repaying the debt in devalued future paper money.

This is one of the main reasons why we have governments, and why they have grown so big. Unsurprisingly, France was the first, followed by England and every other major country.

Ever wonder how the new, impoverished United States paid for the Revolutionary War?

It issued paper money by the bale, which dropped in purchasing power by two thirds by the end of conflict in 1783. The British helped too by flooding the country with counterfeit paper Continental money.

Bondholders can expect to receive a long series of rude awakenings sometime in the future.

No wonder Bill Gross, the former head of bond giant PIMCO, says he will get ashes in his stocking for Christmas next year.

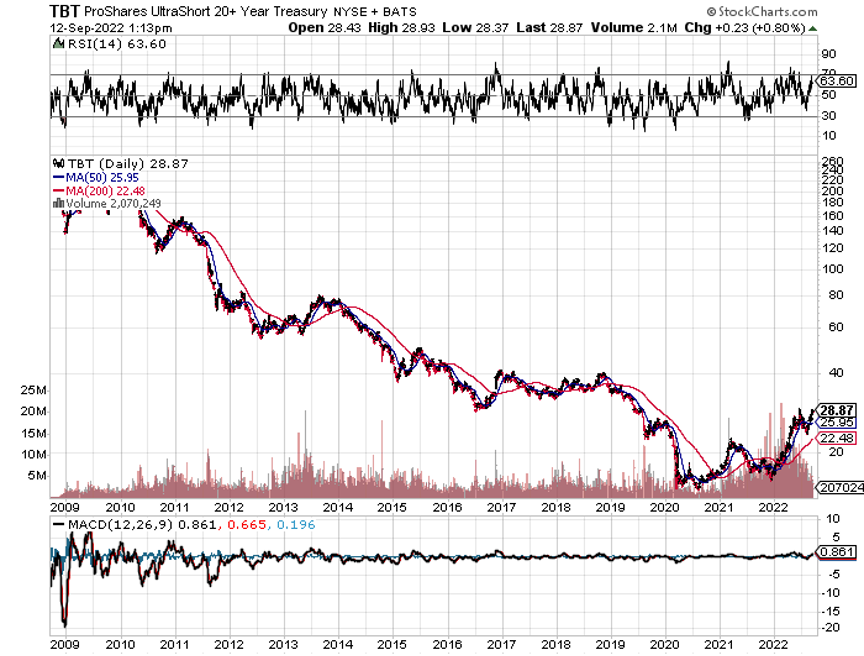

The scary thing is that eventually, we will enter a new 30-year bear market for bonds that lasts all the way until 2049. However, after last month’s frenetic spike up in bond prices and down in bond yields, that is looking more like a 2022 than a 2019 position.

This is certainly what the demographics are saying, which predicts an inflationary blow-off in decades to come that could take short term Treasury yields to a nosebleed 12% high once more.

That scenario has the leveraged short Treasury bond ETF (TBT), which has just cratered down to $23, double to $46, and then soaring all the way to $200.

If you wonder how yields could get that high in a decade, consider one important fact.

The largest buyers of American bonds for the past three decades have been Japan and China. Between them, they have soaked up over $2 trillion worth of our debt, some 12% of the total outstanding.

Unfortunately, both countries have already entered very negative demographic pyramids, which will forestall any future large purchases of foreign bonds. They are going to need the money at home to care for burgeoning populations of old age pensioners.

So who becomes the buyer of last resort? No one, unless the Federal Reserve comes back with QE IV, V, and VI. QE IV, in fact, has already started.

There is a lesson to be learned today from the demise of the Roosevelt debt.

It tells us that the government should be borrowing as much as it can right now with the longest maturity possible at these ultra-low interest rates and spending it all.

With real, inflation adjusted 10-year Treasury bonds now posting negative yields, they have a free pass to do so.

In effect, the government never has to pay back the money. But they do have the ability to reap immediate benefits, such as through stimulating the economy with greatly increased infrastructure spending.

Heaven knows we need it.

If I were king of the world, I would borrow $5 trillion tomorrow and disburse it only in areas that create domestic US jobs. Not a penny should go to new social programs. Long-term capital investments should be the sole target.

