Mad Hedge Biotech & Healthcare Letter

September 16, 2021

Fiat Lux

FEATURED TRADE:

(RIDING THE COVID-19 VACCINE MOMENTUM)

(PFE), (BNTX), (MRNA), (JNJ), (SNY), (GSK), (TRIL)

Mad Hedge Biotech & Healthcare Letter

September 16, 2021

Fiat Lux

FEATURED TRADE:

(RIDING THE COVID-19 VACCINE MOMENTUM)

(PFE), (BNTX), (MRNA), (JNJ), (SNY), (GSK), (TRIL)

The pandemic is exhibiting hints of easing, and one of the names playing a critical role in the vaccine rollout that has made this step towards normalcy possible is Pfizer (PFE).

Actually, Pfizer stock has hit an all-time high courtesy of its COVID-19 vaccine, Comirnaty, which it developed with German biotech firm BioNTech (BNTX).

While this is undoubtedly an exciting time for the company, many investors wonder whether this period also marks the spectacular of Pfizer, and things will go downhill from here. After all, several of its patents are set to expire starting in 2025.

My short answer to this question is no. This isn’t the beginning of the end for Pfizer. Looking at the company’s history, pipeline, and trajectory, I can say that Pfizer’s rise is just getting started.

One of the key reasons behind my belief is Pfizer’s robust pipeline.

To date, the company has roughly 100 drugs queued for regulatory clearance, while others are slated for late-stage clinical testing.

That means that regardless of the patent expirations in Pfizer’s horizon, the company’s strong and diverse pipeline can easily counteract the blow from the loss of exclusivity.

Just last month, Pfizer received full approval from the US FDA for Comirnaty.

Since fellow vaccine developers like Moderna (MRNA) have yet to achieve the same, this makes Pfizer the first COVID-19 vaccine to gain this endorsement from the regulatory committee.

Needless to say, Pfizer could capitalize on this massive opportunity to boost its profits in the quarters.

The availability of a fully approved COVID-19 vaccine could allow establishments to oblige mandatory vaccinations, which could obviously lead to higher demand for Comirnaty, as over 100 million Americans have yet to receive at least a single jab.

In the second quarter of 2021, the company reported $19 billion in revenue, indicating a 92% year-over-year climb thanks to the $7.8 billion raked in by its COVID-19 vaccine.

Pfizer now estimates Comirnaty revenue to reach roughly $33.5 billion, indicating an expected 2.1 billion doses to be delivered within the year.

Excluding Comirnaty’s sales, Pfizer’s revenue increased by 10%. This strong momentum led the company to raise its 2021 full-year guidance to somewhere between $78 and $80 billion.

Before Comirnaty, though, Pfizer had already been known as a prolific vaccine developer.

One of its prized creations is the pneumococcal vaccine Prevnar, which generated $2.52 billion in revenue in the first 6 months of 2021.

Meanwhile, its tick-borne encephalitis vaccine, marketed as TicoVac, gained FDA approval in July and could bring in roughly $1 billion per annum.

Riding this momentum, Pfizer has been busy developing another potential moneymaker in this segment in the form of its respiratory syncytial virus (RSV) vaccine candidate: RSVpreF.

And if the Phase 3 results for RSVpreF come anywhere near its Phase 2 trial, then Pfizer has another blockbuster in its hands.

This is because the RSV vaccine market is projected to grow to approximately $10 billion by 2030, and Pfizer’s candidate is targeting 72% of that population.

However, the RSV market will be a crowded space with the likes of Johnson & Johnson (JNJ), Sanofi (SNY), and GlaxoSmithKline (GSK) working to fill this unmet medical demand.

So, realistically, Pfizer’s RSVpreF has the potential to capture 20% market share, translating to $2.1 billion in annual revenue.

Apart from its vaccine-related efforts, Pfizer’s core businesses have been growing as well. Top contributors come from its oncology arm, specifically Eliquis and Ibrance.

Its recent acquisition of Trillium Therapeutics (TRIL) is anticipated to serve as a catalyst for Pfizer’s cancer segment in the next years as well.

Overall, Pfizer has a blockbuster drug pipeline and an impressively successful COVID-19 vaccine rollout. These provide the company with a long runway for solid and steady growth.

Mad Hedge Biotech & Healthcare Letter

August 26, 2021

Fiat Lux

FEATURED TRADE:

(ANOTHER FORETOLD ACQUISITION)

(PFE), (TRIL), (BNTX), (VTRS), (ALXO)

Another one of my predictions came true.

Last December, I wrote about the impressive potential of Trillium Therapeutics (TRIL) in my letter, titled “The Most Famous Cancer Stock You’ve Never Heard of,” and predicted that it’s going to be an attractive acquisition candidate soon.

Earlier this week, it finally happened.