Here is my shopping list:

$1 trillion – new Interstate freeway system

$1 trillion – additional infrastructure repairs and maintenance

$1 trillion – conversion of our energy system to solar

$1 trillion – construction of a rural broadband network

$1 trillion – investment in R&D for everything

The projects above would create 5 million new jobs quickly. Who would pay for all of this in terms of lost purchasing power? Today’s investors in government bonds, half of whom are foreigners, principally the Chinese and Japanese. Notice that I am not committing a single dollar in spending on any walls.

How did my life turn out? Was it ruined, as my grandfather predicted?

Actually, I did pretty well for myself, as did the rest of my generation, the baby boomers.

My kids did OK too. One son just got a $1 million, two year package at a new tech startup and he is only 30. Another is deeply involved in the tech industry, and my oldest daughter is working on a PhD at the University of California. My two youngest girls became the first ever female eagle scouts.

Not too shabby.

Grandpa was always a better historian than a forecaster. But he did have the last laugh. He made a fortune in real estate, betting correctly on the inflation that always follows big borrowing binges.

You know the five acres that sits under the Bellagio Hotel in Las Vegas today? That’s the land he bought in 1945 for $500. He sold it 32 years later for $10 million.

Not too shabby either.

32 Years of 30-Year Bond Yields

Not Too Shabby for $500

https://www.madhedgefundtrader.com/wp-content/uploads/2015/12/Bellagio-e1467928305548.jpg271400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-14 10:02:152022-09-14 12:28:23What Ever Happened to the Great Depression Debt?

I am writing this from the balcony of my corner suite at the historic Danieli Hotel overlooking the Grand Canal in Venice, Italy.

Every conceivable watercraft imaginable are passing by in large numbers; water taxis, Vaporettos, and even the traditional gondolas. Outside my window, I see two pilots are heatedly arguing over who should enter the side canal first.

This will be my last stay at the Danieli for a while as the 200-year-old hotel cobbled together for three 700-year-old palaces has been sold to the Four Seasons and will imminently close for a three-year gutting and remodeling.

Until Thursday, the market was reaching the top of a three-month range and was ripe to roll over for an August summer correction. Then the Democrats dropped a bombshell. They announced a blockbuster $739 billion stimulus package that will be voted on as early as this week. All of a sudden, the Biden agenda is back on just at one-third its original size.

The package breaks down as follows:

Commits $369 billion to Climate change

Renews a $7,500 tax credit for electric vehicles

Allows Medicare to negotiate prices

Adds a 15% Corporate alternative minimum tax

Reduces the Deficit by $300 billion

It all amounts to a massive stimulus package just as the US economy is entering the most modest of recessions. It also represents a Hail Mary for the Democrats to maintain congressional control.

It just might work.

Who is the biggest victim of the stimulus package? Big oil companies where an alternative minimum neatly sidesteps the oil depletion allowance which enabled them to dodge most taxes since it was passed in 1913.

Who is the biggest winner? Tesla (TSLA), which accounted for 80% of global EV production and benefits enormously from a $7,500 tax credit, is made available for low-income earners purchasing electric cars. It also allows tax credits for the purchase of used EVs for the first time. That is important for the economy as a whole, as both General Motors (GM) and Ford (F) plan to have more than 50% of their production in EVs by 2030.

Traders seemed to know this, taking Tesla shares up 50% from the June bottom and minting several new Mad Hedge millionaires along the way.

The market seemed to sense that something was in the works, even though the meetings were held in secret in a windowless basement room in the Capitol Building. The markets seemed to know something was coming. July posted the best market performance in two years, with the Dow Average up 7.69%.

This is a classic example of markets sensing major events we mere humans are blind to. My favorite example of this is the Battle of Midway, where the Japanese lost a disastrous four aircraft carriers and 350 planes, which ended on June 7, 1942. Even though the outcome was top secret and withheld from the public for months, a 20-year bull market ensued and didn’t end until the 1962 Cuban Missile Crisis.

You may have noticed that I have pulled back from my aggressive shorting of the bond market. That’s because the US budget deficit is seeing the largest decline in American history. Throw in the $300 billion promised by this week’s stimulus package, and the deficit will plunge by a staggering $1.5 trillion in 2022.

That will pay off 37.5% of the $4 trillion deficit run up by the Trump administration. As a result, ten-year US Treasury yields have plunged an eye-popping 90 basis points, from 3.5% to 2.6% in only six weeks. No wonder stocks have been so hot during the same time period.

The Fed Makes Its Move, and the market loved it, taking stocks up 436 points. Notice that the market is not letting anyone in. An increasing number of investors are coming over to my view that the S&P 500 is headed over to $4,800 by yearend. The bottom for this cycle is in. The overnight rate is now 2.25%-2.5%. The Fed is rapidly catching up with the curve. Powell left the door open to raising only 0.50% next time. The futures market is betting that we hit 3.3% this year.

The US is Officially in Recession, after reporting a slight 0.9% decline in Q2. That makes two back-to-back quarters following the 1.6% decline in Q1. The big question is are we already out, given the incredible demand seen in some sectors of the economy, like airlines, hotels, and resorts? It also looks like a big spending bill is about the pass congress. Weekly Jobless Claims Hit 256,000, down 5,000 from the previous week. Is the recession already over?

IMF Cuts GDP Forecast, cutting its 2022 forecast from 3.6% to 3.2%. 2023 gets a haircut from 3.6% to 2.9%. The IMF is always a deep lagging indicator. Inflation, a China slowdown, and the Ukraine War are the reasons. I think largest are about to start discounting a growth resurgence.

Russia and Ukraine Sign Grain Deal, opening up the Black Sea ports for wheat exports. It’s hard to imagine how this is going to work. Two countries at war but continuing international trade? Indeed, one Russian missile hit Odessa the next day with two others shot down. Still, it was enough to drop wheat prices.

Space X Breaks Launch Record, sending 32 reusable Falcon 9’s aloft so far in 2022. The Starlink ramp-up is responsible, Elon Musk’s effort to build a global satellite WIFI network. You can already become a Starlink beta tester in the US at competitive prices.

The S&P Case Shiller National Home Price Index Sees Another Drop, from 20.6% to 19.7% in May. The closely watched figure saw only its second drop in three years. Tampa (36.1%), Miami (34%), and Dallas (30.8%) brought in the strongest gains. These are still incredible mains, meaning high mortgage interest rates have yet to make a serious dent in prices.

Pending Home Sales Fell a Staggering 20% in June, on a signed contracts basis, says the National Association of Realtors. It’s the slowest pace since June 2011. The roll-over of the real estate market has just begun, in volume, if not in price. The hottest cities like Phoenix, Tampa, and Boise are seeing the sharpest falls.

Lumber Prices are Still in Free-Fall, with lumber sales down 25% in June. Commodities are still falling, showing that the end of inflation is near. Some 10.8% of orders have been cancelled and inventories are building. Construction costs are falling too.

Russia Seizes all Foreign Leased Aircraft and re-registers them as Russian. Some 515 leased aircraft worth $10 billion are trapped in the country and are not allowed by sanctions to get spare parts. Ireland is taking the biggest hit, with 40% owned there. Why insurance covers accidents and not theft as large commercial aircraft are so rarely stolen. And 515 at once! This will be a legal headache for the ages.

Walmart Gets Crushed, with the founding Walton family taking $11.4 billion in personal losses on the $13 or 10% drop in the stock suffered yesterday. Low-end retail is not what you want to own if you think a recession is headed our way. That’s on an expected 13% decline in EPS expected for the year. Sam Walton would be rolling over in his grave.

Microsoft Misses Slightly, but the stock jumps 5% anyway as the long term buyers come in. A strong dollar punches foreign earnings in the nose. The crucial azure cloud hosting and storage business is still growing at 40% a year. Buy (MSFT) on dips and sell short the puts.

Meta (META) Post First Loss Ever in Q2, with ever weaker forecasts as Market Zuckerberg’s money machine grinds to a halt. It will take 3-5 years for the metaverse to mature to the point where the world’s largest social media platform is making money again. The required investment is overwhelming. Avoid (META).