Leveraging its extra cash from Comirnaty, the COVID-19 vaccine it developed with BioNTech (BNTX), Pfizer (PFE) has decided to push through with acquisitions instead of pursuing buybacks.

And the candidate at the receiving end of this cash flow is none other than one of my buyout candidates last year: Trillium Therapeutics.

The $2.3 billion acquisition was an excellent deal for Trillium, with Pfizer buying the cancer-centered biotech at a 118% premium over the stock’s average price in the past 60 days.

Given that Trillium stock closed at roughly $6 per share before the announcement, the deal practically tripled its worth at $18.50 each.

The price signifies Pfizer’s willingness to pay up to take over Trillium pipeline and portfolio after initially investing $25 million in the smaller company in 2020.

Trillium shares also skyrocket by 188% following the announcement of the deal.

The plan is for Trillium Therapeutics to bolster Pfizer’s oncology and hematology portfolios, with a focus on blood-related cancers.

This recent turn of events has been long awaited by Pfizer investors.

After all, the last time the company exceeded expectations was during its Viagra-driven frenzy era back in the late 1990s. Since then, the stock has been underperforming the S&P 500.

Unquestionably, Pfizer’s work on the COVID-19 vaccine helped the stock recover.

In its second quarter earnings report, Pfizer posted $7.8 billion in sales for Comirnaty alone. This brought the company’s total revenue to roughly $18.7 billion, showing off an 86% boost year over year.

However, even without Comirnaty’s contribution, Pfizer’s revenues still managed to rise.

Through the first six months of 2021, Pfizer’s revenue has reached $33.5 billion—up by 68% year over year. This is impressive considering that it followed the Upjohn spinoff with Mylan, which later became Viatris (VTRS).

Even without the COVID-19 vaccine, Pfizer still has promising growth prospects involving its core businesses.

For one, it has a number of blockbuster drugs that can easily become strong revenue streams for years to come.

For example, Prevnar sales grew by 34% year over year to reach $5.85 billion, pushing Pfizer’s oncology segment to climb by 16%.

Another blockbuster in the making is blood clot treatment Eliquis, which grew by 13% from the $5 billion in sales it generated in the second quarter of 2020.

As for its biosimilars, these notched a bit to more than $1.5 billion in sales last year and recorded a whopping 88% growth year over year thanks primarily to the newly released cancer drugs Zirabev, Ruxience, and Trazimera.

Meanwhile, heart failure treatment Vyndagel, which generated roughly $1.3 billion in 2020, reported an impressive 77% climb year over year for its $501 million in sales in the second quarter of 2021 alone.

Another heavy hitter in Pfizer’s portfolio is kidney cancer medication Inlyta, which reported $800 million in sales in 2020. For the second quarter of this year, the sales for this drug is up 29% year over year, with $257 million.

Management also boosted the company’s guidance from $70.5 billion to $72.5 billion.

Then, it raised it again to $78 billion, then once more to $80 billion. As for its COVID-19 vaccine sales, it increased its estimates from $26 billion to $33.5 billion.

While the sales from the COVID-19 vaccine definitely provided a comfortable boost for the company, its own portfolio of drugs demonstrates the capacity of its core business to drive revenues on its own.

Considering the FDA approval and support for the additional third booster shot, though, I anticipate that Pfizer will continue towards this path of acquiring smaller biotechnology companies in the foreseeable future.

In terms of other clinical-stage biotech firms potentially up for grabs next, the work of ALX Oncology (ALXO) has recently been put under the spotlight as it relates closely to Trillium’s cancer-centered technology.

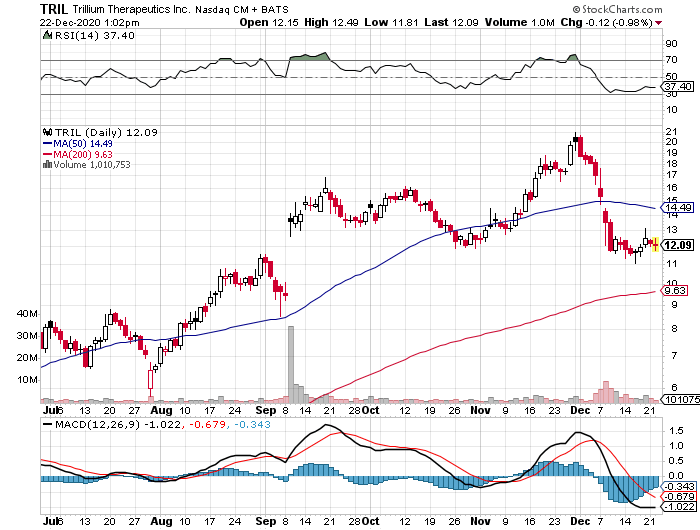

Mad Hedge Biotech & Healthcare Letter

December 22, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

Mad Hedge Biotech & Healthcare Letter

October 20, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.