The Wealthiest 100 Americans Lost $622 Billion Since November when the stock market topped. But they are still richer than pre-pandemic. Who was the biggest loser? My friend Elon Musk, whose stock dropped 50% from $1,200 in the first half, costing him a neat $170,000 billion personally. But it created a spectacular buying opportunity for the stock for the rest of us.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

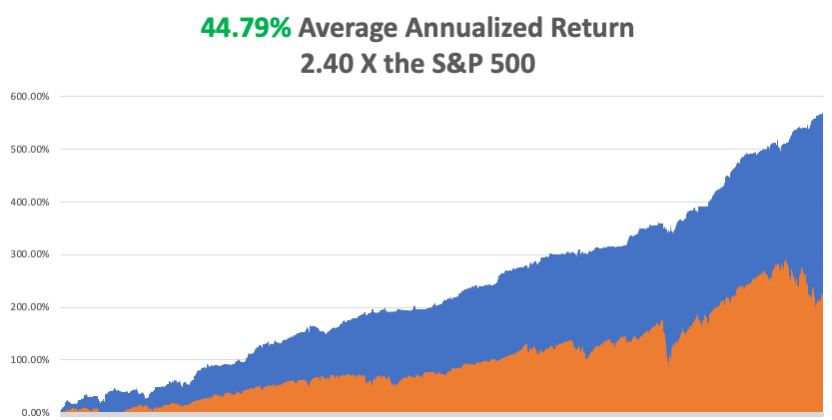

With some of the greatest market volatility in market history, my July month-to-date performance exploded to +3.98%.

My 2022 year-to-date performance ballooned to 54.83%. The Dow Average is down -11.23% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 77.02%.

That brings my 14-year total return to 567.39%, some 2.40 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.79%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 91 million, up 300,000 in a week and deaths topping 1,030,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, August 1 at 7:00 AM, the ISM Manufacturing PMI for July is released. Activision Blizzard (ATVI) announces earnings.

On Tuesday, August 2 at 7:00 AM, the JOLTS Job Openings for July are out. Caterpillar (CAT) and Airbnb (ABNB) announce earnings.

On Wednesday, August 3 at 7:00 AM, ISM Manufacturing PMI for July is published. MGM Resorts (MGM) announces earnings.

On Thursday, August 4 at 8:30 AM, Weekly Jobless Claims are announced. Amgen (AMGN) and Lyft (LYFT) announce earnings. On Friday, August 5 at 8:30 AM, the Nonfarm Payroll Report for July is disclosed. Berkshire Hathaway (BRKB) announces earnings. At 2:00 the Baker Hughes Oil Rig Count is out.

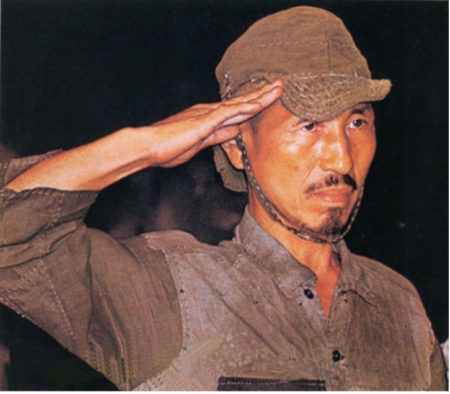

As for me, I have met many interesting people over a half-century of interviews, but it is tough to beat Corporal Hiroshi Onoda of the Japanese Army, the last man to surrender in WWII.

I had heard of Onoda while working as a foreign correspondent in Tokyo. So, I convinced my boss at The Economist magazine in London that it was time to do a special report on the Philippines and interview president Ferdinand Marcos. That accomplished, I headed for Lubang island where Onoda was said to be hiding, taking a launch from the main island of Luzon.

I hiked to the top of the island in the blazing heat, consuming two full army canteens of water (plastic bottles hadn’t been invented yet). No luck. But I had a strange feeling that someone was watching me.

When the Philippines fell in 1945, Onoda’s commanding officer ordered the remaining men to fight on to the last man. Four stayed behind, continuing a 30-year war.

As a massive American military presence and growing international trade raised Philippine standards of living, the locals eventually were able to buy their own guns and kill off Onoda’s companions one by one. By 1972 he was alone, but he kept fighting.

The Japanese government knew about Onoda from the 1950s onward and made every effort to bring him back. They hired search crews, tracking dogs, and even helicopters with loudspeakers, but to no avail. Frustrated, they left a one-year supply of the main Tokyo newspaper and a stockpile of food and returned to Japan. This continued for 20 years.

Onoda read the papers with great interest, believing some parts but distrusting others. His world view became increasingly bizarre. He learned of the enormous exports of Japanese automobiles to the US, so he concluded that while still at war, the two countries were conducting trade.

But when he came to the classified ads, he found the salaries wildly out of touch with reality. Lowly secretaries were earning an incredible 50,000 yen a year, while a salesman could earn an obscene 200,000 yen.

Before the war, there was one Japanese yen to the US dollar. In the hyperinflation that followed, the yen fell to 800, and then only recovered to 360. Onoda took this as proof that all the newspapers were faked by the clueless Americans who had no idea of true Japanese salary levels.

So he kept fighting. By 1974, he had killed 17 Filipino civilians.

After I left Lubang island, a Japanese hippy named Norio Suzuki with long hair, beads, and sandals followed me, also looking for Onoda. Onoda tracked him as he had me but was so shocked by his appearance that he decided not to kill him. The hippy spent two days with Onoda explaining the modern world.

Then Suzuki finally asked the obvious question: what would it take to get Onoda to surrender? Onoda said it was very simple, a direct order from his commanding officer. Suzuki made a beeline straight for the Japanese embassy in Manila and the wheels started turning.

A nationwide search was conducted to find Onoda’s last commanding officer and a doddering 80-year-old was turned up working in an obscure bookstore. Then the government custom-tailored a prewar Imperial Japanese Army uniform and flew him down to the Philippines.

The man gave the order and Onoda handed over his samurai sword and rifle, or at least what was left of it. Rats had eaten most of the wooden parts. You can watch the surrender ceremony by clicking here on YouTube.

When Onoda returned to Japan, he was a sensation. He displayed prewar mannerisms and values like filial piety and emperor worship that had been long forgotten. Emperor Hirohito was still alive.

When I finally interviewed him, Onoda was sympathetic. I had by then been trained in Bushido at karate school and displayed the appropriate level of humility, deference, mannerisms, and reference.

I asked why he didn’t shoot me. He said that after fighting for 30 years, he only had a few shells left and wanted to save them for someone more important.

Onoda didn’t last long in the modern Japan, as he could no longer tolerate modern materialism and cold winters. He moved to Brazil to start a school to teach prewar values and survival skills where the weather was similar to that of the Philippines. Onoda died in 2014 at the age of 91. A diet of coconuts and rats had extended his life beyond that of most individuals.

Onoda wasn’t actually the last Japanese to surrender in WWII. I discovered an entire Japanese division in 1975 that had retreated from China into Laos and just blended in with the population. They were prized for their education and hard work and married well.

During the 1990s, a Japanese was discovered in Siberia. He was released locally at the end of the war, got a job, married a Russian woman, and forgot how to speak Japanese. But Onoda was the last to stop fighting.

The Onoda story reminds me of a fact about journalists very early in their careers. You can provide all the facts in the world to someone. But if they conflict with deeply held beliefs, they won’t buy them for a second. The debate over the 2020 election outcome is a perfect example. There is no cure for this disease.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Hiro Onoda Surrenders

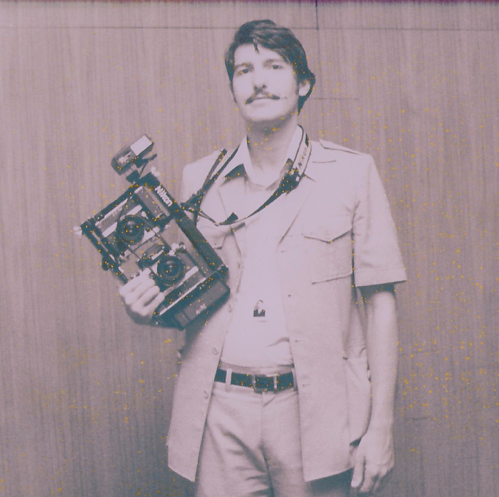

Budding Journalist John Thomas

https://www.madhedgefundtrader.com/wp-content/uploads/2022/08/hiro-onoda-e1659376492740.jpg394450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-01 11:02:482022-08-01 14:18:30The Market Outlook for the Week Ahead, or A Bombshell from Washington

(WHAT EVER HAPPENED TO THE GREAT DEPRESSION DEBT?),

($TNX), (TLT), (TBT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-16 10:04:202022-02-16 10:31:56February 16, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.